global healthcare m&a bigger is better… · after two strong years (2014/15), global...

TRANSCRIPT

Weekly Barometer 25 janvier 2012

Global Healthcare M&A – Bigger Is Better

January 2018

ATONRÂ PARTNERS SA 12, Rue Pierre Fatio – 1204 GENEVA – SWITZERLAND - Tel: + 41 22 310 15 01 http://www.atonra.ch

Global Healthcare M&A – Bigger is Better

➢ The Healthcare M&A Index is a long-only, USD-based, actively managed total return Index

➢ The Index invests in companies which are to benefit from M&A potential (takeover targets

and acquirers) as well as from long-term industry drivers and specific company catalysts

in the healthcare sector

➢ After two strong years (2014/15), Global Healthcare M&A decelerated sharply in 2016 due to

a couple of powerful headwinds (regulations targeting US tax inversion, Trump’s election)

➢ M&A activity in the industry is now back in force and will possibly beat the 2015 record this

year as:

✓ the political environment has become more supportive (less noise from the Trump

administration, clearer view from the FDA, and positive implications from the US tax reform)

✓ financing is abundant and cheap (secondary offerings made by Biotech companies over

the last few months were filled in a few minutes…)

➢ The US tax reform notably should give a boost to mega deals as smaller ones are driven by

fundamentals and are more immune to the political and tax landscape

➢ With increased focus on personalized medicine and continued innovations from the Tech

world (wearables, next-generation sequencing, etc.), MedTech is to top the M&A list

2

Investment Case

Global Healthcare M&A – Bigger is Better

➢ Certificate details

✓ Issuing bank: Natixis SA

✓ Index calculation agent: Natixis SA

✓ ISIN: XS1365787826

✓ Currency: USD

✓ Fees: 1.65% + 15% performance fee, high water mark

✓ Bloomberg ticker: NXSRHEMA

✓ Benchmark: MSCI World Health Care Index (MXWO0HC)

3

The AtonRâ Global Healthcare M&A Index

Global Healthcare M&A – Bigger is Better 4

MedTech

Generics/

Biosimilars

Biotech

Personalized

medicine

Healthcare

Services

Rare

Diseases

Global

Pharma

CDMOs/

CROs

Global Healthcare M&A – Bigger is Better 5

Market Dynamics Are Rapidly Changing: Long-Term Drivers Remain Intact…

Ageing world population

560M people are >65 year old

Prevalence of chronic diseases

Cancer, cardio, neurodegenerative and respiratory notably are to make up more than 50% of

global healthcare expenditures by 2020

Precision medicine and innovative technologies

Artificial Intelligence, VR, wearable biosensors and trackers, 3D printing, Next Generation

Sequencing among others are giving life to new or alternative treatments

Global Healthcare M&A – Bigger is Better

M&A is the natural response to these changing market dynamics as it allows to reignite

growth and deliver operating leverage

6

Slowing organic growth

Blockbuster drugs going

off-patent

Consolidation of customers (drug

wholesalers and pharma retailers

notably)

Rising complexity & costs of

regulatory compliance and

R&D costs

Pricing pressures

Intense competition

Margin compression

… But Challenges Have Never Been Higher

Global Healthcare M&A – Bigger is Better

First Signs Of M&A Recovery In 2017…

7

Source: Thomson One

Announced M&A by Top Ten Target Sectors

Target Sector

Full Year 2017 Full Year 2016

% Volume

ChangeVolume $bn Deals Volume $bn Deals

Real Estate 529.7 4040 359.1 3499 48%

Energy and Power 469.7 3305 608 3320 -23%

High Technology 454.8 7396 486.6 6739 -7%

Industrials 428.4 6783 366.6 6402 17%

Financials 330 5282 351.9 5005 -6%

Healthcare 299.2 3543 274.9 3369 9%

Media and Entertainment 221.7 3414 285.9 3314 -22%

Materials 195.8 4308 393.5 3710 -50%

Consumer Products and

Services176.4 5571 117.3 4984 50%

Consumer Staples 160.9 3097 186.9 2994 -14%

Global Healthcare M&A – Bigger is Better

… As Visibility Is Finally Improving

8

US tax reform✓

Improving FDA process

approvals ✓

Favorable financing

conditions ✓

Easing political pressures✓

➢ Less noise from the Trump administration

on drug pricing

➢ The Obamacare repeal effort is stalling

➢ The reshaping of current regulations

seeks to speed up approvals of new

drugs and to promote competition /

reduce prices

➢ Low interest rates

➢ Strong investor appetite for equity

offerings: recent capital increases in

Biotech have been oversubscribed

➢ One-off tax of 15.5% on offshore cash

(instead of 35%) will incentivize Pharma

& Biotech companies to repatriate cash

Global Healthcare M&A – Bigger is Better

➢ M&A allows to reignite growth and/or deliver operating leverage

➢ Low net debt / EBITDA levels (below a max. level of 3-4x) point to a huge M&A firepower

9

1.71.5

1.41.3

1.1

0.80.7

0.60.5

0.4

-0.4

-1.0

Earnings

accretion

& value

creation

Multiples

rerating

High ROCE in the pharma and

medtech segments, low WACC

The acquirer enriches its product pipeline

through the acquisition of a Biotech

Large Healthcare Players Have All Reasons To Look At M&A

Global Healthcare M&A – Bigger is Better 10

APPLE

• Diabetes management

• Smart contact lenses

• Bioelectric medicines

• Surgical robots

• Genomics

• Cancer diagnostics

MUSK (Tesla)

• Brain implants

• Mind-reading devices

AMAZON • Pharmacies

Tech Giants Are Also Potential Predators

Global Healthcare M&A – Bigger is Better 11

Healthcare M&A Usually Comes with Huge Premiums

Acquirer Target Share price

premium

Deal value ($m) Deal announced

Allergan Tobira 498% 1,695 Sept 2016

Roche Anadys 256% 230 Oct 2011

Merck & Co Idenix 239% 3,850 Jun 2014

Bristol-Myers Squibb Inhibitex 163% 2,500 Jan 2012

Valeant Sanitas 160% 440 May 2011

Alexion Synageva 140% 8,394 May 2015

Cubist Adolor 121% 415 Oct 2011

Bristol-Myers Squibb Amylin 101% 7,000 Jun 2012

GlaxoSmithKlineHuman Genome

Sciences99% 3,600 Apr 2012

Mylan Meda 92% 7,200 Feb 2016

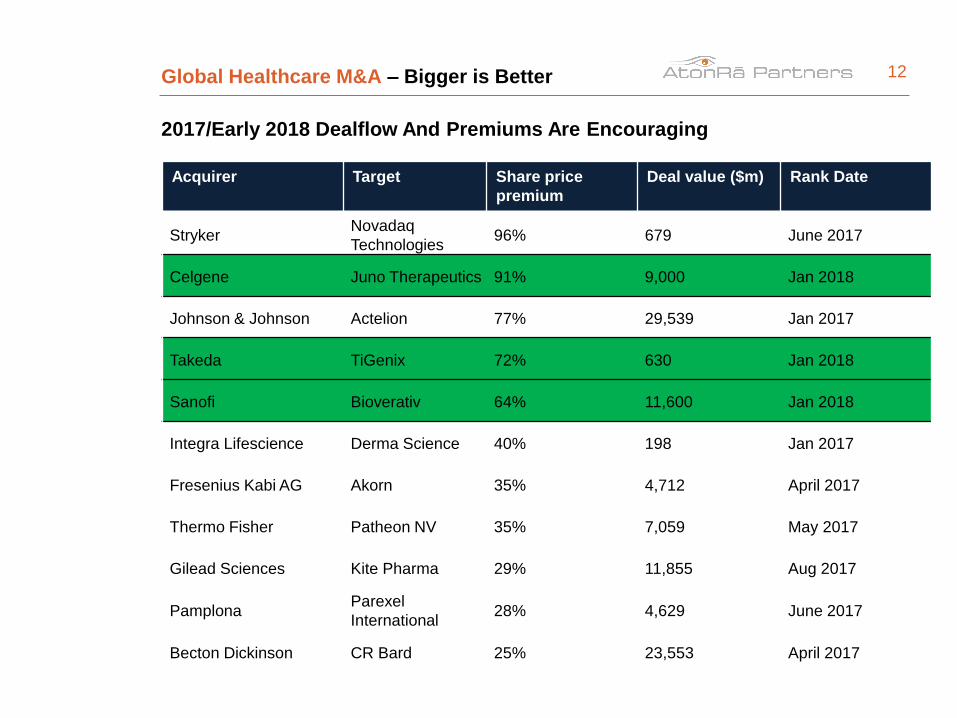

Global Healthcare M&A – Bigger is Better 12

2017/Early 2018 Dealflow And Premiums Are Encouraging

Acquirer Target Share price

premium

Deal value ($m) Rank Date

Stryker Novadaq

Technologies96% 679 June 2017

Celgene Juno Therapeutics 91% 9,000 Jan 2018

Johnson & Johnson Actelion 77% 29,539 Jan 2017

Takeda TiGenix 72% 630 Jan 2018

Sanofi Bioverativ 64% 11,600 Jan 2018

Integra Lifescience Derma Science 40% 198 Jan 2017

Fresenius Kabi AG Akorn 35% 4,712 April 2017

Thermo Fisher Patheon NV 35% 7,059 May 2017

Gilead Sciences Kite Pharma 29% 11,855 Aug 2017

PamplonaParexel

International28% 4,629 June 2017

Becton Dickinson CR Bard 25% 23,553 April 2017

Global Healthcare M&A – Bigger is Better

➢ M&A focus by the large Pharma players is near the post-approval phase but, as shown by

the Gilead-Kite deal (announced before an FDA approval), earlier-stage assets purchases

(notably through contingency deals) are likely to accelerate in the next few quarters

Contingency deals are an important part of the ongoing R&D externalization process

together with outsourcing to private contract research organizations (CROs)

13

Source: IFPMA

Duration: 6-7yrs

Share of budget: up to 65%

Chance of success:

✓ 65% in phase I

✓ 40% in phase II

✓ 50% in phase III

Duration: 0.5-2yrs

Share of budget: up to 3.5%

Duration: 3-6yrs

Share of budget: 21.5%

Chance of success: <0.01%

Drug

Discovery

Screening

of 5,000

to 10,000

compounds

Pre-

clinical

250

compounds

IND

Clinical Trials

Phase I

20-100

volunteers

Phase II

100-500

volunteers

Phase IIII

1’000-5’000

volunteers

NDARegulatory

Review and

Market

Authorization

Scale-Up to

Manufacturing

Post-Marketing

Surveillance

Phase IV trials

Duration: ongoing

Share to budget: up to 10%

Chances for

return on investment (ROI):

1:3

RESEARCH DEVELOPMENT APPROVAL

Expect More Contingency And Pre-Approval Deals

Global Healthcare M&A – Bigger is Better

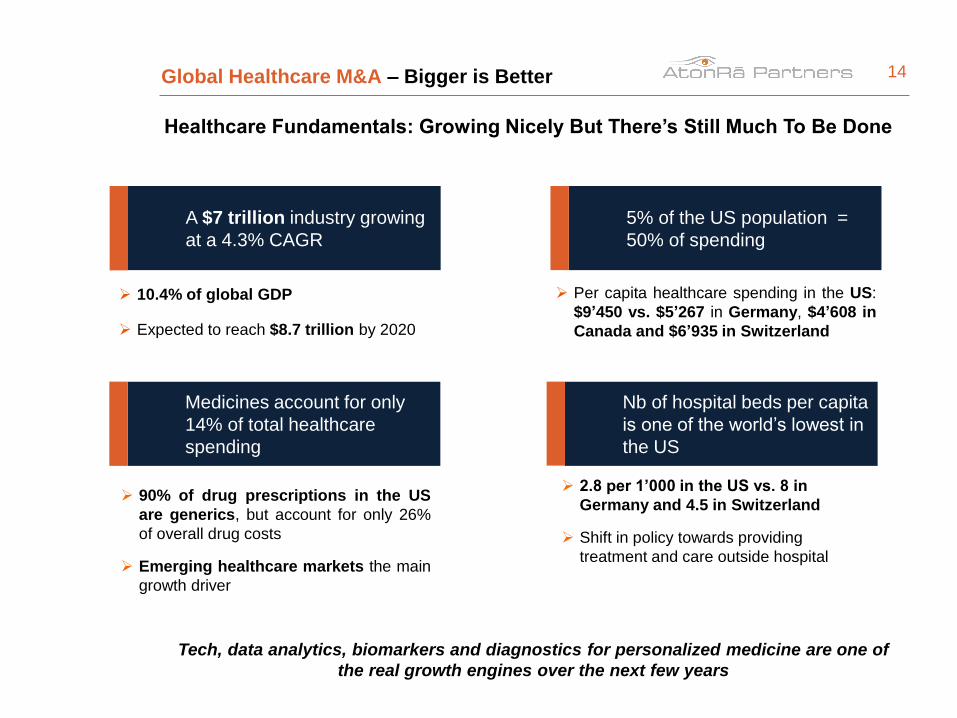

Healthcare Fundamentals: Growing Nicely But There’s Still Much To Be Done

Tech, data analytics, biomarkers and diagnostics for personalized medicine are one of

the real growth engines over the next few years

14

Nb of hospital beds per capita

is one of the world’s lowest in

the US

5% of the US population =

50% of spending

Medicines account for only

14% of total healthcare

spending

A $7 trillion industry growing

at a 4.3% CAGR

➢ 10.4% of global GDP

➢ Expected to reach $8.7 trillion by 2020

➢ Per capita healthcare spending in the US:

$9’450 vs. $5’267 in Germany, $4’608 in

Canada and $6’935 in Switzerland

➢ 90% of drug prescriptions in the US

are generics, but account for only 26%

of overall drug costs

➢ Emerging healthcare markets the main

growth driver

➢ 2.8 per 1’000 in the US vs. 8 in

Germany and 4.5 in Switzerland

➢ Shift in policy towards providing

treatment and care outside hospital

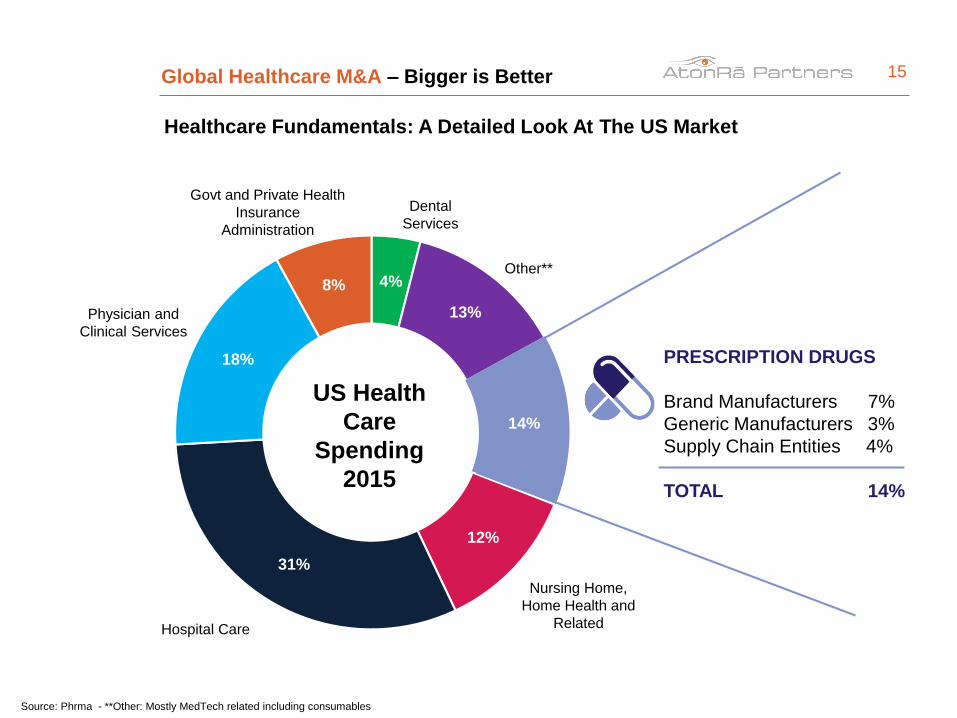

Global Healthcare M&A – Bigger is Better 15

Source: Phrma - **Other: Mostly MedTech related including consumables

4%

13%

14%

12%

31%

18%

8%

US Health

Care

Spending

2015

Govt and Private Health

Insurance

Administration

Physician and

Clinical Services

Hospital Care

Nursing Home,

Home Health and

Related

Other**

Dental

Services

Healthcare Fundamentals: A Detailed Look At The US Market

PRESCRIPTION DRUGS

Brand Manufacturers 7%

Generic Manufacturers 3%

Supply Chain Entities 4%

TOTAL 14%

Global Healthcare M&A – Bigger is Better

➢ Biologics and OTC (over-the-counter) growing the fastest

➢ Oncology the largest therapeutic area → 16% of total pharmaceutical sales by 2021 from

10.7% in 2015

➢ Orphan drugs growing twice (11%) the prescription drug market and to account for more

than 15% of worldwide prescriptions (including generics) by 2021

➢ Increased complexity, larger size

of trials and greater focus on chronic

and degenerative diseases

✓ are the main reasons behind

cost inflation

➢ 70% of drug sales today derive from

drugs initially developed

✓ by smaller companies vs. 30%

during the 1990’s

M&A an important

driver for pipeline enhancement

16

Source: QuntilesIMS - ² Evaluate Pharma 2016

Healthcare Fundamentals: Orphan Drugs, Biologics & Oncology To Stand Out

0

200

400

600

800

1000

1200

1400

1600

2015 2021

Ph

arm

a m

ark

et

siz

e $

bn Biosimilars

Biologics

OTC

Generics

Patented/ Originatorsmall molecule

Global Healthcare M&A – Bigger is Better

➢ Over 14K medicines worldwide are currently in active development…

✓ anticancer therapies leading the pack followed by Neurological and Anti-infective

➢ But “only” 56 (45 FDA approvals of which 47% for rare diseases) were launched in 2015

on a worldwide basis

✓ a strong number as typically out of 10K compounds, only five advance to the human testing

phase and only one is successfully commercialized

17

Source: Pharmaprojects®, January 2017

10,000compounds

250

compounds

5compounds

Stage 3

Drug Discovery

Pre-Clinical

Development

Clinical

Development

Stage 2

Stage 1

Regulatory

Approval

compound

Phases

0- Effect on body

I- Safety in humans

II- Effectiveness at

treating diseases

III- Larger scale safety

and effectiveness

IV- Long term safety

7493

20642357

1025

220 116

1395

79

0

1000

2000

3000

4000

5000

6000

7000

8000

Drug Count

2016 2017

Pipeline by development phase

2017 vs 2016

Healthcare Fundamentals: Number Of Medicines Currently In Development

➢ Over 1/3 of ongoing developments are for rare diseases

➢ Oncology treatment sales (a somewhat crowded space) are expected to reach $190B by

2022¹

✓ 1/3 of total new drugs to be introduced focus on cancer therapies

Global Healthcare M&A – Bigger is Better 18

Source: Evaluate Pharma 2016¹

Cancers

1,919

Infectious Diseases

1,261

Diabetes

401

HIV/ AIDS

208

Cardiovascular Disease

563

Immunological Disorders

1,123

Mental Health Disorders

401

Neurological Disorders

1,308

Healthcare Fundamentals: Number Of Medicines By Key Diseases

Global Healthcare M&A – Bigger is Better

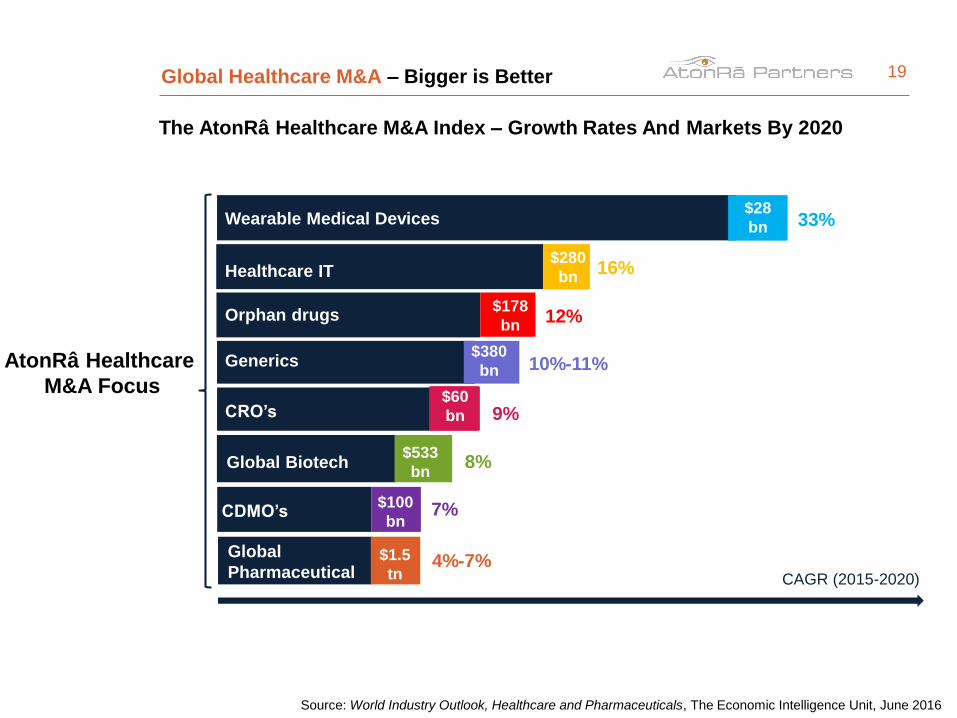

The AtonRâ Healthcare M&A Index – Growth Rates And Markets By 2020

19

Source: World Industry Outlook, Healthcare and Pharmaceuticals, The Economic Intelligence Unit, June 2016

CAGR (2015-2020)

Wearable Medical Devices$28

bn 33%

Global

Pharmaceutical$1.5

tn4%-7%

Global Biotech$533

bn8%

CRO’s $60

bn

CDMO’s$100

bn

9%

7%

Generics $380

bn 10%-11%

Orphan drugs$178

bn12%

Healthcare IT $280

bn16%

AtonRâ Healthcare

M&A Focus

Global Healthcare M&A – Bigger is Better 20

HOT

COLD

Orphan Drugs

MedTech

CDMOs & CROs

Generics

NGS (Next Generation Sequencing)

Healthcare services

Biosimilars

Healthcare IT

Our M&A Thermometer

Global Healthcare M&A – Bigger is Better

➢ Orphan definition by patient population → US = <6.37 out of 10K; Europe = <5

patients out of 10K; Japan = <4 out of 10K

➢ As the population becomes older, the number of rare diseases increases, notably

neurological ones, and 80% of them have genetic origins

✓ half of rare diseases hit children as most of genetic diseases occur at childhood, often

a single gene is responsible

➢ Insurers are set to continue covering such drugs (on average $140K vs. $27K for non-

orphan), as it is in most cases the single possibility for patients

➢ 2016 saw a record number of applications (582, a 23% Y/Y growth) made to the FDA

for orphan drug designations

➢ Larger players include Novartis (11.3% share), Roche (8.8%), Celgene (8%)

✓ others include Alexion Pharmaceuticals, Shire, Vertex and Kite (just bought out by

Gilead Sciences), Tesaro and Bluebird Bio

➢ We believe that gene therapies and advances in machine learning, computer vision,

robotic automation and high throughput sequencers are expected to boost the

discovery of new therapies for rare diseases

Fewer FDA restrictions and faster FDA approvals particularly in the Rare Diseases space

are likely to attract a lot of M&A attention

21

Orphan Drugs – Most Of The Biotech M&A Will Take Place Here

Global Healthcare M&A – Bigger is Better 22

Phase I

Phase II

Phase III

Application submitted

25

82

9151

12

10

10

148

7

31

38

11

13

49

Auto-immune Diseases

Blood Cancer

Blood Disorders

Cancer

Cardiovascular Disease

Digestive Disorders

Eye Disorders

Genetic Disorders

Growth Disorders

Infectious Diseases

Neurologic Disorders

Respiratory Diseases

Transplantation

Other

Source: PhRMA – research progress hope

Orphan Drugs - Medicines In Development In The US For Rare Diseases In 2016

Global Healthcare M&A – Bigger is Better

➢ Healthcare IT spans notably Medical Document Management Solutions, Clinical

Analytics and Mobile Health Applications

➢ It’s a $134B market growing at a 16% CAGR¹, one of the fastest growth rates within

Healthcare

➢ More importantly, Technology is positioned as a tool to deliver improved health outcome

rather than as a contributor to rising Healthcare costs

➢ Aside from Artificial Intelligence, Virtual Reality, Augmented Reality, 3D Printing etc., we

believe that the internet of medical things (IoMT) and blockchain could play a very

important role as:

✓ IoMT (including smart pills) supports the integration of wearables and remote monitoring

devices

✓ blockchain, on the other hand, could overcome the privacy and security issues, when it

comes to managing data from hospitals, doctors, and insurance companies

The most interesting targets are those providing a better consumer experience via

wearables and mobile technologies by exploiting people’s data

23

Source: ¹Markets & Markets

Healthcare Technology – Tech Is To Change Everything

Global Healthcare M&A – Bigger is Better

➢ A huge $370 bn industry growing nicely (5% CAGR)

but still highly fragmented

24

Source: Evaluate Pharma 2016 & Evaluate MedTech 2016

37%

25%

38%

Top 10Companies

11-30Companies

Rest of Market

$138bn

$93bn

A

fragmented

market

In vitro diagnostics (IVD)

Cardiology

Diagnostic Imaging

Orthopedic Ophthalmics

General & Plastic Surgery

Endoscopy

Drug Delivery

Dental

Wound Mangement

0.00%

2.00%

4.00%

6.00%

8.00%

10.00%

12.00%

14.00%

16.00%

3.00% 3.50% 4.00% 4.50% 5.00% 5.50% 6.00% 6.50% 7.00% 7.50%

WW

Ma

rke

t S

ha

re %

in

20

22

% Sales Growth: CAGR 2015-22

Note: Size of Bubble = WW Sales in 2022

Top10 Device Areas in 2022,

Market Share & Sales Growth

MedTech – Still A Highly Fragmented Market (I)

Global Healthcare M&A – Bigger is Better

➢ 2015 was a record year for MedTech M&A with a total of 240 deals and $128B in deal value

✓ Abbott was responsible for a large part with the $30.7B acquisition of St. Jude Medical and

the just-completed embattled $5.3B Alere acquisition

➢ Larger companies in the MedTech space are looking for increased market share and scale

in each of their specialty category

✓ as a way to better respond to endlessly larger clients (hospital systems notably) and secure

market share at the expense of lower margins

➢ This market is also disrupted by new startups and Tech giants developing smart medical

devices or turning their usual devices (smartphones, watches) in medical ones

➢ A few examples of the new MedTech and Tech partnerships:

✓ J&J teamed up with Verily Life Sciences (Alphabet) and both created Verb Surgical, which

focuses on better patient outcome and hospital efficiencies

✓ Glaxo also teamed up with Verily and formed Galvani Biosciences, which has a focus on

bioelectronics medicines (harness electric signals in the body to treat chronic diseases)

✓ Boehringer Ingelheim JV with Qualcomm, designed to create an internet-connected

inhaler for certain respiratory diseases

✓ Illumina founded Helix, which develops liquid biopsy to detect diseases by measuring

snippets of tumor DNA in the bloodstream

25

MedTech – Still A Highly Fragmented Market (II)

Global Healthcare M&A – Bigger is Better

➢ Europe, home to 25’000 MedTech companies (for the most part SMEs) with 31% of the

worldwide MedTech market, is ripe for consolidation

✓ ahead of the new European Medical Devices Regulation (MDR) which applies from May

2020

➢ In the US (6’500 companies and 39% worldwide market share), many companies will face

an increasingly intensive competitive environment

✓ vs. larger specialized players

✓ vs. a new breed competitors coming from the Tech world

➢ We believe that the small-to-mid players on both sides of the Atlantic have a great

opportunity just ahead to further consolidate the market

✓ and the chance to make accretive acquisitions

➢ Larger MedTech players on the other side are likely to keep active in their search for higher

market share and are expected to keep adjusting their portfolios (buying or divesting

assets) accordingly

The interest shown from Tech giants for medical devices could give rise to significant

M&A with huge premiums

26

MedTech – Still A Highly Fragmented Market (III)

Global Healthcare M&A – Bigger is Better

➢ The CRO (Contract Research Organizations) industry barely existed ten years ago →

Outsourcing is the logical consequence of a maturing industry

➢ The CRO market is now consolidated, as the top 10 players command 80% of the market

($60B market by 2020 with a CAGR of 9%), with the APAC region growing the fastest

➢ With greater complexity and competition, mounting pressure on drug cost containment and

the need to cut time for product marketing, an ever increasing number of Pharma, Biotech

and MedTech companies outsource many tasks they previously performed in-house,

notably:

✓ site selection and patient enrollment through final regulatory approval (FDA, EMA etc.)

✓ independent data generation, proving concrete evidence of clinical superiority and cost-

effectiveness of products, a key feature for the future of personalized medicine

➢ Sophisticated data analysis (including AI & machine learning) in clinical trials (and trial

designs) is critical to the drug development process and payer reimbursement strategies

➢ We believe that CROs are to shift their focus to the IT world as shown by the merger of

product and healthcare service provider Quintiles with IT provider IMS Health, creating one

of the largest pure-play service providers in the personalized medicine space

M&A in the Medical Software space is likely as large Tech companies are to play an ever

more important role over the next few years

27

CROs & CDMOs – Tech To Take The Lead in CROs

Global Healthcare M&A – Bigger is Better

➢ The same dynamics apply to CDMOs (Contract Development Manufacturing

Organizations)

➢ CDMOs, a highly fragmented market, has a 25% share of the outsourced manufacturing and

packaging functions (top 10 companies have a 30% combined market share)

➢ CROs bear 50% of the Pharma’s clinical trials → Consolidation in CROs took place fast as

larger CROs were preferred by the Pharma & Biotech industry

✓ with their end-to-end product offering (multiple geographies and multiple complex trials)

➢ We believe that CDMOs mergers are on every banker’s mind as the next logical step would

see CROs and CDMOs merging → The best example is the just completed $7.2B (30%

premium) acquisition of Patheon by Thermo-Fisher

✓ thanks to this merger, Thermo-Fisher has become (for now at least) the sole fully integrated

player servicing the Pharma & Biotech industry

✓ offering services spanning from solutions for drug development, delivery and manufacturing

➢ Companies such as Swiss-based Lonza and US-based Catalent are topping the list of

potential consolidators/M&A targets

The battle for targets is likely to intensify, notably in Europe (the leading CDMO market)

as private equity firms and corporations compete

28

CROs & CDMOs – Toward A Merger Of Both Businesses?

Global Healthcare M&A – Bigger is Better

➢ Due to complexities in the manufacturing process and to reluctance from physicians

prescribing these drugs (very small changes can affect safety/effectiveness), biosimilars are

in a completely different shape from generics as:

✓ discounts vs. branded drugs are lower (in the range of 30% in the US and 50% in Europe) vs.

generics (90% on average)

✓ development costs in the range of $100M/$200M vs. $1M to $2M for generics

✓ dominated by a few large players such as Sandoz (generic arm of Novartis), Pfizer

(Hospira), Amgen, German privately-held Boehringer Ingelheim and South Korean

Celltrion

29

Aspirin

21 atomsHuman Growth Hormone

~ 3000 atoms

Monoclonal antibody

~ 25,000 atoms

SMALL MOLECULE DRUG SMALL BIOLOGIC LARGE BIOLOGIC

INCREASING COMPLEXITY

Biosimilars – Closely Held By The Large Pharma Players But… (I)

Global Healthcare M&A – Bigger is Better

➢ Roughly 50% of biosimilars sales will go off-patent in the next four years

➢ The 3 best-selling biosimilars (out of seven approved by the FDA so far) - Humira,

Enbrel and Remicade - were FDA-approved but only Pfizer’s Inflectra (biosimilar of

Remicade) is currently commercialized

➢ as Humira and Enbrel are held-up in patent litigation and are not expected to be

commercialized before 2018

➢ In Europe the number currently stands at 32 and the main difference between the two

continents is regulations

➢ In the US there are two FDA approval pathways: “highly similar” or “interchangeable”

➢ interchangeable (allows for automatic substitution by pharmacists) means that the

biosimilar is expected to have the same results as the original biological drug

➢ No one of the approved biosimilars got the “interchangeable” status in the US so far and

a such it represents a “legislative” loophole which is to delay the entry of biologics in the

US market but clouds are clearing out under the helm of the new FDA Commissioner

M&A within the biologic manufacturing space is to gain speed as it’s one of the few

growing markets in the pharma space

30

Biosimilars – Closely Held By The Large Pharma Players But…(II)

Global Healthcare M&A – Bigger is Better

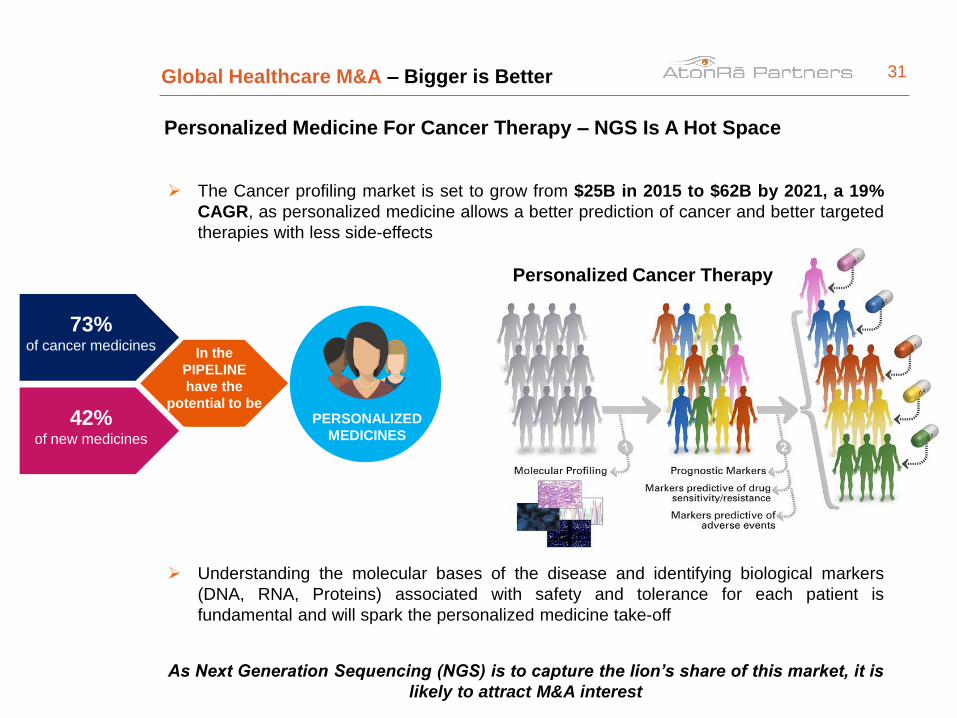

➢ The Cancer profiling market is set to grow from $25B in 2015 to $62B by 2021, a 19%

CAGR, as personalized medicine allows a better prediction of cancer and better targeted

therapies with less side-effects

➢ Understanding the molecular bases of the disease and identifying biological markers

(DNA, RNA, Proteins) associated with safety and tolerance for each patient is

fundamental and will spark the personalized medicine take-off

As Next Generation Sequencing (NGS) is to capture the lion’s share of this market, it is

likely to attract M&A interest

31

73% of cancer medicines

42% of new medicines

In the

PIPELINE

have the

potential to be PERSONALIZED

MEDICINES

Personalized Cancer Therapy

Personalized Medicine For Cancer Therapy – NGS Is A Hot Space

Global Healthcare M&A – Bigger is Better

➢ The Generics industry is seeing increased competition, most notably from Indian drug

makers (24% market share in the US), which pressures industry margins

✓ as volume growth is unable to offset declining prices (Mylan citing high-single digit price

erosion)

➢ The FDA, which approved a record of 800 generics in 2016, is speeding up the

approvals for generics (from four years to ten months), notably on those generic drugs

where fewer or no competition exists

✓ as a way to drive overall drug prices lower

➢ At the same time, manufacturing capacity of products becoming generic is divested from

Pharma, which is an additional catalyst for consolidation in the CDMO space

➢ Finally, from 2018 onwards, the number of drugs going off-patent is expected to

decline sharply, a negative catalyst for this industry

➢ For the generics industry there is no alternative but to search for even larger “economies

of scale” to survive the present environment

✓ entry into Biosimilars is a bet they have to do in the next few quarters or they will take the

risk of being left out from this market

While it might already be too late for small players, large scale M&A is likely to take

place in the next few quarters

32

Generics – Consolidation Among Large Players Is Now Needed

Global Healthcare M&A – Bigger is Better

➢ This is the largest pie of the Global Healthcare sector, representing 2/3 of the total

➢ The future in this space is driven by further consolidation across all segments including

hospitals, physicians organizations, surgery centers, imaging centers and many others as:

✓ downward pressure on margins is set to continue in the next few years

➢ The industry issues are compounded by baby boomers which are exiting the job market and

are adding to an already strained shortage of nurses and physicians

✓ salaries (and costs) are expected to grow more than the rate of inflation

➢ While IT is likely to alleviate some burdens of the labor shortage (telehealth, wearables,

apps etc.), the service providers standing to benefit and to gain market share are those

which are able to be the most efficient ones

The Healthcare services segment is not the key focus of our M&A portfolio but

opportunities can pop up from time to time

33

Healthcare Services – No Choice But To Consolidate In Order To Survive

DISCLAIMER

This report has been produced by the organizational unit responsible for investment research (Research unit) of

AtonRâ Partners and sent to you by the company sales representatives.

As an internationally active company, AtonRâ Partners SA may be subject to a number of provisions in drawing up

and distributing its investment research documents. These regulations include the Directives on the Independence

of Financial Research issued by the Swiss Bankers Association.

Although AtonRâ Partners SA believes that the information provided in this document is based on reliablesources, it cannot assume responsibility for the quality, correctness, timeliness or completeness of the informationcontained in this report.

The information contained in these publications is exclusively intended for a client base consisting of professionalsor qualified investors. It is sent to you by way of information and cannot be divulged to a third party without theprior consent of AtonRâ Partners.

While all reasonable effort has been made to ensure that the information contained is not untrue or misleading atthe time of publication, no representation is made as to its accuracy or completeness and it should not be reliedupon as such.

Past performance is not indicative or a guarantee of future results. Investment losses may occur, and investorscould lose some or all of their investment.

Any indices cited herein are provided only as examples of general market performance and no index is directlycomparable to the past or future performance of the Certificate.

It should not be assumed that the Certificate will invest in any specific securities that comprise any index, norshould it be understood to mean that there is a correlation between the Certificate’s returns and any index returns.

Any material provided to you is intended only for discussion purposes and is not intended as an offer orsolicitation with respect to the purchase or sale of any security and should not be relied upon by you in evaluatingthe merits of investing in any securities.

34