global it-bpo outsourcing deals analysisindia and australia were two other key outsourcing markets....

TRANSCRIPT

Global IT-BPO

Outsourcing Deals

Analysis

3Q15 Analysis:

July to September

October 2015

1© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights

reserved.

About global IT-BPO outsourcing deals analysis

KPMG’s Shared Services and Outsourcing Advisory (SSOA) practice publishes a quarterly analysis on

IT-BPO outsourcing contracts signed across industries and geographies, with a total contract value

(TCV) of USD5 million and above per deal.

Methodology and limitations of the study:

The analysis and findings presented in this report are based on select third party deals database

including, publicly available outsourcing data as identified throughout this presentation. It does not

include contract information gathered from KPMG Sourcing Advisory business engagements.

The count and value of the deals may vary notably in reality and is only indicative of market movements

and trends in the IT-BPO space. Readers are requested to use their discretion while assessing the

global IT-BPO market accordingly.

For more information on this market research, please get in touch with Shailesh Narwaiye

Contents

Section 1: Global deals: An overview

Section 3: IT-BPO outsourcing outlook

Section 2: 3Q15 deal analysis

Section 1

Global deals: An overview

4© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights

reserved.

A summary

Source: IDC (www.idc.com), Contract Database, Oct 2015, KPMG member firms research & analysis based on the IDC contract database

In 3Q15 (July to September), 222 ITO contracts worth USD32.9 billion and 23 BPO contracts worth USD4.5

billion were signed, worldwide.

ADM and SCM contributed approximately USD9.6 billion and USD1.7 billion respectively and were

the largest procured services globally within ITO and BPO outsourced services, respectively.

Globally eight IT-BPO bundled deals were signed in 3Q15 with contract value

worth USD1.4 billion.

In terms of value, approximately 59 per cent of deals originated from the United States, followed by

the United Kingdom at 9.8 per cent. India and Australia were two other key outsourcing markets.

Defense sector continued to be the top consumer of IT-BPO services contributing to 54 per cent in terms of

value of outsourcing deals signed in 3Q15. Telecom sector exhibited continuous growth over past two

quarters doubling in total contract value in 3Q15 over 2Q15

Average annualized contract value in 3Q15 was USD36.4 million as compared to USD24.9 million in 3Q14

showing an increase of 46 per cent between the two quarters.

The average deal tenure decreased to 4 years 3 months in 3Q15 from 4 years 9 months in 2Q15.

5© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights

reserved.

22.7

36.5 35.3

55.9

20.3

43.9

53.3

28.0 25.229.1 39.8 26.4

21.8

75.9

38.8

292

354

428

516

299

426 422

326

259

316324

245192

334

253

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2012 2013 2014 2015

Value (USD billion) No. of deals

Total deal value

USD145.5 billion

Total deal value

USD150.4 billion

Quarterly deal movementsSnapshot

Quarterly movements of global IT-BPO deals*

Number of deals

1,590

-3%

Number of deals

1,473

-7%

*The term deals is interchangeably used with contracts throughout the analysis unless otherwise specified. Deals analyzed are global sourcing contracts of size USD5.0 million and above only.

Source: IDC (www.idc.com), Contract Database, Oct 2015, KPMG member firms research & analysis based on the IDC contract database

Total deal value

USD120.4 billion

-17%

Number of deals

1,144

-22%

Deal value

3Q15

3Q14

3%

No. of deals

3Q14

3Q15

22%

• 3Q15 witnessed a sharp drop in deal activity as compared to 2Q15. There was a decrease of 49 per cent in

total contract value and 24 per cent decrease in total number of deals in 3Q15 as compared to 2Q15

• The average contract value also decreased by 33 per cent in 3Q15 as compared to 2Q15

6© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights

reserved.

Annualized contract value (ACV)Q-o-Q comparison

Annualized* contract value comparison per quarter

* Annualized contract value = ( total value of a contract / tenure in months ) x 12

Contract value for contracts having tenure less than 1 year is considered as annualized value for the analysis. Graph is not to scale and

only represents the division across different parameters

Source: IDC (www.idc.com), Contract Database, Oct 2015, KPMG member firms research & analysis based on the IDC contract database

Average annualized contract value (USD million)

Average tenure per contract

Note: All values in USD million unless otherwise specified

14% increase

Minimum annualized

contract value

Maximum annualized

contract value

46% increase

265.7

1720.4

0.57

0.86

4 years 7 months

24.90

27.73

3Q14

3Q13

10000.85

3Q15

36.41

4 years 3 months

4 years 9 months

• Total annualized contract value in 3Q15 increased by 14 per cent as compared to 3Q14. The average

annualized contract value also increased by 46 per cent in 3Q15 as against 3Q14 indicating a strong

preference for larger value deals

• The average contract tenure decreased to 4 years 3 months in 3Q15 from 4 years 7 months in 3Q14

11,703

8,067

9,212

3,500 5,500 7,500 9,500 11,500 13,500

3Q13

3Q14

3Q15

Total Annualized Contract Value (USD million)

31% decrease

7© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights

reserved.

*Others: Construction, Consumer and Recreational Services, Education, Professional services, Securities and investment services, Social services, Trade unions, Technology, Wholesale

Source: IDC (www.idc.com), Contract Database, Oct 2015, KPMG member firms research & analysis based on the IDC contract database

Sector analysisQ-o-Q comparison

Trends in deal movement from 3Q14 to 3Q15

Decrease >=25% Decrease <25% Increase <25% Increase >=25%No change

• In 3Q15, while there has been an increase in Total Contract Value by more than 25 per cent in few sectors,

there has been a decrease of more than 25 per cent in sectors like Defense and Government which are

the major contributors to total contract value

• Continuous growth over two last quarters was observed in Telecom in terms of all three parameters - total

contract value, total number of contracts and average contract value

• Multi-fold growth in terms of total contract value was observed in Banking and Financial Services,

Insurance, Travel and Logistics and Telecom sectors in 3Q15 as compared to 2Q15

Sector

3Q14->4Q14 4Q14 -> 1Q15 1Q15 -> 2Q15 2Q15 -> 3Q15 3Q14->4Q14 4Q14 -> 1Q15 1Q15 -> 2Q15 2Q15 -> 3Q15 3Q14->4Q14 4Q14 -> 1Q15 1Q15 -> 2Q15 2Q15 -> 3Q15

Automotive & Aerospace -41% 403% -83% 46% 0% 150% 20% 0% -41% 101% -86% 46%

Banking & Financial Services 77% -7% -90% 360% -37% -8% 18% 15% 181% 2% -91% 299%

Defence -72% 45% 710% -63% -56% 27% 114% -53% -36% 14% 279% -22%

Energy & Utilities -75% 64% -14% 27% -32% -31% 11% 20% -63% 137% -23% 6%

Government -54% -82% 439% -51% -14% -61% 37% 22% -46% -53% 294% -60%

Insurance 331% 36% -92% 1107% 100% 17% 0% 0% 115% 16% -92% 1107%

Manufacturing 91% -2% 170% -4% 15% -53% 129% 38% 66% 110% 18% -30%

Pharma & Healthcare -93% 2242% 1072% -99% -75% 200% 267% -82% -72% 681% 220% -97%

Publishing, Media & Entertainment -96% 786% 314% -72% -67% 100% 350% -78% -88% 343% -8% 26%

Retail -25% -48% 631% 52% 40% -71% 400% -10% -47% 82% 46% 69%

Telecom 47% -59% 82% 105% 17% -39% 76% 3% 26% -33% 3% 98%

Travel & Logistics 263% 4% -91% 371% 40% -14% -17% 0% 160% 22% -89% 371%

Others* 956% -43% 281% -81% 13% 22% 45% -34% 838% -53% 162% -71%

Total Contract Value Total Number of Contracts Average Contract Value

8© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights

reserved.

Deal analysis Q-o-Q comparison

Trends in deal movement from 3Q14 to 3Q15

Source: IDC (www.idc.com), Contract Database, Oct 2015, KPMG member firms research & analysis based on the IDC contract database

Decrease >=25% Decrease <25% Increase <25% Increase >=25%No change

• Owing to weak deal activity in 3Q15 added to the fact that 2Q15 was a strong quarter, all the deal

categories witnessed a decrease in total contract value in 3Q15 as compared to 2Q15

• The total number of contracts signed in 3Q15 with tenure between 1 to 5 years increased, both short

tenure (less than 1 year) deals and long tenure (more than 5 years) deals decreased by more than 25 per

cent

• While the total contract value of BPO deals decreased by more than 25 per cent in 3Q15 as compared to

2Q15, the average contract value increased by more than 25 per cent in the same period

Deal Type

3Q14->4Q14 4Q14 -> 1Q15 1Q15 -> 2Q15 2Q15 -> 3Q15 3Q14->4Q14 4Q14 -> 1Q15 1Q15 -> 2Q15 2Q15 -> 3Q15 3Q14->4Q14 4Q14 -> 1Q15 1Q15 -> 2Q15 2Q15 -> 3Q15

ITO 26% -18% 276% -51% 0% -25% 72% -13% 26% 9% 119% -44%

BPO -90% 1% 313% -40% -73% -68% 700% -68% -63% 213% -48% 87%

Bundled -39% -24% -20% -21% -17% 75% -77% 0% -27% -56% 249% -21%

Less than USD 100 MN -27% -18% 78% -20% -20% -20% 56% -25% -9% 2% 14% 6%

Betw een USD 100- 500 MN -51% -10% 214% -44% -32% -29% 159% -25% -28% 27% 21% -25%

More than USD 500 MN -19% -22% 344% -56% -55% -22% 71% -8% 80% 1% 159% -52%

Less than 1-year -54% 61% 21% -66% -37% -5% 33% -25% -27% 68% -9% -55%

Betw een 1 to 5-years -46% 6% 82% -7% -15% -16% 26% 3% -36% 26% 45% -10%

More than 5-years -19% -38% 487% -66% -46% -58% 594% -71% 52% 48% -15% 18%

Total Contract Value Total Number of Contracts Average Contract Value

9© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights

reserved.

36.8

97.6

31.3

64.9

24.7

253

887

211

649

118

3Q13 2013 3Q14 2014 3Q15

2.2

8.8

2.2

8.0

6.1 32

134

20

97

48

3Q13 2013 3Q14 2014 3Q15

14.3

39.1

6.2

47.5

7.9

137

452

93

398

87

3Q13 2013 3Q14 2014 3Q15

Geography analysisIT-BPO deals across geographies: Q-o-Q comparison

Geography-wise break-up of deals*

* Deals originating from the geography

Source: IDC (www.idc.com), Contract Database, Oct 2015, KPMG member firms research & analysis based on the IDC contract database

EMA

AMERICAS

ASPAC

11.4 15.6

7.8

716

608 562

2009 2010 2011

Total Contract Value (USD billion) No. of Contracts

30

122

35

126

13

253

1,066

282

996

157

Q2-2009 2009 Q2-2010 2010 Q2-2011

Total Contract Value (USD billion) No. of Contracts

• AMERICAS continues to be the major outsourcing region contributing 64 per cent of the total deal value

in 3Q15. EMA and ASPAC contribute 21 per cent and 16 per cent respectively

• The outsourcing market in EMA and ASPAC continue to grow with an increase in total deal value by 174

per cent and 27 per cent respectively in 3Q15 as compared to 3Q14

• In terms of number of deals, AMERICAS contributed to 47 per cent of the total number of deals signed in

3Q15, whereas EMA and ASPAC contributed 34 per cent and 19 per cent respectively.

10© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights

reserved.

5.3

0.8 0.2

1.5 0.9

0.6 0.01 0.01 0.1

3.9

2.0

20.7

2.8

5.7

1.2 0.9

1.6

0.8

1.0

0.2 0.05 0.1

1.6

1.1

4.8

5.8

5.3

0.1 0.1

0.1

2.2

0.9

1.9

0.2 0.4

2.9

4.3

7.0

1.1

0.5 1.1

0.2 0.7

2.2 1.1

0.0 0.1 0.6

6.0

0.8

56.3

5.7

0.1

1.6

Sector analysisIT-BPO deals across sectors by value and numbers

Sector-wise break-up of deals (4Q14 to 3Q15)

Banking

and

Financial

Services

Insurance Automotive

and

Aerospace

Travel and

Logistics

Manufacturing Energy and

Utilities

Pharma

and

Healthcare

Publishing,

Media and

Entertainment

Retail Telecom Others * Defense Government

No. of contracts* Others: Construction, Consumer and Recreational Services, Education, Professional services, Securities and investment services, Social services, Trade unions, Technology, Wholesale

Graph is not to scale and only represents the division across different parameters. Figures may not add up to 100 per cent due to rounding off

Source: IDC (www.idc.com), Contract Database, Jul 2015, KPMG member firms research & analysis based on the IDC contract database

Q4-2014 Q1-2015 Q2-2015

TCV : USD38.8 billion

No. of contracts: 253

Q3-2015

12

6

11

776

2

14 1513

1 1

7

28

5

79

3 2

17

30

10

22

12

2 2

9

31

21

12

18

51

22

65 66

50

77

139

• While the Defence sector continue to lead deal activity, contributing 54 per cent of the total deal value in

3Q15, the contribution of Government sector has dropped to 8 per cent. Both the sectors witnessed a

decrease of over 50 per cent in total contract value in 3Q15 as compared to 2Q15

• Telecom sector is continuously growing since past two quarters. The total contract value doubled in

3Q15 as compared to 2Q15

30

2

13

76

10

16

10 11 9 10

32

41

2.5

15

Deal

Valu

e (

US

D b

illi

on

)

11© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights

reserved.

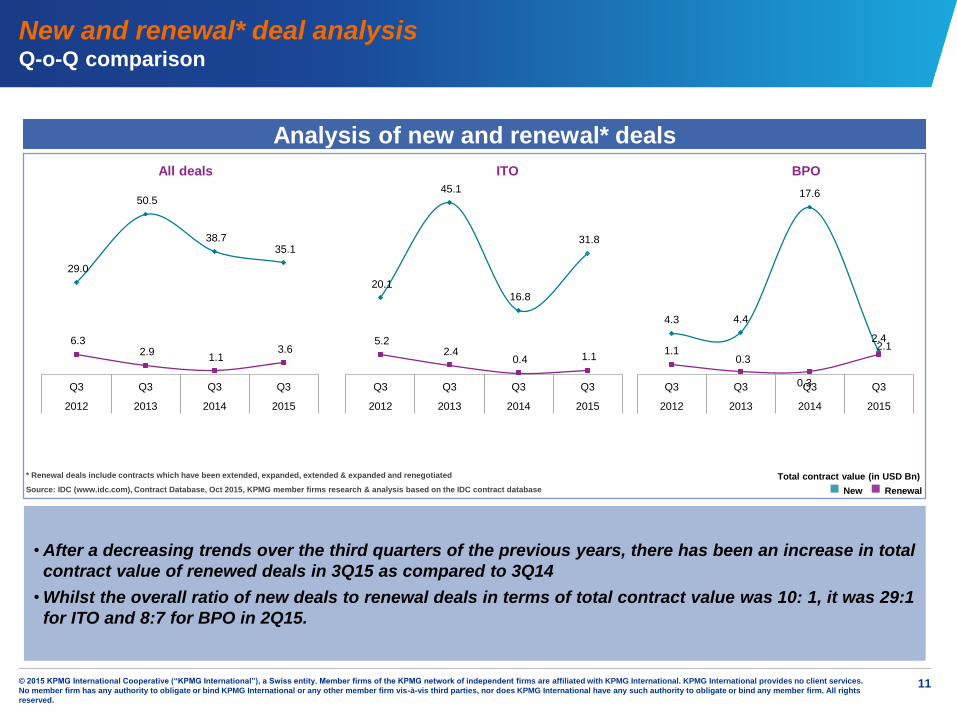

New and renewal* deal analysisQ-o-Q comparison

Analysis of new and renewal* deals

• After a decreasing trends over the third quarters of the previous years, there has been an increase in total

contract value of renewed deals in 3Q15 as compared to 3Q14

• Whilst the overall ratio of new deals to renewal deals in terms of total contract value was 10: 1, it was 29:1

for ITO and 8:7 for BPO in 2Q15.

Analysis of new and renewal* deals

* Renewal deals include contracts which have been extended, expanded, extended & expanded and renegotiated

Source: IDC (www.idc.com), Contract Database, Oct 2015, KPMG member firms research & analysis based on the IDC contract database

29.0

50.5

38.7 35.1

6.3 2.9

1.1 3.6

Q3 Q3 Q3 Q3

2012 2013 2014 2015

20.1

45.1

16.8

31.8

5.2 2.4

0.4 1.1

Q3 Q3 Q3 Q3

2012 2013 2014 2015

4.3 4.4

17.6

2.41.1

0.3

0.3

2.1

Q3 Q3 Q3 Q3

2012 2013 2014 2015

All deals ITO BPO

New Renewal

Total contract value (in USD Bn)

Section 2

3Q15 deal analysis

13© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights

reserved.

ITO32.9

BPO4.5

Bundled1.4

Americas24.7

EMA7.9

ASPAC6.1

Less than USD 100 MN5.9

Between USD 100- 500 MN12.9

More than USD 500 MN19.9

Less than 1-year0.3

Between 1 to 5-years20.3

More than 5-years18.1

Fixed Price23.5

Hybrid14.2

0.6 0.4

Services Region Contract Value Tenure Pricing

* Deals analyzed are USD5.0 million and above only, throughout the analysis. Graph is not to scale and only represents the division across different parameters. Figures may not add up to 100 per cent due to rounding off

# Hybrid pricing includes a combination of various pricing mechanisms

Source: IDC (www.idc.com), Contract Database, Oct 2015, KPMG member firms research & analysis based on the IDC contract database

IT-BPO deals* signed in 3Q15 (Total contract value: USD38.8 billion)

Total

contract

value

USD38.8

billion

• ITO deals continue to dominate the outsourcing space with a contribution of 85 per cent to total deal

value signed in 3Q15

• AMERICAS continues to be the major outsourcing region contributing 64 per cent of the total deal value

in 3Q15. EMA and ASPAC contribute 21 per cent and 16 per cent respectively

• 3Q15 saw the continued dominance of Fixed Price contracting model, contributing 61 per cent of the deal

value, followed by Hybrid model, contributing 37 per cent.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Deal valueGlobal sourcing snapshot: July to September 2015

OthersTime & Material

#

14© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights

reserved.

ITO222

BPO23

Bundled8

Americas118

EMA87

ASPAC48

Less than USD 100 MN180

Between USD 100- 500 MN62

More than USD 500 MN11

Less than 1-year21

Between 1 to 5-years200

More than 5-years32

Fixed Price225

Hybrid9

172

Services Region Contract Value Tenure Pricing

IT-BPO deals* signed in 3Q15 (Total number of contracts: 253)

Total

contracts

253

• While ITO deals and BPO deals decreased by 13 per cent and 68 per cent respectively in terms of number

of deals signed in 3Q15 as compared to 2Q15, bundled deals remained constant in the same period

• 71 per cent of the deals, in terms of number of deals signed in 3Q15, were of value less than USD100

million

• Deals with tenure between 1 to 5 years were largest in number, comprising 79 per cent to the deals

signed in 3Q15. Long tenure deals with tenure more than 5 years made 13 per cent of the total number of

deals

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

* Deals analyzed are USD5.0 million and above only, throughout the analysis. Graph is not to scale and only represents the division across different parameters. Figures may not add up to 100 per cent due to rounding off

# Hybrid pricing includes a combination of various pricing mechanisms

Source: IDC (www.idc.com), Contract Database, Oct 2015, KPMG member firms research & analysis based on the IDC contract database

Number of dealsGlobal sourcing snapshot: July to September 2015

#

OthersTime & Material

15© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights

reserved.

Analysis of ITO deals 3Q15

Number of DealsNote: Size of bubble indicates percentage share of the total number of ITO deals

SI – System Integration, Other IT services – Software testing, IT Education and Training, SaaS

Source: IDC (www.idc.com), Contract Database, Oct 2015, KPMG member firms research & analysis based on the IDC

contract database

• ADM, ICT Services and IT Bundled together contributed to 77 per cent of all ITO deals in terms of value

and 67 per cent in terms of number of deals during 3Q15

• ADM gained activity with multi-fold growth in total contract value in 3Q15 over 2Q15 after a long period of

weak activity. SMAC services are gaining momentum with 43 per cent increase in total contract value

over the same period

Value of contracts (USD Billion)Note: All values in USD billion. Scale of graph is just representative to illustrate the division across different parameters.

Figures may not add up to 100 per cent due to rounding off. Refer L.H.S. figure for legend

Source: IDC (www.idc.com), Contract Database, Oct 2015, KPMG member firms research & analysis based on the IDC

contract database

Services segmentationITO services

9.6

0.2

6.1

9.4

0.02 0.7 0.1

4.7

1.80.3

ADM8%

ERP3%

ICT Services17%

IT Bundled services41%

IT Consulting1%

IT Infrastructure5%

IT Products2%

Other IT Services, 0%

SI7% SMAC

15%

0

5

10

15

20

25

30

35

40

45

0 10 20 30 40 50 60 70 80 90 100

To

tal V

alu

e o

f co

ntr

acts

(U

SD

Billio

n)

32.9

ADM ERP Total

ITO

ICT IT

Bundled

IT

Infra.

IT

Products

SMACSIIT

Conslt.

Other IT

Services

16© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights

reserved.

Analysis of BPO deals 3Q15

Note: Size of bubble indicates percentage share of the total number of BPO deals

Other BPO services – Data management, logistics etc.

Source: IDC (www.idc.com), Contract Database, Oct 2015, KPMG member firms research & analysis based on the IDC contract

database

Note: All values in USD million. Scale of graph is just representative to illustrate the division across different parameters.

Figures may not add up to 100 per cent due to rounding off. Refer L.H.S. figure for legend

Source: IDC (www.idc.com), Contract Database, Oct 2015, KPMG member firms research & analysis based on the IDC

contract database

• SCM and BPO Bundled together contributed to 60 per cent of all BPO deals in terms of value and 61 per

cent in terms of number of deals during 3Q15

• F&A and CRM services have also exhibited multifold growth in 3Q15 in terms of deal value as compared

to 2Q15

Services segmentationBPO services

929

63

550

331

0 55

1729

BPO Bundled services

17%

Content Management

4%

CRM9%

F&A13%

HRO9%

Other BPO Services

4%

SCM43%

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

0 4 8 12

4,455

BPO

Bundled

Services

Content

Mgmt.

CRM Total

BPOHRO KPO Other

BPO

Services

To

tal V

alu

e o

f co

ntr

acts

(U

SD

Millio

n)

Number of Deals Value of contracts (USD Million)

SCM

Section 3

IT-BPO outsourcing outlook

18© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights

reserved.

OutlookGlobal outsourcing industry

■ 3Q15 shows a outsourcing deal activity in lines with the weak economic activity in most major

industrialized markets – though there is a sharp dip as compared to 2Q15, it is comparable to the third

quarters of the last couple of years.

■ Renewal deals value is miniscule as compared to new deals values with many organizations actively

exploring outsourcing as a part of their business transformation efforts from a more wide-ranging process

standpoint.

■ Government and Defense sectors are the main consumers of IT&BPO services – while 2Q15 saw an

upturn in the deal activity both the sectors witnessed a significant downturn in 3Q15

■ Many organizations chose traditional pricing models as compared to a hybrid model continuing the

decreasing trend in the share of hybrid pricing deals over the quarters. This may indicate a reduction in

the risk appetite of the vendors

■ While EMA is continuing to gain outsourcing momentum, 3Q15 deal activity has been driven by the

AMERICAS which continues to be the major outsourcer

■ SMAC services and automation are major drivers for the commoditization of the outsourcing services

and this is especially true for IT services. There are still only a few stand-alone SMAC deals but are

now becoming a common part of bundled deals.

■ Buyers are seeking more commoditized solutions tailor made to specific industry, geographic and

regulatory needs that can drive benefits more than cost savings*

1 KPMG SSOA Pulse survey 2Q15

Source: IDC (www.idc.com), Contract Database, Oct 2015, KPMG member firms research & analysis based on the IDC contract database

19© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights

reserved.

To learn more, log on to https://institutes.kpmg.us/institutes/shared-services-outsourcing-institute.html/

Advice Worth Keeping Blog: http://blog.equaterra.com/

Advice Worth Keeping podcast series: http://www.kpmginstitutes.com/shared-services-outsourcing-institute/events/podcast_series/advice-worth-keeping-

podcast-series.aspx

Global IT-BPO Outsourcing Deals Analysis: http://www.kpmg.com/IN/en/IssuesAndInsights/ArticlesPublications/KPMG-Deal-Tracker/Pages/Default.aspx

Latest from the KPMG Shared Services and Outsourcing Institute

•Global Business Services (GBS) Journey to Excellence

•Robotic Revolution – Separating Hype from Reality

•From Human to Digital: The Future of Global Business Services

About KPMG Institutes

KPMG Institutes is dedicated to

helping organisations and their

stakeholders identify and understand

emerging trends, risks and

opportunities. We do this by creating

an open forum where peers can

exchange insights, share leading

practices, and access the latest

thought leadership publications.

As a result, corporate executives,

business managers, industry

leaders, government officials,

academics, and others have access

to the thought leadership documents

and knowledge which they can use

to make better informed decisions

and meet their marketplace

challenges.

KPMG Shared Services and Outsourcing Advisory (SSOA) research

20© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights

reserved.

Glossary (1/2)

Terms Definition

ITO Information Technology Outsourcing

BPO Business Process Outsourcing

ACV Annualized contract value = ( total value of a contract/tenure in months ) x 12

TCV Total contract value

AMERICAS North America and South America

ASPAC Asia and Oceania

EMA Europe, Middle East and Africa

21© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights

reserved.

Glossary (2/2)

Terms Definition

ITO Services

ADM Application development and maintenance

ERP Enterprise resource planning implementation and support services

ICT ServicesInformation and communication technology services (e.g. contact center technology, telecommunication, and

related services)

IT Bundled Services Any combination of two or more IT services mentioned above

IT Consulting Information technology consulting services

IT InfrastructureIT hardware deployment (e.g. data centre outsourcing, network management, hardware deploy and support,

hosting services, etc.)

IT Products Software products typically developed and branded by IT companies and sold as own Intellectual Property

Other IT ServicesTypically services that do not fall in other buckets (e.g. Software testing, IT helpdesk support services, Cyber

security)

SMAC Social, Mobile, Analytics and Cloud services (i.e. Social Media, Mobility, Analytics and Cloud computing)

System Integration IT system integration services (application or enterprise system integration services)

BPO Services

BPO Bundled Services Any combination of two or more BPO services mentioned above

Content Management Data management services (e.g. document management, print management, etc.)

CRM Customer Relationship Management solutions and services

F&A Finance and Accounting services

HRO Human Resource outsourcing services

KPO Knowledge process outsourcing services

Other BPO Services Typically services that do not fall in other buckets (e.g. Industry specific processes, Facilities Management)

SCM Supply Chain Management services (including procurement, logistics etc.)

22© 2015 KPMG International Cooperative (“KPMG International”), a Swiss entity. Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services.

No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm. All rights

reserved.

Jehil ThakkarPartner – Advisory Services

KPMG in India

+91 22 3090 1670

Viral ThakkerPartner – Advisory Services

KPMG in India

+91 22 3090 1730

KPMG contacts:

Stan Lepeak Director – Global Research,

Management Consulting

KPMG in the US

+1 203 458 0677

Thank you

Analyst Team Contact:

Shailesh Narwaiye

KPMG in India

+91 20 3050 4000

Analysts (KPMG in India):

Esther Jaydevi

Swati Kumari

The information contained herein is of a general nature and is not

intended to address the circumstances of any particular individual

or entity. Although we endeavour to provide accurate and timely

information, there can be no guarantee that such information is

accurate as of the date it is received or that it will continue to be

accurate in the future. No one should act on such information

without appropriate professional advice after a thorough

examination of the particular situation.

© 2015 KPMG International Cooperative (“KPMG International”), a

Swiss entity. Member firms of the KPMG network of independent

firms are affiliated with KPMG International. KPMG International

provides no client services. No member firm has any authority to

obligate or bind KPMG International or any other member firm vis-

à-vis third parties, nor does KPMG International have any such

authority to obligate or bind any member firm. All rights reserved.

The KPMG name, logo and “cutting through complexity” are

registered trademarks or trademarks of KPMG International.