global pharma market · 2020-07-03 · global pharma market & covid-19 impact –2019-2024...

TRANSCRIPT

July 2020Global Pharma Market & Covid-19 Impact – 2019-2024 Perspectives

Global Pharma Market& Covid-19 Impact

Position Paper1, rue Houdart de Lamotte – 75015 Paris – France

Tel. +33 6 11 96 33 78 Email : [email protected] – Website : www.smart-pharma.com

July 2020

2019-2024 Perspectives

MARKET INSIGHTS SERIES (#14)

“Wrong decisions are often due to weak market insights”

July 2020Global Pharma Market & Covid-19 Impact – 2019-2024 Perspectives 2

Introduction

Smart Pharma Consulting proposes to share insights regarding 8 topics that are essential to play and to win in the pharmaceutical industry

▪ This position paper provides specific insights for those who want to anticipate the global pharma market evolution over the 2019-2024 period, while considering the impact of the Covid-19

▪ We have selected 8 topics for which we share our knowledge and thoughts:

Global Pharma Market & Covid-19 Impact

Sources: Smart Pharma Consulting

Part A - Pharma Market Insights

1. Size and Dynamics by Geography

2. Size and Dynamics by Business

3. Attractiveness

4. Access to Market

Part B - Pharma Company Insights

5. Strategic Directions

6. R&D Operations

7. Manufacturing & Supply Chain Operations

8. Medico-Marketing & Sales Operations

July 2020Global Pharma Market & Covid-19 Impact – 2019-2024 Perspectives

533 (43%)665 (43%)

174 (14%)

188 (12%)142 (11%)

190 (12%)87 (7%)

89 (6%)

71 (6%)

98 (6%)244 (19%)

320 (21%)1 250

1 550

0

200

400

600

800

1 000

1 200

1 400

1 600

2019 2024

3

1 France, Germany, Italy, Spain, UK – 2 Ex-factory price before rebates – 3 Brazil, Russia, India – 4 USA and Canada

Part A – Pharma Market Insights – 1. Size and Dynamics by Geography

Sales of EU51 should grow slowly by 2024 due to stringent cost containment measures leading to a two-point decrease of their weight in the global pharmaceutical market

Global Pharma Market & Covid-19 Impact

Sources: IQVIA Institute (March 2020) – Smart Pharma Consulting estimates

Sales in USD B2CAGR

Total +4.4%

+5.6%Rest of the word +25%

+6.6%BRI3 +9%+0.5%Japan +1%

+1.6%EU53 +5%

+4.5%North America4 +44%

Contributionto growth

+6.1%China +16%

▪ The global pharma market is expected to grow with of a CAGR of +4.4% by 2024 including the impact of Covid-19, that should negatively impact volumes over 4 to 6 months in 2020 and lead to higher pressure on prices worldwide in the next 5 years

▪ EU5 countries account together for only 14% of the global pharma market (Germany: 4%, France: 3%, Italy: 3%, UK: 2% and Spain: 2%) and should see their weight drop by 2 points by 2024, due to higher price pressure than in the average of the other countries

▪ North America should continue to weigh for 43% of the global pharma market in value and contribute to 44% to worldwide market growth over the 2019 – 2024 period

July 2020Global Pharma Market & Covid-19 Impact – 2019-2024 Perspectives

475 (38%)550 (36%)

238 (19%)

310 (20%)

400 (32%)

530 (34%)138 (11%)

160 (10%)

1 250

1 550

0

200

400

600

800

1 000

1 200

1 400

1 600

2019 2024

4

1 Ex-factory price before rebates – 2 Including branded and unbranded generics and biosimilars, excluding OTC –3 Excluding biosimilars, already included in the “Generics” segment

Part A – Pharma Market Insights – 2. Size and Dynamics by Business

All the business segments of the pharma market will be affected by the Covid-19 crisis through a volume effect in 2020 and a strong price pressure over the 2019-2024 period

Global Pharma Market & Covid-19 Impact

Sources: IQVIA Institute (March 2020) – Smart Pharma Consulting estimates

Sales in USD B1

OTCs

▪ OTCs, which should remain the smallest segment of the global pharma market, has been significantly affected by the Covid-19crisis, especially during the lockdown period and the following months

▪ Generics and biosimilars should continue to grow in volume due to patents expiry, but pressure on prices should intensify on this market segment

▪ Biotech originators should become the main driver of innovation in the next 5 years

▪ Non-biotech originators should be less dynamic, but they should remain the largest segment of the global pharma market

CAGR Contributionto growth

+49%

+8%

Total

+25%Non-biotech originators +3.0%

Generics2 +43%+5.8%

Biotech originators3 +24%+5.5%

+3.1%

+3.8%

+4.4%

July 2020Global Pharma Market & Covid-19 Impact – 2019-2024 Perspectives 5

1 Including branded and unbranded generics and excluding OTC – 2 Excluding biosimilars, already includedin the “Generics” segment – 3 Earnings before interest, taxes, amortization and depreciation

Part A – Pharma Market Insights – 3. Attractiveness

By 2024, the sales growth of the pharma market should be essentially driven by generics and biotech originators, but pharma companies should lose two points of profitability

Global Pharma Market & Covid-19 Impact

Sources: IQVIA Institute (January 2019) – Smart Pharma Consulting estimates

▪ By 2024, the global pharma market should reach USD 1,550 B and grow at a pace of +4.4% per year, i.e. 1.8 point of percentage above the forecasted worldwide economic growth, but 0.6 point below the pre-Covid-19 estimates

▪ The average EBITDA of the Pharma industry should decrease from ~32% in 2019 to ~30% in 2024, mainly as a result of increasing price pressure

▪ In 2024, the average profitability of pharma companies should remain more than 4 times higher than the average of all other business sectors

▪ The biotech segment will remain very attractive but biosimilar competition will ramp up

▪ The OTC segment appears to be the least attractive

2024 estimated margin (EBITDA)3

20

19

-20

24

sal

es g

row

th (

CA

GR

)

10% 50%30% 40%

0%

8%

2024 sales in USD B

Generics1 &Biosimilars

30% for total sales

6%

2%

550(36%)

310(20%)

OTC

+4.4%4%

0%

Non-biotech originators

Biotech originators2530

(34%)

20%

160(10%)

Worldwide economic growth – CAGR 2019-2024: +2.6%

July 2020Global Pharma Market & Covid-19 Impact – 2019-2024 Perspectives 6

Part A – Pharma Market Insights – 4. Access to Market

The Covid-19 crisis will have a negative impact, irrespective of the countries, over the 2019-2024 period due to lockdown restrictions and its economic consequences

Global Pharma Market & Covid-19 Impact

Sources: Patients W.A.I.T. Indicator – EFPIA (April 2019) – Smart Pharma Consulting analyses

119146

171209 220

269288

385 395 402

486 498

612 618 634

0

100

200

300

400

500

600

700

Median time in days between marketing authorizationand price and reimbursement1,2

▪ The Covid-19 pandemics should defer the availability of new medicines in all countries, due to:– Lockdown measures having delayed the assessment of drug

registration and market access negotiations– The induced economic crisis which will lead to stricter cost

containment measures

▪ In most European countries, delays between marketing authorization and drugs availability exceed the 180 days recommended by the European Commission

▪ The UK and Germany have no delay since reimbursement and price negotiations occur once the product is in the market

▪ Delays vary widely, due to the time required to obtain their inclusion on reimbursement list and to agree on a price

▪ Delays are harmful for pharma companies which face a loss of revenues1 and patients who do not have access to innovation

▪ The slowing down of the pricing and reimbursement approval process is used by several countries to contain the cost of new drugs with a price likely to be higher than the existing ones

▪ The delay is also often due to the difficulties for the drug pricing committee and the pharma company to come to an agreement2018 analysis based on a sample of 121 products approved

by EMA (European Medicines Agency) between January 2015 and December 2017

1 Excluding early access programs for breakthrough innovations (e.g. ATU in France) –2 For drugs receiving their first marketing authorization between 2015 and 2017

July 2020Global Pharma Market & Covid-19 Impact – 2019-2024 Perspectives 7

Part A – Pharma Market Insights – 4. Access to Market

Drug price pressure imposed by public or private payers is going to intensify, more than ever, irrespective of the value created

Global Pharma Market & Covid-19 Impact

Sources: Smart Pharma Consulting analyses

▪ Strong squeezes drug (innovative, me-toos, biosimilars, generics, vaccines) prices which are likely to affect by ~2 points the average profitability of the pharma sector

▪ Value-based pricing models, incl. pay-per-performance, will become the rule, especially for innovative drugs, if the implementation is not too complex

▪ Generalization of a budget approach by disease (e.g. € 700M budgeted for antidiabetic drugs on a given year) with a mechanism of drawbacks per drug prescriber for that disease

▪ Delays in drug assessment due to lockdown (part-time activities, backlog assessment put on hold)

▪ Redirected priorities to assess technologies related to the Covid-19

▪ Price negotiations becoming tougher due to tighter budgets resulting from financial disruption, across the board

▪ Considering the anticipated worldwide financial recession, HTAs and payers should put more emphasis than ever on assessing the value of drugs for patients and healthcare systems

▪ Payers1 put in place increasingly drastic measures to control drug cost growth

▪ Drugs account for ~20% of the total healthcare costs2, but are used by payers as the main lever of cost-containment3

▪ HTA4 agencies and drug pricing committees control drug cost through:

– The definition of the target population

– The positioning of the drug in the therapy

– The price set per unit of the drug

– A capping of the drug turn-over reimbursed

▪ Progressive shift from pay-per-product topay-per-performance pricing model

2020 Impact 2021 – 2024 ImpactHistorical Trends

1 Either public or private – 2 After the OECD publication “Health at a Glance” (2019) – 3 Cost-containment measures applied to drugs are easy to implement and well accepted by citizens, unlike those applied to hospital, ambulatory care,

long-term care, which have a significant deleterious social impact (layoffs, pay cuts) – 4 Health Technology Assessment

July 2020Global Pharma Market & Covid-19 Impact – 2019-2024 Perspectives 8

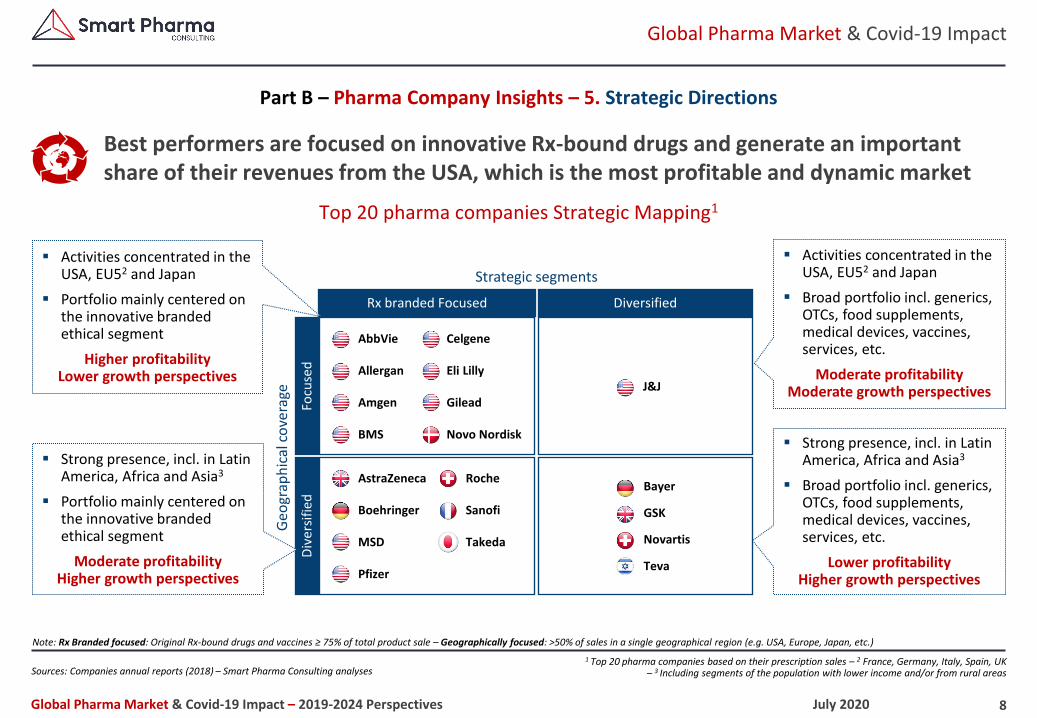

Part B – Pharma Company Insights – 5. Strategic Directions

Best performers are focused on innovative Rx-bound drugs and generate an important share of their revenues from the USA, which is the most profitable and dynamic market

Global Pharma Market & Covid-19 Impact

Sources: Companies annual reports (2018) – Smart Pharma Consulting analyses

Strategic segmentsG

eogr

aph

ical

co

vera

ge

AbbVie

Allergan

Amgen

BMS

Celgene

Eli Lilly

Gilead

Novo Nordisk

J&J

Bayer

GSK

Novartis

Teva

AstraZeneca

Boehringer

MSD

Pfizer

Roche

Sanofi

Takeda

Rx branded Focused DiversifiedFo

cuse

dD

ive

rsif

ied

Note: Rx Branded focused: Original Rx-bound drugs and vaccines ≥ 75% of total product sale – Geographically focused: >50% of sales in a single geographical region (e.g. USA, Europe, Japan, etc.)

Top 20 pharma companies Strategic Mapping1

1 Top 20 pharma companies based on their prescription sales – 2 France, Germany, Italy, Spain, UK – 3 Including segments of the population with lower income and/or from rural areas

▪ Activities concentrated in the USA, EU52 and Japan

▪ Portfolio mainly centered on the innovative branded ethical segment

Higher profitability Lower growth perspectives

▪ Activities concentrated in the USA, EU52 and Japan

▪ Broad portfolio incl. generics, OTCs, food supplements, medical devices, vaccines, services, etc.

Moderate profitability Moderate growth perspectives

▪ Strong presence, incl. in Latin America, Africa and Asia3

▪ Broad portfolio incl. generics, OTCs, food supplements, medical devices, vaccines, services, etc.

Lower profitability Higher growth perspectives

▪ Strong presence, incl. in Latin America, Africa and Asia3

▪ Portfolio mainly centered on the innovative branded ethical segment

Moderate profitability Higher growth perspectives

July 2020Global Pharma Market & Covid-19 Impact – 2019-2024 Perspectives 9

The important growth in oncology will be mainly driven by anti PD-1 products while immunosuppressants will benefit from an increased incidence of chronic diseases

Global Pharma Market & Covid-19 Impact

Sources: World Preview 2019 – Outlook to 2024 , Evaluate Pharma (June 2019) – Smart Pharma Consulting estimate

▪ The 2024 therapeutic area forecasts shows the steadily increasing weight of specialty products, sustained by the development of new biological drugs

▪ Oncology prevails as the leading therapeutic area and will be notably driven by the growth of PD-1 inhibitors

▪ Immunosuppressants will have the highest CAGR through 2024, driven by the incidence of chronic diseases and the use of immunotherapeutic agents in clinical development for other therapeutic areas

▪ Biosimilars are beginning to make their mark on the anti-rheumatic segment, which should see a decline in its CAGR despite the high drive in sales from JAK inhibitors

▪ If a vaccine and/or a treatment for the Covid-19were discovered, the Vaccines and the Anti-viralssegments could be boosted over the period

25

31

31

32

36

42

45

55

58

237

0 50 100 150 200 250

Anti-coagulants

Sensory organs

Bronchodilators

Dermatologicals

Immunosuppressants

Anti-virals

Vaccines

Anti-rheumatics

Anti-diabetics

Oncology drugs

USD B

CAGR2019-2024

+11%

+3%

-1%

+7%

+1%

+17%

+2%

+5%

+13%

+4%

2024 sales per top 10 therapeutic area

1

2

3

4

5

6

7

8

9

10

Part B – Pharma Company Insights – 6. R&D Operations

2024 Market share

19%

5%

5%

4%

4%

3%

3%

3%

3%

2%

July 2020Global Pharma Market & Covid-19 Impact – 2019-2024 Perspectives 10

1 Two articles related to the Covid-19

The Covid-19 crisis should contribute to accelerate AI use and further increase partnerships between pharma players to speed up the development of new drugs

Global Pharma Market & Covid-19 Impact

Sources: Smart Pharma Consulting analyses – Exscientia website – BenvolentAI website

Part B – Pharma Company Insights – 6. R&D Operations

▪ The value of AI to select the drugcandidates likely to have the best efficacy / safety ratio will lead to a significant increase of their use

▪ Big pharma companies will increase their partnerships with other pharma companies, with public and private research centers and data centers to improve their R&D productivity

▪ The articles1 published in the New England Journal of Medicine and the Lancet and then withdrawn due to lack of data reliability will lead much stricter peer review processes

▪ The Covid-19 pandemic appears to be a tipping point for the use of AI in accelerating the R&D timeline to find a vaccine or a treatment

▪ For example, BenvolentAI, in three days, selected six out of more than 370 drug candidates that could be active on the Covid-19, with an AI-based discovery platform

▪ The Covid-19 crisis has led numerous collaborations, as surprising as the one between the “enemy brothers”, Sanofi and GSK, to co-develop a vaccine

▪ A lot of hope has been placed in the potential contribution of Artificial Intelligence (AI) to streamline the development of drugs

▪ In January 2020, for the 1st time, the UK firm, Exscientia, managed to move a drug from the pre-clinical to the clinical stage in 12 months by using AI; which is five times less than what it would have taken without AI

▪ The use of AI can potentially accelerate timeline and reduce cost of R&D, but most pharma companies are not yet using it

2020 Impact 2021 – 2024 ImpactHistorical Trends

July 2020Global Pharma Market & Covid-19 Impact – 2019-2024 Perspectives 11

1 Contract Manufacturing Organizations – 2 For instance, Sanofi has recently announced that it will spin off its API business into a separate company by 2022 – 3 In general, to CMOs

The Covid-19 crisis might lead to relocate the manufacturing of certain essential drugs in Europe, while CMOs1 should account for ~30% of the drugs produced by the end of 2024

Global Pharma Market & Covid-19 Impact

Sources: Smart Pharma Consulting analyses – E. Wilson, NS Healthcare, May 25, 2020

Part B – Pharma Company Insights – 7. Manufacturing & Supply Chain Operations

▪ Pharma companies will keep on streamlining their manufacturing capabilities by shutting down, spinning off2 or selling plants3

▪ The outsourcing of drug production should increase from ~25% to ~30% of the volumes, over the period

▪ To de-risk the supply chain, pharma companies will favor partnerships:

– With CMOs having an internationalpresence

– With multiple CMOs in parallel

Moving from fee-for-service deals tocomplex joint ventures

▪ With China and India representing 70 to 80% of the APIs manufactured in the world, the EU, under the pressure of the German and French governments, is going to develop a plan to increase EU sovereignty on medical and pharmaceutical products

▪ If financial and regulatory incentives are introduced at the EU and/or national levels, some pharma companies may relocate certain drugs in Europe, but it is likely to be limited due to the negative impact of such a move on cost of good sold and thus on their profitability

▪ Pharma companies have tried to control or even reduce their manufacturing costs, which account for ~27% of their revenues, by implementing strategies such as:

– Relocation in low manufacturing cost countries like India or China

– Outsourcing to CMOs which are flexible and/or have specific assets and expertise (e.g. in biologicals)

‒ Shifting from conventional batch to continuous manufacturing system

‒ Digitalization of production and distribution to increase efficiency

2020 Impact 2021 – 2024 ImpactHistorical Trends

July 2020Global Pharma Market & Covid-19 Impact – 2019-2024 Perspectives 12

Medical Affairs will become, more than ever, essential to engage KOLs and other key stakeholders to take the full benefit of the products pharma companies offer

Global Pharma Market & Covid-19 Impact

Sources: Smart Pharma Consulting analyses

Part B – Pharma Company Insights – 8. Medico Marketing & Sales Operations

▪ The on-going decreasing efficacy of marketing and sales activities to engage HCPs will make Medical Affairs more and more important, to do so

▪ Medical Affairs should help key stakeholders prioritize the increasing abundance of scientific data, incl. clinical and real-world evidence data, to make better therapeutic decisions

▪ Medical Affairs, Market Access and Commercial teams should work closely and in a coordinated way to optimize the perceived value of their products

▪ The Covid-19 outbreak and the related lockdown restrictions have led to:

– Limited interactions with KOLs and other stakeholders

– Cancellations or transformations of medical meetings3 into e-meetings

– Disruptions in the recruitment and follow-up of patients in clinical studies / IISs4

▪ Interactions between Medical Affairs, KOLs and other stakeholders are progressively resuming with the lifting of the lockdown restrictions

▪ Medical Affairs operations are increasingly essential to generate and disseminate high-quality scientific data related to:

– Diseases and corresponding treatments

– Pharma company’s products

▪ Medical Affairs play a key role in engaging KOLs1 and other stakeholders2 by showing how their products improve patient outcomes with clinical and real-world evidence data

▪ They also gather information on patient unmet needs to direct the R&D

2020 Impact 2021 – 2024 ImpactHistorical Trends

1 Key Opinion Leaders – 2 Such as healthcare professionals, patient advocacy groups, health authorities, payers, etc. – 3 Congresses, symposiums, ad boards, etc. – 4 Investigator-Initiated Studies

Medical Affairs Operations

July 2020Global Pharma Market & Covid-19 Impact – 2019-2024 Perspectives 13

1 Conventional or digital, including Apps – 2 Patient Advocacy Groups – 3 Two or three months, depending on the countries – 4 See the “Brand Preference Mix” concept and tools developed by Smart Pharma Consulting: https://smart-pharma.com/wp-content/uploads/2019/07/Stakeholders-Brand-Preference-Mix-2016-EN-web.pdf

Pharma marketing strategies should, more than ever, focus on offering high-value content and building strong relationships, so that to raise HCPs preference for marketed brands

Global Pharma Market & Covid-19 Impact

Sources: Smart Pharma Consulting analyses

Part B – Pharma Company Insights – 8. Medico Marketing & Sales Operations

Marketing Operations

2020 Impact 2021 – 2024 ImpactHistorical Trends

▪ AI will be more systematically leveraged to gather actionable insights

▪ HCPs engagement will take greater account of their individual profile

▪ HCPs will require high-value marketing content and service offering, while interacting with pharma companies' collaborators

▪ The marketing battle will be focused on raising HCPs brand preference by leveraging the drug value, the quality of associated services and the corporate reputation4

▪ During the lockdown period3 and the following months, congresses and other meetings have been digitalized, postponed or even cancelled

▪ The number of commercial interactions will be lower than in 2019…

▪ … while the importance of digital channels will significantly increase vs. conventional ones

▪ Pharma companies are crafting multi-or omni-channel strategies in the hope of securing regular interactions with HCPs, across the year

▪ The number of marketing interactions per HCP has significantly decreased

▪ Marketing initiatives have become much more customer-focused, as shown by the development of services1 for:

– Institutions and HCPs to facilitate diagnosis and treatment choices

– Patients, often through PAGs2, to improve adherence, quality of life, etc.

▪ Invitations of HCPs to congresses and to other medical meetings have also significantly dropped and been even stopped by certain pharma companies

July 2020Global Pharma Market & Covid-19 Impact – 2019-2024 Perspectives 14

To positively influence HCPs, med reps should be able to carry out regular and highly valued interactions – either in-person or digital – and propose them useful services

Global Pharma Market & Covid-19 Impact

Sources: Smart Pharma Consulting analyses

Part B – Pharma Company Insights – 8. Medico Marketing & Sales Operations

Sales Operations

2020 Impact 2021 – 2024 ImpactHistorical Trends

▪ The number of interactions between HCPs and med reps (either in-person or remotely) will further decrease1

▪ To keep on interacting with HCPs, med reps have no choice but to create bespoke service-led interactions2

▪ Content communicated must be adapted to each HCP fields of interest and needs to offer him a high value

▪ Med reps should orchestrate their interactions, combining different channels, according to the content to convey and to each HCP preference

▪ During the lockdown period (~2-3 months) in-person and remote interactions between HCPs and med reps have been largely restricted

▪ 10-15% of HCPs are likely to not accept anymore calls from medical reps, following the Covid-19 crisis

▪ The proportion of remote vs. in-person calls will increase but their sum will be significantly reduced vs. previous years

▪ HCPs are more than ever expecting useful and interesting contents from medical reps

▪ Strong decrease in face-to-face interactions between HCPs and med reps (40 to 50% over the last 10 years)…

▪ … partially outweighed by virtual contacts

▪ The youngest generation of physicians(below 40-45 years old) considers medical calls (either in-person or remotely) as useless, most of the time

▪ Coordination between med reps and MSLsis increasing but remains limited, due to regulatory and compliance barriers

▪ Sales activities are mainly in-person and still very focused on quantitative aspects

1 By 30% to 40% between 2019 and 2024 – 2 See our position paper: https://smart-pharma.com/wp-content/uploads/2019/12/Service-led-Medical-Calls-VW.pdf

July 2020Global Pharma Market & Covid-19 Impact – 2019-2024 Perspectives 15

Conclusions

The Global Pharmaceutical Market will remain very attractive despite a much stronger pressure on drug prices, partly outweighed by early and broader access to patients

Global Pharma Market & Covid-19 Impact

Sources: Smart Pharma Consulting analyses

▪ Despite the Covid-19, the pharma market should increase by 4.4% p.a., on average, over the 2019-2024 period

▪ Access to high quality healthcare is the top priority of governments and citizens

▪ Boosted opportunities to discover new treatments – such as for a Covid-19 vaccine – through partnerships:

– Public-Private with academics1 or public funds2

– Private-Private with other pharma companies3

▪ Increasing price pressure on all categories of drugs (innovative or not, reimbursed or not) from public and private health insurers; and from patients for OTCs

▪ Higher risks and stricter regulations re. R&D and registrations, leading to higher costs to launch innovations

▪ Increasing difficulties to interact with healthcare professionals to inform them or create partnerships due to lack of interest and time, and regulatory constraints

1 AstraZeneca and Oxford University in the UK – 2 Sanofi and the BARDA (Biomedical Advanced Research and Development Authority) in the USA – 3 Sanofi and GSK biologicals

Global Pharma Market Perspectives 2019-2024

Market Opportunities Market Threats

Implications

▪ The Global Pharma Market will remain one of the most dynamic and profitable industrial sectors over 2019-2024, despite a decrease from 5.0% to 4.4% of its CAGR and from 32% to 30% of its profitability, due to the Covid-19 pandemic

▪ Drastic budget constraints of payers and willingness of governments to give patients, early and broad access to innovations, will lead pharma companies to accept lower prices than in the past that should be partly offset by higher volume sold

July 2020Global Pharma Market & Covid-19 Impact – 2019-2024 Perspectives 16

Conclusions

The future of pharma companies should be bright, provided they adopt a focused strategy, keep on improving their operational efficiency and design a lean organization

Global Pharma Market & Covid-19 Impact

Sources: Smart Pharma Consulting analyses

▪ Improving portfolio management with a more focused strategy on the most attractive strategic segments

▪ Breakthrough innovative drugs to come by the end of 2024

▪ Increased manufacturing efficiency with Artificial Intelligence

▪ Better clinical studies quality and development of real word evidence data contributing to optimize drugs benefits

▪ Reduction or removal of marketing and sales investments having no or limited business impact

▪ Weak negotiating power of pharma companies vs. public or private payers (e.g. HMOs in the USA)

▪ Lack of robust strategy as shown by frequent changes of priorities amongst numerous pharma companies1

▪ Rigidity and complexity of internal processes preventing pharma companies from optimally seizing opportunities and addressing threats1

▪ Underperforming marketing and sales investments

1 See the position paper “Best-in-class Pharma Strategy Crafting”: https://smart-pharma.com/wp-content/uploads/2019/07/Best-in-class-Pharma-Strategy-WFV.pdf

Global Pharma Companies Perspectives 2019-2024

Pharma Companies Strengths Pharma Companies Weaknesses

Implications

▪ R&D-based companies should focus on a limited number of attractive TAs and countries with the USA being the top priority

▪ The potential for efficiency and efficacy improvements along the value chain of pharma companies is important, especially in R&D, marketing and sales operations

▪ Pharma companies’ organizations should need to simplify their processes and become further agile

July 2020Global Pharma Market & Covid-19 Impact – 2019-2024 Perspectives

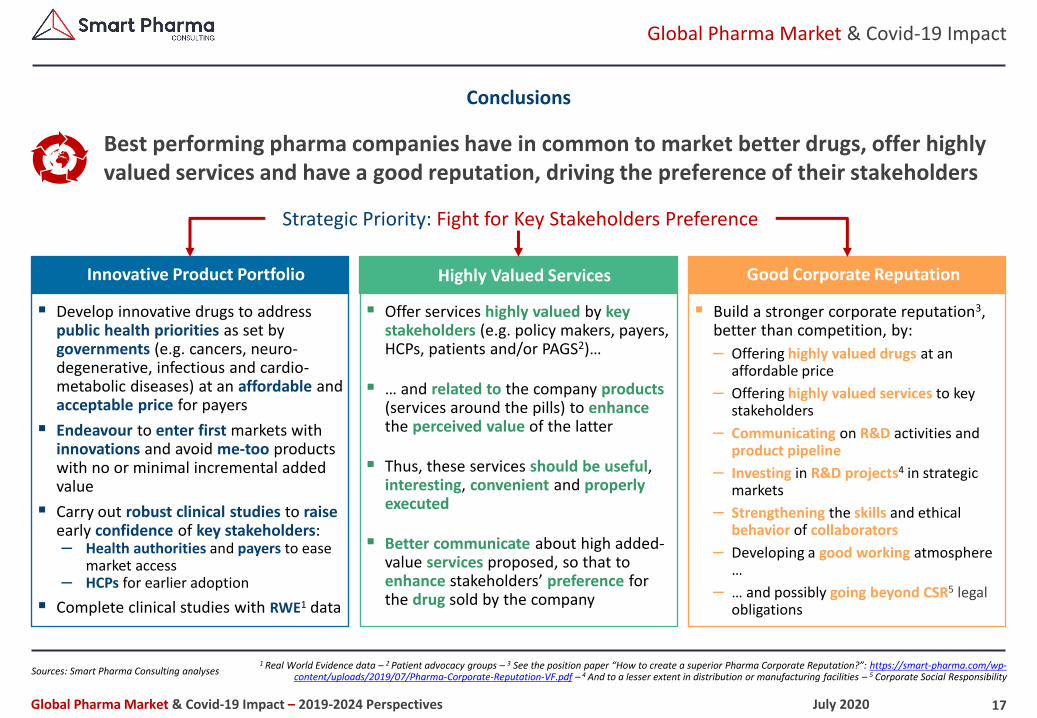

Innovative Product Portfolio Highly Valued Services Good Corporate Reputation

17

Best performing pharma companies have in common to market better drugs, offer highly valued services and have a good reputation, driving the preference of their stakeholders

Global Pharma Market & Covid-19 Impact

Sources: Smart Pharma Consulting analyses

▪ Develop innovative drugs to addresspublic health priorities as set by governments (e.g. cancers, neuro-degenerative, infectious and cardio-metabolic diseases) at an affordable and acceptable price for payers

▪ Endeavour to enter first markets with innovations and avoid me-too products with no or minimal incremental added value

▪ Carry out robust clinical studies to raiseearly confidence of key stakeholders:‒ Health authorities and payers to ease

market access‒ HCPs for earlier adoption

▪ Complete clinical studies with RWE1 data

▪ Offer services highly valued by key stakeholders (e.g. policy makers, payers, HCPs, patients and/or PAGS2)…

▪ … and related to the company products(services around the pills) to enhancethe perceived value of the latter

▪ Thus, these services should be useful, interesting, convenient and properlyexecuted

▪ Better communicate about high added-value services proposed, so that to enhance stakeholders’ preference for the drug sold by the company

▪ Build a stronger corporate reputation3, better than competition, by:

‒ Offering highly valued drugs at an affordable price

‒ Offering highly valued services to key stakeholders

‒ Communicating on R&D activities and product pipeline

‒ Investing in R&D projects4 in strategic markets

‒ Strengthening the skills and ethical behavior of collaborators

‒ Developing a good working atmosphere …

‒ … and possibly going beyond CSR5 legalobligations

Strategic Priority: Fight for Key Stakeholders Preference

1 Real World Evidence data – 2 Patient advocacy groups – 3 See the position paper “How to create a superior Pharma Corporate Reputation?”: https://smart-pharma.com/wp-content/uploads/2019/07/Pharma-Corporate-Reputation-VF.pdf – 4 And to a lesser extent in distribution or manufacturing facilities – 5 Corporate Social Responsibility

Conclusions

July 2020Global Pharma Market & Covid-19 Impact – 2019-2024 Perspectives

Consulting firm dedicated to the pharmaceutical sector operating in the complementary domains of strategy, management and organization

Smart Pharma Consulting Editions

▪ Besides our consulting activities which take 85% of our time, we are strongly engaged in sharing our knowledge and thoughts through:

– Our teaching and training activities

– The publication of articles, booklets, books and expert reports

▪ More than 80 publications, in free access, can be downloaded from our website, of which:

– 18 business reports (e.g. The French Pharma Market)

– 9 position papers in the “Best-in-Class Series”

– 14 position papers in the “Market Insights Series”

– 8 position papers in the “Smart Manager Series”

– 10 position papers in the “Smart Tool Series”

▪ Our research activities in pharma business management and our consulting activities have shown to be highly synergistic

▪ We hope that this new publication will be useful for you

▪ We remain at your disposal to carry out consulting projects or training seminars to help you improve your operations

Best regards

Jean-Michel Peny

The Market Insights Series▪ The Market Insights Series have on common to:

Be well-documented with recent facts and figures

Highlight key points to better understand the situations

Determine implications for key stakeholders

▪ Each new issue is designed to be read in 15 to 20 minutes and not to exceed 20 pages

Issue #14Global Pharma Market & Covid-19 Impact

2019-2024 Perspectives

▪ We have estimated the likely evolution of the market, following the Covid-19 crisis, through the analysis of 8 specific topics:

Part A – Pharma Market Insights1. Size and Dynamics by Geography2. Size and Dynamics by Business3. Attractiveness 4. Access to Market

Part A – Pharma Company Insights5. Strategic Directions6. R&D Operations7. Manufacturing & Supply Chain Operations8. Medico-Marketing & Sales Operations