global beer report volume sinks amid economic difficulties ... · volume sinks amid economic...

TRANSCRIPT

Global Beer Report

Volume Sinks Amid Economic Difficulties And Increased Competition From Wine And Spirits THE GLOBAL BEER MARKET DECREASED FOR THE FIRST TIME IN

19 years last year as the worldwide economic crunch took a bite out of sales. Rising taxes and prices, lower consumer confidence, increased competition from wine and spirits, trading down trends and a shift toward the off-premise in mature markets contributed to the global beer market's decline. Growth in China remains strong at 4.6% but slowed from recent years and could not offset declines in mature markets like the U.S., Germany and Japan. The global recession is cutting deep as the worldwide economy and per-capita income (both down about 1%) decreased in 2009 for the first time since World War II. Seven of the top 15 brewers worldwide declined in volume last year. Increases from the other eight brewers offset those losses and the top 15 brewers (accounting for nearly 75% of global beer sales) registered a combined increase of 1.4% to approximately 1.3 billion hectoliters.

Top-ranked Anheuser-Busch InBev (ABI) experienced a 2.6% de-crease to 358.8 million hectoliters. For fiscal 2009, ABI experienced decreases in the U.S. and markets in Central, Eastern and Western Europe and Asia Pacific, while the brewing giant posted strong growth in Brazil. U.K-based SABMiller, ranked second, bucked trends and increased 1% last year to 212.6 million hectoliters. "In a year char-acterized by very difficult trading conditions, the business has deliv-ered another strong performance, capitalizing on our unique port-folios of leading local and international brands," says Meyer Kahn, chairman of SABMiller.

The pace and magnitude of industry acquisitions has slowed slightly from last year's megadeals involving ABI and MillerCoors but major transactions continue to consolidate worldwide brewing operations. Earlier this year, Heineken NV acquired Mexico's FEMSA for $7.6 billion. The deal positions Heineken as a leading brewer in

BEER - TOP 15 BREWERS WORLDWIDE, PRO FORMA' (Millions of Hectoliters)

Percent World Share

Rank Brewer Headquarters 2008 2009 Change2 2008 2009

I Anheuser-Busch InBev 3 Belgium 368.5 358.8 -2.6% 2 1.0% 20.6% 2 SABMiller United Kingdom 210.4 212.6 1.0 12.0 12.2

3 Heineken 4 Netherlands 166.9 165.7 -0.7 9.5 9.5 4 Carlsberg Breweries Denmark 109.3 116.0 6.1 6.2 6.7

5 China Resources Enterprise China 72.6 83.7 15.3 4.1 4.8

Total Top 5 927.6 936.8 1.0 53.0 53.7

6 Tsingtao Brewery Co China 53.8 59.7 11.0 3.1 3.4

7 Grupo Modelo Mexico 52.3 52.5 0.4 3.0 3.0 8 Molson Coors Brewing Co United States 51.5 50.0 -3.0 2.9 2.9

9 Beijing Yanjing Beer Group China 42.2 46.7 10.7 2.4 2.7 10 Kirin Brewery CO 5 Japan 33.3 32.6 -2.0 1.9 1.9

Total Top 10 1,160.7 1,178.3 1.5 66.3 67.6

11 Asahi Breweries 5 Japan 28.5 27.7 -2.8 1.6 1.6 12 Guinness Brewing Worldwide (Diageo) United Kingdom 22.4 22.4 - 1.3 1.3 13 Efes Beverage Group Turkey 22.5 22.1 -1.8 1.3 1.3 14 Kingstar Beer Group China 18.1 19.3 6.5 1.0 1.1

15 San Miguel Brewery Philippines 17.6 17.4 -1.5 1.0 1.0 Total Top 156 1,269.8 1,287.1 1.4% 72.5% 73.8%

Includes agency/license/non-alcoholic brands and equity interests in other brewers. 2 Based on unrounded data. 'Adjusted to exclude Tennent's (C&C), Oriental Brewery (KKR) and central European operations (CVC).

Adjusted to include FEMSA Cerveza, which it acquired in 2010. 'Includes happoshu and zasshu. 6 Addition of columns may not agree due to rounding.

Source: Impact Databank

26 OCTOBER 1, 2010

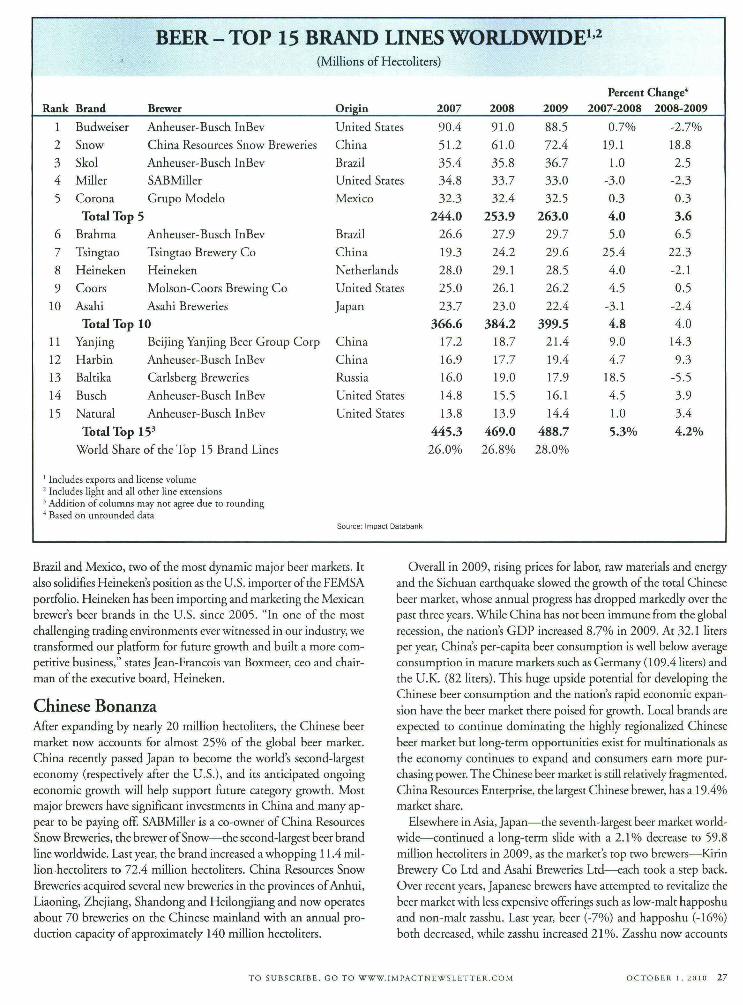

BEER - TOP 15 BRAND LINES WORLDWIDE1 '2

(Millions of Hectoliters)

Percent Change 4 Rank Brand Brewer Origin 2007 2008 2009 2007-2008 2008-2009

1 Budweiser Anheuser-Busch InBev United States 90.4 91.0 88.5 0.7% -2.7% 2 Snow China Resources Snow Breweries China 51.2 61.0 72.4 19.1 18.8

3 Skol Anheuser-Busch InBev Brazil 35.4 35.8 36.7 1.0 2.5 4 Miller SABMiIIer United States 34.8 33.7 33.0 -3.0 -2.3 5 Corona Grupo Modelo Mexico 32.3 32.4 32.5 0.3 0.3

Total Top 5 244.0 253.9 263.0 4.0 3.6

6 Brahma Anheuser-Busch InBev Brazil 26.6 27.9 29.7 5.0 6.5 7 Tsingtao Tsingtao Brewery Co China 19.3 24.2 29.6 25.4 22.3 8 Heineken Heineken Netherlands 28.0 29.1 28.5 4.0 -2.1

9 Coors Molson-Coors Brewing Co United States 25.0 26.1 26.2 4.5 0.5 10 Asahi Asahi Breweries Japan 23.7 23.0 22.4 -3.1 -2.4

Total Top 10 366.6 384.2 399.5 4.8 4.0 11 Yanjing Beijing Yanjing Beer Group Corp China 17.2 18.7 21.4 9.0 14.3 12 Harbin Anheuser-Busch InBev China 16.9 17.7 19.4 4.7 9.3 13 Baltika Carlsberg Breweries Russia 16.0 19.0 17.9 18.5 -5.5 14 Busch Anheuser-Busch InBev United States 14.8 15.5 16.1 4.5 3.9 15 Natural Anheuser-Busch InBev United States 13.8 13.9 14.4 1.0 3.4

Total Top 15 3 445.3 469.0 488.7 5.3% 4.2%

World Share of the Top 15 Brand Lines 26.0% 26.8% 28.0%

Includes exports and license volume 2 Includes light and all other line extensions

Addition of columns may not agree due to rounding Based on unrounded data

Source: Impact Databank

Brazil and Mexico, two of the most dynamic major beer markets. It also solidifies Heineken's position as the U.S. importer of the FEMSA portfolio. Heineken has been importing and marketing the Mexican brewer's beer brands in the U.S. since 2005. "In one of the most challenging trading environments ever witnessed in our industry, we transformed our platform for future growth and built a more com-petitive business," states Jean-Francois van Boxmeer, ceo and chair-man of the executive board, Heineken.

Chinese Bonanza After expanding by nearly 20 million hectoliters, the Chinese beer market now accounts for almost 25% of the global beer market. China recently passed Japan to become the world's second-largest economy (respectively after the U.S.), and its anticipated ongoing economic growth will help support future category growth. Most major brewers have significant investments in China and many ap-pear to be paying off. SABMiller is a co-owner of China Resources Snow Breweries, the brewer of Snow-the second-largest beer brand line worldwide. Last year, the brand increased a whopping 11.4 mil-lion .hectoliters to 72.4 million hectoliters. China Resources Snow Breweries acquired several new breweries in the provinces of Anhui, Liaoning, Zhejiang, Shandong and Heilongjiang and now operates about 70 breweries on the Chinese mainland with an annual pro-duction capacity of approximately 140 million hectoliters.

Overall in 2009, rising prices for labor, raw materials and energy and the Sichuan earthquake slowed the growth of the total Chinese beer market, whose annual progress has dropped markedly over the past three years. While China has not been immune from the global recession, the nation's GDP increased 8.7% in 2009. At 32.1 liters per year, China's per-capita beer consumption is well below average consumption in mature markets such as Germany (109.4 liters) and the U.K. (82 liters). This huge upside potential for developing the Chinese beer consumption and the nation's rapid economic expan-sion have the beer market there poised for growth. Local brands are expected to continue dominating the highly regionalized Chinese beer market but long-term opportunities exist for multinationals as the economy continues to expand and consumers earn more pur-chasing power. The Chinese beer market is still relatively fragmented. China Resources Enterprise, the largest Chinese brewer, has a 19.4% market share.

Elsewhere in Asia, Japan-the seventh-largest beer market world-wide-continued a long-term slide with a 2.1% decrease to 59.8 million hectoliters in 2009, as the market's top two brewers-Kirin Brewery Co Ltd and Asahi Breweries Ltd-each took a step back. Over recent years, Japanese brewers have attempted to revitalize the beer market with less expensive offerings such as low-malt happoshu and non-malt zasshu. Last year, beer (-7%) and happoshu (-16%) both decreased, while zasshu increased 21%. Zasshu now accounts

TO SUBSCRIBE, GO TO WWW.IMPACTNEWSLETTER.COM OCTOBER t, 2010 27

Rank Market 2005

BEER - TOP 10 MARKETS' (Millions of Hectoliters)

Percent Change 2

2006 2007 2008 2009 2005-2006 2006-2007 2007-2008 2008-2009

1 China 309.3 339.0 381.2 413.0 431.9 9.6% 12.4% 8.3% 4.6% 2 United States 235.0 238.0 240.7 241.6 237.1 1.3 1.1 0.4 -1.8 3 Brazil 91.4 95.4 102.2 103.6 104.5 4.4 7.1 1.4 0.8 4 Russia 87.2 96.0 111.0 110.6 99.5 10.1 15.6 -0.4 -10.0 5 Germany 95.1 95.5 91.9 91.1 89.9 0.4 -3.8 -0.8 -1.4

Total Top 5 818.0 863.9 926.9 959.9 962.9 5.6 7.3 3.6 0.3

6 Mexico 57.5 60.7 63.3 64.3 64.7 5.5 4.4 1.6 0.6 7 Japan3 63.3 63.4 62.7 61.1 59.8 0.2 -1.1 -2.5 -2.1 8 United Kingdom 56.4 55.6 53.1 51.5 50.5 -1.5 -4.4 -3.2 -1.9 9 Spain 31.3 32.7 33.2 32.6 32.7 4.3 1.5 -1.8 0.3

10 Poland 30.7 32.8 35.5 35.9 32.3 6.8 8.3 1.1 -10.1 Total Top 101 1,057.2 1,109.0 1,174.7 1,205.3 1,202.9 4.9% 5.9% 2.6% -0.2%

Top 10's World Share 68.0% 68.3% 68.6% 68.8% 69.0%

Excludes non-alcoholic brews. 2 Based on unrounded data.

Includes happoshu and zasshu Addition of columns may not agree due to rounding.

Source: Impact Databank

for about one-third of the Japanese beer market, but its growth was not enough to offset losses among beer and happoshu.

U.S. Beer Blues For the first time in six years, beer volume in the U.S. decreased last year and continued to lose market share to wine and spirits. Under pressure from economic woes, price increases, stiff competition from other beverages and changing consumer preferences, the U.S. beer market declined 1.8% in volume in 2009 to 237.1 million hectoli-ters. The volume difference between the Chinese and the U.S. beer markets grew to nearly 200 million hectoliters last year. Major brew-ers increased average beer prices in the U.S. by 3.7% last year to try and offset increased operating costs due to higher prices for trans-portation, packaging materials such as glass and aluminum and malt. Price increases created downward pressure on volume sales but also led to increased dollar sales (up about 1.8%).

The two top U.S. brewers-ABI and MillerCoors-concentrated on integrating their operations created from megadeals done in 2008. That year, Miller and Coors formed a U.S. joint venture-Miller-Coors-and InBev acquired A-B for $52 billion to create ABI, the world's largest brewer. A major development emerging from these deals was that Coors Light, which was flat last year, passed new sta-blemate Miller Lite (which decreased 5.5%), to become the third-largest beer brand in the U.S. If current trends hold firm, Coors Light will pass Budweiser in the short term to become the second-largest beer brand in the U.S.

Specialty beers (+9.3%) and domestic ice beers (+6.9%) were the only two segments in the U.S. beer market to grow last year. Spe-cialty growth was driven by brands like Blue Moon Belgian White Ale, Fat Tire Amber Ale, Shiner Bock and Sam Adams Octoberfest. Despite the apparent surge in specialty beers, American consumers

are much more price-conscious than they were several years ago. As a sign of the tough economic times, the imported beer segment de-creased for the second consecutive year in the U.S. in 2009 and the rate of erosion accelerated to 5.8% last year from a 3.1% decline in 2008. Import leader Corona Extra has lost volume for three consecu-tive years. Given the U.S. market's conditions, the major brewers are in a cutthroat share battle. ABI upped the ante on the ad front. Hav-ing been the Super Bowl's exclusive alcoholic beverage advertiser for many years, it will also become the official sponsor of the NFL be-ginning in the 2011 season, in a deal estimated at $1.2 billion over six years.

Latin American Growth Of the four top 10 beer markets to post growth in 2009, two of them-Brazil and Mexico-are in Latin America. With 0.8% growth to 104.5 million hectoliters, Brazil eclipsed Russia last year to be-come the world's third-largest beer market. ABI dominates the Bra-zilian beer market, with a near 70% market share. Its Skol and Brahma brands were both on the rise last year. The market contin-ues to be highly competitive and has diverse regional and consump-tion patterns. Other market leaders include Grupo Schincariol (12% market share), Petropolis (9.3%) and Heineken (7.8%), which owns Kaiser through its acquisition of FEMSA. A projected increase in per-capita consumption and population growth are expected to con-tinue to contribute to growth for Brazil's beer market.

The Mexican beer market increased 0.6% to 64.7 million hecto-liters in 2009. Grupo Modelo and FEMSA essentially control the Mexican beer market. In a manner similar to Brazil and China, the growth rate of the Mexican beer market has slowed over the past couple of years. Last year, drug-related violence along the U.S. bor-der and the swine flu scare contributed to reduced growth.

28 OCTOBER 1. 2010

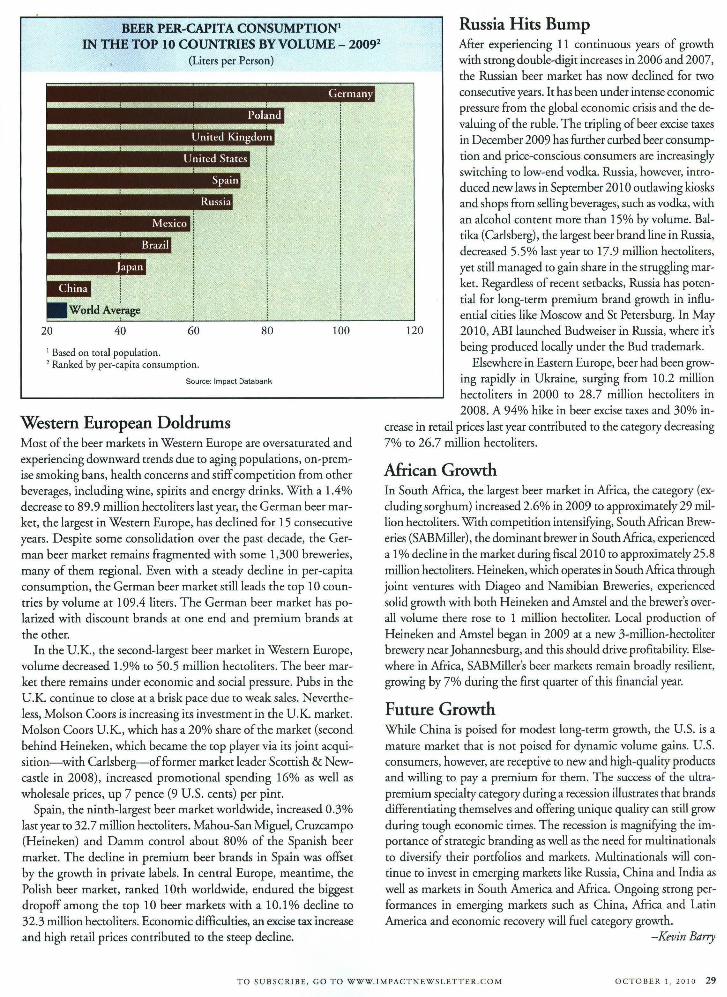

BEER PER-CAPITA CONSUMPTION' IN THE TOP 10 COUNTRIES BY VOLUME - 20092

(Liters per Person)

United I

I States

_iThI

1W1.1d Average

20 40 60 80 100

Based on total population. 2 Ranked by per-capita consumption.

Source: Impact Databank

Western European Doldrums Most of the beer markets in Western Europe are oversaturated and experiencing downward trends due to aging populations, on-prem-ise smoking bans, health concerns and stiff competition from other beverages, including wine, spirits and energy drinks. With a 1.4% decrease to 89.9 million hectoliters last year, the German beer mar-ket, the largest in Western Europe, has declined for 15 consecutive years. Despite some consolidation over the past decade, the Ger-man beer market remains fragmented with some 1,300 breweries, many of them regional. Even with a steady decline in per-capita consumption, the German beer market still leads the top 10 coun-tries by volume at 109.4 liters. The German beer market has po-larized with discount brands at one end and premium brands at the other.

In the U.K., the second-largest beer market in Western Europe, volume decreased 1.9% to 50.5 million hectoliters. The beer mar-ket there remains under economic and social pressure. Pubs in the U.K. continue to close at a brisk pace due to weak sales. Neverthe-less, Molson Coors is increasing its investment in the U.K. market. Molson Coors U.K., which has a 20% share of the market (second behind Heineken, which became the top player via its joint acqui-sition—with Carlsberg—of former market leader Scottish & New-castle in 2008), increased promotional spending 16% as well as wholesale prices, up 7 pence (9 U.S. cents) per pint.

Spain, the ninth-largest beer market worldwide, increased 0.3% last year to 32.7 million hectoliters. Mahou-San Miguel, Cruzcampo (Heineken) and Damm control about 80% of the Spanish beer market. The decline in premium beer brands in Spain was offset by the growth in private labels. In central Europe, meantime, the Polish beer market, ranked 10th worldwide, endured the biggest dropoff among the top 10 beer markets with a 10.1% decline to 32.3 million hectoliters. Economic difficulties, an excise tax increase and high retail prices contributed to the steep decline.

Russia Hits Bump After experiencing 11 continuous years of growth with strong double-digit increases in 2006 and 2007, the Russian beer market has now declined for two consecutive years. It has been under intense economic pressure from the global economic crisis and the de-valuing of the ruble. The tripling of beer excise taxes in December 2009 has further curbed beer consump-tion and price-conscious consumers are increasingly switching to low-end vodka. Russia, however, intro-duced new laws in September 2010 outlawing kiosks and shops from selling beverages, such as vodka, with an alcohol content more than 15% by volume. Bal-tika (Carlsberg), the largest beer brand line in Russia, decreased 5.5% last year to 17.9 million hectoliters, yet still managed to gain share in the struggling mar-ket. Regardless of recent setbacks, Russia has poten-tial for long-term premium brand growth in influ-ential cities like Moscow and St Petersburg. In May

120 2010, ABI launched Budweiser in Russia, where it's being produced locally under the Bud trademark.

Elsewhere in Eastern Europe, beer had been grow-ing rapidly in Ukraine, surging from 10.2 million hectoliters in 2000 to 28.7 million hectoliters in 2008. A 94% hike in beer excise taxes and 30% in-

crease in retail prices last year contributed to the category decreasing 7% to 26.7 million hectoliters.

African Growth In South Africa, the largest beer market in Africa, the category (ex-cluding sorghum) increased 2.6% in 2009 to approximately 29 mil-lion hectoliters. With competition intensifying, South African Brew-eries (SABMiller), the dominant brewer in South Africa, experienced a 1% decline in the market during fiscal 2010 to approximately 25.8 million hectoliters. Heineken, which operates in South Africa through joint ventures with Diageo and Namibian Breweries, experienced solid growth with both Heineken and Amstel and the brewer's over-all volume there rose to 1 million hectoliter. Local production of Heineken and Amstel began in 2009 at a new 3-million-hectoliter brewery near Johannesburg, and this should drive profitability. Else-where in Africa, SABMiIIer's beer markets remain broadly resilient, growing by 7% during the first quarter of this financial year.

Future Growth While China is poised for modest long-term growth, the U.S. is a mature market that is not poised for dynamic volume gains. U.S. consumers, however, are receptive to new and high-quality products and willing to pay a premium for them. The success of the ultra-premium specialty category during a recession illustrates that brands differentiating themselves and offering unique quality can still grow during tough economic times. The recession is magnifying the im-portance of strategic branding as well as the need for multinationals to diversify their portfolios and markets. Multinationals will con-tinue to invest in emerging markets like Russia, China and India as well as markets in South America and Africa. Ongoing strong per -formances in emerging markets such as China, Africa and Latin America and economic recovery will fuel category growth.

—Kevin Barry

TO SUBSCRIBE, GO TO WWW.IMPACTNEWSLETTER.COM OCTOBER 1, 2010 29