global statistics from the international union of marine ...euroland united kingdom brazil china...

TRANSCRIPT

1

© 2012 The Actuarial Profession www.actuaries.org.uk

GIRO Conference and Exhibition 2012 Juggling uncertainty the actuary’s part to play

Wednesday 19th September 2012

GIRO Conference and Exhibition 2012

Global Statistics from the International

Union of Marine Insurance Facts and

Figures Committee

Darren Farr, R&Q / Skuld 1897

© 2011 The Actuarial Profession

www.actuaries.org.uk

2

3

This is about Marine Insurance, so there will be none of this ….

4

… those these gals are okay!

3

5

AGENDA

IUMI and the Facts and Figures Committee

Report on World Merchant Fleet and World Trade

Global Marine Insurance Report

6

International Union of Marine Insurance (IUMI)

o Founded in 1874.

o A professional NGO run by and for its members.

o Members are:

• national insurance associations;

• marine insurance associations; and

• marine professionals.

o Provides an important forum to discuss and exchange ideas of

common interest to marine (re)insurers.

o Enables views and ideas on matters of marine (re)insurance to be

disseminated to all interested parties – including NGOs, IGOs, and the

shipping industry.

o Dedicated to maintain and expand international trade.

4

7

IUMI Facts & Figures Committee

o Created in 2002.

o Provides IUMI with

• updated shipping and marine insurance key data and statistics;

• and an overview of trends in these industries.

o Provide marine insurers with risk data to improve the decision making

processes in risk pricing and risk transfer.

o Industry reports are presented twice a year:

• In September (at the annual IUMI Conference) and in March.

o As well as Casualty and Exposure statistics produce:

• Global Marine Insurance Report

• Global Shipping Market Trends

• Ship Repair Cost Index

8

The following presentations are abridged versions

presented yesterday at the IUMI Conference in San Diego….

…where it’s 30oC and

… but they don’t have

5

Report on World Merchant Fleet and World Trade (abridged)

9

Facts & Figures Country data collection 2012 – 2011 Premium

10

Premium volume of all countries covered in 2011: 31.9 billion USD

6

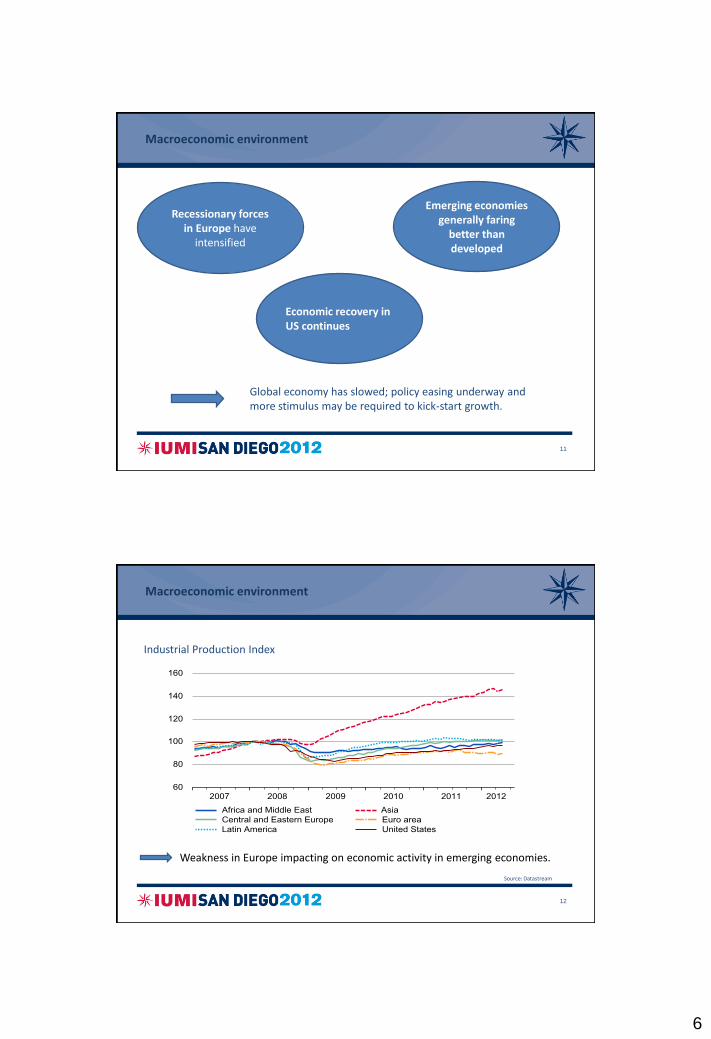

Macroeconomic environment

11

Global economy has slowed; policy easing underway and more stimulus may be required to kick-start growth.

Recessionary forces in Europe have

intensified

Emerging economies generally faring

better than developed

Economic recovery in US continues

Macroeconomic environment

Industrial Production Index

12

Weakness in Europe impacting on economic activity in emerging economies.

Source: Datastream

7

Macroeconomic environment

Real GDP growth rates by region (forecasts)

13

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

2009 2010 2011 2012 2013 2014

Real GDP growth

United States

Euroland

United Kingdom

Japan

South & East Asia

World

Brazil

China

India

Pace of recovery likely to remain modest and significant near-term downside risks.

Source: Swiss Re Economic Research & Consulting

Macroeconomic environment

Inflation (CPI) forecasts

14

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

14%

2009 2010 2011 2012 2013 2014

CPI inflation

United States

Euroland

United Kingdom

Japan

Brazil

China

India

Inflation likely to remain well contained (despite recent food price rises).

Source: Swiss Re Economic Research & Consulting

8

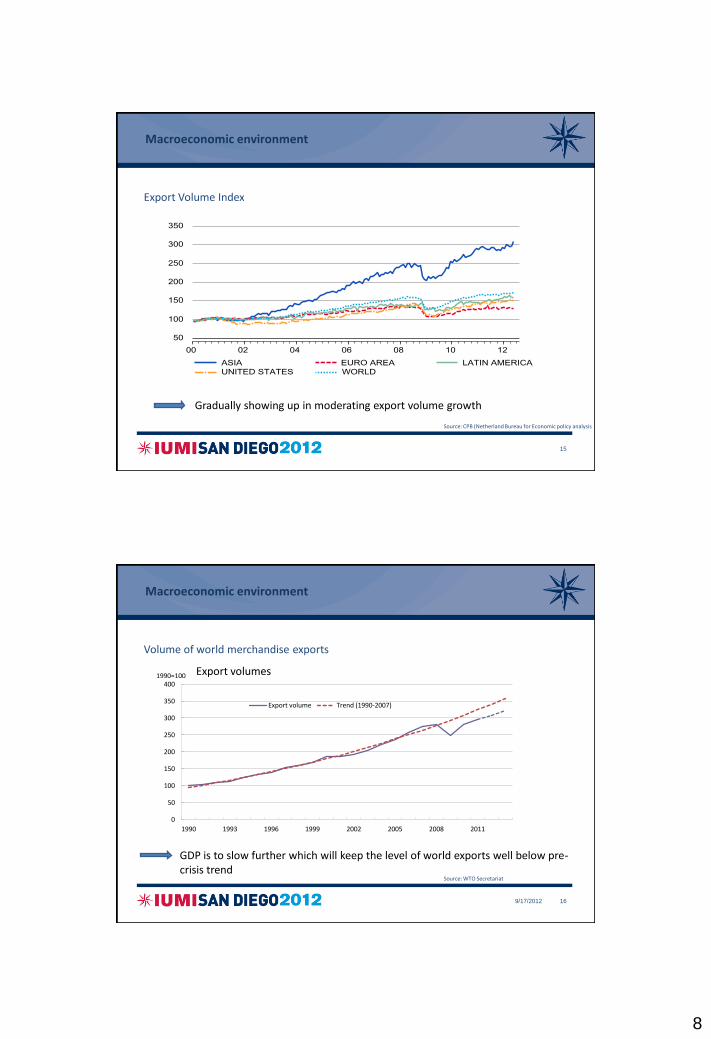

Macroeconomic environment

Export Volume Index

15

Gradually showing up in moderating export volume growth

Source: CPB (Netherland Bureau for Economic policy analysis

Macroeconomic environment

Volume of world merchandise exports

9/17/2012 16

0

50

100

150

200

250

300

350

400

1990 1993 1996 1999 2002 2005 2008 2011

Export volume Trend (1990-2007)

1990=100 Export volumes

GDP is to slow further which will keep the level of world exports well below pre-crisis trend

Source: WTO Secretariat

9

Shipping market

Fleet Capacity

17

0

4'000

8'000

12'000

16'000

20'000

24'000

28'000

32'000

36'0002

00

0

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

*

DW

T

0

250

500

750

1'000

1'250

1'500

1'750

2'000

2'250

No

. of V

es

se

ls

Tanker Fleet Bulkcarrier Fleet Containership/MPPs Fleets Deliveries Scrapping

*2012 data is year-to-date.

Source: Clarkson Research, August 2012

Shipping Market

Average Age of the World Fleet 2000-2012

18

10

12

14

16

18

20

22

24

26

Ja

n 0

0

Ju

l 0

0

Ja

n 0

1

Ju

l 0

1

Ja

n 0

2

Ju

l 0

2

Ja

n 0

3

Ju

l 0

3

Ja

n 0

4

Ju

l 0

4

Ja

n 0

5

Ju

l 0

5

Ja

n 0

6

Ju

l 0

6

Ja

n 0

7

Ju

l 0

7

Ja

n 0

8

Ju

l 0

8

Ja

n 0

9

Ju

l 0

9

Ja

n 1

0

Ju

l 1

0

Ja

n 1

1

Ju

l 1

1

Ja

n 1

2

Ju

l 1

2

Av

era

ge

Ag

e

Total Tanker Bulkcarrier Containership/MPP Gas Others

Source: Clarkson Research, August 2012

10

Shipping Market

Freight Rates

19

0

5000

10000

15000

20000

Jan 2008 Jul 2008 Jan 2009 Jul 2009 Jan 2010 Jul 2010 Jan 2011 Jul 2011 Jan 2012 Jul 2012

Baltic Panama Index Baltic Supramax Index Capesize

... and freight rates remain low. Source: Bloomberg

Shipping Market

20

• Freight rates are still suffering and are slightly below historical average rate due to the higher cost basis for shipowners

• Current newbuildings orderbook still suggests significant capacity to come on stream in the future even if there's a considerable uncertainty (possible cancellations and delays)

• Bulkcarriers average age dropped from approximately 14 years on January 2010 to 10.5 years on July 2012

• Vessels' demolition rate is still high compared to 2011 for both tankers and bulk carriers

• Shipping market uncertainty remains

linked to macro-economic scenario

11

Outlook for the marine insurance industry

21

weak and often negative growth

risk of inflation

low interest rate environment

further instability in the Euro zone

22

Conclusion

12

2012 Global Marine Insurance Report (abridged)

23

Global Marine Insurance Report 2012

• Cargo – market & results

• Hull – market & results (with some words on major losses...)

• Offshore Energy – market & results ____________________________________________________________

• Underlying Data – for download (Premium by country, Loss ratio triangulations)

13

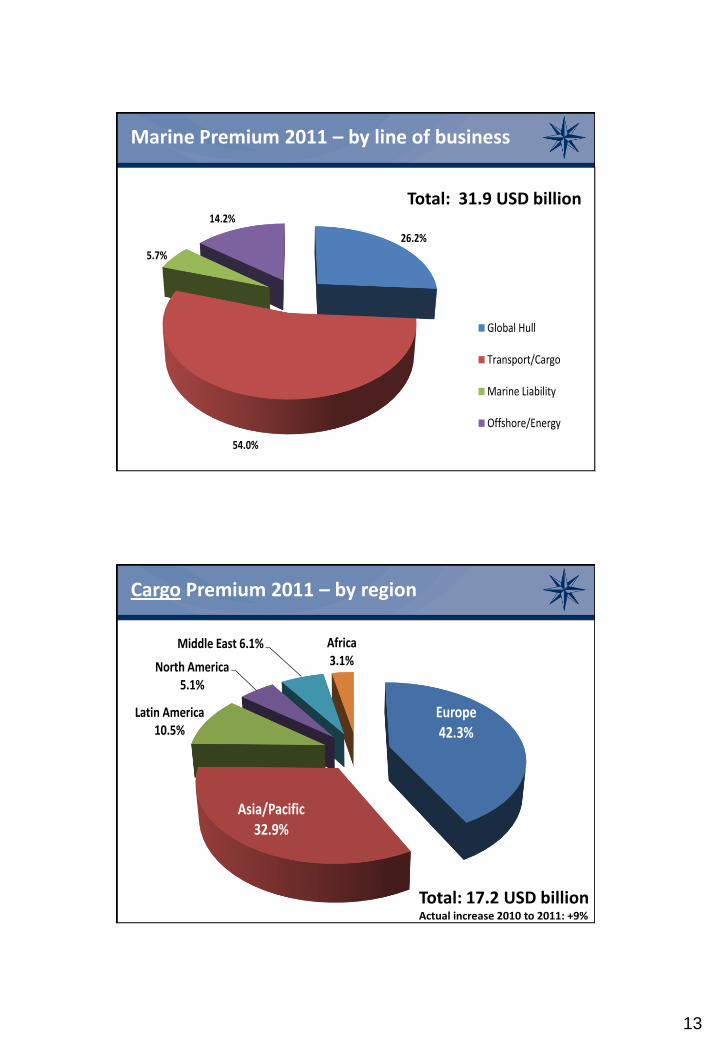

26.2%

54.0%

5.7%

14.2%

2011

Global Hull

Transport/Cargo

Marine Liability

Offshore/Energy

Marine Premium 2011 – by line of business

Total: 31.9 USD billion

Europe42.3%

Asia/Pacific 32.9%

Latin America 10.5%

North America 5.1%

Middle East 6.1% Africa3.1% 2011

Cargo Premium 2011 – by region

Total: 17.2 USD billion Actual increase 2010 to 2011: +9%

14

Belgium2.1%

Brasil4.2%

China9.0%

France5.0%

Germany7.0%

Italy2.9%

Japan11.4%

Mexico2.0%Netherlands

3.0%

Nordic2.2%

Russia2.9%

Spain1.6%

UK (IUA)2.3%

UK (Lloyds)6.8%

USA4.5%

Other markets33.1%

2011

Cargo Premium 2011 – by markets

Total: 17.2 USD billion

**

** includes proportional and facultative reinsurance

0%

20%

40%

60%

80%

100%

120%

140%

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

Cargo – Gross* Ultimate Loss Ratio Underwriting years 1996 to 2011 Data from: Belgium, France, Germany, NL, Italy, Spain (no update 2011), UK, USA (2010 Japan tsunami affected mainly Japanese market)

* Technical break even: gross loss ratio does not exceed 100% minus the expense ratio (usually 20%-30% acquisition cost, capital cost, management expenses)

2011: Starts high at 72%, may end at 74%. No technical profit.

Since 2007: Deterioration of results .

2002 to 2006: Gross loss ratios stayed below 60% - technical profit.

..and 2012?

15

40%

50%

60%

70%

80%

1 2 3 4 5

2004

2005

2006

2007

2008

2009

2010

2011

Cargo – Gross reported Loss Ratios Underwriting years 2004–11, as reported after 1, 2, 3, 4, 5 years

2011:

Starts high at new

maximum of 72%.

2010:

follows 2007/2008

pattern; passed 70%

2007/2008:

improved, but still at

high levels > 70%

Since 2007:

Market changes

demand adjustment

of claims reserves

=> Change in typical

pattern

Previous loss ratio level

Recent loss ratio level 2011

Summing up Cargo

2011 Premium growth reflects upswing in trade Commodity prices rising, stock throughput programs expanding (US), but economical environment remains unstable.

Increase in claims reserves – change in pattern 2007/2008 improved later, but loss ratios stay high.

2011 Loss ratio starts at new maximum of 72% Impact of Natural catastrophes (Thailand floods), more general average claims, increasing acquisition costs.

Claim cost unlikely to decrease Increased accumulation risk, moral hazard, theft frequency, natural catastrophes. Sanctions and piracy still a concern.

16

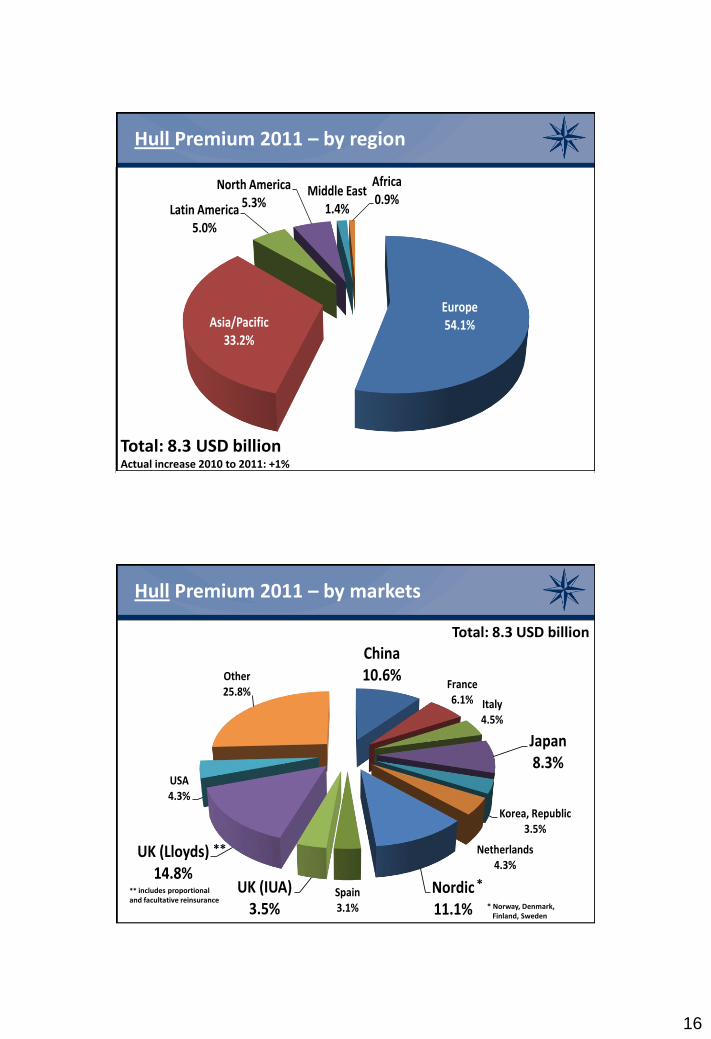

Europe54.1%Asia/Pacific

33.2%

Latin America5.0%

North America5.3%

Middle East1.4%

Africa0.9% 2011

Hull Premium 2011 – by region

Total: 8.3 USD billion Actual increase 2010 to 2011: +1%

China10.6%

France6.1% Italy

4.5%

Japan8.3%

Korea, Republic3.5%

Netherlands4.3%

Nordic11.1%

Spain3.1%

UK (IUA)3.5%

UK (Lloyds)14.8%

USA4.3%

Other25.8%

2011

** ** includes proportional and facultative reinsurance

Hull Premium 2011 – by markets

Total: 8.3 USD billion

*

* Norway, Denmark, Finland, Sweden

17

5.4%7.0%

2.4%

8.3%

5.4%

-14.5%

-9.2%

-3.2%

-7.3%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%2

00

4

200

5

200

6

200

7

200

8

200

9

201

0

2011

201

2

Average annual change in insured values on renewed vessels

Source: Cefor - Nordic Marine Insurance Statistics as of 30 June 2012

Decrease in insured values continues

Change in insured values on renewed vessels

by year of renewal

(= insured value on renewal / insured value previous year)

0%

20%

40%

60%

80%

100%

120%

140%

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

2012: strong total loss impact (on uw years 2011 & 2012) Costa Concordia: Carnival Corporation & PLC website: 508+17 MUSD from H&M insurance. (2Q financial report, issued 02.07.2012)

...and more total losses in excess of 30 MUSD did incur 1st half 2012 (partly attaching to uw year 2011).

Hull – Gross Ultimate Loss Ratio Underwriting years 1996 to 2011

Data from: Belgium, Germany, France, NL, Nordic, Spain (no update 2011) ,UK, USA

18

40%

50%

60%

70%

80%

90%

1 2 3 4 5

2003

2004

2005

2006

2007

2008

2009

2010

2011

Hull – Gross* Reported Loss Ratio Underwriting years 2003-2011, as reported after 1, 2, 3, 4, 5 years

Previous loss ratio level

Recent loss ratio level

2011

2011:

starts at normal level.

2009-2010:

Price-driving factors

return to ”normal”

levels, but no stable

environment.

2010 strong increase.

2006-2008:

Repair cost driven up

by changing frame

conditions => Change

in claims pattern

40%

50%

60%

70%

80%

90%

100%

110%

1 2 3 4 5

2003

2004

2005

2006

2007

2008

2009

2010

2011

Hull – Gross* Ultimate Loss Ratios Underwriting years 2003-2011 – estimated development towards ultimate

2011:

Unprecedented

total loss impact –

loss ratio may

reach new heights.

1st half 2012:

Increase in no. of

losses xs 30 MUSD.

Impact on

underwriting years

2011 and 1012.

2011 – new heights?

19

Summing up Hull (1)

Frame conditions – still unstable Steel prices / repair yard capacity / exchange rates / commodity prices / vessel utilization /newbuildings / world trade / Euro crisis... Influence • Income (ship values) • Cost (claim frequency/repair cost).

Repair cost / Claim frequency – Stabilize But: catching up of trade/higher utilization rates may cause repair cost to rise again

Major claims – strong impact 1st half 2012 Unprecedented costly event Increase in total loss frequency 1st half 2012 Continuing downturn in insured values creates more

constructive total losses

Summing up Hull (2)

Hull technically at loss for 16 consecutive years!

Future Global Hull Market:

Understand dependencies between macroeconomic parameters and repair cost

Models to estimate expected claim cost (=risk premium)

Trade / Fleet development

Market discipline / capacity

The impact of major claims

Understand the actually covered exposure

20

Major losses 2012

39 « The Economist » June 9th-15th 2012

Major Hull losses 2012

40

21

0.000%

0.050%

0.100%

0.150%

0.200%

0.250%

0.300%

0.350%

0.400%

0.450%

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

40,000,0002000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

Claim per Sum Insured & Average Sum Insured

Average Sum Insured excluding total losses including total losses

Source: Cefor Nordic Marine Insurance Statistics as of 30 June 2012; Figures reflect 100% of all vessels, not the share written in a specific market

Average insured value Claim cost in % of total total insured value

41

Watch your Exposure – one Costa Concordia can double the cost relative to the total insured value

Can it get worse...?

Increasing vessel size

Increasing value accumulation per vessel

22

UK (Lloyds)58.1%

Brasil4.8%

USA4.6%

Nigeria4.2%

Malaysia4.0%

UK (IUA)3.5%

Nordic3.0% India

2.9%

Japan2.8%

Italy2.1%

Other10.0%

2011

Offshore Energy Premium 2011 – by markets

No data: Kazakhstan.

*

* includes proportional and

facultative reinsurance

Total: 4.5 USD billion Actual increase 2010 to 2011: 11%

(new)

0%

50%

100%

150%

200%

250%

300%

350%

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

outstanding

paid 12th year

paid 11th year

paid 10th year

paid 9th year

paid 8th year

paid 7th year

paid 6th year

paid 5th year

paid 4th year

paid 3rd year

paid 2nd year

paid 1st year

2005

Katrina & Rita

2004

Ivan

2008

Ike

Soft market

2009-11 no

major hurricane

activity, but…

Offshore Energy – Gross Reported Loss Ratios including liability – Underwriting years 1996 to 2011

As of December 2011:

23

Summing up Offshore Energy

Volatile business, strong hurricane impact – less in recent years.

Long time lag between accident and claims payment (due to technical complexity of the insured objects)

No regular claims patterns. (Claims reserves set according to knowledge about individual claims).

Recent development:

Reduced hurricane impact (2012 Hurricane Isaac: first Gulf of Mexico hurricane in four years, little impact on results)

Increasing frequency of large single loss events (physical loss and liability)

Events with high liability cost in 2009 and 2010

2011: two losses xs 300 MUSD (Gryphon Alpha, Banff) 2012: one loss xs 300 MUSD (KS Endeavour)

46

Thank you

Further details at

www.iumi.com

and

http://www.iumi.com/index.php/committees/fa

cts-a-figures-committee/statistics

24

47

Questions?