global healthcare trends and outlook •the global pharmaceutical market: description and trends...

TRANSCRIPT

Copyright © 2016 QuintilesIMS. All rights reserved.

Global Healthcare

Trends and Outlook

Joint 23rd Medicines for Europe and

20th IGBA Annual conference

Lisbon June 15th 2017

Alan Sheppard

Principal, Thought Leadership

1

• The global pharmaceutical market: description and trends

• The global generic market trends

• Trends in new launches: innovator products and generic medicines

• Will the future generic medicines launches be sufficient to cope with the high costs of

new innovative medicines?

• Will future biosimilar launches balance the new high cost innovative medicines?

• Summary

Outline

2

We live in difficult times….

Political instability

Ukraine, South Africa, Brazil

Oil price exposure;

depreciating currency

Russia, Nigeria, Venezuela,

Algeria, Brazil

ME and USA IMPACT

Runaway inflation,

default risk

Venezuela, Argentina, Egypt

IP breakdowns,

Bribery Allegations

India, China, Nigeria, Turkey Syria, Turkey, Lebanon, Iraq

EUROPE IMPACT

Refugee crisis

Terrorism

Nigeria, Pakistan, India,

Egypt, Turkey

GLOBAL IMPACT

3

We live in difficult times….

Political instability

Ukraine, South Africa, Brazil

Oil price exposure;

depreciating currency

Russia, Nigeria, Venezuela,

Algeria, Brazil

Runaway inflation,

default risk

Venezuela, Argentina, Egypt

IP breakdowns,

Bribery Allegations

India, China, Nigeria, Turkey Syria, Turkey, Lebanon, Iraq

Refugee crisis

Terrorism

Nigeria, Pakistan, India,

Egypt, Turkey

One constant,

the need for

healthcare

4

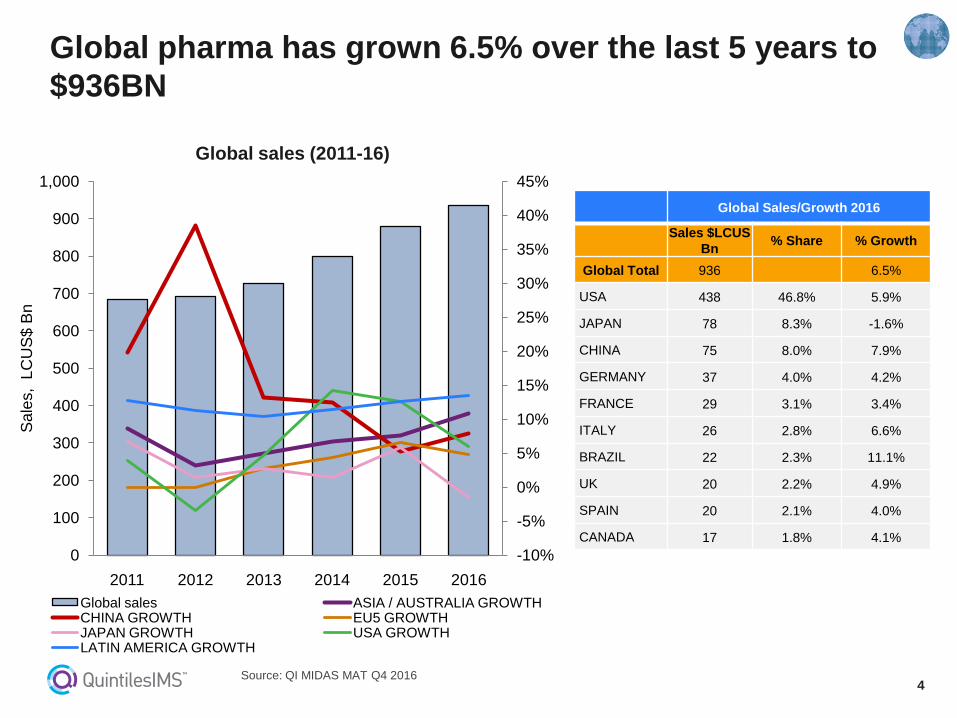

Global pharma has grown 6.5% over the last 5 years to

$936BN

Source: QI MIDAS MAT Q4 2016

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

0

100

200

300

400

500

600

700

800

900

1,000

2011 2012 2013 2014 2015 2016

Sa

les, L

CU

S$

Bn

Global sales ASIA / AUSTRALIA GROWTH CHINA GROWTH EU5 GROWTH JAPAN GROWTH USA GROWTH LATIN AMERICA GROWTH

Global sales (2011-16)

Gro

wth

Global Sales/Growth 2016

Sales $LCUS

Bn % Share % Growth

Global Total 936 6.5%

USA 438 46.8% 5.9%

JAPAN 78 8.3% -1.6%

CHINA 75 8.0% 7.9%

GERMANY 37 4.0% 4.2%

FRANCE 29 3.1% 3.4%

ITALY 26 2.8% 6.6%

BRAZIL 22 2.3% 11.1%

UK 20 2.2% 4.9%

SPAIN 20 2.1% 4.0%

CANADA 17 1.8% 4.1%

5

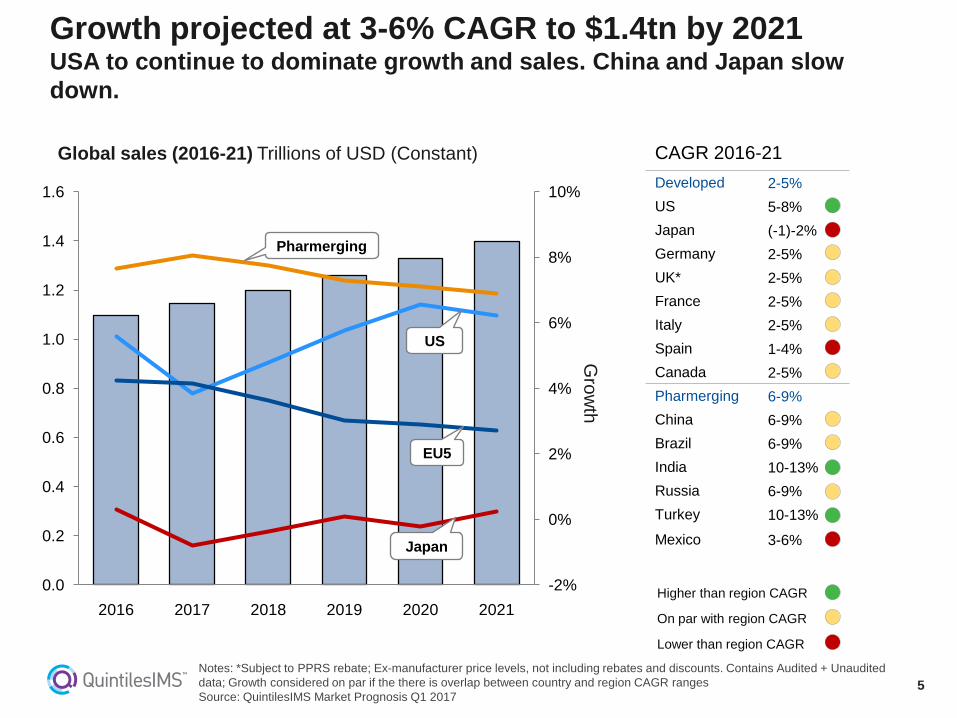

Growth projected at 3-6% CAGR to $1.4tn by 2021 USA to continue to dominate growth and sales. China and Japan slow

down.

Notes: *Subject to PPRS rebate; Ex-manufacturer price levels, not including rebates and discounts. Contains Audited + Unaudited

data; Growth considered on par if the there is overlap between country and region CAGR ranges

Source: QuintilesIMS Market Prognosis Q1 2017

Higher than region CAGR

On par with region CAGR

Lower than region CAGR

-2%

0%

2%

4%

6%

8%

10%

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

2016 2017 2018 2019 2020 2021

Global sales (2016-21) Trillions of USD (Constant)

EU5

US

Pharmerging

Japan

CAGR 2016-21

Developed 2-5%

US 5-8%

Japan (-1)-2%

Germany 2-5%

UK* 2-5%

France 2-5%

Italy 2-5%

Spain 1-4%

Canada 2-5%

Pharmerging 6-9%

China 6-9%

Brazil 6-9%

India 10-13%

Russia 6-9%

Turkey 10-13%

Mexico 3-6%

Gro

wth

6

-2

-1

0

1

2

3

4

5

6

7

8

-2 -1 0 1 2 3 4 5 6 7 8

Fore

ca

st G

row

th %

(C

AG

R 2

01

6-2

021)

Historic Growth % (CAGR 2011-2016)

Norway

Czech Republic

Ireland

Hungary

Denmark

Romania

Portugal

Sweden

Austria

Greece Netherlands Belgium

Switzerland

Poland

Spain

UK*

Italy

France

Germany

Finland

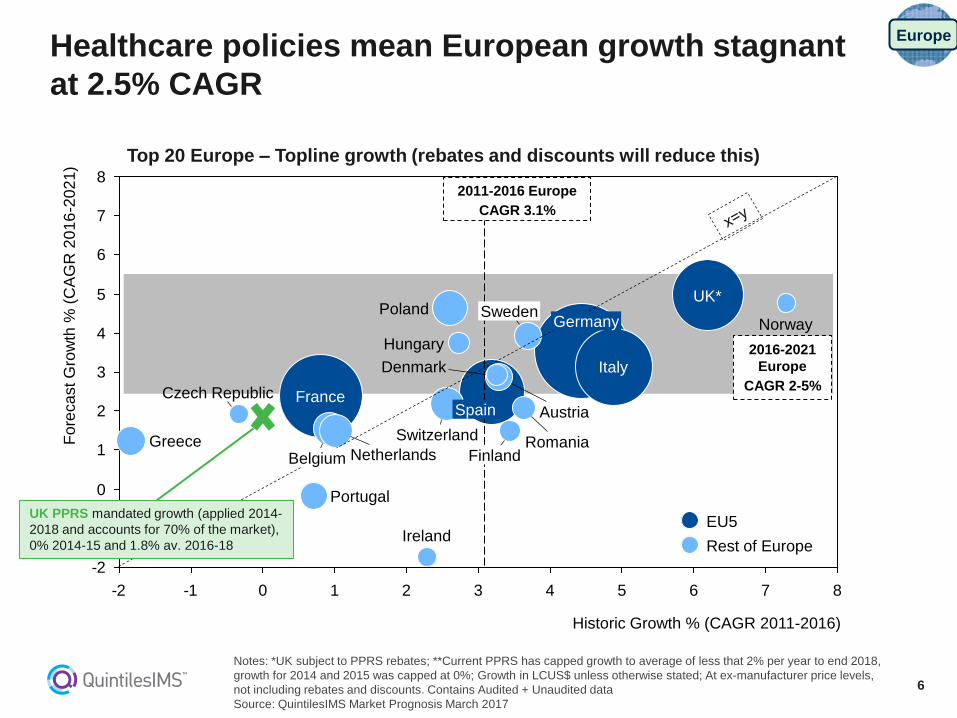

Healthcare policies mean European growth stagnant

at 2.5% CAGR

Notes: *UK subject to PPRS rebates; **Current PPRS has capped growth to average of less that 2% per year to end 2018,

growth for 2014 and 2015 was capped at 0%; Growth in LCUS$ unless otherwise stated; At ex-manufacturer price levels,

not including rebates and discounts. Contains Audited + Unaudited data

Source: QuintilesIMS Market Prognosis March 2017

Rest of Europe

EU5

Top 20 Europe – Topline growth (rebates and discounts will reduce this)

2011-2016 Europe

CAGR 3.1%

2016-2021

Europe

CAGR 2-5%

UK PPRS mandated growth (applied 2014-

2018 and accounts for 70% of the market),

0% 2014-15 and 1.8% av. 2016-18

Europe

7

1

2

3

4

5

6

7

8

9

10

11

12

13

14

2 4 6 8 10 12 14 16 18

Historic CAGR (2011-16)

Fore

ca

st C

AG

R (

20

16

-21

)

Kazakhstan Nigeria

Chile

South Africa

Bangladesh

Algeria

Philippines Colombia

Egypt

Vietnam

Pakistan

Indonesia

Poland

Saudi Arabia

Mexico

Turkey

Russia

India

Brazil

China

Wide dispersion in growth but CAGR falls to single

digits…China dominates but moderating

Notes: At ex-manufacturer price levels, not including rebates and discounts. Contains Audited and Unaudited data;

Argentina excluded due to hyperinflation

Source: QuintilesIMS Market Prognosis March 2017

BRICTM Pharmerging Tier 3

Bubble Size proportional to

2016 LCUS$ Sales

Top 20 Pharmerging Markets Forecast Growth Dynamics

Pharmerging Forecast

CAGR: 7.4%

Pharmerging Historic

CAGR: 10.8%

Pharmerging

$100bn

$20bn

$7bn

8

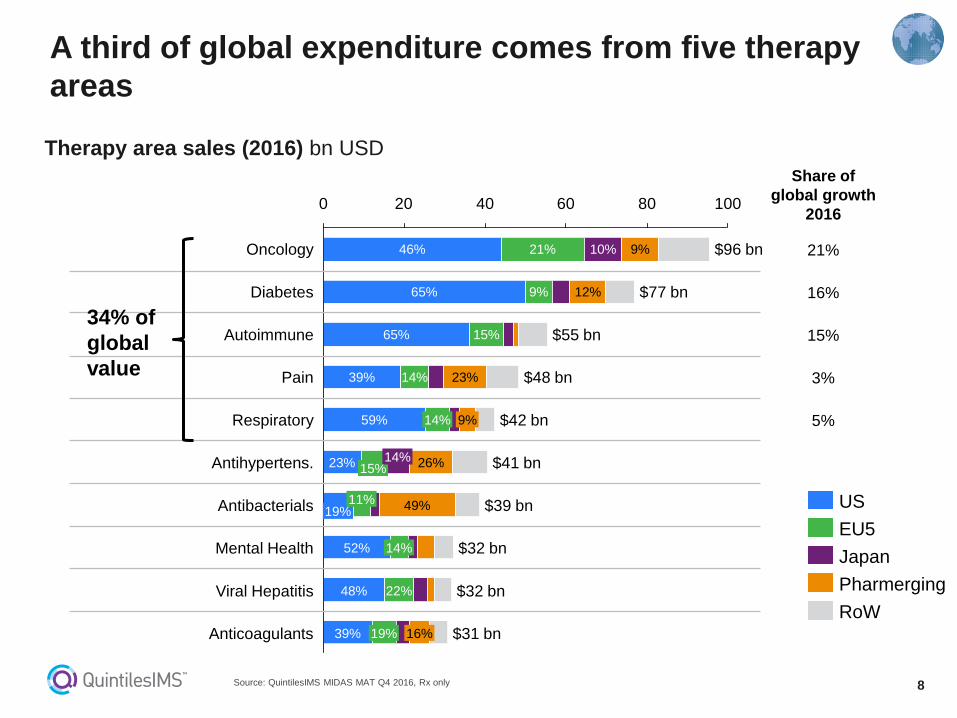

A third of global expenditure comes from five therapy

areas

Source: QuintilesIMS MIDAS MAT Q4 2016, Rx only

80 0 20 60 40 100

Pain

26%

65% $55 bn

9%

65%

$48 bn

10%

$77 bn

Oncology $96 bn

23%

46%

9%

39%

19% $39 bn

$41 bn

Antibacterials

Antihypertens.

12%

$32 bn

49% 11%

23%

52% 14%

$42 bn 59%

15%

Respiratory 9%

14%

Mental Health

Diabetes

19%

$32 bn

$31 bn Anticoagulants

21%

15%

Viral Hepatitis

14%

14%

Autoimmune

16%

48%

39%

22%

US

Pharmerging

Japan

EU5

RoW

Share of

global growth

2016

21%

16%

15%

3%

5%

34% of

global

value

Therapy area sales (2016) bn USD

9

Over 60% of global growth comes from just five TAs

Source: QuintilesIMS MIDAS MAT Q4 2016, Rx only

12 10 8 6 4 2 0 -2

1.4

Pain 1.6

Nervous System 1.7 73%

GI 1.7 59%

Respiratory 2.8 76%

HIV 3.0 86%

Anticoagulants 3.9 64%

Autoimmune 8.7 79% 10%

Diabetes 9.3 80%

Oncology 11.7 53% 21%

68%

145%

MS

-44% All Others

Pharmerging

Japan

EU5

US

Share of

global growth

2016

21%

16%

15%

7%

5%

5%

3%

3%

3%

3%

64% of

global

growth

Absolute one year growth 2016

(LCUS$ Bn)

Concentration has reduced

from the previous iteration (73%

in top 5 TAs) because we have

passed peak Hepatitis C

10

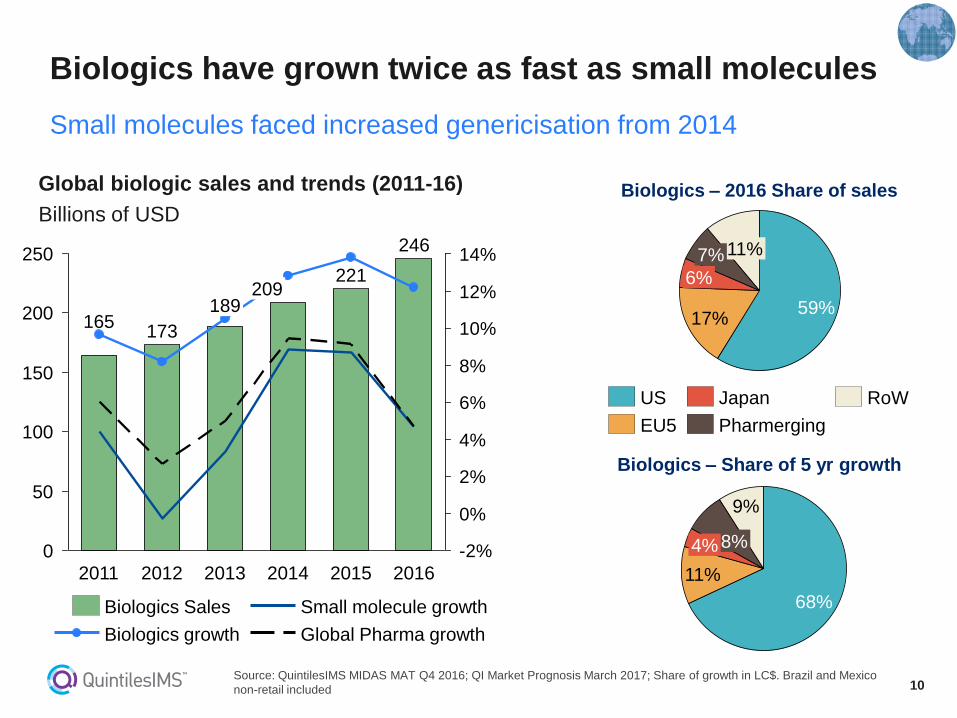

Biologics have grown twice as fast as small molecules

Small molecules faced increased genericisation from 2014

Source: QuintilesIMS MIDAS MAT Q4 2016; QI Market Prognosis March 2017; Share of growth in LC$. Brazil and Mexico

non-retail included

Global biologic sales and trends (2011-16)

Billions of USD Biologics – 2016 Share of sales

Biologics – Share of 5 yr growth

-2%

0%

2%

4%

6%

8%

10%

12%

14%

150

0

100

50

200

250

189

2012

246

209

2014 2013

221

2016 2015

173

2011

165

Global Pharma growth Biologics growth

Small molecule growth Biologics Sales

11%

59%

6%

7%

17%

8% 4%

11%

9%

68%

US

EU5

Japan RoW

Pharmerging

11

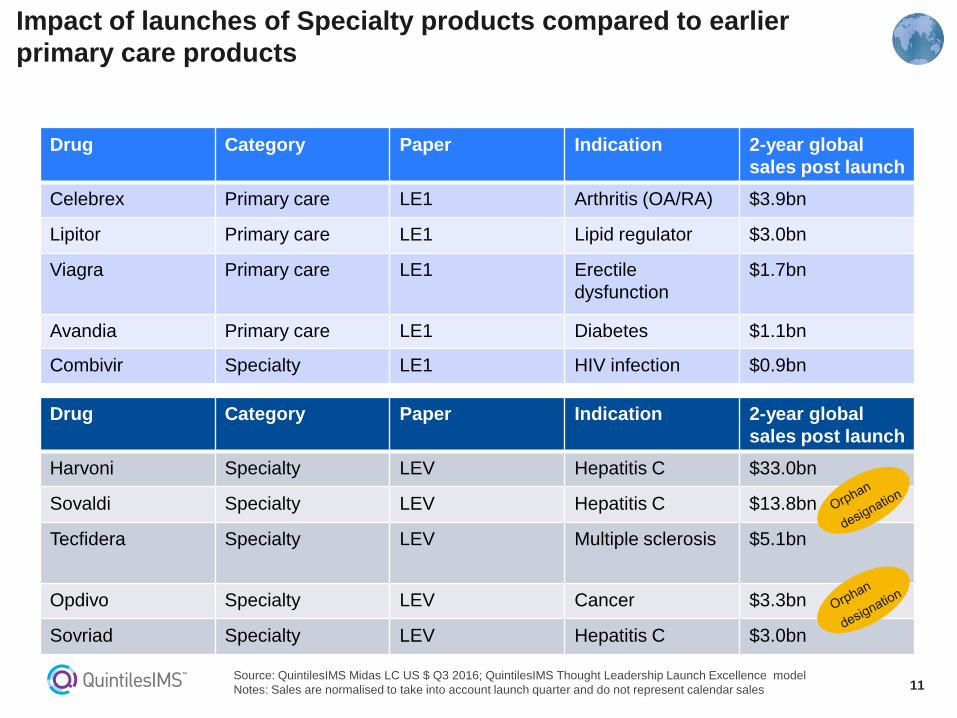

Drug Category Paper Indication 2-year global

sales post launch

Celebrex Primary care LE1 Arthritis (OA/RA) $3.9bn

Lipitor Primary care LE1 Lipid regulator $3.0bn

Viagra Primary care LE1 Erectile

dysfunction

$1.7bn

Avandia Primary care LE1 Diabetes $1.1bn

Combivir Specialty LE1 HIV infection $0.9bn

Impact of launches of Specialty products compared to earlier

primary care products

Source: QuintilesIMS Midas LC US $ Q3 2016; QuintilesIMS Thought Leadership Launch Excellence model

Notes: Sales are normalised to take into account launch quarter and do not represent calendar sales

Drug Category Paper Indication 2-year global

sales post launch

Harvoni Specialty LEV Hepatitis C $33.0bn

Sovaldi Specialty LEV Hepatitis C $13.8bn

Tecfidera Specialty LEV Multiple sclerosis $5.1bn

Opdivo Specialty LEV Cancer $3.3bn

Sovriad Specialty LEV Hepatitis C $3.0bn

12

• The global pharmaceutical market: description and trends

• The global generic market trends

• Trends in new launches: innovator products and generic medicines

• Will the future generic medicines launches be sufficient to cope with the high costs of

new innovative medicines?

• Will future biosimilar launches balance the new high cost innovative medicines?

• Summary

Outline

13

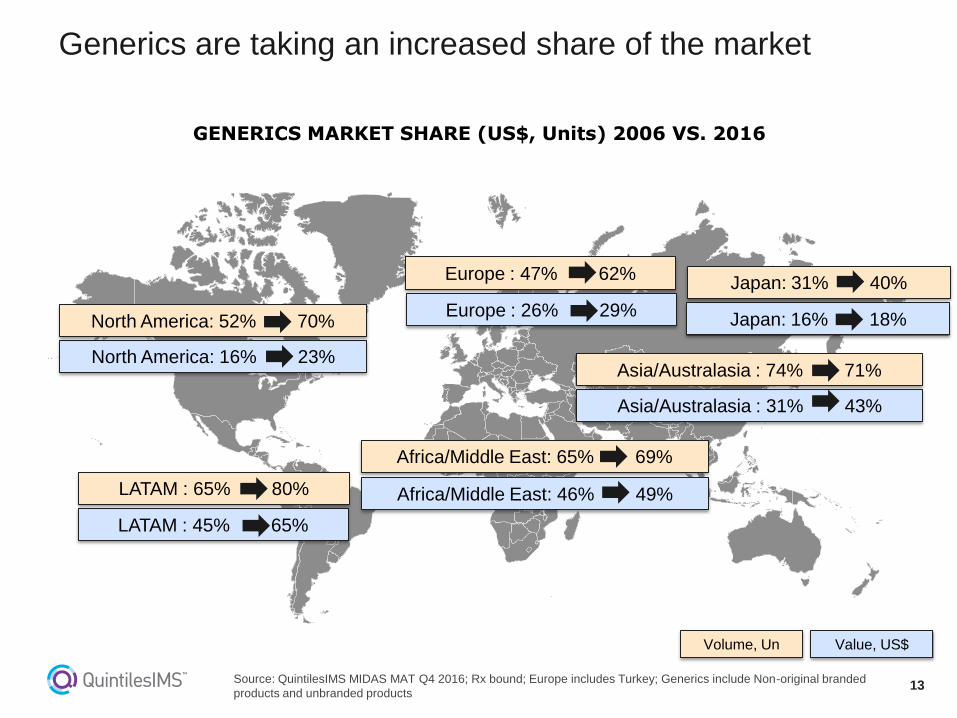

Generics are taking an increased share of the market

GENERICS MARKET SHARE (US$, Units) 2006 VS. 2016

LATAM : 45% 65%

Africa/Middle East: 46% 49%

Asia/Australasia : 31% 43%

Europe : 26% 29%

North America: 16% 23%

Japan: 16% 18%

Source: QuintilesIMS MIDAS MAT Q4 2016; Rx bound; Europe includes Turkey; Generics include Non-original branded

products and unbranded products

North America: 52% 70%

Europe : 47% 62% Japan: 31% 40%

Asia/Australasia : 74% 71%

Africa/Middle East: 65% 69%

LATAM : 65% 80%

Volume, Un Value, US$

14

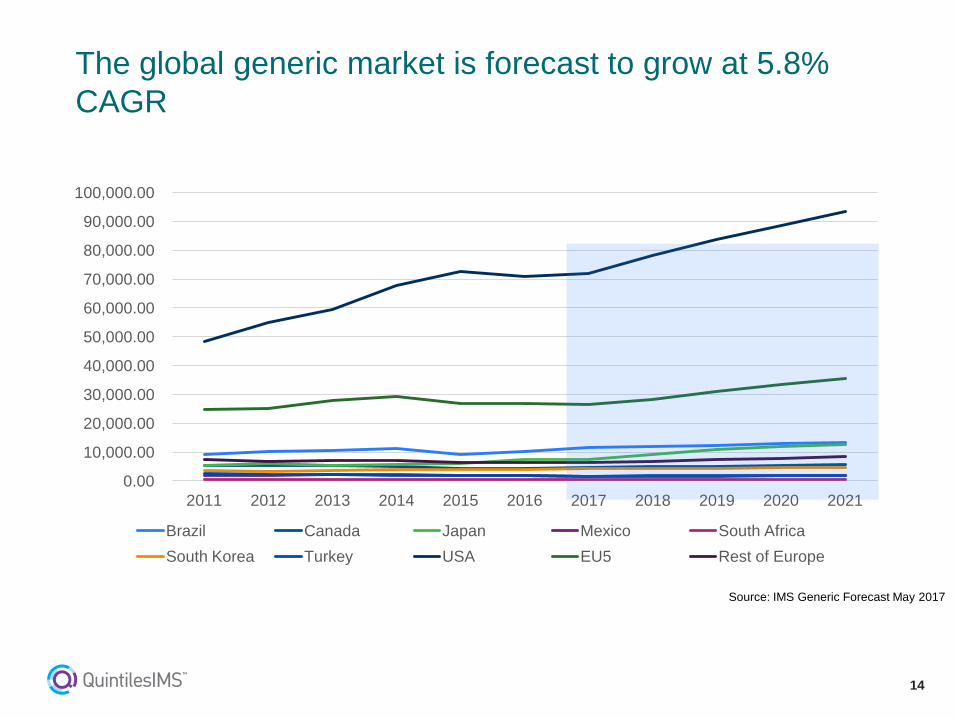

The global generic market is forecast to grow at 5.8%

CAGR

0.00

10,000.00

20,000.00

30,000.00

40,000.00

50,000.00

60,000.00

70,000.00

80,000.00

90,000.00

100,000.00

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021

Brazil Canada Japan Mexico South Africa

South Korea Turkey USA EU5 Rest of Europe

Source: IMS Generic Forecast May 2017

15

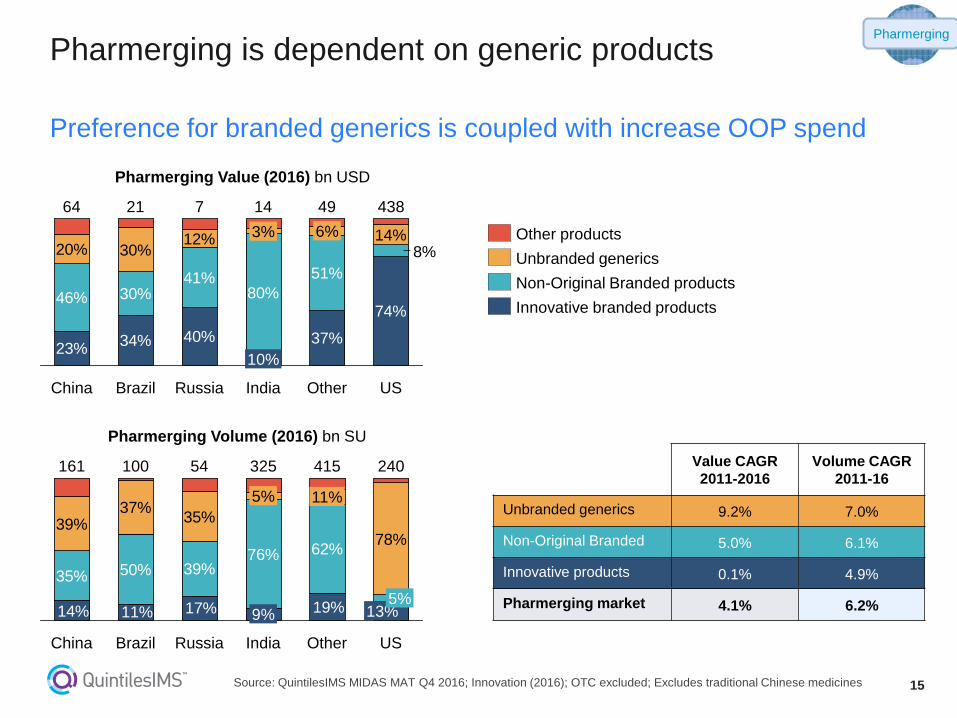

Preference for branded generics is coupled with increase OOP spend

Pharmerging is dependent on generic products

Source: QuintilesIMS MIDAS MAT Q4 2016; Innovation (2016); OTC excluded; Excludes traditional Chinese medicines

23%34% 40% 37%

74%46% 30%

41%

20% 30%12% 14%

80%

8%

51%

US

438

Other

49

6%

India

14

10%

3%

Russia

7

Brazil

21

China

64

Unbranded generics

Innovative branded products

Other products

Non-Original Branded products

35% 50% 39%76% 62%

39% 35%

78%

17% 19%11%14%

37%

Russia

161 415

China India

325

11%

Other

13%

240 54

5%

US

5%

100

9%

Brazil

Pharmerging

Value CAGR

2011-2016

Volume CAGR

2011-16

Unbranded generics 9.2% 7.0%

Non-Original Branded 5.0% 6.1%

Innovative products 0.1% 4.9%

Pharmerging market 4.1% 6.2%

Pharmerging Value (2016) bn USD

Pharmerging Volume (2016) bn SU

16

• Affordability

• Headroom in budgets for newer treatments

• Treatment guidelines

• Incentives/ budgets for prescribers

• Patient co-payments

• Earnings for pharmacist

• Products coming off patent

What is driving the generic market?

17

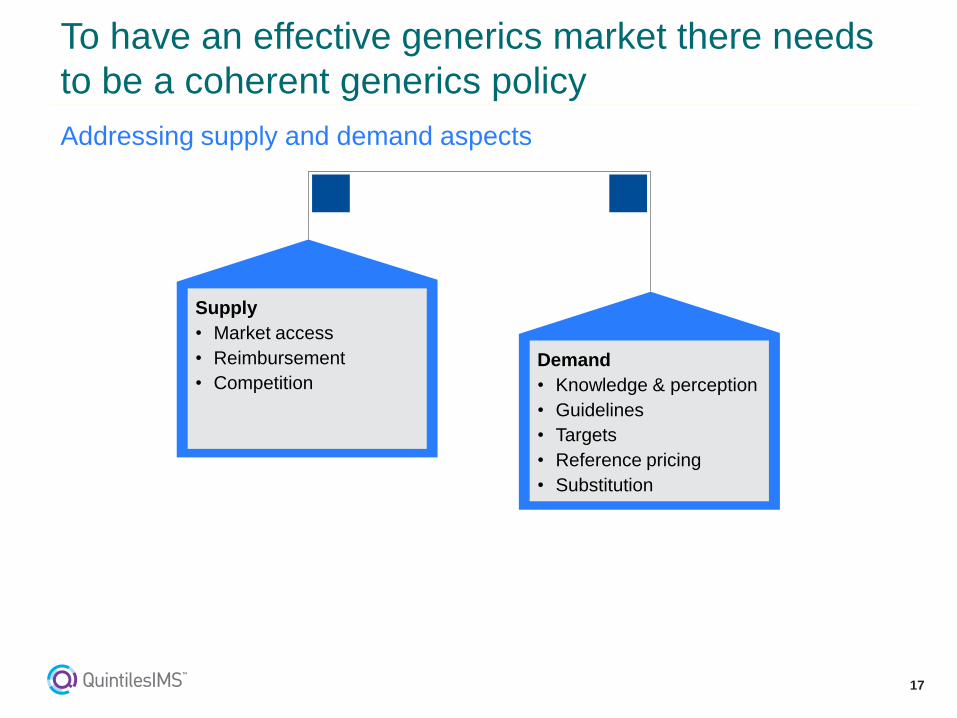

To have an effective generics market there needs

to be a coherent generics policy

Addressing supply and demand aspects

Supply

• Market access

• Reimbursement

• Competition

Demand

• Knowledge & perception

• Guidelines

• Targets

• Reference pricing

• Substitution

18

• The global pharmaceutical market: description and trends

• The global generic market trends

• Trends in new launches: innovator products and generic medicines

• Will the future generic medicines launches be sufficient to cope with the high costs of

new innovative medicines?

• Will future biosimilar launches balance the new high cost innovative medicines?

• Summary

Outline

19

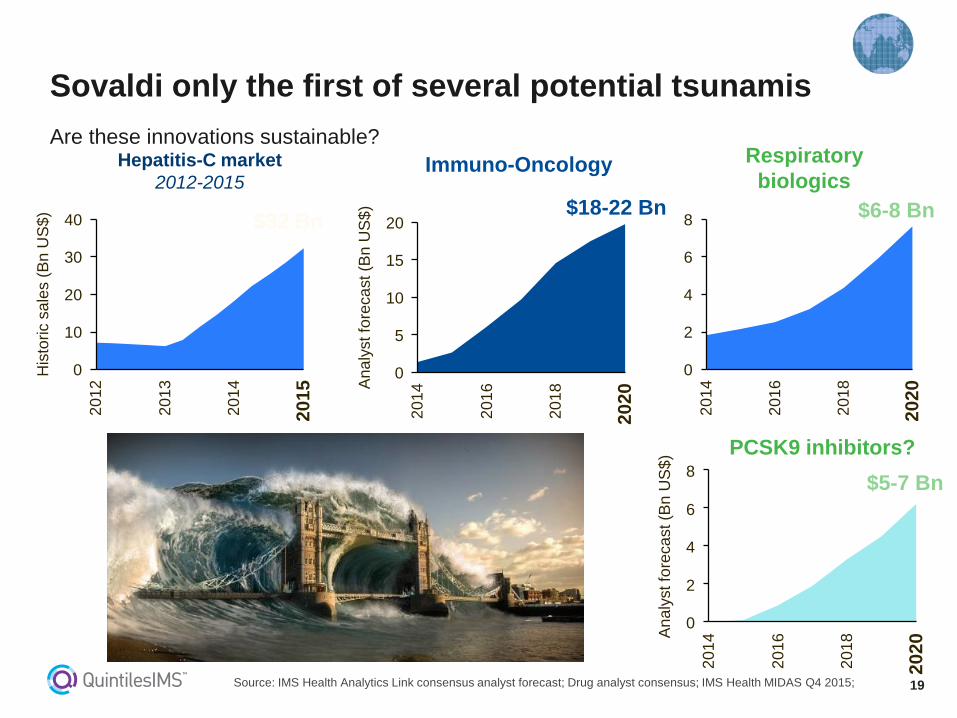

Are these innovations sustainable?

Sovaldi only the first of several potential tsunamis

Source: IMS Health Analytics Link consensus analyst forecast; Drug analyst consensus; IMS Health MIDAS Q4 2015;

20

15

10

5

0 A

na

lyst fo

reca

st (B

n U

S$

)

2020

20

18

20

16

20

14

$18-22 Bn

8

6

4

2

0

An

aly

st fo

reca

st (B

n U

S$

)

2020

20

18

20

16

20

14

$5-7 Bn

8

6

4

2

0

2020

20

18

20

16

20

14

$6-8 Bn

Immuno-Oncology Respiratory

biologics

PCSK9 inhibitors?

40

30

20

10

0 His

toric s

ale

s (

Bn

US

$)

2015

20

14

20

13

20

12

Hepatitis-C market

2012-2015

$32 Bn

20

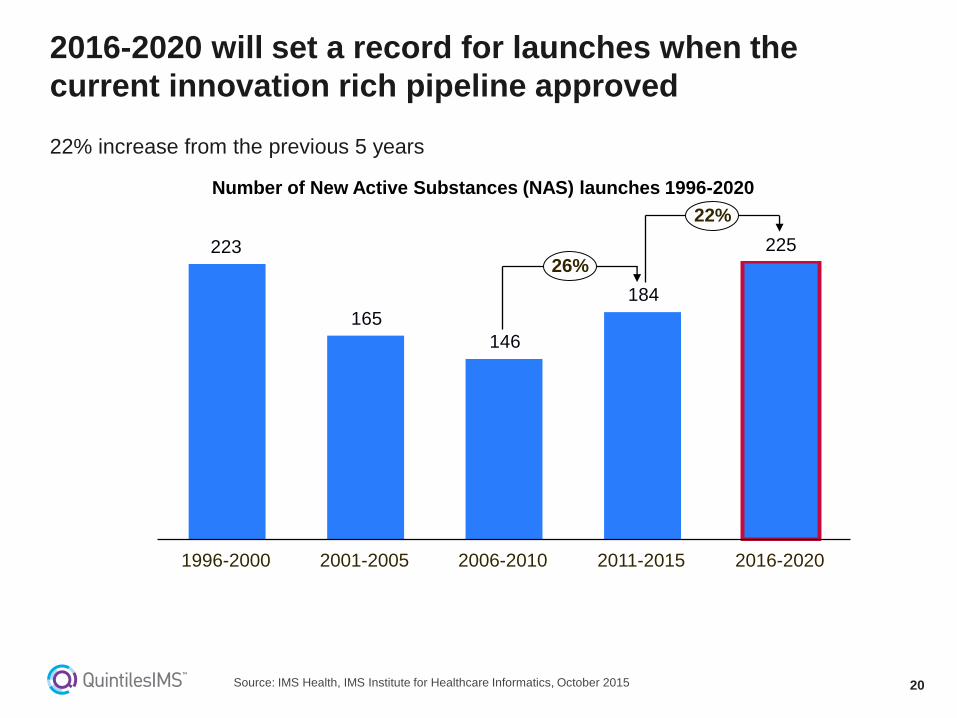

22% increase from the previous 5 years

2016-2020 will set a record for launches when the

current innovation rich pipeline approved

Source: IMS Health, IMS Institute for Healthcare Informatics, October 2015

Number of New Active Substances (NAS) launches 1996-2020

223

165

146

184

225 26%

22%

2016-2020 2011-2015 2006-2010 2001-2005 1996-2000

21

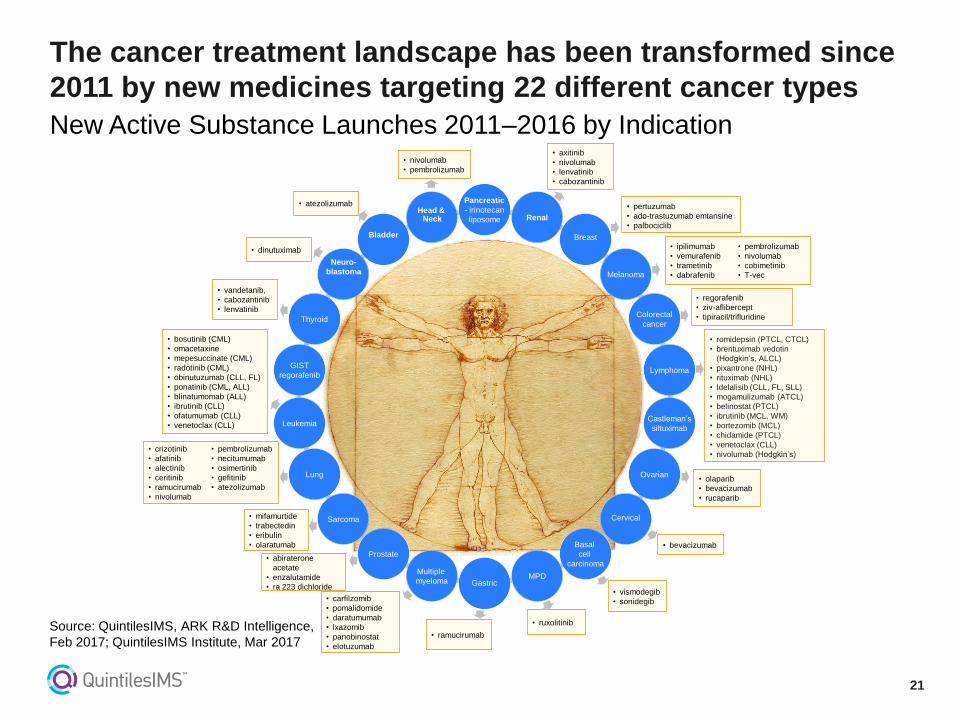

The cancer treatment landscape has been transformed since

2011 by new medicines targeting 22 different cancer types

New Active Substance Launches 2011–2016 by Indication

Pancreatic

- irinotecan

liposome

Neuro-

blastoma

Thyroid

GIST

regorafenib

Leukemia

Lung

Sarcoma

Prostate

Multiple

myeloma Gastric MPD

Basal

cell

carcinoma

Cervical

Ovarian

Castleman’s

siltuximab

Lymphoma

Colorectal

cancer

Melanoma

Breast

Renal

Bladder

Head & Neck

• axitinib

• nivolumab

• lenvatinib

• cabozantinib

• pertuzumab

• ado-trastuzumab emtansine

• palbociclib

• ipilimumab

• vemurafenib

• trametinib

• dabrafenib

• pembrolizumab

• nivolumab

• cobimetinib

• T-vec

• regorafenib

• ziv-aflibercept

• tipiracil/trifluridine

• romidepsin (PTCL, CTCL)

• brentuximab vedotin

(Hodgkin’s, ALCL)

• pixantrone (NHL)

• rituximab (NHL)

• Idelalisib (CLL, FL, SLL)

• mogamulizumab (ATCL)

• belinostat (PTCL)

• ibrutinib (MCL, WM)

• bortezomib (MCL)

• chidamide (PTCL)

• venetoclax (CLL)

• nivolumab (Hodgkin’s)

• olaparib

• bevacizumab

• rucaparib

• vismodegib

• sonidegib • carfilzomib

• pomalidomide

• daratumumab

• lxazomib

• panobinostat

• elotuzumab

• abiraterone

acetate

• enzalutamide

• ra 223 dichloride

• mifamurtide

• trabectedin

• eribulin

• olaratumab

• crizotinib

• afatinib

• alectinib

• ceritinib

• ramucirumab

• nivolumab

• pembrolizumab

• necitumumab

• osimertinib

• gefitinib

• atezolizumab

• bosutinib (CML)

• omacetaxine

• mepesuccinate (CML)

• radotinib (CML)

• obinutuzumab (CLL, FL)

• ponatinib (CML, ALL)

• blinatumomab (ALL)

• ibrutinib (CLL)

• ofatumumab (CLL)

• venetoclax (CLL)

• vandetanib,

• cabozantinib

• lenvatinib

• dinutuximab

• atezolizumab

• nivolumab

• pembrolizumab

• ramucirumab

• ruxolitinib

• bevacizumab

Source: QuintilesIMS, ARK R&D Intelligence,

Feb 2017; QuintilesIMS Institute, Mar 2017

22

3

2

2

1

4

6

1

CLL

Melanoma

Lung Cancer

Prostate Cancer

Breast Cancer

HER2 Hormonals Chemotherapy CDK

Others Immunotherapy EGFR ALK

BRAF Anti-CD Other small molecules

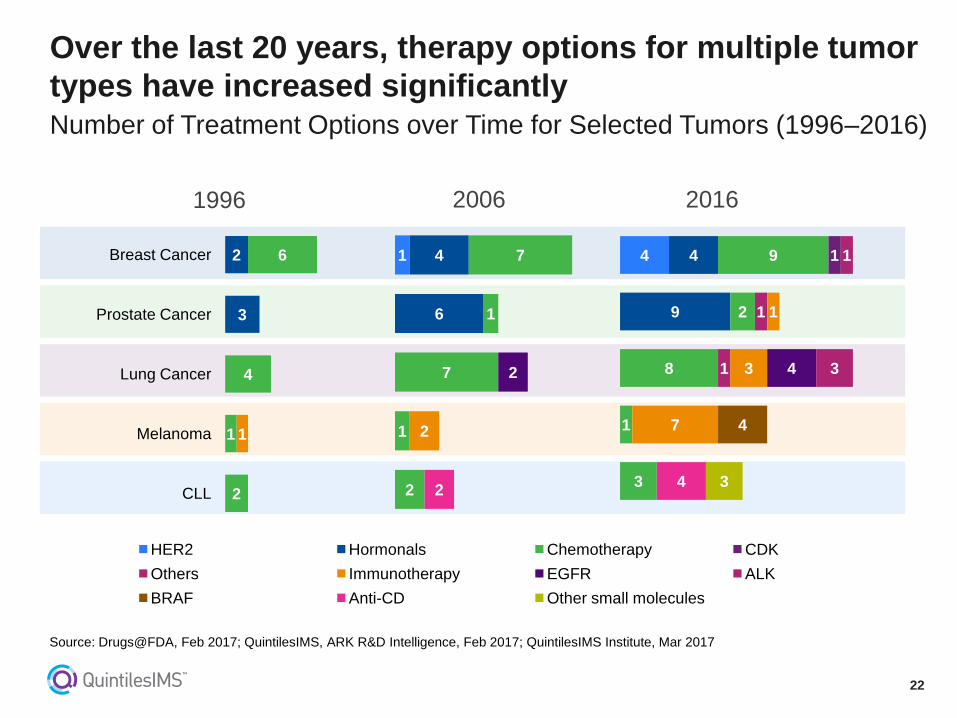

Over the last 20 years, therapy options for multiple tumor

types have increased significantly Number of Treatment Options over Time for Selected Tumors (1996–2016)

1996

Source: Drugs@FDA, Feb 2017; QuintilesIMS, ARK R&D Intelligence, Feb 2017; QuintilesIMS Institute, Mar 2017

1

6

4

2

1

7

1

7

2

2

2

4

9

4

3

1

8

2

9 1

1

1

1

7

3

1

4 3

4

4 3

2006 2016

23

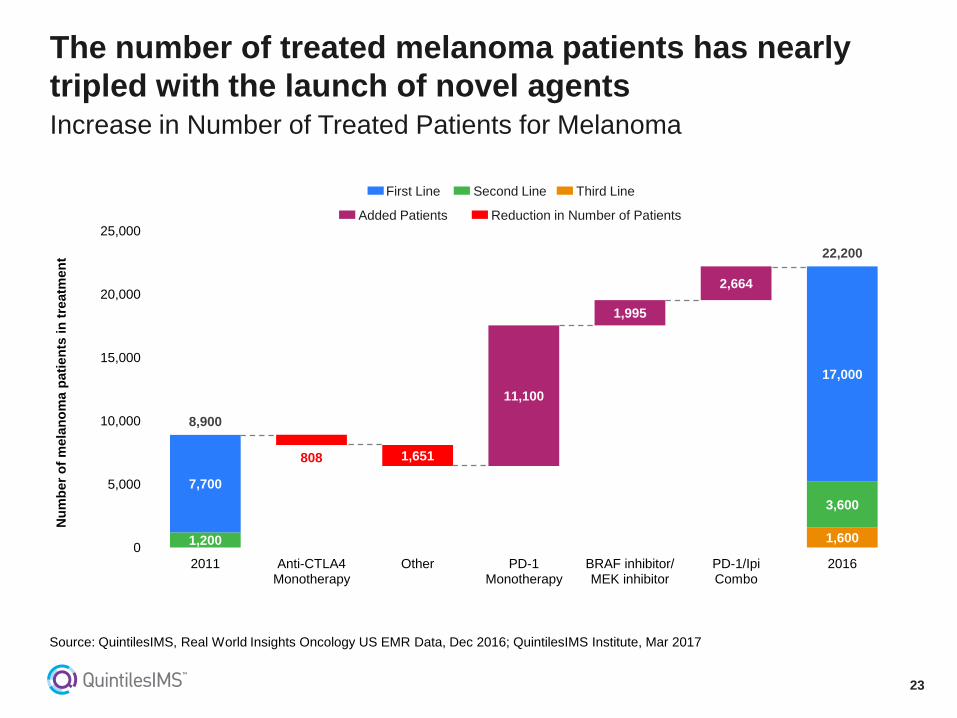

1,200

808 1,651

11,100

1,995

2,664

1,600

7,700

3,600

17,000

8,900

22,200

0

5,000

10,000

15,000

20,000

25,000

2011 Anti-CTLA4 Monotherapy

Other PD-1 Monotherapy

BRAF inhibitor/ MEK inhibitor

PD-1/Ipi Combo

2016

Nu

mb

er

of

mela

no

ma p

ati

en

ts i

n t

reatm

en

t The number of treated melanoma patients has nearly

tripled with the launch of novel agents Increase in Number of Treated Patients for Melanoma

Source: QuintilesIMS, Real World Insights Oncology US EMR Data, Dec 2016; QuintilesIMS Institute, Mar 2017

First Line Second Line Third Line

Added Patients Reduction in Number of Patients

24

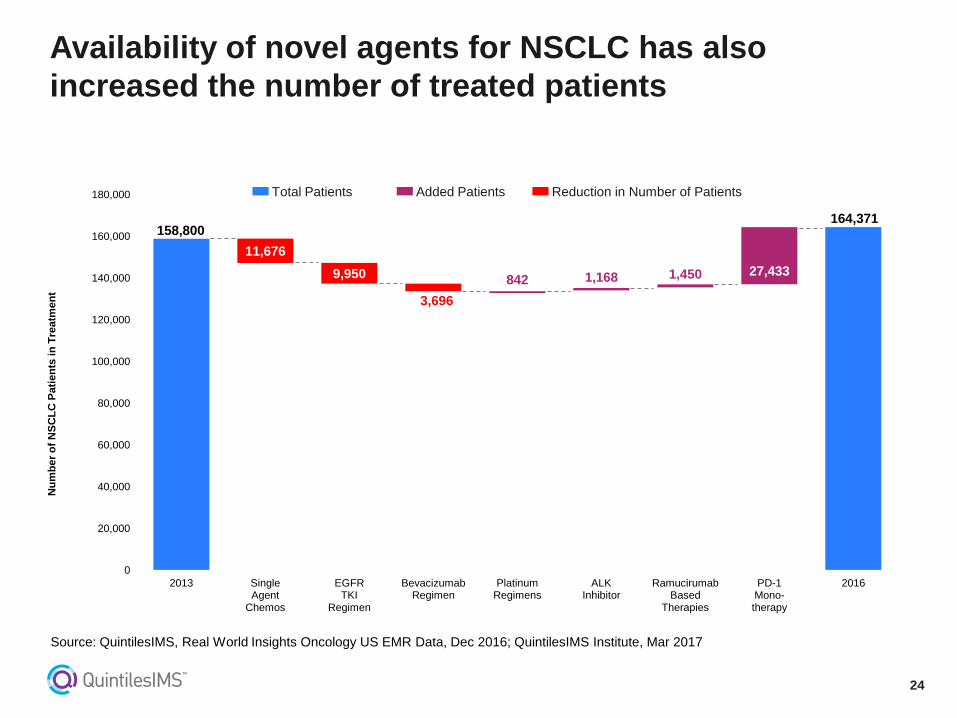

Availability of novel agents for NSCLC has also

increased the number of treated patients

158,800

11,676

9,950

3,696

842 1,168 1,450 27,433

164,371

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

2013 Single Agent

Chemos

EGFR TKI

Regimen

Bevacizumab Regimen

Platinum Regimens

ALK Inhibitor

Ramucirumab Based

Therapies

PD-1 Mono- therapy

2016

Nu

mb

er

of

NS

CL

C P

ati

en

ts in

Tre

atm

en

t

Added Patients Reduction in Number of Patients Total Patients

Source: QuintilesIMS, Real World Insights Oncology US EMR Data, Dec 2016; QuintilesIMS Institute, Mar 2017

25

The global R&D pipeline for oncology remains robust

with 631 unique molecules in late-phase development Global Late Phase Oncology Pipeline in 2016

Source: QuintilesIMS ARK R&D Intelligence, QuintilesIMS Institute, Dec 2016

39

139

453

391

191

79

544

Phase II

Phase III

Pre-Reg/ Registered

Late Phase Active Pipeline

Phase II Phase III Pre-Reg/Registered

Molecules in the Late Phase Pipeline: 631 Companies with a Late Phase Pipeline: 544

26

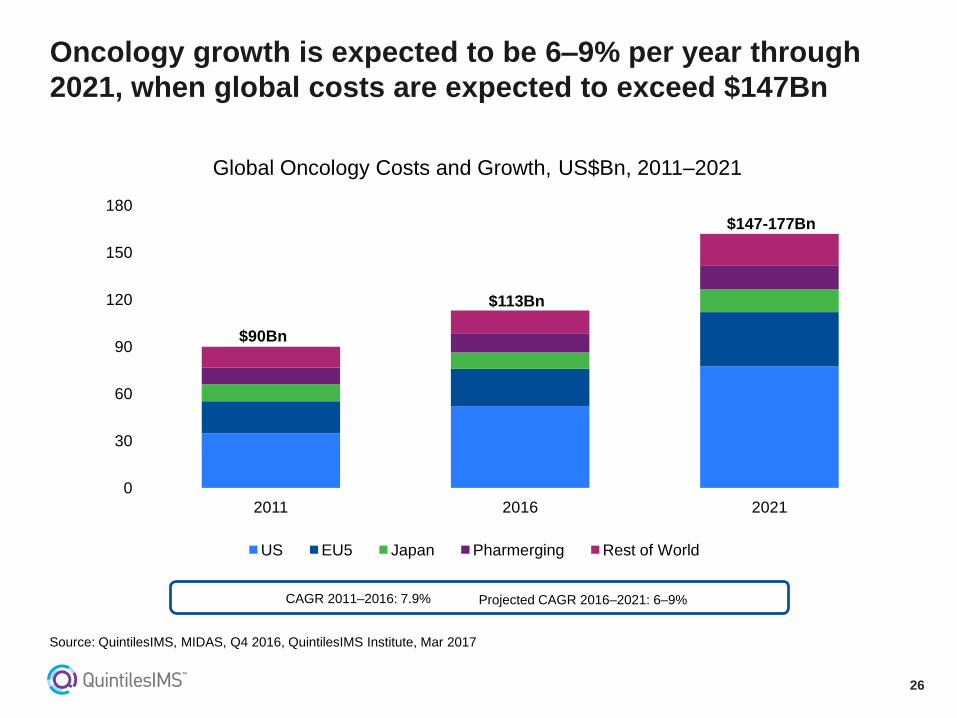

Oncology growth is expected to be 6–9% per year through

2021, when global costs are expected to exceed $147Bn

Global Oncology Costs and Growth, US$Bn, 2011–2021

0

30

60

90

120

150

180

2011 2016 2021

US EU5 Japan Pharmerging Rest of World

$90Bn

$113Bn

$147-177Bn

CAGR 2011–2016: 7.9% Projected CAGR 2016–2021: 6–9%

Source: QuintilesIMS, MIDAS, Q4 2016, QuintilesIMS Institute, Mar 2017

27

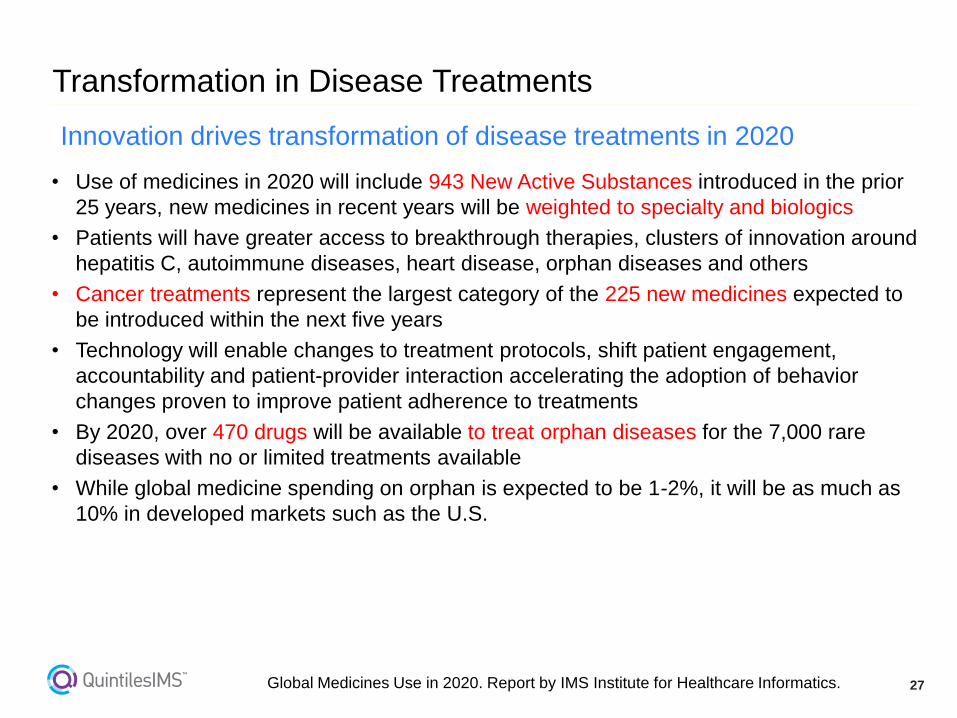

• Use of medicines in 2020 will include 943 New Active Substances introduced in the prior

25 years, new medicines in recent years will be weighted to specialty and biologics

• Patients will have greater access to breakthrough therapies, clusters of innovation around

hepatitis C, autoimmune diseases, heart disease, orphan diseases and others

• Cancer treatments represent the largest category of the 225 new medicines expected to

be introduced within the next five years

• Technology will enable changes to treatment protocols, shift patient engagement,

accountability and patient-provider interaction accelerating the adoption of behavior

changes proven to improve patient adherence to treatments

• By 2020, over 470 drugs will be available to treat orphan diseases for the 7,000 rare

diseases with no or limited treatments available

• While global medicine spending on orphan is expected to be 1-2%, it will be as much as

10% in developed markets such as the U.S.

Global Medicines Use in 2020. Report by IMS Institute for Healthcare Informatics.

Transformation in Disease Treatments

Innovation drives transformation of disease treatments in 2020

28

• The global pharmaceutical market: description and trends

• The global generic market trends

• Trends in new launches: innovator products and generic medicines

• Will the future generic medicines launches be sufficient to cope with the high

costs of new innovative medicines?

• Will future biosimilar launches balance the new high cost innovative medicines?

• Summary

Outline

29

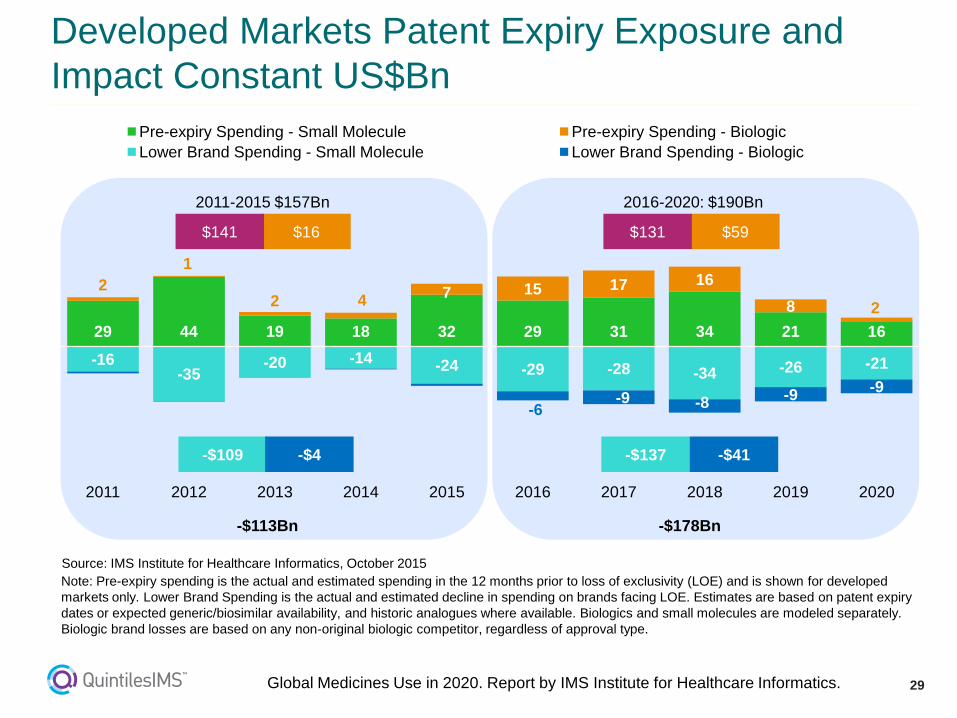

29 44 19 18 32 29 31 34 21 16

2

1

2 4 7 15 17 16

8 2

-16 -35

-20 -14 -24 -29 -28 -34 -26 -21

-6 -9 -8

-9 -9

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Pre-expiry Spending - Small Molecule Pre-expiry Spending - Biologic

Lower Brand Spending - Small Molecule Lower Brand Spending - Biologic

Developed Markets Patent Expiry Exposure and

Impact Constant US$Bn

Source: IMS Institute for Healthcare Informatics, October 2015

$16 $59 $141 $131

-$109 -$137 -$4 -$41

2011-2015 $157Bn 2016-2020: $190Bn

-$113Bn -$178Bn

Note: Pre-expiry spending is the actual and estimated spending in the 12 months prior to loss of exclusivity (LOE) and is shown for developed

markets only. Lower Brand Spending is the actual and estimated decline in spending on brands facing LOE. Estimates are based on patent expiry

dates or expected generic/biosimilar availability, and historic analogues where available. Biologics and small molecules are modeled separately.

Biologic brand losses are based on any non-original biologic competitor, regardless of approval type.

Global Medicines Use in 2020. Report by IMS Institute for Healthcare Informatics.

30

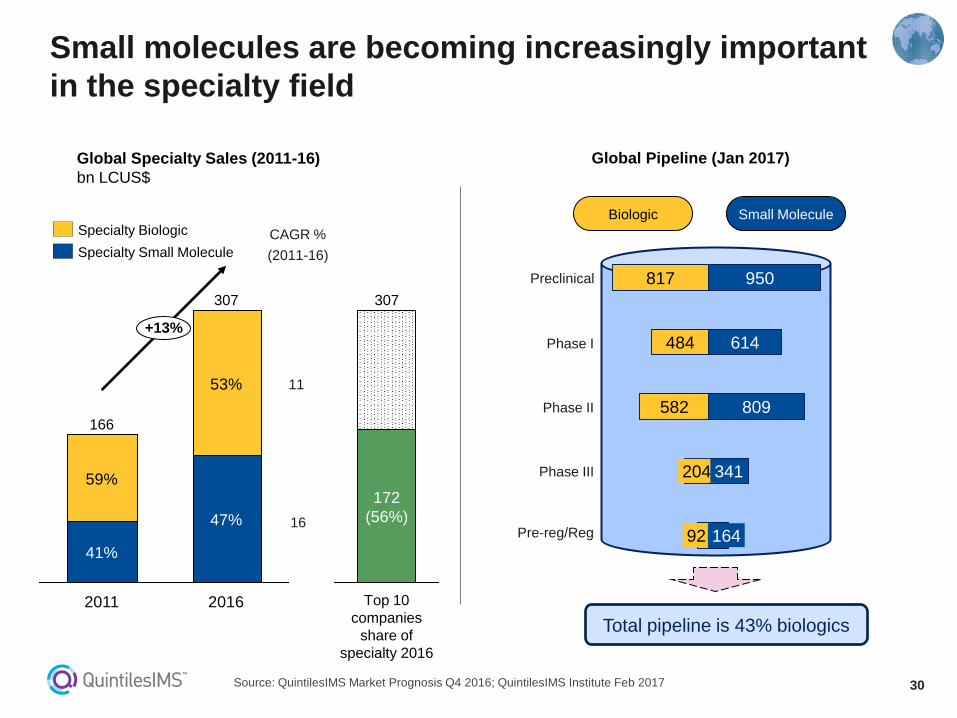

Small molecules are becoming increasingly important

in the specialty field

Source: QuintilesIMS Market Prognosis Q4 2016; QuintilesIMS Institute Feb 2017

Global Pipeline (Jan 2017)

92

204

582

484

817

164

341

809

614

950

Small Molecule Biologic

Pre-reg/Reg

Preclinical

Phase I

Phase II

Phase III

Global Specialty Sales (2011-16)

bn LCUS$

2016

307

+13%

166

41%

53%

2011

59%

47%

11

16

CAGR %

(2011-16)

Specialty Biologic

Specialty Small Molecule

Total pipeline is 43% biologics

Top 10

companies

share of

specialty 2016

172

(56%)

307

31

• The global pharmaceutical market: description and trends

• The global generic market trends

• Trends in new launches: innovator products and generic medicines

• Will the future generic medicines launches be sufficient to cope with the high costs of

new innovative medicines?

• Will future biosimilar launches balance the new high cost innovative medicines?

• Summary

Outline

32

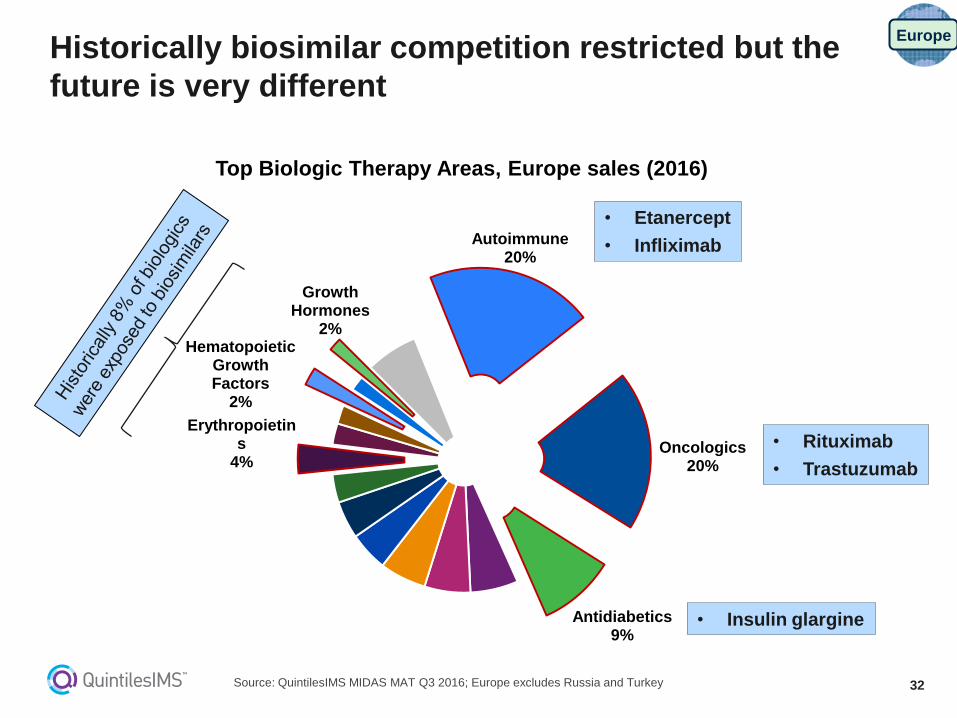

Historically biosimilar competition restricted but the

future is very different

Source: QuintilesIMS MIDAS MAT Q3 2016; Europe excludes Russia and Turkey

Autoimmune 20%

Oncologics 20%

Antidiabetics 9%

Erythropoietins

4%

Hematopoietic Growth Factors

2%

Growth Hormones

2%

• Rituximab

• Trastuzumab

• Etanercept

• Infliximab

• Insulin glargine

Top Biologic Therapy Areas, Europe sales (2016)

Europe

33

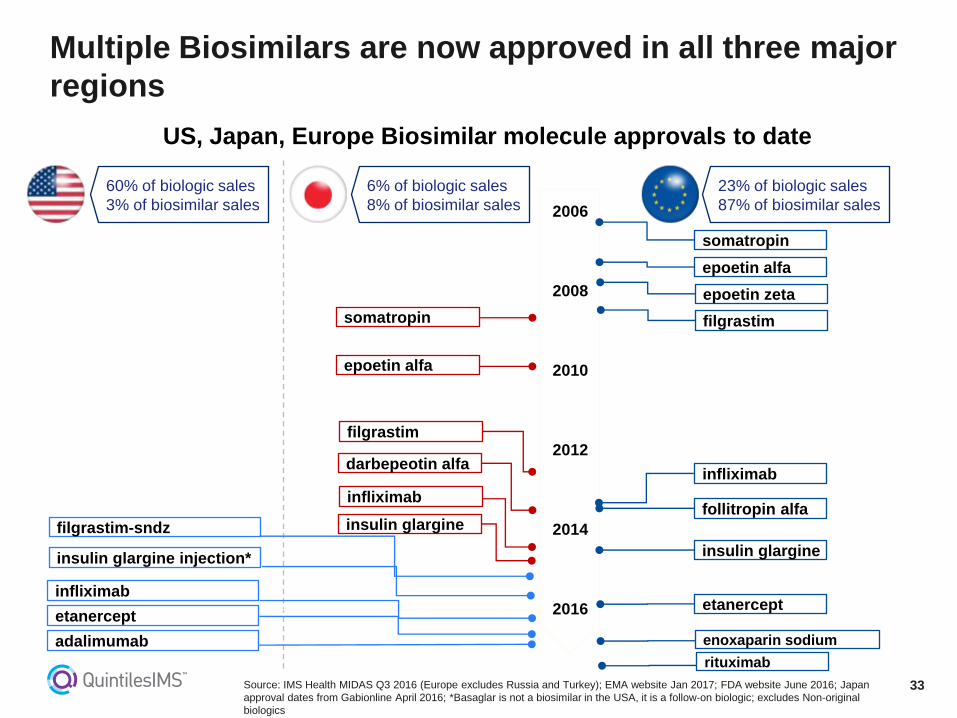

Multiple Biosimilars are now approved in all three major

regions

Source: IMS Health MIDAS Q3 2016 (Europe excludes Russia and Turkey); EMA website Jan 2017; FDA website June 2016; Japan

approval dates from Gabionline April 2016; *Basaglar is not a biosimilar in the USA, it is a follow-on biologic; excludes Non-original

biologics

2006

2008

2010

2012

2014

2016

insulin glargine

somatropin

epoetin alfa

epoetin zeta

filgrastim

infliximab

follitropin alfa

etanercept

filgrastim-sndz insulin glargine

infliximab

insulin glargine injection*

epoetin alfa

filgrastim

infliximab

darbepeotin alfa

somatropin

23% of biologic sales

87% of biosimilar sales

6% of biologic sales

8% of biosimilar sales

60% of biologic sales

3% of biosimilar sales

US, Japan, Europe Biosimilar molecule approvals to date

etanercept

adalimumab enoxaparin sodium

rituximab

34

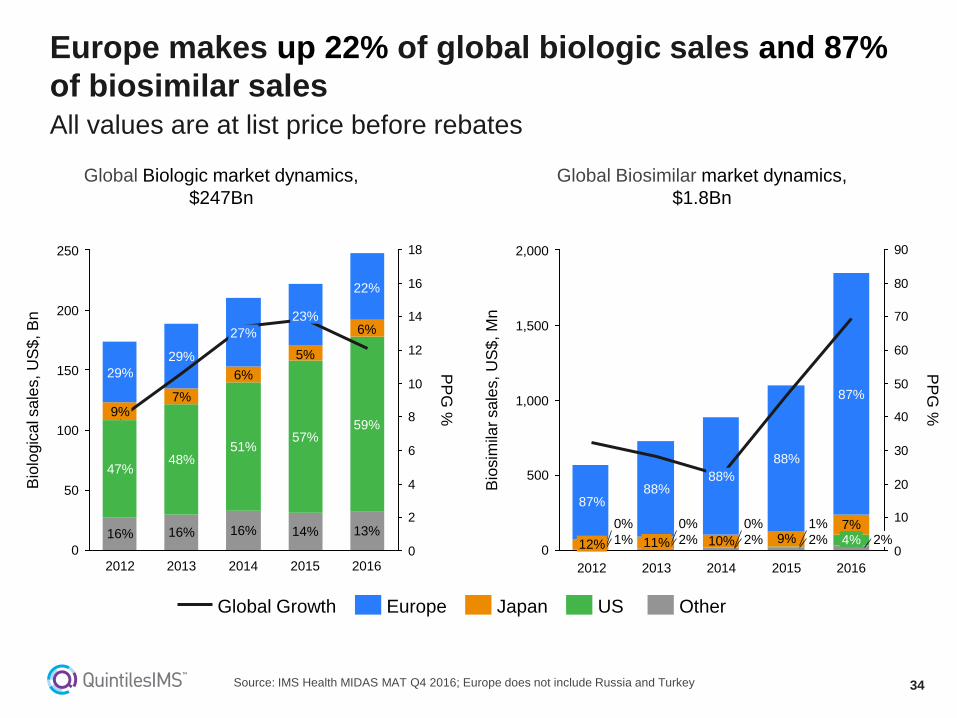

Europe makes up 22% of global biologic sales and 87%

of biosimilar sales All values are at list price before rebates

Source: IMS Health MIDAS MAT Q4 2016; Europe does not include Russia and Turkey

Global Biosimilar market dynamics,

$1.8Bn

Global Biologic market dynamics,

$247Bn

0

2

4

6

8

10

12

14

16

18

200

0

150

100

250

50

59%

6%

22%

2015

14%

57%

PP

G %

2016

13%

5%

23%

2014

16%

51%

6%

7%

29%

2012

16%

47%

9%

29%

27%

2013

16%

48%

Bio

logic

al s

ale

s, U

S$

, B

n

0

10

20

30

40

50

60

70

80

90

500

1,500

1,000

2,000

0

88%

2012

1%

0%

12%

87%

2013 2014

2%

0%

10%

88%

2%

0%

Bio

sim

ilar

sa

les, U

S$

, M

n

PP

G %

11% 9% 1%

2015

2%

88%

7% 4% 2%

2016

87%

Japan Europe US Global Growth Other

35

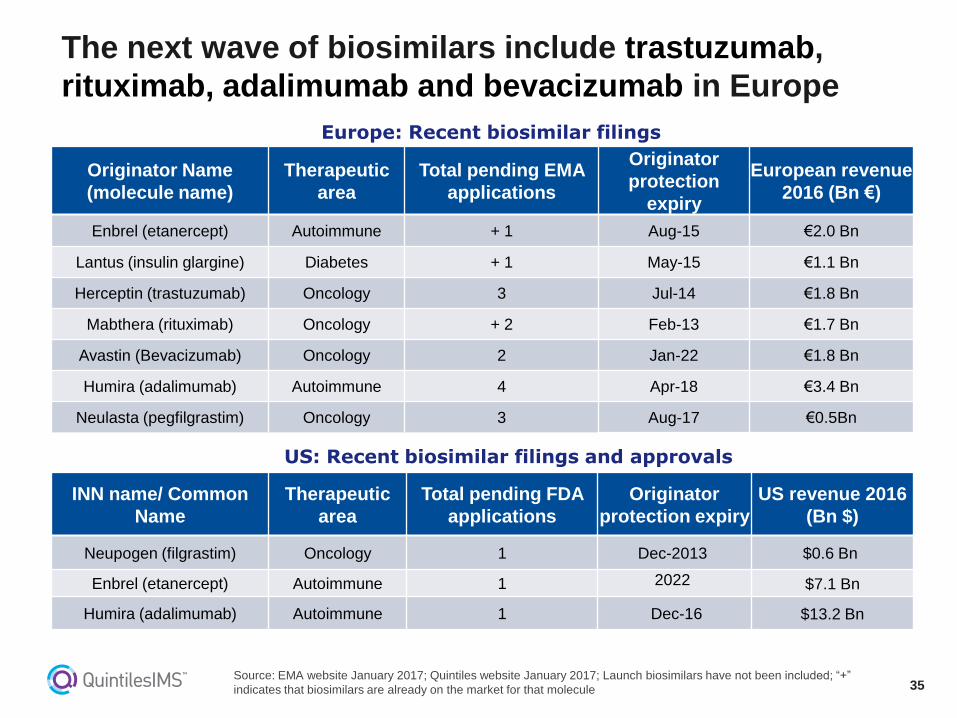

The next wave of biosimilars include trastuzumab,

rituximab, adalimumab and bevacizumab in Europe

Source: EMA website January 2017; Quintiles website January 2017; Launch biosimilars have not been included; “+”

indicates that biosimilars are already on the market for that molecule

Europe: Recent biosimilar filings

US: Recent biosimilar filings and approvals

Originator Name

(molecule name)

Therapeutic

area

Total pending EMA

applications

Originator

protection

expiry

European revenue

2016 (Bn €)

Enbrel (etanercept) Autoimmune + 1 Aug-15 €2.0 Bn

Lantus (insulin glargine) Diabetes + 1 May-15 €1.1 Bn

Herceptin (trastuzumab) Oncology 3 Jul-14 €1.8 Bn

Mabthera (rituximab) Oncology + 2 Feb-13 €1.7 Bn

Avastin (Bevacizumab) Oncology 2 Jan-22 €1.8 Bn

Humira (adalimumab) Autoimmune 4 Apr-18 €3.4 Bn

Neulasta (pegfilgrastim) Oncology 3 Aug-17 €0.5Bn

INN name/ Common

Name

Therapeutic

area

Total pending FDA

applications

Originator

protection expiry

US revenue 2016

(Bn $)

Neupogen (filgrastim) Oncology 1 Dec-2013 $0.6 Bn

Enbrel (etanercept) Autoimmune 1 2022 $7.1 Bn

Humira (adalimumab) Autoimmune 1 Dec-16 $13.2 Bn

36

• Ageing populations and social costs outpacing health care provision and in the

absence of curative therapies will diminish share of budgets for medicines

• Specialty care innovation continues to grow but true innovation is happening in

several therapeutic areas, not just specialty

• Payers will seek more intensive cost containment measures to drive down

prices

• The need for affordable quality medicines remains key for sustainability of

healthcare systems

Cutting medicine prices is not the solution to reduce costs; improving

outcomes should be the objective

Efficient healthcare is the mantra

Summary