global construction outlook - ihs · pdf file• powerhouse of global growth: 2002–06...

TRANSCRIPT

Global Construction Outlook

Scott HazeltonDirector of Construction Services

Copyright © 2008 Global Insight, Inc. 2

Global Shock Waves

• The “double-shock” world economy— subprime crisis plus record-high oil prices

• Crisis status—we are not out of the woods yet• Global transmission of crisis—no de-coupling• Crisis management—shifting into high gear• Global inflation—how big of a threat?• Weaker growth in the developed economies…

…Means that emerging markets will eventually slow as well

• The risks are predominantly on the downside

Copyright © 2008 Global Insight, Inc. 3

-2

-1

0

1

2

3

4

5

6

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

Perc

ent c

hang

e

Real GDPIndustrial Production

The World’s Economic Expansion Is Slowing

Copyright © 2008 Global Insight, Inc. 4

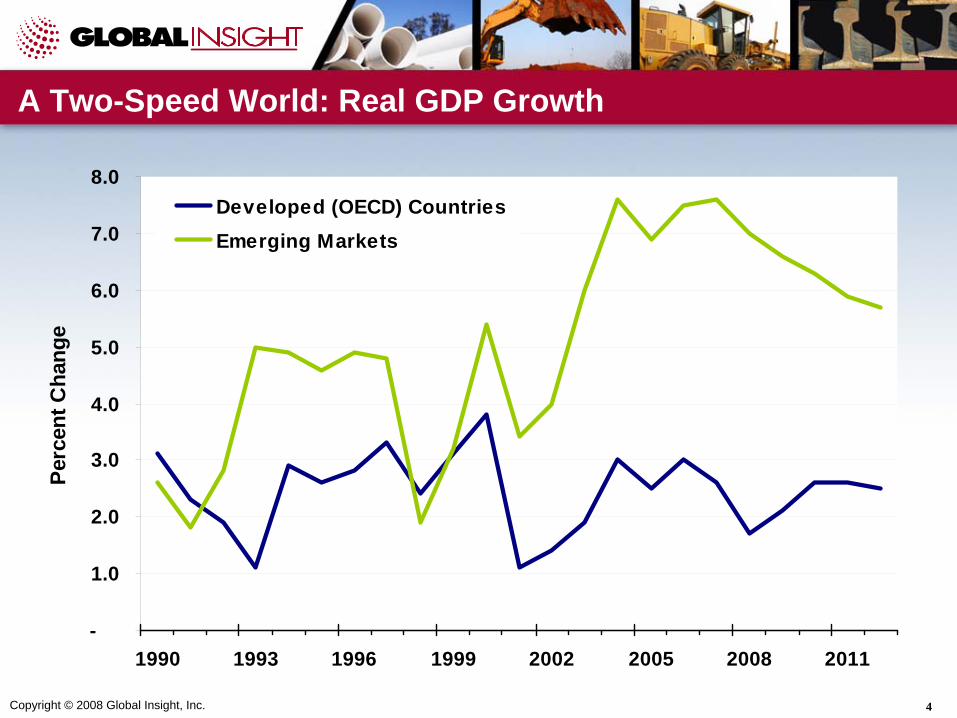

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

1990 1993 1996 1999 2002 2005 2008 2011

Perc

ent C

hang

e

Developed (OECD) CountriesEmerging Markets

A Two-Speed World: Real GDP Growth

Copyright © 2008 Global Insight, Inc. 5

Wide Variations in Regional Economic Growth

0

1

2

3

4

5

6

7

8

9

NAFTA WesternEurope

Japan OtherAsia

EmergingEurope

Mideast -N. Africa

OtherAmericas

Rea

l GD

P, P

erce

nt c

hang

e

20062007200820092010

Copyright © 2008 Global Insight, Inc. 6

Source: OECD

Output Gaps Show Little Spare Capacity

-4

-3

-2

-1

0

1

2

3

4

5

1990 1993 1996 1999 2002 2005

Gap

as

Perc

ent o

f Pot

entia

l Rea

l GD

P

Total OECDUnited StatesEurozoneJapan

Copyright © 2008 Global Insight, Inc. 7

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Rea

l GD

P, P

erce

nt c

hang

e

Eurozone

Eurozone: Real GDP Growth

Copyright © 2008 Global Insight, Inc. 8

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

France Germany Italy Spain U.K.

Rea

l GD

P, P

erce

nt c

hang

e

20062007200820092010

Real GDP Growth Rates Vary Across Europe

Copyright © 2008 Global Insight, Inc. 9

Asia: Cyclical Peak

• Powerhouse of global growth: 2002–06 average growth 7.0%; 8.0% in 2007 (excl. Japan)

• BOP positions have strengthened, debt burdens have eased, strong fiscal positions more resilience to shocks

• Big plus: investment and private consumption are finally recovering

• Slowdown will be moderate, but risks have increased• No true “de-coupling”• Inflation is a problem: currency appreciation a better

policy option than interest rate hikes

Copyright © 2008 Global Insight, Inc. 10

Japan: Sluggish Growth Ahead

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2004 2005 2006 2007 2008 2009 2010 2011

Rea

l GD

P, P

erce

nt c

hang

e

Japan

Copyright © 2008 Global Insight, Inc. 11

Real GDP Growth in Asia-Pacific Economies

0.0

2.0

4.0

6.0

8.0

10.0

12.0

China India South Korea Australia Taiwan

Rea

l GD

P, P

erce

nt c

hang

e

20062007200820092010

Copyright © 2008 Global Insight, Inc. 12

Real GDP Growth in Asia-Pacific Economies

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Indonesia Hong Kong Malaysia Singapore Philippines Thailand

Rea

l GD

P, P

erce

nt c

hang

e

20062007200820092010

Copyright © 2008 Global Insight, Inc. 13

China: The “Double Squeeze”

• Economy could be squeezed domestically and externallyMonetary policy tightening has startedExports to the United States already slowing

• Policy dilemma—exports and investment/inflation in different phases of cycle, and require countering policies

• Without inflation risk, Beijing is willing to continue loose monetary policy to cushion the impact of sliding exports

• Asset bubbles may also be a threat• Risks of a boom-bust are still 35% to 40%

Copyright © 2008 Global Insight, Inc. 14

-5

0

5

10

15

20

25

1980 1983 1986 1989 1992 1995 1998 2001 2004 2007 2010

Perc

ent C

hang

e

Real GDPGDP Deflator

China’s Current Business Cycle Is Relatively Mild

Copyright © 2008 Global Insight, Inc. 15

Emerging Europe: Robust Despite Deteriorating External Environment

• While exports have been supportive, domestic demand has been driving output growth

• Central Europe continues to expand share of key Western European markets as FDI boosts export capacity, productivity

• Baltics, Balkans show signs of overheating; tighter global credit conditions could help orchestrate a softer landing

• Russia, other energy exporters in CIS riding world market oil prices. Domestic demand will continue to grow rapidly, but surging imports trimming external surpluses

Copyright © 2008 Global Insight, Inc. 16

Real GDP Growth in Emerging Europe

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

Russia Turkey Poland CzechRepublic

Hungary Romania

Rea

l GD

P, P

erce

nt c

hang

e

20062007200820092010

Copyright © 2008 Global Insight, Inc. 17

Latin America: One Region, Two Stories

• Mexico, Central America, and Colombia: the United States is their main trading partner

• Rest of South America: a commodities storyStrong demand from the rest of the world will continue to support high growth rates in an environment of relative capital intensive exports

• The Latin American region is now better prepared to avoid crisis contagion…

• …But while the vulnerability to external finance is less, the vulnerability to external demand is substantial

• Parts of the region are vulnerable to a China hard landing

Copyright © 2008 Global Insight, Inc. 18

Real GDP Growth in Latin America

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Argentina Brazil Chile Colombia Mexico Peru Venezuela

Rea

l GD

P, P

erce

nt c

hang

e

2006 2007 20082009 2010

Copyright © 2008 Global Insight, Inc. 19

Middle East / North Africa — Maybe a Bust, But Not Now

• MENA’s current economic boom will not falter this year—it is actually intensifying

• Even an oil crash will not immediately affect the region’s economy, thanks to improved fundamentals

• However, the boom has strained the economy’s capacity, leading to increasingly severe overheating

• Sectors hurt most by capacity limits: energy, utilities, housing, construction, and manufacturing

• The boom may be headed for a bust, but not in 2008

Copyright © 2008 Global Insight, Inc. 20

MENA Fiscal Balances Are Strongly Positive…

-18

-13

-8

-3

2

7

12

1990 1993 1996 1999 2002 2005 2008

Fisc

al b

alan

ce, (

Per

cent

of G

DP)

Middle East & North AfricaMiddle EastNorth Africa

Copyright © 2008 Global Insight, Inc. 21

Large External Assets Can Cushion Any Oil Price Shock…

0.00

0.25

0.50

0.75

1.00

1.25

1.50

1.75

1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

MEN

A E

xter

nal A

sset

Sto

cks,

(tril

lions

of U

.S. d

olla

rs)

MENA, External Asset Stocks

Copyright © 2008 Global Insight, Inc. 22

Region is Overheating, Making a Boom-Bust Worrisome

0

1

2

3

4

5

6

7

8

9

10

2000 2001 2002 2003 2004 2005 2006 2007

CPI

Infla

tion,

(per

cent

)

MENAMiddle EastNorth Africa

Copyright © 2008 Global Insight, Inc. 23

Real GDP Growth in the Middle East and Africa

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Saudi Arabia South Africa Iran UAE Israel Nigeria

Rea

l GD

P, P

erce

nt c

hang

e

20062007200820092010

Copyright © 2008 Global Insight, Inc. 24

Total Construction Regional Review

50

100

150

200

250

300

350

1997 2000 2003 2006 2009 2012

Inde

x, 1

998

= 10

0

WorldAsiaNon-Japan AsiaWestern EuropeEastern EuropeNorth AmericaSouth AmericaMiddle East & Africa

Copyright © 2008 Global Insight, Inc. 25

Asia is Gaining Share from Developed Countries

Asia46%

South America

5%

Western Europe

23%

Eastern Europe

4%

North America

18%

Middle East & Africa

4%Asia39%

South America

5%

Western Europe

28%

Middle East & Africa

4%

North America

21%

Eastern Europe

3%

2007 2017

Copyright © 2008 Global Insight, Inc. 26

Circle Size = Total Nominal Construction Spending in 2006

United StatesJapan

China

Germany

United Kingdom

Italy

France

Spain

Canada

Netherlands

MexicoAustralia

South Korea

Russia

Brazil

India

-2%

0%

2%

4%

6%

8%

10%

12%

14%

5 10 15 20 25 30 35 40 45 50

Construction Risk Score - 5 Year

Tota

l Con

stru

ctio

n Sp

endi

ng G

row

th

(Rea

l 200

0 U

.S. D

olla

rs, C

AG

R %

, 200

7-20

12)

Med

ian

Con

stru

ctio

n R

isk

Average Global Construction Growth

Construction Risk-Reward Outlook

Copyright © 2008 Global Insight, Inc. 27

Total Construction Spending 2000 US$ Billions

2006Growth % 2007-2008

Growth % 2008-2009

Growth, CAGR % 2007-2012

United States 831.4 (-8.8%) +2.4% +2.2%

Japan 771.9 +0.4% +1.2% +1.1%

China 418.2 +16.5% +9.2% +9.2%

United Kingdom 263.5 +0.2% +1.7% +2.7%

France 178.3 +2.2% +2.6% +2.7%

Germany 168.8 +1.4% +1.9% +1.6%

Spain 155.5 +1.7% +1.0% +1.4%

Italy 141.7 (-0.1%) +0.9% +0.8%

Korea 126.0 +2.7% +2.7% +3.3%

Canada 116.9 +0.8% +1.7% +2.8%

India 113.3 +9.9% +9.6% +9.4%

Brazil 94.6 +5.6% +4.2% +4.6%

Mexico 72.7 +5.6% +6.6% +6.1%

Australia 71.5 +4.6% +4.9% +5.1%

Netherlands 58.0 +1.8% +1.9% +1.8%

Saudi Arabia 53.9 +6.7% +5.5% +5.7%

68 Country Total 4,399.3 +2.5% +3.9% +3.9%

Total Real Construction Spending Growth2000 US$

Top 15 Countries by Construction Spending

Copyright © 2008 Global Insight, Inc. 28

Top 15 Countries by Construction Growth

Total Construction Spending 2000 US$ Billions

2006Growth % 2007-2008

Growth % 2008-2009

Growth, CAGR % 2007-2012

Vietnam 11.5 +14.8% +15.0% +14.5%Romania 8.2 +15.6% +12.0% +12.1%Panama 1.8 +9.2% +8.2% +10.1%Venezuela 26.2 +13.5% +10.3% +9.7%India 113.3 +9.9% +9.6% +9.4%China 418.2 +16.5% +9.2% +9.2%Colombia 13.2 +11.8% +9.4% +8.6%Russia 41.6 +11.4% +8.4% +8.4%Senegal 0.9 +8.5% +8.2% +8.1%Peru 8.0 +13.8% +10.1% +8.1%United Arab Emirates 29.2 +11.8% +6.9% +7.8%Tunisia 4.1 +7.3% +7.8% +7.7%Iran 16.7 +8.3% +7.6% +7.1%Indonesia 41.5 +7.4% +7.0% +6.6%Chile 14.1 +6.7% +6.8% +6.5%

68 Country Total 4,399.3 +2.5% +3.9% +3.9%

Total Real Construction Spending Growth2000 US$

Copyright © 2008 Global Insight, Inc. 29

Total Construction Growth by Region

3.2%

2.1%

5.9%

6.0%

6.5%

5.3%

9.3%

3.9%

0.0% 2.0% 4.0% 6.0% 8.0% 10.0%

North America

Western Europe

Middle East & Africa

Eastern Europe

Asia

South America

Non-Japan Asia

World

Compound Annual Growth 2007-2012 (Percent)

Copyright © 2008 Global Insight, Inc. 30

Total Construction Growth Looks Strong

0%

1%

2%

3%

4%

5%

6%

7%

Total NonresidentialStructures

Infrastructure Residential

Com

poun

d A

nnua

l Gro

wth

(Per

cent

)

2002-072007-122012-17

Copyright © 2008 Global Insight, Inc. 31

Nonresidential Growth Outlook is Mixed

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

NonresidentialStructures

Office Commercial Institutional Industrial

Com

poun

d A

nnua

l Gro

wth

(Per

cent

) 2002-072007-122012-17

Copyright © 2008 Global Insight, Inc. 32

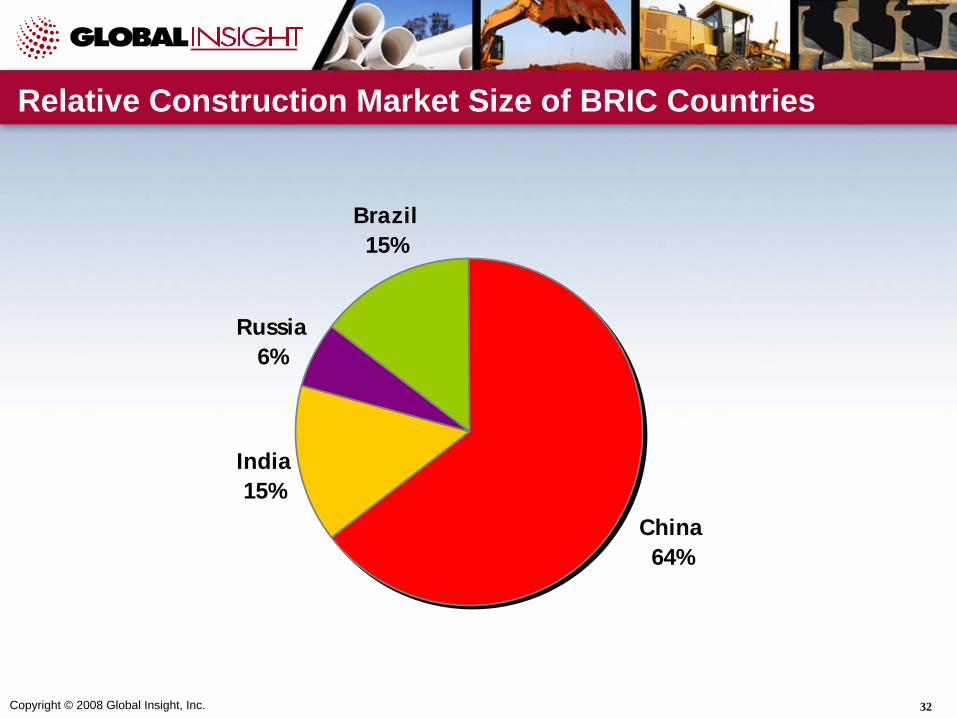

Relative Construction Market Size of BRIC Countries

India15%

China64%

Brazil15%

Russia6%

Copyright © 2008 Global Insight, Inc. 33

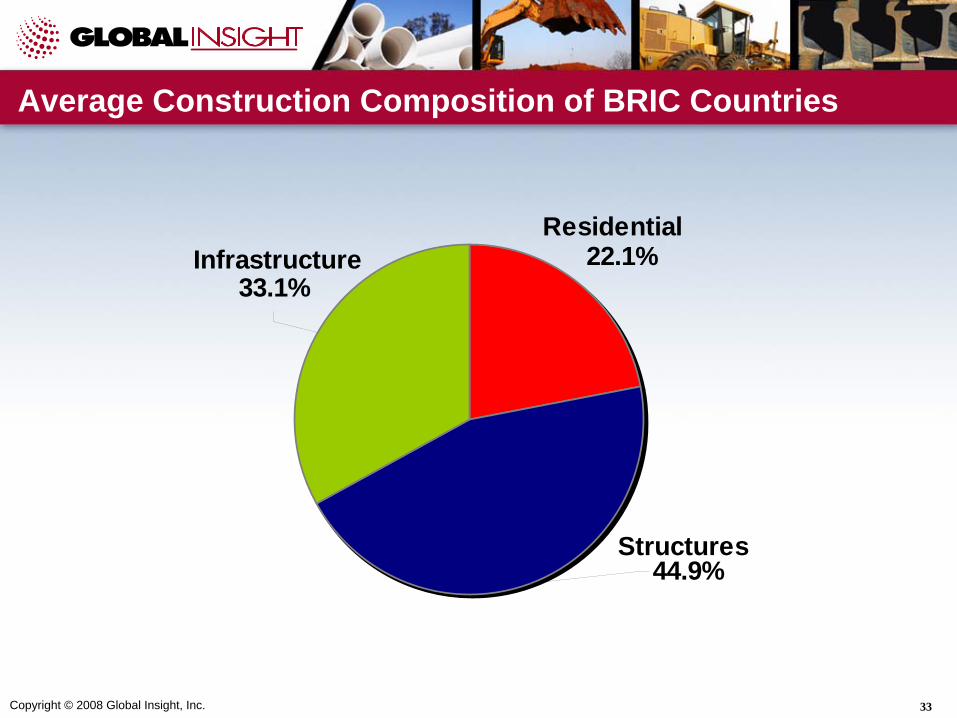

Average Construction Composition of BRIC Countries

22.1%33.1%

44.9%

InfrastructureResidential

Structures

Copyright © 2008 Global Insight, Inc. 34

25%39%

15% 21%

Industrial

Commercial

OfficeInstitutional12%10%

66%

12%

Industrial

Commercial

OfficeInstitutional

10%13%

49%

28%

Industrial

Commercial

OfficeInstitutional

15%44%

25%

16%

Industrial Commercial

Office

Institutional

Composition of Nonresidential Structures

China

India

Brazil

Russia

Copyright © 2008 Global Insight, Inc. 35

Relative Construction Market Size of GCC Countries

Saudi Arabia

55%

Bahrain2%

Qatar4%

United Arab

Emirates31%

Oman2%

Kuwait6%

Copyright © 2008 Global Insight, Inc. 36

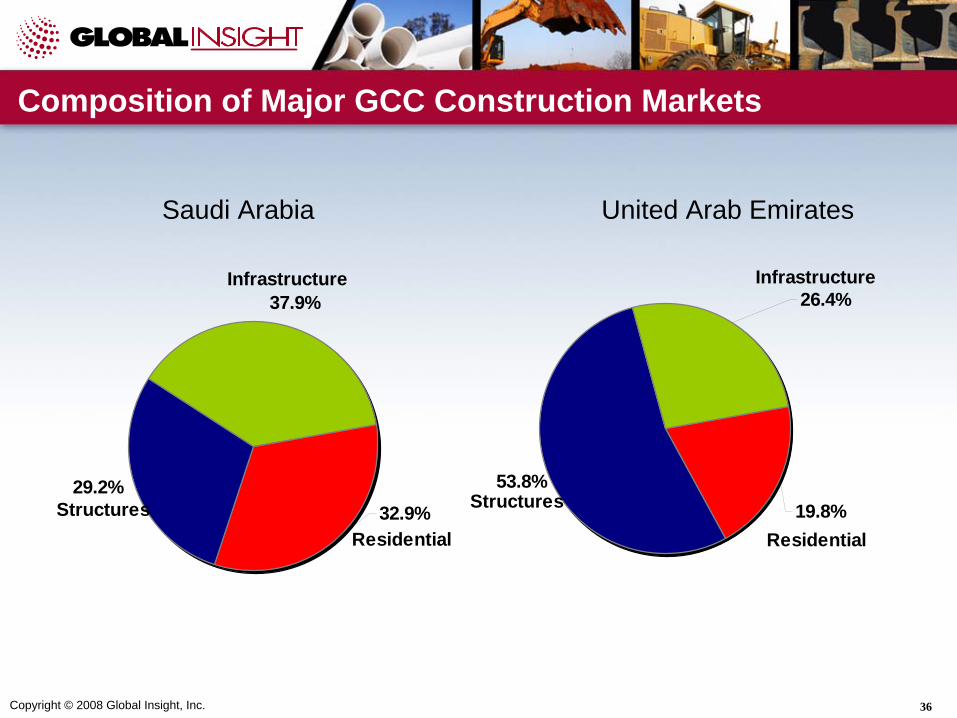

37.9%

32.9%29.2%

Infrastructure

ResidentialStructures

26.4%

53.8%19.8%

Infrastructure

Residential

Structures

Composition of Major GCC Construction Markets

Saudi Arabia United Arab Emirates

Copyright © 2008 Global Insight, Inc. 37

16%

26%

39%

18%

Industrial

Commercial

Office

Institutional

17%

22%

47% 15%

IndustrialCommercial

Office

Institutional

Relative Construction Market Size of GCC Countries

Saudi Arabia United Arab Emirates

Kuwait

16%21%

34%

28%Industrial Commercial

OfficeInstitutional

Copyright © 2008 Global Insight, Inc. 38

Composition of Major GCC Infrastructure Markets

26%

43%

31%Transportation

Energy

Water/Sewer

Saudi Arabia United Arab Emirates

64%

24%12%Transportation

Energy

Water/Sewer

Thank You

Scott HazeltonDirector of Construction Services

E-mail: [email protected]

Presentations are available for download at www.globalinsight.com/events/2008ConstructionChicago