goods and services tax (gst) place of supply rules (march...

TRANSCRIPT

GOODS AND SERVICES TAX (GST)

PLACE OF SUPPLY RULES

(MARCH 2015)

CA. UPENDER GUPTA Additional Commissioner

GST Cell CBEC

1

Taxation of Inter-State Sales / Supplies Present Proposed

Place of Supply – Significance Place of Supply Rules Significance Present Rules for Goods Present Rules for Services

Guiding Principles Place of Supply Rules – Issues??

PRESENTATION PLAN

2

TAXATION OF INTER-STATE SALES / SUPPLIES

3

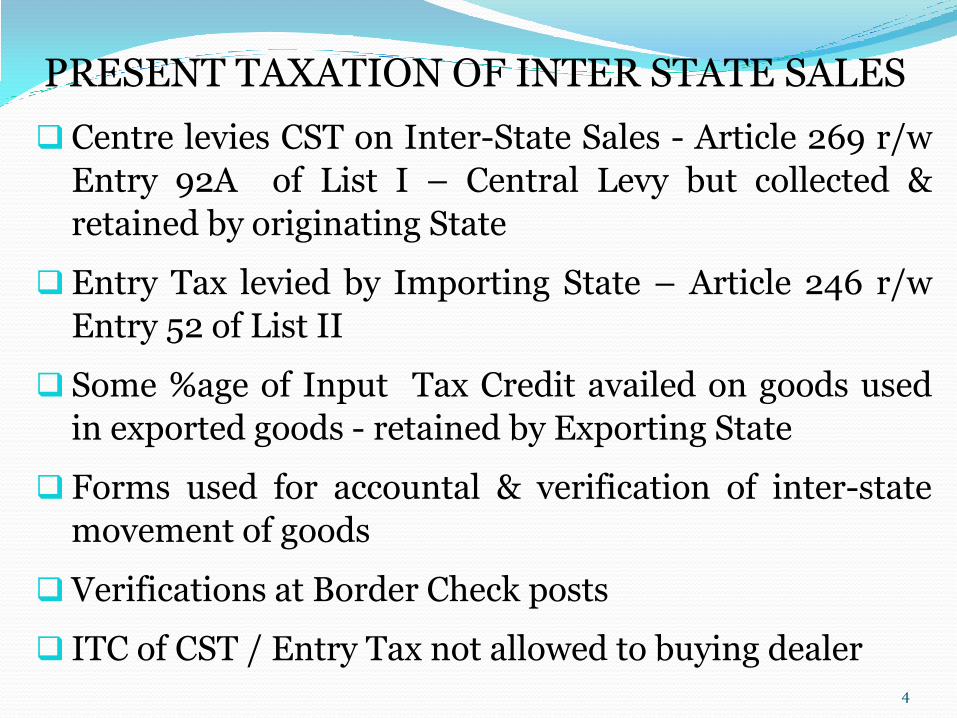

Centre levies CST on Inter-State Sales - Article 269 r/w

Entry 92A of List I – Central Levy but collected &

retained by originating State

Entry Tax levied by Importing State – Article 246 r/w

Entry 52 of List II

Some %age of Input Tax Credit availed on goods used

in exported goods - retained by Exporting State

Forms used for accountal & verification of inter-state

movement of goods

Verifications at Border Check posts

ITC of CST / Entry Tax not allowed to buying dealer

PRESENT TAXATION OF INTER STATE SALES

4

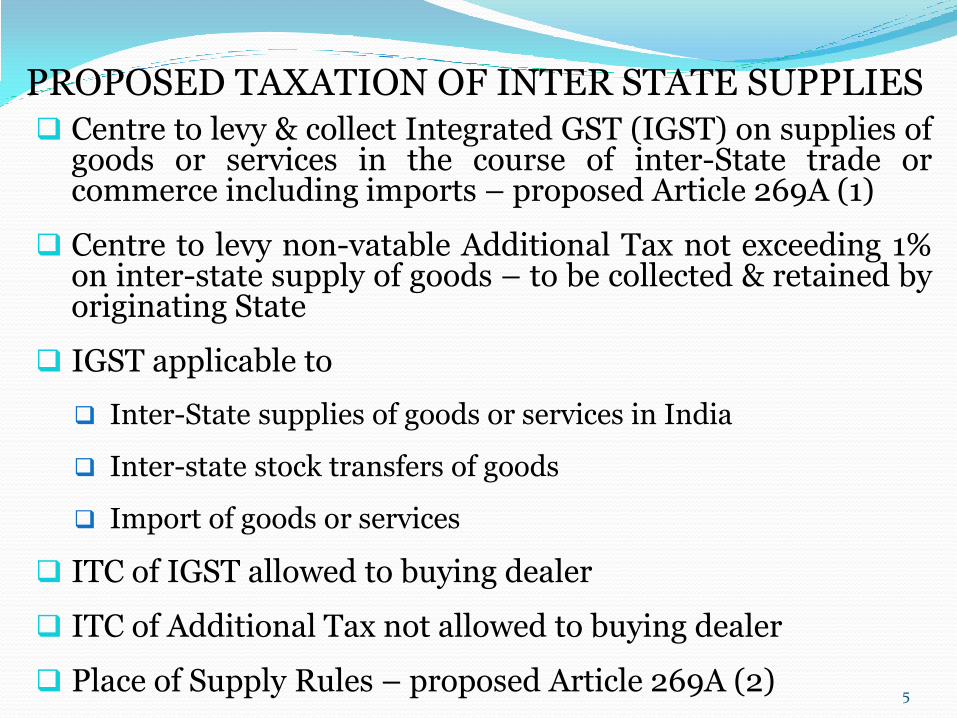

Centre to levy & collect Integrated GST (IGST) on supplies of goods or services in the course of inter-State trade or commerce including imports – proposed Article 269A (1)

Centre to levy non-vatable Additional Tax not exceeding 1% on inter-state supply of goods – to be collected & retained by originating State

IGST applicable to

Inter-State supplies of goods or services in India

Inter-state stock transfers of goods

Import of goods or services

ITC of IGST allowed to buying dealer

ITC of Additional Tax not allowed to buying dealer

Place of Supply Rules – proposed Article 269A (2)

PROPOSED TAXATION OF INTER STATE SUPPLIES

5

PLACE OF SUPPLY

6

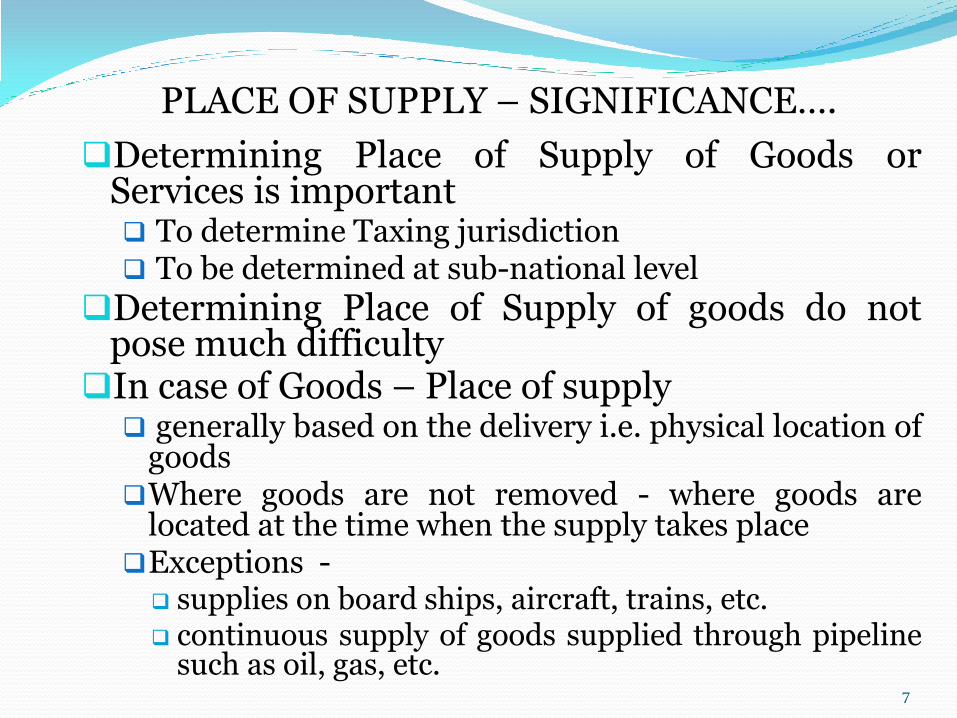

PLACE OF SUPPLY – SIGNIFICANCE…. Determining Place of Supply of Goods or

Services is important To determine Taxing jurisdiction To be determined at sub-national level

Determining Place of Supply of goods do not pose much difficulty

In case of Goods – Place of supply generally based on the delivery i.e. physical location of

goods Where goods are not removed - where goods are

located at the time when the supply takes place Exceptions - supplies on board ships, aircraft, trains, etc. continuous supply of goods supplied through pipeline

such as oil, gas, etc.

7

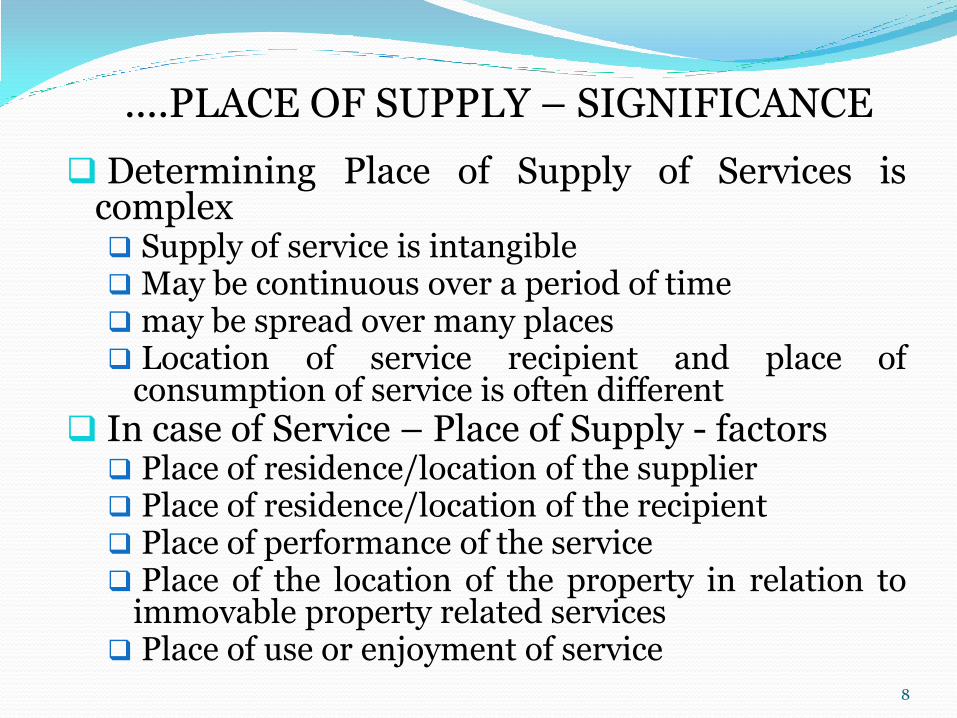

....PLACE OF SUPPLY – SIGNIFICANCE

Determining Place of Supply of Services is complex Supply of service is intangible May be continuous over a period of time may be spread over many places Location of service recipient and place of

consumption of service is often different In case of Service – Place of Supply - factors

Place of residence/location of the supplier Place of residence/location of the recipient Place of performance of the service Place of the location of the property in relation to

immovable property related services Place of use or enjoyment of service

8

PLACE OF SUPPLY RULES

9

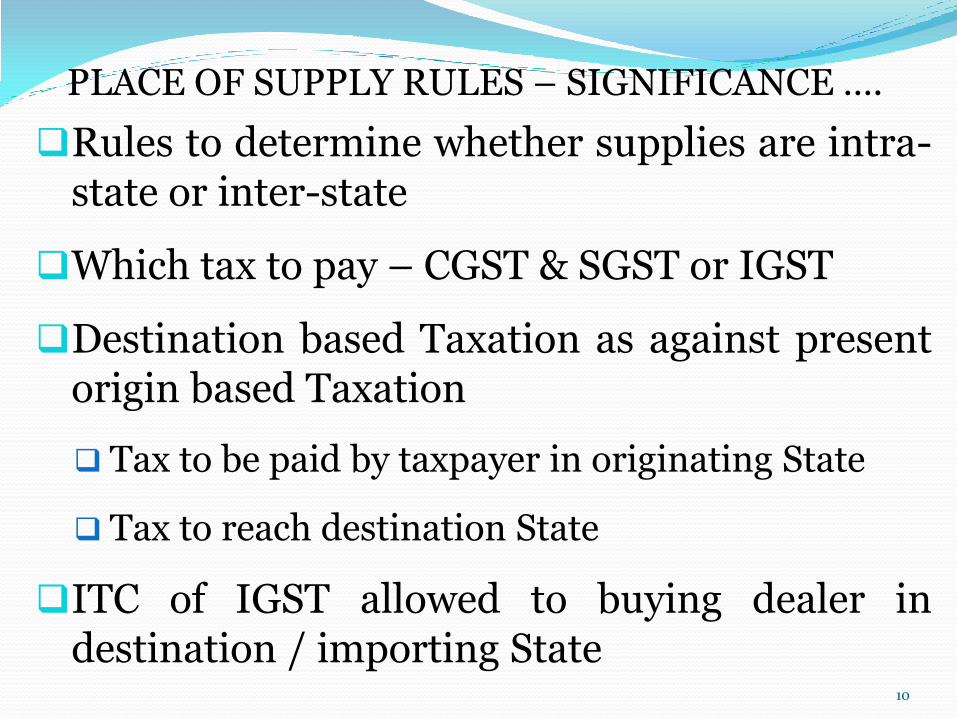

Rules to determine whether supplies are intra-state or inter-state

Which tax to pay – CGST & SGST or IGST

Destination based Taxation as against present origin based Taxation

Tax to be paid by taxpayer in originating State

Tax to reach destination State

ITC of IGST allowed to buying dealer in destination / importing State

PLACE OF SUPPLY RULES – SIGNIFICANCE ….

10

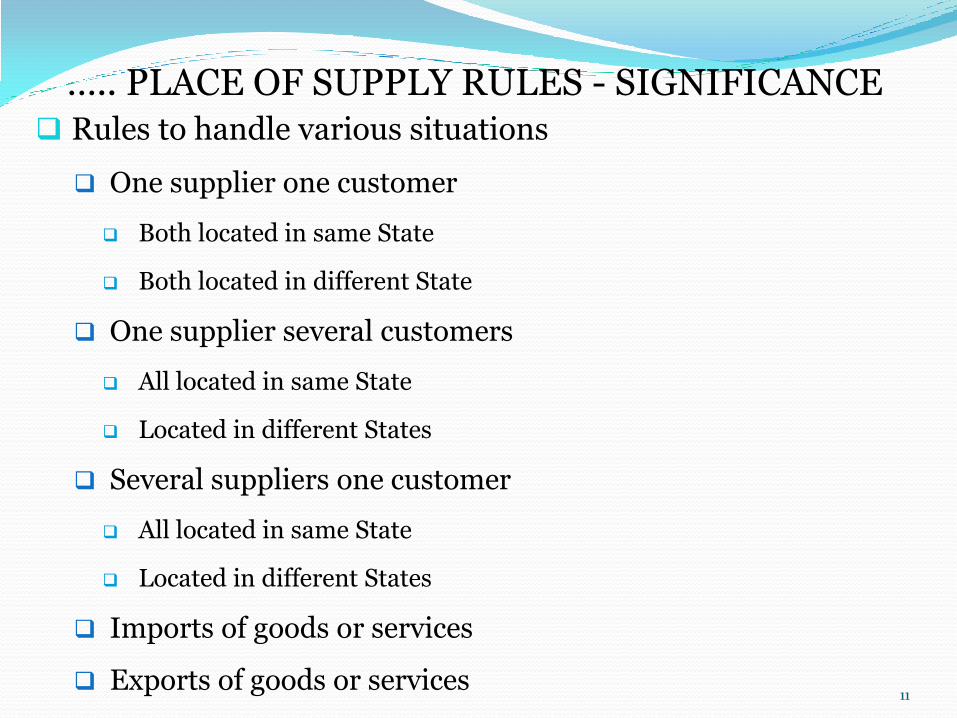

Rules to handle various situations

One supplier one customer

Both located in same State

Both located in different State

One supplier several customers

All located in same State

Located in different States

Several suppliers one customer

All located in same State

Located in different States

Imports of goods or services

Exports of goods or services

….. PLACE OF SUPPLY RULES - SIGNIFICANCE

11

PRESENT RULES FOR GOODS

12

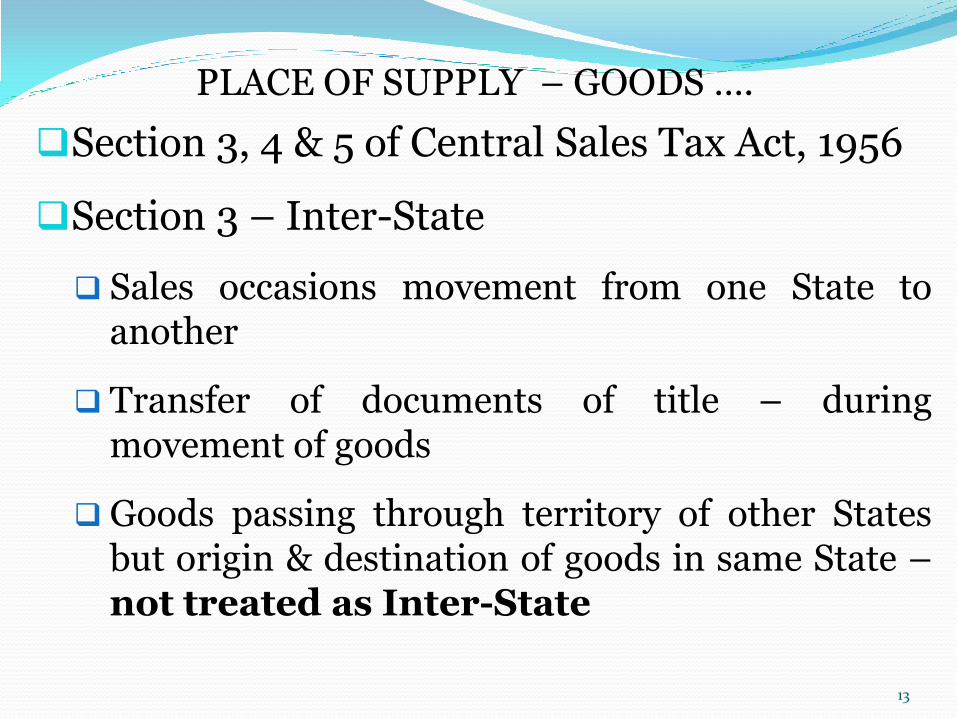

Section 3, 4 & 5 of Central Sales Tax Act, 1956

Section 3 – Inter-State

Sales occasions movement from one State to another

Transfer of documents of title – during movement of goods

Goods passing through territory of other States but origin & destination of goods in same State – not treated as Inter-State

PLACE OF SUPPLY – GOODS ….

13

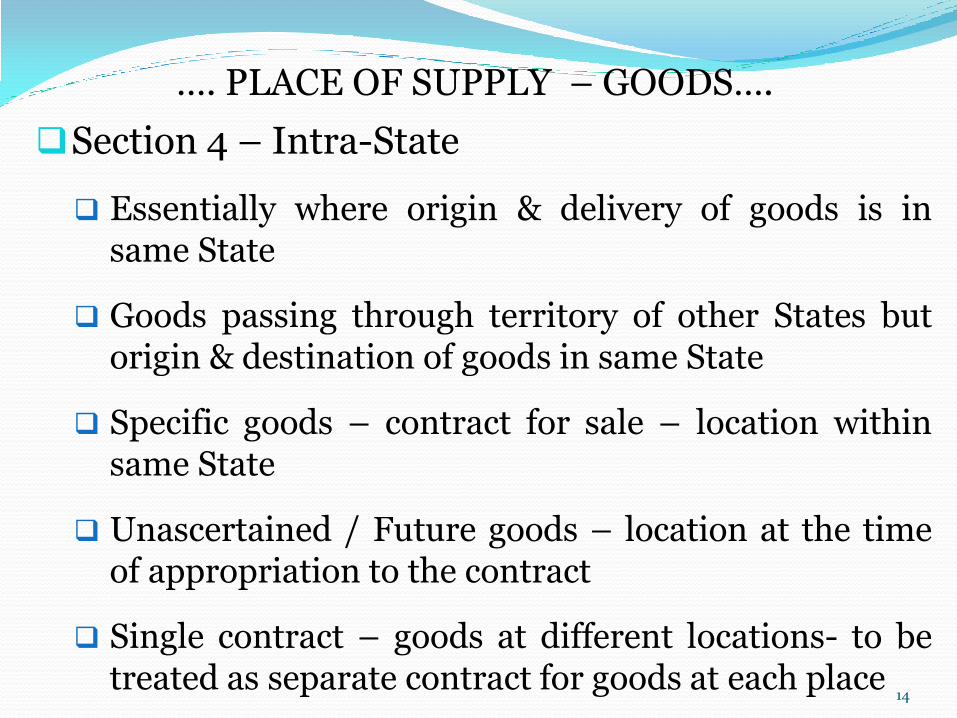

Section 4 – Intra-State

Essentially where origin & delivery of goods is in same State

Goods passing through territory of other States but origin & destination of goods in same State

Specific goods – contract for sale – location within same State

Unascertained / Future goods – location at the time of appropriation to the contract

Single contract – goods at different locations- to be treated as separate contract for goods at each place

…. PLACE OF SUPPLY – GOODS….

14

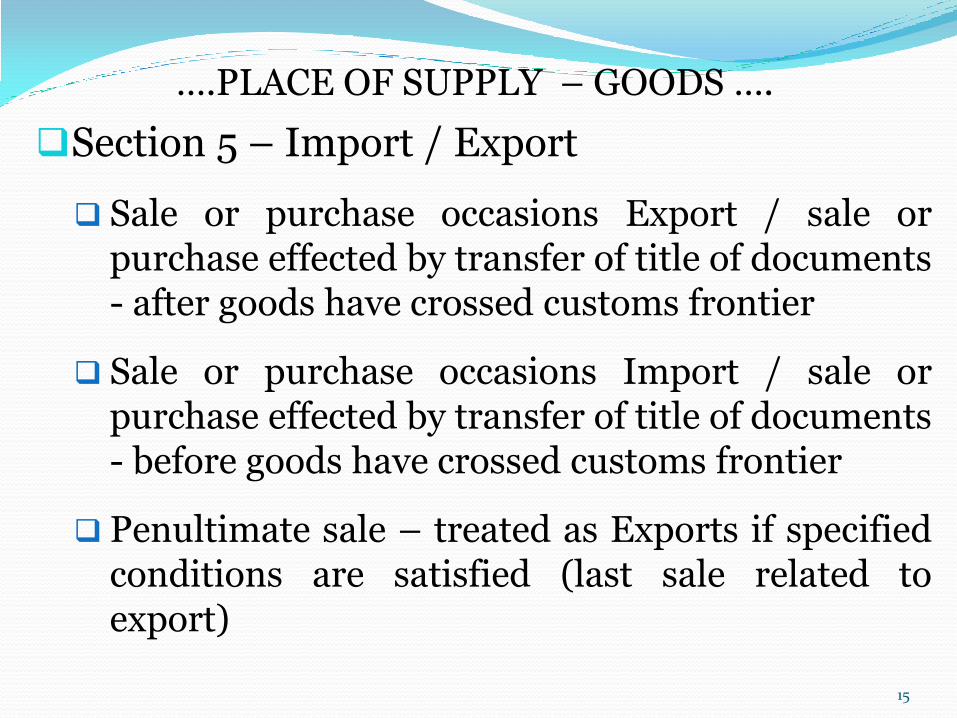

Section 5 – Import / Export

Sale or purchase occasions Export / sale or purchase effected by transfer of title of documents - after goods have crossed customs frontier

Sale or purchase occasions Import / sale or purchase effected by transfer of title of documents - before goods have crossed customs frontier

Penultimate sale – treated as Exports if specified conditions are satisfied (last sale related to export)

….PLACE OF SUPPLY – GOODS ….

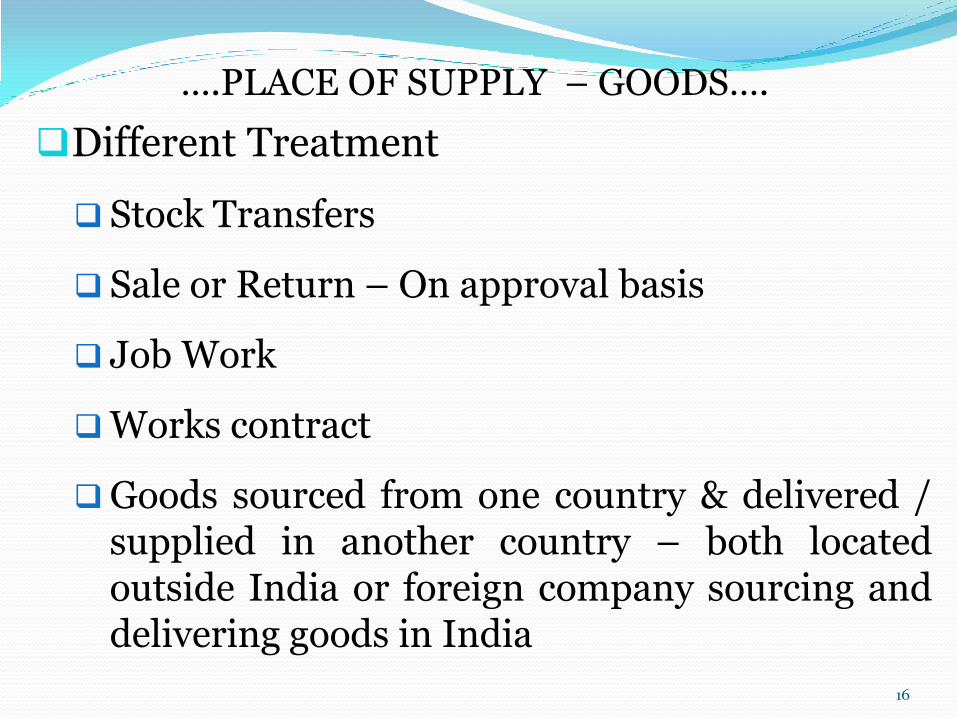

15

Different Treatment

Stock Transfers

Sale or Return – On approval basis

Job Work

Works contract

Goods sourced from one country & delivered / supplied in another country – both located outside India or foreign company sourcing and delivering goods in India

….PLACE OF SUPPLY – GOODS….

16

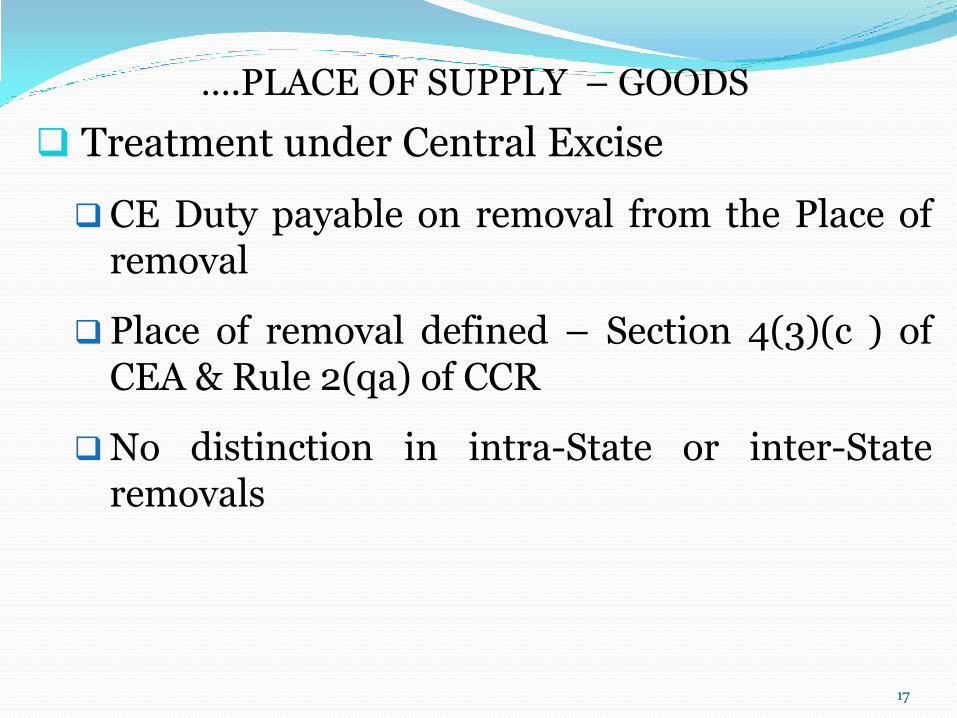

Treatment under Central Excise

CE Duty payable on removal from the Place of removal

Place of removal defined – Section 4(3)(c ) of CEA & Rule 2(qa) of CCR

No distinction in intra-State or inter-State removals

….PLACE OF SUPPLY – GOODS

17

PRESENT RULES FOR SERVICES

18

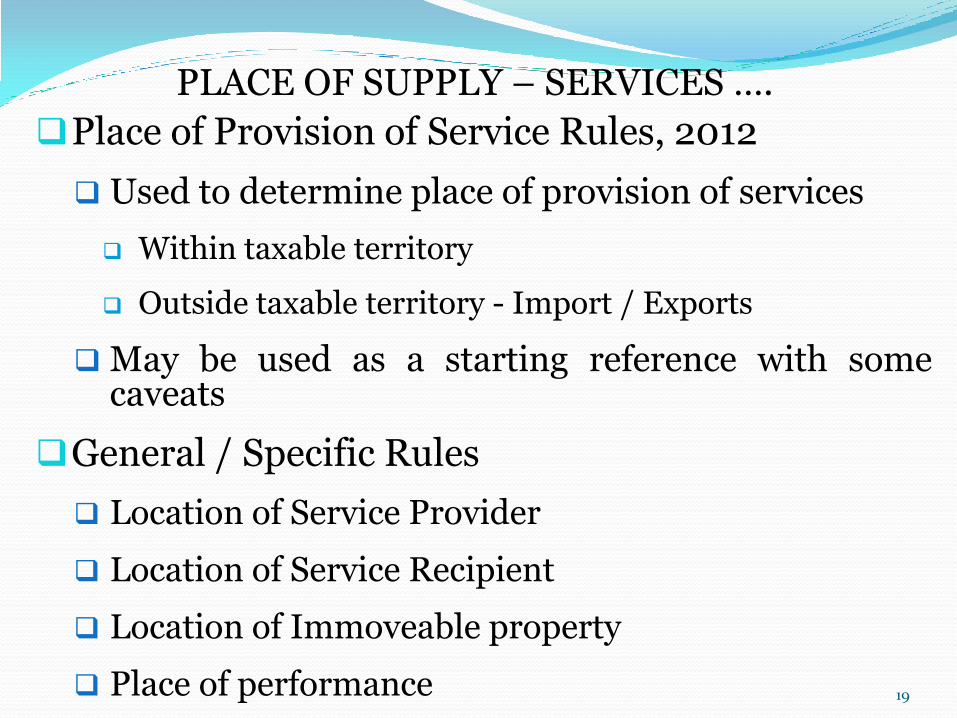

Place of Provision of Service Rules, 2012

Used to determine place of provision of services

Within taxable territory

Outside taxable territory - Import / Exports

May be used as a starting reference with some caveats

General / Specific Rules

Location of Service Provider

Location of Service Recipient

Location of Immoveable property

Place of performance

PLACE OF SUPPLY – SERVICES ….

19

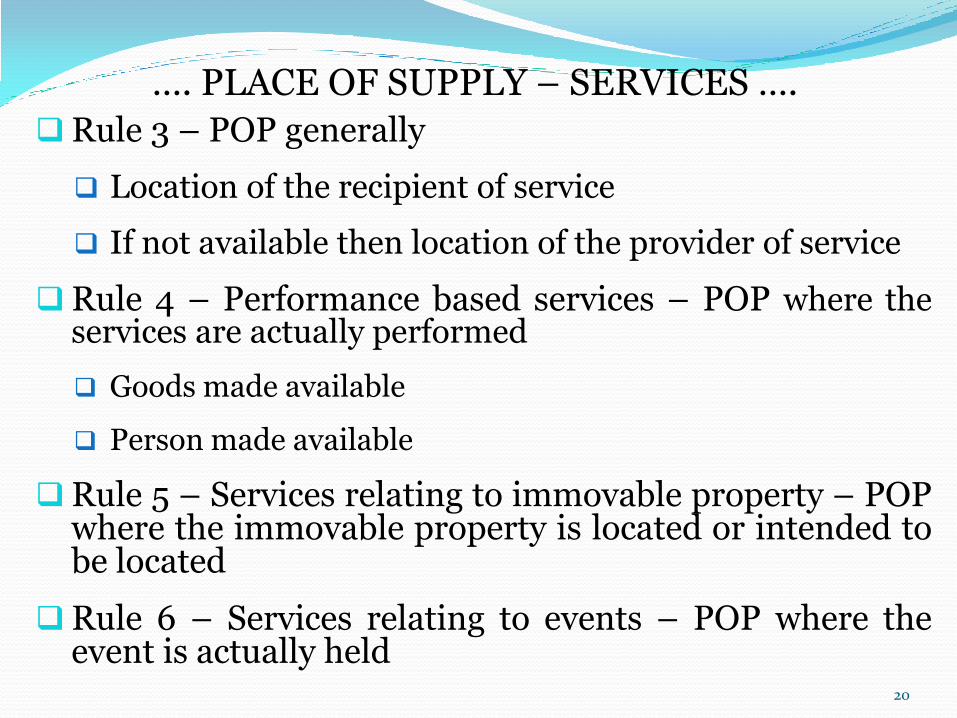

Rule 3 – POP generally

Location of the recipient of service

If not available then location of the provider of service

Rule 4 – Performance based services – POP where the services are actually performed

Goods made available

Person made available

Rule 5 – Services relating to immovable property – POP where the immovable property is located or intended to be located

Rule 6 – Services relating to events – POP where the event is actually held

…. PLACE OF SUPPLY – SERVICES ….

20

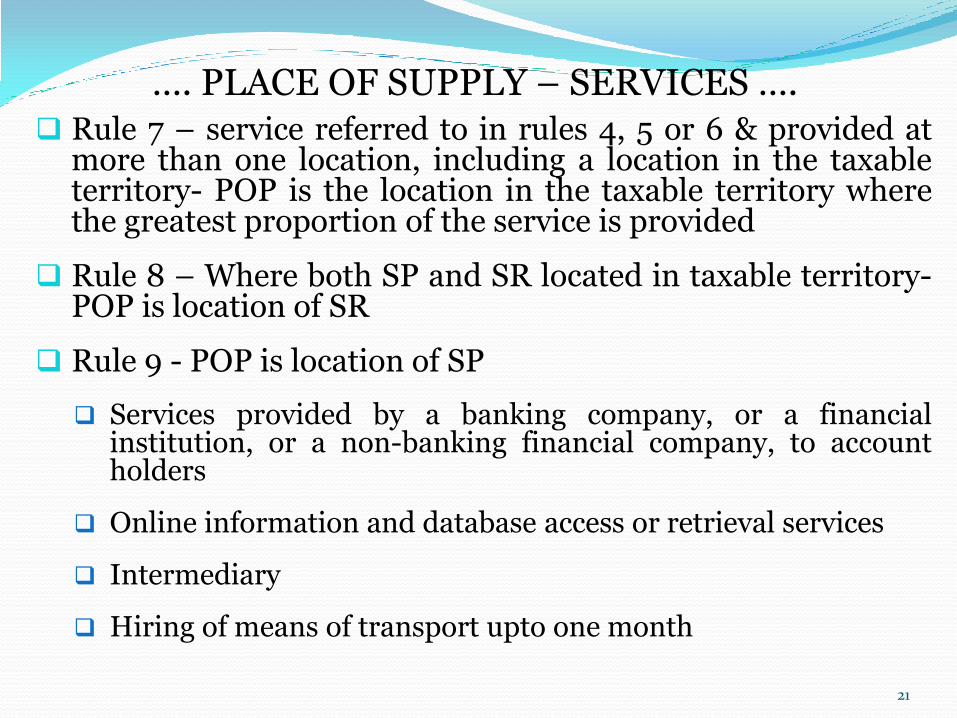

Rule 7 – service referred to in rules 4, 5 or 6 & provided at more than one location, including a location in the taxable territory- POP is the location in the taxable territory where the greatest proportion of the service is provided

Rule 8 – Where both SP and SR located in taxable territory- POP is location of SR

Rule 9 - POP is location of SP

Services provided by a banking company, or a financial institution, or a non-banking financial company, to account holders

Online information and database access or retrieval services

Intermediary

Hiring of means of transport upto one month

…. PLACE OF SUPPLY – SERVICES ….

21

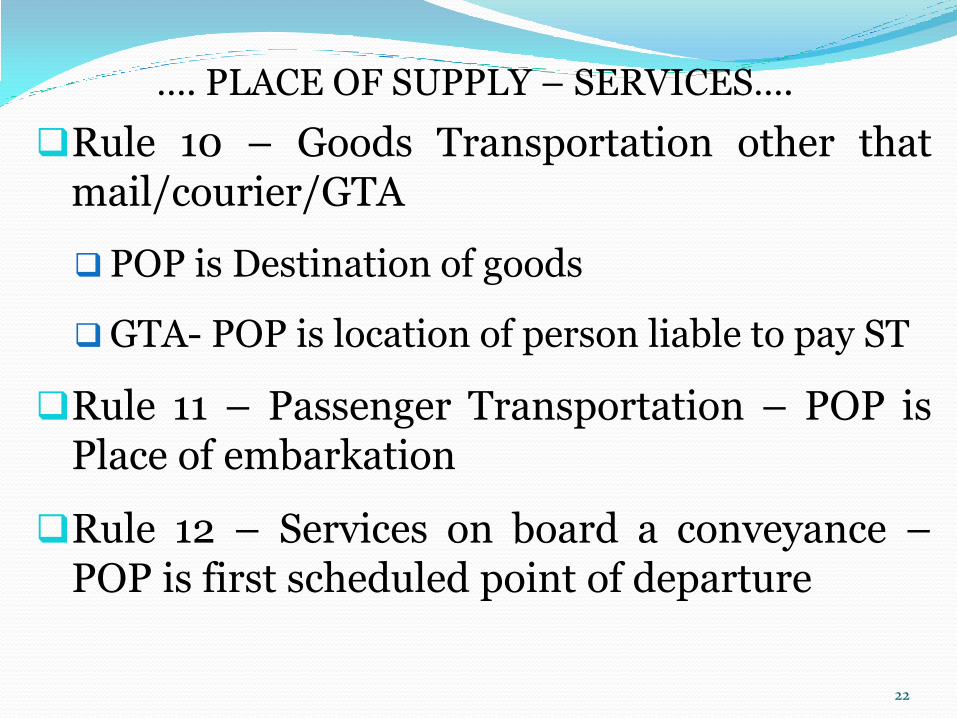

Rule 10 – Goods Transportation other that mail/courier/GTA

POP is Destination of goods

GTA- POP is location of person liable to pay ST

Rule 11 – Passenger Transportation – POP is Place of embarkation

Rule 12 – Services on board a conveyance – POP is first scheduled point of departure

…. PLACE OF SUPPLY – SERVICES….

22

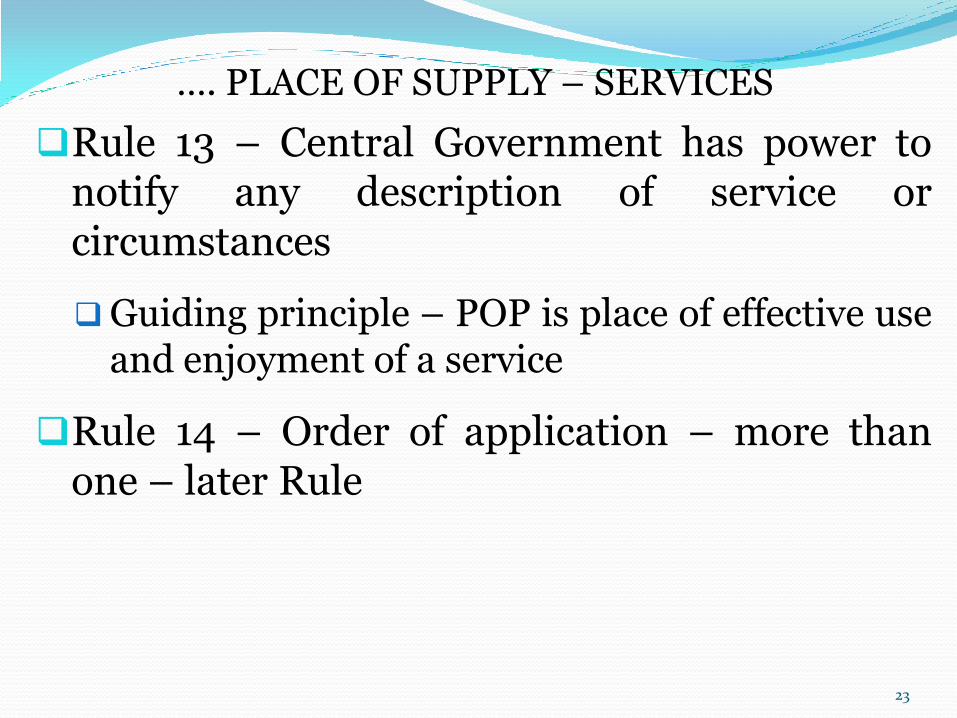

Rule 13 – Central Government has power to notify any description of service or circumstances

Guiding principle – POP is place of effective use and enjoyment of a service

Rule 14 – Order of application – more than one – later Rule

…. PLACE OF SUPPLY – SERVICES

23

GUIDING PRINCIPLES

24

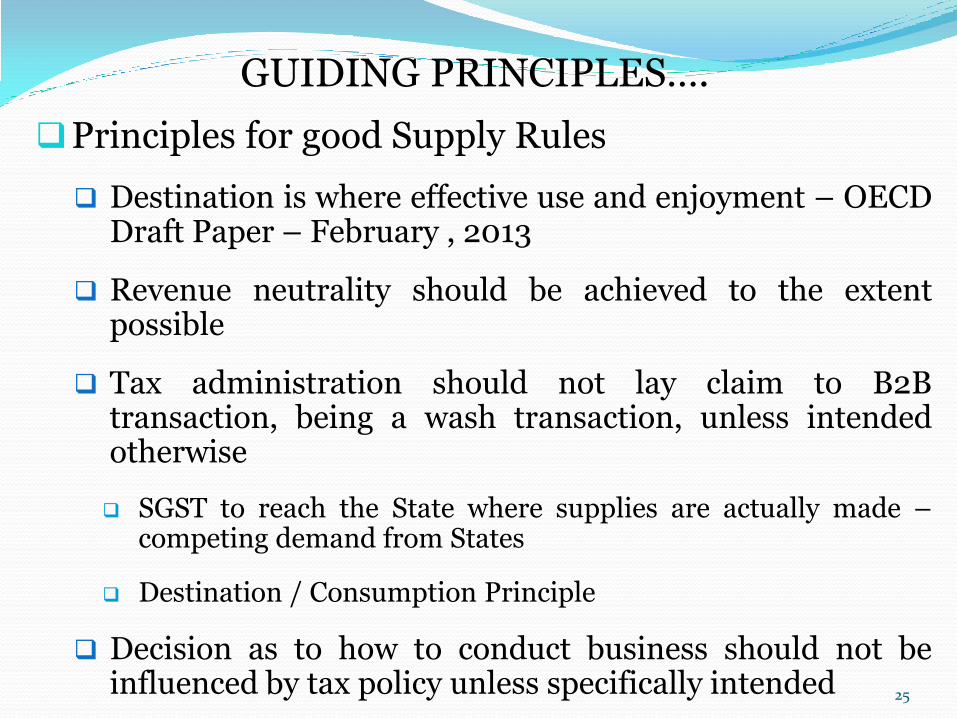

Principles for good Supply Rules

Destination is where effective use and enjoyment – OECD Draft Paper – February , 2013

Revenue neutrality should be achieved to the extent possible

Tax administration should not lay claim to B2B transaction, being a wash transaction, unless intended otherwise

SGST to reach the State where supplies are actually made – competing demand from States

Destination / Consumption Principle

Decision as to how to conduct business should not be influenced by tax policy unless specifically intended

GUIDING PRINCIPLES….

25

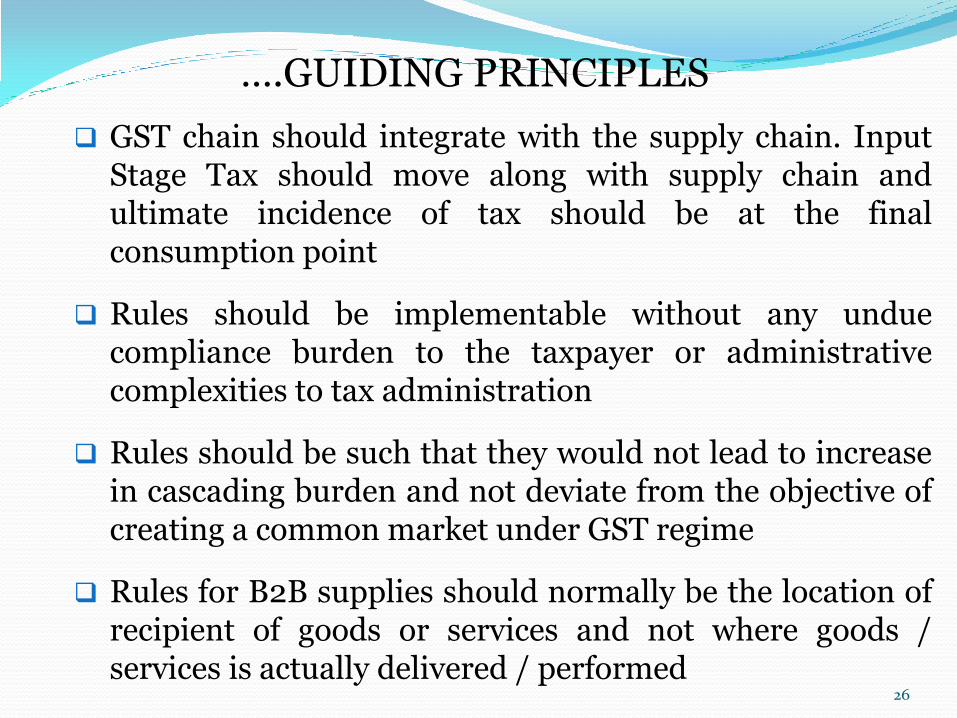

GST chain should integrate with the supply chain. Input Stage Tax should move along with supply chain and ultimate incidence of tax should be at the final consumption point

Rules should be implementable without any undue compliance burden to the taxpayer or administrative complexities to tax administration

Rules should be such that they would not lead to increase in cascading burden and not deviate from the objective of creating a common market under GST regime

Rules for B2B supplies should normally be the location of recipient of goods or services and not where goods / services is actually delivered / performed

….GUIDING PRINCIPLES

26

PLACE OF SUPPLY RULES – ISSUES??

27

How to determine inter-state?

Location of recipient vs Place of consumption

Rules for B2B & B2C supplies - certain services

Telecommunication

Banking & Financial Services

Works Contract

Sporting / recreational event

Repairs

Job work

PLACE OF SUPPLY RULES – ISSUES??

28