global trade and technology 080630 -...

TRANSCRIPT

b e v e r l ychamber of commerceMembership MeetingMembership Meeting

The Crossroads:

www.bostonstrategies.com

Global Trade and Technology

Page 1© 2008 Boston Strategies International, Inc.6/30/2008

www.bostonstrategies.com(1) (781) 250‐8150

This report has been prepared by Boston Strategies International at the request of CLIENT for the purpose of establishing its operating strategies. It may not be appropriate for other purposes or audiences. This report contains forward-looking statements andprojections with respect to anticipated future performance of CLIENT, suppliers, customers, and/or general or specific economic conditions and factors that are based on Boston Strategies International’s analysis of market trends and external data. Forward-lookingstatements and projections are not guarantees of future performance and involve significant business, economic and competitive risks, contingencies and uncertainties, which are difficult to predict. Accordingly, these projections and forward-looking statements may

not be realized and actual results may vary up or down. This report may not be reproduced or distributed without express written approval from Boston Strategies International.

Global Supply Chain Economists™

IndustryResearch

Cost and Pricing Analysis

StrategyConsultingResearch Analysis Consulting

®

Page 2© 2008 Boston Strategies International, Inc.6/30/2008

Summary• Data explosion

• Explosion of IT platforms and concepts• Data changing our world• Information = value• IT sustaining global economic growth

• Global trade• Beyond outsourcing• Asian import boom• China: the new empire• Asian traffic growth compounding

• The IT imperativep• To handle trade• To reduce cost of long supply chains• Operating a global IT network• Investing in the IT infrastructure

• What it means for you• One-time opportunity• Plan ahead, profit from the opportunity

Page 3© 2008 Boston Strategies International, Inc.6/30/2008

Agenda

• Data Explosion• Global TradeGlobal Trade• The IT Imperative• What it Means for You

Page 4© 2008 Boston Strategies International, Inc.6/30/2008

Data ExplosionData Explosion

Page 5© 2008 Boston Strategies International, Inc.6/30/2008

Explosion of IT Platforms and Concepts

Rosetta SRMCRM

ASCIIB2BB2CBOI

Chat Client DNS Domain

Auction XML

CADCIOCPCCPPCTO

Domain FTP Gateway Hypertext Internet M ltiM di

WMS ERPData

CTOCTREDIHTM/HTMLISP

MultiMedia OPAC Packet Port PPP

APS GPS

ISSKMMIMEMRPPOP

Protocol Router Server Signature SPAM

TMSeRFQ

RFID

POPPOSPoint Of SaleROIXBRL

SPAM TCP Telnet Trojan Horse WWW

Page 6© 2008 Boston Strategies International, Inc.6/30/2008

Data changing our world

• Innovation from outside• Collaborative sellingCollaborative selling• Supply networks• Standardized subassemblies

“We’re moving towards a world where operations are networkWe re moving towards a world where operations are network-centric. There used to be vertical silos, [but in the future we’ll] have horizontal businesses that can integrate with each other.”

- Stephen Miles MITStephen Miles, MIT

Page 7© 2008 Boston Strategies International, Inc.6/30/2008

Information = value

100%Market Capitalization by Type of Asset

Information Assets

75%

Other Tangible

50%

Property, Plant & Equipment

Assets25%

& Equipment0%

1987 1991 1995 1999 2003 2007 2011 2015

Page 8© 2008 Boston Strategies International, Inc.6/30/2008

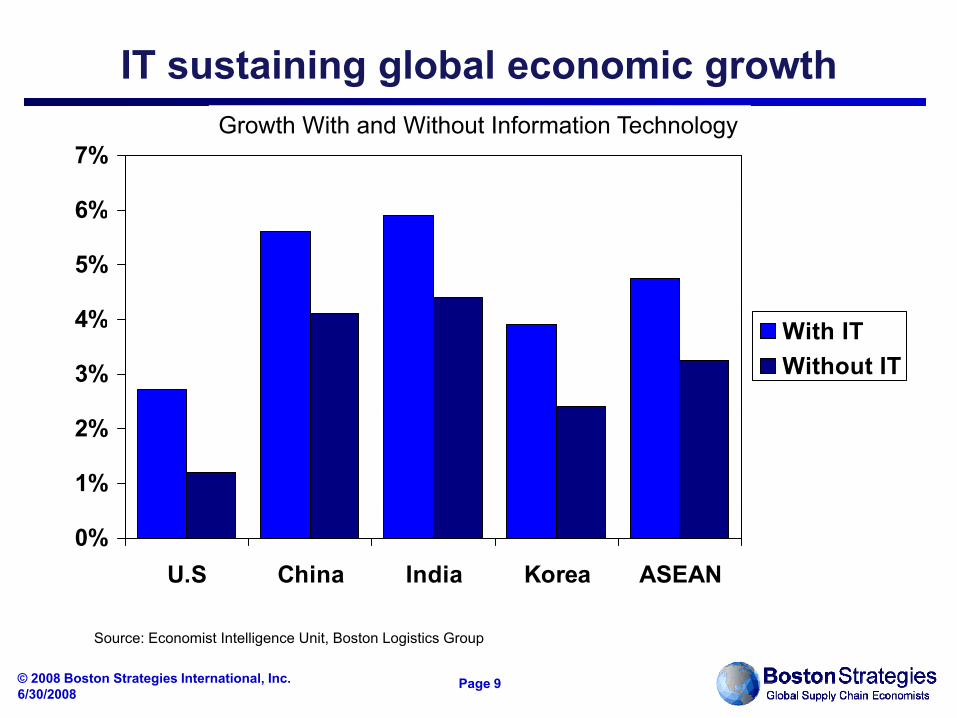

IT sustaining global economic growth

6%

7%Growth With and Without Information Technology

5%

6%

3%

4% With ITWithout IT

1%

2%

0%U.S China India Korea ASEAN

Page 9© 2008 Boston Strategies International, Inc.6/30/2008

Source: Economist Intelligence Unit, Boston Logistics Group

Global TradeGlobal Trade

Page 10© 2008 Boston Strategies International, Inc.6/30/2008

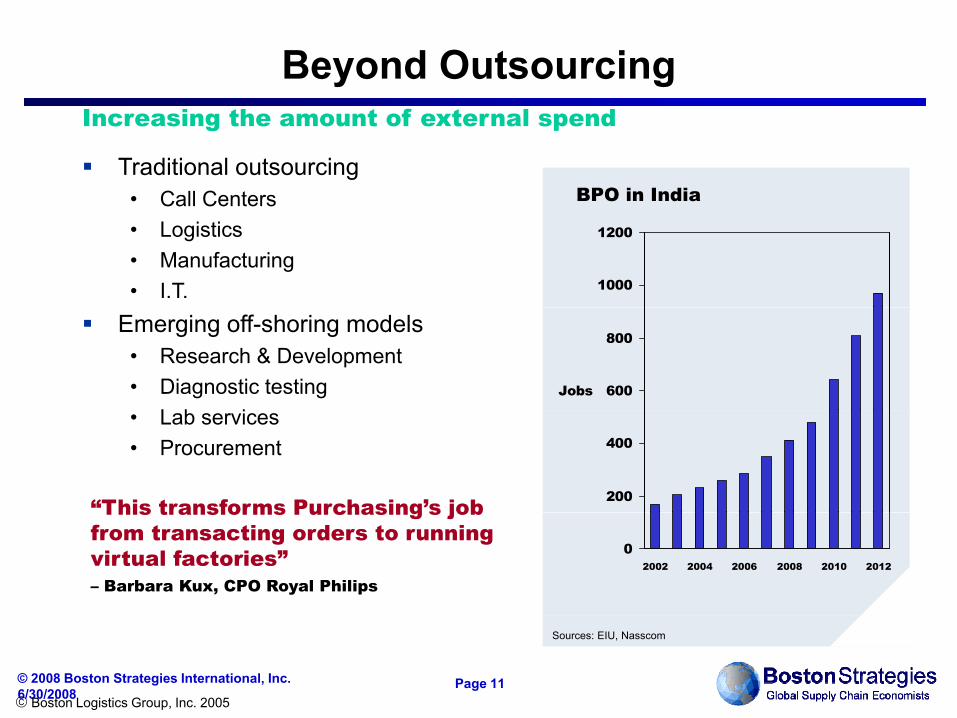

Beyond Outsourcing

Traditional outsourcing• Call Centers BPO in India

Increasing the amount of external spend

Call Centers • Logistics• Manufacturing• I.T. 1000

1200

Emerging off-shoring models• Research & Development• Diagnostic testing

L b i600

800

Jobs

• Lab services• Procurement

“This transforms Purchasing’s job 200

400

This transforms Purchasing s job from transacting orders to running virtual factories”– Barbara Kux, CPO Royal Philips

02002 2004 2006 2008 2010 2012

Page 11© 2008 Boston Strategies International, Inc.6/30/2008

Sources: EIU, Nasscom

© Boston Logistics Group, Inc. 2005

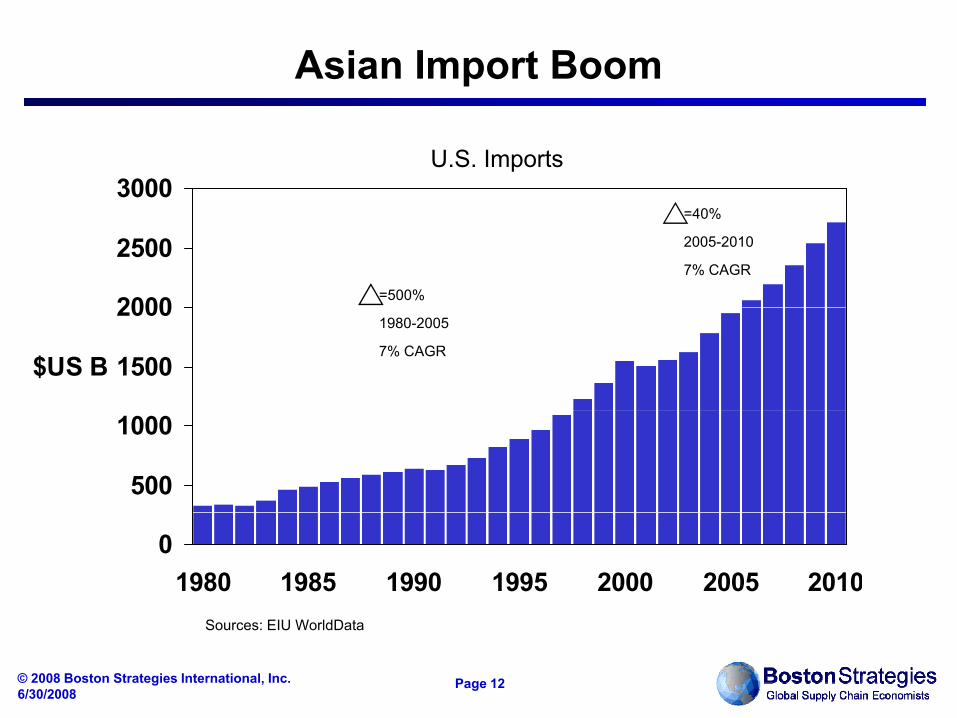

Asian Import Boom

3000U.S. Imports

2000

2500=500%

=40%

2005-2010

7% CAGR

1500

2000

$US B

1980-2005

7% CAGR

500

1000

01980 1985 1990 1995 2000 2005 2010

Page 12© 2008 Boston Strategies International, Inc.6/30/2008

Sources: EIU WorldData

China: the New Empire

Share of World ProductionShare of World Consumption

20%

25%

10%

12%

10%

15%6%

8%

0%

5%

10%

0%

2%

4%

0%China U.S.

2005 2006 2007 2008 2009

0%China U.S.

2005 2006 2007 2008 2009

Page 13© 2008 Boston Strategies International, Inc.6/30/2008

Source: Economist Intelligence Unit

Asian Traffic Growth Compounding

Sales Forecast by Geographic Area

35

40

45

15

2025

30Sales in

Billions of Dollars

0

5

10

15

Assumes current growth rates

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Asia-Pacific United States Europe International

Page 14© 2008 Boston Strategies International, Inc.6/30/2008

Source: HSBC, Datamonitor, Baird

The IT ImperativeThe IT Imperative

Page 15© 2008 Boston Strategies International, Inc.6/30/2008

To Handle Trade

• Launching More New Products Faster• Launching New Products More Frequently• Launching New Products Faster

• Delivering Better Service• Customizing product and service delivery

• Increasing Margins: Rapid, Flexible Response• Rapid Response• Postponementp• Dynamic Pricing

Page 16© 2008 Boston Strategies International, Inc.6/30/2008

To Reduce Cost of Long Supply Chains

• Lean manufacturing• Lean inventory managementLean inventory management• Supplier partnering• Cross-docking and fleet rationalization

Page 17© 2008 Boston Strategies International, Inc.6/30/2008

So UPS Operates a Global IT Network

S ( f ) 96 000

Technology Profile of UPS

• DIADS (Delivery Information Acquisition Device): 96,000 in daily use• UPS's Global Telecommunications Network Sites: 2,700• LAN Workstations: 149,000• Servers: 8 700• Servers: 8,700• Number of Technology Employees: 4,700• Data Centers: Mahwah, NJ and Atlanta, GA• Mainframes: 15Mainframes: 15• Mainframe Capacity (Millions instructions per second, MIPS):

37,399• Terabytes of Storage (Direct Access Storage Device, DASD): 471• Mid-range Computers: 2,342

Page 18© 2008 Boston Strategies International, Inc.6/30/2008

And Others Are Investing in IT

• Web (FedEx)• Package tracking• Cost calculation

• Driver/dispatching (DP)• “IT Demand Units” optimize

application landscape for each• Cost calculation• Customs• Payment• Powerpad: collects data,

Bl t th

application landscape for each division

• Mail and Express invested in technical equipment and the expansion of ITBluetooth

• Hub/sorting (UPS)• Package Flow Technology• $600 million,

expansion of IT. • Network infrastructure in Europe

and the United States• Centrally located data centers in

ll ti$600 o ,• 61% complete at 2005 year-end• $20 billion in IT over 2 decades• Data on 97% of packages• Tech equipment investments of

all time zones• IT risk management system to

guard against natural disasters• Will replace hand scanners in

• Tech equipment investments of $362 mil, total tech equip value, $1,639

30,000 or more districts• Customer interface (TNT)

• SAP integrated solutions• Proprietary customer interface

Page 19© 2008 Boston Strategies International, Inc.6/30/2008

Proprietary customer interface technology

What it Means for YouWhat it Means for You

Page 20© 2008 Boston Strategies International, Inc.6/30/2008

One-Time Opportunity

• Investors• Logistics sector

• Manufacturers and service industries• Asian sourcing and outsourcing

• IT vendors: transportation=communicationIT vendors: transportation communication• Mobile Solutions• Advanced IP Telephony• Communications Equipment• VPN Security• Fast Voice Technology• Interactive Voice Response• Call Center Hardware and Software• Training• Converged Infrastructure• Intelligent System and Network Management

Page 21© 2008 Boston Strategies International, Inc.6/30/2008

Plan Ahead, Profit from the Opportunity

• Speed benefits• Faster NPD cycle time (Hayes & Wheelwright)

• Scale benefits• Bigger and bigger

• Winner takes allWinner takes all• Losers get bought or sold

• Many mega-trends are in fact predictable long in advance (demographics globalization) but most areadvance (demographics, globalization), but most are slow to adapt. Be on top by thinking ahead.

Page 22© 2008 Boston Strategies International, Inc.6/30/2008

Global Supply Chain Economists™Boston Strategies International helps supply chain executives make critical supply chain decisions that involve investment and risk by forecasting the evolution of supply markets and technologies. Our mission is to help our clients develop globally competitive supply networks that maximize Supply Chain Value.™ Our products and services include:

Industry Research that helps investors and policy makers identify emerging issues that affect their supply chains and• Industry Research that helps investors and policy makers identify emerging issues that affect their supply chains, and quantify the impact that they will have

• Cost and Pricing Analysis that helps financial and operational managers plan and budget by providing benchmark, best practice, and forecast data tailored to their companies' supply chains

• Strategy Consulting that helps supply chain leaders make high-stakes decisions related to mergers & acquisitions, market entr capital in estments o tso rcing off shoring and make or bentry, capital investments, outsourcing, off-shoring, and make-or-buy

David Jacoby: djacoby@bostonstrategies com

Boston, MA, USA445 Washington St

Wellesley, MA 02482 USA

Dubai, UAEExecutive Suite

P.O. Box 121601Sharjah, United Arab Emirates (U.A.E.)

Shanghai, China31F Jin Mao Tower88 Shi Ji Avenue

Shanghai 200120, China

Page 23© 2008 Boston Strategies International, Inc.6/30/2008

David Jacoby: [email protected]