going global - digital riverinfo.digitalriver.com/rs/digitalriver/images/digitalriver_go...

TRANSCRIPT

Sponsored by

GOING GLOBAL

HOWARD WESTSR. DIRECTOR GLOBAL STRATEGIES

2

• Strategic decision maker with a background in global supply chain automation.

• Collaborates with Branded Manufactures to define strategic goals for Global Online Solutions.

• Over 15 years of experience implementing direct to consumer online solutions for some of the world’s most recognized brands.

3

GLOBAL ECOMMERCE MARKET AND TRENDS

STRATEGIES FOR EXPANDING YOUR BUSINESS GLOBALLY

• Market Analysis

• Mobile and Social Trends related to eCommerce

• How do companies “Go Global” online.

• Beware of the Operational Hurdles

• Marketplace strategies

4

GLOBAL INTERNET TRAFFIC BY REGION

$383b $1053b

$1252b $2357b

Source: Cysco Visual Networking Index Forecast, 2011-2016

Asia Pacific40.6%

Western Europe 22.4%

North America20.0%

Latin America7.7%

Central & Eastern

Europe 5.6%

Middle East & Africa 3.6%

5

DOES THIS TRANSLATE INTO ONLINE BUYERS?

6

52%

57%

64%

33%

64%

34%

84%

62%

31%

57%

UnitedStates

UnitedKingdom

Germany Japan Brazil Russia China India SouthAfrica

Nigeria

Global Average(54%)

% who say the prefer to shop online

Source: A.T. Kearney, July 2014

7

ECOMMERCE SPENDING WORLDWIDE

Asia Pacific174%

Middle East & Africa90%

World Wide 88%

Latin America55%

$431b $660b

$312b $445b$49b $73b

$383b $1053b$27b $51b

$48b $75b

$1252b $2357b

North America53%

Western Europe43%

Central & Eastern Europe48%

Source: eMarketer, Jan 2014; A.T. Kearney

8

ECOMMERCE PURCHASES BY CATEGORY

Category Global Avg.UnitedStates

United Kingdom Germany Japan India Brazil Russia China

South Africa Nigeria

Electronics 77% 83% 84% 90% 53% 79% 86% 71% 96% 60% 65%

Fashion and Apparel 76% 87% 85% 88% 66% 84% 75% 64% 97% 47% 65%

Services 76% 80% 76% 77% 63% 82% 70% 63% 87% 79% 80%

Books 73% 82% 82% 80% 65% 70% 75% 52% 89% 64% 71%

Music & Games 64% 74% 75% 66% 64% 65% 62% 43% 69% 64% 57%

Tickets 63% 74% 69% 63% 43% 79% 65% 51% 71% 69% 47%

Home Appliances 59% 46% 65% 58% 41% 67% 70% 62% 83% 41% 52%

Beauty Products 57% 50% 56% 62% 48% 68% 59% 53% 85% 41% 45%

Home Furnishings 52% 56% 65% 66% 53% 59% 48% 43% 65% 34% 30%

Sports and Outdoor 51% 56% 53% 66% 36% 52% 49% 51% 78% 35% 35%

Toys, Kids, Babies 48% 48% 53% 49% 32% 61% 47% 44% 75% 38% 34%

Groceries 45% 26% 60% 36% 68% 52% 29% 31% 90% 31% 30%

Household Items 45% 36% 48% 40% 41% 60% 35% 36% 84% 31% 35%

>70% 45%-70% <45%

% of survey respondents that purchased from this category in the past 90 days.

9

ECOMMERCE SPENDING VS. TRAFFIC

Source: eMarketer, Jan 2014; A.T. Kearney

45%

28%

19%

3%

3%

2%

40%

20%

22%

8%

6%

4%

Asia Pacific

North America

Western Europe

Latin America

Central & Eastern Europe

Middle East & Africa

0% 10% 20% 30% 40% 50%

Traffic

Sales

10

11

WHERE DO I GO NEXT?

12

HOW DO I GET THERE?

14

GO TO MARKET – REVENUE VS DIFFICULTY

United States

Canada

GermanyUnited Kingdom

Australia

France

Netherlands

Italy

Sweden

China

South Korea

New Zealand IrelandSpain

Brazil

Russia

Japan2.8

Denmark

Belgium

Singapore

Finland

Hong Kong

Luxembourg

Austria

Taiwan

India

Poland

MalaysiaCzech Republic

Turkey

Chile

Mexico

Switzerland

Indonesia

Greece

ArgentinaSouth Africa

IsraelUnited Arab Emirates

PortugalHungary

Vietnam

Thailand

Bulgaria

Colombia

Saudi Arabia

PeruRomania

EgyptKenyaUkraine

Nigeria

Ease o

f Im

ple

menta

tion

Revenue Opportunity

15

STRATEGIES FOR EXPANDING YOUR BUSINESS GLOBALLY

• How do companies “Go Global” online.

• Beware of the Operational Hurdles

• Marketplace strategies

16

OFFSHORE VS. ONSHORE

Local EntityLocal BankingLocal Payment TypesTax Management

Cross-Border EntityInternational PaymentsForeign Tax Registration

Off-Shore WarehouseEnd User Typically Imports ProductsCustomer Must Pay Duties and Taxes Higher Customer Shipping CostsSlower Delivery Time

Local WarehouseProducts are ImportedImporter Pays Duties and TaxesProducts Shipped Domestically Delivery is Faster

OFFSHORE VS. ONSHORE

17

The Merchant of Record is the organization that is held financially liable by the acquiring bank (i.e., the financial institution that processes the customer's credit and/or debit card payments) for all full and partial returns to the customer's card as well as any chargebacks initiated by the customer.

The Seller of Record must be able to prove they have legal title of the product and is allowed to sell.

ISPs / Mailbox Providers

MERCHANT OF RECORD SELLER OF RECORD

Tax Collection & Remittance

Fraud Management &

Liability

Legal Entities

(in-country)

Security and Privacy

Banking Relationships

Compliance with all laws and regulations

UNDERSTANDING THE COMPLEXITIESOF COMMERCE GLOBALLY

18

INSTILLING KANDO THROUGH THE RIGHT EXPERIENCE

CRAWL / GOOD WALK / BETTER RUN / BEST

Cross-Border PaymentsInternational Credit CardPayPal

Off-Shore WarehouseCustomer is Importer of Record

LocalizationLanguageCurrency

LocalizationAddress Validation, Landed Costs of Duties & Taxes

LocalizationSite flow & Experience

LocalizationLanguageCurrency

Cross-Border PaymentsInternational Credit CardPayPal

Off-Shore WarehouseCustomer is Importer of Record

Local EntityLocal Credit CardsLocal Payment Types

Local WarehouseClient is Importer of Record

LocalizationLanguageCurrency

LocalizationSite flow & Experience

marketForceLocal Marketing expertise and services

HOW COMPANIES EXPAND GLOBALLY

CRAWL TO WALK

Fujisan JP

http://www.fujisan.co.jp/

Local Site, providing a

Japanese consumer with a

comfortable Japanese

experience.

19

Fujisan US

http://www.fujisan.com

Japanese site roughly

translated into English

Shipping from Japan to the

US.

FROM CRAWL TO WALK

CRAWL TO WALK

Rakutan JP

http://www.rakuten.co.jp/

Local Japanese Site

Japanese Specific marketing

20

Rakutan US

http://www.rakuten.com/

New US experience

Unique product marketing

Domestic Shipping

Complete US experience

RUNNING GLOBALLY

$1252b $2357b

84%

82%

60%

78%

81%

80%

100%

27%

48%

55%

33%

52%

44%

75%

26%

29%

38%

24%

35%

31%

58%

GLOBAL AVERAGE

ASIA PACIFIC

EUROPE

MID EAST/AFRICA

LATIN AMERICA

NORTH AMERICA

21

DEVICES USED FOR ONLINE SHOPPING

Source: Nielsen Global Survey of E-Commerce, Q1 2014

MOBILE DEVICE TABLETCOMPUTER

Branded manufacturers (manufacturers of branded products) are developing three sales channels that co-exist and each channel has its own unique strategy. They will continue to sell via traditional retailers and also on Rakutan or Amazon (marketplaces), but are increasingly adding emphasis to their direct-to-

consumer channel.

RETAIL

DIRECT-TO-CONSUMER

RAKUTAN-AMAZON

MULTIPLE SELLING CHANNELS CO-EXISTMULTIPLE SELLING CHANNELS CO-EXIST

GOING DIRECT VS. THROUGH A MARKETPLACE

23

Lower Price

HighService Level

LowService Level

Higher Price

Rakutan

Going Direct

JD.com

Tmall

Amazon

WORKING TOGETHER WITH MARKETPLACES

Forrester, February 2013 “The Marketing Case For A Branded Sales Channel ”

PwC research found that more than a third of consumers globally have purchased products directly from branded manufacturers. Forrester research reports that a third of consumers are interested in

buying directly from branded manufacturers for the reasons listed below:

Sources: PWC, Demystifying the online shopper 10 myths of multichannel retailing, January 2013:

UNIQUE SELECTION

Manufacturers are able to provide their full product range and increasingly value-added services or special SKUs

BRAND LOYALTY

Consumers want to buy direct

when they love the brand

WARRANTIES

Consumers believe they can

get better warranties and

guarantees from manufacturers

COUNTERFEIT PRODUCTS

Marketplaces often have knock-

off products mixed with

brands due to inventory co-

mingling

UNIQUE BUNDLES

Since manufacturers

control the assortment, they can offer unique

bundles and bundle pricing

AND/OR

KNOWLEDGE

Consumers believe manufacturers

know their products best and will provide better advice and support

WHY WILL COMSUMERS BUY FROM MANUFACTURES DIRECTLY INSTEAD OF RAKUTEN, AMAZON OR ALIBABA?

25

APPENDIX

26

MARKETING STRATEGIES

27

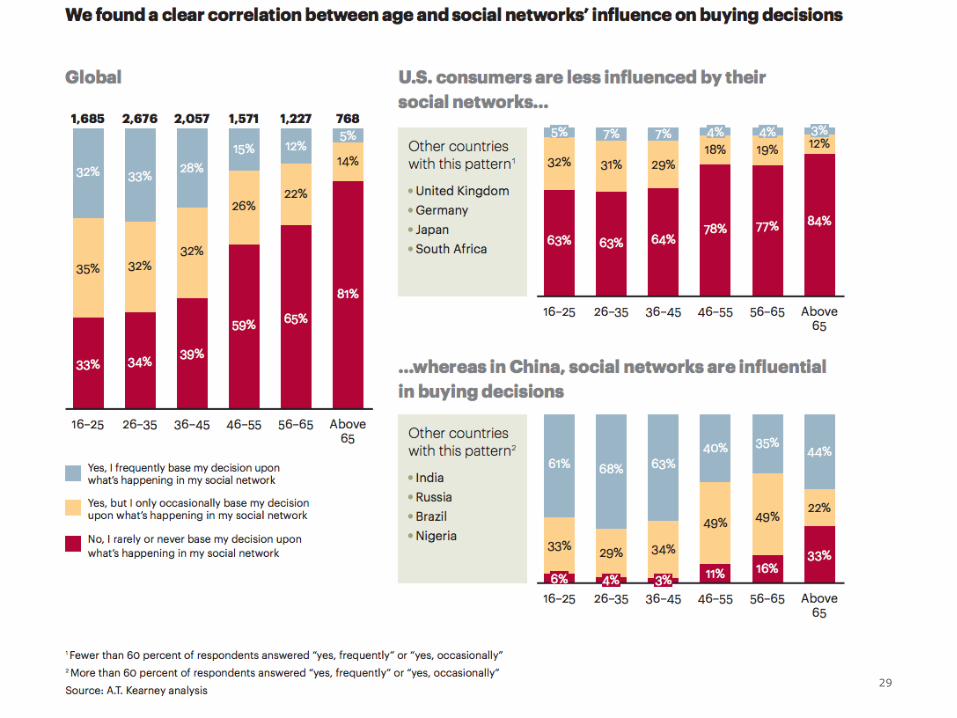

28

29

MARKET OVERVIEW

Online Activity

Total Population: 1,394 mln

Online Population: 670 mln

2014- 48% of Total Pop 2019- 60% of Total

Pop

Online buyers 365.3 mln

2014- 55% of online pop 2019- 72% of Total

Pop

Online Retail Revenue (excl travel sales)

2014- $439 bln 2019- RMB 1,088 bln

Market Trends & Insights

Top Category: Apparel. 43% growth

Motivation: Price (87%), Variety (76%),

Convenience (75%)

Frequency: 44% buy online weekly

Compliance: Vendor need to register local entity

and sales license for Online business

30

CHINA

$184

$149

$123

$117

$107

$85

$74

$67

$54

APPAREL

MEDIA

BEAUTY

FOOTWEAR

CE

IT & SOFTWARE

APPLIANCES

HOMEWARE

GROCERY

Online Sales by Category2014 Gross Revenue, USD Billions

MARKET OVERVIEW

Online Activity

Total Population: 1.3 bln

Online Population: 425 mln (32% of total pop)

Online Buyers: 63 mln (15% of online

population)

Online Retail Revenue (excl travel sales):

2016- $16 bln 2019- $ 30.9 bln

Online Retail via Mobile:

2016- $6.2 bln 2019- $19.1 bln

Market Trends & Insights

Business Model: Indian-owned entity must act

as ROR

Payment Methods: Low credit card penetration.

COD

Mobile is hot! Devices are primary access to

Internet. 81 mln smartphone sold in 2014

Logistics is next wave of investment.

31

INDIA

$10.1

$7.1

$5.1

$1.8

$1.7

$1.3

$0.4

$0.6

$3.1

CE

IT & SOFTWARE

APPAREL & FOOTWEAR

BEAUTY

MEDIA

HOMEWARE

APPLIANCES

GROCERY

OTHER

Online Sales by Category2019 Gross Revenue, USD Billions

MARKET OVERVIEW

Online Activity

Total Population:127 mln

Online population: 103 mln (81% of total pop)

Online Buyers: 73 mln (71% of online pop)

Online Retail Revenue (excl travel sales):

2014- $54 bln 2019- $86 bln

Market Trends & Insights

Leading Category: Apparel & Footwear. 43%

growth

Motivation: Price (87%), Variety (76%),

Convenience (75%)

Frequency: 44% buy online weekly

Compliance: Vendor need to register local entity

and sales license for Online business.

32

JAPAN

$9.1

$9.6

$10.1

$10.3

$10.4

$10.8

$15.2

$17.8

$22.4

IT & SOFTWARE

BEAUTY

OTHER

APPLIANCES

MEDIA

GROCERY

CE

HOMEWARE & FURNITURE

APPAREL & FOOTWEAR

Online Sales by Category2019 Gross Revenue, USD Billions

MARKET OVERVIEW

Online Activity

Total Population: 50 mln

Online Population: 42 mln (87% of total pop)

Online Buyers: 29 mln (70% of online pop)

Online Retail Revenue (excl travel sales)

2014- $21 bln 2019- $36 bln

Market Trends & Insights

Tech savvy with preference for luxury brands

Highest credit card penetration

Motivation: Avoid high imported product prices

Parcel forwarded used to avoid shipping charges

.

33

KOREA

$7.4

$6.2

$4.7

$4.4

$3.9

$2.8

$2.6

$2.1

APPAREL & FOOTWEAR

GROCERY

CE

IT & SOFTWARE

OTHER

BEAUTY

MEDIA

APPLIANCES

Online Sales by Category2019 Gross Revenue, USD Billions

MARKET OVERVIEW

Online Activity

Total Population: 23.4 mln (2013)

Online Population: 18.7 mln (2014, 80% of total

pop)

Online buyers 5.3 mln (30% of online pop, 2014)

Online Retail Revenue (excl travel sales): $33 bln

(2015)

Market Trends & Insights

125% mobile distribution. 25 mln 3G subscribers.

Growth mainly fuelled by m-commerce- 40% of

shoppers purchase from smartphones.

Omni channel- 30% of online stores in local

marketplaces have a physical store.

Shoppers very price sensitive.

34

TAIWAN

Online Sales by Category2014 Gross Revenue, USD Billions

$4.5

$3.5

$3.1

$0.8

$5.2

Apparel & Footwear

CE, IT & Software

Beauty

Media

Other