global product liability

DESCRIPTION

Global Product Liability. Coverages Worth B uying and Claims to L earn From. • Jim Gothier, Enterprise Risk Manager The Sherwin-Williams Company • Tanja Maffei Chan, CPCU, ARM SVP, International, Willis Based in Chicago, USA and Geneva Switzerland. - PowerPoint PPT PresentationTRANSCRIPT

Page 1

Recording of this session via any media type is strictly prohibited.

Page 1

Global Product Liability

Coverages Worth Buying and Claims to Learn From

Page 2

Recording of this session via any media type is strictly prohibited.

• Jim Gothier, Enterprise Risk Manager The Sherwin-Williams Company

• Tanja Maffei Chan, CPCU, ARMSVP, International, Willis

Based in Chicago, USA and Geneva Switzerland.Responsible for production and account stewardship of international business. Multilingual, almost 20 years in insurance. Enjoys teaching and mentoring, traveling and cooking.

Page 3

Recording of this session via any media type is strictly prohibited.

What to ExpectWe will examine global claims statistics and case

studies to help you understand if the coverage you purchase will pay the claim.

You should be able to:• Consider global liability coverage options.

• Improve your current liability program.• Assess the impact to your company of global claims settlement and litigiousness trends.

Page 4

Recording of this session via any media type is strictly prohibited.

COMMUNICATION

LAWS

SERVICE PROTOCOL

TAX CLAIMS

TECHNOLOGYPROGRAM

STRUCTURE

INSURERS

The Issues At A GlanceThe Issues at a Glance

Page 5

Recording of this session via any media type is strictly prohibited.5

Source: Norris& Bazemo law firm, Paris

Page 6

Recording of this session via any media type is strictly prohibited.

US vs. Foreign ProgramsCountry Non-Admitted Permitted &

Comments Compulsory Taxes Standard USD GL Limits

Standard USD Auto Limits Standard USD EL Limits

Australia G Except for compulsory WC & AL (see taxes)

WC, AL/CTP, Aviation, various PI and specialty lines

GST: 10% 10-50 unagg 20-30M 50M incl in WC

Brazil R Prohibited AL, SS, WC, Fire for large exposures only

All lines - 7.38% <1M <50K <500K in GL

China R Prohibited, except international cargo AL, SS Schemes, Construction Policy issuing tax of 5% 1-5M <10K <50K

France Y Not advised; EU policies accepted

AL, Property – Natural Catastrophe, various specialty lines Various up to 34.20% 5-30M BI unlim, PD max

133M 2-8M gross negligence

India R Prohibited WC (“highly recommended”)& AL Service Tax - 12.36% (non-life policies)

1-2M <10K 500K-1M

Japan R Prohibited AL & PI for Brokers Stamp tax paid by insurer 1-2M unlim BI, 200K PD 1-2 infrequent

Mexico R Except where cover is unavailable locally

AL (specific states), D&O (publicly-listed companies), various specialty

linesVAT - 16% 110K-10M 100K to 300K

recently N/A

Russia R ProhibitedAviation/Railway, AL, various

specialty , professional,Compulsory liability hazardous

None 500K-1M 10-500K very rare 500K-1M

South Africa R Prohibited AL (State) VAT 14% 1-2M R160K WC benefit set by Govt

United Arab Emirates R Prohibited

AL, PD, Insurance brokers and consultants E&O, Gov't Projects insurance. D&O but not strictly

enforced. Medical Insurance

None 220K-1M <300K <500K

United Kingdom(incl. NI) G Except for compulsory

classes AL, EL, statutory inspection of certain types of machinery & specialty lines

IPT - 6% VAT - 17.5% 7.5-30M umlim BI, max

75M PD 7.5/15 compulsory

United States of America G Permitted, except for

compulsory classes

AL, WC, Nuclear Operators, Social Security, Environmental Impairment,

Fidelity Insurance.Within the premium 1-200M 1-5M 1-2M then umbrella

Source: Willis Dbase, Axco

Page 7

Recording of this session via any media type is strictly prohibited.

Where to Buy Local Policies?

Other Contributing Factors

Is local representation important for legal issues, claims adjusting or risk management consulting?

Are there important coverage extensions on local policies not available through the corporate program?

Can coverage be obtained more efficiently in other ways, e.g. as a good corporate citizen?

Tax considerations: local premium taxes, tax deductibility of local premiums, premium allocations and recharges to local entities, local capital injection duties, income tax payments on non-admitted claims.

Establish insurers’ approach to mitigate regulatory and tax risks.

Is the local establishment a joint venture with capital injection requirements?

Will the local establishment disregard corporate instructions and independently purchase local policies?

Start

Is there a local legal entity-subsidiary,

branch, factory etc with assets, personnel or

revenue?

Is a local policy compulsory? (i.e. for workers’ comp

or auto liability)

Yes

No

Rely on Corporate

Global Program

Is a local policy required by

contract, e.g. lease, customer agreement, etc.?

Is non-admitted coverage illegal &

local “self insurance”

uncommon?

Do other contributing

factors justify a local policy?

No Obtain a locally admitted policy

Yes

Yes

Yes

Yes

No

No

No

Can an exemption be obtained from

local regulator?

No

Establish potential local exposure and appropriate local limits.

Yes

LOCAL POLICY ISSUES

Evaluate where the risks are located and the potential loss exposure.

Determine what level of cover would be appropriate.

Clarify where claims will be paid by the insurer and the implications of this (i.e. taxes, legality, etc).

Do the insurers on the program have the ability to issue a local policy?

Local Policy Decision Tree

Page 8

Recording of this session via any media type is strictly prohibited.

Cover/limits

Recommended Structure - CMP Advantages Uniformity of cover worldwide

Maximum bulk purchasing benefits

Tax benefits to local subsidiary

Uniform risk management approach

Solid claims coordination

Disadvantages Needs firm central control

Considerable administration burden if no broker involvement

Master DIC DIL Policy

FOS GL/ EL China

GL/ EL

Brazil GL/ EL

Page 9

Recording of this session via any media type is strictly prohibited.

Why Buy Foreign GL?• To protect foreign legal entities, employees and assets • To act as a good citizen and prevent reputational risk (social

media),• To provide local certification,• To be able to deduct premiums locally and show proof of IPT

payments, • To obtain broader coverage in some cases, • To tap into local insurer expertise- adjustors, lawyers.• Can be guaranteed cost and often less expensive than US rates• Continental EU, UK, Australia are all well developed and

litigious societies- increasing class action claims -some punitive damages

• Vendor’s programs- negotiate to ensure coverage. Consider an intl carrier for leverage, for broader territory (not only CHINA) and claims handling expertise outside China.

Page 10

Recording of this session via any media type is strictly prohibited.

Defining Good Local StandardsLimits-•is 1-2M still enough? consider changing local laws, class actions, your contracts and certification requests, •Consider having your umbrella issue a higher limit FOS on an admitted basis Coverages-•Beyond property damage- PFL/ DINC, Extended products, Recall•Fines, penalties, punitive damages•Tenant’s & Neighbor’s libaility•S&A versus EIL, EU directive, China, Russia•Duty of care/EL•Decennial liability•German warranty

Page 11

Recording of this session via any media type is strictly prohibited.

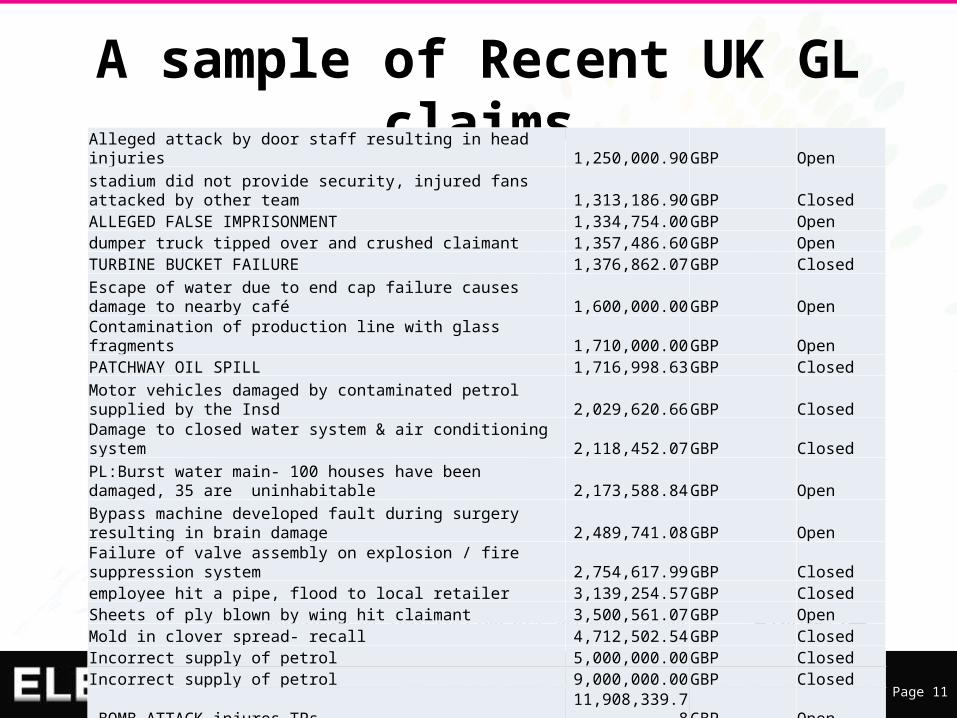

A sample of Recent UK GL claimsAlleged attack by door staff resulting in head injuries 1,250,000.90 GBP Open

stadium did not provide security, injured fans attacked by other team 1,313,186.90 GBP ClosedALLEGED FALSE IMPRISONMENT 1,334,754.00 GBP Opendumper truck tipped over and crushed claimant 1,357,486.60 GBP OpenTURBINE BUCKET FAILURE 1,376,862.07 GBP Closed

Escape of water due to end cap failure causes damage to nearby café 1,600,000.00 GBP OpenContamination of production line with glass fragments 1,710,000.00 GBP OpenPATCHWAY OIL SPILL 1,716,998.63 GBP Closed

Motor vehicles damaged by contaminated petrol supplied by the Insd 2,029,620.66 GBP ClosedDamage to closed water system & air conditioning system 2,118,452.07 GBP ClosedPL:Burst water main- 100 houses have been damaged, 35 are uninhabitable 2,173,588.84 GBP OpenBypass machine developed fault during surgery resulting in brain damage 2,489,741.08 GBP OpenFailure of valve assembly on explosion / fire suppression system 2,754,617.99 GBP Closedemployee hit a pipe, flood to local retailer 3,139,254.57 GBP ClosedSheets of ply blown by wing hit claimant 3,500,561.07 GBP OpenMold in clover spread- recall 4,712,502.54 GBP ClosedIncorrect supply of petrol 5,000,000.00 GBP ClosedIncorrect supply of petrol 9,000,000.00 GBP Closed BOMB ATTACK injures TPs 11,908,339.78 GBP Open

Page 12

Recording of this session via any media type is strictly prohibited.

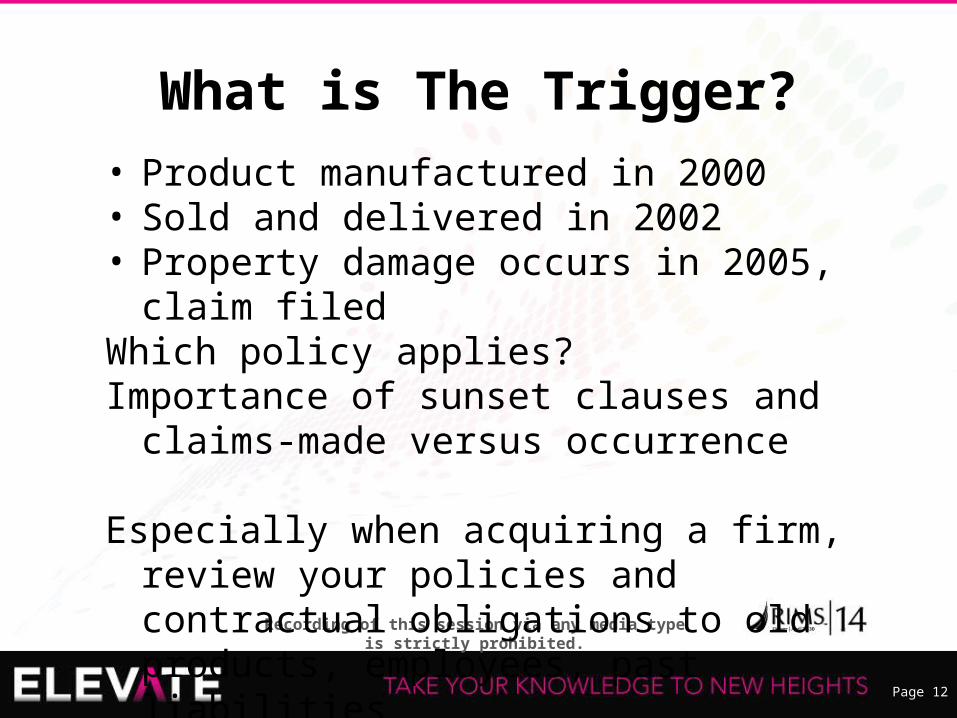

What is The Trigger?• Product manufactured in 2000• Sold and delivered in 2002• Property damage occurs in 2005, claim filedWhich policy applies? Importance of sunset clauses and claims-made

versus occurrence

Especially when acquiring a firm, review your policies and contractual obligations to old products, employees, past liabilities

Page 13

Recording of this session via any media type is strictly prohibited.

Why Buy FVWC?• Guaranteed cost- voluntary WC (occupational-medical, disability,

income replacement) and excess EL (some countries excluded), • As coverage is voluntary, benefits can be provided in a more flexible

manner than as legally mandated • Can cover all employees and some coverages can be extended to

family, spouse, outside D&O,• More 24/7 than US WC and often on primary basis, can provide

cover for personal deviation, commuting to/from work in situ,• Accidents and some endemic disease- sars, avian flu, malaria, yellow

fever, H1N1, can manifest upon return,• Expert claims handling, • Assistance services and training- travel, medical, evacuation

(disease/ accident and political),• Some ancillary coverages- K&R, AD&D. Other options: SOS, DBA,

BTA, EB

Page 14

Recording of this session via any media type is strictly prohibited.

Why Buy Employer’s Liability?• With globalization, employees are seeking remedies above smaller WC

payouts• Often can be added to the local GL policy with minimal premium, compulsory

in many countries• Duty of care- A concept that employers provide a place of employment that

is safe and free from hazards that could cause injury or death. A corporation could be considered negligent.

• UK Manslaughter Act – holds a company criminally liable for negligence that results in the death of an employee outside the UK.

• Australian Case Law has expanded to include injuries to employees that occur during activities of their own choosing. Contractors on your premises filing GL claims.

• Workforce (HSA /OSHA) audits to protect employees- often need to report US expats, tcns, volunteers, apprenticeship

• Subrogation by Government health systems- Gross Negligence France, Italy

Page 15

Recording of this session via any media type is strictly prohibited.

Why Buy UK Employer’s Liability?• It’s compulsory. MOJ reforms and the portal- speeding up claims, limits

plaintiff attorney’s fees, loser pays defense costs.• UK EL very strict standard- reputable presumption of liability that ER did not

provide a safe work place.• Insurers can offer training, loss control assistanceThe most common disease claims:• Deafness (75% of the total disease claims)- average £5K plus costs (overall

about £15K). Frequency is increasing with aging population.• HAVS (vibration claims) around £20K plus costs. Also on the rise. • The average Mesothelioma claim settles around £250K in about 3 years and

liability remains often with the last employer.Last 10 yrs- UK Insurer Samples GBP Total Incurred Forklift injured TP while unloading 1,354,206.04Steel beam snapped back of TP- paralysis 1,500,000.00Back injury to truck driver which hit bridge 1,736,768.12Knee injured- sitting in shunter hit by another lorry 1,779,688.16Hit by panel on production line 1,934,867.09Fall down stairs- water on steps 3,015,247.95

Page 16

Recording of this session via any media type is strictly prohibited.

Why Buy Excess Foreign Auto?• Local Limits are often very low in developing countries• To be able to schedule under the umbrella• To provide excess cover over foreign car rentals• When multiple claimants are involved, the claim can

easily reach over 1M USD• Largest UK auto claim in recent years almost 14M

USD: insured vehicle hits two third party cars, multiple injuries

• Many injuries due to distractions- backing over cyclists and kids, not signaling lane changes, running red lights

Page 17

Recording of this session via any media type is strictly prohibited.

17

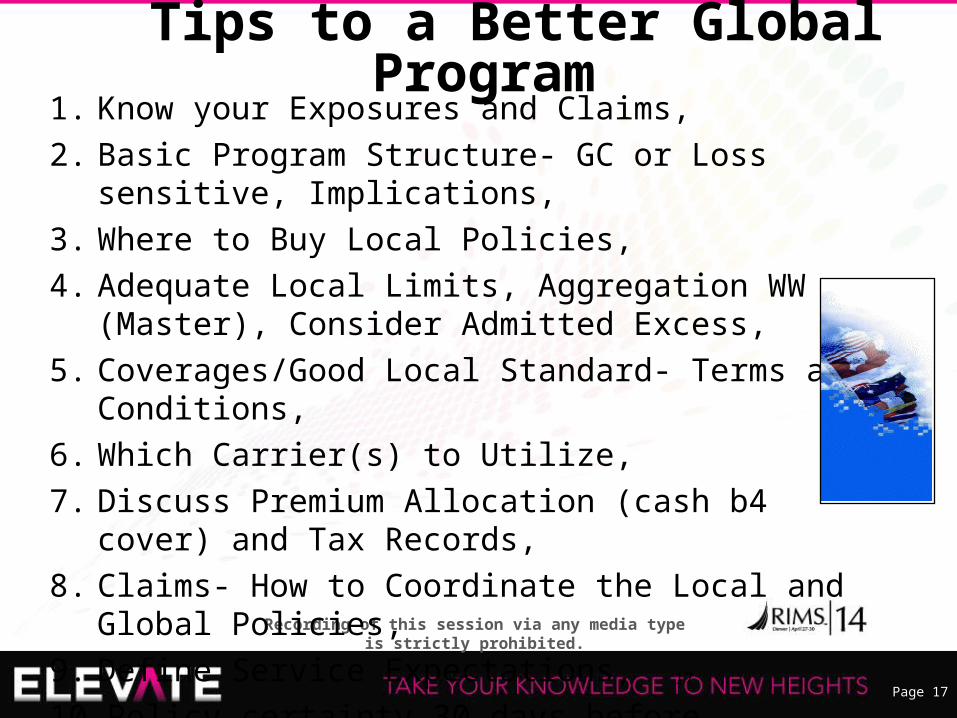

1. Know your Exposures and Claims, 2. Basic Program Structure- GC or Loss sensitive, Implications,3. Where to Buy Local Policies, 4. Adequate Local Limits, Aggregation WW (Master), Consider

Admitted Excess,5. Coverages/Good Local Standard- Terms and Conditions,6. Which Carrier(s) to Utilize,7. Discuss Premium Allocation (cash b4 cover) and Tax

Records,8. Claims- How to Coordinate the Local and Global Policies,9. Define Service Expectations,10. Policy certainty 30 days before binding.

Tips to a Better Global Program

Page 18

Recording of this session via any media type is strictly prohibited.

Tips to a Better Global Program1) Global Territory Provision (good), US occurrences foreign

suits, US occurrences US suits, local policies should be ww2) Broad named insured – All entities- past, present, newly

acquired, formed, JVs 3) Global Liberalization Clause 4) Contract commitment to issue local policies upon request5) Financial Interest Named Insured Clause (may be a problem

or a solution)6) Waiver of subrogation, Additional insured- blanket, broker

to issue certs where possible7) EL as part of GL if available or separate where compulsory

Page 19

Recording of this session via any media type is strictly prohibited.

Questions?

THANK YOU for your attendance and for your active participation. We appreciate your candid feedback on the evaluations.

Jim GothierERM, The Sherwin Williams [email protected]+1 (216) 566-2916

Tanja Maffei ChanSVP, International, [email protected]+1-312-288-7324 Chicago Office+41-79-1374744 Swiss Cell

Please complete the session survey on the RIMS14 mobile application.