global investment performance standards - societies · global investment performance standards a...

TRANSCRIPT

Global Investment Performance Standards A practical point of view on implementation and verification

GIPS® Standards Workshop

25/10/2017 Aspire with assurance

2 Public © 2017 Deloitte Audit

Contents

Background

Our approach to certification

List of required documentation and Q&A

3 Public © 2017 Deloitte Audit

Background

4 Public © 2017 Deloitte Audit

Consultants and Institutionals consider compliance and verification when selecting managers

Globalization

Which standards ? • AIMR-PPS • SPPS (Switzerland) • DVFA (Germany) • UKIPS (UK) • …

Rationale for creation of Global Investment Performance Standards GIPS®

From a Benchmark Practice …

5 Public © 2017 Deloitte Audit

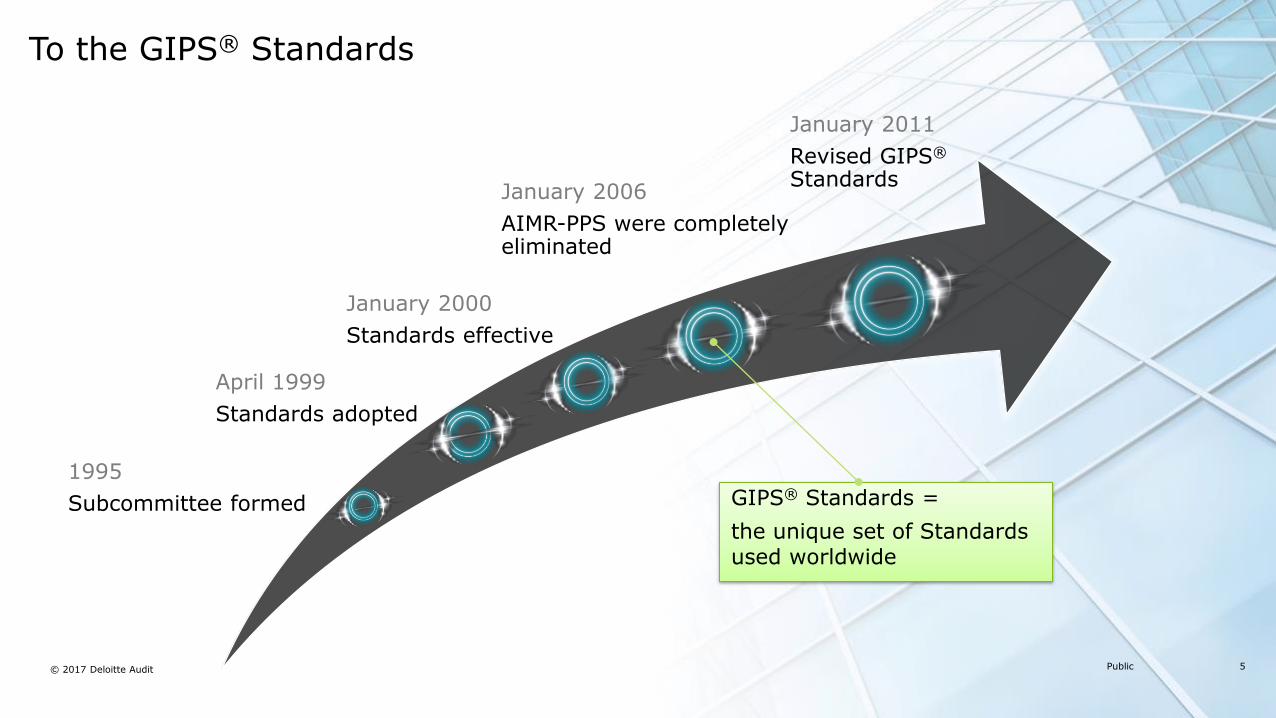

January 2000

Standards effective

1995

Subcommittee formed

January 2006

AIMR-PPS were completely eliminated

January 2011

Revised GIPS® Standards

To the GIPS® Standards

April 1999

Standards adopted

GIPS® Standards =

the unique set of Standards used worldwide

6 Public © 2017 Deloitte Audit

Fundamentals of Compliance Definition of the Firm Foundation for firm-wide compliance Firms can only define themselves as follows:

“Defined as an investment firm,

subsidiary or division held out to

clients or prospective clients

as a distinct business entity”

Encouraged “to adopt broadest, most meaningful definition of the

Firm and consider how it is held out to

the public”

Reason for defining GIPS® at Firm level is to avoid partial disclosure of performance no cherry-picking of the

best performing portfolios

7 Public © 2017 Deloitte Audit

7 Public © 2017 Deloitte Audit

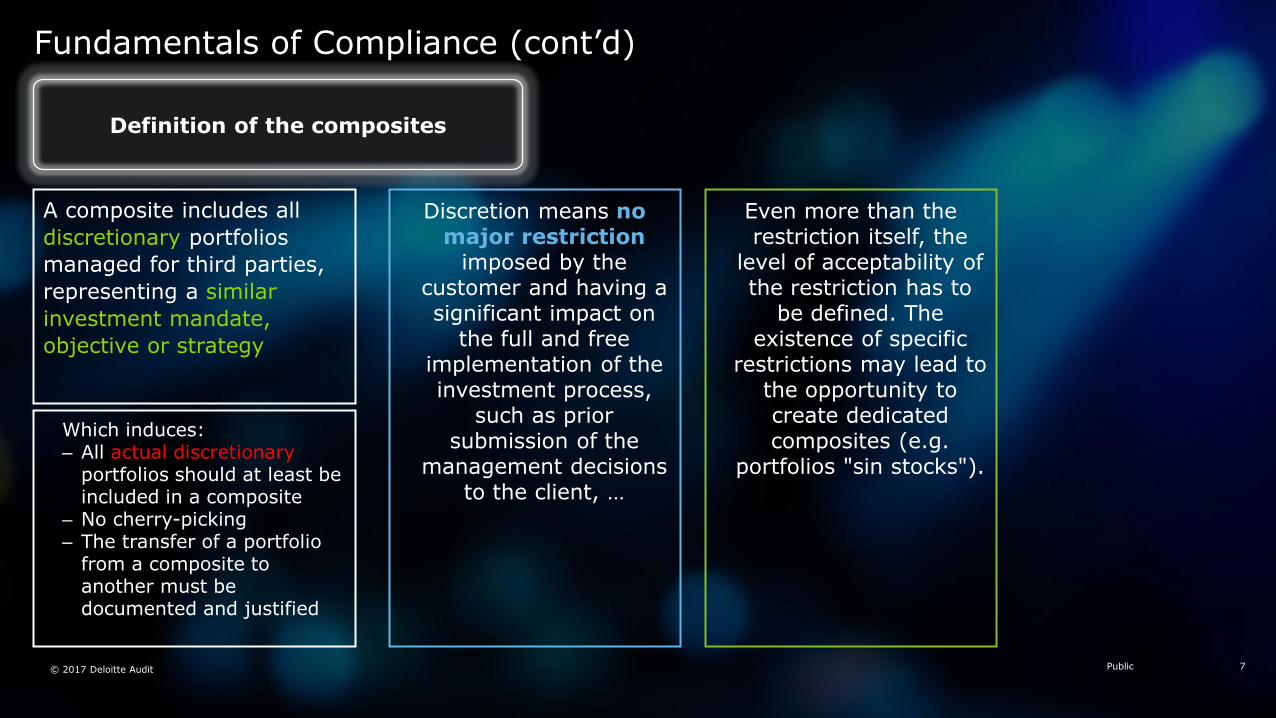

Definition of the composites

Discretion means no major restriction

imposed by the customer and having a significant impact on

the full and free implementation of the investment process,

such as prior submission of the

management decisions to the client, …

A composite includes all

discretionary portfolios

managed for third parties,

representing a similar

investment mandate,

objective or strategy

Even more than the restriction itself, the

level of acceptability of the restriction has to

be defined. The existence of specific

restrictions may lead to the opportunity to create dedicated composites (e.g.

portfolios "sin stocks").

Fundamentals of Compliance (cont’d)

Which induces: ‒ All actual discretionary

portfolios should at least be included in a composite

‒ No cherry-picking ‒ The transfer of a portfolio

from a composite to another must be documented and justified

8 Public © 2017 Deloitte Audit

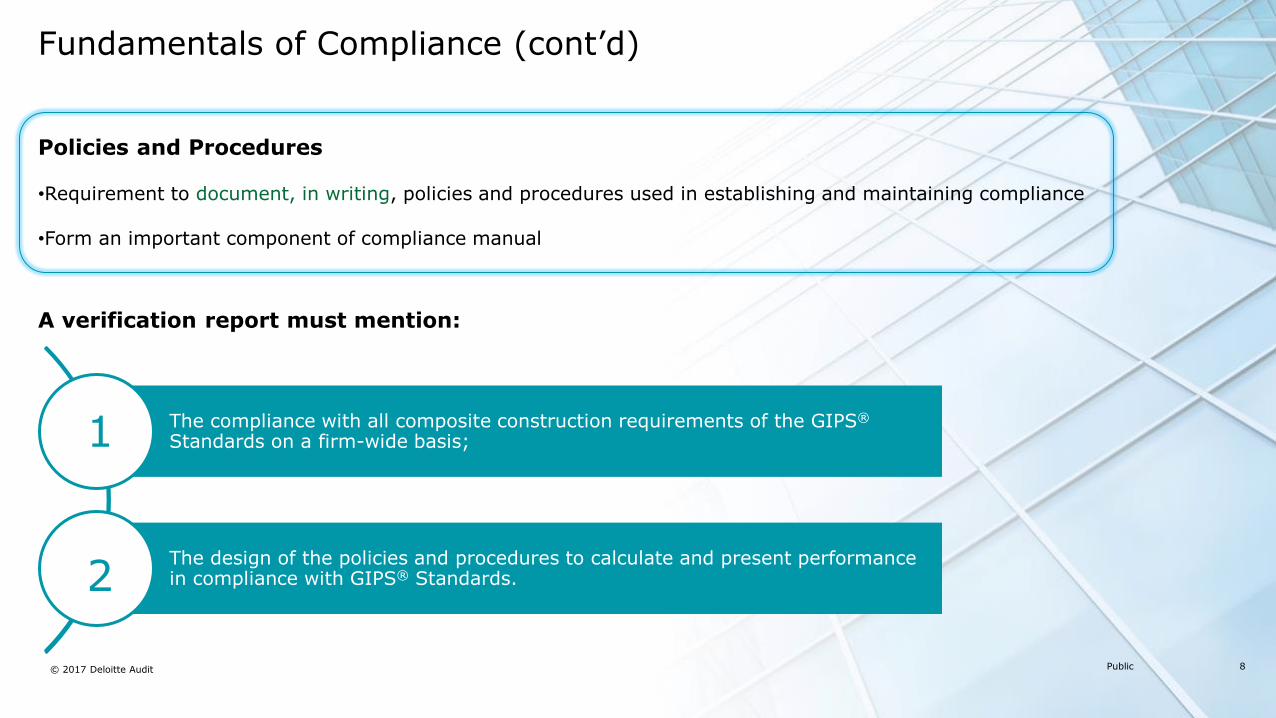

The compliance with all composite construction requirements of the GIPS® Standards on a firm-wide basis;

The design of the policies and procedures to calculate and present performance in compliance with GIPS® Standards.

1

2

A verification report must mention:

Fundamentals of Compliance (cont’d)

Policies and Procedures •Requirement to document, in writing, policies and procedures used in establishing and maintaining compliance •Form an important component of compliance manual

9 Public © 2017 Deloitte Audit

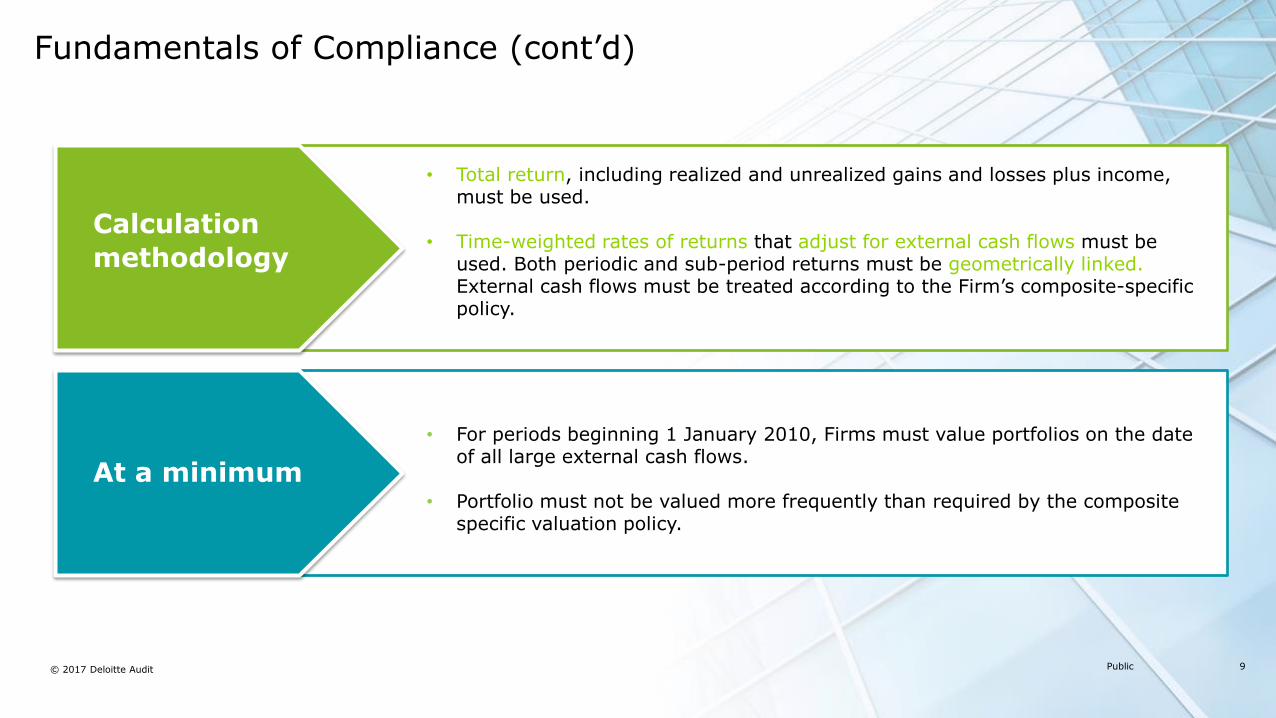

Fundamentals of Compliance (cont’d)

• Total return, including realized and unrealized gains and losses plus income,

must be used.

• Time-weighted rates of returns that adjust for external cash flows must be used. Both periodic and sub-period returns must be geometrically linked. External cash flows must be treated according to the Firm’s composite-specific policy.

Calculation

methodology

• For periods beginning 1 January 2010, Firms must value portfolios on the date

of all large external cash flows.

• Portfolio must not be valued more frequently than required by the composite specific valuation policy.

At a minimum

10 Public © 2017 Deloitte Audit

GIPS® Advertising Guidelines

• Advertising rules effective June 2004 for those including a claim of compliance

• Requirement to present 1, 3, and 5 year (or since inception) annualized composite returns OR 5 years (or since inception) of annual composite returns

Advertisements

• Must provide compliant presentation to all clients and prospects

• Provide list and description (abbreviated definition) of composites upon request

• Firms to include performance of sub-advisor, provided discretion exercised over sub-advisor

Compliant

Materials to

clients/prospects

11 Public © 2017 Deloitte Audit

• Should not present a compliant presentation of the composite to prospects known not to meet the composite’s minimum level

• Statements referring to the calculation methodology used in a composite presentation as being “in accordance,” “in compliance,” or “consistent” with the GIPS®, or similar statements, are prohibited

Others

GIPS® Advertising Guidelines (cont’d)

The GIPS® compliance statement for advertisements :

“ [insert name of firm] claims compliance with the Global Investment Performance Standards (GIPS).”

12 Public © 2017 Deloitte Audit

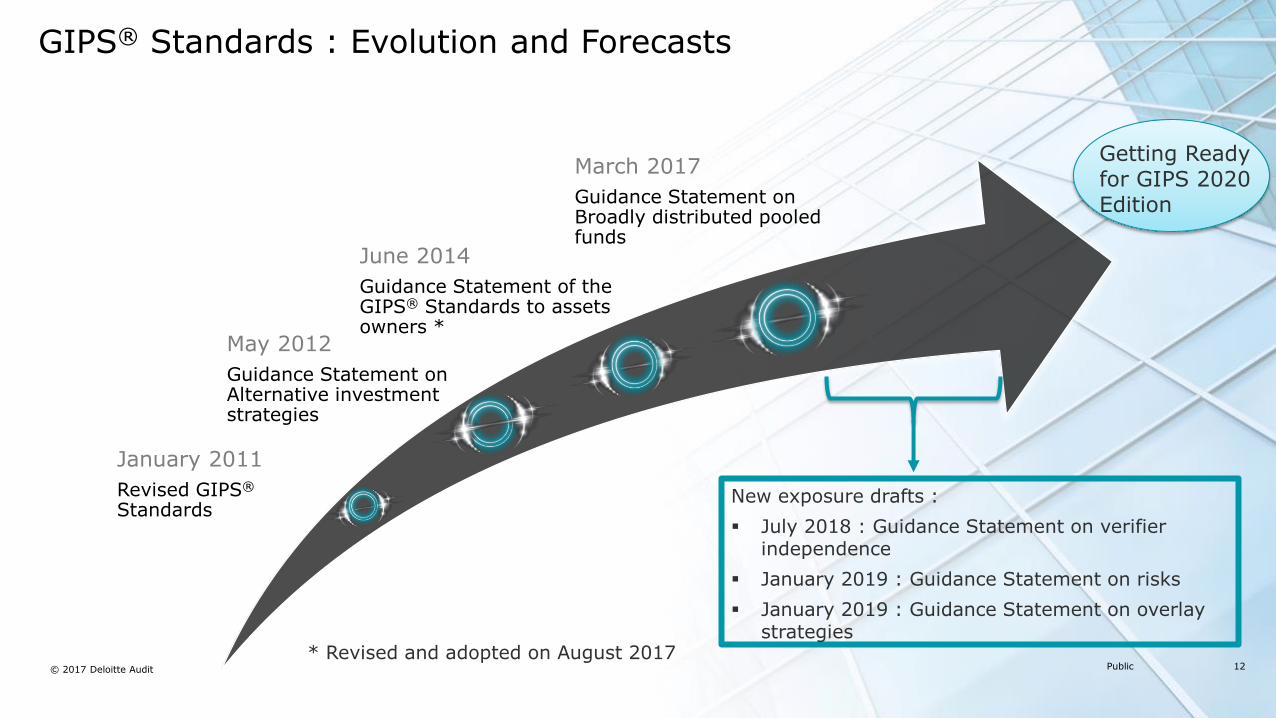

GIPS® Standards : Evolution and Forecasts

June 2014

Guidance Statement of the GIPS® Standards to assets owners *

January 2011

Revised GIPS® Standards

March 2017

Guidance Statement on Broadly distributed pooled funds

May 2012

Guidance Statement on Alternative investment strategies

New exposure drafts :

July 2018 : Guidance Statement on verifier independence

January 2019 : Guidance Statement on risks

January 2019 : Guidance Statement on overlay strategies

Getting Ready for GIPS 2020 Edition

* Revised and adopted on August 2017

13 Public © 2017 Deloitte Audit

Reasons for GIPS®

Compliance

A powerful and differentiating

marketing tool for early movers

An industry-wide response to clients’ increasing need for transparency, good

governance, and structuring exercise

A must-have for RFPs launched by institutional

investors

Conclusion

14 Public © 2017 Deloitte Audit

Our approach to certification

15 © 2017 Deloitte Audit

15 Public © 2017 Deloitte Audit

Approach to compliance

• Internal investigations and interviews

• Involve Marketing and Sales but also IT, Accounting, and Asset Management

• Review of processes, controls and documentation

• Gap analysis

• Proposition of solutions (firm definition, composite building, …) or suggestions (marketing strategy, …)

• Validation of propositions

Diagnosis

• Project management

• Procedures manual

• Internal controls Set-up

• Input data and performance calculation (simple or sophisticated tool)

• Reporting preparation following GIPS® guidelines

• Transfer of know-how to internal team

Implementation

• Verification of the adequacy of procedures with retained solution

• Quality review of data and composites

• Verification of performance calculations

• Verification of mandatory information

• Validation of GIPS® report and advertising documents

• Reporting to Steering Committee / feedback from users to improve N+1

Verification

Illustrative steps to a GIPS® report :

Steps performed by the Asset Manager or with Deloitte’s assistance Steps only performed by the Asset manager

Steps performed by Deloitte

16 © 2017 Deloitte Audit

16 Public © 2017 Deloitte Audit

Approach to compliance – Diagnosis

The diagnosis process is tailored to each manager

Working closely, our teams define the scope covered

which accurately reflects the organization

and that can withstand future developments

Through investigation, interviews and documentation review, a gap analysis is realized and provides you with propositions covering organizational, technical as well as operational aspects.

insights relating to utilization of GIPS report (marketing plan)

Diagnosis

Typical points for discussion • How many types of investment

strategies/composites does the firm manage and are these funds? Are they audited ?

• Could your management team be confused with other investment management teams ?

• Are your procedures regarding Investment management processes available in writing? Further to analysis of documentation and workshop: • definition of the firm drafted • potential need in terms of procedures

documentation identified

17 © 2017 Deloitte Audit

17 Public © 2017 Deloitte Audit

Approach to compliance - Implementation

Best practice advises for a project manager to stay in charge of following the implementation project, to ensure smooth and efficient results.

This phase is an opportunity to finalize the procedures manual which:

presents rules and the approach adopted to comply with the requirements of the Standards

Identifies and describes the procedures for maintenance and supply databases

Data collection and handling is also performed before actual performance calculation, including all controls described in the procedures manual.

Typical points for discussion •Are portfolio performances calculated on a daily basis and under which format (Excel?) •Are “accruals” (fees, interest income, etc.) considered in the calculations • Is there an independent valuation for each investment ?

If confirmed with the analysis of documentation and further workshop: • If needed, implementation of adjustments

(i.e. accruals) and calculation of performances over the period could be started

Some examples of procedures manuals

Implementation

18 © 2017 Deloitte Audit

18 Public © 2017 Deloitte Audit

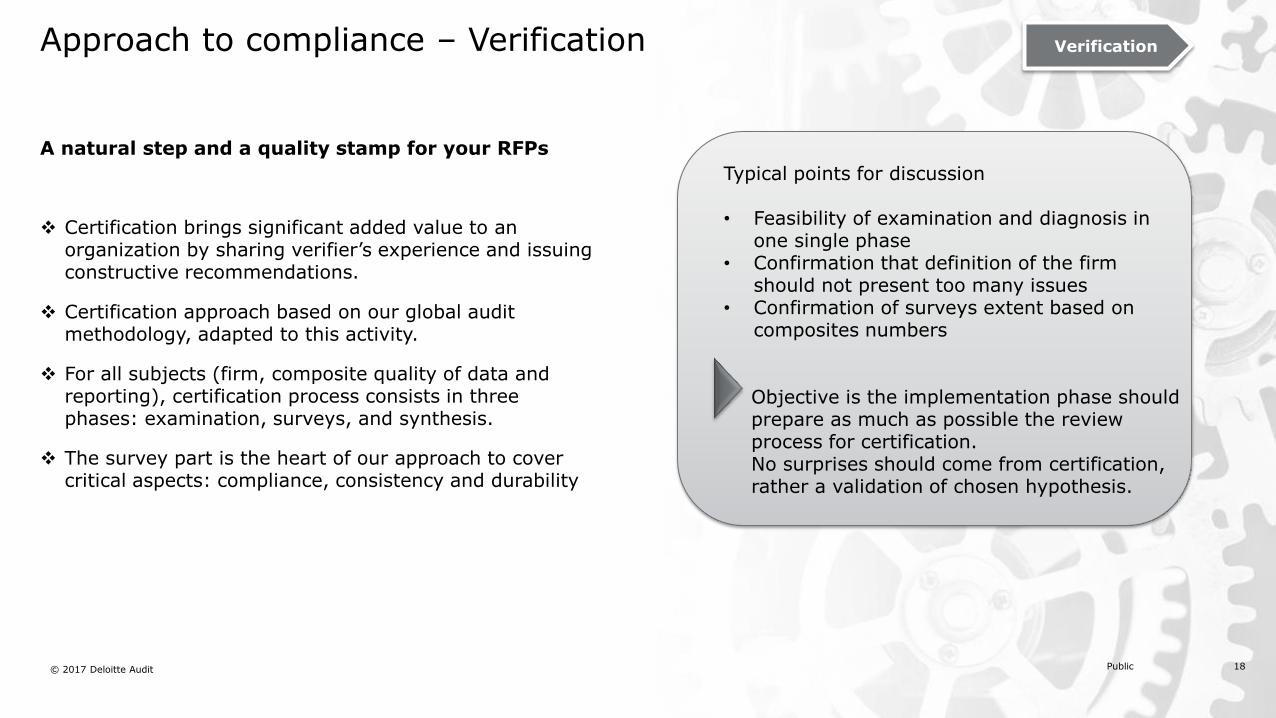

Approach to compliance – Verification

A natural step and a quality stamp for your RFPs

Certification brings significant added value to an organization by sharing verifier’s experience and issuing constructive recommendations.

Certification approach based on our global audit methodology, adapted to this activity.

For all subjects (firm, composite quality of data and reporting), certification process consists in three phases: examination, surveys, and synthesis.

The survey part is the heart of our approach to cover critical aspects: compliance, consistency and durability

Typical points for discussion • Feasibility of examination and diagnosis in

one single phase • Confirmation that definition of the firm

should not present too many issues • Confirmation of surveys extent based on

composites numbers Objective is the implementation phase should prepare as much as possible the review process for certification. No surprises should come from certification, rather a validation of chosen hypothesis.

Verification

19 © 2017 Deloitte Audit

19 Public © 2017 Deloitte Audit

Approach to compliance – Verification Verification

Verification details

Definition of the firm (past & present)

Update of composites

All portfolios are at least in one composite

Definition of non-discretionary management

Relevance of indices

Control of composite inclusion and exclusion dates

Reasonableness of composite

Transfer of portfolios

Calculation methodology and verification of performance

Reliability of information

Validity

Completeness - Validity – Recording – Cut-off

Completeness

Completeness - Validity

Validity

Accounting

Validity - Completeness

Validity – Cut-off

Completeness - Validity

Completeness - Validity

Risks

Consistency of internal organisation and image vis à vis third parties

IT review of database and analysis of modifications

Sample testing for under- or overstatement

Sample testing for over-evaluation

Statistical review

Justification of inclusion and exclusion dates

Substantive testing (statistical review, investment processes analyses …). Testing for understatement

Analysis of modifications

Review of information system and substantive testing

Review of appendices

Response to risks

20 © 2017 Deloitte Audit

20 Public © 2017 Deloitte Audit

Our Performance Measurement Practice

Extensive experience in implementation consulting, assisting clients with GIPS® Standards compliance and verification.

Deloitte has sponsored the Annual AIMR and then GIPS® Conference.

Deloitte has a global GIPS® practice with centers of specialization in Toronto, New York, Boston, London, Paris, Luxembourg

21 © 2017 Deloitte Audit

21 Public © 2017 Deloitte Audit

GIPS® past and present Clients in EMEA

• BNP Paribas

• AGF Asset Management

• Crédit Agricole Asset Management

• Wafa Gestion

• AXA Investment Managers

• Banque Populaire

• Credit Lyonnais Asset Management

• State Street

• CPR Asset Management

• CP2G

• Rothschild

• CDC IXIS Asset Management

• Attijari Management

• SINOPIA

• Overlay Asset Management

• Lyxor

• Allianz

• Natixis

• Unibank

• ABN AMRO

• BlackRock

• LEGG MASON

• RBC

• JPMorgan

• MFS Investment Management

• Julius Bär

• Merrill Lynch

22 © 2017 Deloitte Audit

22 Public © 2017 Deloitte Audit

Your contacts at Deloitte Luxembourg

Marine Maigrat

Associate

Tel: +352 451 454 662

Mail: [email protected]

Audit

Laurent Fedrigo

Partner

Tel: +352 451 452 534

Mail: [email protected]

Audit

Isabelle Pasque

Director

Tel: +352 451 452 760

Mail: [email protected]

Advisory & Consulting

23 Public © 2017 Deloitte Audit

List of required documentation and Q&A

24 Public © 2017 Deloitte Audit

List of required information and documentation

Engagement letter

Verification of the firm

and initial diagnosis

Verification of figures*

• Name of the firm • Contact names and addresses • Supporting documents in order

to understand the Firm, including the corporate structure of the Firm and how it operates

• Assets under Management • System used • Confirmation of independent

valuation process • Sample of performance

calculation • Definition of the firm • Definition of discretionary

management • Complete list of composite

descriptions

• SSAE 16 / ISAE 3402, if any • Audit report of the funds for the

years concerned by the certification

• Copy of the Firm’s policies and procedures used to establish and maintain compliance with the GIPS® standards

• Supporting documents for: • the inception date of the firm

• Details of Assets under Management

• Calculation spreadsheets (incl. adjustments, gross and net of fees)

• Underlying portfolios • Confirmation of the assets by

third party (i.e. custody) • Draft GIPS® report (some

samples provided) • Any supporting documentation

• “in” and “out” portfolios (if any)

• investment policy • discretionary management • allocation to a specific

composite • Independent

* Depending on the results of our tests, we may ask additional supporting documentation

Deloitte is a multidisciplinary service organization which is subject to certain regulatory and professional restrictions on the types of services we can provide to our clients, particularly where an audit relationship exists, as independence issues and other conflicts of interest may arise. Any services we commit to deliver to you will comply fully with applicable restrictions. This communication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte network”) is, by means of this communication, rendering professional advice or services. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. No entity in the Deloitte network shall be responsible for any loss whatsoever sustained by any person who relies on this communication. Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see www.deloitte.com/about for a more detailed description of DTTL and its member firms. Deloitte provides audit, consulting, financial advisory, risk advisory, tax and related services to public and private clients spanning multiple industries. Deloitte serves four out of five Fortune Global 500® companies through a globally connected network of member firms in more than 150 countries bringing world-class capabilities, insights, and high-quality service to address clients’ most complex business challenges. To learn more about how Deloitte’s approximately 245,000 professionals make an impact that matters, please connect with us on Facebook, LinkedIn, or Twitter.

25 Public © 2017 Deloitte Audit