global overview of middle distillate supply and demand · global overview of middle distillate...

TRANSCRIPT

© OECD/IEA 2014 © OECD/IEA 2014

Global Overview of Middle Distillate

Supply and Demand

19 January 2015

Matt Parry

© OECD/IEA 2014

The total medium-term supply outlook carries a premium to demand

- 1

0

1

2

3

4

5

6

7

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

mb/d

Implied spare capacity

Effective OPEC spare

capacity

World demand growth

World supply capacity

growth

Medium-term oil market balance

© OECD/IEA 2014

Oil demand nears 100 mb/d by 2019, but peak oil demand growth is in sight

Average 1.3%/yr growth on tentative macroeconomic gains

Overall progress slows on fuel switching and efficiency gains

Global oil demand 2001-07 Average Global Oil Demand Growth 2004-2009/2009-2014/2014-2019 2007-13 thousand barrels per day

2013-19

2001-07 1 102 1.3%

2007-13 727 0.8%

2013-19 1 272 1.3% Source: IEA, Medium-Term Oil Market Report 2014

This map is w ithout prejudice to the status of or sovereignty over any territory, to the delimitation of international frontiers and boundaries and to the name of any territory, city or area.

Average global demand growth

(kb/d)

28

-327

-30 39 82100

71

-91

70

127262 307

58101

170

Americas

Africa

Middle East

Europe FSU

779

700

655

Asia/Pacific

© OECD/IEA 2014

Oil’s place in the energy mix is changing

With a few exceptions, oil is being pushed out of the power generation and residential sectors

More than 5 in every 10 barrels of oil are used for transport, including 4 for road transport

Non-energy use of oil – petrochemicals – rising steeply

54.6%

54.8%

55.0%

55.2%

55.4%

55.6%

0

10

20

30

40

50

60

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

mb/

d

Shipping

Jet

Rail

Road diesel

Gasoline

Transport (rhs)

Relative share of transport use is global oil demand

© OECD/IEA 2014

Latest data shows a notable weakening in middle distillate demand

Slower gasoil demand led the global 2H13-2014 slowdown

Jet/kerosene held up better

-4%

-3%

-2%

-1%

0%

1%

2%

3%

4%

-4

-3

-2

-1

0

1

2

3

4

1Q2008 1Q2010 1Q2012 1Q2014

mb/d Global y-on-y absolute growthTotal products growth rate

LPG Naphtha GasolineJetKero Diesel RFOOther Total (RHS)

© OECD/IEA 2014

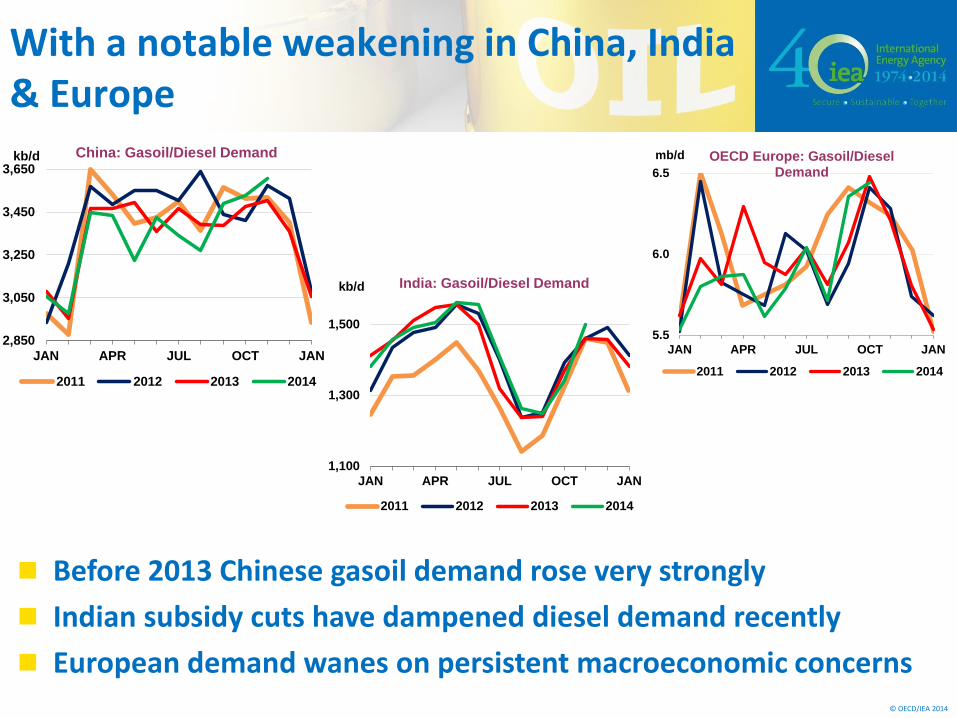

With a notable weakening in China, India & Europe

Before 2013 Chinese gasoil demand rose very strongly

Indian subsidy cuts have dampened diesel demand recently

European demand wanes on persistent macroeconomic concerns

5.5

6.0

6.5

JAN APR JUL OCT JAN

mb/d OECD Europe: Gasoil/Diesel Demand

2011 2012 2013 2014

2,850

3,050

3,250

3,450

3,650

JAN APR JUL OCT JAN

kb/d China: Gasoil/Diesel Demand

2011 2012 2013 2014

1,100

1,300

1,500

JAN APR JUL OCT JAN

kb/d India: Gasoil/Diesel Demand

2011 2012 2013 2014

© OECD/IEA 2014

…changing shipping regulations provide an additional fillip to gasoil

Tightening sulphur emission standards should encourage some product shifting

0

1 000

2 000

3 000

4 000

5 000

6 000

2007 2008 2009 2010 2011 2012 2013 2014 2015

kb/d

Marine gasoil,

domestic

navigation

Fuel oil,

domestic

navigation

Marine gasoil,

international

marine bunkers

Fuel oil,

interntaional

marine bunkers

© OECD/IEA 2014

Oil supply growth is bifurcated - robust in non-OPEC, facing headwinds in OPEC

2014 Medium-Term Outlook envisaged total oil supply capacity growth of 9 mb/d, to 105 mb/d by 2019

Strong non-OPEC growth, slowing later in the forecast period

-0.5

0.0

0.5

1.0

1.5

2.0

2013 2014 2015 2016 2017 2018 2019

mb/d

OPEC Crude capacity OPEC NGLsGlobal Biofuels Non-OPEC (excl. Biofuels)World

Global oil supply capacity growth

© OECD/IEA 2014

MENA turmoil, weak investment climate weigh on OPEC capacity growth

OPEC capacity seen growing by 2.1 mb/d to 37.1 mb/d in 2019

Iraq to supply 60% of growth

Worsening political stability and security issues add major downside risk in Iraq, Libya, others

Incremental OPEC crude production capacity 2013-19 (mb/d)

OPEC crude production capacity

32

33

34

35

36

37

38

2013 2014 2015 2016 2017 2018 2019

mb/d

Current data May 2013 -0.6 -0.4 -0.2 0.0 0.2 0.4 0.6 0.8 1.0 1.2 1.4

1

Iraq

UAE

Angola

Venezuela

Ecuador

Saudi Arabia

Iran

Qatar

Libya

Nigeria

Algeria

Kuwait

© OECD/IEA 2014

The unconventional revolution comes of age

N. America continues to lead non-OECD supply growth

But growth slows in N. America and diversifies later in the period

Annual non-OPEC supply growth

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2003 2005 2007 2009 2011 2013 2015 2017

mb/d

PG and

biofuelsOther Asia

China

Middle

EastAfrica

Latin

AmericaFSU

OECD

Pacif icOECD

EuropeOECD

AmericasTotal

© OECD/IEA 2014

NGLs, field condensate account for growing share of global supply

NGL capacity grows jumps 18% to 10.7 mb/d in 2019

OPEC NGLs rise by 13% to 7 mb/d, fuelled by quest for natural gas for utilities, water desalination and industry

Iran accounts for ~40% of OPEC NGL growth, followed by Libya, Saudi Arabia, UAE and Qatar

0

2

4

6

8

10

12

2013 2014 2015 2016 2017 2018 2019

mb/d

Pentanes

LPG

Ethane

World NGLs production

5.25

5.50

5.75

6.00

6.25

6.50

6.75

7.00

7.25

2013 2014 2015 2016 2017 2018 2019

mb/d

Current data May 2013

OPEC NGLs production

© OECD/IEA 2014

In crude trade, all roads lead to Asia

Asia imports surge 16% to more than 22 mb – 65% of the inter’l crude market – as North America swings over to net oil exporter

Crude Exports in 2019 and Growth in 2013-19 for Key Trade Routes1

(million barrels per day)

0.2 0.3

(0) 2.0 (0.2)

(-0.6) 4.1(-0.6)

0.1(-0.7)

3.1

1.2 (0.3)

1.0 (+0.1)

-0.6

2.2

1.8 (+0.8)

(-0.6)

1.1(+0.3)

Red number in brackets denotes growth in period 2013-19 1.21Excludes Intra-Regional Trade (+0.6)2 Includes Chile3 Includes Israel

5.2

(+0.3)

Other Asia

China

OECD Europe

1.6(-0.2)

1.3 (+0.6)

OECD Asia

Oceania3

0.5 (-0.0)

0.7(+0.4)

3.6 (-0.5)

OECDAmericas2

© OECD/IEA 2014

Refinery capacity growth sets stage for new round of consolidation

Almost all growth come from non-OECD, including half from Asia

Plans are getting scaled back in the face of rising over-capacity

CDU Expansions 2013-2019 by Region Refinery utilization rates

70.0%

75.0%

80.0%

85.0%

90.0%

1Q06 1Q09 1Q12 1Q15 1Q18

World OECD Non-OECD

© OECD/IEA 2014

Total Chinese product output to balance demand as projects scaled back

Apparent slowdown in gasoil demand growth sees surpluses emerging. Indeed, China turned net gasoil exporter in 2013

Chinese gasoil refinery output vs. demand Chinese refinery output vs. demand

6.0

7.0

8.0

9.0

10.0

11.0

12.0

13.0

1Q06 1Q09 1Q12 1Q15 1Q18

mb/d

Reported output Modelled output Demand

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

1Q06 1Q09 1Q12 1Q15 1Q18

mb/d

Reported output Modelled output Demand

© OECD/IEA 2014

Atlantic Basin product trade to increase

European middle distillate deficit likely balloons

US refinery industry renaissance increases export potential

OECD America’s key product balances Europe’s key product balances

-2 000

-1 500

-1 000

- 500

0

500

1 000

1 500

2008 2010 2012 2014 2016 2018

kb/d

Naphtha/gasoline Jet/gasoil

Imports

Exports

-1 000

- 500

0

500

1 000

1 500

2008 2010 2012 2014 2016 2018kb

/d

Naphtha/gasoline Jet/gasoil

Imports

© OECD/IEA 2014

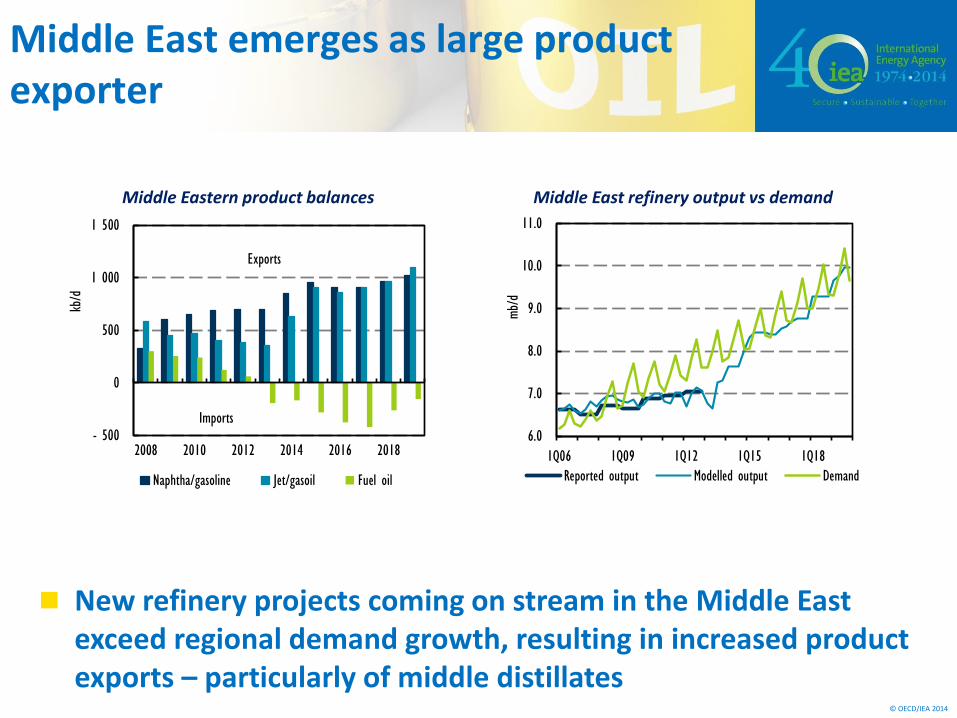

Middle East emerges as large product exporter

New refinery projects coming on stream in the Middle East exceed regional demand growth, resulting in increased product exports – particularly of middle distillates

Middle East refinery output vs demand Middle Eastern product balances

- 500

0

500

1 000

1 500

2008 2010 2012 2014 2016 2018

kb/d

Naphtha/gasoline Jet/gasoil Fuel oil

Imports

Exports

6.0

7.0

8.0

9.0

10.0

11.0

1Q06 1Q09 1Q12 1Q15 1Q18

mb/d

Reported output Modelled output Demand

© OECD/IEA 2014

Europe faces growing import dependence for middle distillates…

Europe’s middle distillate deficit balloons to 1.6 mb/d by 2019

Increased supplies coming from Middle East, N. America, Russia

Product Supply Balances - Gasoil/Kerosene

Regional Balances in 2013 and 20191

Thousand barrels per day

897 1167

FSU

-1057 -1592

Europe

9841377

OECD Americas

-559 -548

Latin America

3581094

Middle East

1280801

Asia

-657-998

Africa

Refinery production and supplies from other sources vs. end-user demand. Regional total does not add to zero due to feedstock trade and differences in product classifications.

1. Positive number indicates net-export potential, negative number net-import requirement