global generic trends and more - home page | association ... · global generic trends and more for...

TRANSCRIPT

Global Generic Trends and More

For IGPA 11/20/14

By Doug Long

VP Industry Relations

IMS Health

Agenda

• Major trends and Global Medicines Spend

• Specialty medicines

• Generic medicines and purchasing alliances

• Conclusions

Global spending growth will peak in 2014 at 7%, 4-7% CAGR through 2018

Report by the IMS Institute for Healthcare Informatics The Global Use of Medicines: Outlook through 2018 4

Global spending and growth, 2009-2018

0%

2%

4%

6%

8%

10%

12%

14%

0

200

400

600

800

1,000

1,200

1,400

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

GRO

WTH

CO

NST U

S$%

SPEN

DIN

G U

S$BN

Sales Growth

Source: IMS Health Market Prognosis, September 2014

2014-18 CAGR, 4-7%

Forecast

The global pharmaceutical market is expected to grow to nearly $1.3 trillion by 2018

Report by the IMS Institute for Healthcare Informatics

Global spending and growth, 2008-2018

2008 2009-2013 2013 2014-2018 2018

$795Bn

$194Bn

$989Bn

$290-320Bn

$1,280-1,310 Bn

Source: IMS Health Market Prognosis, September 2014

5 The Global Use of Medicines: Outlook through 2018

Developed markets recovery (pre rebates/discounts) lead by US, UK and Canada in the next five years

Developed Markets

CAGR 2014-2018

US 5-8%

Japan 1-4%

Germany 2-5%

France (-2)-1%

Italy 2-5%

Canada 3-6%

Spain (-1)–2%

UK* 4-7%

Developed 3-6%

Pharmerging Markets

CAGR 2014-18

Tier 1 (China) 9-12%

Tier 2 9-12%

Brazil 9-12%

Russia 7-10%

India 9-12%

Tier 3 6-9%

Pharmerging 8-11%

At par with region CAGR

Lower than region CAGR

Higher than region CAGR

0%

2%

4%

6%

8%

10%

12%

14%

0

200

400

600

800

1,000

1,200

1,400

2013 2014

(f)

2015

(f)

2016

(f)

2017

(f)

2018

(f)

% G

RO

WTH

(CO

NST U

S$)

SALES U

S$BN

Pharmerging US EU5 Global growth

Contains Audited + Unaudited data. All CAGR calculations are 5 years

Source: IMS Health Market Prognosis, Sep 2014, at ex-manufacturer price levels, not including rebates and discounts. *UK growth is pre-PPRS

Pharmerging sees deceleration across all major countries except Turkey

-5

0

5

10

15

20

0 5 10 15 20 25

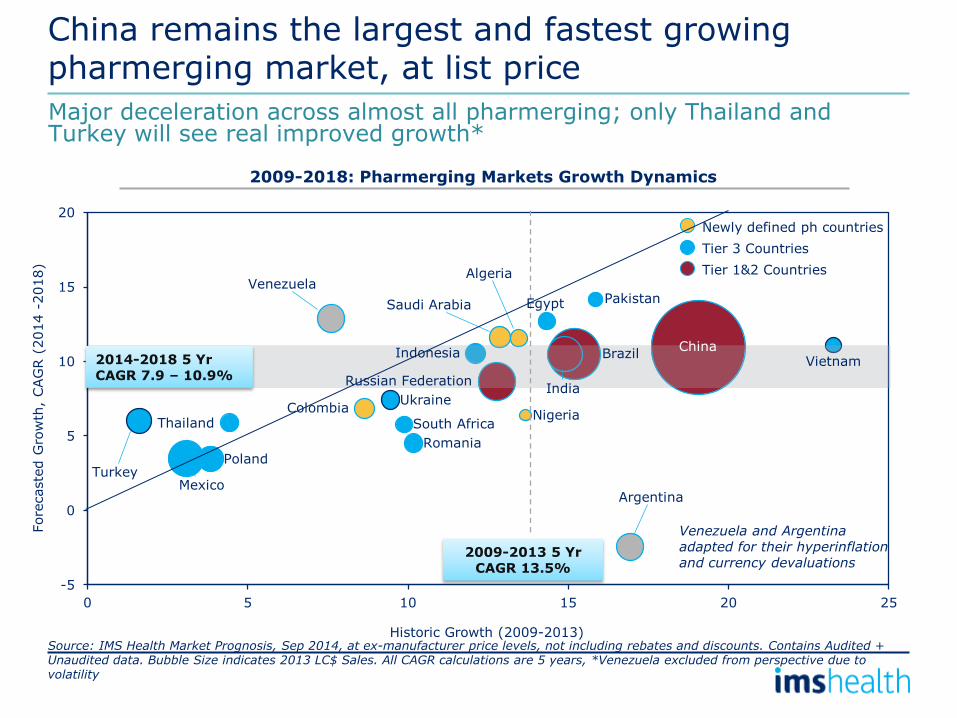

China remains the largest and fastest growing pharmerging market, at list price

Major deceleration across almost all pharmerging; only Thailand and Turkey will see real improved growth*

2009-2018: Pharmerging Markets Growth Dynamics

2014-2018 5 Yr CAGR 7.9 – 10.9%

2009-2013 5 Yr CAGR 13.5%

Source: IMS Health Market Prognosis, Sep 2014, at ex-manufacturer price levels, not including rebates and discounts. Contains Audited + Unaudited data. Bubble Size indicates 2013 LC$ Sales. All CAGR calculations are 5 years, *Venezuela excluded from perspective due to volatility

Fore

caste

d G

row

th,

CAG

R (

2014 -

2018)

Historic Growth (2009-2013)

South Africa

Saudi Arabia

Russian Federation

Romania Poland

Pakistan

Nigeria

Mexico

Indonesia

India

Egypt

Colombia

China Brazil

Argentina

Algeria

Vietnam

Venezuela

Ukraine

Turkey

Thailand

Tier 3 Countries

Newly defined ph countries

Tier 1&2 Countries

Venezuela and Argentina adapted for their hyperinflation and currency devaluations

Pharmerging will account for 55% of all the pharmaceutical market’s value growth to 2018

24% 24%

1% 2% 8% 6% 0% 2% 6% 5% 1% 1%

25% 27%

14% 16%

12% 12%

8% 7%

2009-2013 2014-2018

*Rest of Europe excludes Russia, Turkey, Poland, Romania, Ukraine, which are included in Pharmerging

Region Contribution to Global Growth 2018 Region Market Share

United States

32%

Canada

2%

EU5

14% Rest of Europe*

5%

Japan

8%

S. Korea

1%

Pharmerging Tier

1 (China) 14%

Pharmerging Tier

2 8%

Pharmerging Tier

3 9%

Rest of World

6%

United States

Canada

EU5

Rest of Europe*

Japan

S. Korea

Pharmerging Tier 1 (China)

Pharmerging Tier 2

Pharmerging Tier 3

Rest of World

Share

of Regio

nal Contr

ibution

to G

row

th (

%)

Source: IMS Market Prognosis, March 2014, at ex-manufacturer price levels, not including rebates and discounts. Contains Audited+Unaudited data. Growth and 2018 Market share based on LCUS$

55% of all value growth 31% of all

value

And the US still account for a quarter of growth

Growth is a mix of volume and pack price growth

Positive Growth No growth Negative Growth

Elements of Market Growth Total, Rx Pharmaceutical Market (MAT 06 2013- MAT 06 2014)

Priced at ex-mnf level before rebates and discounts

US DE ES FR IT UK JP KR BR MX CN

Value (lc$) 10.9 7.4 3.2 -0.1 4.1 7.7 2.6 4.3 14.7 1.9 13.1

Unit/Pack 1.4 0.6 2.0 -0.3 1.7 6.4 3.4 3.6 9.8 0.3 9.7

Avg. pack price

9.2 6.7 1.1 0.2 2.4 1.2 -0.8 0.7 4.5 1.6 3.1

SOURCE: IMS HEALTH MIDAS YEAR MAT 06 2014

Pharmaceutical market trending remains relatively unchanged

• Mature markets show low growth, continuing cost containment 1

• Pharmerging markets exhibiting higher growth but with key market variations due to GDP growth challenges

3

• Still an increasingly generic world 5

• Biologics growth continues apace with payers embracing biosimilars ideology

6

• Europe still under pressure with hospital debt and further austerity measures

2

• Consolidation within the industry continues but strategy and acquisition candidate profiles changing

4

Impact of the crisis: in half OECD-European countries, health spending was lower in 2012 than in 2009

Change in real total Health spending between 2009 and 2012(%)

-30.0%

-25.0%

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

Note: (1) current spending; (2) change between 2009 and 2011 Source: OECD Health data 2014

Increased health spending will be a major pressure on public budgets across all OECD countries

Source: OECD Economic Policy Paper n°06, 2013

0%

2%

4%

6%

8%

10%

12%

Average public spending 2006-2010 Increase of public spending 2010-2030

Increase of public spending 2030-2060 % GDP

Several drivers & constraints are forcing markets to re-examine current HC policies, leading to reforms

Key factors shaping healthcare and payer reforms

Uncertain picture

Reforms

Demographic/ Epidemiological

• Population

• Life-expectancy

• Disease burden

Socio-economic

• Literacy and awareness

• Affordability and willingness to pay

Funding

• Economic environment leading to financial constraints

Infrastructure

• Shortage of healthcare professionals

• Sub-optimal healthcare infrastructure

Demographic Development*

Ageing is associated with increasing health costs

System Impact: Severity, length and increased incidence

87mn

152mn +75%

65+ Years

16% 16% 15% 14% 14% 14%

67% 64% 62% 59% 57% 56%

20% 24% 27% 29% 30%

60

40

100

30

20

10

0

50

90

80

70

%

2060 2050 2040 2030 2020 2010

17%

0-14 Years 15-64 Years 65+ Years

Source: * European Commission (2012); † Hopkins University (2007); ∆ UK Dept. of Health (2010), European Commission; ♯ WHO (2013)

Increase in severity of Degenerative Diseases†

Extended impact of Chronic Diseases∆

Increased incidence

of Cancer♯

7.5

3.2

0

5

10

mn people +136%

2050 2006

19.116.4

0

10

20

years +16%

2030 2009

Life expectancy after T2 diabetes diagnosis

Late-stage Alzheimer’s Disease

3

2

1

0

mn cases +16%

2020

2.7

2010

2.3

New Cancer Incidences

Drivers of healthcare expenditure growth between 1995 and 2009 in OECD countries

But ageing is not the key driver of health spending growth

Healthcare expenditure growth (100%)

Demography (12%)

Age structure

Health by age

Income (42%)

Residual (46%)

Relative prices

Technology

Institutions and policies

Source: OECD Economic Policy Paper n°06, 2013

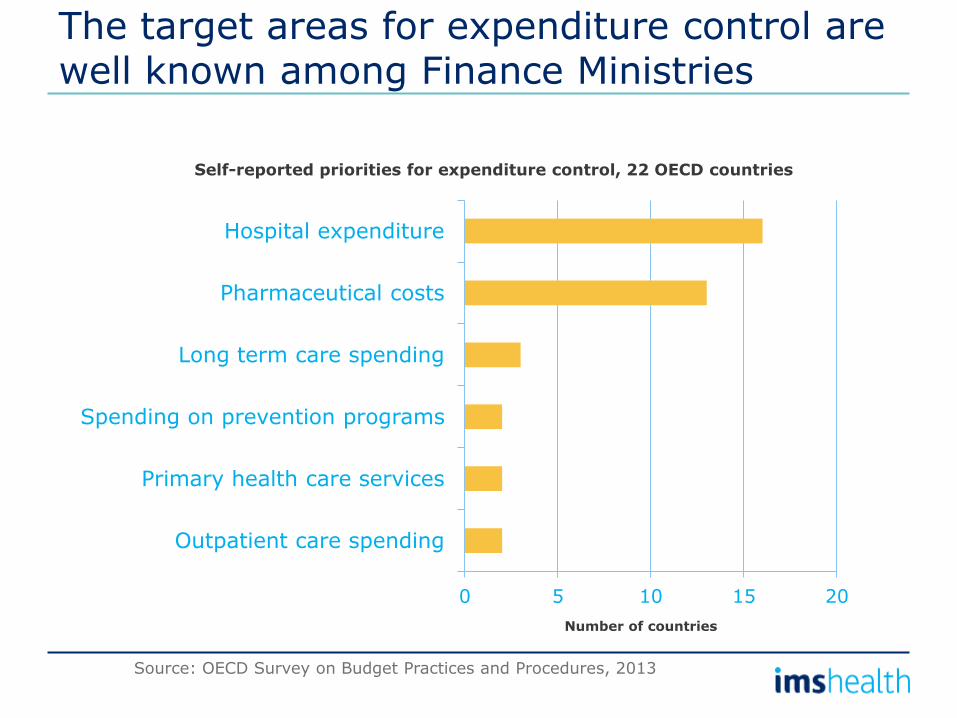

The target areas for expenditure control are well known among Finance Ministries

0 5 10 15 20

Outpatient care spending

Primary health care services

Spending on prevention programs

Long term care spending

Pharmaceutical costs

Hospital expenditure

Source: OECD Survey on Budget Practices and Procedures, 2013

Number of countries

Self-reported priorities for expenditure control, 22 OECD countries

The crisis has been used to slow growth in desirable areas, but has fallen short on prevention

4.8% 4.8%

5.9%

2.9%

6.9%

2.5%

3.2%

4.6%

6.2%

2.8%

6.4%

3.5%

0.7% 0.9%

5.3%

0.2%

-1.5%

-0.9%

1.0%

1.7% 1.6%

-1.7% -1.7%

1.7%

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

7%

8%

Inpatient care Outpatient care Long-term care Pharmaceuticals Prevention Administration

2007/08 2008/09 2009/10 2010/11

Source: OECD Health Statistics 2013

Average annual growth rates of spending for selected functions, OECD average, in real terms

Generics are a Solution!

• Generics saved the US $239 billion in 2013

• 14% increase over 2012

• $1.5 Trillion in savings from 2014-2013

IMS Harbingers of Change in Healthcare

• Consumer Technology Companies are rushing to healthcare to transform patient engagement

• Governments are Unshackling Data to aid research and spark medical innovation

• US Clinicians are being encouraged to consider costs in clinical treatment decisions

• China has loosened the price caps of 530 low cost essential drugs

• Medicine spending growth is returning to developed countries

• Trans-Atlantic supply chain

• A wave of innovation in Hepatitis C drug development

• New breakthrough vaccines foreshadows a new era of improved public health

• The growing use of biologics is bringing new treatment options

• US Payment and delivery system changes are shifting the focus to outcomes and performance

Agenda

• Major trends and Global Medicines Spend

• Specialty medicines

• Generic medicines and purchasing alliances

• Conclusions

0%

2%

4%

6%

8%

10%

12%

-

50

100

150

200

250

2008 2009 2010 2011 2012 2013 2014

Gro

wth

, LC

US

$

Sale

s,

US

$ b

illio

ns

Specialty sales Specialty Growth

Total Pharma growth

Growth of Specialty outpaces the total market

9.5%

18.8%

13.0% 17.5%

41.1%

Japan Pharmerging ROW EU5 US

2.3%

24.4%

4.2%

8.8%

60.3%

Specialty – Share of sales

Specialty– Share of growth

Global market trends Sales and Growth

SOURCE: IMS HEALTH MIDAS MAT 06 2014

Specialty products are outperforming traditional ones

0%

20%

40%

60%

80%

100%

US GER SPA FRA ITA UK JP KR BR (R) MX (R) CN

Valu

e m

arket

sh

are

Specialty versus traditional medicine market value dynamics (2013 value market share vs. 10 year value growth (2005- MAT 06 2014)

Retail Hospital

Specialty

Retail Hospital

Traditional

SOURCE: IMS HEALTH MIDAS YEAR 2013, Only retail data is available for NL, NL Growth rate = CAGR 2009 -MAT 06 2014, PT growth rate = CAGR 2010-

MAT 06 2014

10 yr value CAGR %

Traditional Specialty

4% 13%

1% 8%

-1% 6%

2% 9%

1% 14%

0% 10%

21% 21%

2% 6%

3% 7%

14% 15%

7% 13%

There is longer term shift to hospital

9%

5% 5% 9% 4% 11% 11% 2% 9% 36% 12% 21%

5% 5% 2% 2% -1% 0% 4% 14% 4% N/A

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

US GER SPA FRA ITA UK JP KR BR MX CN

Valu

e m

arket

sh

are

Evolution of hospital share of Rx Pharmaceutical Value Sales (2014 value market share vs. 10 year value growth (2004-2014)

Many European countries distribute products through the hospital channel due to:

Medical need, controlling prescribing, avoiding wholesaler & pharmacy margins and the ability to negotiate discounts

Hospital Retail % represents 10 year growth rate (2004-14)

Source: IMS Health, at ex-manufacturer price levels, not including discounts and rebates, MAT June 2014

Few prescribers/ centers

Low inventory important

Processing of pre-approval essential and competitive skill

Requires patient training to administer

Support to achieve adherence needed

Cold chain when needed

No need for supplying all pharmacies through all warehouses

IMS Health definition of Specialty Products

• Initiated only by a specialist

• High expense

• Requires reimbursement assistance

• Generally not oral

• Warrants intensive patient counseling

• Require special handling

• Unique distribution

Medicines that treat specific, complex chronic diseases with the min 4 of the 7 following attributes:

Top 10 Specialty Therapeutic Areas globally

0 10 20 30 40 50 60 70 80

OCULAR

ANTINEOVASCULARISATION

BLOOD COAGULATION

IMMUNOSUPPRENETS

ERYTHROPOIETINS

GROWTH FACTORS

VIRAL HEPATITIS

MULTIPLE SCLEROSIS

HIV ANTIVIRALS

AUTOIMMUNE DISEASES

ONCOLOGICS

US$ Billions

Top specialty TAs by value MAT 06 2014

CAGR 2005-14

11%

16%

11%

14%

15%

6%

-4%

6%

8%

29%

Oncology is largest area of spend by 2014 in developed markets and of growing importance in Pharmerging

0 20 40 60

Anti-Ulcerants

Antibacterials

Anticoagulants

HIV Antivirals

Lipid Regulators

Antihypertensives, Plain and

Combo

Autoimmune Disease

Respiratory Agents

Mental Health

Pain

Antibacterials

Oncologics

US$ Billions

Spending by Therapy area, 2014

Source: IMS Health Thought Leadership, MAT 06 2014

- 10 20

Mental Health

GI Products

Other CNS

Anti-Ulcerants

Hospital Solutions

Other Cardiovascular

Oncologics

Antidiabetics

Pain

Antyhypertensives, Plain

and Combo

Kampo + Chinese

Antibacterials

US$ Billions

Pharmerging Markets

Traditional

Specialty

Developed Markets

2020 for oncology forecast is $120 billion

14%

10%

28%

44%

3%

11%

25%

14%

10% 39%

ROW US

EU5 Pharmerging

Japan

Oncology Global Split

2003: $20bn

2013: $69bn

Source: IMS Health, MIDAS, MAT Dec 2013. Oncology (L1&L2&V3C&Revlimid&Xgeva&Proleukin&Pomalyst),Rx bound

34%

16%

12%

23%

15%

2020: $120-130bn

50% in USA and Japan

Europe and US illustrate growing importance of specialty therapies

For generics, LoEs have shifted the focus from small molecules to biologics

2010 2011 2012 2013 2014*

1 LIPITOR HUMIRA HUMIRA HUMIRA HUMIRA

2 SERETIDE SERETIDE SERETIDE ENBREL MABTHERA

3 HUMIRA LIPITOR ENBREL SERETIDE ENBREL

4 ENBREL ENBREL HERCEPTIN HERCEPTIN HERCEPTIN

5 HERCEPTIN HERCEPTIN LOVENOX REMICADE SERETIDE

6 AVASTIN LOVENOX MABTHERA AVASTIN REMICADE

7 LOVENOX REMICADE REMICADE MABTHERA AVASTIN

8 ZYPREXA MABTHERA AVASTIN LOVENOX LOVENOX

9 MABTHERA AVASTIN SPIRIVA LUCENTIS LYRICA

10 REMICADE SPIRIVA LYRICA LYRICA LUCENTIS

Europe Top 10 products 2010-14

Small molecule

Source: IMS Health, MIDAS, MAT Jun 2014. Europe doesn’t include Turkey and Russia; 2014= Q1 and Q2 2014

US Top 10 products 2010-14

2010 2011 2012 2013 2014*

1 LIPITOR LIPITOR NEXIUM ABILIFY SOVALDI

2 NEXIUM PLAVIX ABILIFY NEXIUM ABILIFY

3 PLAVIX NEXIUM SERETIDE LANTUS LANTUS

4 SEROQUEL SEROQUEL CRESTOR SERETIDE HUMIRA

5 SERETIDE ABILIFY CYMBALTA HUMIRA NEXIUM

6 ABILIFY SERETIDE HUMIRA CRESTOR CRESTOR

7 SINGULAIR SINGULAIR LANTUS CYMBALTA SERETIDE

8 CRESTOR CRESTOR ENBREL ENBREL ENBREL

9 ACTOS CYMBALTA REMICADE REMICADE REMICADE

10 ENBREL ENBREL COPAXONE COPAXONE NEULASTA

Specialty

Top products vary in Developed and Pharmerging markets

Small molecule

Source: IMS Health, MIDAS, MAT Jun 2014

Specialty

Top products 2014

KR JP BR MX CN

1 BARACLUDE PLAVIX HERCEPTIN HERCEPTIN XUE SHUAN

TONG

2 LIPITOR BLOPRESS HUMIRA CELEBREX SHEN JIE

3 HERCEPTIN CRESTOR SILDENAFILA HUMIRA SODIUM

CHLORIDE

4 CRESTOR AVASTIN TORSILAX CIALIS ADEGOLD

5 PREVNAR BENICAR LOVENOX AVASTIN PLAVIX

6 TWYNSTA REMICADE POLIO

VACINE LYRICA BEI TONG

7 EXFORGE SECTOR PNEUMOC

VACINE DOLO

NEUROBION

SOD CHLORIDE

KELU

8 PROGRAF JANUVIA LOSARTAN

HYPM NEXIUM

SHU XUE NING

9 GLIVEC DIOVAN CIALIS SERETIDE LIPITOR

10 CELEBREX ARICEPT LANTUS LANTUS DANSHEN

DUOFENSUAN

New Hepatitis C treatments breaking the bank

Sovaldi now the #1 drug in US

• Sovaldi from Gilead • Cures 90% of the patients • Launched in November in US

for $84,000/ full cycle • Price justified versus life

time cost for treatment • If full used, it would have

significant impact on drug spend

• The US congress held a hearing and condemned the pricing

The number of new molecular entities launched in 2013 is the highest in the last 10 years

New molecular entities launched in the U.S. 2004-2013

12 11 10 6 7 8 8

10 11 7

5 4

9

5 6

7 10

12 7

17

3 6

9

7 7

18 9

13

10

12

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

New mechanism Orphan Existing mechanism

Source: IMS Institute for Healthcare Informatics, Feb 2014

In a specialist world, more innovation is from smaller corporations

Big pharma continues to take the lead on commercialisation

FDA new drugs approval: development focus by origin of patent

Source: FDA Website. IMS Analysis based on best possible disclosed information. Large pharma defined as Top11-25 corps with revenues >$5bn; Medium corps $500mn+; Small corps less than $500mn; Others include university, hospitals and other companies.

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

2013

70%

30%

2003

71%

29%

Acquired Fully developed in house

Source of innovation by corporation type (patent originator)

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

2013

13%

17%

57%

3%

10%

2003

21%

14%

39%

14%

11%

Others

Medium corps

Small corps

Top 10

Large pharma

A number of big value biologics are set to lose patent protection in the next few years

All these products will lose patent protection by 2020, except Enbrel (US patent extended until 2028)

Not considered existing biosimilars such as Epoetin Alfa expired in EU, but still patent protected in the US

Source: IMS MIDAS, 06/2014, IMS Patent focus

EU expiry date US expiry date

2018 2016

2015 2028 (extended)

2013/15 2018

2014 2015

Expired 2018

2019 2019

Expired Expired

2015 2016

2014 2019

2017 2014

2015 2015

2016 2016

Global Sales (MAT 06/2014), US$ billion

Total ~ US$ 78

billion

- 5,000 10,000

INSULIN ASPART (Novomix, Novorapid)

RANIBIZUMAB (Lucentis)

PEGFILGRASTIM (Neulasta)

GLATIRAMER ACETATE (Copaxone)

TRASTUZUMAB (Herceptin)

INTERFERON BETA-1A (Avonex, Rebif)

BEVACIZUMAB (Avastin)

RITUXIMAB (Mabthera)

INFLIXIMAB (Remicade)

ETANERCEPT (Enbrel)

INSULIN GLARGINE (Lantus)

ADALIMUMAB (Humira)

US$ Millions

Japan Pharmerging ROW Top 5 Europe US

Despite biosimilars gradually emerging

2012

ROW

Europe

2013

Italy, largest Biosimilars

market in EU*

Mar Jun

Biosimilar G-CSF (Zarzio)

prescribed more than originator

N° of Biosimilar applications

(EMA) all-time high (8)

Lilly & BI submission for insulin glargine

biosimilar

Market trends

Regulatory

2nd GSF approved in Japan

Inflectra# (Infliximab Biosimilar)

approved EU

2014

Market trends

Regulatory

Source: Secondary research. List not exhaustive. (*) at ex-manufacturer price levels, not including rebates and discounts. (#) Recommended for RA (Rheumatoid arthritis), CD (Crohn’s disease), UC (Ulcerative colitis), AS (Ankylosing spondylitis), PA (Psoriasis), PsA (Psoriatic arthritis)

Follitropin alfa biosimilar approved

Jul

FDA approved Tbo-filgrastim but filed in the

U.S. as BLA

Remsima (Infliximab Biosimilar)

launched in Korea

Teva announce launch of

GRANIX in USA

Nov

Sandoz Omnitrope to be sole subsidised

somatropin from Jan 2015 in NZ

Herzuma (Trastuzumab bs)

approved in Korea

In Europe, biosimilar uptake exhibits different paces

A few countries have reached or approached the maturity stage

-10%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Mar-07 Dec-07 Jun-08 Dec-08 Jun-09 Dec-09 Jun-10 Dec-10 Jun-11 Dec-11 Jun-12 Dec-12 Jun-13 Dec-13

% U

pta

ke,

SU

Biosimilar uptake across Europe MAT 03/2007 – 12/2013 (Volumes, SU)

AUSTRIA BELGIUM FRANCE GERMANY HUNGARY

ITALY ROMANIA SPAIN SWEDEN UK

Total 10 countries 425M €

MAT 12/2013 Fast uptake at launch, now mature

Consistent uptake

Slow uptake, cultural resistance

Fast growing due to faster growing market trend

Payers incentivized Biosimilars

Source: IMS MIDAS, MAT Sep 2013

The global playing field continues to expand with players finding niches

Players differ not only in geographical spread but also a wider biologic portfolio

Emerging markets players

Domestic players

Serving domestic market only*

Serving 2+ countries

# Pharmerging markets only

Source: IMS Health, MIDAS, MAT Dec 2012. (*) restricted to MIDAS sales data and recombinant and synthesised prods only.

© 2013, IMS HEALTH

International Reach

Government backed players

Fastest growing corporations are focused on specialty

Top Globally Top Specialty Top Generics

Rank Corp US$bn 2014

CAGR 2005-14

1 ROCHE 29.0 10%

2 AMGEN 18.3 4%

3 NOVARTIS 18.0 13%

4 JOHNSON & JOHNSON

16.8 11%

5 GILEAD SCIENCES

15.7 29%

6 ABBVIE 13.3 16%

7 PFIZER 8.4 6%

8 BRISTOL-MYERS SQB.

7.2 10%

9 TEVA 6.6 16%

10 MERCK & CO 6.5 8%

Rank Corp US$bn 2014

CAGR 2005-14

1

NOVARTIS

48.0 6%

2

PFIZER

42.7 -4%

3

SANOFI 35.9 1%

4

MERCK & CO 35.3 1%

5 ROCHE 35.0 7%

6 ASTRAZENECA 31,4 3%

7 GSK 30.3 -1%

8 JOHNSON & JOHNSON

28.4 3%

9 TEVA 24.1 7%

10 LILLY 21.5 5%

Rank Corp US$bn 2014

CAGR 2005-14

1 TEVA 13.7 6%

2 NOVARTIS 11.2 -4%

3 MYLAN 9.9 1%

4 ACTAVIS 8.2 1%

5 SANOFI 5.0 7%

6 PFIZER 3.3 -1%

7 APOTEX 2.5 3%

8 PAR PHARM

2.2 7%

9 EMS 2.1 5%

10 STADA 2.1 8%

Recent large M&A activity is high though even by historic levels

Buyer Target Announced Close Type Value Stated Intent

Apr ‘14 - Takeover $116B Oncology pipeline, UK move could taxes

Apr ‘14 - Takeover $49B Become top 5 pharma by 2016

Feb ’14 Mid

2014 Acquisition $25B

Become fastest growing specialty pharma company

Apr ‘14 H1 2015 Swap $14.5B Novartis establish global Oncology leadership position

Apr ‘14 H1 2015 Swap $7.1B GSK Increase scale and quality in Flu Vaccines

Apr ‘14 H1 2015 JV $10.0B Add scale, reduce costs

Apr ‘14 Q1 2015 Swap $5.4B Lilly consolidating in Animal Health

Apr ‘14 - Acquisition $4.0B Complimentary platform in growth markets

Apr ‘14 - Divestiture $7.0B Looking to sell mature drugs portfolio

May ‘14 H2 2014 Acquisition $14.2B Consolidate Global Leadership in OTC

Rejected

Agenda

• Major trends and Global Medicines Spend

• Specialty medicines

• Generic medicines and purchasing alliances

• Conclusions

Global Generic Rx market, Value, US$ at ex-mnf price

before rebates and discounts

The US and Pharmerging markets generate most of generic value sales; volume growth is declining

SOURCE: IMS HEALTH MIDAS Q2 2014

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

-

20

40

60

80

100

120

140

160

180

200

US

$ B

illi

on

s

Japan Pharmerging

ROW Top 5 Europe

US Pharma Growth

Generics Growth

Global Generic Rx market, Volume, SU

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

20%

-

100

200

300

400

500

600

700

800

900

1,000

SU

Bil

lion

s

Japan Pharmerging

ROW Top 5 Europe

US Pharma Growth

Generics Growth

Generics are taking an increased share in all markets

REGIONAL GENERIC VOLUME MARKET SHARE (SU) 2004 VS. 2013, RX. RETAIL MARKET

LATAM : 46% 58%

USA: 52% 78%

Africa/Middle East: 46% 58%

Asia/Australasia : 34% 45%

Europe : 41% 56%

Canada: 56% 61%

Protected sales will decline in the Mature Eight to 2016

Source: IMS Health Market Prognosis, March 2014, Audited data only

350

300

250

200

150

100

50

0

Valu

e S

ale

s,

LC$bn

2018 2017 2016 2015 2014 2013 2012 2011 2010 2009 2008

2008 - 2018 Value Sales of Protected Brands, Mature eight

Forecasted numbers

2014-2018 Protected brands CAGR (-2)-1%

2009-2013 Protected brands

CAGR 0.6%

Mature Eight

Based on constant dollar forecasts, protected brands growth will slow and share decline

Generics to dominate growth

2009: 539 Bn 2013: 588 Bn

5 Yr CAGR

Region 2009 -2013 2014-2018

Top 8 Mature 3% 2 - 5%

Protected (Non-Generic) 1% (-2) – 1%

Generics 11% 9 – 12%

Unprotected (Non-Generic) 5% 4 – 7%

2018: 676 – 696 Bn

12% 12%

15%

60% 55%

17% 12%

16%

12%

18%

46%

24%

Source: IMS Health Market Prognosis, March 2014 (*) at ex-manufacturer price levels, not including rebates and discounts. Audited data only. Market size represented in constant US$. All CAGR calculations are 5 years

Protected (Non-generic) Generics Other Unprotected (Non-generic)

Top 8 Mature

61%

57%

31%

72%

27%

27%

58%

16%

12%

16%

11%

12%

World

Rest of the

world

Pharmerging

Developed

Brand Generic Other

Generics will represent a larger share of the market in volume and value terms

Global spending, 2012 and 2017

2012

52%

52%

26%

67%

36%

31%

63%

21%

12%

17%

11%

12%

2017

$622Bn $650-680Bn

$224Bn $370-400Bn

$120Bn $125-155Bn

$965Bn $1,170-1,200Bn

Source: IMS Health Thought Leadership, September 2013

17.1%

24.6%

15.4%

30.6%

5.9%

13.3%

16.9%

17.9%

24.1%

22-24%

26-28%

19-21%

30-32%

7-9%

16-18%

18-20%

24-26%

23-25%

2012 Generic Share

2017 Share Increase

2017 Generic Share

Developed Markets Generic Share

Canada

France

Germany

Italy

Japan

S Korea

Spain

UK

US

Generics will represent 20% of spending in most developed markets, volume shares considerably higher

Source: IMS Market Prognosis, Sep 2013

Price decreases in traditional areas are off-set by volume increases

Evolution of therapy volume, price of treatment and overall treatment cost in 7 therapy areas, Rx retail market from Q1 2004-Q4 2013,

Normalized to population growth

0.0

0.5

1.0

1.5

2.0

2.5

Q3 2

003

Q4 2

003

Q1 2

004

Q2 2

004

Q3 2

004

Q4 2

004

Q1 2

005

Q2 2

005

Q3 2

005

Q4 2

005

Q1 2

006

Q2 2

006

Q3 2

006

Q4 2

006

Q1 2

007

Q2 2

007

Q3 2

007

Q4 2

007

Q1 2

008

Q2 2

008

Q3 2

008

Q4 2

008

Q1 2

009

Q2 2

009

Q3 2

009

Q4 2

009

Q1 2

010

Q2 2

010

Q3 2

010

Q4 2

010

Q1 2

011

Q2 2

011

Q3 2

011

Q4 2

011

Q1 2

012

Q2 2

012

Q3 2

012

Q4 2

012

Q1 2

013

Q2 2

013

Q3 2

013

IN

DE

X

VOLUME WEIGHTED PRICE/TD NUMBER OF TREATMENT DAYS/CAPITA COST OF TREATMENT INDEX

SOURCE: IMS HEALTH MIDAS YEAR MAT 09 2013. SELECTED THERAPY AREAS ANGIOTENSIN II ANTAGNOISTS, ANTI-EPILEPTICS, ANTI-

PSYCHOTICS, ANTI-ULCERANTS, CHOLESTEROL REGULATORS AND ORAL ANTI-DIABETICS. POPULATION STATISTICS: OECD

Low income countries seeing large increases in access to medicine

Country Price

(€/TD) Volume

(TD/cap) Treatment

cost

Denmark -75% 117% -47%

UK -67% 122% -27%

France -45% 33% -26%

US -39% 35% -17%

Italy -59% 105% -15%

Spain -48% 95% 1%

Ireland -48% 107% 7%

Greece -30% 57% 10%

Germany -57% 158% 11%

Austria -43% 102% 15%

Mexico -6% 84% 73%

Brazil -3% 485% 467%

Impact of generic entry on price, volume and total treatment cost in 7 therapy areas, Rx retail market from

Q1 2004-Q4 2013

SOURCE: IMS HEALTH MIDAS YEAR MAT 09 2013. SELECTED THERAPY AREAS ANGIOTENSIN II ANTAGNOISTS, ANTI-EPILEPTICS, ANTI-

PSYCHOTICS, ANTI-ULCERANTS, CHOLESTEROL REGULATORS AND ORAL ANTI-DIABETICS. POPULATION STATISTICS: OECD

Impact of price decline >

volume increase Decline in overall treatment

cost

Impact of price decline equivalent to

volume increase Stabilisation of overall

treatment cost

Increased access in under-served markets

Price per treatment day is highly variable

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

Pric

e/

TD

, €

SOURCE: IMS HEALTH MIDAS YEAR MAT 09 2013. SELECTED THERAPY AREAS ANGIOTENSIN II ANTAGNOISTS, ANTI-EPILEPTICS, ANTI-

PSYCHOTICS, ANTI-ULCERANTS, CHOLESTEROL REGULATORS AND ORAL ANTI-DIABETICS. POPULATION STATISTICS: OECD

Price per treatment day, based on DDD, Q4 13, European weighted

The level of generic penetration does not indicate that a market is generating cost savings

NORWAY SWEDEN

FINLAND UK

BELGIUM

AUSTRIA GERMANY

PORTUGAL

ITALY SWITZERLAND FRANCE

SPAIN

IRELAND

GREECE

USA

CANADA

-90%

-80%

-70%

-60%

-50%

-40%

-30%

30% 40% 50% 60% 70% 80% 90%

20

13

OFF

-PA

TEN

T EF

FIC

IEN

CY

FO

R S

MA

LL

MO

LEC

ULE

UN

DER

-GO

ING

LO

E B

ETW

EEN

2

00

4-2

01

3

GENERIC PENETRATION IN THE UN-PROTECTED RX RETAIL MARKET (2013)

SOURCE: IMS HEALTH MIDAS YEAR 2013

Finland and UK save about the same – but Finland has 20% lower generic penetration

UK and Canada have about the same generic penetration– but UK saves ~30% more

Major markets moving but remaining inefficiencies provide opportunities!

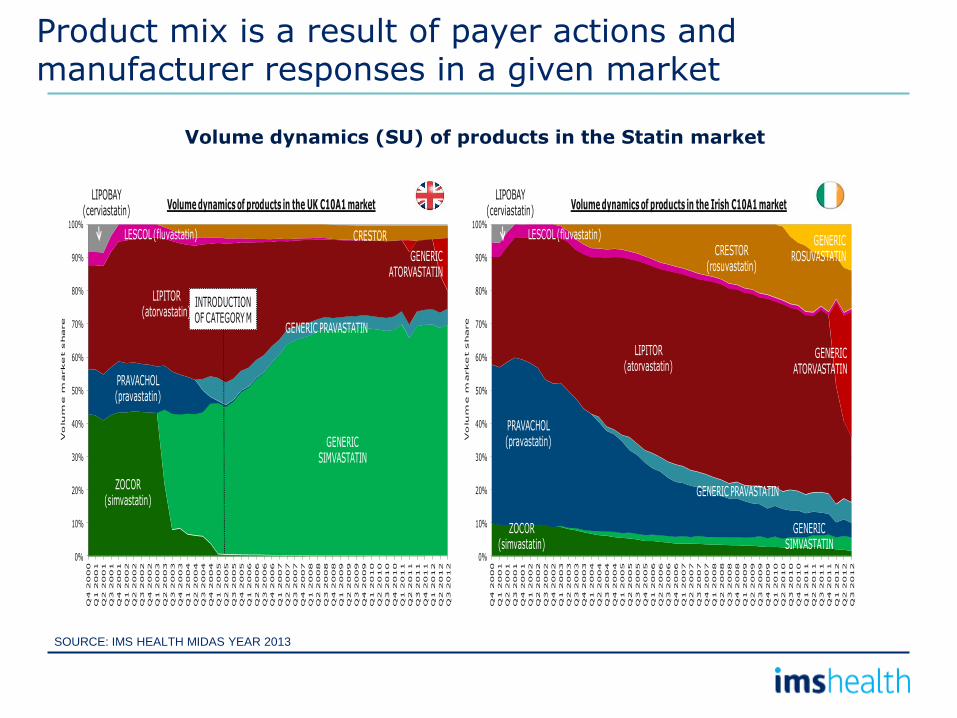

Product mix is a result of payer actions and manufacturer responses in a given market

Volume dynamics (SU) of products in the Statin market

SOURCE: IMS HEALTH MIDAS YEAR 2013

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Q4 2000

Q1 2001

Q2 2001

Q3 2001

Q4 2001

Q1 2002

Q2 2002

Q3 2002

Q4 2002

Q1 2003

Q2 2003

Q3 2003

Q4 2003

Q1 2004

Q2 2004

Q3 2004

Q4 2004

Q1 2005

Q2 2005

Q3 2005

Q4 2005

Q1 2006

Q2 2006

Q3 2006

Q4 2006

Q1 2007

Q2 2007

Q3 2007

Q4 2007

Q1 2008

Q2 2008

Q3 2008

Q4 2008

Q1 2009

Q2 2009

Q3 2009

Q4 2009

Q1 2010

Q2 2010

Q3 2010

Q4 2010

Q1 2011

Q2 2011

Q3 2011

Q4 2011

Q1 2012

Q2 2012

Q3 2012

Volum

e m

arket share

Volume dynamics of products in the Irish C10A1 market

LIPITOR(atorvastatin)

CRESTOR(rosuvastatin)

PRAVACHOL(pravastatin)

ZOCOR(simvastatin)

GENERIC PRAVASTATIN

GENERICATORVASTATIN

GENERICSIMVASTATIN

LESCOL (fluvastatin)

LIPOBAY(cerviastatin)

GENERICROSUVASTATIN

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Q4 2000

Q1 2001

Q2 2001

Q3 2001

Q4 2001

Q1 2002

Q2 2002

Q3 2002

Q4 2002

Q1 2003

Q2 2003

Q3 2003

Q4 2003

Q1 2004

Q2 2004

Q3 2004

Q4 2004

Q1 2005

Q2 2005

Q3 2005

Q4 2005

Q1 2006

Q2 2006

Q3 2006

Q4 2006

Q1 2007

Q2 2007

Q3 2007

Q4 2007

Q1 2008

Q2 2008

Q3 2008

Q4 2008

Q1 2009

Q2 2009

Q3 2009

Q4 2009

Q1 2010

Q2 2010

Q3 2010

Q4 2010

Q1 2011

Q2 2011

Q3 2011

Q4 2011

Q1 2012

Q2 2012

Q3 2012

Volum

e m

arket share

Volume dynamics of products in the UK C10A1 market

INTRODUCTION OF CATEGORY M

LIPITOR(atorvastatin)

CRESTOR

PRAVACHOL(pravastatin)

ZOCOR(simvastatin)

GENERIC PRAVASTATIN

GENERICATORVASTATIN

GENERICSIMVASTATIN

LESCOL (fluvastatin)

LIPOBAY(cerviastatin)

All markets are potentially addressable – the issue is business model and profitability

• What is current addressable market?

• What changes are required to expand the addressable market?

• Who retains the “margin” – wholesaler or pharmacy?

• What will happen with generic prices and industry over time?

• How will generic manufacturers play with a consolidating supply chain?

Wh

o s

ele

cts

th

e m

an

ufa

ctu

rer?

Patient

Pre

scriber

Pharm

acy

/WH

S

Payer

How are prices set?

Tender Free pricing

Regulated

1

2 3

4

5

1. Tender markets

2. Regulated price & dispensing choice

3. Market driven pricing & dispensing choice

4. Regulated price & prescribing choice

5. Out of Pocket markets

Price levels are linked to the generic model but with significant variations and agendas

0%

50%

100%

150%

200%

250%

Generic Price index 40 molecules Dec 2013

Tender Regulated price & dispensing choice

Market driven pricing & dispensing choice

Out Of Pocket Regulated price & prescribing choice

Buyers are for the first time exercising leverage on the Global market

RATIONALE FOR COMPANY MERGERS/CONSOLIDATION

Walgreen’s – Alliance Boots

- AmerisourceBergen

“...streamline the distribution of pharmaceuticals to Walgreens’ stores and

leverage global supply chain efficiencies while

improving patient access to affordable pharmaceuticals to increase the efficiency of the

healthcare system.”

Source: AmerisourceBergen Press Release March 2013

McKesson – Celesio –RITE AID

“A Celesio acquisition will allow McKesson to buy as much as $10 billion a year in generic

drugs for distribution, compared with $6 billion to $7

billion on its own”

Source:

http://www.bloomberg.com January 2014

CVS – Cardinal Health

“This partnership will enable us to maintain our leadership role

in navigating the dynamic U.S. generics market. With its combined volume and capabilities, the joint venture

will develop innovative purchasing strategies with generic manufacturers and

enhance supply chain efficiencies.”

Source: Cardinal health press

release1

84% of the US generic market consolidated to 4 buying consortia 15% of Europe added to the US consortia

SOURCE: 1http://ir.cardinalhealth.com/files/doc_news/2013/CAH%20Press%20Release%2012.10.13.pdf

What drives the ability to negotiate prices?

Type of formulation

• Complexity

− Oral solids the easiest

− Injectables & inhalers the most difficult

Time as generic

• Initial period hardest

• 2 – 10 years period highest opportunity

• >10 years more un-predictable

In addition to the relative size of the buyer, there is a series of factors that determine the ability to negotiate down price

Number of viable suppliers

• A high number (4+) essential for low prices

Price differences give different potential

BRAZIL - 261% 253%- ARGENTINA

VENEZUELA - 242%

234%- SWITZERLAND

MEXICO - 218%

202%-IRELAND GREECE- 194%

CANADA- 152% 149%-FRANCE

BELGIUM-142%

AUSTRIA-126% 122% - ITALY GERMANY &

SPAIN109%

USA-100% 95% - POLAND PORTUGAL-91%

89% - CZECH NORWAY-80%

70%-UK HUNGARY-65%

56%-TURKEY SWEDEN-49%

44%-NETHERLANDS

DENMARK-27%

Buyers from other markets may leverage price from the US markets

Buyers in US may leverage

price from these markets

SOURCE: IMS HEALTH MIDAS YEAR 2013

RELATIVE GENERIC PRICES AT EX-MNF PRICE BEFORE REBATES (100% = USA)

Target segment for international negotiations

The top 200 U.S./European generic molecules accounting for 88% of total value

9%

4%

Source: IMS MIDAS 2013

Highest Potential

Highest Potential

Europe only

target market for negotiations (56%)

U.S. only

Pre-2003

2003-11

2012-13

7%

34%

22%

7%

14% 9%

4%

1% 1%

% of sales for each category split by those products only present in the US, only present in Europe, present in both

% of sales for age band of products versus 1st US generics

Both

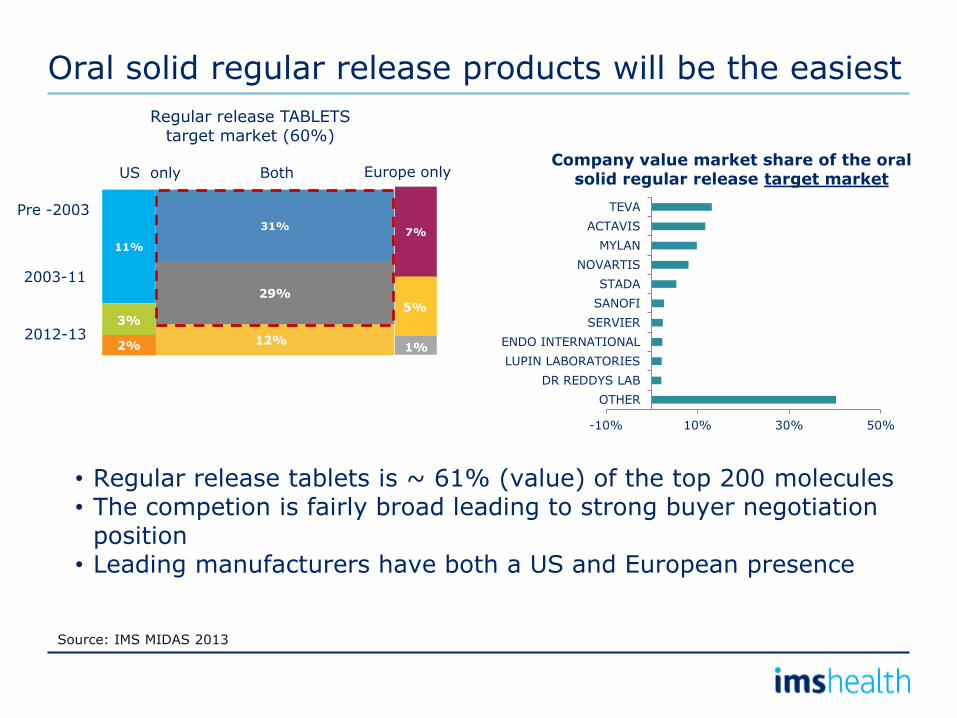

Regular release TABLETS target market (60%)

7% 31%

29%

12%

11%

3%

2%

5%

1%

7%

Source: IMS MIDAS 2013

• Regular release tablets is ~ 61% (value) of the top 200 molecules • The competion is fairly broad leading to strong buyer negotiation

position • Leading manufacturers have both a US and European presence

-10% 10% 30% 50%

OTHER

DR REDDYS LAB

LUPIN LABORATORIES

ENDO INTERNATIONAL

SERVIER

SANOFI

STADA

NOVARTIS

MYLAN

ACTAVIS

TEVA

Company value market share of the oral

solid regular release target market

Pre -2003

2003-11

2012-13

US only Europe only Both

1%

Oral solid regular release products will be the easiest

INJECTABLES Target market (21%)

6%

51%

14%

7%

18%

2% 1%

1%

7%

Source: IMS MIDAS 2013

Injectables will be much more challenging

-10% 10% 30% 50%

OTHER

TEVA

BAYER

APOTEX

DR REDDYS LAB

SUN PHARMA

PFIZER

MEDAC

NOVARTIS

ACTAVIS

SANOFI

Company value market share of the

injectables target market

• Injectables is ~ 4% (value) of the top 200 molecules • The difference in consumption profile is very significant • The competion profile leads to weaker buyer negotiation

position • Leading manufacturers has both a US and European presence

US only Europe only Both Pre -2003

2003-11

2012-13

Europe offers a set of access issues when it comes to securing generic volume

TENDER MARKETS BRANDED GENERICS MARKET

Tendering means that a supplier (for that payer group) is either in or out. This makes planning hard. Tender markets can have products with low competion. Tender market almost always also have non-tendered generic segments

• International contracts have limited impact in European branded generic models

European wholesalers all have limitations of overall country reach.

In most European markets, pharmacists are very open to entertain offers from short liners or direct from manufacturers

WHOLESALER REACH COMPETITION

Tender markets have high price pressure and low volume stability

2 weeks

2 years

1 monthh

0.5 - 2 years

Length of contract

- Volume Predictability +

(-) Market exit as prices become un-sustainable

(-) Without fixed fees for service loss of money (-) Inability to predict volumes

(-)Increased handling & logistics costs (-) Time for explaining product switches to patients (-)Decrease remuneration if no fixed fee in place

MANUFACTURER

WHOLESALER

PHARMACY

PHYSICIAN

PATIENT

(-) Compliance problems (-) Time for explaining changes of products to patients

(-) Patients who reject substitution must pay for alternatives (-) Patient uncertainty/compliant (+) Reduce/stabilise premiums

(+) Cost savings PAYER

PRICE EVOLUTION VOLUME PREDICTABILITY

IMPACT ON STAKEHOLDERS

0.0

0.2

0.4

0.6

0.8

1.0

DE DK NL SE Q4 2013

Q1 2008

SOURCE: IMS HEALTH MIDAS YEAR 2013.

GENERIC SIMVASTATIN (leading form-strength)

Branded Gx markets: dominance of local players, high levels of promotion for all mnf’s and strong brand loyalty

0%

20%

40%

60%

80%

100%

US

FR

NL

UK

BE

DE

ES

PT

SE

AU

CH

NO

IT

FI

IE

HU

CZ

SK

PL

GR

% u

pta

ke

BRANDED GENERICS AS % OF GENERICS MANUFACTURER DYNAMICS (POLAND)

PATIENT BRAND LOYALTY (POLAND)

0.0

0.5

1.0

1.5

2.0

0% 5% 10% 15% 20%

Avr P

ati

en

t co

-pay/

CU

Volume market share %

0.0

0.5

1.0

1.5

2.0

0% 5% 10% 15% 20%

Avr P

ati

en

t co

-pay/

CU

Volume market share%

GENERIC ATORVASTATIN (leading form-strength)

GENERIC PANTOPRAZOLE (leading form-strength)

Segment Retail m/s Promotion*

Originators 49.6% 33.8%

Local generics 17.0% 18.2%

Int. generics 24.0% 33.1%

Other 3.9% 3.6%

* Promotion to doctors and retail pharmacists

Top 50 companies

SOURCE: IMS HEALTH MIDAS YEAR 2013.

Rank Generics

sales 2013 (SU)

MS 2008

MS 2013

MS change 2013/2008

1 TEVA 59.3bn 8% 6% -2

2 NOVARTIS 47.5bn 6% 5% -1

3 MYLAN 32.1bn 4% 3% -1

4 SANOFI 24.5bn 2% 2% 0

5 ACTAVIS 23.7bn 3% 2% -1

6 SUN / RNBX 19.6bn 2% 2% 0

7 LUPIN 12.8bn 1% 1% 0

8 DR REDDY’S 9.1bn 1% 1% 0

Growth from leading manufacturers is from acquisitions

Size is increasing through acquisitions / strategic alliances

Top Global and Indian generic corporations are heavily dependent on the US market

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

TEVA NOVARTIS MYLAN ACTAVIS SANOFI DRL LUPIN SUN / RNBX

Sh

are

Vo

lum

e

Sale

s (

SU

)

US Canada Top 5 Europe ROW Pharmerging Japan

Selected top Gx companies – Volume sales breakdown 2013

Top 5

Source: IMS Health, MIDAS, MAT Dec 2013. Market Segmentation + LIC countries. (market seg. not coded and protection not covered excluded)

India

Sanofi is an exception with strong presence in EMs gained through acquisitions

Global generic market is more fragmented

3%

SANOFI

2%

ABBOTT

others

MENARINI

1%

APOTEX

2% CIPLA

3% NOVARTIS

4%

MYLAN 6%

MERCK KGAA

7%

GSK

9%

TEVA

11%

53%

Top 5 molecules 2013 Sales Split, 110 bn SU

MENARINI

TEVA

13%

6%

8%

BAYER 6%

GSK

48% others

SANOFI

4% MERCK KGAA

2%

3%

NOVARTIS

CIPLA AMPHASTAR

2%

MYLAN 3% 4%

Top 5 molecules 2008 Sales Split, 81 bn SU

Top molecules 2008: OMEPRAZOLE SIMVASTATIN FENTANYL AMOXICILLIN#CLAVULANIC ACID PANTOPRAZOLE Top molecules 2013: AMOXICILLIN#CLAVULANIC ACID , METHYLPHENIDATE , PANTOPRAZOLE , ATORVASTATIN , OMEPRAZOLE

The top 5 manufacturers

1. Heavily dependent on the US market

2. Represent < than 35% MS of Top 5 molecules by value sales, facing strong competition from a large number of smaller players

3. Several MNFs (Sanofi, Teva, Novartis) are increasingly focus on “specialty”

4. Top Global and Indian MNF’s are often the “first to market” in the US (e.g. Lipitor/RNBX, Losartan/Teva)

5. Portfolio varies with each of them focusing on different molecules

6. Are losing MS to smaller players. Growth is generated through acquisitions /strategic alliances

Reasons for Generic Price Inflation

Regulatory/Quality – with the increased scrutiny from the FDA, manufacturers need to invest more into their quality systems and when a quality / supply issue arises due to 483s, it creates the opportunity to increase prices to recoup part of their investment

Customer consolidation – with the increased purchasing power of the customers, manufacturers need to make up value on products where they can

Fewer new product launches – generic manufacturers make money by launching new products, reducing CGS, M&A activity and raising prices; with fewer launches, it puts more pressure on the “in-line” product portfolio which again is a driver to increase prices

67 Walgreens

November 18, 2014

Therapy lifecycle model over time

• Generics dominate in most areas of high volume chronic use

Note: Size of bubbles = 2012 European Medicines spend

Source: A.T.Kearney analysis, IMS ATC analysis (2013)

‘Delivering Innovation’

‘Addressing Unmet Needs’

‘Generic medicines dominate’

Rew

ard

ing

In

no

vati

on

S

ocie

ty

ben

efi

t

Hormonal Contraception

Respiratory

Pain

Hypertension

Oncology

Autoimmune

Direct Thrombin Inhibitors

Bacterials

Antifungals

Gene Therapy

Lipid Regulators

Nervous System

Diabetes

Time

Stem Cells

Antihypertensives and pain therapies are the largest value GX therapy areas while antibacterials and lipid regulators the most penetrated

Source: IMS Health, MIDAS, Market Segmentation, MAT Jun 2013, Rx only. It doesn’t include Denmark

5,000

9,000

10,000

2,000

0

1,000

3,000

4,000

6,000

7,000

8,000

3,058

37%

63%

Hepari

ns

2,761

96%

4%

5,014

Menta

l H

ealth

Antibacte

rials

Oncolo

gic

s

5,848

63%

80%

Nnerv

ous S

yste

m D

is

50%

20%

49% 50%

Antihypert

ensiv

es

48%

57%

Pain

37%

43%

5,445

Valu

e $U

S (

thousands M

illions)

51% Anti-u

lcera

nts

9,558

52%

4,898

3,890

39%

Respir

ato

ry

61%

3,215

63%

37%

Lip

id R

eg

7,955

Generics Non Generics

EU- Generic penetration rate by therapy area (overall leading 10 Therapy Area)

Unprotected MK value segmentation

Antihypertensives is the largest volume GX therapy area while anti-diabetics, anti-ulcerants and lipid regulators the most penetrated

Source: IMS Health, MIDAS, Market Segmentation, MAT Jun 2013, Rx only. It doesn’t include Denmark

65

10

5

0

30

45

40

35

25

20

15

50

55

60

64%

36%

Oth

er

CN

S

16,8

45%

55%

Anti-u

lcera

nts

15,5

20%

80% Antidia

betics

15,3

19%

29%

Menta

l H

ealth

14,9

30%

70%

Lip

id R

eg

13,7

18%

82%

Nerv

ous S

yste

m D

is.

9,7

55%

45% Volu

me S

tandard

Units (

SU

) Billions

9,1

19%

81%

Antihypert

ensiv

es

60,1

71%

81%

Pain

34,8

30%

70%

Respir

ato

ry

31,5

Thyro

id P

reps

Generics Non Generics

EU- Generic penetration rate by therapy area (overall leading 10 Therapy Area)

Unprotected MK volume segmentation

The future generic potential rests across several therapeutic areas

Source: IMS MIDAS Q3 2012. Based on ethical market. Revenues based on MAT 9/2012. * Immunostim ag ex Intfron left out (it would be the 8th largest TA, with LoE in 2012 and 2014 for a total of US $4,3 Bn)

0

2

4

6

8

10

12

14

16

US

$ B

n R

even

ues f

acin

g L

oE

2016

2015

2014

2013

2012

Top 10 Therapeutic groups facing LoE 2012-2016

71

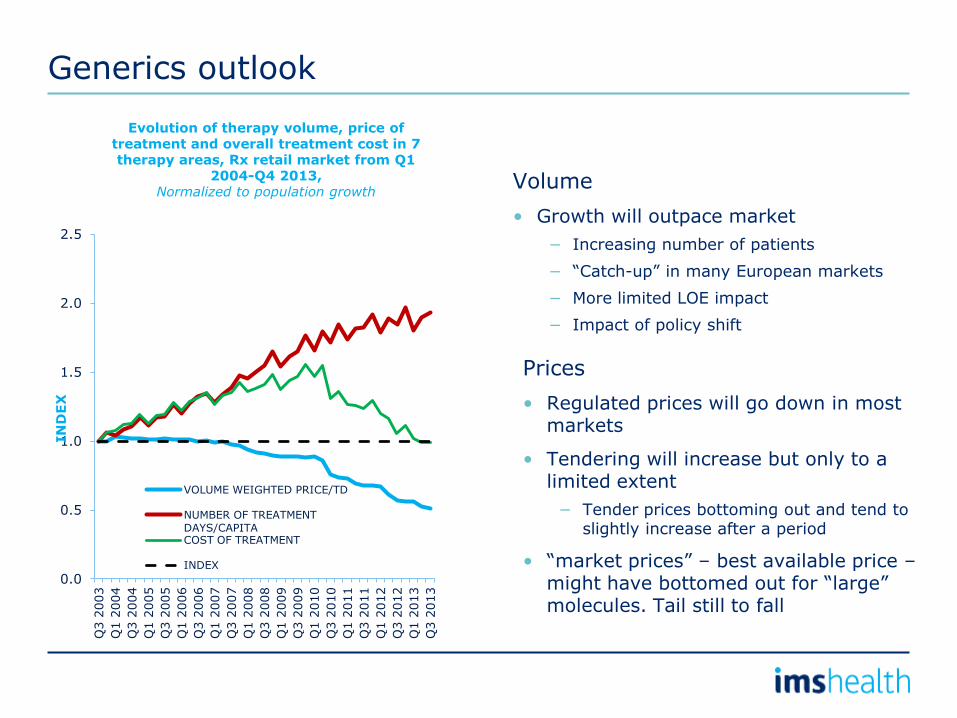

Generics outlook

Volume

• Growth will outpace market

− Increasing number of patients

− “Catch-up” in many European markets

− More limited LOE impact

− Impact of policy shift

Prices

• Regulated prices will go down in most markets

• Tendering will increase but only to a limited extent

− Tender prices bottoming out and tend to slightly increase after a period

• “market prices” – best available price – might have bottomed out for “large” molecules. Tail still to fall

Evolution of therapy volume, price of treatment and overall treatment cost in 7 therapy areas, Rx retail market from Q1

2004-Q4 2013, Normalized to population growth

0.0

0.5

1.0

1.5

2.0

2.5

Q3 2

003

Q1 2

004

Q3 2

004

Q1 2

005

Q3 2

005

Q1 2

006

Q3 2

006

Q1 2

007

Q3 2

007

Q1 2

008

Q3 2

008

Q1 2

009

Q3 2

009

Q1 2

010

Q3 2

010

Q1 2

011

Q3 2

011

Q1 2

012

Q3 2

012

Q1 2

013

Q3 2

013

IN

DE

X

VOLUME WEIGHTED PRICE/TD

NUMBER OF TREATMENT DAYS/CAPITA COST OF TREATMENT

INDEX

Agenda

• Major trends and Global Medicines Spend

• Specialty medicines

• Generic medicines and purchasing alliances

• Conclusions

Conclusions

• Dollar growth is improving in the developed markets and softening a bit in Pharmerging markets

• As the small molecule opportunity drought hits and the specialty drug wave accelerates, payers will be desperate to get cost savings somewhere…

− Generics

− Biosimilars

• Generic share will continue to grow but there will be more regulatory oversight

• Generics are a solution

IMS Health

Thank You!