going public in canada - cassels brock… · · 2013-11-15tables for mergers and acquisitions and...

TRANSCRIPT

GOING PUBLIC IN CANADA

Cassels Brock & Blackwell LLP Going Public in Canada

CASSELS BROCK IN BRIEF

•Canadianlawfirmofmorethan200lawyersbasedinTorontoandVancouverfocusedonservingthetransaction,advocacyandadvisoryneedsofthecountry’smostdynamicbusinesssectors

•Emphasisoncorepracticeareasofmergersandacquisitions,securities,finance,corporateandcommerciallaw,litigation,taxation,intellectualpropertyandinformationtechnology,internationalbusinessandgovernmentrelations

•OneofthelargestbusinesslawpracticesinCanada,servingmultinational,nationalandmid-marketentitiesandwithaparticularstrengthintheminingandnaturalresourcessector

•ConsistentlyrankedatornearthetopofBloomberg,ThomsonFinancialandMergermarketdealsleaguetablesformergersandacquisitionsandequityofferings

•CitedasmarketleadersbyChambers Global, ALM 500, Best Lawyers, Lexpert, Global Counselandothers

•RegularlyactondealshonouredattheCanadianDealmakers’GalaandforcounselrecognizedattheCanadianGeneralCounselAwards

GoingPublicinCanada:Overview 1InitialPublicOffering 3ReverseTake-Over 6QualifyingTransactionwitha CapitalPoolCompany(“CPC”) 9LifeAfterListing 10

TABLEOFCONTENTS

Cassels Brock & Blackwell LLPGoing Public in Canada 1

Thedecisiontobecomeareportingissuerandoffersecuritiestobetradedonapublicexchangeisamilestoneforacompanyofanysize.Therearemanyadvantagestogoingpublic,however,doingsobringsnewresponsibilitiesforwhichabusinessmustbeprepared.Managementisencouragedtocarefullyconsiderthefollowingandthendecidewhethertheyarepreparedtobecome,andoperateas,apubliccompany.

GOINGPUBLICINCANADA: OVERVIEW

Advantages

Whenaprivatecompanygoespublic,currentshareholdersbenefitfromthenewmarketfortheirsecurities.Increasedliquiditycanraisethevalueofthesharesandallowsexistingshareholdersanopportunitytoexitalloraportionoftheirpositionandrealizegains.Thecompanymayalsodiversifyitscapitalstructure;accesstopublicmarketsgivesthecompanymoreflexibilityinitscapitalstructureasequitycanbesoldforcashorissuedinsatisfactionofdebt.Goingpubliccanincreasebargainingpowerwhendealingwithpartiesoutsidethebusinessaspubliccompaniesareseenasmoresecurethanprivatecompanies;contractorsandsupplierswilldealmorereadilywithapubliccompany.Publiccompaniesarealsoregardedmorehighlybycapitalandlabourmarkets.Employeescanbeofferedstockoptionsaspartoftheircompensationpackage,allowingthecompanytoattractandretainbettertalentandcreatinganincentivetoworktowardacommongoal.

ISITINTHECOMPANY’SBESTINTERESTTOGOPUBLIC?

Other considerations

Therearenumberofconsequencestobecomingapubliccompanythatmustbecarefullyconsidered.Tostart,thecompany’smanagementwillloseadegreeofcontroloverthebusiness.Managersandboardmembersareaccountabletoabroaderrangeofshareholdersandmustbeabletojustifytheirdecisionstothem.Thismeansthatmaximizingshareholdervalueisapriority,creatingpressureforshort-termperformance.Acompanymustalsobepreparedfortherequirementsofincreasedtransparencyandtheheightenedlevelofscrutinyapubliccompanyreceives.Businessinformationthatwasformerlyprivate,suchasbusinessstrategy,financialperformanceandcompensationofseniorofficers,isrequiredtoberevealedtothepublic,includingtocompetitors.Additionally,materialcontractsarerequiredtobemadeavailablepublicly,subjecttocertainexceptions.Thecontinuousdisclosureobligationscanbeonerousandcostly,andmanyjudgmentcalls willrequiretheassistanceofoutsideprofessionals.

Theinitialcostofgoingpublicmustbejustifiable.Apublicofferingwillrequiretheretentionoflawyers,auditorsandinvestmentbankersaswellasothertechnicalconsultants.Further,administrationcoatsforprintingtheprospectus,“roadshows”andlistingfeescanbesubstantial.Goingpublicalsoexposesthecompanyanditsdirectorstopotentialliability.Comparedtoprivateshareholders,publicshareholderswilllikelytakeamoreactiveinterestinthebusinessandmaybemorelikelytosue.Thisriskissomewhatmitigatedbytheavailabilityofdirectorinsurance,however,itonlycoverslimitedsituations.Goingpublicalsoincreasestheriskofatake-overbid.

Cassels Brock & Blackwell LLP Going Public in Canada2

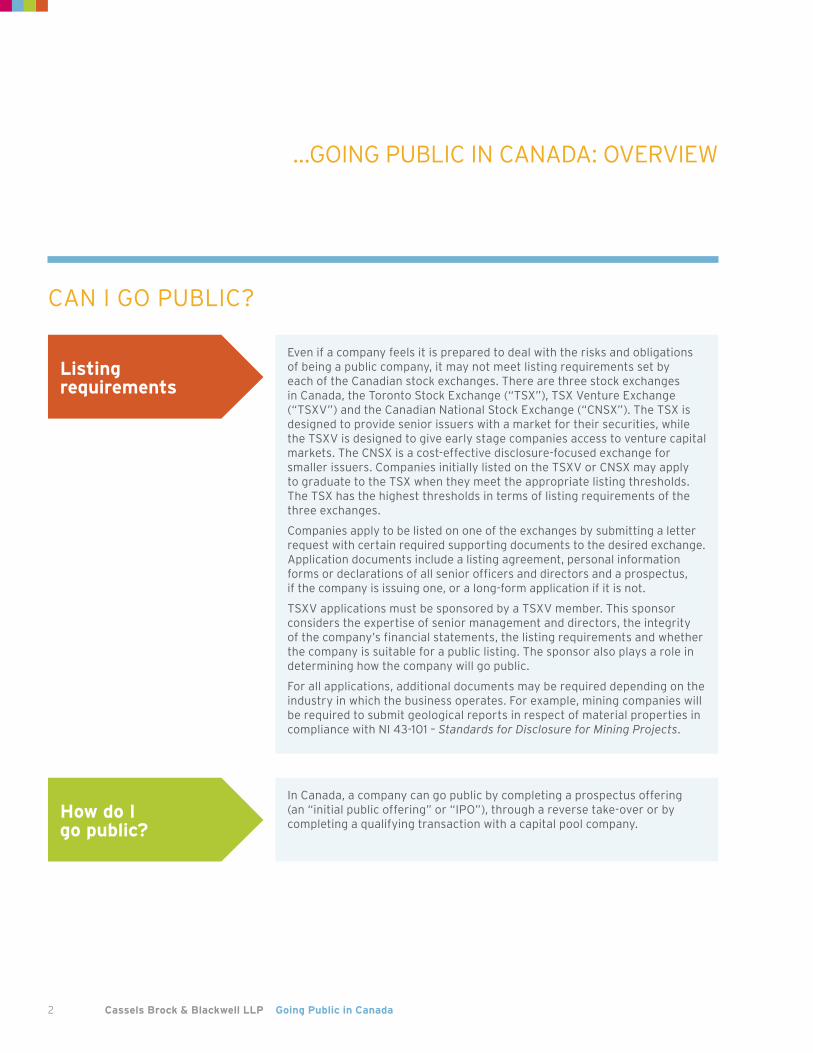

Listing requirements

Evenifacompanyfeelsitispreparedtodealwiththerisksandobligationsofbeingapubliccompany,itmaynotmeetlistingrequirementssetbyeachoftheCanadianstockexchanges.TherearethreestockexchangesinCanada,theTorontoStockExchange(“TSX”),TSXVentureExchange(“TSXV”)andtheCanadianNationalStockExchange(“CNSX”).TheTSXisdesignedtoprovideseniorissuerswithamarketfortheirsecurities,whiletheTSXVisdesignedtogiveearlystagecompaniesaccesstoventurecapitalmarkets.TheCNSXisacost-effectivedisclosure-focusedexchangeforsmallerissuers.CompaniesinitiallylistedontheTSXVorCNSXmayapply tograduatetotheTSXwhentheymeettheappropriatelistingthresholds.TheTSXhasthehighestthresholdsintermsoflistingrequirementsofthethreeexchanges.

Companiesapplytobelistedononeoftheexchangesbysubmittingaletterrequestwithcertainrequiredsupportingdocumentstothedesiredexchange.Applicationdocumentsincludealistingagreement,personalinformationformsordeclarationsofallseniorofficersanddirectorsandaprospectus, ifthecompanyisissuingone,oralong-formapplicationifitisnot.

TSXVapplicationsmustbesponsoredbyaTSXVmember.Thissponsorconsiderstheexpertiseofseniormanagementanddirectors,theintegrityofthecompany’sfinancialstatements,thelistingrequirementsandwhetherthecompanyissuitableforapubliclisting.Thesponsoralsoplaysaroleindetermininghowthecompanywillgopublic.

Forallapplications,additionaldocumentsmayberequireddependingontheindustryinwhichthebusinessoperates.Forexample,miningcompanieswillberequiredtosubmitgeologicalreportsinrespectofmaterialpropertiesincompliancewithNI43-101–Standards for Disclosure for Mining Projects.

…GOINGPUBLICINCANADA:OVERVIEW

How do I go public?

InCanada,acompanycangopublicbycompletingaprospectusoffering(an“initialpublicoffering”or“IPO”),throughareversetake-overorbycompletingaqualifyingtransactionwithacapitalpoolcompany.

CANIGOPUBLIC?

Cassels Brock & Blackwell LLPGoing Public in Canada 3

Aninitialpublicofferingisthemostconventionalwaythatprivatecompaniesgopublic.AnIPOrequiresthepreparationofaprospectus,whichprovidesinvestorswiththeinformationneededtomakeaneducatedinvestmentdecision.Thelevelofdisclosureneededfortheprospectusisfull,trueandplaindisclosure,thehigheststandardinsecuritieslaw.Asaresult,creatingaprospectusisalonganddetailedprocessthatrequirestheco-operationofmanagement,securitieslawyers,externalauditors,investmentbankers,technicalconsultantsandinvestorrelationsprofessionals.

Apreliminaryprospectusispubliclyfiledwitheachofthesecuritiescommissionsoftheprovinceswherethesecuritieswillbeofferedandwiththedesiredexchange.Thepreliminaryprospectusisreviewedbytheregulatoryauthoritiesandcommentsaresenttothecompanyanditslawyerstoadviseofdeficienciesandissues,ifany.Onceallcommentshavebeensatisfactorilyaddressedandsettled,afinalprospectusisfiledandafinalreceiptisgiven.Thesecuritiesarethensold,theofferingisclosedandthesecuritiesarelistedontheapplicableexchange.

INITIALPUBLIC OFFERING

Will my IPO be successful?

Fortheretobeapublicofferingofsecurities,thecompanymustfirstfindunderwriterswhoareconfidentthesecuritieswillsell.Underwriterswillconsiderthecompany’spotentialforgrowthandwhetherthefundsraisedcanbeusedtoincreasethevalueofthecompany.Thecompany’spastearningsandfutureprospects,aswellastheabilitiesandpreviousexperienceofthemanagementteamandboardofdirectorswillalsobeconsidered.Apubliccompanyneedsamanagementteamandboardofdirectorswithexperienceoperatingpubliccompanies.

Why do an IPO?

AnIPOallowsforawidedistributionofsecurities.Fromamarketingperspective,thecompanyisgivenmorepublicityasmorepeoplebecomeawareoftheoffering.Unlikeareversetake-over,anIPOdoesnotinvolvedealingwithanothercompanythatmayhavepotentialliabilities,issuesorobligationsattachedtoitthatwouldbeinheritedorassumedbytheentitythatcontinuesforwardfollowingthereversetake-over.

What financial statements are required?

Generally,boththepreliminaryandfinalprospectusmustinclude:

» Astatementofcomprehensiveincome,astatementofchangesinequityandastatementofchangesincashflowforeachofthethreemostrecentlycompletedfinancialyears;and

» Astatementoffinancialpositionforeachofthetwomostrecentlycompletedfinancialyears.

Therearespecialrulesforquarterlyreportsandpossibleexceptionstotheaboverequirementsincertain,veryspecificsituations.Acompanypreparingtogopublicalsoneedstobeawarethatadditionalstatementsarerequiredifa“significantacquisition”hasbeencompletedinthemostrecentlycompletedfinancialyear(orthecompanyproposestocompleteone).Allannualfinancialstatementsincludedinaprospectusmustbeaudited.AuditsarerequiredtobepreparedinaccordancewithInternationalFinancialReportingStandards(IFRS).

Cassels Brock & Blackwell LLP Going Public in Canada4

…INITIALPUBLICOFFERING

TIMELINE FOR AN IPO IN CANADA

TIMING TASK

Weeks1-2 » Managementconfirmsthecurrentboardofdirectorsandmanagementteamwillmeettheregulatoryrequirementsofapubliccompany

» Managementchoosesandengagesprofessionaladvisors:underwriters,securitieslawyers,externalauditorsandinvestorrelationsprofessionals

» Meetingwithauditorsandotheradvisorstodiscussfinancialsand,ifapplicable,technicalreports(suchasNI43-101compliantreportsformineralproperties)andcommencepreparationofsame

» Internaldocumentationorganizedtoensureduediligenceandpreliminaryprospectuspreparationarecompletedefficiently

» Underwritersbeginduediligencereview » Draftingofpreliminaryprospectuscommences

Weeks3-4 » Preparationofexchangelistingapplication » Attendtoexchangelistingrequirements(i.e.,application

forCUSIPnumber,distributionofpersonalinformationformstodirectorsandofficers)

» Legalandbusinessduediligencetocontinue » Commencepreparationofmarketingmaterials » Arrangeforfinancialprinters

Week5 » Oralduediligencesessionwiththecompany’smanagement,auditorsandlegalcounsel

» Finalizepreliminaryprospectus » Boardmeetingtoapprovepreliminaryprospectus

(includingfinancialstatementsandtechnicalreports) » Preliminaryprospectusandsupportingdocument,including

financialstatements,filedwiththeexchangeandapplicableprovincialsecuritiesregulators

Weeks6-9 » “Waitingperiod”begins:thecompanyandtheunderwritersarepermittedtosolicitinterestinsecuritiesbyforwardingcopiesofpreliminaryprospectustoprospectiveinvestors

» Underwriters’counseldistributesdraftunderwritingagreement

» Provincialsecuritiesregulatorsandtheexchangereviewpreliminaryprospectusandadviseapplicantissuerandprofessionaladvisorsofanydeficiencies

» Applicantissuer(withaidofsecuritiescounsel)toaddressdeficienciesandfilenecessaryamendmentstoprospectuswithsecuritiesregulators

» Underwritersbeginmarketingefforts » Listingapplicationfiledwiththeapplicableexchange

What are the steps and timing?

Cassels Brock & Blackwell LLPGoing Public in Canada 5

…INITIALPUBLICOFFERING

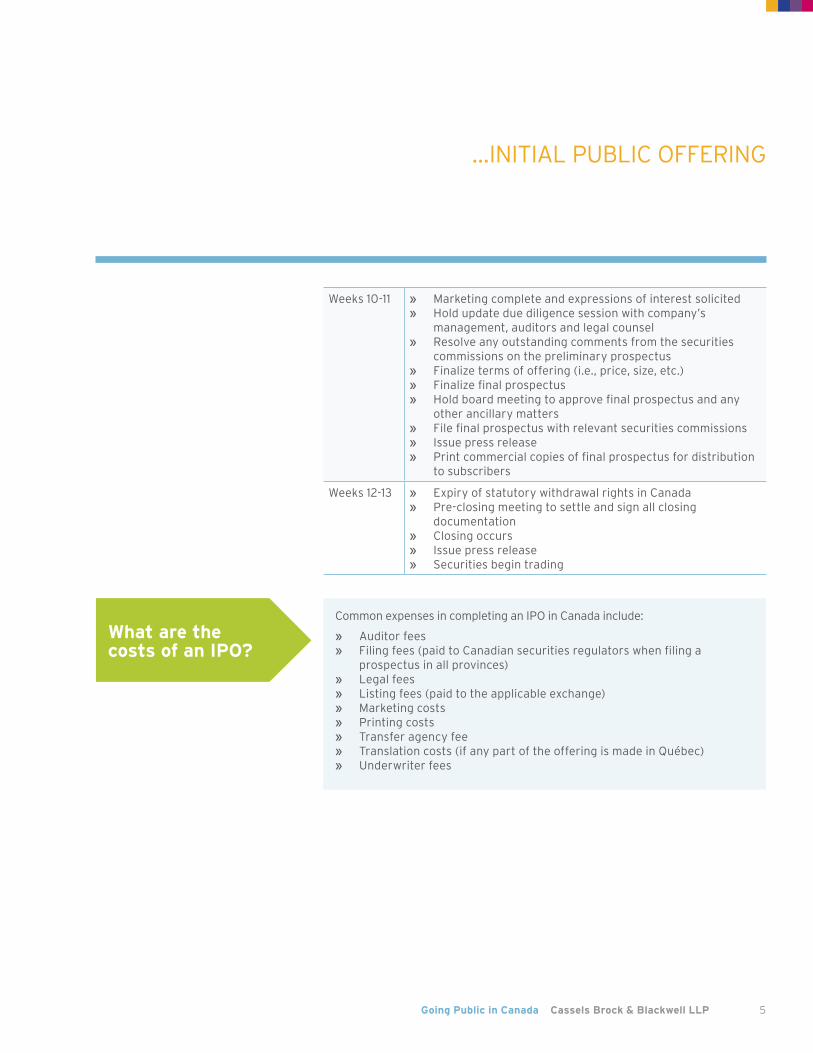

What are the costs of an IPO?

CommonexpensesincompletinganIPOinCanadainclude:

» Auditorfees » Filingfees(paidtoCanadiansecuritiesregulatorswhenfilinga

prospectusinallprovinces) » Legalfees » Listingfees(paidtotheapplicableexchange) » Marketingcosts » Printingcosts » Transferagencyfee » Translationcosts(ifanypartoftheofferingismadeinQuébec) » Underwriterfees

Weeks10-11 » Marketingcompleteandexpressionsofinterestsolicited » Holdupdateduediligencesessionwithcompany’s

management,auditorsandlegalcounsel » Resolveanyoutstandingcommentsfromthesecurities

commissionsonthepreliminaryprospectus » Finalizetermsofoffering(i.e.,price,size,etc.) » Finalizefinalprospectus » Holdboardmeetingtoapprovefinalprospectusandany

otherancillarymatters » Filefinalprospectuswithrelevantsecuritiescommissions » Issuepressrelease » Printcommercialcopiesoffinalprospectusfordistribution

tosubscribers

Weeks12-13 » ExpiryofstatutorywithdrawalrightsinCanada » Pre-closingmeetingtosettleandsignallclosing

documentation » Closingoccurs » Issuepressrelease » Securitiesbegintrading

Cassels Brock & Blackwell LLP Going Public in Canada6

Anotherwayforaprivatecompanytobecomeapubliccompanyisforittobeacquiredbyanexistingpubliccompanylistedonanexchange,knownasa“reversetake-over”or“RTO”.AnRTOoccurswhenapubliclistedshellcompanyacquiresormergeswithaprivatecompany,andtheownersoftheprivatecompanybecomethemajorityownersofthepubliclylistedcompany.Theshellcompanywillnothaveanoperatingbusinessandwilltypicallyhavefew,ifany,assets.Theacquisitionoftheprivatecompanymaybeachievedthroughanumberofmeans,includingbymergerofthetwocompanies,assetacquisitionofshareacquisition.ThestructureoftheRTOwilldependonanumberoffactorsincludingtaxconsiderations.TheAcquisitiongenerallyrequiresthepreparationofmaterialsforameetingofshareholderstoapprovethesetransactionswhichcontainprospectusleveldisclosureonboththelistedcompanyandtheprivatecompany.

REVERSE TAKE-OVER

Why do a reverse take-over?

Thebenefitofpursuingareversetake-overisthatthepublicparenthasapre-existingshareholderbasethatwillsatisfytheexchange’spublicfloatrequirement.Thereforeitmaynotbenecessarytoattractasmanynewinvestorsorhireateamofunderwriterstodistributestock.

AlthoughanIPOmayestablishastrongerretaildistribution,anRTOprovidesahistoricalretailbasetherebyreducingtherequirementtomarkettoretailinvestors.Incertaincircumstances,theshellcompanycanprovidethecompanywithcommercialadvantagessuchascash,qualifiedresidentCanadiandirectorsandacompatibleasset.

Cassels Brock & Blackwell LLPGoing Public in Canada 7

…REVERSE TAKE-OVER

Other considerations

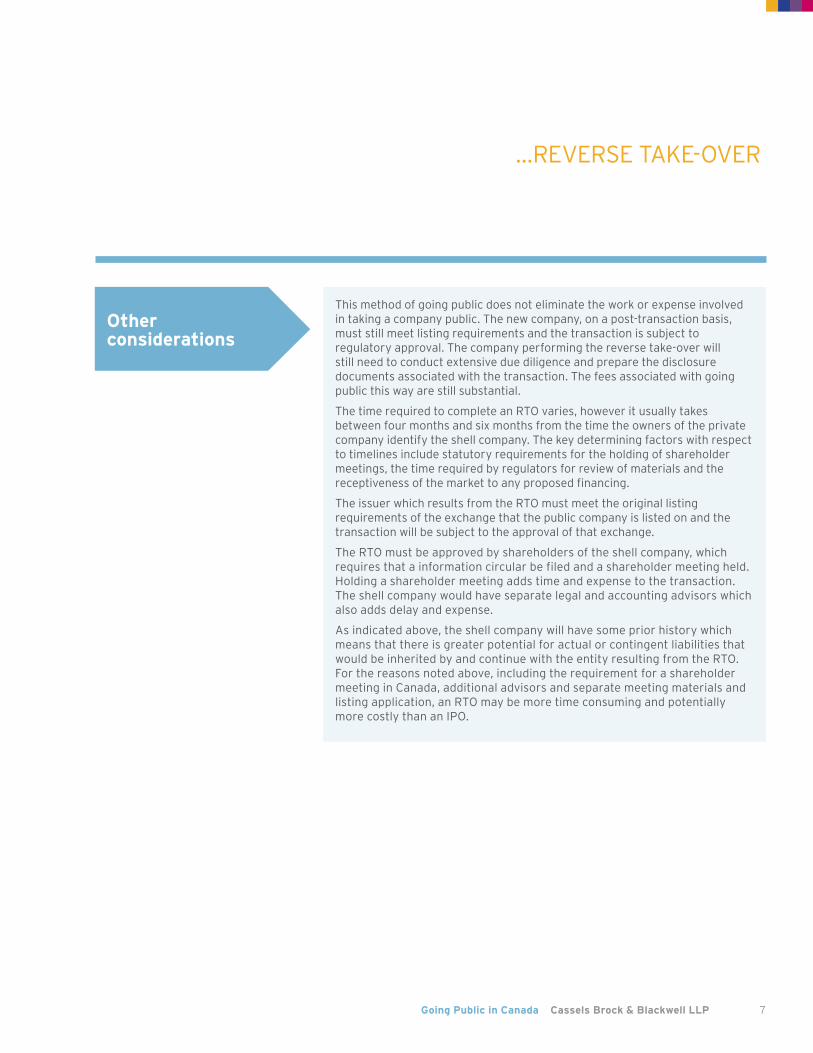

Thismethodofgoingpublicdoesnoteliminatetheworkorexpenseinvolvedintakingacompanypublic.Thenewcompany,onapost-transactionbasis,muststillmeetlistingrequirementsandthetransactionissubjecttoregulatoryapproval.Thecompanyperformingthereversetake-overwillstillneedtoconductextensiveduediligenceandpreparethedisclosuredocumentsassociatedwiththetransaction.Thefeesassociatedwithgoingpublicthiswayarestillsubstantial.

ThetimerequiredtocompleteanRTOvaries,howeveritusuallytakesbetweenfourmonthsandsixmonthsfromthetimetheownersoftheprivatecompanyidentifytheshellcompany.Thekeydeterminingfactorswithrespecttotimelinesincludestatutoryrequirementsfortheholdingofshareholdermeetings,thetimerequiredbyregulatorsforreviewofmaterialsandthereceptivenessofthemarkettoanyproposedfinancing.

TheissuerwhichresultsfromtheRTOmustmeettheoriginallistingrequirementsoftheexchangethatthepubliccompanyislistedonandthetransactionwillbesubjecttotheapprovalofthatexchange.

TheRTOmustbeapprovedbyshareholdersoftheshellcompany,whichrequiresthatainformationcircularbefiledandashareholdermeetingheld.Holdingashareholdermeetingaddstimeandexpensetothetransaction.Theshellcompanywouldhaveseparatelegalandaccountingadvisorswhichalsoaddsdelayandexpense.

Asindicatedabove,theshellcompanywillhavesomepriorhistorywhichmeansthatthereisgreaterpotentialforactualorcontingentliabilitiesthatwouldbeinheritedbyandcontinuewiththeentityresultingfromtheRTO.Forthereasonsnotedabove,includingtherequirementforashareholdermeetinginCanada,additionaladvisorsandseparatemeetingmaterialsandlistingapplication,anRTOmaybemoretimeconsumingandpotentiallymorecostlythananIPO.

Cassels Brock & Blackwell LLP Going Public in Canada8

What are the steps and timing?

…REVERSETAKE-OVERBID

TIMELINE FOR AN RTO IN CANADA

TIMING TASK

Weeks1-3 » Identifyandcommencenegotiationswithshellcompany » Partiestocommenceduediligenceprocessoneachother » Determinestockconsiderationratioorrange » Considerwhetherafinancingisrequiredinconnection

withtheRTO » Commencedraftingoftechnicalreports(suchas

NI43-101complainttechnicalreportsformineralproperties),ifapplicable

» Preparefinancialstatementsforinclusionininformationcircular

Weeks4-6 » Announcetransactionwithshellcompany » Commencepreparationofmeetingmaterials » Continuepreparationoffinancialstatementsandtechnical

reports » Legalandbusinessduediligencetocontinue » Selectmanagementandboardofdirectorsofresulting

issuer

Week7 » Deliverinitialdraftdocumentationtotheexchange (i.e.,informationcircular,financialstatements,technicalreports,listingapplication,personalinformationforms)

» Publishrecorddateforshareholdersmeeting (atleast7dayspriortotherecorddate)

Weeks8-11 » Recorddateforshareholdersmeeting (mustbeatleast30dayspriortomeetingdate)

» Obtainconditionallistingapprovaloftheapplicableexchange

» Printingandmailingofmeetingmaterialsforshareholdersmeeting(mustbeatleast21dayspriortothemeetingdate)

Weeks12-13 » Holdshareholdermeetingandobtainshareholderapproval » Filingofpost-shareholderapprovaldocumentswiththeTSX

(i.e.,scrutineer’sreport,legalopinion,balanceoffilingfees) » ClosingofRTO » Exchangeissuesfinalexchangebulletin(evidencingfinal

listingapproval) » Commonsharesoftheresultingissuercommencetrading

Cassels Brock & Blackwell LLPGoing Public in Canada 9

A“qualifyingtransaction”issimilartoareversetake-overexceptitisdoneusinga“CapitalPoolCompany”or“CPC”. ACPCisaparticularkindofTSXVlistedpublicshellcompanythatisverylimitedintermsofwhatitcandountilitcompletesa“QualifyingTransaction”byacquiringormergingwithanoperatingprivatecompanyoracquiringaqualifyingasset. TheCPCprogramisofferedbytheTSXVinanattempttoprovidesmallerbusinesseswithalternativeaccesstocapitalmarkets.ShareholdersoftheprivatecompanybecomeshareholdersoftheCPC.OncetheCPCcompletesthetransactionitssharescontinuetobetradedontheTSXV.

QUALIFYINGTRANSACTION WITHACAPITALPOOLCOMPANY

Why choose a CPC?

AprivatecompanymaychoosetodoaqualifyingtransactionwithaCPCtoallowtheprivatecompanytogopublicwhereitisnototherwisereadytohaveitssecuritiesverywidelyheld,orifthemarketisnotstrongenoughforasuccessfulIPO.BecauseaCPCisarecentlyincorporatedshellcompanywithlittlehistory,thereisatypicallymuchlowervolumeofduediligencethanforaregularreversetake-over.

TheCPCprogramprovidesanalternativeroutetoaccessingcapitalthatmayallowthecompanyfounderstoretainahigherownershipthanthroughatraditionalIPOorRTO.AqualifyingtransactionwithaCPCprovidesagoingpublicprocessthathasgreaterflexibility,morecertainty,andallowsformorecontrolbythecompaniesinvolved.Ingeneral,ittakesthesomeoftheriskoutofthegoingpublicprocess.

Other considerations

Aswiththeothermethodsforgoingpublic,astrongmanagementteamwithexperienceoperatingpubliccompaniesisneeded.Additionally,asuiteofprofessionaladvisorsincludingsecuritieslawyers,externalauditors,investmentbankersandtechnicalconsultantsarerequiredtobeinvolvedinthetransaction.Thecompanyalsoneedstoensurethatithasalong-termstrategyforgrowthasapubliccompanyandengagefinancialadvisorstoensurethatthecompany’smessageiscommunicatedtopotentialshareholdersandthatthereisinvestorsupportforthecompany’ssharesfollowingthegoingpublictransaction.

Thestepsinvolvedandtimetocompleteaqualifyingtransactionaresimilartothoseforareversetake-over.

Cassels Brock & Blackwell LLP Going Public in Canada10

LIFEAFTER LISTING

What happens once the company goes public?

Itisimportantforbusinessestogiveseriousconsiderationtotheobligationsassociatedwithbeingapubliccompany.Companiesarerequiredtoprovidebothperiodicandtimelydisclosureandthecontinuousdisclosurerequirementscanbeonerousandcostly.Periodicdisclosuremeansthattherewillberegularreportingoffinancialstatements,includingauditor’sreports,management’sdiscussionandanalysis,annualmeetingmaterials,businessacquisitionreportsfor“significantacquisitions”,technicalreports(ifapplicable)andanannualinformationform(whichisoptionalifthecompanyislistedontheTSXV).Theseitemsrequiresignificantresourcestoprepare,reviewandfile.Thetimelydisclosureregulationsmayalsobeonerous,ascompaniesarerequiredtoreportmaterialchangesbypressreleaseimmediatelyandtofileamaterialchangereportwithin10daysofthematerialchange.Decidingwhatconstitutesamaterialchangerequirescarefulconsiderationbytheboardofdirectorsandoftentheassistanceofanexperiencedsecuritieslawyer.Theconsequencesoffailingtodiscloseamaterialchangecanbesevere.

Onebenefittothecontinuousdisclosureregimeisthereducedcostandincreasedspeedwithwhichsubsequentprospectusofferingscanoccur. Ifacompanyisup-to-datewithitsfilingsitmayqualifytousetheshort-formprospectusregime.Theshort-formprospectusrulesallowacompanytoincorporatedocumentsbyreferenceandisamuchfasterprospectusprocessthanforalong-formprospectus.

Cassels Brock & Blackwell LLPGoing Public in Canada 11

Corporate governance requirements

Thereareimportantcorporategovernancematterstoconsiderwhengoingpublic,includingensuringthatthecompany’sboardandmanagementarecomprisedinaccordancewithCanadiangovernancestandardsandthatresidencyrequirementsfordirectorsaremet.

TheTSXrequiresaminimumoftwoindependentdirectorsinordertomeetminimumlistingrequirements.Threeindependentdirectorswhopossessknowledgeandunderstandingoffinancialmatters,arenecessaryinordertohaveaproperlyconstitutedauditcommittee.

Tobeconsidered“independent”,adirector:

» Mustnotcurrentlybeanexecutiveofferoremployeeoftheissuer (orhavefulfilledsucharoleinthelastthreeyears)

» Mustnotreceivecompensationfromtheissuerotherthanpaymentforactingasamemberoftheboardandhavenootherdirectorindirectmaterialrelationshipwiththeissuer

Managementandboardsarealsorequiredtobefamiliarwithapubliccompanystructureandhaveexperienceintheissuer’sbusiness/industry.

Residencyrequirementsvaryfromprovincetoprovince.Forexample,AlbertaandOntariorequirethatresidentCanadiandirectorscompriseatleast25%ofthetotalnumberofdirectorswhiletherearenocurrentCanadianresidencyrequirementsfordirectorsofcorporationsinBritishColumbiaandQuebec.BoardsofdirectorsofcompaniesexistingundertheCanada Business Corporations Actarealsorequiredtobecomprisedofatleast25%Canadianresidentdirectors.

…LIFEAFTERLISTING

Cassels Brock & Blackwell LLP

Suite 2100, Scotia Plaza Suite 2200, HSBC Building40 King Street West 885 West Georgia StreetToronto, ON Canada M5H 3C2 Vancouver, BC Canada V6C 3E8

Tel: 416 869 5300 Tel: 604 691 6100Fax: 416 360 8877 Fax: 604 691 6120

© 2011–2013 CASSELS BROCK & BLACKWELL LLP. ALL RIGHTS RESERVED.

This document and the information in it is for illustration only and does not constitute legal advice. The information is subject to changes in the law and the interpretation thereof. This document is not a substitute for legal or other professional advice. Users should consult legal counsel for advice regarding the matters discussed herein.