goethe business school chapter ix: exchange rates a.what is an exchange rate? b.purchasing power...

TRANSCRIPT

Goethe Business SchoolGoethe Business School

Chapter IX: Exchange ratesA. What is an exchange rate?

B. Purchasing power parity (long run)

C. Exchange rates in the short run

D. The organization of foreign exchange markets

E. Exchange rate crises

F. Interventions in foreign exchange markets

Goethe Business SchoolGoethe Business School

2

What is an “exchange rate”? The price of one currency in terms

of another (say dollars per euro) is called the exchange rate

Foreign exchange (forex) transactions are effected on specific markets for: spot transactions; forward transactions; futures transactions; options

Goethe Business SchoolGoethe Business School

3

Appreciation and depreciation

If you pay more € for forex, your currency € is said to “depreciate”; if you pay less, your currency “appreciates”

w=€/$Depreciation

w=€/$Appreciation

Goethe Business SchoolGoethe Business School

4

Why are exchange rates important? They affect the relative price of domestic

and foreign goods When a country’s currency appreciates,

the country’s goods become more expensive abroad, and foreign goods become cheaper

Will the exchange rate equate foreign and domestic prices?

Goethe Business SchoolGoethe Business School

5

The law of one price

Under market conditions, arbitrage will indeed equate prices in the different regions of the domestic economy

If there are no barriers to trade, this also applies to international trade

If the price level in country A is higher than in country B, the exchange rate should correct for this difference

Goethe Business SchoolGoethe Business School

6

The law of one price Identical goods should sell for the same price in

two separate markets when there are no transportation costs and no differential taxes applied in the two markets

Consider the following information about movie video tapes sold in the US and Mexican markets: Price of videos in US market (Pv) = $20

Price of videos in Mexican market (Pv) = p150

Spot exchange rate (p/$) = 10 p/$

Goethe Business SchoolGoethe Business School

7

The law of one price The dollar price of videos sold in Mexico can be

calculated by dividing the video price in pesos by the spot exchange rate

If the law of one price held, then the dollar price would have to be p150/10p/$ = $15 in Mexico to match the price in the US

Since the dollar price of the video is less than the dollar price in the US, the law of one price does not hold in this circumstance

If the law holds, we speak of “purchasing-power parity” (PPP)

Goethe Business SchoolGoethe Business School

8

The Big-Mac index (PPP ?)

Goethe Business SchoolGoethe Business School

9

Effective exchange rate and PPP (against the $)

Goethe Business SchoolGoethe Business School

10

PPP and short-term exchange rate

PPP, et

Time t

Short-term exchange rate (e)

PPP

Goethe Business SchoolGoethe Business School

11

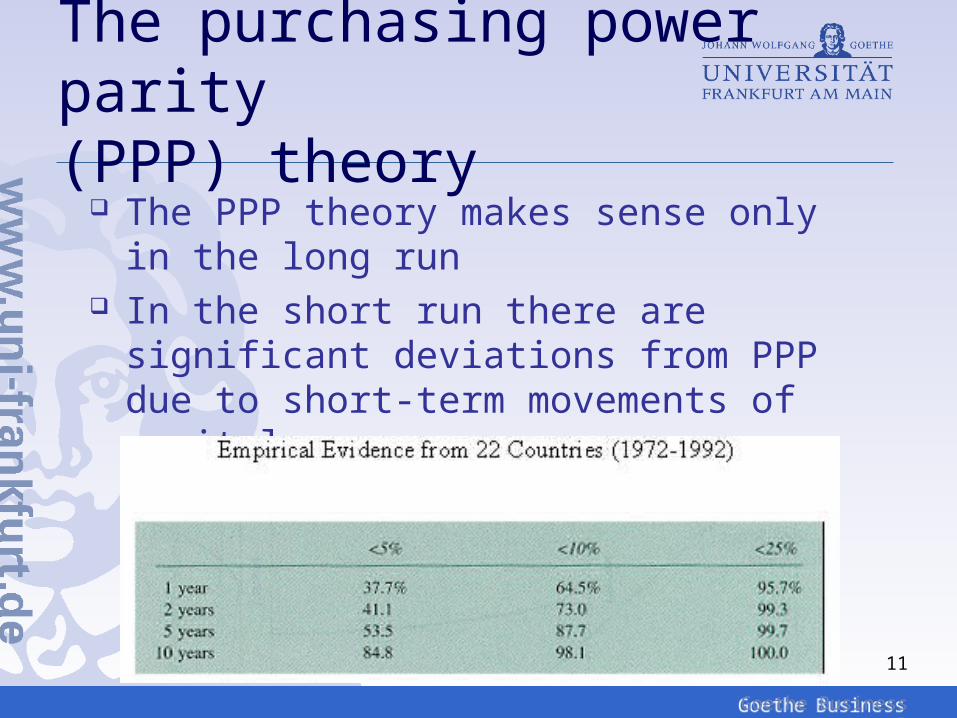

The purchasing power parity (PPP) theory

The PPP theory makes sense only in the long run

In the short run there are significant deviations from PPP due to short-term movements of capital

Goethe Business SchoolGoethe Business School

12

Readings

Reading 9-1: “Purchasing Power Parity”, OECD, Main Economic Indicators, May 2005

Reading 9-2: “Big Mac Index”, The Economist, December 16, 2004

Goethe Business SchoolGoethe Business School

13

Factors that affect exchange rates: long run Factors that affect the exchange rates are

(w = depreciation, w = appreciation): Relative price levels: if P/P*, then w Tariffs and quota: if import duty , then w A shift in preferences for domestic

versus foreign goods: if export demand , then w if import demand , then w

Productivity: If productivity , then w

Goethe Business SchoolGoethe Business School

14

Exchange rates in the short run The theory of the long-run behavior of

exchange rates cannot explain the large changes of current (spot) exchange rates

In order to understand the short-run behavior, we have to recognize that the exchange rate reflects the price of domestic bank deposits (in €) denominated in terms of foreign bank deposits (in $)

Goethe Business SchoolGoethe Business School

15

Comparing expected returns across nations We consider Euroland the “home country”, and

the domestic currency €. The USA are the “foreign country” with the

foreign currency $.Euro deposits bearan interest rate i€.

Dollar deposits bearan interest rate i$.

How does Hans, the European, compare the return on dollar deposits abroad

with the return on domesticinvestments in € ?

Goethe Business SchoolGoethe Business School

16

Comparing expected returns across nations If Hans invests in the USA, he must realize that

his return in terms of € is not i$. He must adjust the return for any expected appreciation/depreciation of the $ against the €

If $-deposits bring an interest rate of i$ =5% p.a., and the dollar is expected to depreciate by 10% p.a. (w = $/€ ), the expected return in € is 5% - 10% = -5%

Goethe Business SchoolGoethe Business School

17

Comparing expected returns across nations More formally

€

RET$(€) = i$ −w e t+1 −wtwt

€

Differential RET (€) = i€ − (i$ −w e t+1 −wtwt

)

= i€ − i$ +w e t+1 −wtwt

Goethe Business SchoolGoethe Business School

18

Comparing expected returns across nations If Bill invests in Euroland, he must realize

that his return in terms of $ is not i€. He must adjust the return for any expected appreciation/depreciation of the € against the $

If €-deposits bring an interest rate of i€ =3% p.a., and the euro is expected to appreciate by 10% p.a. (w = $/€ ), then the expected return is 3%+10%=13%

Goethe Business SchoolGoethe Business School

19

Comparing expected returns across nations More formally

€

RET€($) = i€ +w e t+1 −wtwt

€

Differential RET ($) = i$ − (i€ +w e t+1 −wtwt

)

= i$ − i€ −w e t+1 −wtwt

Goethe Business SchoolGoethe Business School

20

The key point:RET$ and RET€ are symmetrical (with opposite sign)

As the relative expected return on €-deposits increases, both domestic and foreign residentsrespond in the same way: they want to holdmore €-deposits and fewer deposits in $€

- Differential RET ($){ } = − i$ − i€ −

w e t+1 −wtwt

⎧ ⎨ ⎩

⎫ ⎬ ⎭

= i€ − i$ +w e t+1 −wtwt

€

Differential RET (€) = i€ − i$ +w e t+1 −wtwt

Goethe Business SchoolGoethe Business School

21

Interest parity condition

At present, international capital markets are relatively open. There are few impediments to the flow of capital, and $ and € have similar liquidity and risk

When capital is mobile and bank deposits are perfect substitutes, the expected return must become identical:

€

i€ = i$ −w e t+1 −wtwt

Goethe Business SchoolGoethe Business School

22

Why? Arbitrage and liquidity trading

Whenever there emerge small differences between interest rates and/or changes of expectations on the exchange rate, there will be arbitrage in international money markets that evens out the differential between domestic and foreign returns denominated in one currency => Interest parity condition

Goethe Business SchoolGoethe Business School

23

The organization of globalforex markets

Paul Bernd SpahnPaul Bernd SpahnPaul Bernd Spahn

EuroEuroEuro

Goethe Business SchoolGoethe Business School

24

Fx transactions by currency pairs, 2004 (in %)

¥

$ € Other

€ 28

17 3

£ 14 2

SFr 4 1

Other 26 2 2

Goethe Business SchoolGoethe Business School

25

Volume of fx transactions in bill. US $, daily (April)

Goethe Business SchoolGoethe Business School

26

Fx transactions by market place (April 2001)

Geographical distribution of fx turnover, 2004

United Kingdom32%

United States20%Japan

8%

Singapore5%

Germany5%

Hong Kong4%

Australia3%

Switzerland3%

France3%

Canada2%

Other15%

Goethe Business SchoolGoethe Business School

Most traded currencies 2007

27

Goethe Business SchoolGoethe Business School

28

Which type of activities must be distinguished ?

Financing of real economic activity Exports and imports Foreign direct investment

Portfolio management Life insurers Investment funds Hedge funds

Liquidity trading (arbitraging) Speculative „noise trading“

Goethe Business SchoolGoethe Business School

29

Example of a trading desk

Goethe Business SchoolGoethe Business School

30

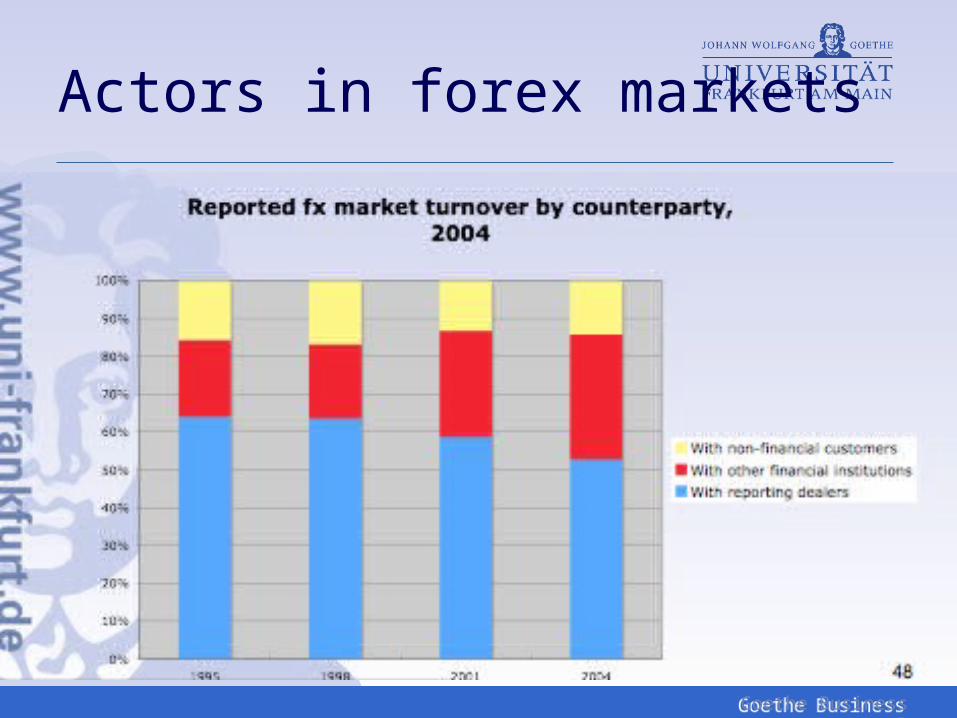

Actors in forex markets

Reported fx market turnover by counterparty, 2004

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1995 1998 2001 2004

With non-financial customers

With other financial institutions

With reporting dealers

Goethe Business SchoolGoethe Business School

31

And will be concentrated even more …

Since September 2002 the forex market has changed: The CLS Bank started operating. It highly concentrates forex dealings due to a new technology

Goethe Business SchoolGoethe Business School

32

Short and long run: the DEM/$-market

Goethe Business SchoolGoethe Business School

33

Short and long run: the DEM/£-market

Goethe Business SchoolGoethe Business School

34

Interventions in forex markets

Our analysis of foreign exchange markets assumed completely free markets so far

In practice, there are also monetary policy interventions in these markets

Under the present system („managed floating” or „dirty floating“), exchange rates might fluctuate daily, but central banks attempt to „smooth“ price behavior in the very short run, and even over some extended period of time

Goethe Business SchoolGoethe Business School

35

Forex interventions By statute, Treasuries (governments) possess

typically the lead role in setting forex policy, but in practice it is usually based on a consensus between the government and the central bank

However stabilizing forex interventions for longer periods have become extremely rare in the US (‘benign neglect’) and in the EU

In carrying out stabilizing interventions, the central bank sells/buys international reserves

Goethe Business SchoolGoethe Business School

36

Balance sheet of a central bank

Assets Liabilities

Base moneyGold

International reserves

Securities

Goethe Business SchoolGoethe Business School

37

Sterilized intervention in forex markets If a central bank buys/sells international

reserves, this has the same effect on the monetary base as OMOs

If the central bank allows this effect to happen, this is called an “unsterilized foreign exchange intervention”

If the expansionary (or contractionary) effect on base money is offset by a counteracting OMO, this is called “sterilization”

Goethe Business SchoolGoethe Business School

38

“Sterilized” forex intervention

Central BankAssets Liabilities

Foreign assets(International reserves)

-€1 billion

Government bonds

+€1 billion

Monetary base(reserves)

Remains unchanged

Goethe Business SchoolGoethe Business School

39

Unsterilized forex intervention

As this type of policy is equivalent to an OMO, it also produces the same results

An increase in the money supply leads to a higher price level in the long run, and hence to a devaluation of the currency

This increases the expected return on foreign deposits, and shifts the RETF-schedule to the right

Goethe Business SchoolGoethe Business School

40

Effect of a purchase of $ against €

Exchange rate($/€)

Expected return in €

1

RETF1RETD

1

iD1

E1

2

RETF2

E2

Goethe Business SchoolGoethe Business School

41

The long-run adjustment process In the short run, not only the return on

foreign asset increases, but also the return on domestic assets declines

The short-run outcome is a fall in the exchange rate from E1 to E3

In the long run, however, the domestic interest rate returns to the former level.

The exchange rate moves back to its new longer term position at point E2

Goethe Business SchoolGoethe Business School

42

Effect of a purchase of $ against €

Exchange rate($/€)

Expected return in €

1

2

RETF2

RETF1RETD

1

iD1iD2

E1

E2

3

RETD2

E3

In the long run the RETD-curvemoves back to theoriginal position.

In the short run the RETD-curvemoves to the left

Goethe Business SchoolGoethe Business School

43

Consequences An unsterilized intervention in which domestic

currency is sold to purchase foreign assets leads to a gain in international reserves, an increase in the money supply, and a depreciation of the domestic currency

An unsterilized intervention in which domestic currency is purchased by selling foreign assets leads to a drop in international reserves, a decrease in the money supply, and an appreciation of the domestic currency

Goethe Business SchoolGoethe Business School

Reading 9-3: “The domino effect”, The Economist, July 3rd, 2008

44

Goethe Business SchoolGoethe Business School

45

Discussion 9: Dealing with exchange rates Why is understanding exchange rates so

important for businesses, even for non-financial firms?

What could decision makers do to hedge against exchange rate risks?

Should governments or central banks try to intervene in the exchange markets?