graduate seminar - etf · graduate seminar: etf options strategies --- ... ebs, thomson reuters,...

TRANSCRIPT

Graduate Seminar: ETF Options Strategies ---

Hedging Risk, Building Income

Sponsored by:

Moderator

Eric Cott

Director

The Options Industry Council

MODERATOR

Panelists

Blaine Docker

Chief Operating Officer

Main Management

SPEAKER

SPEAKER

Kapil Rathi

Vice President, Options Business Strategy

Bats Global Markets

Michael Khouw

President Chief Strategist

Optimize Advisors &

Business News Contributor for CNBC

SPEAKER

There is a Q&A box on the upper left side of your screen.

Type your question in the lower box and hit Submit.

If you do not see a Q&A box in the upper left corner, please click on the red QA widget on the lower part of your screen.

To talk among other attendees we have included a “Group Chat” function. Please click the brown widget that has 3 people visible.

It’s Easy to Submit a Question

This presentation will be streaming audio through your computer only. If you are not seeing slide movement once the presentation has begun please refresh your screen or hit F5 to refresh. A replay of this presentation and CE Credit information will be sent to you tomorrow via email.

Important Information

If you have any technical difficulty, please click on the Help widget. It has a question mark and covers common technical issues.

Important Information

• Options Overview

• Options on ETFs

• Strategies for the Financial Advisor and their clients

• Income Generation, Hedging and

Concentrated positions

• Volatility

• Q and A

Presentation Outline

Options involve risks and are not suitable for everyone. Prior to buying or selling options, an investor

must receive a copy of Characteristics and Risks of Standardized Options. Individuals should not enter

into options transactions until they have read and understood the risk disclosure document,

Characteristics and Risks of Standardized Options, available by visiting OptionsEducation.org. Copies

may be obtained by contacting your broker or The Options Industry Council at One North Wacker

Drive, Chicago, IL 60606.

In order to simplify the computations, commissions, fees, margin interest and taxes have not been

included in the examples used in these materials. These costs will impact the outcome of all stock and

options transactions and must be considered prior to entering into any transactions. Investors should

consult their tax advisor about any potential tax consequences.

Any strategies discussed, including examples using actual securities and price data, are strictly for

illustrative and educational purposes only and are not to be construed as an endorsement,

recommendation, or solicitation to buy or sell securities. Past performance is not a guarantee of future

results.

LEAPS® is a registered trademark of the Chicago Board Options Exchange, Incorporated. Long-term

Equity AnticiPation SecuritiesSM and WeeklysSM are service marks of the Chicago Board Options

Exchange, Incorporated. Copyright © 2016. The Options Industry Council. All rights reserved.

The Options Industry Council

Who We Are

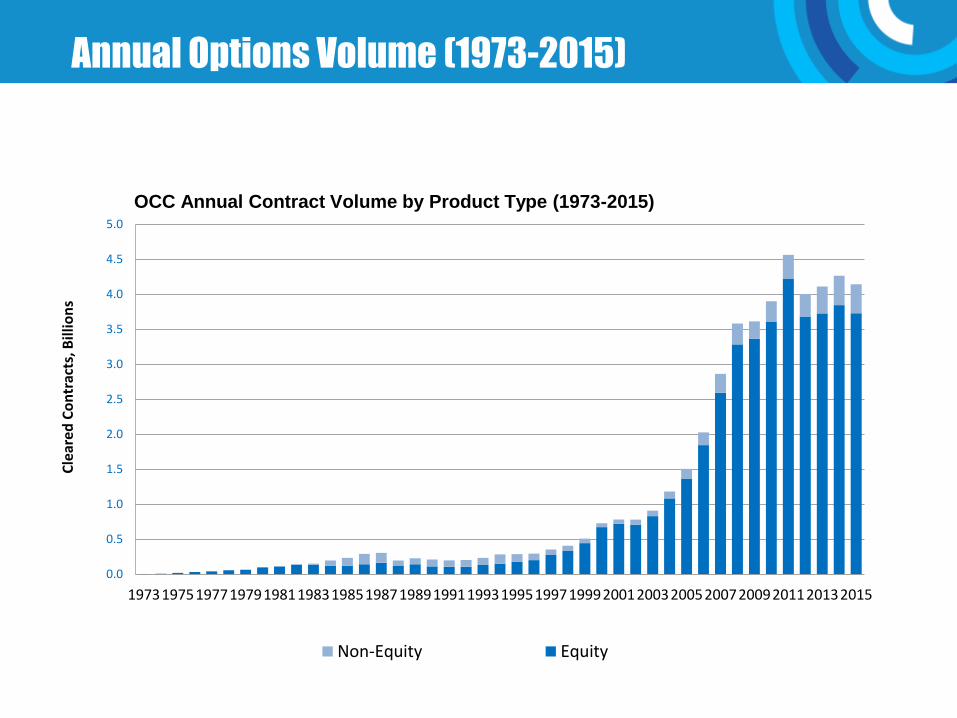

Annual Options Volume (1973-2015)

OCC Annual Contract Volume by Product Type (1973-2015)

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

1973197519771979198119831985198719891991199319951997199920012003200520072009201120132015

Cle

ared

Co

ntr

acts

, Bill

ion

s

Non-Equity Equity

• Options give you more ways to implement your market research

• Options make it possible to target a variety of investment objectives:

− Reduce risk

− Increase income

− Unique tradeoffs

Options Are Tools

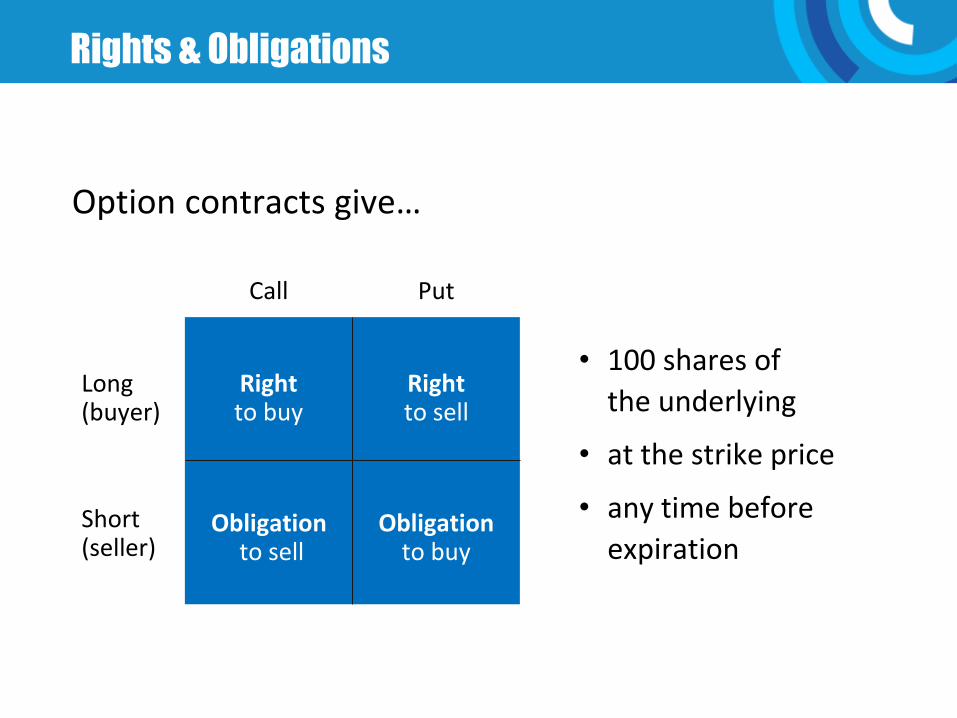

Option contracts give…

• 100 shares of

the underlying

• at the strike price

• any time before

expiration

Call Put

Right to buy

Right to sell

Obligation to buy

Obligation to sell

Short (seller)

Long (buyer)

Rights & Obligations

• There are two “types” of options:

− Calls

− Puts

• For equity options, the underlying asset to be purchased or sold:

− 100 shares of underlying stock* or

− 100 shares of an ETF (Exchange Traded Fund)*

*Standard options contracts include 100 shares of the underlying, but jumbo (1000 shares) and mini (10 shares) options are new products entering the market.

Two Types of Options

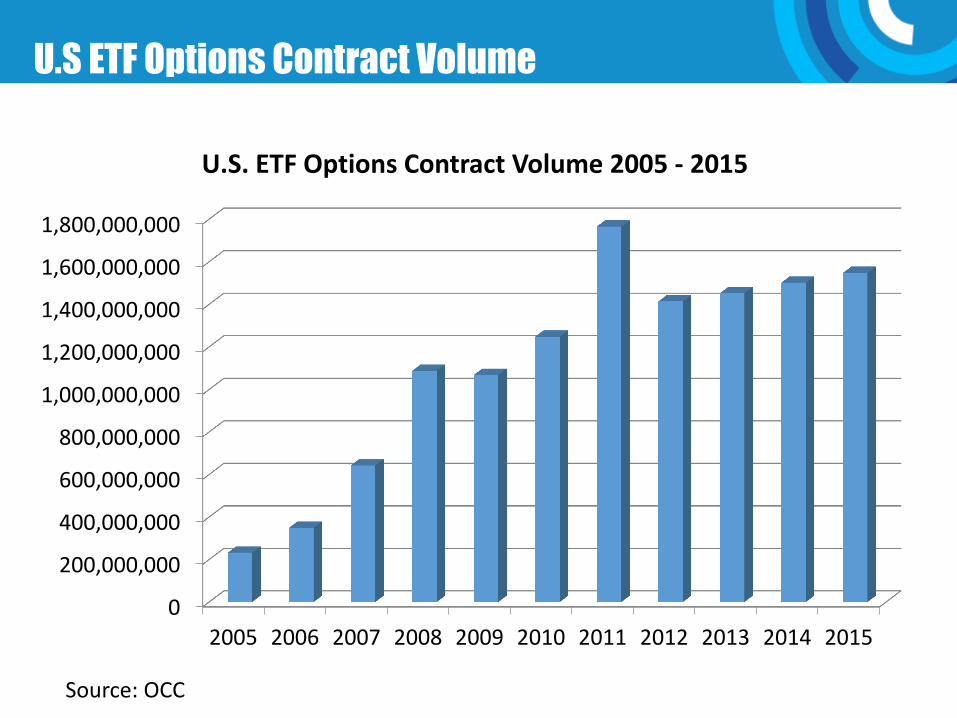

0

200,000,000

400,000,000

600,000,000

800,000,000

1,000,000,000

1,200,000,000

1,400,000,000

1,600,000,000

1,800,000,000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

U.S. ETF Options Contract Volume 2005 - 2015

Source: OCC

U.S ETF Options Contract Volume

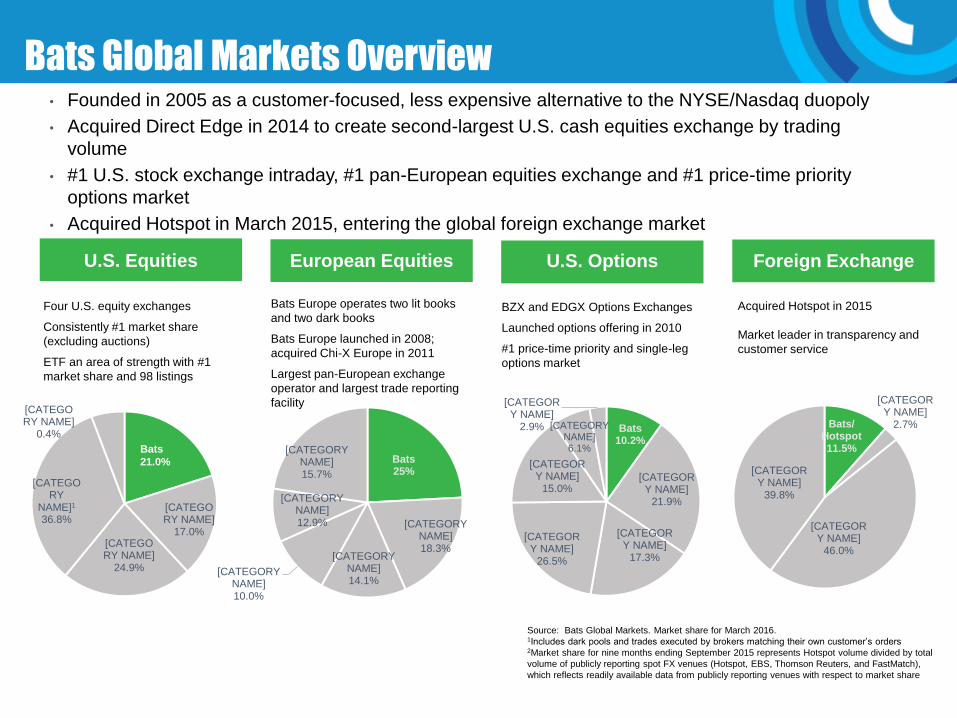

Bats Global Markets Overview • Founded in 2005 as a customer-focused, less expensive alternative to the NYSE/Nasdaq duopoly

• Acquired Direct Edge in 2014 to create second-largest U.S. cash equities exchange by trading

volume

• #1 U.S. stock exchange intraday, #1 pan-European equities exchange and #1 price-time priority

options market

• Acquired Hotspot in March 2015, entering the global foreign exchange market

Four U.S. equity exchanges

Consistently #1 market share

(excluding auctions)

ETF an area of strength with #1

market share and 98 listings

Bats Europe operates two lit books

and two dark books

Bats Europe launched in 2008;

acquired Chi-X Europe in 2011

Largest pan-European exchange

operator and largest trade reporting

facility

BZX and EDGX Options Exchanges

Launched options offering in 2010

#1 price-time priority and single-leg

options market

U.S. Equities European Equities U.S. Options Foreign Exchange

Acquired Hotspot in 2015

Market leader in transparency and

customer service

Bats 25%

[CATEGORY NAME] 18.3%

[CATEGORY NAME] 14.1%

[CATEGORY NAME] 10.0%

[CATEGORY NAME] 12.9%

[CATEGORY NAME] 15.7%

[CATEGORY NAME]

17.0% [CATEGORY NAME]

24.9%

[CATEGORY

NAME]1 36.8%

[CATEGORY NAME]

0.4% Bats

10.2%

[CATEGORY NAME]

21.9%

[CATEGORY NAME]

17.3%

[CATEGORY NAME]

26.5%

[CATEGORY NAME]

15.0%

[CATEGORY NAME] 6.1%

[CATEGORY NAME]

2.9% Bats/ Hotspot 11.5%

[CATEGORY NAME]

2.7%

[CATEGORY NAME]

46.0%

[CATEGORY NAME]

39.8%

Bats

21.0%

Source: Bats Global Markets. Market share for March 2016. 1Includes dark pools and trades executed by brokers matching their own customer’s orders 2Market share for nine months ending September 2015 represents Hotspot volume divided by total

volume of publicly reporting spot FX venues (Hotspot, EBS, Thomson Reuters, and FastMatch),

which reflects readily available data from publicly reporting venues with respect to market share

Leader in ETF volume

16

SM

SM

23.4%

[VALUE]

13.8%

Source: Bats Global Markets (ETFMarketplace.com)

for month of June 2016. Includes volume executed

on exchanges only, including auctions.

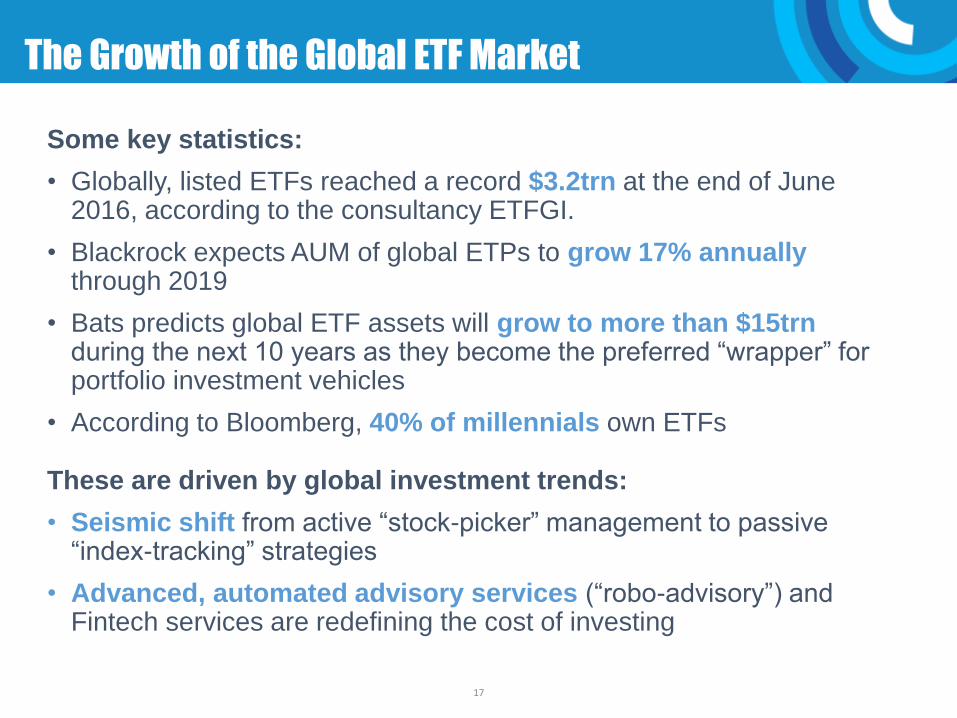

The Growth of the Global ETF Market

17

Some key statistics:

• Globally, listed ETFs reached a record $3.2trn at the end of June 2016, according to the consultancy ETFGI.

• Blackrock expects AUM of global ETPs to grow 17% annually through 2019

• Bats predicts global ETF assets will grow to more than $15trn during the next 10 years as they become the preferred “wrapper” for portfolio investment vehicles

• According to Bloomberg, 40% of millennials own ETFs

These are driven by global investment trends:

• Seismic shift from active “stock-picker” management to passive “index-tracking” strategies

• Advanced, automated advisory services (“robo-advisory”) and Fintech services are redefining the cost of investing

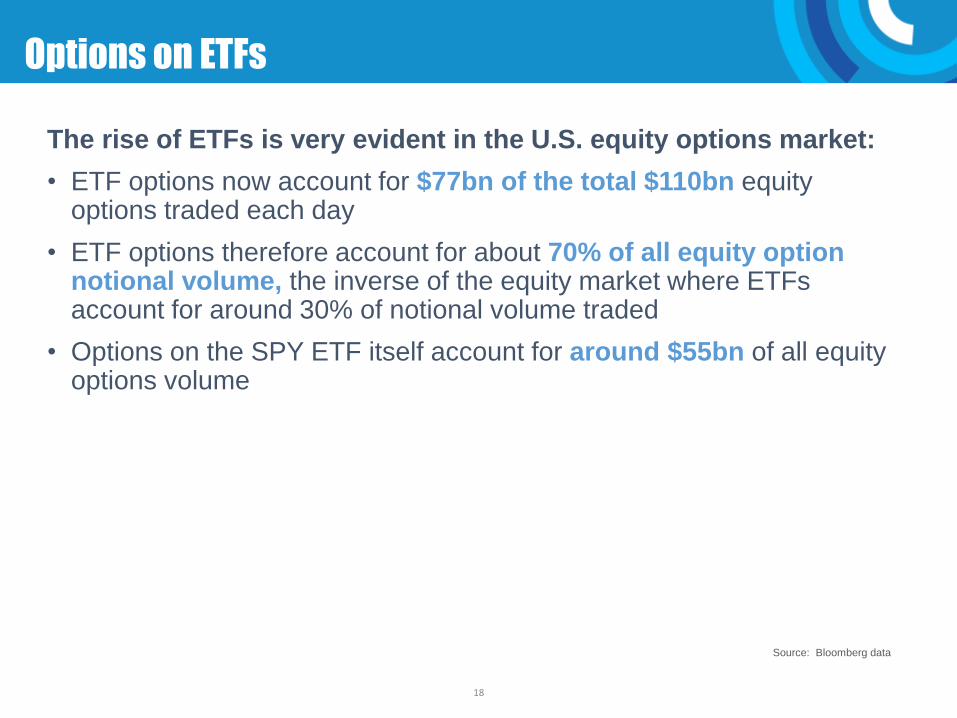

Options on ETFs

18

The rise of ETFs is very evident in the U.S. equity options market:

• ETF options now account for $77bn of the total $110bn equity options traded each day

• ETF options therefore account for about 70% of all equity option notional volume, the inverse of the equity market where ETFs account for around 30% of notional volume traded

• Options on the SPY ETF itself account for around $55bn of all equity options volume

Source: Bloomberg data

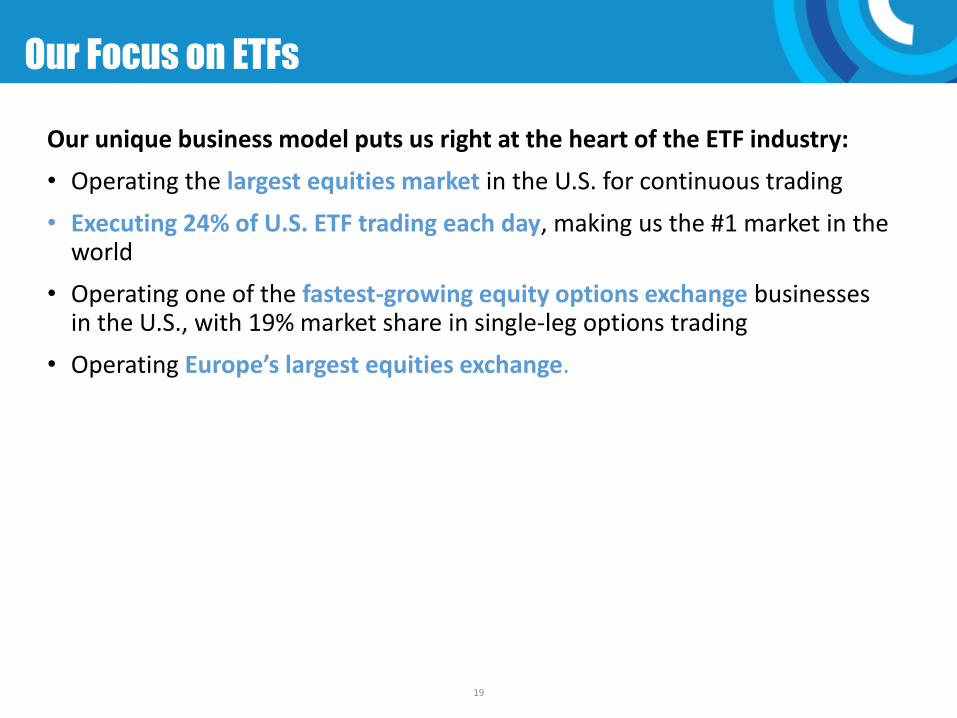

Our Focus on ETFs

19

Our unique business model puts us right at the heart of the ETF industry:

• Operating the largest equities market in the U.S. for continuous trading

• Executing 24% of U.S. ETF trading each day, making us the #1 market in the world

• Operating one of the fastest-growing equity options exchange businesses in the U.S., with 19% market share in single-leg options trading

• Operating Europe’s largest equities exchange.

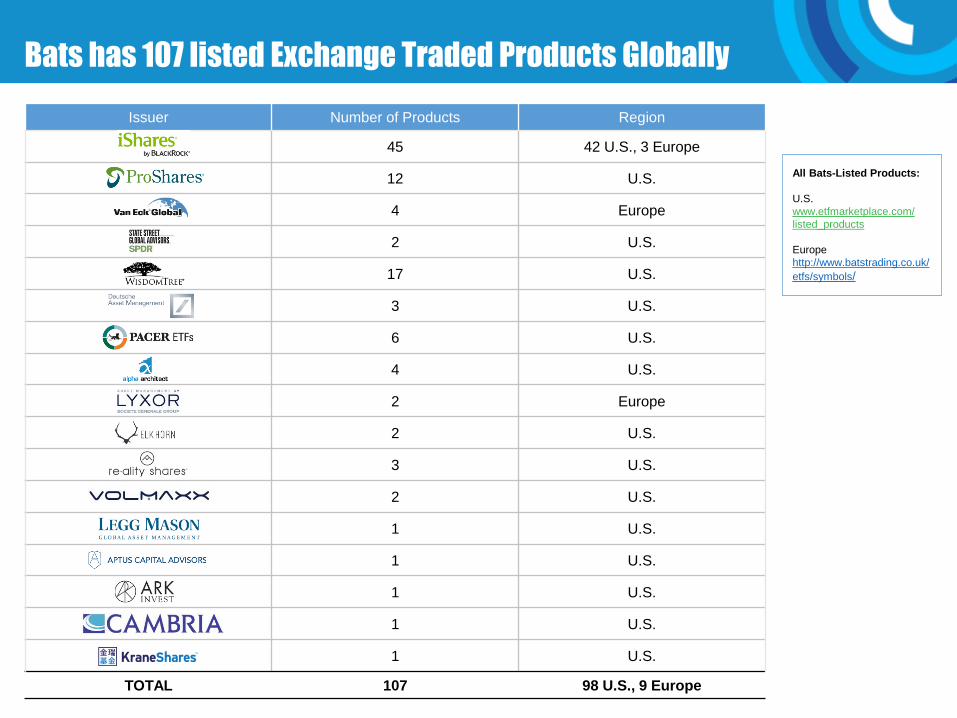

Bats has 107 listed Exchange Traded Products Globally

Issuer Number of Products Region

45 42 U.S., 3 Europe

12 U.S.

4 Europe

2 U.S.

17 U.S.

3 U.S.

6 U.S.

4 U.S.

2 Europe

2 U.S.

3 U.S.

2 U.S.

1 U.S.

1 U.S.

1 U.S.

1 U.S.

1 U.S.

TOTAL 107 98 U.S., 9 Europe

All Bats-Listed Products:

U.S.

www.etfmarketplace.com/

listed_products

Europe

http://www.batstrading.co.uk/

etfs/symbols/

Covered Call Definition

• Covered call: investor simultaneously −Writes (sells) one or more equity call contracts

−Buys equivalent number of underlying shares

−One short call for each 100 long shares

• If stock is bought and call written at same time

−“Covered write” or “buy-write”

• If stock already owned when call is written

−“Overwrite”

Why Write Covered Calls?

• Primary goal – increase returns −Call premium received and kept (assigned or not)

−Generate additional income (over any dividends)

• Investor’s forecast −Neutral to bullish on the underlying stock

−Within a small price range over strategy’s lifetime

• Call premium’s limited downside benefits −Lowers stock’s break-even point (BEP)

−Reduces cost basis for long stock by call premium amount

Covered Call Writer’s Obligations?

• Like any call writer (short call position) −Has the obligation to sell underlying shares

−At strike price

−If assigned

• Assignment (your potential obligation) −Possible at any time before expiration

−Equity options are American-style

• In return for this obligation −Call writer receives and keeps option premium

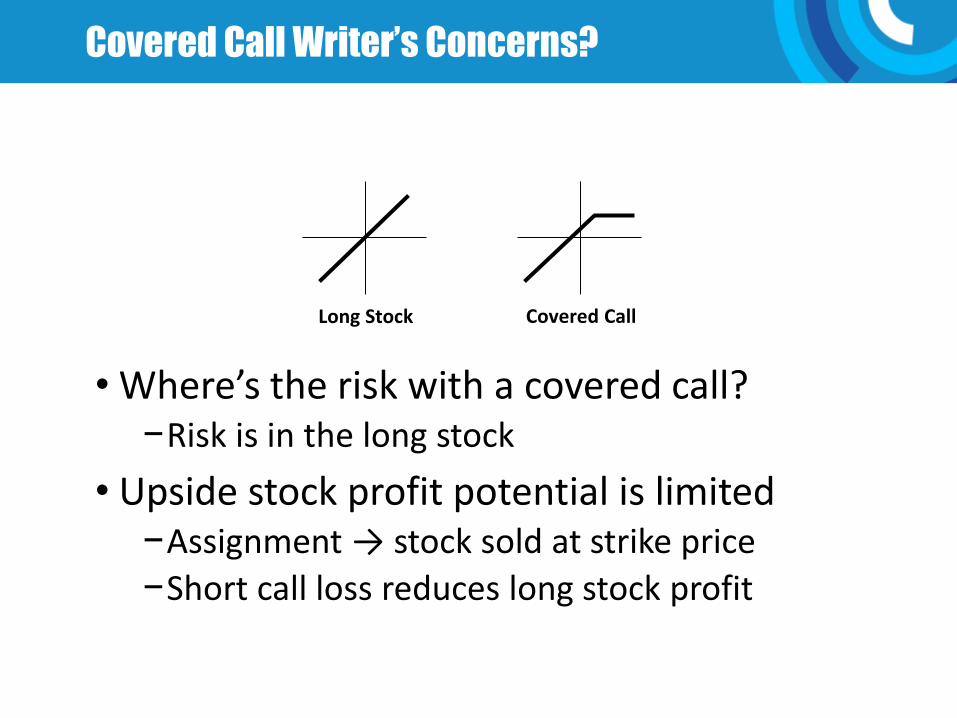

Covered Call Writer’s Concerns?

• Where’s the risk with a covered call? −Risk is in the long stock

• Upside stock profit potential is limited −Assignment → stock sold at strike price

−Short call loss reduces long stock profit

Long Stock Covered Call

Covered Call: ITM vs. OTM

• Writing in-the-money covered call −Defensive and more conservative

−More premium received → more downside protection

−Less upside profit potential

• Writing out-of-the-money covered call −Aggressive and less conservative

−Less premium received → less downside protection

−More upside profit potential

ETF Options Strategies - Income

• Why Options for Income? • Alternative to Fixed Income • Lower Risk than Equity Income • Popular & Tested Strategies

ETF Options Strategies - Income • Covered call or buy-write:

• Short call + long underlying • Earn premium • Forego some upside; almost full downside (On

a Monthly Basis) • Fully collateralized

ETF Options Strategies – Income

• Covered call: Earn income from non-traditional sources

• QQQ • GLD • SLV

ETF Options Strategies - Income

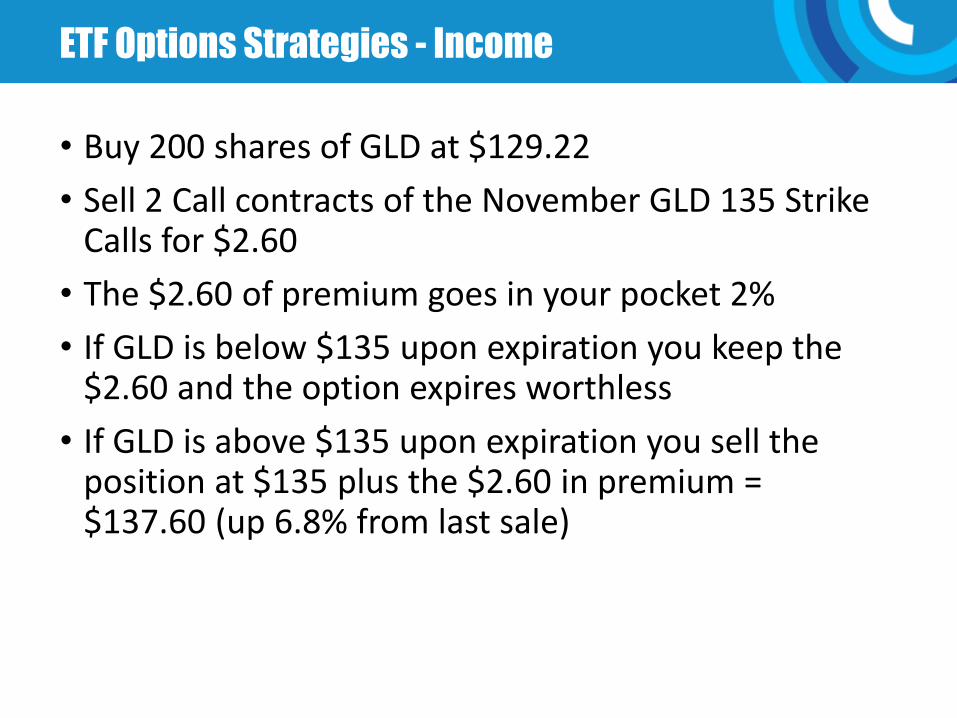

• Buy 200 shares of GLD at $129.22

• Sell 2 Call contracts of the November GLD 135 Strike Calls for $2.60

• The $2.60 of premium goes in your pocket 2%

• If GLD is below $135 upon expiration you keep the $2.60 and the option expires worthless

• If GLD is above $135 upon expiration you sell the position at $135 plus the $2.60 in premium = $137.60 (up 6.8% from last sale)

ETF Options Strategies - Income

• Cash Secured Put Write • Same payoff profile as covered call

• Useful for entering new positions

ETF Options Strategies - Income

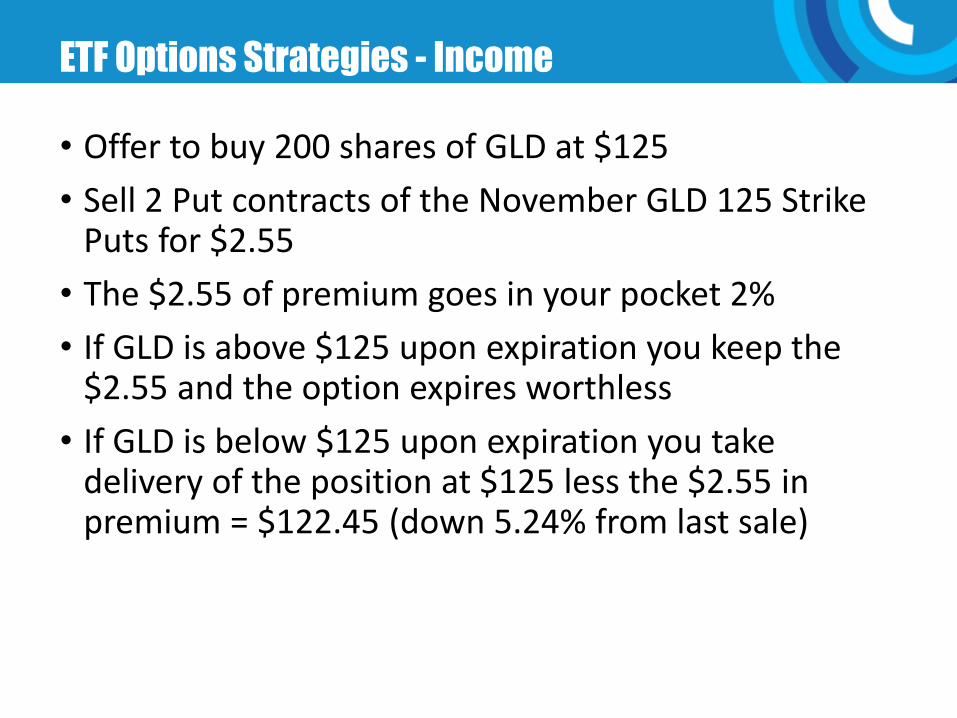

• Offer to buy 200 shares of GLD at $125

• Sell 2 Put contracts of the November GLD 125 Strike Puts for $2.55

• The $2.55 of premium goes in your pocket 2%

• If GLD is above $125 upon expiration you keep the $2.55 and the option expires worthless

• If GLD is below $125 upon expiration you take delivery of the position at $125 less the $2.55 in premium = $122.45 (down 5.24% from last sale)

ETF Options Strategies - Trading

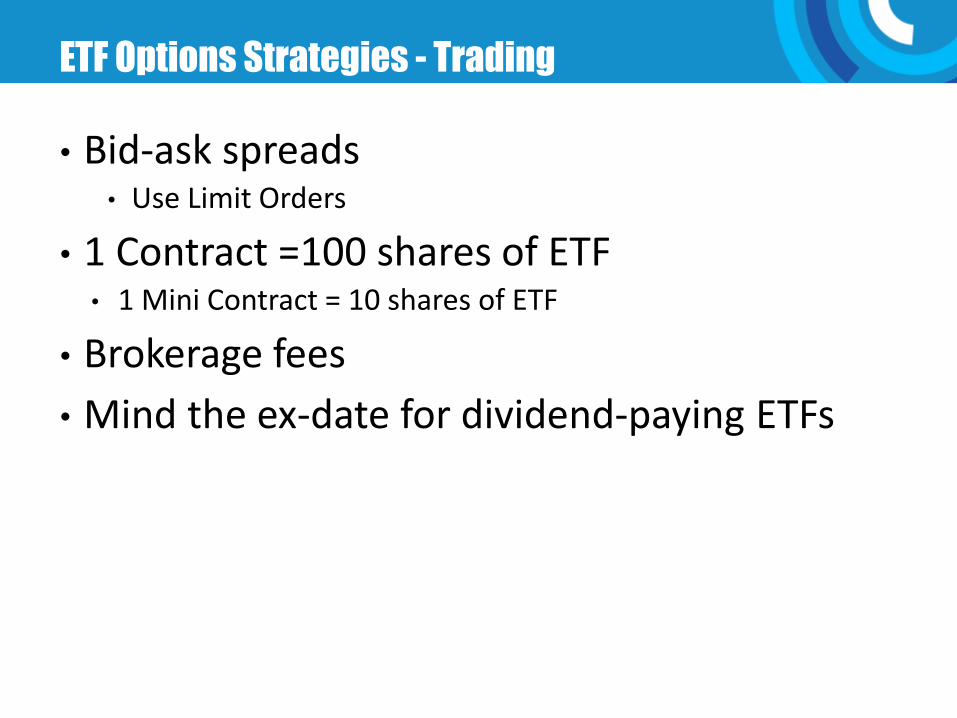

• Bid-ask spreads • Use Limit Orders

• 1 Contract =100 shares of ETF • 1 Mini Contract = 10 shares of ETF

• Brokerage fees

• Mind the ex-date for dividend-paying ETFs

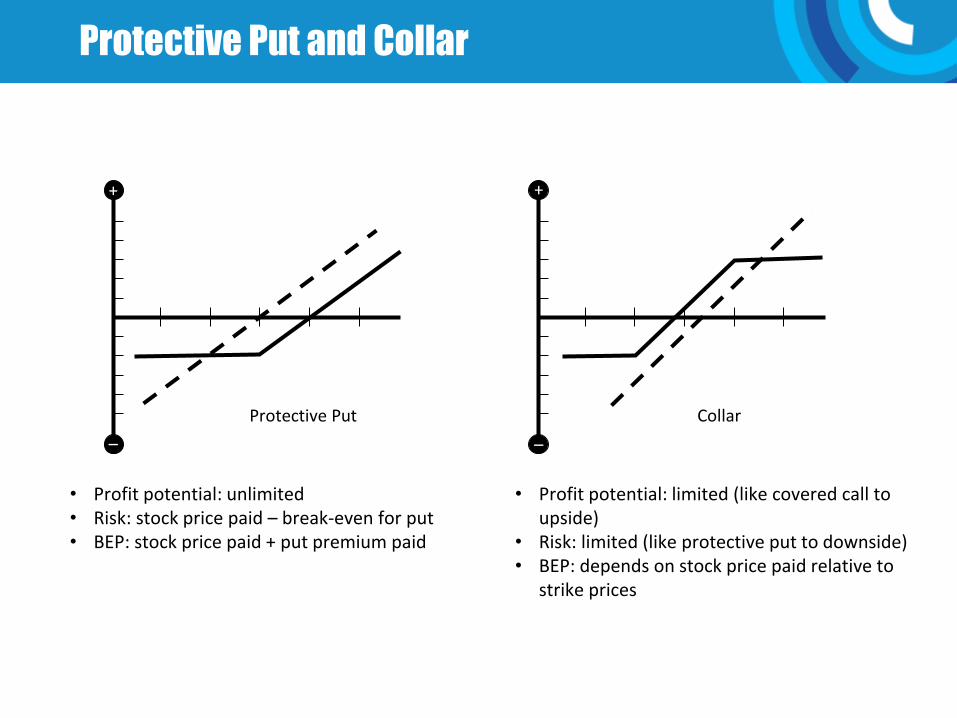

• Profit potential: unlimited • Risk: stock price paid – break-even for put • BEP: stock price paid + put premium paid

• Profit potential: limited (like covered call to upside)

• Risk: limited (like protective put to downside) • BEP: depends on stock price paid relative to

strike prices

Protective Put Collar

+

–

+

–

Protective Put and Collar

Collar: Two Strategies in One

• The 100 shares of stock play a part in both

• On the downside you have a protective put − OTM put purchased

− Grants right to sell shares at put’s strike until expiration

− OTM call will expire worthless

• On the upside you have a covered call − OTM call sold

− Upside profit limited by call’s strike price if assigned

− OTM put will expire worthless

Motivations

• Stock investor has unrealized profits −Wants downside protection for all or part

−Cost of put more than willing to pay for insurance

• Investor feels some upside profit potential remains −Sells OTM call

−Offsets all or part of put cost with premium received

• Investor accepts tradeoff −Limited upside worth downside protection desired

Definition of a Perfect Hedge: Maintain Returns, Eliminate Volatility

Goal: Introduce hedging as a value added proposition

Same returns at lower volatility

Higher returns at same volatility

Challenge

Hedging often introduce negative alpha

Hedging often impacts desired risks exposures

-10%

0%

10%

20%

30%

40%

50%

60%

0.0 1.0 4.0 5.0 2.0 3.0

Time (Years)

Portfolio Returns

Perfectly Hedged Portfolio Returns

How can we generate alpha through the hedging process?

Beta Hedging

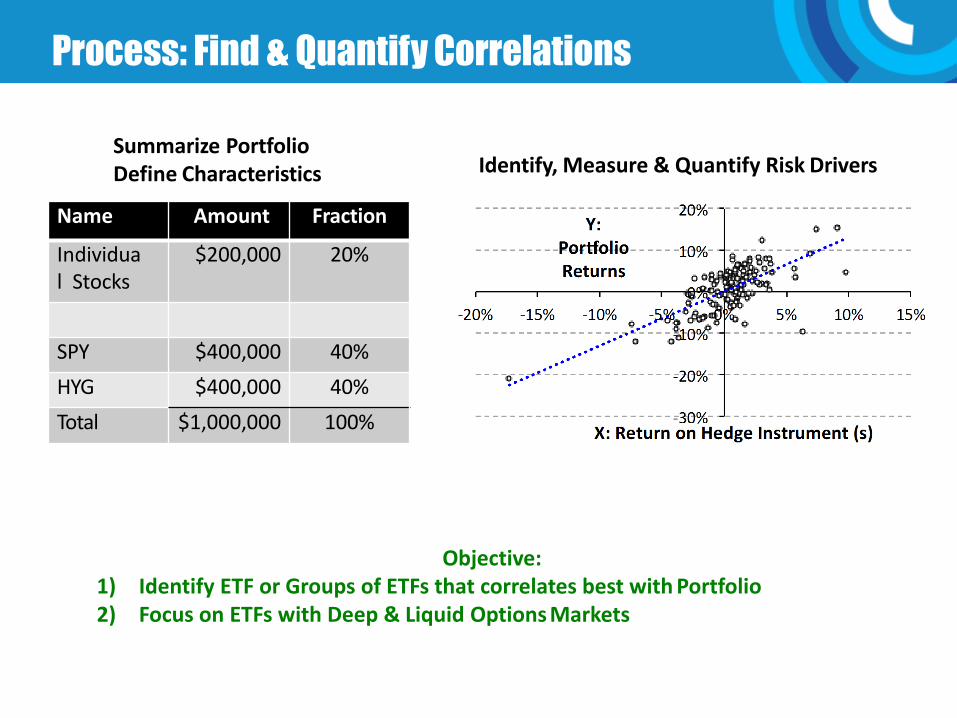

Process: Find & Quantify Correlations

Summarize Portfolio Define Characteristics

Name Amount Fraction

Individual Stocks

$200,000 20%

SPY $400,000 40%

HYG $400,000 40%

Total $1,000,000 100%

Identify, Measure & Quantify Risk Drivers

Objective: 1) Identify ETF or Groups of ETFs that correlates best with Portfolio 2) Focus on ETFs with Deep & Liquid Options Markets

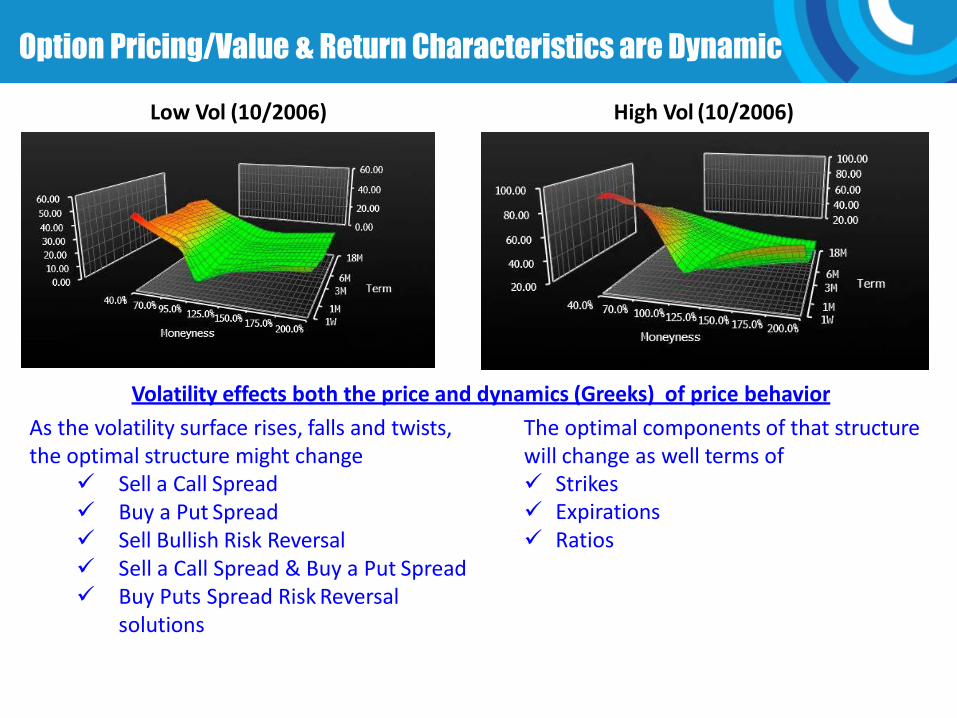

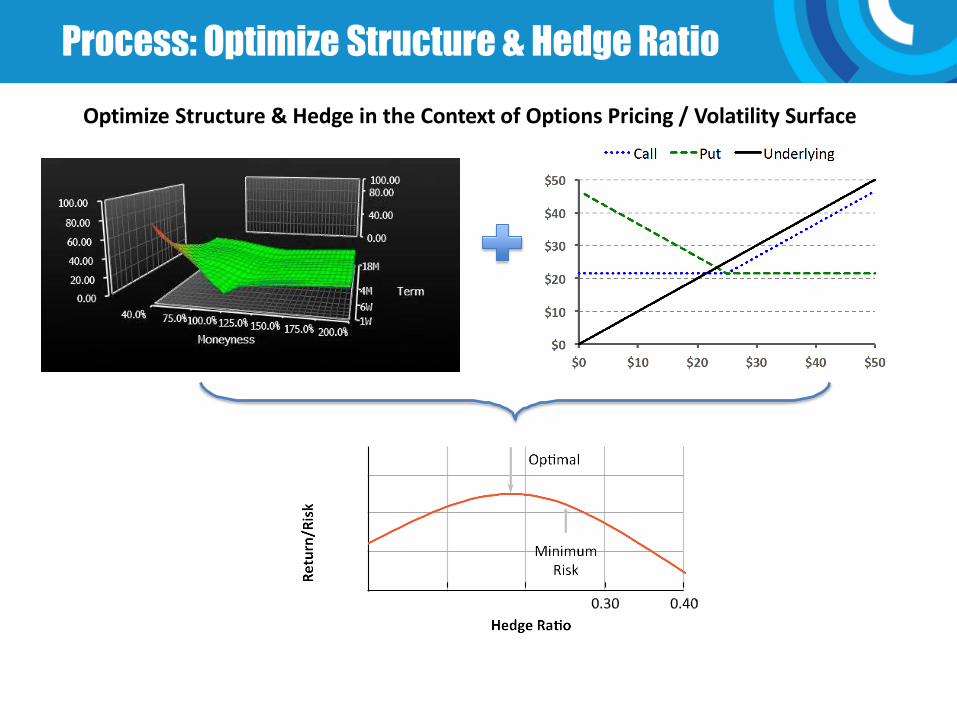

Option Pricing/Value & Return Characteristics are Dynamic

Low Vol (10/2006) High Vol (10/2006)

As the volatility surface rises, falls and twists, the optimal structure might change

Sell a Call Spread Buy a Put Spread Sell Bullish Risk Reversal Sell a Call Spread & Buy a Put Spread Buy Puts Spread Risk Reversal

solutions

The optimal components of that structure will change as well terms of Strikes Expirations Ratios

Volatility effects both the price and dynamics (Greeks) of price behavior

Process: Optimize Structure & Hedge Ratio

Optimize Structure & Hedge in the Context of Options Pricing / Volatility Surface

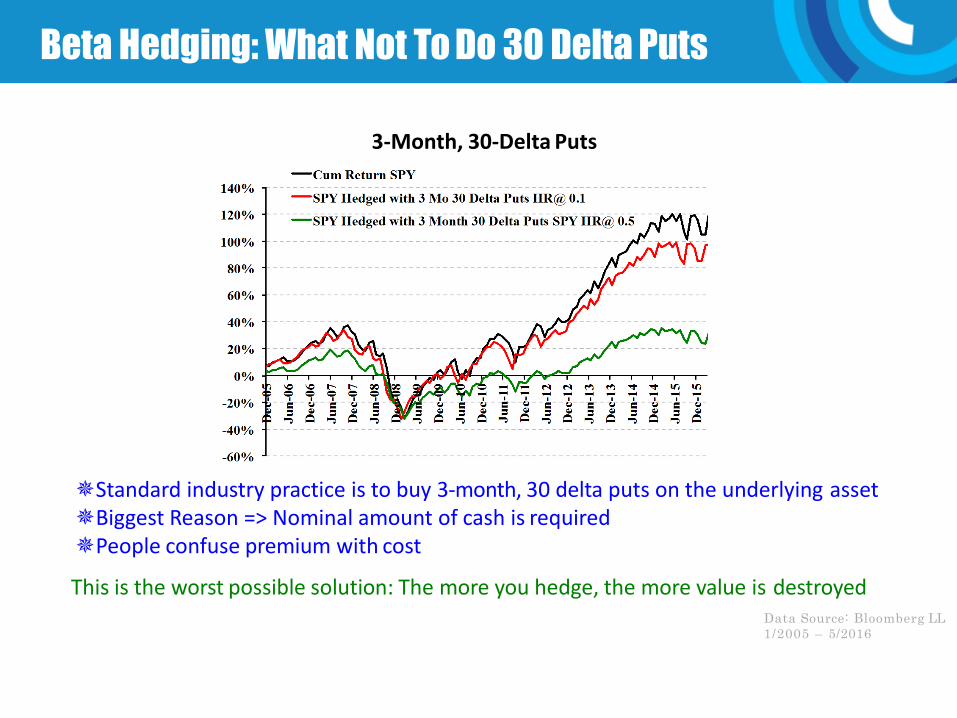

Beta Hedging: What Not To Do 30 Delta Puts

3-Month, 30-Delta Puts

Data Source: Bloomberg LL

1/2005 – 5/2016

Standard industry practice is to buy 3-month, 30 delta puts on the underlying asset Biggest Reason => Nominal amount of cash is required People confuse premium with cost

This is the worst possible solution: The more you hedge, the more value is destroyed

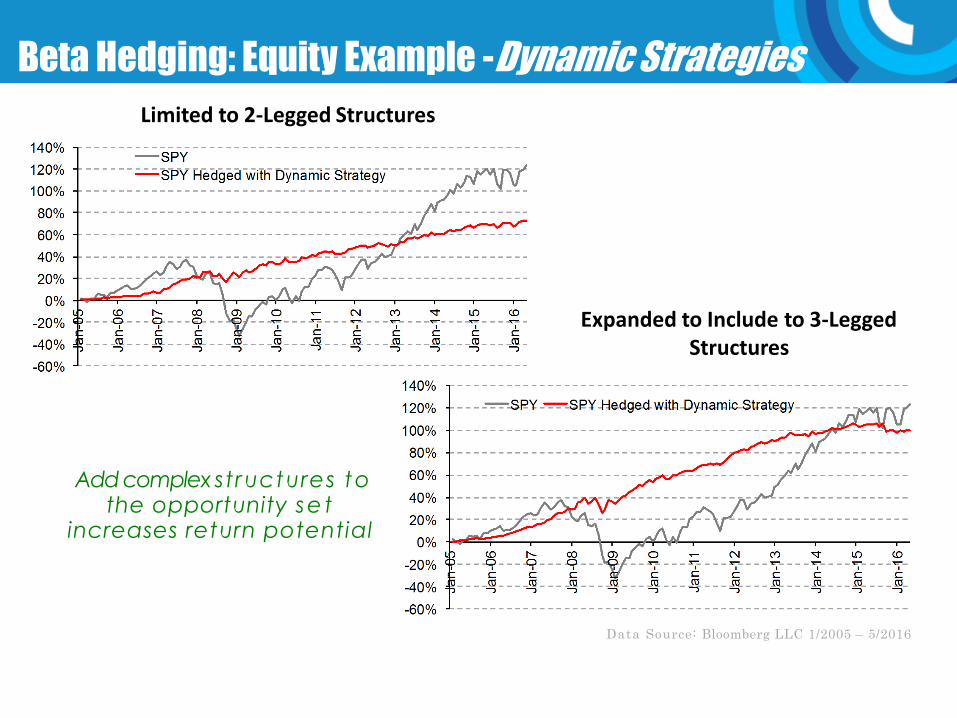

Beta Hedging: Equity Example -Dynamic Strategies

Data Source: Bloomberg LLC 1/2005 – 5/2016

Limited to 2-Legged Structures

Expanded to Include to 3-Legged Structures

Add complex structures to the opportunity se t

increases return potential

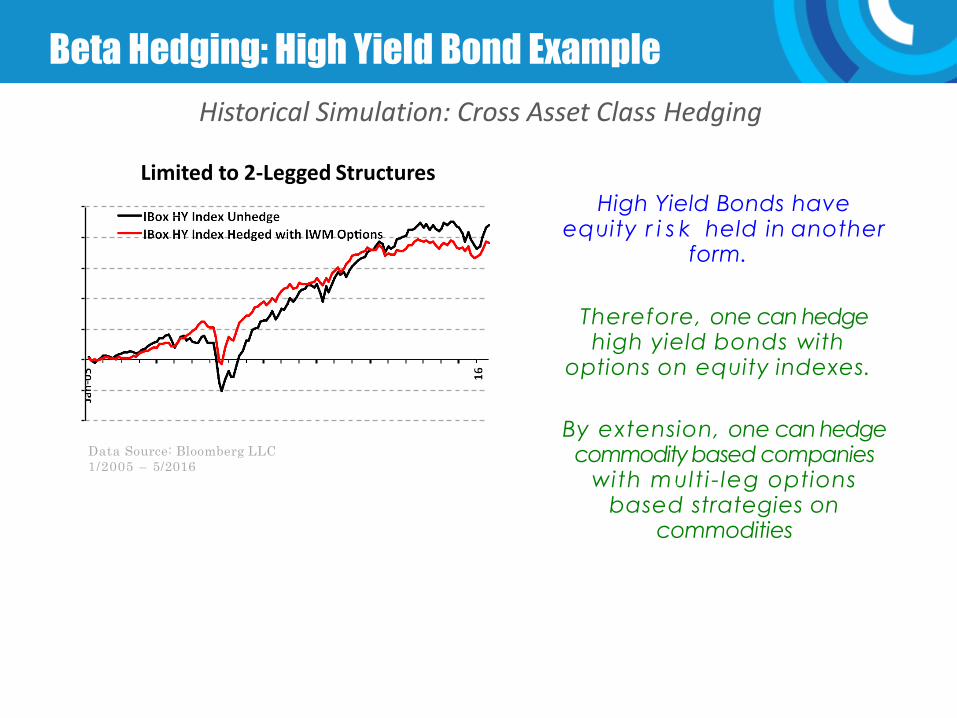

Historical Simulation: Cross Asset Class Hedging

Data Source: Bloomberg LLC

1/2005 – 5/2016

High Yield Bonds have equity r i s k held in another

form.

Therefore, one can hedge high yield bonds with

options on equity indexes.

By extension, one can hedge commodity based companies

with mult i - leg options based strategies on

commodities

Limited to 2-Legged Structures

Beta Hedging: High Yield Bond Example

SPYIX

43

• Bats T3 SPY Volatility Index: A measure of expected 30-day volatility in the SPDR S&P 500 ETF (SPY)

• The SPYIX is calculated using highly active, electronically traded, multiply listed SPY options

• Improvement over the slower, manually traded, floor-based S&P 500 index options used to calculate other volatility benchmarks

• Incorporates a proprietary “price-dragging” technique to capture live options prices; Reduces erratic intraday movement in the index

• SPYIX uses the well-known variance swap methodology to estimate the market's expectation of volatility

• Highly compatible with existing volatility-based futures, options and exchange-traded products

Reliability

44

• www.OptionsEducation.org

• Investor Services: [email protected]

• OIC’s Mobile App

• OIC YouTube Channel

For More Information

Covered Calls Benefits & Tradeoffs

Joe Burgoyne Director, Options Industry Council

Thank you for attending

www.OptionsEducation.org