global mobile consumer survey 2016 the netherlands mobile consumer survey 2016 the netherlands...

TRANSCRIPT

Global Mobile Consumer Survey 2016

The Netherlands

Welcome to the Dutch edition of the 2016 Deloitte Global Mobile Consumer Survey, our research study into global mobile consumer trends. This “Dutch cut” outlines the details around connectivity, device ownership, smartphone addiction, smartphone usage and emerging technologies.

For several years now, Deloitte has researched mobile consumer behavior on a global scale, focusing on the key aspects of devices, connectivity and usage. Our research provides not only the most important insights into the state of the market, but it also reveals the most insightful developments.

So what makes Dutch consumers tick, according to this year’s “Dutch Cut”? Is it quality or price? And is SIM only penetration still spreading rapidly?

And what about device ownership? Have smartphone penetration and tablet and laptop ownership increased again? In fact, the Netherlands is among the leading countries in the field of smartphone penetration. The Dutch have even grown a little addicted to using their phones around the clock, responding to messages in the middle of the night.

The question rises what Dutch consumers use their smartphones for - for social networks, gaming, checking their e-mails, mobile banking, or all of the above? And are they prepared for a future in which connected devices –the Internet of Things – will become common usage? The answers to these questions, and more, are included in this survey.

We hope this study gives you the insight and data to enhance your understanding of the opportunities and challenges ahead, and we welcome your feedback.

3Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

Global Mobile Consumer Survey 2016

4Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

Global Mobile Consumer Survey 20165 continents, 31 countries, 53,000 respondents

The Netherlands3,000 Respondents Nationally representativeAdults 18-75 Online polling

United States

Russia

China

Indonesia

Australia

Thailand

Philippines

Colombia

Brazil

Canada

IndiaMexico

Argentina

Israel

Saudi Arabia

JapanSouth Korea

SingaporeMalaysia

France

United Kingdom Netherlands

Finland

Italy

Belgium

Sweden

Luxembourg

Norway

PolandIrelandGermany

Contents

Executive Summary 6

The Speed Game 8

Smartphone Society 24

Addiction Around The Clock 38

The Device of Unlimited Opportunities 46

The Future Starts Tomorrow (Not Today) 56

Contact 62

6Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

Executive Summary (1/2)

The Speed Game

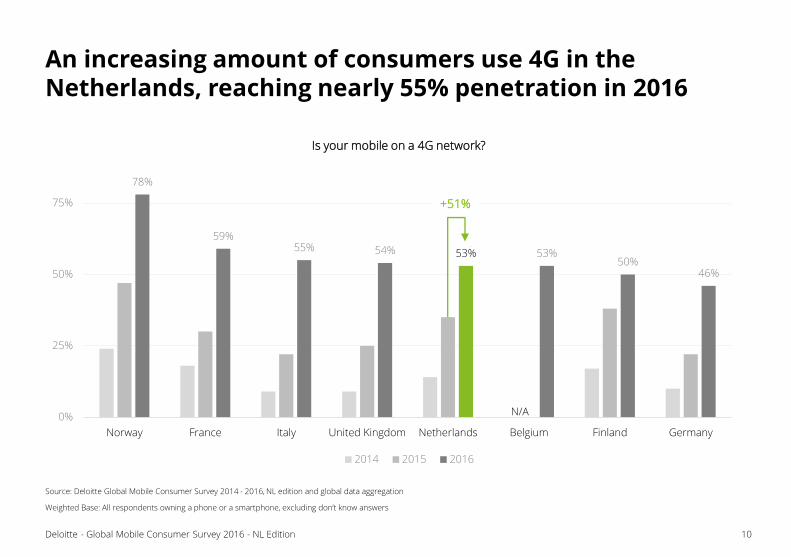

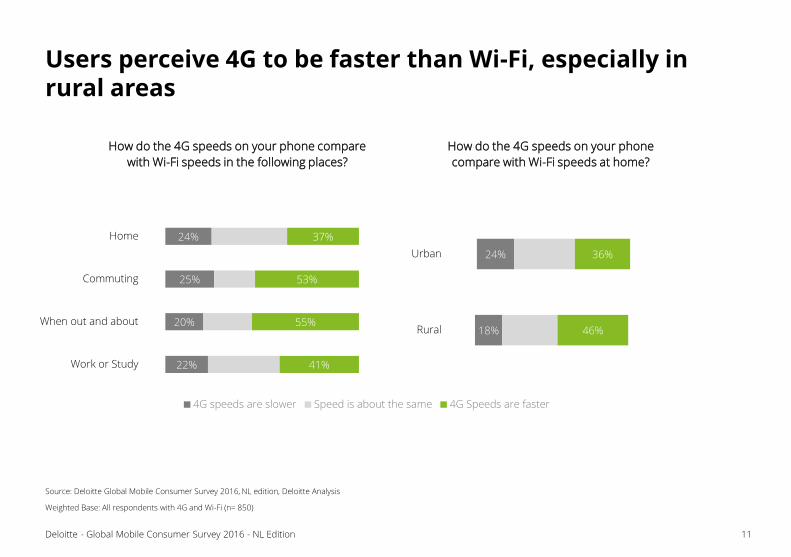

The Dutch are well connected – and they like speed. In fact, 4G technology is now used by over half of all the Dutch. Those who use 4G perceive it to be faster than Wi-Fi, especially in rural areas. They are also more likely to recommend their operator than customers on 3G technology.

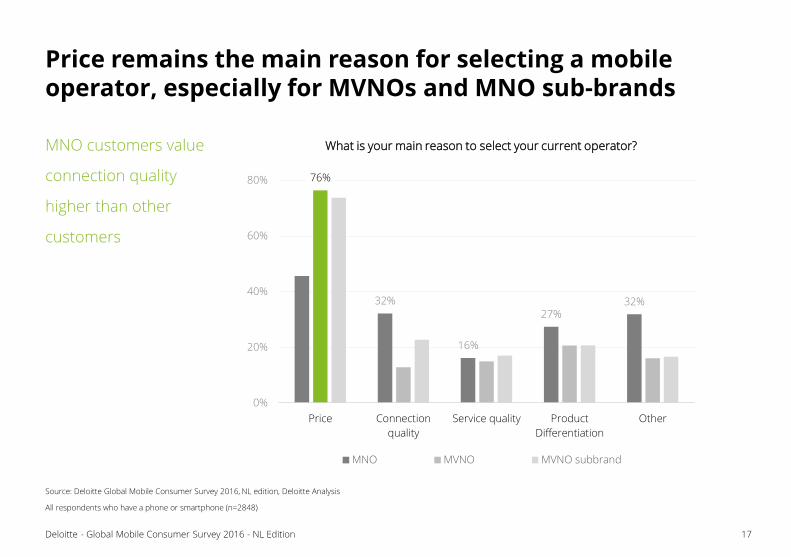

However, even though the speed and quality of a mobile connection are important to the Dutch, their most important criterion for choosing an operator remains pricing. How very Dutch. This is especially true for customers of MVNOs and MNO sub-brands. These customers are more likely to recommend their operator to others than MNO customers. A trend which is also reflected in the shift in market share. MVNOs and MNO sub-brands are gaining market share at the cost of MNOs.

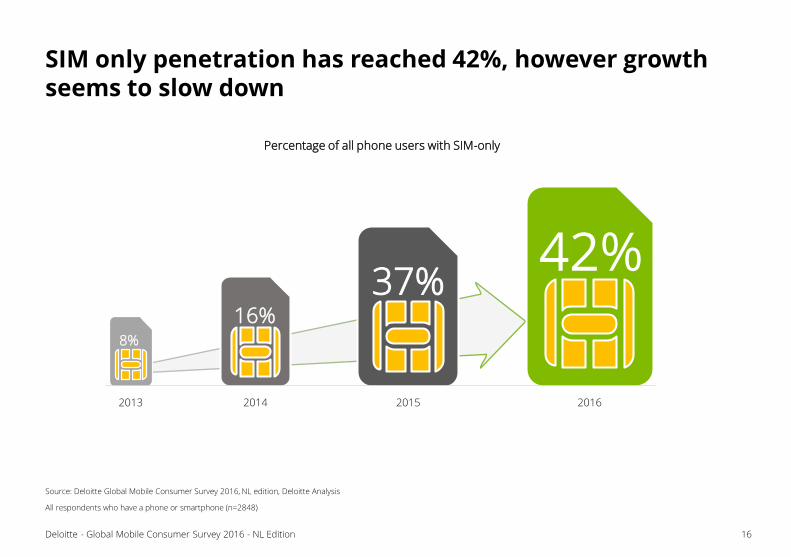

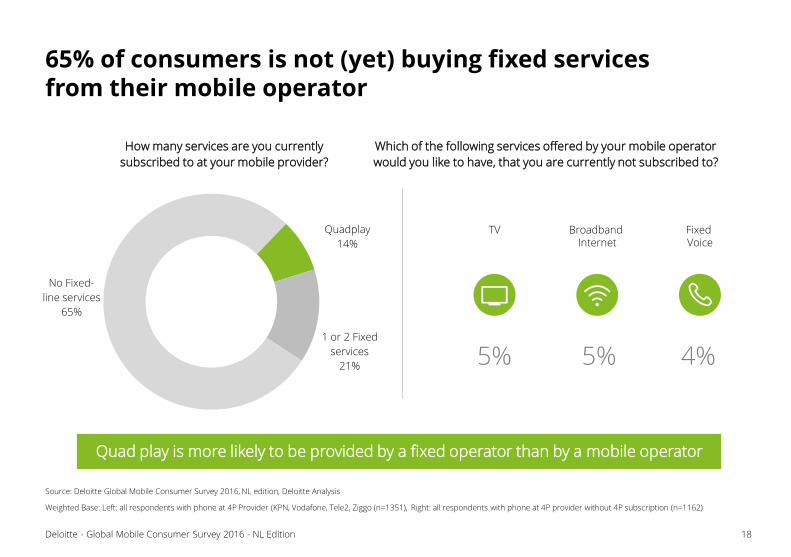

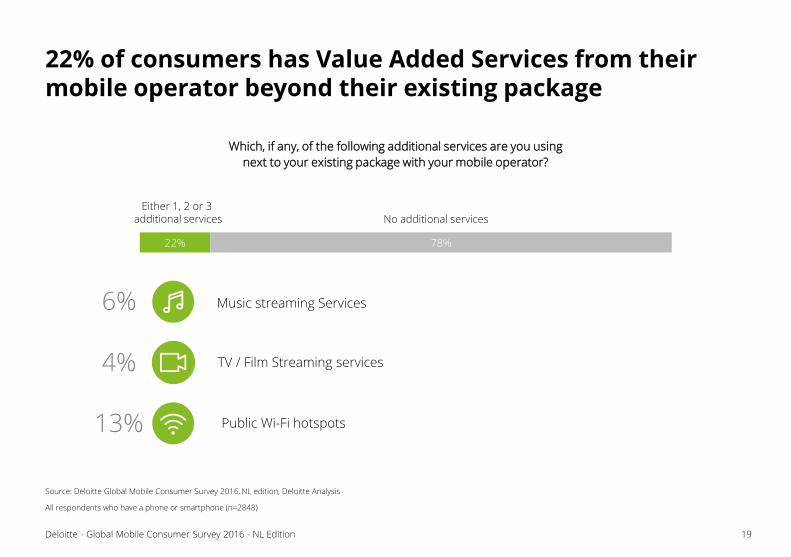

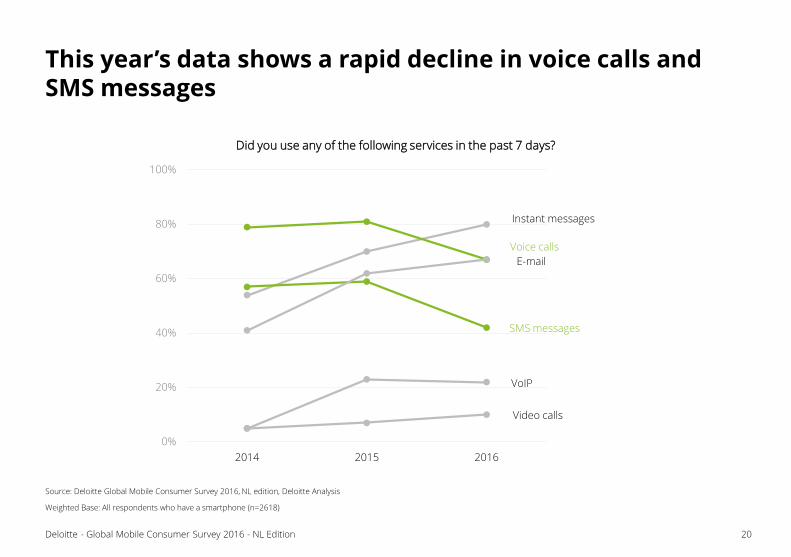

The growth of SIM only, which was significant last year, is more moderate now. Of all mobile customers, 42% is now on a SIM only contract. Consumers mainly use mobile voice and data. Interest in other services is low, with only 13% of consumers having Value Added Services (such as music streaming services) from their mobile operator and only 35% of consumers buying their fixed services. Also, voice and SMS services are rapidly declining, in favor of mobile VoIP.

Smartphone Society

The Dutch are growing more and more fond of their smartphones. In fact, the Netherlands is among the leading countries when it comes to smartphone penetration. This penetration is still increasing, mainly driven by the 19% year-on-year growth in the 55+ age segment. On the other hand, tablet and laptop ownership has stabilized.

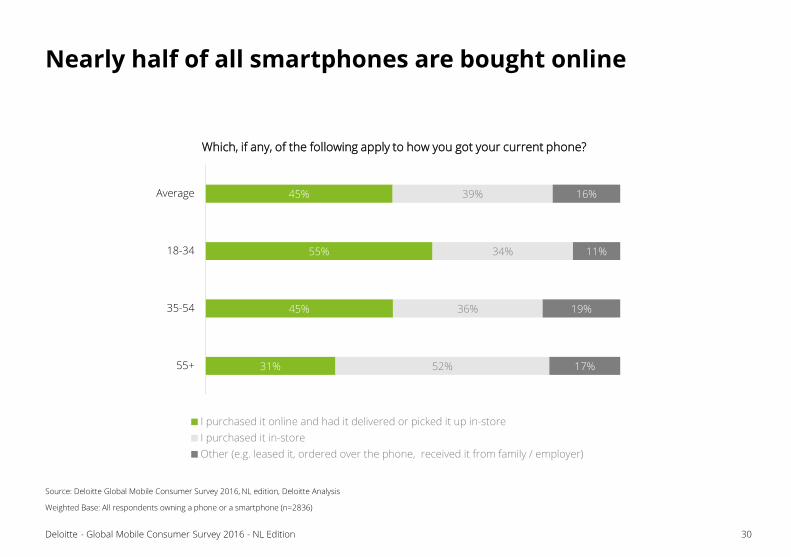

How do Dutch consumers obtain their smartphones? In nearly half the cases they purchase them online. When it comes to purchasing a brand new model, Apple users are most likely to purchase it immediately after release. Apple can also claim the highest market share in the corporate smartphone market and in brand loyalty of their customers. However, market share of new devices is still highest for Samsung, as well as the total market share.

7Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

Executive Summary (2/2)

Addiction Around The Clock

Not only has smartphone penetration increased – so has smartphone usage. Consumers prefer a tablet for most activities, but they have grown accustomed to using their phones around the clock for a variety of activities. Some of them even respond to messages in the middle of the night. 31% of all respondents have had arguments about their phone usage, especially with their significant other. Phone usage at night is highest among 18 – 24 year olds: 54% check their phone when they should be sleeping.

The Device Of Unlimited Opportunities

One of the activities for which smartphones are used, is sharing and recording photos and videos, especially when consumers have access to 4G technology. Also, smartphones are preferred for social networking – and increasingly for mobile banking. When it comes to commercial activities, consumers mostly surf shopping sites and pay for products on smartphones. 43% of respondents have used their phone to transfer money to another individual. In fact, the Netherlands has become one of the leading countries in the field of mobile banking. However, security is still an issue, with 26% of people not having a security measure in place to lock their phone. Fingerprint readers are used by 68% of consumers who have one on their phone.

The Future Starts Tomorrow (Not Today)

When it comes to technologies such as the Internet of Things, consumers seem a little cautious. Connected devices are still a niche market for consumers. Even though 50% has a connected device, these are mostly entertainment products and only 10% considers to purchase connected products in the coming year. Virtual Reality device adoption is also low, especially considering the amount of low-end, cardboard, products. Apparently, the future starts tomorrow for most consumers - not today.

The Speed Game

The name of the game is speed, and this seems especially

true for smartphone users. This year, adoption of 4G has

reached nearly 55%. Even though this is an increase of 51%

since last year, the Netherlands lost its top 3 position in

Europe in terms of adoption. Our analysis shows that

consumers also perceive 4G to be faster than Wi-Fi, whether

they are out and about or at home. We see that this

perception of speed is especially higher in rural areas. The

perception and availability of speed is also reflected in

operator appreciation, as consumers with a 4G connection

tend to give their mobile operator a higher Net Promoter

Score (NPS) than 3G users. When looking at operators’ NPS,

our research shows that consumers score MVNOs higher

than MNOs or their sub-brands.

Similar to last year, MNOs continue to lose market share,

predominantly to their sub-brands. We see that SIM only

penetration continues to grow for the third year in a row,

although growth seems to slow down this year. Our research

also shows that consumers’ choice for an operator is still

mainly driven by price. Even though this is especially true for

MVNO and MNO sub-brand subscribers, price is also an

important consideration for MNO subscribers, next to a good

connection quality and sufficient product differentiation.

This year’s research also shows a decline in consumers’ use

of traditional telecommunication services such as traditional

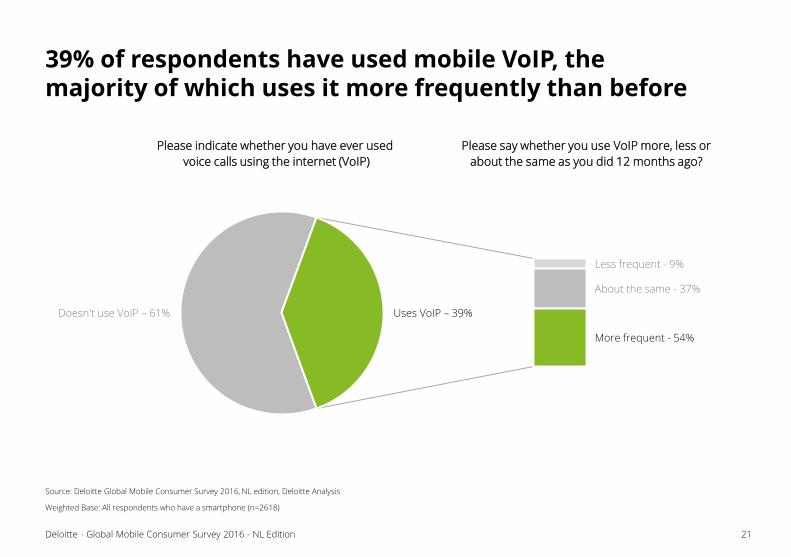

voice and SMS. As much as 39% of respondents indicate that

they have used mobile VoIP and the majority of this group is

using VoIP more often than before. Furthermore, instant

messages and e-mail are still growing, though growth seems

to slow down. Looking at online preferred communications

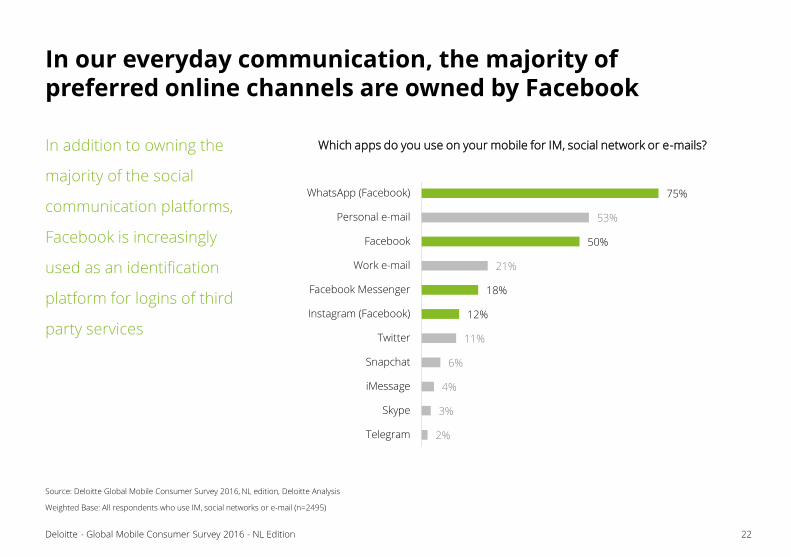

services, analysis shows that two-thirds of our top 6 channels

are owned by Facebook.

78%

59%55% 54% 53% 53%

50%46%

0%

25%

50%

75%

Norway France Italy United Kingdom Netherlands Belgium Finland Germany

2014 2015 2016

.

10Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

An increasing amount of consumers use 4G in the Netherlands, reaching nearly 55% penetration in 2016

Source: Deloitte Global Mobile Consumer Survey 2014 - 2016, NL edition and global data aggregation

Weighted Base: All respondents owning a phone or a smartphone, excluding don’t know answers

Is your mobile on a 4G network?

.

+51%

N/A

11Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

Users perceive 4G to be faster than Wi-Fi, especially in rural areas

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition, Deloitte Analysis

Weighted Base: All respondents with 4G and Wi-Fi (n= 850)

22%

20%

25%

24%

41%

55%

53%

37%

Work or Study

When out and about

Commuting

Home

4G speeds are slower Speed is about the same 4G Speeds are faster

How do the 4G speeds on your phone compare

with Wi-Fi speeds in the following places?

18%

24%

46%

36%

Rural

Urban

How do the 4G speeds on your phone

compare with Wi-Fi speeds at home?

12Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

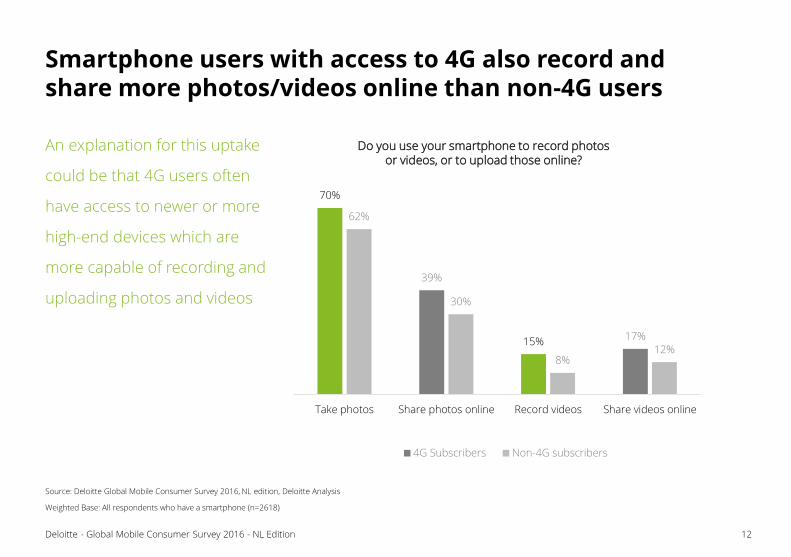

Smartphone users with access to 4G also record and share more photos/videos online than non-4G users

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition, Deloitte Analysis

Weighted Base: All respondents who have a smartphone (n=2618)

70%

39%

15% 17%

62%

30%

8%12%

Take photos Share photos online Record videos Share videos online

4G Subscribers Non-4G subscribers

An explanation for this uptake

could be that 4G users often

have access to newer or more

high-end devices which are

more capable of recording and

uploading photos and videos

Do you use your smartphone to record photos or videos, or to upload those online?

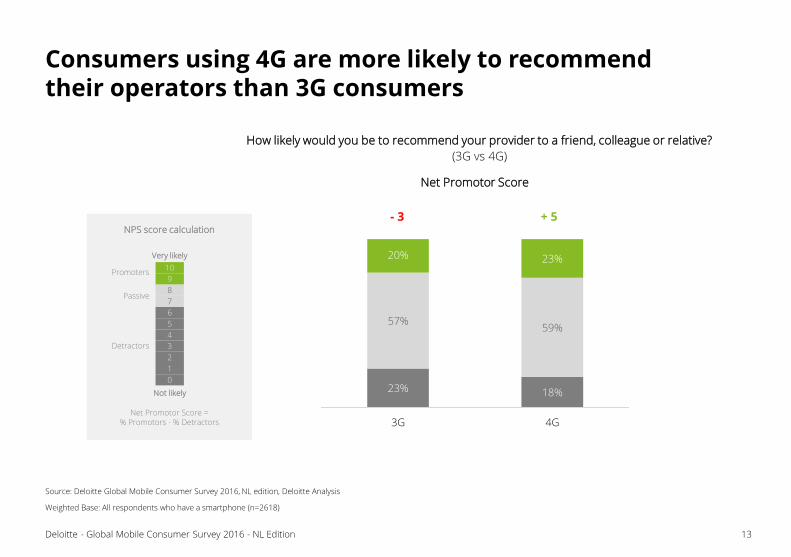

NPS score calculation

Passive

Detractors

Promoters

Very likely

Not likely

Net Promotor Score =% Promotors - % Detractors

13Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

Consumers using 4G are more likely to recommend their operators than 3G consumers

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition, Deloitte Analysis

Weighted Base: All respondents who have a smartphone (n=2618)

10

9

8

7

6

5

4

3

2

1

0

How likely would you be to recommend your provider to a friend, colleague or relative?

(3G vs 4G)

23% 18%

57%59%

20% 23%

3G 4G

+ 5- 3

Net Promotor Score

14Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

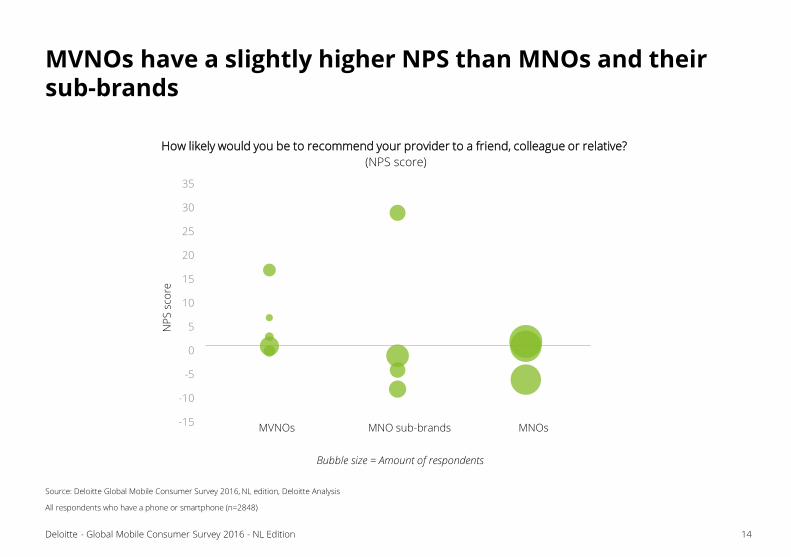

MVNOs have a slightly higher NPS than MNOs and their sub-brands

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition, Deloitte Analysis

All respondents who have a phone or smartphone (n=2848)

-15

-10

-5

0

5

10

15

20

25

30

35

MVNOs MNO sub-brands MNOs

NP

S s

core

How likely would you be to recommend your provider to a friend, colleague or relative?

(NPS score)

Bubble size = Amount of respondents

15Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

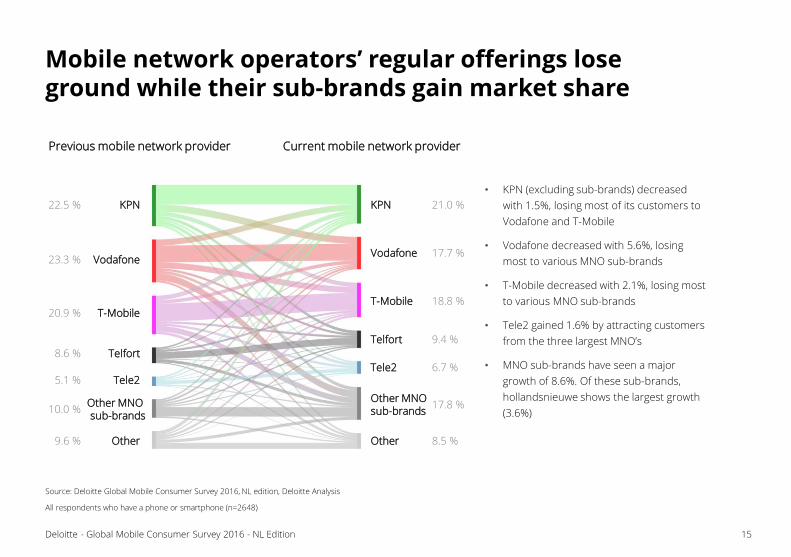

Mobile network operators’ regular offerings lose ground while their sub-brands gain market share

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition, Deloitte Analysis

All respondents who have a phone or smartphone (n=2648)

KPN 21.0 %KPN22.5 %

Vodafone 17.7 %Vodafone23.3 %

T-Mobile 18.8 %T-Mobile20.9 %

Tele2 6.7 %Tele25.1 %

Telfort 9.4 %

Telfort8.6 %

Other 8.5 %Other9.6 %

Other MNO sub-brands

17.8 %Other MNO sub-brands

10.0 %

Previous mobile network provider Current mobile network provider

• KPN (excluding sub-brands) decreased

with 1.5%, losing most of its customers to

Vodafone and T-Mobile

• Vodafone decreased with 5.6%, losing

most to various MNO sub-brands

• T-Mobile decreased with 2.1%, losing most

to various MNO sub-brands

• Tele2 gained 1.6% by attracting customers

from the three largest MNO’s

• MNO sub-brands have seen a major

growth of 8.6%. Of these sub-brands,

hollandsnieuwe shows the largest growth

(3.6%)

16Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

SIM only penetration has reached 42%, however growth seems to slow down

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition, Deloitte Analysis

All respondents who have a phone or smartphone (n=2848)

2014

16%

2013

8%

2015

42%

2016

Percentage of all phone users with SIM-only

37%

17Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

Price remains the main reason for selecting a mobile operator, especially for MVNOs and MNO sub-brands

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition, Deloitte Analysis

All respondents who have a phone or smartphone (n=2848)

32%

16%

27%32%

76%

0%

20%

40%

60%

80%

Price Connection

quality

Service quality Product

Differentiation

Other

What is your main reason to select your current operator?

MNO MVNO MVNO subbrand

MNO customers value

connection quality

higher than other

customers

18Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

65% of consumers is not (yet) buying fixed services from their mobile operator

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition, Deloitte Analysis

Weighted Base: Left: all respondents with phone at 4P Provider (KPN, Vodafone, Tele2, Ziggo (n=1351), Right: all respondents with phone at 4P provider without 4P subscription (n=1162)

No Fixed-

line services

65%

Quadplay

14%

1 or 2 Fixed

services

21%

Broadband Internet

5%

TV

5%

Fixed Voice

4%

Which of the following services offered by your mobile operator

would you like to have, that you are currently not subscribed to?

Quad play is more likely to be provided by a fixed operator than by a mobile operator

How many services are you currently

subscribed to at your mobile provider?

19Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

22% of consumers has Value Added Services from their mobile operator beyond their existing package

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition, Deloitte Analysis

All respondents who have a phone or smartphone (n=2848)

22% 78%

TV / Film Streaming services4%

Music streaming Services6%

Public Wi-Fi hotspots13%

Which, if any, of the following additional services are you using

next to your existing package with your mobile operator?

Either 1, 2 or 3 additional services No additional services

20Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

This year’s data shows a rapid decline in voice calls and SMS messages

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition, Deloitte Analysis

Weighted Base: All respondents who have a smartphone (n=2618)

Instant messages

Video calls

Voice calls

SMS messages

VoIP

0%

20%

40%

60%

80%

100%

2014 2015 2016

Did you use any of the following services in the past 7 days?

Doesn't use VoIP – 61%

Less frequent - 9%

About the same - 37%

More frequent - 54%

Uses VoIP – 39%

21Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

39% of respondents have used mobile VoIP, the majority of which uses it more frequently than before

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition, Deloitte Analysis

Weighted Base: All respondents who have a smartphone (n=2618)

Please indicate whether you have ever used

voice calls using the internet (VoIP)

Please say whether you use VoIP more, less or

about the same as you did 12 months ago?

22Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

In our everyday communication, the majority of preferred online channels are owned by Facebook

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition, Deloitte Analysis

Weighted Base: All respondents who use IM, social networks or e-mail (n=2495)

2%

3%

4%

6%

11%

12%

18%

21%

50%

53%

75%

Telegram

Skype

iMessage

Snapchat

Instagram (Facebook)

Facebook Messenger

Work e-mail

Personal e-mail

WhatsApp (Facebook)

Which apps do you use on your mobile for IM, social network or e-mails?In addition to owning the

majority of the social

communication platforms,

Facebook is increasingly

used as an identification

platform for logins of third

party services

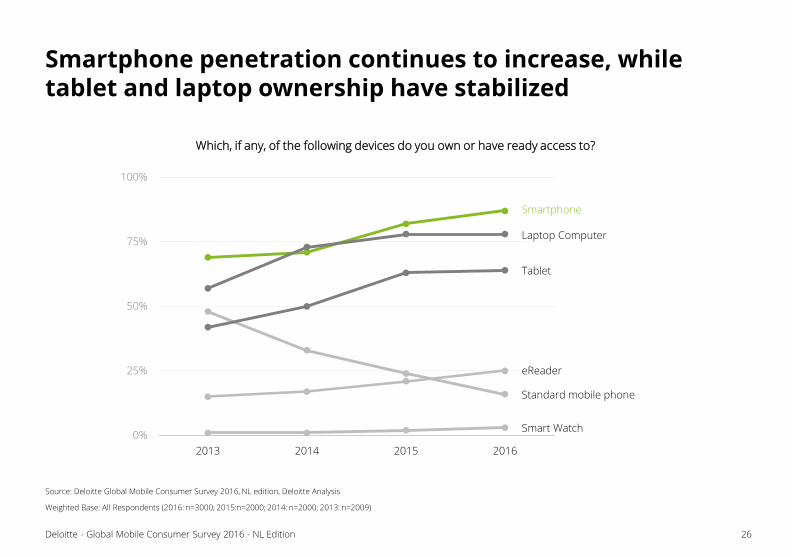

Smartphone Society

For years, smartphones have been steadily replacing our

former regular or ‘dumb’ phones. Even though this adoption is

still growing, we are now slowly seeing a plateau for

smartphone ownership. This stabilization is already seen with

tablets and laptops, the growth of which has come to a halt.

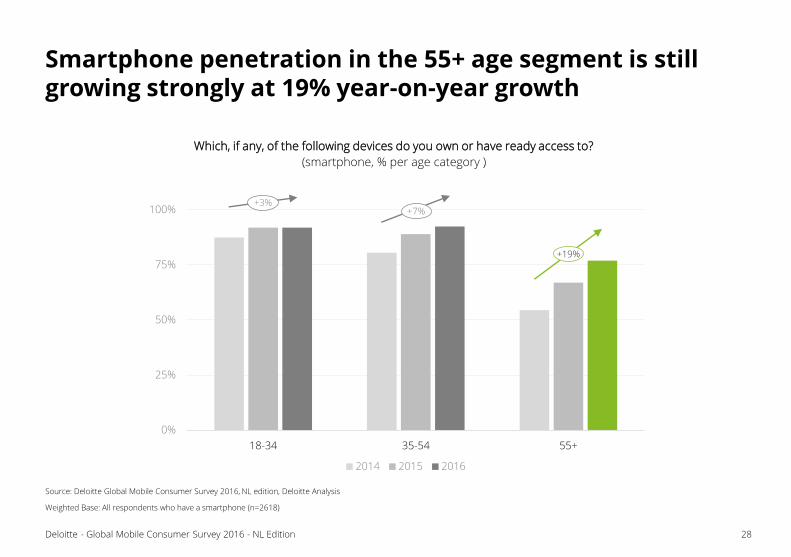

Whilst a high smartphone adoption among younger age

segments was already a fact, older generations have been

quickly catching up during the last few years. This year we see

that trend continuing with a 19% year-on-year growth over the

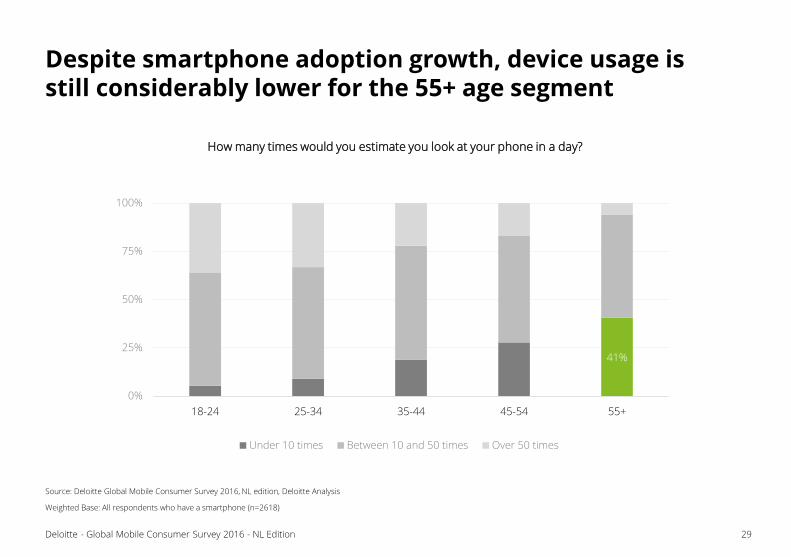

last 2 years. However, when looking at device usage, this age

group still has a lot of catching up to do. Over 40% uses their

smartphone less than 10 times a day.

Naturally we also further analyzed the smartphone market. We

noticed that today, almost half of all smartphones is purchased

online. As one might expect, this is mostly true for younger

people and applies less to older generations. As in last year’s

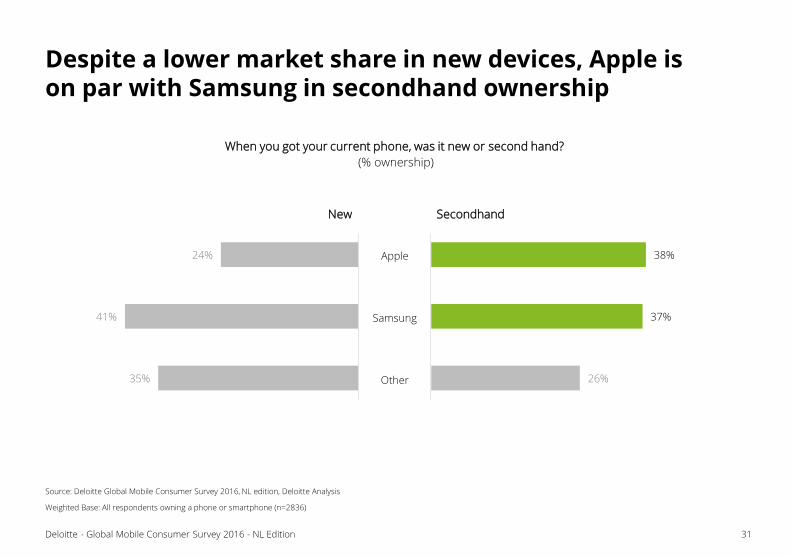

survey, we also looked into the 2nd hand market. We see that

Apple and Samsung are equally dominating this market, with a

joint market share of just under 80%. Looking at newly

purchased devices, Samsung clearly has the biggest market

share with 41%.

We also see that Apple users are most keen on buying the

latest device. They are also still most loyal to the brand and

their brand was rated with the highest net promoter score

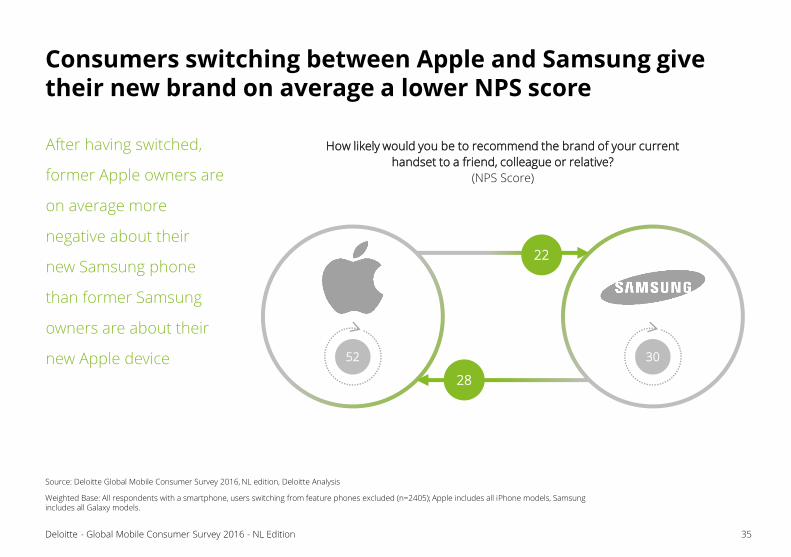

(NPS). On average, consumers give their new brand a lower

NPS than their previous brand after having switched from

Apple to Samsung or vice versa.

This year we also investigated the balance between consumer

and corporate device ownership. We see that whilst Samsung is

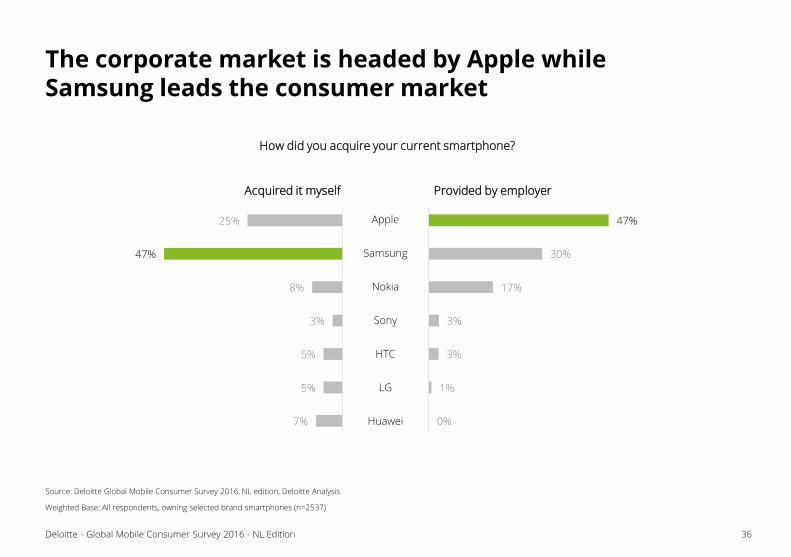

dominating private ownership, Apple is clearly leading when it

comes to smartphones provided by employers.

26Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

Smartphone penetration continues to increase, while tablet and laptop ownership have stabilized

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition, Deloitte Analysis

Weighted Base: All Respondents (2016: n=3000; 2015:n=2000; 2014: n=2000; 2013: n=2009)

Which, if any, of the following devices do you own or have ready access to?

0%

25%

50%

75%

100%

2013 2014 2015 2016

Standard mobile phone

eReader

Tablet

Laptop Computer

Smartphone

Smart Watch

27Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

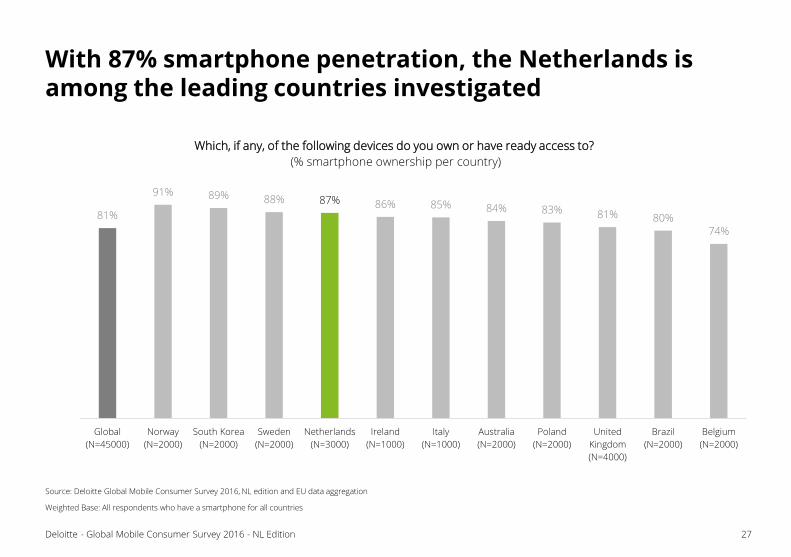

With 87% smartphone penetration, the Netherlands is among the leading countries investigated

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition and EU data aggregation

Weighted Base: All respondents who have a smartphone for all countries

Which, if any, of the following devices do you own or have ready access to?

(% smartphone ownership per country)

81%

91% 89% 88% 87% 86% 85% 84% 83% 81% 80%74%

Global

(N=45000)

Norway

(N=2000)

South Korea

(N=2000)

Sweden

(N=2000)

Netherlands

(N=3000)

Ireland

(N=1000)

Italy

(N=1000)

Australia

(N=2000)

Poland

(N=2000)

United

Kingdom

(N=4000)

Brazil

(N=2000)

Belgium

(N=2000)

0%

25%

50%

75%

100%

18-34 35-54 55+

2014 2015 2016

28Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

Smartphone penetration in the 55+ age segment is still growing strongly at 19% year-on-year growth

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition, Deloitte Analysis

Weighted Base: All respondents who have a smartphone (n=2618)

Which, if any, of the following devices do you own or have ready access to?

(smartphone, % per age category )

+3%+7%

+19%

29Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

Despite smartphone adoption growth, device usage is still considerably lower for the 55+ age segment

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition, Deloitte Analysis

Weighted Base: All respondents who have a smartphone (n=2618)

41%

0%

25%

50%

75%

100%

18-24 25-34 35-44 45-54 55+

Under 10 times Between 10 and 50 times Over 50 times

How many times would you estimate you look at your phone in a day?

30Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

Nearly half of all smartphones are bought online

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition, Deloitte Analysis

Weighted Base: All respondents owning a phone or a smartphone (n=2836)

31%

45%

55%

45%

52%

36%

34%

39%

17%

19%

11%

16%

55+

35-54

18-34

Average

I purchased it online and had it delivered or picked it up in-store

I purchased it in-store

Other (e.g. leased it, ordered over the phone, received it from family / employer)

Which, if any, of the following apply to how you got your current phone?

31Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

Despite a lower market share in new devices, Apple is on par with Samsung in secondhand ownership

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition, Deloitte Analysis

Weighted Base: All respondents owning a phone or smartphone (n=2836)

When you got your current phone, was it new or second hand?

(% ownership)

35%

41%

24%

New

26%

37%

38%

Secondhand

Apple

Samsung

Other

32Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

Apple users are most likely to buy the latest model directly when, or soon after it is launched

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition, Deloitte Analysis

Weighted Base: All respondents, with a smartphone (n=2616)

42%

26%

28%

31%

14%

26%

Apple

Samsung

Nokia

Sony

Huawei

LG

I buy the latest devices as soon

as they enter the market

I tend to buy the latest devices if I

really like them

I buy devices after they've been

out for a while

I only replace devices when they

go wrong or are broken

Don't know

Which of the following best describes your attitude towards new devices?

(%)

33Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

Apple has the highest Net Promoter Score of all smartphone manufacturers

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition, Deloitte Analysis

Weighted Base: All respondents who have a smartphone(n=2618); Apple includes all iPhone models, Samsung includes all Galaxy models

1 https://www.thestreet.com/story/13095775/1/blackberry--who-knew--wins-most-improved-from-us-consumers.html

-10

9

11

16

20

24

40

LG

Huawei

HTC

Nokia

Sony

Samsung

Apple

How likely would you be to recommend the brand of your current handset

to a friend, colleague or relative?

(NPS Score)

Dutch consumers rate

their devices lower

compared to UK and US

consumers1: Apple has a

NPS of 63 in the US and

46 in the UK

34Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

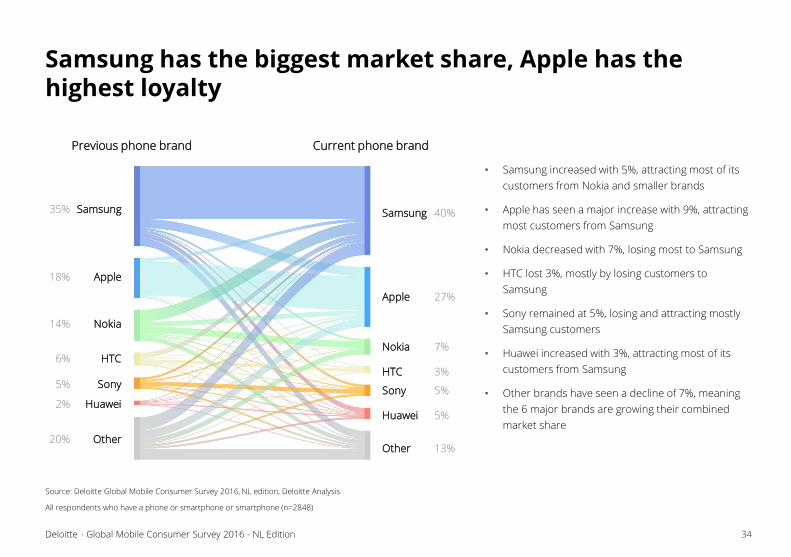

Samsung has the biggest market share, Apple has the highest loyalty

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition, Deloitte Analysis

All respondents who have a phone or smartphone or smartphone (n=2848)

Samsung35% Samsung 40%

Nokia14%

Nokia 7%

Apple18%

Apple 27%

HTC6%HTC 3%

Sony5%Sony 5%

Huawei2%Huawei 5%

Other20%Other 13%

Previous phone brand Current phone brand

• Samsung increased with 5%, attracting most of its

customers from Nokia and smaller brands

• Apple has seen a major increase with 9%, attracting

most customers from Samsung

• Nokia decreased with 7%, losing most to Samsung

• HTC lost 3%, mostly by losing customers to

Samsung

• Sony remained at 5%, losing and attracting mostly

Samsung customers

• Huawei increased with 3%, attracting most of its

customers from Samsung

• Other brands have seen a decline of 7%, meaning

the 6 major brands are growing their combined

market share

35Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

Consumers switching between Apple and Samsung give their new brand on average a lower NPS score

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition, Deloitte Analysis

Weighted Base: All respondents with a smartphone, users switching from feature phones excluded (n=2405); Apple includes all iPhone models, Samsung includes all Galaxy models.

After having switched,

former Apple owners are

on average more

negative about their

new Samsung phone

than former Samsung

owners are about their

new Apple device

22

28

52 30

How likely would you be to recommend the brand of your current

handset to a friend, colleague or relative?

(NPS Score)

36Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

The corporate market is headed by Apple while Samsung leads the consumer market

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition, Deloitte Analysis

Weighted Base: All respondents, owning selected brand smartphones (n=2537)

7%

5%

5%

3%

8%

47%

25%

Acquired it myself

0%

1%

3%

3%

17%

30%

47%

Provided by employer

How did you acquire your current smartphone?

Apple

Samsung

Nokia

Sony

HTC

LG

Huawei

Addiction around the clock

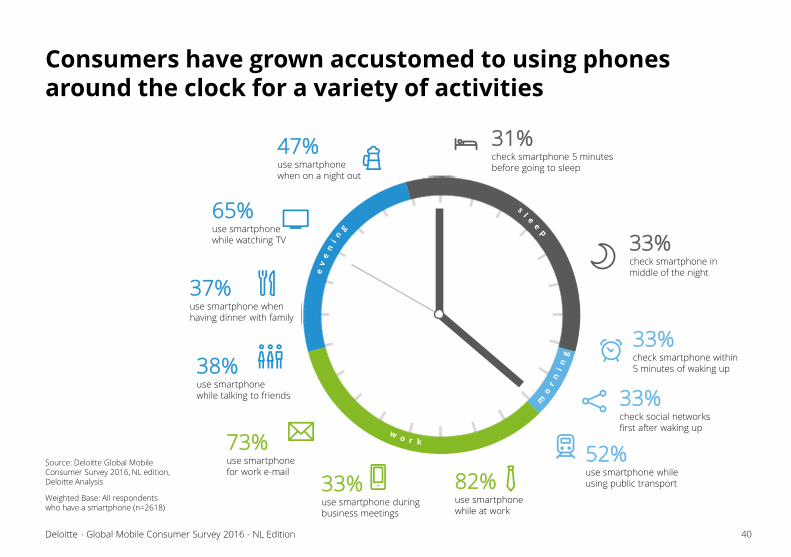

The high adoption of smartphones and their wide array of

functionalities is also reflected in our daily use. Consumers

nowadays use their smartphones practically anytime and for

anything. Whether it is in the morning, right after we wake up

or when we want to check our missed messages, or during

the day, during meetings at the office or when we want to

check our work e-mail. After work, we further pick up our

smartphone activity when meeting up with friends and family.

As much as 65% of consumers also uses their smartphone

when watching television.

This non-stop around the clock use also leads to arguments

with our family. At least 31% of respondents indicated that

they have had at least one argument about their smartphone

usage.

Even during the night, consumers do not cease their

smartphone activities. Our analysis shows that 33% of

respondents also use their smartphone in the middle of the

night.

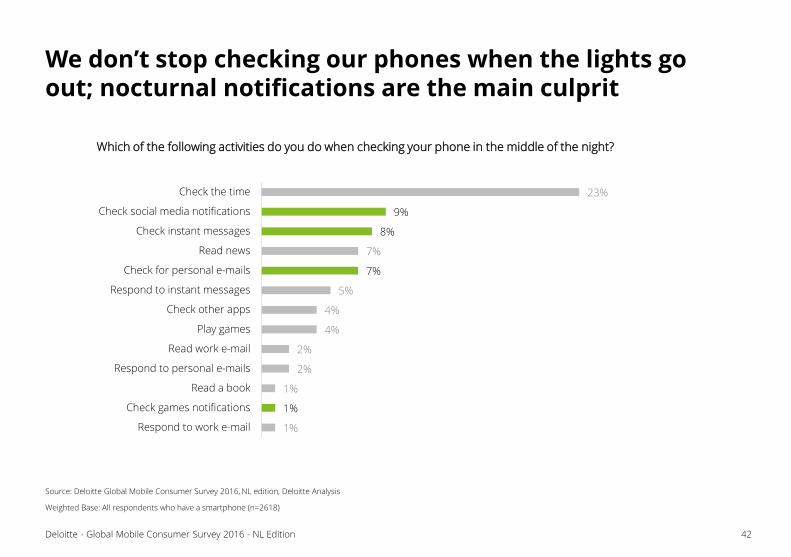

Consumers use their smartphone at night for a wide array of

activities. Most of them, almost a quarter, say they use their

phone to check the time. Some use it to read a book or to

play a game. However we see that the most notable nightly

activities are usually related to (social) interactions.

Nocturnal use is especially high among younger generations.

Over 54% in the age segment of 18 to 24 say they check their

phone in the middle of the night. Of that group, 15% also

replies to messages in the middle of the night.

40Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

Consumers have grown accustomed to using phones around the clock for a variety of activities

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition, Deloitte Analysis

Weighted Base: All respondents who have a smartphone (n=2618)

31% check smartphone 5 minutes before going to sleep

33% check smartphone inmiddle of the night

33% check smartphone within 5 minutes of waking up

52% use smartphone while using public transport33%

use smartphone during business meetings

82% use smartphone while at work

73% use smartphone for work e-mail

38% use smartphone while talking to friends

37% use smartphone when having dinner with family

65% use smartphone while watching TV

47% use smartphonewhen on a night out

33% check social networksfirst after waking up

41Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

31% of respondents have argued about phone usage with relatives, especially with their significant other

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition, Deloitte Analysis

All respondents who have a phone or smartphone or smartphone (n=2848)

8%

8%

10%

12%

14%

24%

Children

Grandparents

Siblings

Housemates or friends

Parents

Spouse

31%

69%

Have you ever had arguments with relatives about your mobile phone use?

Do you have disagreements with one of the following people about your mobile phone use?

(% of respondents that have arguments)

42Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

We don’t stop checking our phones when the lights go out; nocturnal notifications are the main culprit

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition, Deloitte Analysis

Weighted Base: All respondents who have a smartphone (n=2618)

1%

1%

1%

2%

2%

4%

4%

5%

7%

7%

8%

9%

23%

Respond to work e-mail

Check games notifications

Read a book

Respond to personal e-mails

Read work e-mail

Play games

Check other apps

Respond to instant messages

Check for personal e-mails

Read news

Check instant messages

Check social media notifications

Check the time

Which of the following activities do you do when checking your phone in the middle of the night?

43Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

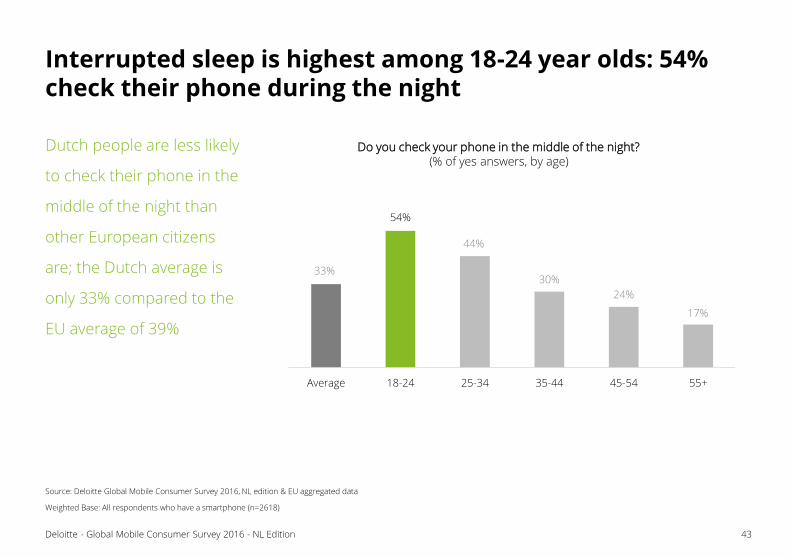

Interrupted sleep is highest among 18-24 year olds: 54% check their phone during the night

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition & EU aggregated data

Weighted Base: All respondents who have a smartphone (n=2618)

33%

54%

44%

30%

24%

17%

Average 18-24 25-34 35-44 45-54 55+

Dutch people are less likely

to check their phone in the

middle of the night than

other European citizens

are; the Dutch average is

only 33% compared to the

EU average of 39%

Do you check your phone in the middle of the night? (% of yes answers, by age)

44Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

A part of these interrupted sleepers even replies to messages in the middle of the night

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition, Deloitte Analysis

Weighted Base: All respondents who have a smartphone (n=2618)

15%

33%

54%

44%

30%

24%

17%

Average 18-24 25-34 35-44 45-54 55+

Responds to instant messages in the middle of the night

When checking your phone in the middle of the night, do you also respond to instant messages?

(by age)

The device of unlimited opportunities

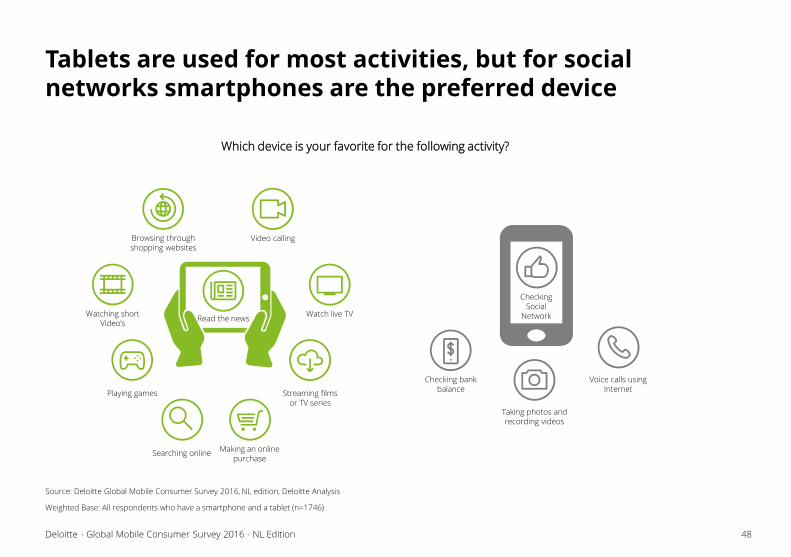

Previous chapters show that consumers have access to a

range of mobile devices and like to use these devices for a

variety of activities throughout the day. Our analysis shows

that consumers prefer to use a tablet when it comes to

everyday activities such as watching TV or videos, playing

games and searching or shopping online. However, when it

comes to checking social networks, using VoIP or taking

pictures, consumers have a strong preference for using their

smartphone.

Our research also focused on consumers’ preference for an

app or browser when it comes to online activities. We see

that consumers usually prefer to use an app, except when

they are making travel arrangements or doing online

shopping. In those cases, they prefer to use a browser.

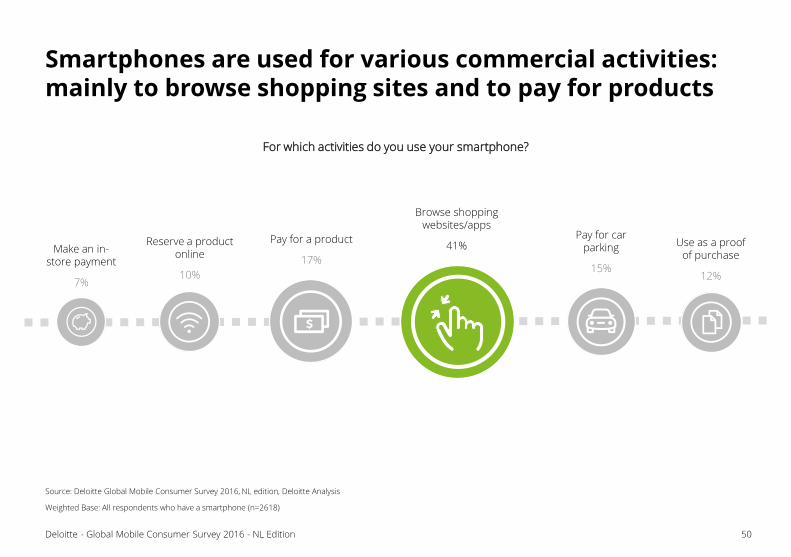

Dutch consumers have also embraced mobile banking. More

than half of respondents check their balance and 43%

transfers money domestically by using a smartphone. We see

that these banking activities are no longer accommodated by

incumbent banks only. As much as 41% of respondents (also)

use a payment provider other than their own bank. When we

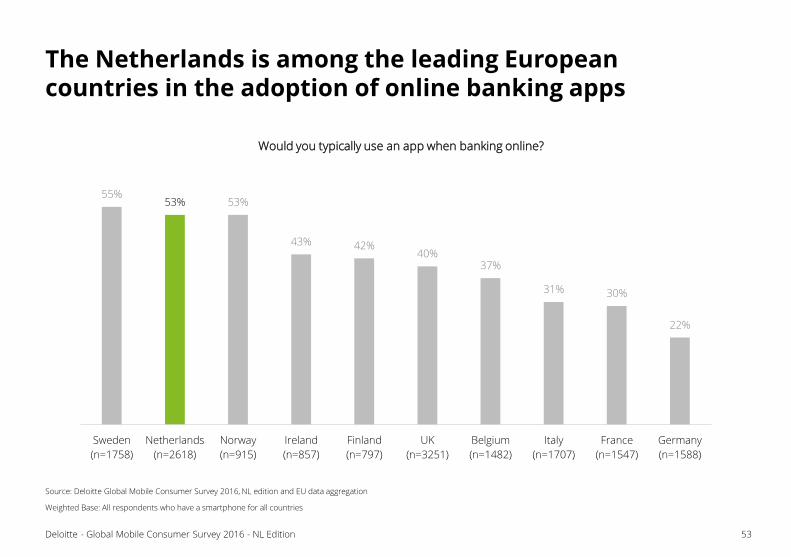

put this in a European context, the Netherlands ranks among

the highest countries when it comes to the adoption of online

banking apps.

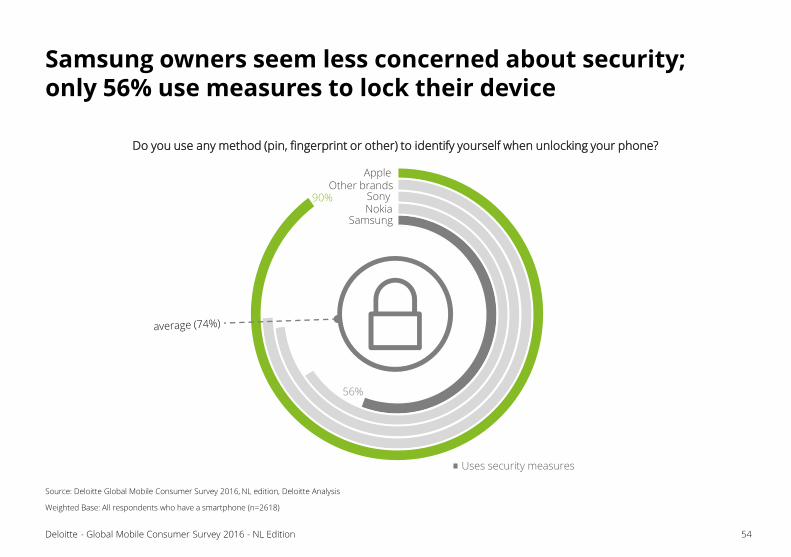

This high penetration of online banking made us research

consumer propensity to secure their phone. We noticed that

on average, 74% of consumers use security measures to lock

their device. Whilst this adoption is particularly high for Apple

users (i.e. over 90%), this cannot be said for Samsung owners.

Only 56% of that group says it uses security measures on

their phone. We also see that the availability of a fingerprint

reader increases the likeliness of having security in place.

48Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

Tablets are used for most activities, but for social networks smartphones are the preferred device

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition, Deloitte Analysis

Weighted Base: All respondents who have a smartphone and a tablet (n=1746)

Voice calls using Internet

Taking photos and recording videos

Checking bank balance

Checking Social

Network

Video calling

Watch live TV

Browsing through shopping websites

Playing games Streaming filmsor TV series

Watching shortVideo’s

Read the news

Making an onlinepurchase

Searching online

Which device is your favorite for the following activity?

49Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

Mobile users prefer apps over browsers, except for shopping online or making travel arrangements

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition, Deloitte Analysis

Weighted Base: All respondents who have a smartphone (n=2618)

Respondents show a

significant preference for

an app when it provides

content that is accessed

on a frequent basis.

Content that is accessed

spontaneously is mostly

viewed in a browser

0% 10% 20% 30% 40% 50% 60% 70%0%10%20%30%40%

Weather

Social Networking

Navigation

Online banking

News

Play Games

Stream Music / Video

Order a takeaway

Online Shopping

Travel Booking

Browser App

For each of the mobile activities below, would you typically use a browser or an app?

50Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

Smartphones are used for various commercial activities: mainly to browse shopping sites and to pay for products

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition, Deloitte Analysis

Weighted Base: All respondents who have a smartphone (n=2618)

For which activities do you use your smartphone?

Browse shopping websites/apps

41%Make an in-store payment

7%

Pay for a product

17%

Pay for car parking

15%

Use as a proof of purchase

12%

Reserve a product online

10%

42%

54%

43%

15%

9%

6%

None of these

Check bank balances

Transfer money (within NL)

Pay for a services bill

Transfer money (abroad)

Pay a utility bill (e.g. gas, water)

51Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

43% of respondents have used their smartphone to transfer money to another individual

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition, Deloitte Analysis

Weighted Base: All respondents who have a smartphone (n=2618)

Even though most people

use their phone to transfer

money or check balances,

42% of respondents still do

not use their mobile phone

for any kind of financial

transactions

For which of the following financial transactions have you ever used your mobile phone?

52Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

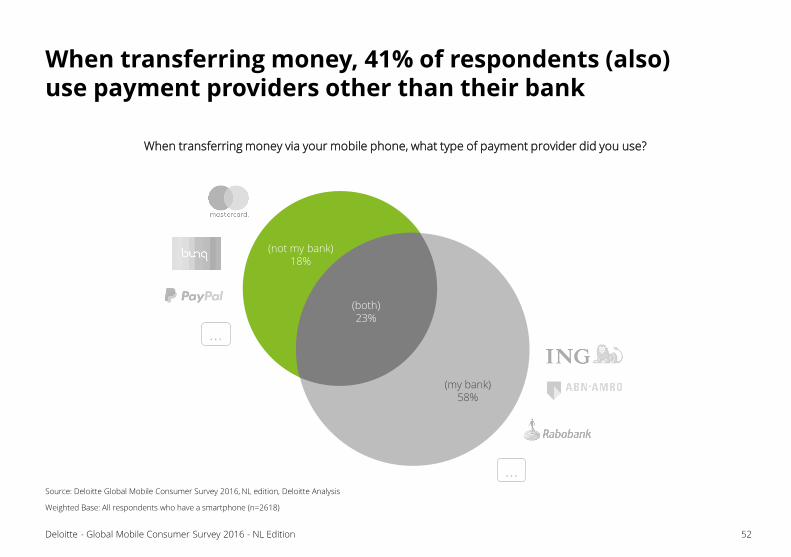

When transferring money, 41% of respondents (also) use payment providers other than their bank

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition, Deloitte Analysis

Weighted Base: All respondents who have a smartphone (n=2618)

…

(not my bank)18%

(my bank)58%

When transferring money via your mobile phone, what type of payment provider did you use?

…

(both)23%

53Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

The Netherlands is among the leading European countries in the adoption of online banking apps

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition and EU data aggregation

Weighted Base: All respondents who have a smartphone for all countries

55%53% 53%

43% 42%40%

37%

31% 30%

22%

Sweden

(n=1758)

Netherlands

(n=2618)

Norway

(n=915)

Ireland

(n=857)

Finland

(n=797)

UK

(n=3251)

Belgium

(n=1482)

Italy

(n=1707)

France

(n=1547)

Germany

(n=1588)

Would you typically use an app when banking online?

SamsungNokiaSony

Other brandsApple

Uses security measures

54Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

Samsung owners seem less concerned about security; only 56% use measures to lock their device

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition, Deloitte Analysis

Weighted Base: All respondents who have a smartphone (n=2618)

Do you use any method (pin, fingerprint or other) to identify yourself when unlocking your phone?

56%

90%

55Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

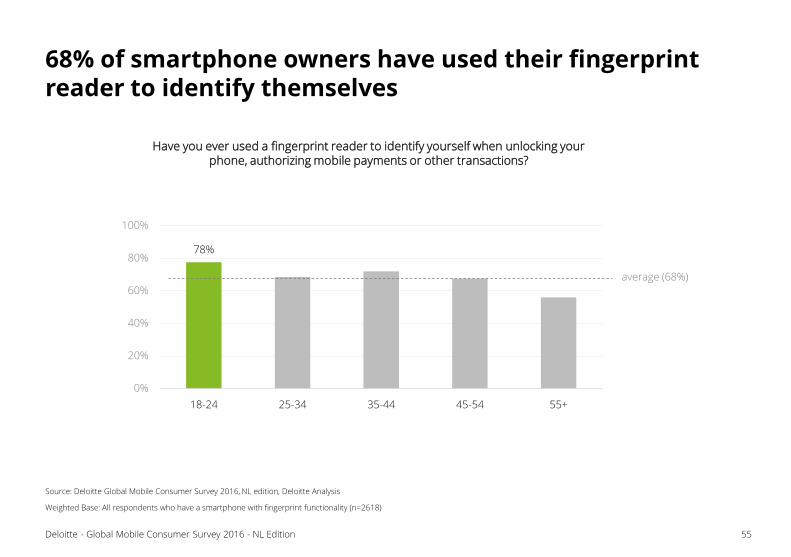

68% of smartphone owners have used their fingerprint reader to identify themselves

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition, Deloitte Analysis

Weighted Base: All respondents who have a smartphone with fingerprint functionality (n=2618)

78%

0%

20%

40%

60%

80%

100%

18-24 25-34 35-44 45-54 55+

average (68%)

Have you ever used a fingerprint reader to identify yourself when unlocking your phone, authorizing mobile payments or other transactions?

The future startstomorrow (not today)

This year, one of the hottest topics in consumer electronics is

Internet of Things (IoT). As a result, we have investigated the

uptake in IoT devices among consumers and their propensity

to buy these type of devices in the near future. We noticed

that even though everyone is expecting IoT to be the next big

thing, reality shows that adoption of these devices is still very

low among consumers. Connected Entertainment devices

such as Smart TVs and Game Consoles have the highest

penetration (with respectively 28% and 15%), however the

uptake of other connected devices is still rather low. Even the

adoption of wearables such as Smart Watches and Fitness

bands, devices that have already been available for a few

years, is still low with an adoption rate of only 5% or less.

In a nutshell, among all connected product categories, the

penetration of Connected Entertainment is the highest with

43%. The question remains whether this high percentage is

driven by actual demand for IoT functionality or the mere

standard availability of these connected services in everyday

household devices.

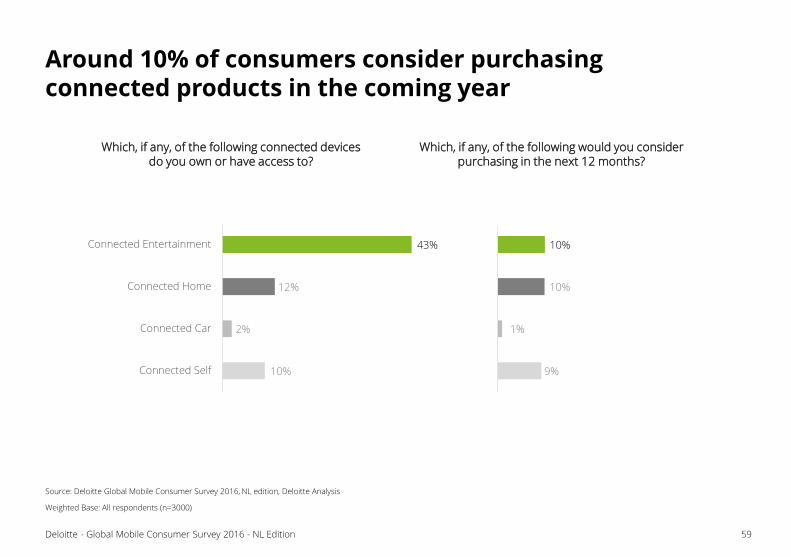

Our respondents also indicate that on average, only 10% is

considering to purchase some type of connected product in

the next 12 months. This is not true for connected car

products for which only 1% considers a purchase within the

next 12 months.

The market’s high expectation of future IoT devices is also

focused on a strong uptake in Virtual Reality (VR). However,

we see that consumer adoption of these IoT devices is still

very low as well. Roughly 5% of consumers owns a VR device,

of which the vast majority owns a low-end or cardboard type

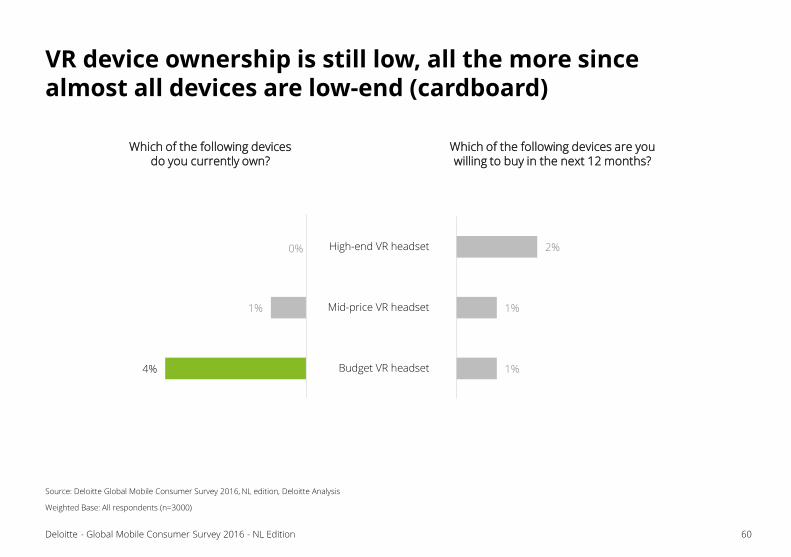

of VR headset. Also consumer’s willingness to buy is low.

58Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

Internet of Things (IoT) device uptake is still low, apart from connected entertainment products

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition, Deloitte Analysis

Weighted Base: All respondents (n=3000)

0% 5% 10% 15% 20% 25% 30%

Wearables for tracking/vital signs

Fitness band

Smart watch

Connected Car system

Interactive robot

A home appliance

Smart lighting systems

Surveillance security system

Smart thermostat

Wireless speaker

Video streaming device

Games console

Smart TV

Connected Home

Connected Entertainment

Which, if any, of the following connected devices do you own or have ready access to?

Connected Self

Connected Car

59Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

Around 10% of consumers consider purchasing connected products in the coming year

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition, Deloitte Analysis

Weighted Base: All respondents (n=3000)

Which, if any, of the following connected devices do you own or have access to?

10%

2%

12%

43%

Connected Self

Connected Car

Connected Home

Connected Entertainment

Which, if any, of the following would you consider purchasing in the next 12 months?

9%

1%

10%

10%

4%

1%

0%

60Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

VR device ownership is still low, all the more since almost all devices are low-end (cardboard)

Source: Deloitte Global Mobile Consumer Survey 2016, NL edition, Deloitte Analysis

Weighted Base: All respondents (n=3000)

1%

1%

2%

Budget VR headset

Mid-price VR headset

High-end VR headset

Which of the following devices do you currently own?

Which of the following devices are you willing to buy in the next 12 months?

Contact

39Deloitte - Global Mobile Consumer Survey 2016 - NL Edition

Contact

Vincent Kuijvenhoven

Manager | Deloitte Digital

+31 6 5359 8526

Remco Gaykema

Senior Consultant | Deloitte Digital

+31 6 5359 8479

Dirk Reuser

Manager | Deloitte Digital

+31 6 8201 9345

Michiel Mennen

Manager | Operational Excellence

+31 6 1258 1756

Marc Beijn

Director | Deloitte Digital

+31 6 8201 9400

Patrick Steemers

Partner | Segment Lead Telecom

+31 6 8201 9347

Rob Oudehand

Morris Boermann

Joël van Veen

Iris Olde Klieverik

Somil Sharma

Christie Tan

Erik Bookholt

Consultant | Enterprise Architecture

+31 6 8201 2578

With special thanks to:

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.nl/about for a more detailed description of DTTL and its member firms.

Deloitte provides audit, consulting, financial advisory, risk management, tax and related services to public and private clients spanning multiple industries. Deloitte serves four out of five Fortune Global 500® companies through a globally connected network of member firms in more than 150 countries bringing world-class capabilities, insights, and high-quality service to address clients’ most complex business challenges. To learn more about how Deloitte’s approximately 225,000 professionals make an impact that matters, please connect with us on Facebook, LinkedIn, or Twitter.

This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte Network”) is, by means of this communication, rendering professional advice or services. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this communication.

© 2016 Deloitte The Netherlands