global finance and growth case uk 2016

TRANSCRIPT

Global Finance and Growth

Joeri Schasfoort

University of Groningen

Dirk Bezemer

University of Groningen

and thanks to

Final assignment

and thanks to

Final assignment

Overview

1. The assignment

2. Example: United Kingdom 1. Finance in the domestic economy

2. International financial relations

3. Policy options and conclusions

3. Q&A

4. Break

5. Guest lecture Joram Kok (Pelargos capital)

6. Q&A

Chapter 1 –Finance in the Domestic Economy Chapter 2 – International Financial Relations Chapter 3 - Opportunities and Risks Chapter 4 – Summary and Policy Options

The Assignment An investment company has come to you to help them assess macro-financial risks and opportunities. You are going to write a country report for them. Report Structure:

Groups

Example: United Kingdom

What do you know about the British economy?

Biggest risks and opportunities.

• ?

• ?

• ?

• ?

Example: United Kingdom

Chapter 1 –Finance in the Domestic Economy

Ch1: Finance in the Domestic Economy

and thanks to

Disclaimer: not a full report

Composition of GDP

Source: UN

Chapter 1 –Finance in the Domestic Economy

How is GDP growth financed?

Is it sustainable?

Chapter 1 –Finance in the Domestic Economy

Population boom, inflation, unemployment, government finances.

Source: IMF

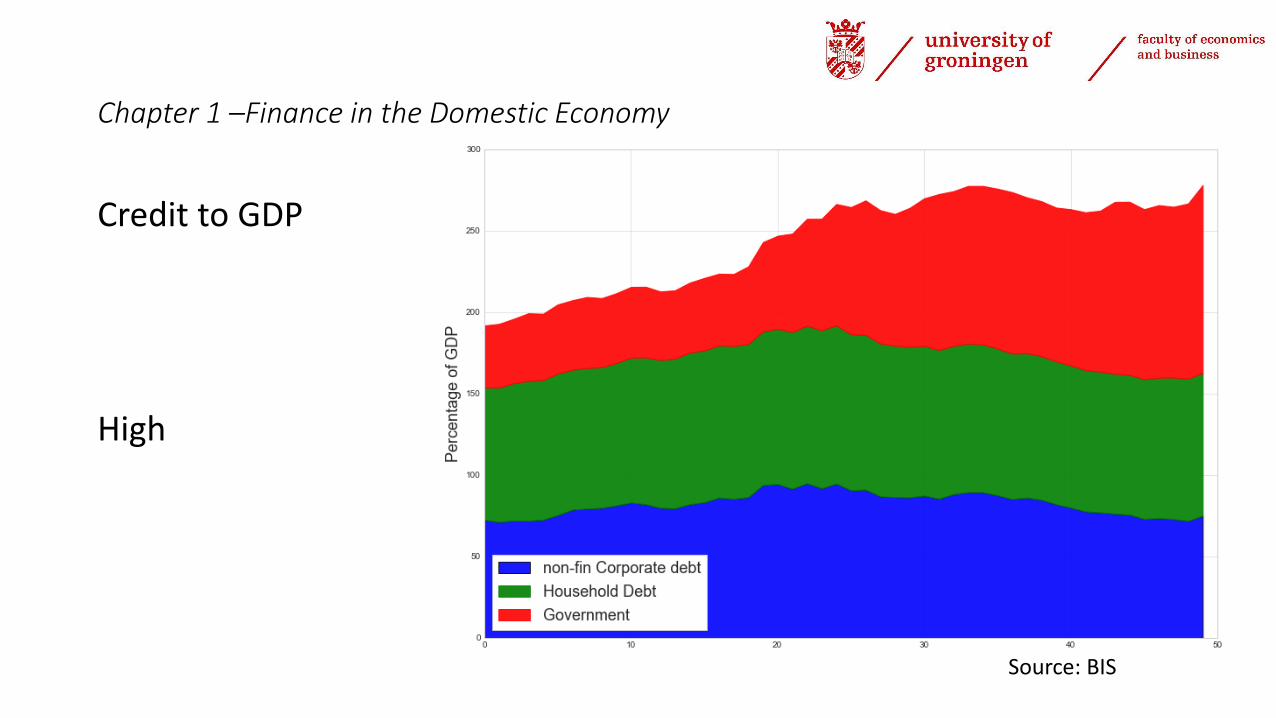

Chapter 1 –Finance in the Domestic Economy

Credit to GDP

High

Source: BIS

Chapter 1 –Finance in the Domestic Economy

Chapter 1 –Finance in the Domestic Economy

Household credit expansion

Source: BoE

Housing market boom

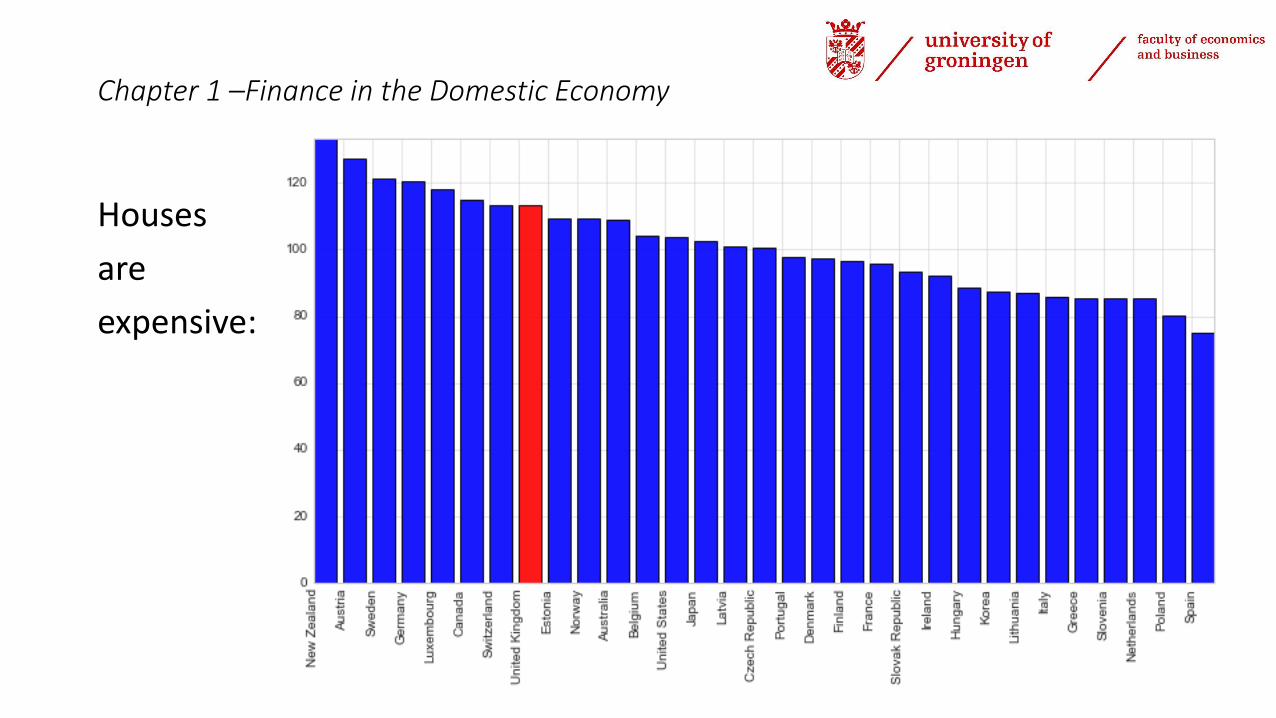

Chapter 1 –Finance in the Domestic Economy

Houses

are

expensive:

Source: BIS

Chapter 1 –Finance in the Domestic Economy

Ch3: Risks

• Population growth might slow down (Brexit)

• House prices Can it go up much further?

• Consumer credit boom ….

• High credit to GDP, not much room?

Ch3: Opportunities

• Credit growth seems to have slowed down.

• Government budget can expand.

Ch2: International financial relations

and thanks to

Disclaimer: not a full report

International financial relations

Negative

Current account

Source: IMF

International financial relations

Capital &

Financial accounts

Source: IMF

International financial relations

Smaller gross flows

Source: IMF Source: BIS

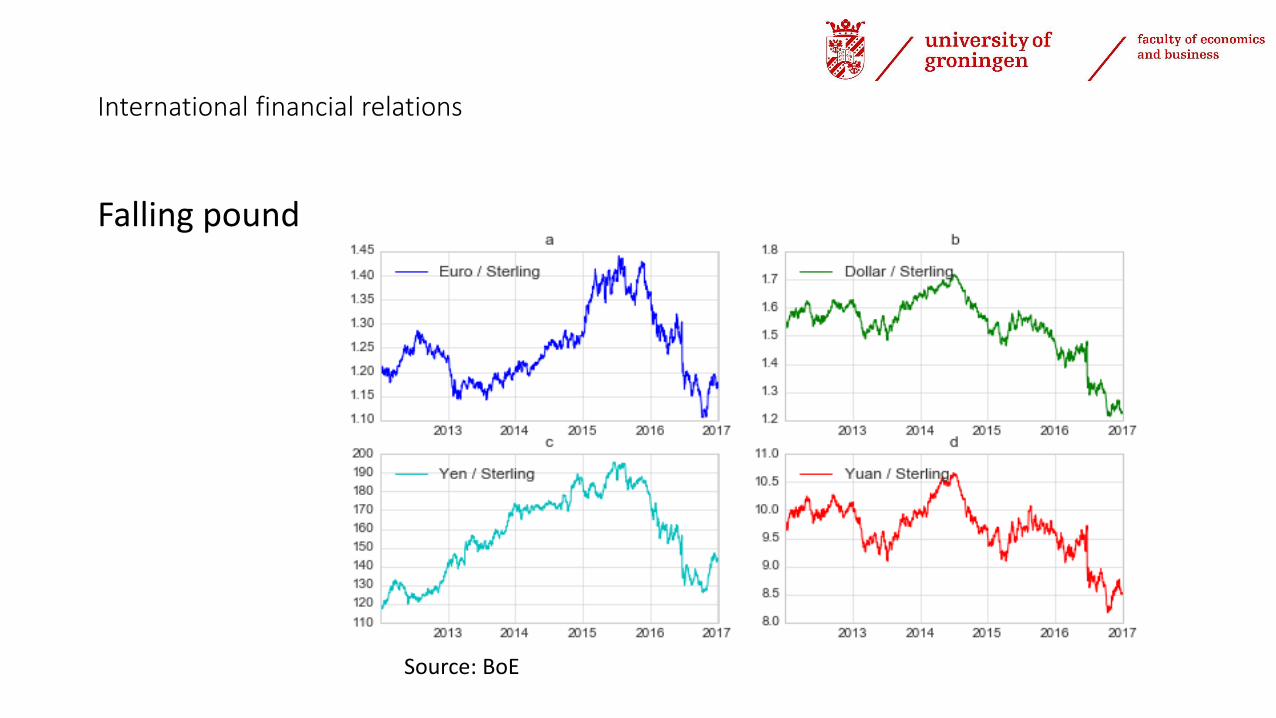

International financial relations

Falling pound

Source: BoE

Ch3: Risks

• Persistent current account deficit

• Might worsen because of brexit? direct FX effect – service revenue

• Might improve because of brexit? indirect FX effect

competitiveness of manufacturing industry.

• Relatively modest gross flows

International financial relations

Negative international

investment position

Source: IMF

International financial relations

Foreign Assets & Liabilities

Source: BIS

Ch3: Opportunities & Risks

London is a global banking center:

• Banks have assets and liabilities in FX

• Large global exposure

International financial relations

High

short term

Debt

(Calvo)

Sudden-stop

Ch3: Risks

London is a global banking center:

• Lot of short-term debt

Ch3: Opportunities & Risks

(Rey) Global financial cycle

Source: OECD

Ch3: Opportunities & Risks

(Merhling) Hierarchy of money GBP 3rd used currency

Ch4 Policy options and conclusion

and thanks to

Policy options and conclusions

Biggest risks

• Household credit Consumption driven economy

• House prices

• Large current account deficit

• Large global banking sector global & sudden stop exposure

Policy options and conclusions

Biggest opportunities?

The Policy Trilemma

UK

Policy options and conclusions

Policy options

• Monetary policy (limited high credit)

• Capital controls (limited global banking system)

• Fiscal policy some headroom

• These were examples of graphs you can make … not a full-fledged assignment

• Also think about tables, correlations, international comparisons…

• Can you use or make the graphs and tables in the course literature for your country?

Thank you for listening… Questions?

Time for a break!

Applying Theory in Practice

January, 2017

Overview

Pelargos > Overview

Agenda

- U.K. case

- Financial markets perspective

- China case

- The impossible Trinity, a practical theory

Goals

Practical use of the course in general and assignment in particular;

Interrelatedness between financial asset prices and economic environment;

Complexity of the real world;

U.K. Case

Pelargos > U.K Case

U.K. Case

Pelargos > U.K Case

0

5

10

15

20

25

30

1700 1750 1800 1850 1900 1950 2000

S. Ireland included in NGDP before 1920

per cent of nominal GDP

The Bank of England Balance sheet 1700-2014

0%

5%

9%

14%

18%

The bank of England Policy Rate

0

1

2

3

4

5

6

7

8

9

1-5

-20

02

1-1

2-2

00

2

1-7

-20

03

1-2

-200

4

1-9

-20

04

1-4

-20

05

1-1

1-2

00

5

1-6

-20

06

1-1

-20

07

1-8

-20

07

1-3

-20

08

1-1

0-2

00

8

1-5

-20

09

1-1

2-2

00

9

1-7

-20

10

1-2

-20

11

1-9

-20

11

1-4

-20

12

1-1

1-2

01

2

1-6

-20

13

1-1

-20

14

1-8

-201

4

1-3

-20

15

1-1

0-2

01

5

1-5

-20

16

1-1

2-2

01

6

UK GOVT. BOND 10 YEAR YIELD UK CORP BOND AAA 10Y YIELD

UK CORP BOND BBB 10Y YIELD

China Case: Overview

Pelargos > China Case

• The Three Angles

1. Independent Monetary Policy

2. Free movement of Capital

3. Fixed Exchange Rate

• Conclusion

1. Exchange Rate to be weakened

2. Execution: Currency Option to hedge Financial Market Instability

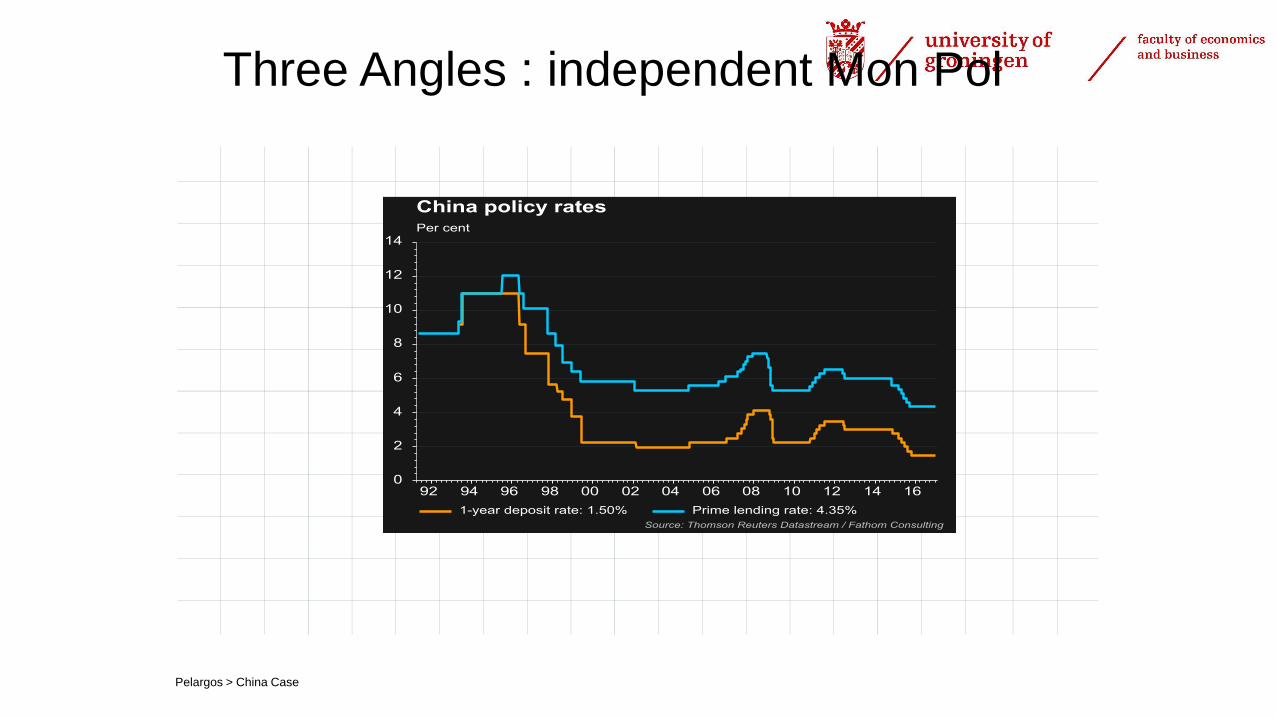

Three Angles : independent Mon Pol

Pelargos > China Case

Three Angles : independent Mon Pol

Pelargos > China Case

10

15

20

25

30

35

40

45

50

70

90

110

130

150

170

190

210

230

Q12006

Q32006

Q12007

Q32007

Q12008

Q32008

Q12009

Q32009

Q12010

Q32010

Q12011

Q32011

Q12012

Q32012

Q12013

Q32013

Q12014

Q32014

Q12015

Q32015

Q12016

CH CREDIT TO NONFINL CORPS % GDP CH CDT TO PRIV NONFINL SCT % GDP

CREDIT TO HSDS & NPISHS % GDP (RHS)

80

85

90

95

100

105

110

115

1-1

-19

96

1-9

-19

96

1-5

-19

97

1-1

-19

98

1-9

-199

8

1-5

-19

99

1-1

-20

00

1-9

-20

00

1-5

-20

01

1-1

-20

02

1-9

-20

02

1-5

-20

03

1-1

-20

04

1-9

-20

04

1-5

-20

05

1-1

-20

06

1-9

-20

06

1-5

-20

07

1-1

-20

08

1-9

-20

08

1-5

-20

09

1-1

-20

10

1-9

-20

10

1-5

-20

11

1-1

-20

12

1-9

-201

2

1-5

-20

13

1-1

-20

14

1-9

-20

14

1-5

-20

15

1-1

-20

16

1-9

-20

16

PPI CPI

Three Angles: independent Mon Pol

Pelargos > China Case

Three Angles : independent Mon Pol

Pelargos > China Case

Three Angles : Free Movement of Cap.

Pelargos > China Case

Three Angles : Fixed Exchange Rate

Pelargos > China Case

5

6

7

8

9

10

11

Q1

199

9

Q3

199

9

Q1

200

0

Q3

200

0

Q1

200

1

Q3

200

1

Q1

200

2

Q3

200

2

Q1

200

3

Q3

200

3

Q1

200

4

Q3

200

4

Q1

200

5

Q3

200

5

Q1

200

6

Q3

200

6

Q1

200

7

Q3

200

7

Q1

200

8

Q3

200

8

Q1

200

9

Q3

200

9

Q1

201

0

Q3

201

0

Q1

201

1

Q3

201

1

Q1

201

2

Q3

201

2

Q1

201

3

Q3

201

3

Q1

201

4

Q3

201

4

Q1

201

5

Q3

201

5

Q1

201

6

Q3

201

6

Q1

201

7

CHINESE YUAN TO US $ (WMR) - EXCHANGE RATE CHINESE YUAN TO EURO (WMR) - EXCHANGE RATE

CHINESE YUAN TO 100 JAPANESE YEN - EXCHANGE RATE

Three Angles : Fixed Exchange Rate

Pelargos > China Case

0,00%

5,00%

10,00%

15,00%

20,00%

25,00%

30,00%

35,00%Q

1 1

99

4

Q1

19

95

Q1

19

96

Q1

19

97

Q1

19

98

Q1

19

99

Q1

20

00

Q1

20

01

Q1

20

02

Q1

20

03

Q1

20

04

Q1

20

05

Q1

20

06

Q1

20

07

Q1

20

08

Q1

20

09

Q1

20

10

Q1

20

11

Q1

20

12

Q1

20

13

Q1

20

14

Q1

20

15

Q1

20

16

Foreign Exchange Reserves/M2

China IMF Lower Bound

China

Source: Thomson Reuters,

Conclusion

Pelargos > China Case

- China ‘needed’ looser monetary policy to deal with slowing growth, high private debt

levels, PPI deflation;

- China wanted more open capital account;

- China had a ‘managed’ exchange rate.

Hence, something had to give, we figured it would be the exchange rate:

- Would increase inflation;

- Would make exporters more competitive, easing pressure on corporate profitability,

improving debt service capabilities, lower non-performing assets of banking sector;

- Would allow China to continue financial market reform (needed for IMF SDR

inclusion);

- Enable Central Bank to keep foreign exchange reserves

Conclusion

Pelargos > China Case

Given these assumptions, how to execute?

- Time horizon

- When will China devalue the currency?

- How quick will China devalue? Credible one-off or managed devaluation?

- Scope

- What would be the size of the devaluation?

Thank you for listening… Questions (round 2)?