got nexus? – gaining a handle on sales tax compliance

TRANSCRIPT

Start Time: 2:00pm EST

Welcome!

Webinar Details

• Presentation is roughly 1 hour

• All phone lines are muted

• If anyone has any questions during this webinar – please type them in your Questions Box located at the bottom of your webinar panel

Today’s Presenters

Sean Munzert Net@Work

Michael Fleming Peisner Johnson & Company, LLP

Complimentary Nexus Review

Peisner Johnson has offered a Complimentary Nexus Review to all Attendees

• You will receive the Webinar Recording, Slide Deck and link to a short Questionnaire tomorrow.

• Fill out the questionnaire and Peisner Johnson will follow-up with you for a Free Review.

Got Nexus?Common myths about filing in a new state

● Founded in 1992

● Registered CPA firm

● State & local taxes only

● Former state auditors & other professionals

● Consult in all states & Canada

Who Are We?

● Materiality - Even though a state may assert you should register and collect taxes, it may not make good business sense.

● Be conservative when planning.

● Be aggressive when under Audit.

Important Points

QUESTION

What is nexus?

Nexus: A connection; a link or tieMinimum level of physical presence that allows a jurisdiction to require you to register, collect, and remit sales and use tax

In the News● Marketplace Fairness Act● Online Sales Tax Proposals● Revisit Quill?

Nexus Myth 1

If the Marketplace Fairness Act Passes,

Everyone Will Have Nexus Everywhere,

and Nexus Will Be Obsolete.

Let's Go to Court

Court Cases

● ScriptoGeorgia company used independent sales reps in Florida, and Supreme Court held that it had significant connection (1960)

● National Bellas Hess1967 Supreme Court Case. National Bellas Hess, Inc. v. Department of Revenue of Ill., 87 S.Ct. 1389 (1967)

Court Cases● Tyler Pipe

Texas company with no property, offices, or employees in Washington. Supreme Court agreed that activities created nexus and assessment stood (1987)

● Quill CorporationFor sales and use tax purposes, the Supreme Court held that a taxpayer must have a physical presence in the state. Quill Corporation v. North Dakota, 112 S.Ct. 1912 (1992)

What Creates Nexus?

Obvious

Less Obvious

Trade Shows

● Some states consider software TPP even when downloaded

● Licensing of software vs. sale of software.

● Customer downloads TPP you have ownership of. You now have a physical presence.

● Decision, Hearing No. 108,626, Texas Comptroller of Public Accounts, September 19, 2014

Downloaded Software?

NecessitatesWatching

Nexus-Creating Activities

Obvious● Buildings, property● Employees

Less Obvious● Independent sales reps● Sub-contractors, agents● Installation, training, maintenance● Rented or leased property

Generally:● Register

● Collect the sales tax/pay the income tax

○ Collect a proper resale certificate in lieu of tax

● File regular tax returns

I have nexus. Now what?

Nexus Myth 2

Unless We Have An Office or

Employees in A State, We

Do Not Have Nexus.

● Auditing your customers

● Information sharing with other states

● Special task forces

● Leads○ Former employees○ Competitors

How do states find you?

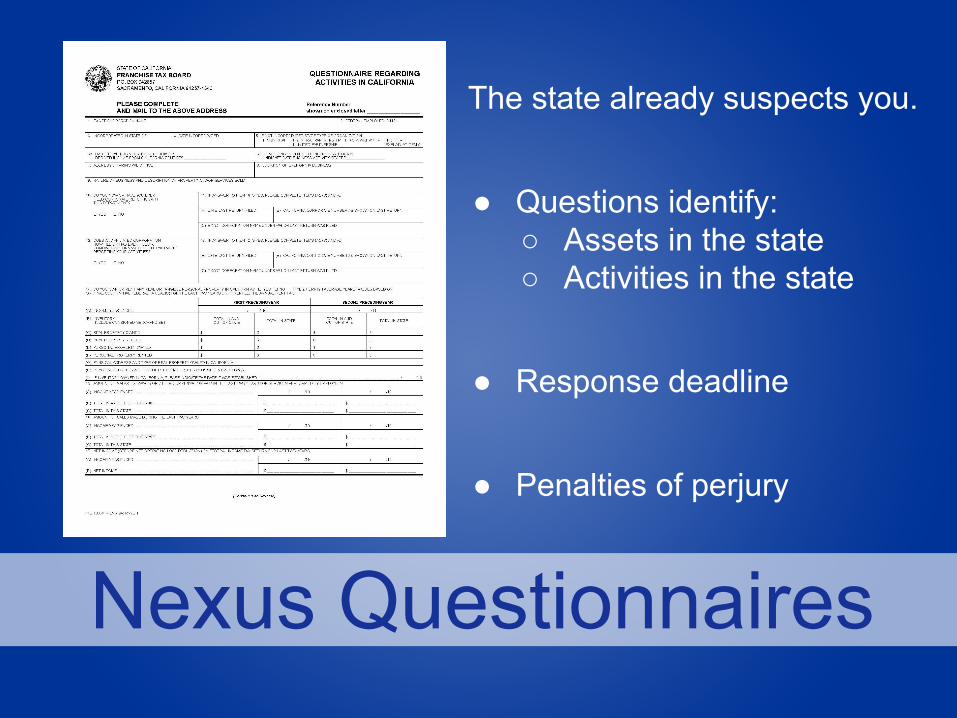

Nexus Questionnaires

The state already suspects you.

● Questions identify:○ Assets in the state○ Activities in the state

● Response deadline

● Penalties of perjury

Alabama"I declare that the information furnished in response to this questionnaire is to the best of my knowledge and belief, true, correct and complete.”

Michigan“I declare, under penalty of perjury, that the information provided in this questionnaire and any attachments is, to the best of my knowledge, true, correct and complete. If prepared by a person other than officer, partner or owner of the business, this declaration is based on all information you have knowledge.”

Questionnaire Verbiage

Texas"I declare that the information in this document and any attachment is true and correct to the best of my knowledge and belief.”

Michigan“Under penalties of perjury, I declare that the information furnished in this questionnaire is, to the best of my knowledge and belief, true, correct and complete. If prepared by a person other than an officer of this corporation, this declaration is based on all information of which you have knowledge.”

Questionnaire Verbiage

Nexus Myth 3

The Best Time To Take Action is

After We Get a Nexus

Questionnaire.

● No statute of limitations

● Seven or more years of tax assessments

● Penalties and interest○ Up to 60%

If the State Finds You

QUESTION

THE PROBLEM NEVER GOES AWAY…

IT ONLY GETS

BIGGER

CASE STUDIES

Service Company

● Small company in a couple of states

● Got national contract

● Used subcontractors to do local work

● Audited and assessed

● Registered in all states

Nexus Myth 4

Independent Subcontractors

Do Not Give Us Nexus.

Software Company

● Specialized software

● Traveled to customer sites to install and train

● Audited one of their customers

● States requested prior seven years returns

● $6,500,000 + liability

Bank Bag Company

● Largest client requested tax be charged

● Register in every state

● Set up the billing systems with correct rates and taxability

● Registered in all states

Nexus Myth 5

We Can Collect Tax From

Just One of Our Customers

in a State.

Sale of Company

● Purchaser conducted due diligence

● Determined they had nexus in states where they were not registered

● Purchaser requested they either discount price of business for amount owed or place funds in trust until resolved.

QUESTION

The Biggest Tragedy in Sales Tax

Tax you could have collected (willingly) from your customer at the time of the transaction ends up coming out of your pocket three years later…

With Penalties and Interest!

THE PROBLEM NEVER GOES AWAY…

IT ONLY GETS

BIGGER

● What states am I registered in now?

● Where else do I have nexus?

● What do I sell in those states?

Define the Problem

● Sales

● Purchases

● Net Income

● Apportionment

● Refund opportunities

Quantify the Problem

Fix the Problem● Rank your states by potential

liability

● Possible approaches○ Do nothing○ Register○ Amnesty○ Voluntary disclosure

agreement (VDA)

Nexus Myth 6

We Can Just Get Registered

and Collect The Tax Going

Forward.

Problems with Registering Now

When did you first start doing business in our state?

● All back taxes returns due○ Back to day one

● Penalty and interest applies

State Amnesty● Not true amnesties● Amnesties are rare - short lived● Read the fine print● Not usually the best alternative

● SSTP is a true amnesty● All or nothing● OH & TN

● Most states allow for anonymous application

● Generally 3-4 year look back period.

● Generally 100% penalty waiver. Civil & Criminal.

● A handful of states eliminate or reduce interest.

VDA Basics

VDA Basics continued

● Many states restrict VDAs to out-of state companies and/or companies not already registered.

● Most states disallow VDAs if previously contacted.

● Many states require income/franchise taxes be included.

● Some states are requiring SOS registrations.

● No VDA ○ New Mexico - managed

audit- 7 year lookback

● Longer look back periods○ Hawaii - ten year look back○ Iowa - five years or ½ the

time○ South Dakota - five years

● Fully disclosed at application○ California, Illinois, New York

Variants

● Allow for VDAs after contact○ Connecticut, Florida & Michigan

● Waive some or all interest○ Texas, New Mexico, Nevada -

100%○ Oklahoma - 50%○ Wisconsin reduced from - 18-

12%○ South Dakota - Negotiated

Additional Variants

● MA company received poor advice from CPA stating they were not subject to sales tax and therefore did not register.

● SALT “expert” from MA said VDA not available due to MA headquarters. They needed to pay eight years plus penalty and interest.

● We knew a VDA was available, but generally no lookback benefit. We believed we could make a case for an exception for 36 months and were told to apply and ask for it. We got it and client was ecstatic.

Knowledge + Contacts

QUESTION

Costly Mistakes● Ignoring the situation

● Failing to collect tax at the time of sale

● Registering without a VDA in place

● Remitting tax to the wrong jurisdiction

Nexus Myth 7

Sales Tax Compliance is Too

Complicated and Too Costly.

Thank You For Attending

Sean Munzert, Net@Work Phone: 646-293-1781 [email protected] www.netatwork.com

For more information: