governance in india

DESCRIPTION

Logistics In India,TRANSCRIPT

GOVERNANCE IN INDIA: INFRASTRUCTURE

TABLE OF CONTENTS

Contents

ABSTRACT ________________________________________________________________________________________________ 1

Introduction ______________________________________________________________________________________________ 2

History of infrastructure in India. _______________________________________________________________________ 3

Current state of India’s infrastructure __________________________________________________________________ 4

Importance of Infrastructure in India___________________________________________________________________ 6

Potentials of the India’s infrastructure _________________________________________________________________ 7

Employment generation in Infrastructure Sector. _____________________________________________________ 8

Sub-sectors ________________________________________________________________________________________________ 9

Foreign trade policy on infrastructure sector ________________________________________________________ 14

Related articles and extra read ________________________________________________________________________ 15

Conclusion ______________________________________________________________________________________________ 16

References ______________________________________________________________________________________________ 17

Page 1

ABSTRACT

The Indian infrastructure sector continues its sluggish journey in 2012, marked by poor

macroeconomic forces, policy gridlock and political instability. Delays in land

acquisition and environmental clearances continue to be key areas of concern, while

the poor enforcement of contracts, ineffective monitoring and high input costs are also

factors that are hindering growth. Nonetheless, some areas have witnessed progress.

The telecom sector saw the emergence of the National Telecom Policy, a cohesive

document covering a broad range of communication services. In both civil aviation and

power sectors, the Government of India has approved foreign investment of 49 per

cent, bringing relief to the heavily leveraged public and private companies. However,

several events in the infrastructure sector have been disappointing this year — the

telecom sector dealt with the fallout of the 2G scam, the power sector witnessed the

coal scam and the grid collapse, the roads and urban sectors saw the poor private

participation, and the civil aviation sector witnessed the poor financial health of the

airport and airline operators. The end of the 11th Five-Year Plan saw India missing

targets in infrastructure development in sectors such as railways, ports, electricity, and

airports, while investing beyond the budgeted investment in others — the roads and

telecom sectors. Overall, Rs9.45 trillion as invested in Indian infrastructure between

fiscal years 2007–08 and 2011–12, 95 per cent of the projected Rs 20.56 trillion.

The 12th Five-Year Plan projects the total investment in infrastructure during the

period to be Rs 51.46 trillion, with 47 per cent contributed by private participation and

53 per cent by the central and state governments.

This report addresses the achievements, policy developments and problems faced by

various sectors. Physical and financial progress are tracked in these crucial sectors,

along with the introduction of new policies and participation of the private sector.

Page 2

Introduction

India's emerging economic power, like that of neighboring China, has been spurred by

its momentous growth rates in the past few decades. But years of underinvestment in

infrastructure have left the country with poorly functioning transit systems and power

grids that have further endangered its slowing economy. Growth slipped from 10.5

percent in 2010 to 4.8 percent in 2013, according to the World Bank. Burgeoning trade

is putting pressure on India's inefficient ports, and rapid urbanization is straining the

country's unreliable electricity and water networks. Bureaucratic red tape and political

inertia have thwarted the success of foreign investment partnerships and bruised India's

international standing, discouraging further outside investment. Such large-scale

failures have raised sharp debate about how the country's infrastructure weaknesses

will hamper its economic future as it struggles to recover from a slowdown.

Post-independence, the government led a state-centric approach to infrastructure

development by building, owning, and managing projects. The system created a host of

inefficiencies; after years of unmet demand and growing financial constraints, the

government opened the sector to private investment as part of its economic liberalization

in the early 1990s. The endemic dysfunction has bruised India's international standing

and further discouraged direly needed outside investment. India ranked 85 out of 148

for its infrastructure in the World Economic Forum's most recent Global Competitiveness

Report. Delhi and Mumbai, its two largest cities, ranked far below other regional capitals

like Beijing and Bangkok for infrastructure in a UN report.

In this report the main focus on infrastructure sub sectors are:

1) Airports 2) Railways 3) Roads 4) Telecom 5) Ports 6) Power

The Indian economy is still expanding significantly, and substantial investment in

infrastructure continues to be required in order to sustain India’s economic progress.

The country’s capacity to absorb and benefit from new technology and industries

depends on the availability, quality and efficiency of more basic forms of infrastructure

including energy, water and land transportation. In some areas, roads, rail lines, ports

and airports are already operating at capacity, so expansion is a necessary prerequisite

to further economic growth.

Page 3

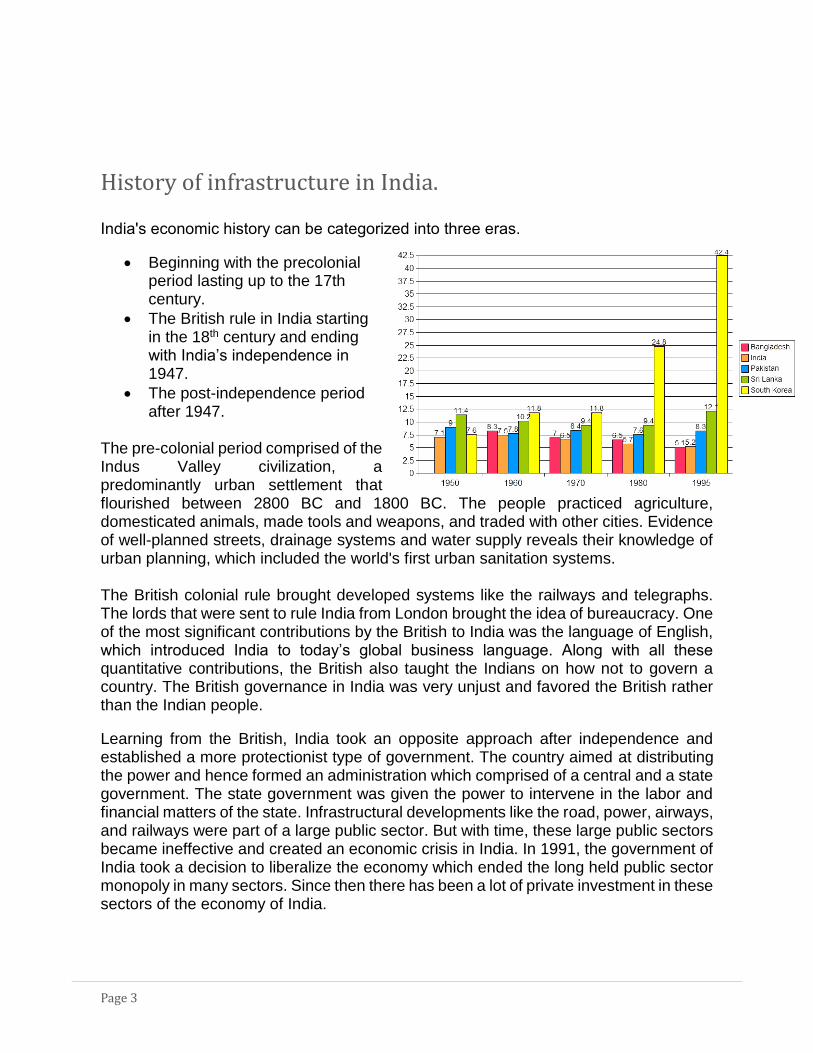

History of infrastructure in India.

India's economic history can be categorized into three eras.

Beginning with the precolonial period lasting up to the 17th century.

The British rule in India starting in the 18th century and ending with India’s independence in 1947.

The post-independence period after 1947.

The pre-colonial period comprised of the Indus Valley civilization, a predominantly urban settlement that flourished between 2800 BC and 1800 BC. The people practiced agriculture, domesticated animals, made tools and weapons, and traded with other cities. Evidence of well-planned streets, drainage systems and water supply reveals their knowledge of urban planning, which included the world's first urban sanitation systems. The British colonial rule brought developed systems like the railways and telegraphs. The lords that were sent to rule India from London brought the idea of bureaucracy. One of the most significant contributions by the British to India was the language of English, which introduced India to today’s global business language. Along with all these quantitative contributions, the British also taught the Indians on how not to govern a country. The British governance in India was very unjust and favored the British rather than the Indian people.

Learning from the British, India took an opposite approach after independence and established a more protectionist type of government. The country aimed at distributing the power and hence formed an administration which comprised of a central and a state government. The state government was given the power to intervene in the labor and financial matters of the state. Infrastructural developments like the road, power, airways, and railways were part of a large public sector. But with time, these large public sectors became ineffective and created an economic crisis in India. In 1991, the government of India took a decision to liberalize the economy which ended the long held public sector monopoly in many sectors. Since then there has been a lot of private investment in these sectors of the economy of India.

Page 4

Current state of India’s infrastructure

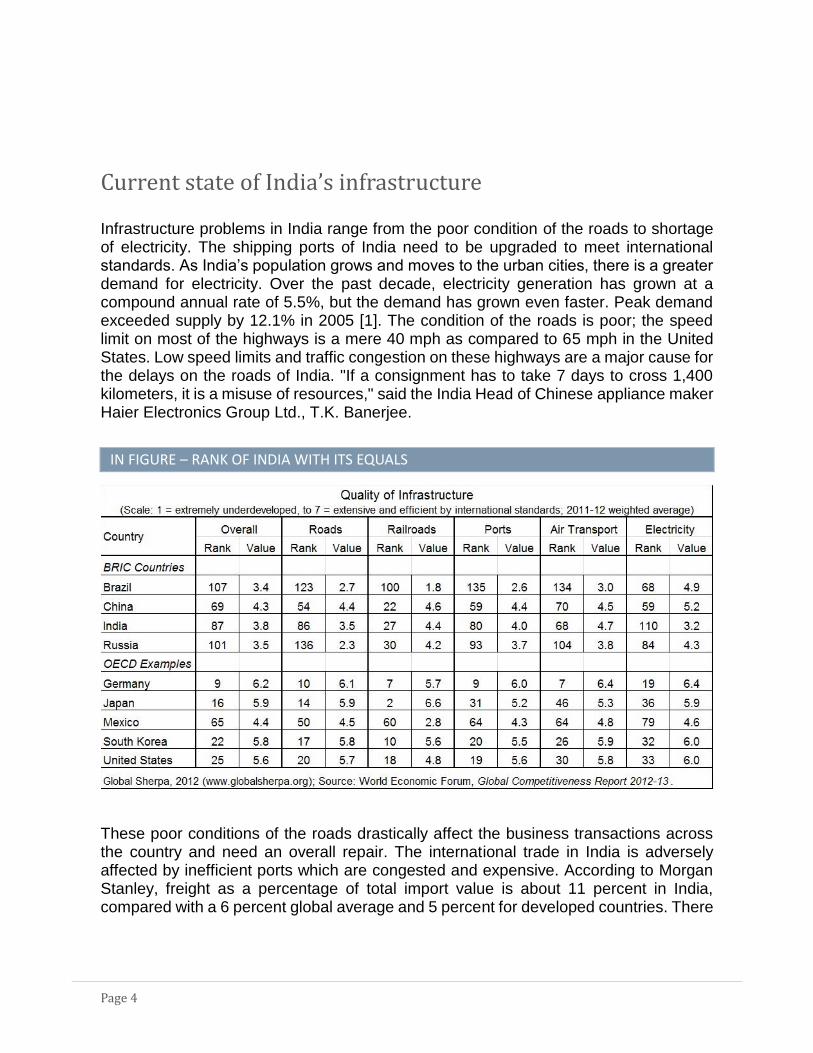

Infrastructure problems in India range from the poor condition of the roads to shortage of electricity. The shipping ports of India need to be upgraded to meet international standards. As India’s population grows and moves to the urban cities, there is a greater demand for electricity. Over the past decade, electricity generation has grown at a compound annual rate of 5.5%, but the demand has grown even faster. Peak demand exceeded supply by 12.1% in 2005 [1]. The condition of the roads is poor; the speed limit on most of the highways is a mere 40 mph as compared to 65 mph in the United States. Low speed limits and traffic congestion on these highways are a major cause for the delays on the roads of India. "If a consignment has to take 7 days to cross 1,400 kilometers, it is a misuse of resources," said the India Head of Chinese appliance maker Haier Electronics Group Ltd., T.K. Banerjee.

IN FIGURE – RANK OF INDIA WITH ITS EQUALS

These poor conditions of the roads drastically affect the business transactions across the country and need an overall repair. The international trade in India is adversely affected by inefficient ports which are congested and expensive. According to Morgan Stanley, freight as a percentage of total import value is about 11 percent in India, compared with a 6 percent global average and 5 percent for developed countries. There

Page 5

is also a higher lead-time for trade: 6 to 12 weeks for India's trade with the United States, compared with China's 2 to 3 weeks.

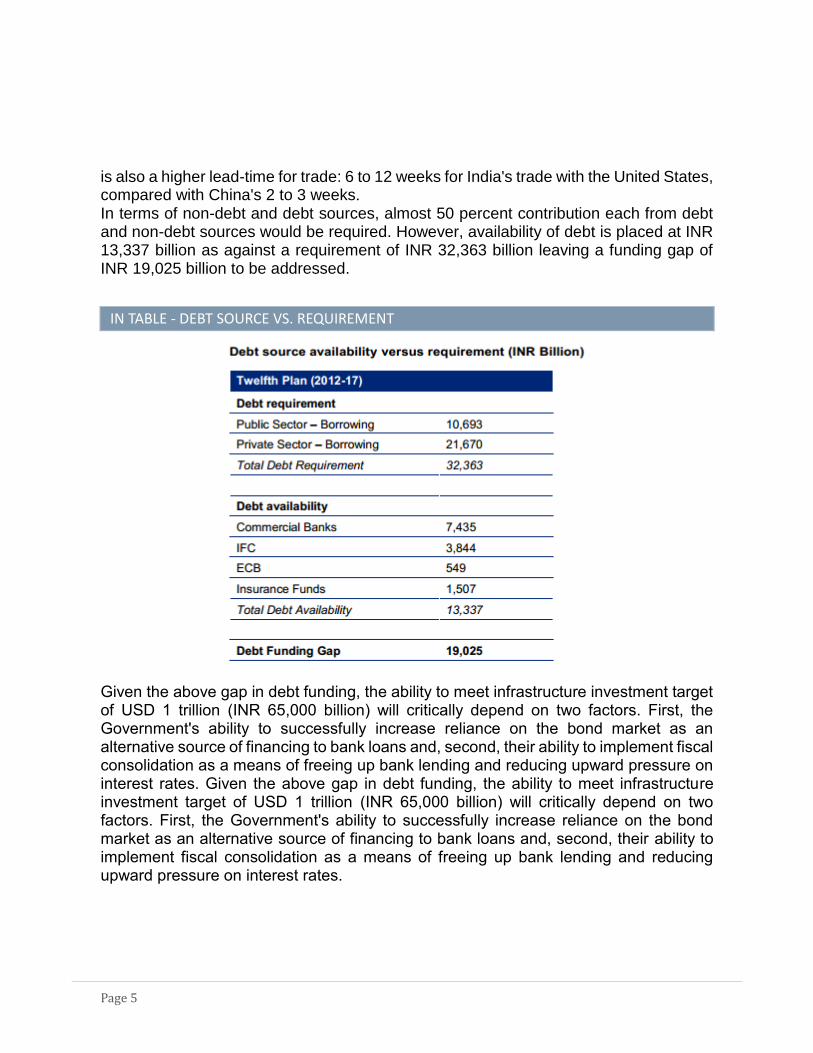

In terms of non-debt and debt sources, almost 50 percent contribution each from debt and non-debt sources would be required. However, availability of debt is placed at INR 13,337 billion as against a requirement of INR 32,363 billion leaving a funding gap of INR 19,025 billion to be addressed.

IN TABLE - DEBT SOURCE VS. REQUIREMENT

Given the above gap in debt funding, the ability to meet infrastructure investment target of USD 1 trillion (INR 65,000 billion) will critically depend on two factors. First, the Government's ability to successfully increase reliance on the bond market as an alternative source of financing to bank loans and, second, their ability to implement fiscal consolidation as a means of freeing up bank lending and reducing upward pressure on interest rates. Given the above gap in debt funding, the ability to meet infrastructure investment target of USD 1 trillion (INR 65,000 billion) will critically depend on two factors. First, the Government's ability to successfully increase reliance on the bond market as an alternative source of financing to bank loans and, second, their ability to implement fiscal consolidation as a means of freeing up bank lending and reducing upward pressure on interest rates.

Page 6

Importance of Infrastructure in India

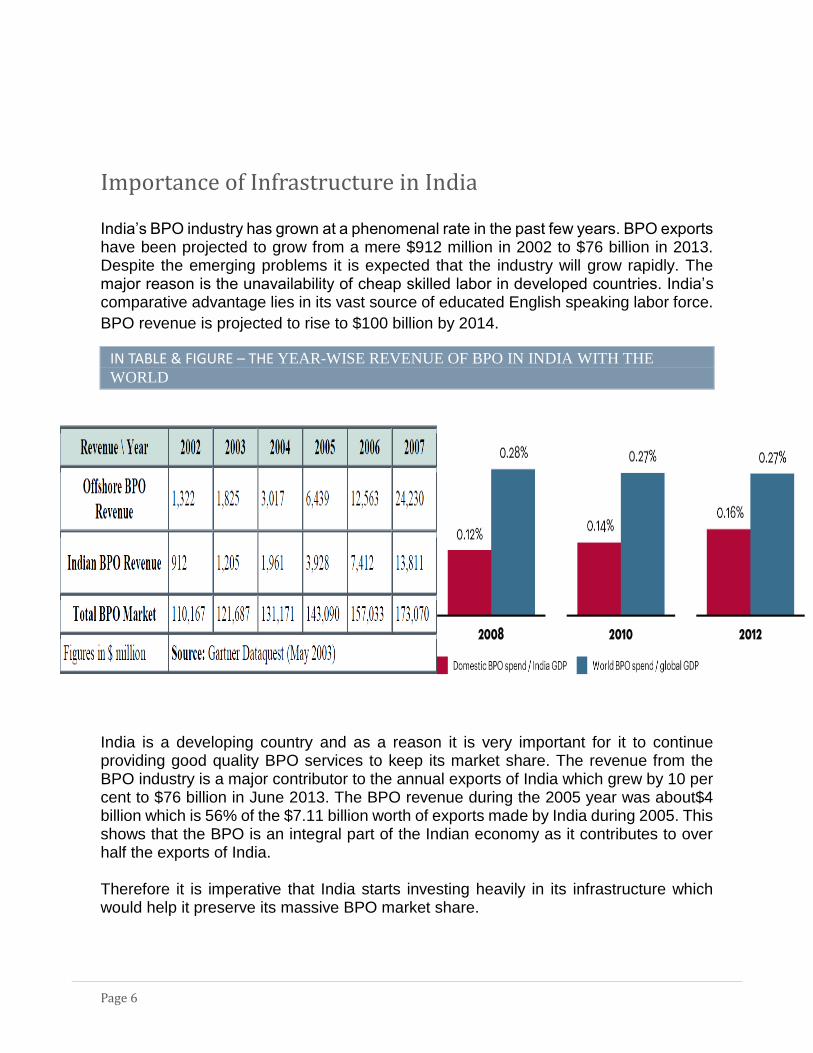

India’s BPO industry has grown at a phenomenal rate in the past few years. BPO exports have been projected to grow from a mere $912 million in 2002 to $76 billion in 2013. Despite the emerging problems it is expected that the industry will grow rapidly. The major reason is the unavailability of cheap skilled labor in developed countries. India’s comparative advantage lies in its vast source of educated English speaking labor force.

BPO revenue is projected to rise to $100 billion by 2014.

IN TABLE & FIGURE – THE YEAR-WISE REVENUE OF BPO IN INDIA WITH THE

WORLD

India is a developing country and as a reason it is very important for it to continue providing good quality BPO services to keep its market share. The revenue from the BPO industry is a major contributor to the annual exports of India which grew by 10 per cent to $76 billion in June 2013. The BPO revenue during the 2005 year was about$4 billion which is 56% of the $7.11 billion worth of exports made by India during 2005. This shows that the BPO is an integral part of the Indian economy as it contributes to over half the exports of India. Therefore it is imperative that India starts investing heavily in its infrastructure which would help it preserve its massive BPO market share.

Page 7

Potentials of the India’s infrastructure

After sixty five years of Indian independence, India is still often referred to as a developing country and its long term growth seems to stagnate at ~7%. A direct consequence of this arrested growth in the Indian economy, has been the increase in the inequality between modern, urban India and backward, rural India. If India could capitalize on its vast resources, including an integration of its rural, urban and coastal areas, India would be well placed to increase its economic growth by leaps and bounds. The reality remains that any such integration will only be possible if Indian infrastructure improves. There is a crying need for improved rail, road, port, electricity. Infrastructure in India is increasingly being viewed as a potential sector of growth and investment. Opportunities are aplenty in related segments such as power, civil aviation, roads and highways etc. Earlier this year, Dr. Manmohan Singh, the Hon'ble Prime Minister of India, during a conference on 'Building Infrastructure: Challenges and Opportunities' organized by the Planning Commission in New Delhi, on March 23, 2010, had indicated of a 10 per cent growth target per annum being set for the 12th Five-Year Plan (2012-17). "In effect the investment in infrastructure should be doubled to US$ 1 trillion in the 12th Five Year Plan as against the target of US$ 439.46 billion in the 11th Plan", he remarked.

As per the national spending plan under the Eleventh Five Year Plan (2006-2007 to 2011-2012), a sum of US$ 354 billion is required to be spent in various infrastructure projects. Such projects are being implemented under Public Private Partnership (PPP) and many projects will be implemented through foreign investments. To achieve long term growth, the Government of India has set an ambitious target of increasing total investment in infrastructure from 5% of GDP in the base year of the Plan 2006-07 to 9% by the year 2011-2012.

Based on the plan, around 30% of the required investment of around Rs. 2,056,150 Crores (US $ 154 billion) is required to be invested through private capital. Such capital is expected to be invested through debt and equity by the private sector under PPP projects.

India needs to develop a rupee-denominated long term bond market for funding the infrastructure sector that requires an investment of around US$ 459 to US$ 500 billion by 2012. The recent move by the government to issue tax-free infrastructure bonds and US $11 billion debt fund will help the government get about US$ 1 trillion target by 2017. Therefore, infrastructure investment in India is expected to grow dramatically under the Twelfth Five Year Plan (2012-2013 to 2016-2017).

Page 8

Employment generation in Infrastructure Sector.

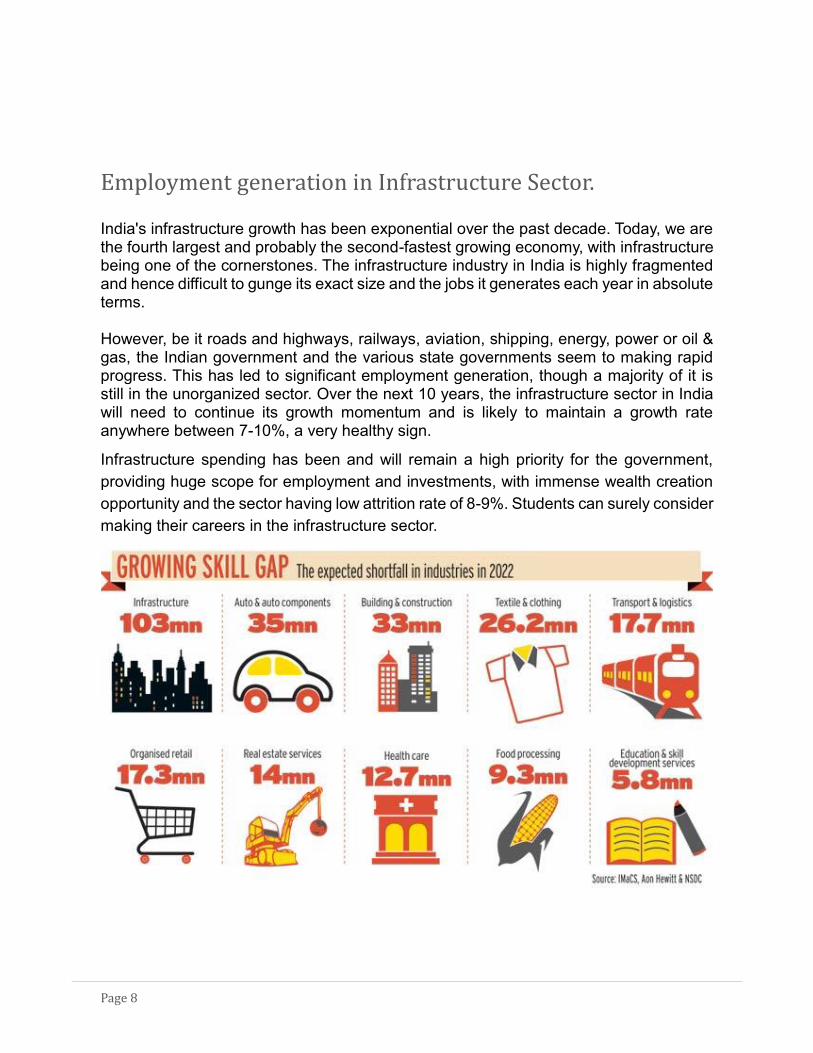

India's infrastructure growth has been exponential over the past decade. Today, we are the fourth largest and probably the second-fastest growing economy, with infrastructure being one of the cornerstones. The infrastructure industry in India is highly fragmented and hence difficult to gunge its exact size and the jobs it generates each year in absolute terms. However, be it roads and highways, railways, aviation, shipping, energy, power or oil & gas, the Indian government and the various state governments seem to making rapid progress. This has led to significant employment generation, though a majority of it is still in the unorganized sector. Over the next 10 years, the infrastructure sector in India will need to continue its growth momentum and is likely to maintain a growth rate anywhere between 7-10%, a very healthy sign.

Infrastructure spending has been and will remain a high priority for the government,

providing huge scope for employment and investments, with immense wealth creation

opportunity and the sector having low attrition rate of 8-9%. Students can surely consider

making their careers in the infrastructure sector.

Page 9

Sub-sectors

POWER

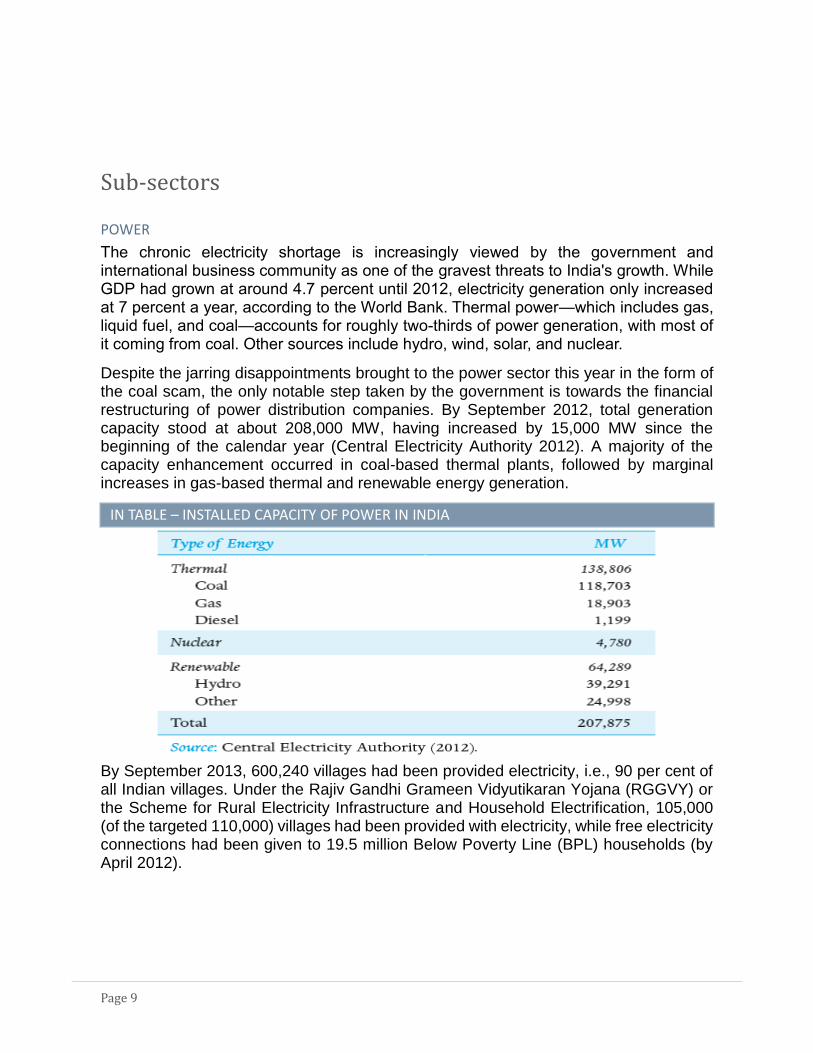

The chronic electricity shortage is increasingly viewed by the government and international business community as one of the gravest threats to India's growth. While GDP had grown at around 4.7 percent until 2012, electricity generation only increased at 7 percent a year, according to the World Bank. Thermal power—which includes gas, liquid fuel, and coal—accounts for roughly two-thirds of power generation, with most of it coming from coal. Other sources include hydro, wind, solar, and nuclear.

Despite the jarring disappointments brought to the power sector this year in the form of the coal scam, the only notable step taken by the government is towards the financial restructuring of power distribution companies. By September 2012, total generation capacity stood at about 208,000 MW, having increased by 15,000 MW since the beginning of the calendar year (Central Electricity Authority 2012). A majority of the capacity enhancement occurred in coal-based thermal plants, followed by marginal increases in gas-based thermal and renewable energy generation.

IN TABLE – INSTALLED CAPACITY OF POWER IN INDIA

By September 2013, 600,240 villages had been provided electricity, i.e., 90 per cent of all Indian villages. Under the Rajiv Gandhi Grameen Vidyutikaran Yojana (RGGVY) or the Scheme for Rural Electricity Infrastructure and Household Electrification, 105,000 (of the targeted 110,000) villages had been provided with electricity, while free electricity connections had been given to 19.5 million Below Poverty Line (BPL) households (by April 2012).

Page 10

Prominent companies

Public sector o Power Finance Corporation o Central Electricity Regulatory Commission o Damodar Valley Corporation o Nuclear Power Corporation of India Limited o NHPC Limited o NTPC Limited

Private sector

o Adani Power o Tata Power Company Ltd o Suzlon o Reliance Power Limited

IN FIGURE- PROPOSED BUDGET FOR POWER SECTOR IN 12TH FIVE-YEAR PLAN

ROADS

In September 2013, the total length of the road network was 33 lakhs km. The National Highway Development Program (NHDP) being implemented by the National Highways Authority of India (NHAI) had achieved 17,372 km of four-lane national highways (by October 2012) out of the total 48,254 km covered under the NHDP (NHAI 2012). Under the Pradhan Mantri Gram Sadak Yojana (PMGSY) about 55 per cent of all rural settlements had been connected by 214,758 km of new roads and 142,528 km of improved roads by June 2012. During the fiscal year 2011–12, NHAI constructed roads at the rate of 6.16 km per day, while the State Public Work Departments and Border Roads Organization completed 4.23 km per day. The average road length constructed, however, falls well short of the targeted 20 km per day. Given that the road freight volumes have grown by 9.08 per cent and vehicles have grown by 10.76 per cent, it is important to achieve the 20 km per day target.

Prominent companies

M/s L & T Ltd M/s Uttar Pradesh Rajkiya Nirman Nigam Ltd

Page 11

M/s B.G. Shirke Construction. Tech. Ltd. M/s PBA Infrastructures Ltd M/s Unity Infra Projects Ltd. M/s Nagarjuna Construction Co. Ltd. M/s Reliance Construction Co., M/s Advance Constuction Co. Pvt. Ltd

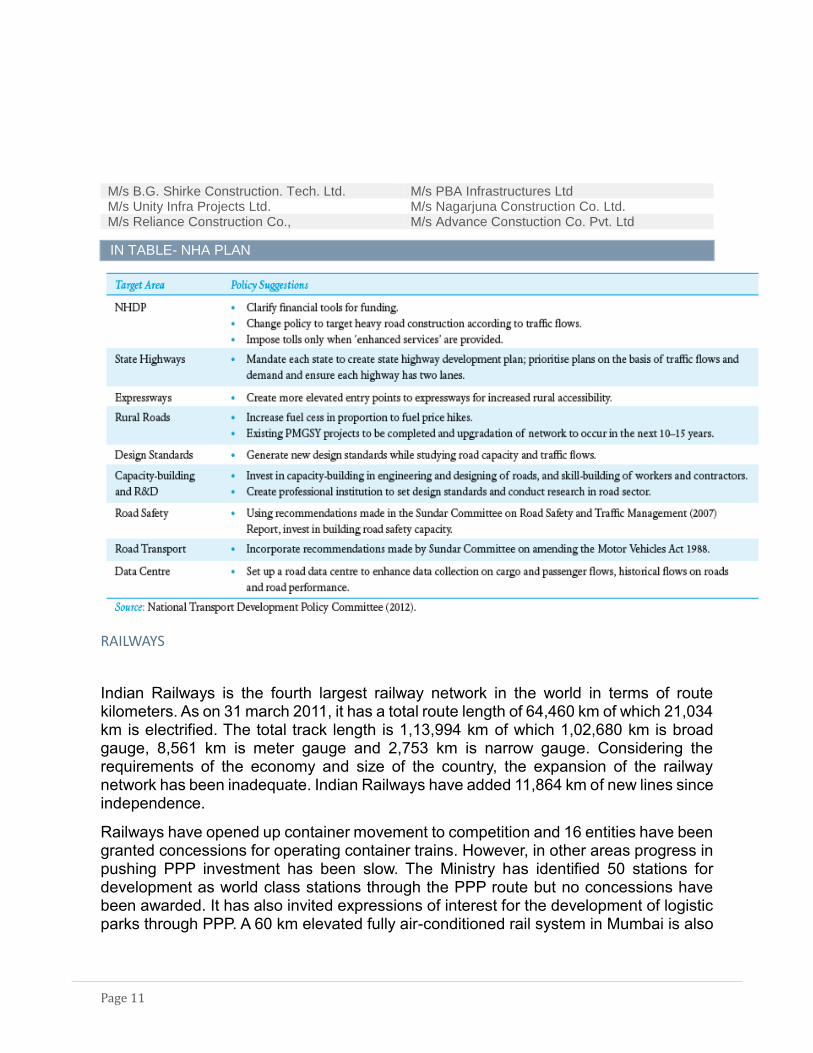

IN TABLE- NHA PLAN

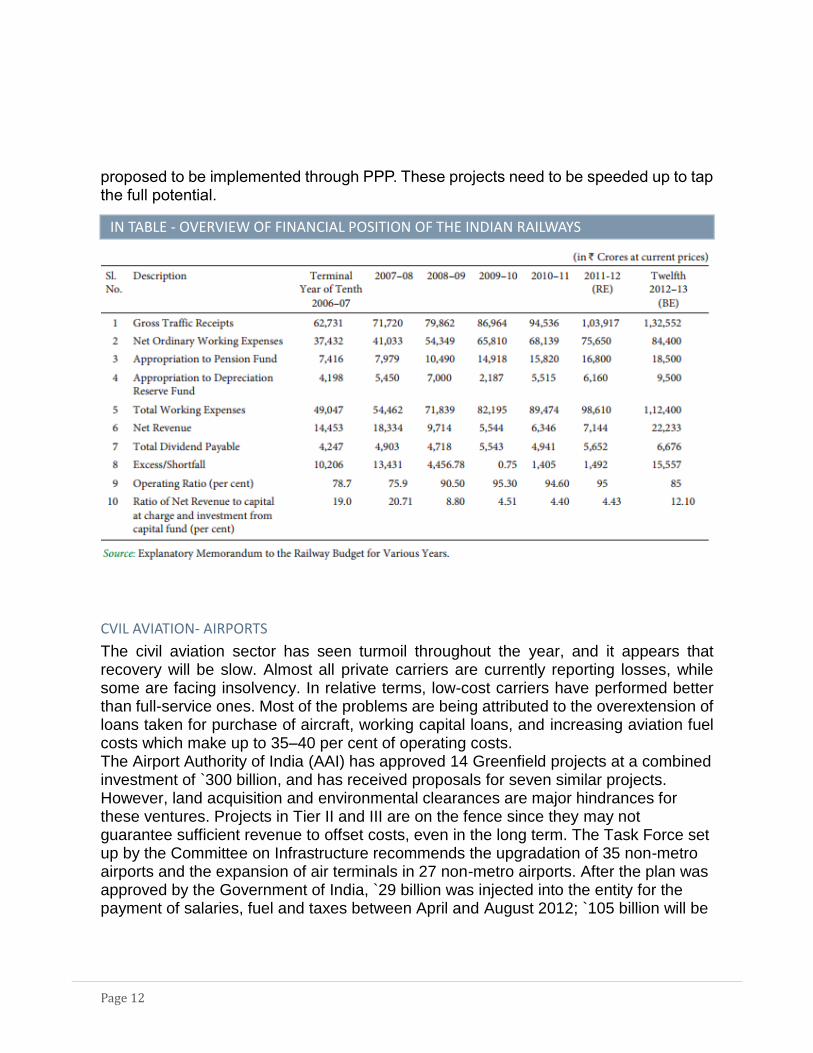

RAILWAYS

Indian Railways is the fourth largest railway network in the world in terms of route kilometers. As on 31 march 2011, it has a total route length of 64,460 km of which 21,034 km is electrified. The total track length is 1,13,994 km of which 1,02,680 km is broad gauge, 8,561 km is meter gauge and 2,753 km is narrow gauge. Considering the requirements of the economy and size of the country, the expansion of the railway network has been inadequate. Indian Railways have added 11,864 km of new lines since independence.

Railways have opened up container movement to competition and 16 entities have been granted concessions for operating container trains. However, in other areas progress in pushing PPP investment has been slow. The Ministry has identified 50 stations for development as world class stations through the PPP route but no concessions have been awarded. It has also invited expressions of interest for the development of logistic parks through PPP. A 60 km elevated fully air-conditioned rail system in Mumbai is also

Page 12

proposed to be implemented through PPP. These projects need to be speeded up to tap the full potential.

IN TABLE - OVERVIEW OF FINANCIAL POSITION OF THE INDIAN RAILWAYS

CVIL AVIATION- AIRPORTS

The civil aviation sector has seen turmoil throughout the year, and it appears that recovery will be slow. Almost all private carriers are currently reporting losses, while some are facing insolvency. In relative terms, low-cost carriers have performed better than full-service ones. Most of the problems are being attributed to the overextension of loans taken for purchase of aircraft, working capital loans, and increasing aviation fuel costs which make up to 35–40 per cent of operating costs. The Airport Authority of India (AAI) has approved 14 Greenfield projects at a combined investment of `300 billion, and has received proposals for seven similar projects. However, land acquisition and environmental clearances are major hindrances for these ventures. Projects in Tier II and III are on the fence since they may not guarantee sufficient revenue to offset costs, even in the long term. The Task Force set up by the Committee on Infrastructure recommends the upgradation of 35 non-metro airports and the expansion of air terminals in 27 non-metro airports. After the plan was approved by the Government of India, `29 billion was injected into the entity for the payment of salaries, fuel and taxes between April and August 2012; `105 billion will be

Page 13

converted to long-term debt with tenure of 10–15 years, while `74 billion will berepaid through non-convertible debentures with government guarantees. Recent developments have indicated that Air India will be selling or leasing some of its domestic and international properties for additional fund raising.

Prominent companies

Air India, Indigo, JETAIR, DECCAN AIR. Etc

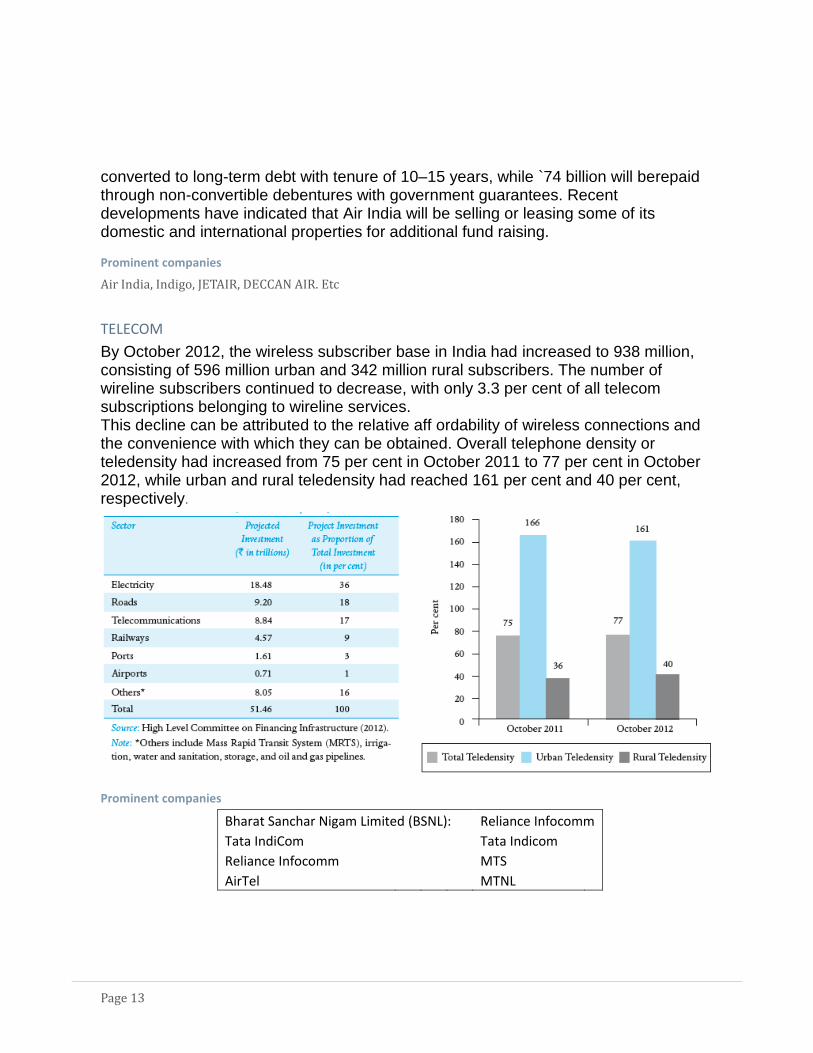

TELECOM

By October 2012, the wireless subscriber base in India had increased to 938 million, consisting of 596 million urban and 342 million rural subscribers. The number of wireline subscribers continued to decrease, with only 3.3 per cent of all telecom subscriptions belonging to wireline services. This decline can be attributed to the relative aff ordability of wireless connections and the convenience with which they can be obtained. Overall telephone density or teledensity had increased from 75 per cent in October 2011 to 77 per cent in October 2012, while urban and rural teledensity had reached 161 per cent and 40 per cent, respectively.

Prominent companies

Bharat Sanchar Nigam Limited (BSNL): Reliance Infocomm

Tata IndiCom Tata Indicom

Reliance Infocomm MTS

AirTel MTNL

Page 14

Foreign trade policy on infrastructure sector

PROMOTIONAL MEASURES IN DEPARTMENT OF COMMERCE

Scheme for Assistance to States for Developing Export for Developing Export Infrastructure

and Allied Activities (ASIDE)

Scheme for Assistance to States for Developing Export for Developing Export Infrastructure and Allied Activities (ASIDE) is formulated Infrastructure and to involve the States in the export effort by providing Allied Activities (ASIDE) assistance to the States Governments for creating appropriate infrastructure for the development and growth of exports. The Scheme is administered by Department of Commerce (DoC)

The activities aimed at development of infrastructure for exports can be funded from the scheme provided such activities have overwhelming export content and their linkage with exports is full established. The specific purposes for which funds allocated under the Scheme can be sanctioned and utilized are as follows:

Creation of new Export Promotion Industrial Parks/Zones (SEZs/Agri Business Zones) and augmenting facilities in the existing ones.

Setting up of electronics and other related infrastructure in export conclave.

Equity participation in infrastructure projects including the setting up of SEZs.

Meeting requirements of capital outlay of EPIPs/EPZs/SEZs.

Development of complementary infrastructure such as, roads connecting the production centers with the ports, setting up of Inland Container Depots and Container Freight Stations.

Stabilizing power supply through additional transformers and islanding of export production center

Development of minor ports and jetties to serve export purpose.

Assistance for setting up Common Effluent Treatment facilities and

Any other activity as may be notified by DoC.

EPCG for Retail Sector

To create modern infrastructure in retail sector, concessional duty benefits under EPCG scheme shall be extended for import of capital goods required by retailers having minimum area of 1000 sq. meters. Such retailer shall fulfill export obligation i.e. 8 times of duty saved, in 8 years.

Page 15

Related articles and extra read

India's Planning Commission details its infrastructure investment plans under

the twelfth Five-Year Plan in this report.

Power and electricity specialist Sunila Kale writes about the politics behind

India's power failure in this Foreign Affairs article.

2013 Deloitte report addresses India's infrastructure investment gap.

The New Yorker delves into the narrative of India's growth story in this 2012

article.

India's Federation of Indian Chambers of Commerce and Industry released this

October 2011 report on the country's urban infrastructure.

PwC released a 2013 report on the opportunities and challenges of India's

infrastructure.

This World Bank index gives snapshots of India's infrastructure projects.

Page 16

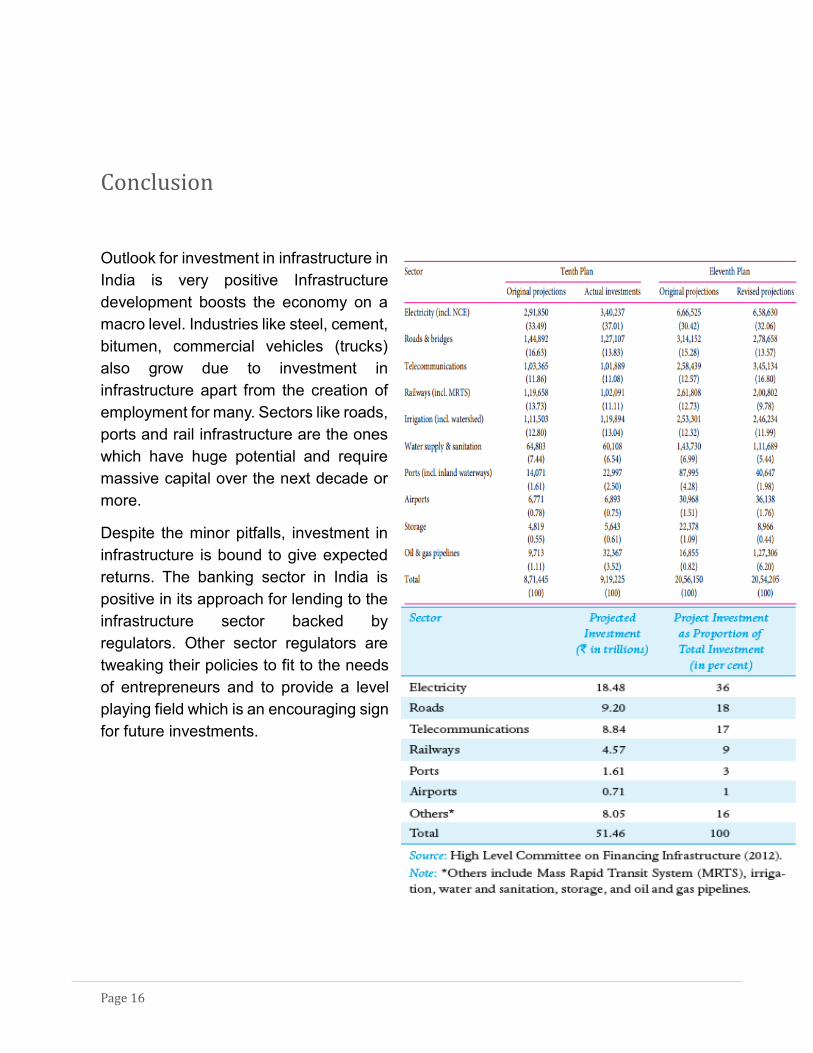

Conclusion

Outlook for investment in infrastructure in

India is very positive Infrastructure

development boosts the economy on a

macro level. Industries like steel, cement,

bitumen, commercial vehicles (trucks)

also grow due to investment in

infrastructure apart from the creation of

employment for many. Sectors like roads,

ports and rail infrastructure are the ones

which have huge potential and require

massive capital over the next decade or

more.

Despite the minor pitfalls, investment in

infrastructure is bound to give expected

returns. The banking sector in India is

positive in its approach for lending to the

infrastructure sector backed by

regulators. Other sector regulators are

tweaking their policies to fit to the needs

of entrepreneurs and to provide a level

playing field which is an encouraging sign

for future investments.

Page 17

References

1. “Underpowering” The Economist, 2005.

2. Governance in India: Infrastructure- http://www.cfr.org/india/governance-india-

infrastructure/p32638

3. Five Year Plan

4. Investment in Infrastructure – http://infrafin.in/pdf/IBEF.pdf

5. Working Sub-Group on Infrastructure

6. Infrastructure Funding Requirements and its Sources over the implementation

period of the Twelfth Five Year Plan (2012- 2017) –

http://planningcommission.gov.in/aboutus/committee/wg_sub_infrastructure.pdf

7. Report on Indian Urban Infrastructure and Services –

http://niua.org/projects/hpec/finalreport-hpec.pdf

8. Mahadevia, D. (2010). Urban Reforms in Three Cities: Bangalore, Ahmedabad

and Patna. In Chand.V (eds.), Public Service Delivery in India: Understanding

the Reform Process. Oxford University Press.