global asset and auto finance survey may 2015

TRANSCRIPT

Global Asset & Auto Finance SurveyMAY 2015

ASSET FINANCE INTERNATIONAL IN ASSOCIATION WITH WHITE CLARKE GROUP

GLOBAL ASSET AND AUTO FINANCE SURVEY MAY 2015

White Clarke Group

White Clarke Group is the market leader in software solutions and business consultancy to the automotive and asset finance sector for retail, fleet and wholesale. White Clarke Group solutions enable end-to-end credit processing and administration to streamline business practice, cut operational cost and deliver outstanding customer service. White Clarke Group has a 23 year track record of leadership and innovation in finance technology, consultancy and new market entry. Clients value White Clarke Group's industry knowledge, market intelligence and innovation. The company employs some 600 finance and technology professionals, with offices in the UK, USA, Canada, China, Australia, Austria and Germany.

Acknowledgements

Jonathan Andrew, global CEO, commercial finance business, Siemens Financial ServicesJohn Bills, director, Australian Equipment Leasing Association (AELA)Philippe Bismut, CEO of ArvalNidhi Bothra, Vinod Kothari ConsultantsJurgita Bucyte, Leaseurope adviser in statistics and economic affairs Rafael Castillo-Triana, CEO of The Alta Group Latin American RegionBill Choi, vice president of research and industry services, US Equipment Leasing and Finance Association (ELFA)Carl Chrappa, senior managing director/asset management practice leader of the Independent Equipment CompanyRichard Cordray, director Consumer Financial Protection Bureau Felix Daniliuc, President of ALBWilliam Douglass, group head and managing director, CIT corporate finance, healthcarePaul Errington, CEO, Connaught Finance InvestmentsRich Green, President of CIT International FinanceGeraldine Kilkelly, FLA head of research and chief economistGeorge Lagos, senior general manager of Canon Finance AustraliaHugh Lander, CEO, BOQ Finance, Bank of QueenslandKai Ostermann, CEO of Deutsche Leasing GroupJeff Schuster, senior vice president of forecasting, LMC AutomotiveWilliam Sutton, president and CEO, US Equipment Leasing and Finance Association (ELFA)Hugh Swandel , managing director of The Alta Group in CanadaMelinda Zabritski, senior director at Experian Automotive http://www.whiteclarkegroup.com/http://www.assetfinanceinternational.com

Publisher: Edward Peck Editor: Brian Rogerson Author: Pat Sweet Asset Finance International Ltd.

39 Manor Way,London SE3 9XGUNITED KINGDOMTelephone: +44 (0) 207 617 7830

© Asset Finance International, 2015, All rights reserved No part of this publication may be reproduced or used in any form or by any means – graphic; electronic; or mechanical, including photocopying, recording, taping or information storage and retrieval systems – without the written permission from the publishers.

GLOBAL ASSET AND AUTO FINANCE SURVEY MAY 2015

Contents

Introduction 4

NORTH AMERICA 6

What’s happened since the financial crisis? 6What are the challenges? 8What does the future hold? 12Rules and regulations 13

EUROPE 20

What’s happened since the financial crisis? 20What are the challenges? 22What does the future hold? 23Rules and regulations 25

ASIA PACIFIC 28

What’s happened since the financial crisis? 28What are the challenges? 31What does the future hold? 32Rules and regulation 36

SOUTH AMERICA 41

What’s happened since the financial crisis? 41What are the challenges? 42What does the future hold? 43Rules and regulations 45

Conclusion 47

GLOBAL ASSET AND AUTO FINANCE SURVEY MAY 2015

4 © A

sset

Fin

ance

Int

erna

tion

al, a

ll r

ight

s re

serv

ed.

Introduction

The outlook for the asset and auto finance industry worldwide brightened in the immediate aftermath of the first Global Asset and Auto Finance Survey in 2013, when key players in North America, Europe, Asia Pacific and South America regions were all reporting only limited growth as most were still struggling to deal with the fall-out from the financial crisis.

Updates during 2014 suggested real improvements were on their way, starting in the US where leasing business volumes showed signs of reaching new highs. Business volume was also on the increase in Europe, admittedly from low levels in those countries which have been worse affected by the Eurozone crisis, although the situation was more mixed in the Asia Pacific markets. There, changes in government in Australia coupled with an economic revival based on a residential property boom have had a dampening effect on the traditional mining services and manufacturing asset finance sectors, but the Chinese market had started to expand markedly, and new markets were starting to open up across south east Asia.

Lenders and the commercial organisations they support have come to see the corporate belt tightening forced on them as a result of the shortage of available credit as a virtue, rather than a limitation. Austerity has brought with it a focus on value for money which, in the immediate short term, translates into opportunities to offer funding for replacement equipment now reaching capacity.

Longer term, contributors to the report indicate finance companies are starting to develop innovative approaches to help companies unlock capital tied up in plant and equipment so it can be used for investment.

Indeed, over the last three or four years, asset based finance of all kinds has had the opportunity to demonstrate both its resilience and the role

GLOBAL ASSET ANDAUTO FINANCE SURVEY

Introduction

The equipment and automotive leasing industry around the globe has beennavigating a path through some choppy waters in the aftermath of thefinancial crisis of 2008. After the tidal wave of problems which submergedthe industry in 2009 and 2010, the sector started to right itself in 2011 andhas since been on course for calmer waters, with new business volumesbuilding and revenues starting to grow in many countries.

Indeed, over the last three or four years, asset based finance of all kinds hashad the opportunity to demonstrate both its resilience and the role it can playwhen credit, generally, is in short supply. In response, the industry has donemuch to get itself ship shape, with leaner finance providers emerging whomake greater use of technology to tighten underwriting approaches, introduceefficiencies across a range of back office processes and improve customerservice.

However, the leasing industry’s fortunes are inextricably linked to those of theeconomies of the countries in which finance providers operate, and there isstill considerable instability and nervousness about economic prospectsglobally.

While mature markets in North America and Europe have started to moveback towards pre-recession levels of activity, growth in asset finance remainsmuted as many companies and individuals continue to prove reluctant toinvest. Leasing here has been characterized by replacement cycles, ratherthan by a surge in new investment.

© A

sset

Fin

ance

Int

erna

tion

al, A

ll r

ight

s re

serv

ed.

4

Written by Dara Clarke and Ed White,founders of White Clarke Group

GLOBAL ASSET AND AUTO FINANCE SURVEY MAY 2015

5 © A

sset

Fin

ance

Int

erna

tion

al, a

ll r

ight

s re

serv

ed.

it can play when credit, generally, is in short supply. In response, the industry has done much to get itself ship shape, with leaner finance providers emerging who make greater use of technology to tighten underwriting approaches, introduce efficiencies across a range of back office processes and improve customer service.

However, the leasing industry’s fortunes are inextricably linked to those of the economies of the countries in which finance providers operate. Looking ahead to 2015, while prospects now appear considerably better than they did in the darkest days of the Great Recession, they are not currently shining quite as brightly as some may have hoped.

Political worries and economic uncertainties have re-surfaced, resulting in some investment decisions being delayed, while poor weather in the first three months resulted in a slow down in production and product delivery in some of the key markets for asset finance.

In the Asia Pacific and South America regions leasing is a less mature form of finance. A year ago, it looked as if the opportunities for growth in the leasing market were also strong here, and certainly major finance providers, seeing the slow pace of pick-up in their long standing areas of activity, started to look closely at both areas as a potential source of new business.

However, these countries bring their own challenges. Cultural differences, difficulties in establishing due diligence and the widely differing political regimes can all prove barriers to entry for finance providers keen to investigate new markets, while local players sometimes struggle to find ways to illustrate the benefits of leasing in markets dominated by other forms of finance provision. Brazil, once viewed as the powerhouse of South America, has seen its leasing market decline very markedly, while the economic slowdown in China is also having an impact on the leasing industry there.

Around the world, regulation and new legislation remain a concern, particularly in North America and Europe, where many jurisdictions in these two regions have sought to address what were widely perceived as the financial excesses of the pre-crisis years with stringent new regulations on tax and on the use of capital.

The beginning of 2015 marked yet another update on the latest round of deliberations on new international accounting rules on leasing which are likely to see most leases brought onto company balance sheets in the longer term. With the two main standards-setting boards indicating that there is still some distance between their views on the most appropriate model for achieving this, there remains considerable uncertainty in the short term as to how the proposed “two model” approach will work in practice, but both regulators have committed to producing a standard by the end of this year. Many companies will be fearful that a complex and costly compliance burden may jeopardise future prospects, while changes to the tax regime for leasing may serve to undermine its appeal.

Worldwide, the biggest issue now for many in the asset finance industry is find ways to navigate the regulatory uncertainties, keep tight control on costs, and push forward with innovations. But while lessors have got their own house in order, they are now operating in a business climate dominated by issues over which they have no control: a predicted rise in US interest rates; electoral uncertainty in the UK; a potential Greek exit from the Eurozone; and militant terrorist action in the Middle East and Russia are all factors which are combining to build a sense of unease which is proving a drag on investment.

GLOBAL ASSET AND AUTO FINANCE SURVEY MAY 2015

6 © A

sset

Fin

ance

Int

erna

tion

al, a

ll r

ight

s re

serv

ed.

NORTH AMERICA

What’s happened since the financial crisis?

The US leasing market was hit by a perfect storm during the financial turmoil which followed the collapse of Lehman Brothers in 2008. Accessing capital markets for debt became increasingly difficult and the finance that was accessible came at significantly higher rates than before. Customers’ businesses were adversely impacted by the crisis, so that they found it difficult to make payments and attempted to delay payments as well, leading to significantly higher delinquency and potential write-offs, especially in the automotive leasing arena. At the same time, leasing volumes declined substantially as customers postponed equipment acquisition.

Bill Choi, vice president of research and industry services for the US Equipment Leasing and Finance Association (ELFA), highlights that the fallout from the banking crisis was not immediate, with the market dropping by around 5% to 6% in 2008, but when the downturn did arrive it was very steep. His estimate suggests the leasing market there then fell by 30% in 2009 alone.

Bill Choi, ELFA vice president, research and industry services

GLOBAL ASSET AND AUTO FINANCE SURVEY MAY 2015

7 © A

sset

Fin

ance

Int

erna

tion

al, a

ll r

ight

s re

serv

ed.

The situation was even more stark in the wider North America region, with the leasing market in Canada undergoing a major reversal due in part to the particularities of how the different categories of lenders operated in that country.

Hugh Swandel is managing director of The Alta Group in Canada and a board director of the Canadian Finance & Leasing Association (CLFA). He reported the financial crisis had a significant impact on both equipment and automotive leasing activity in the country.

“The global financial crisis caused major paradigm shifts in Canadian auto financing. In Canada, banks are not permitted to provide vehicle leasing to consumers, so at the time of the crisis captive lessors controlled a large share of the Canadian auto financing market and their inability to access securitization markets caused a rapid decline in the leasing share of the market,” Swandel explained.

Moving up

Since then, developments have been on a much more positive upwards trend. The Equipment Leasing and Finance Association(ELFA) annual survey of equipment finance activity (SEFA) reported a 16.5% increase in new business volume in 2011, with a similar rate of growth (16.4%) in 2012. This contrasts with an increase of just 3.9% reported for 2010 and the 30.3% decline in 2009.

Source: ELFA 2014 Survey of Equipment Finance Activity

However, ELFA’s latest SEFA report shows that, while the industry is performing well, the rate of growth eased as the year went on, with new business volume growing 9.3% in in 2013. ELFA’s data indicates that after lagging for several years, independent equipment finance organizations led the industry in new business volume growth rates. Independents saw the strongest increase in new business volume (17.7%) over the year, while captives saw their volume grow by 11.3% and banks posted a 6.2% increase. The top-five most-financed equipment types were transportation, computer equipment, agricultural, construction and medical equipment.

A companion report from the association focused on small-ticket and micro-ticket equipment transactions among the SEFA respondents and found that new business volume in this market sector grew by 10.2% in 2013. Indeed, small businesses seem to have become the strongest growing segment of the lending market.

GLOBAL ASSET AND AUTO FINANCE SURVEY MAY 2015

8 © A

sset

Fin

ance

Int

erna

tion

al, a

ll r

ight

s re

serv

ed.

The Thomson Reuters/PayNet Small Business Lending Index hit a record high at the end of 2014, with a December reading of 133.5, the highest since the index’s launch in January 2005. That fell back to 120.9 in the early months of 2015, but with the index up 5% PayNet’s president, William Phelan, said the US economy is “still on track with continued expansion.”

“We’re finally seeing what looks to be a period of sustained growth and expansion in the economy – and this is good news for the equipment finance industry,” Phelan said. “We track the small business sector as a leading economic indicator. When a small business owner invests to expand or replace worn out equipment, he/she does so based on current and anticipated growth in demand for goods and services, which is what we are seeing now, and this is causing business owners to

increase capacity to some level. We are seeing consistent single-digit growth, which leads us to conclude that there is demand to replace worn out equipment and purchase new equipment.”

At the same time, 30-day delinquency rates are well below the highs seen in 2005 and 2006, leading to much improved credit conditions for small businesses, who now have the financial capacity to take on more debt and expand their operations. In doing so, they will fuel more growth, and be looking to make more equipment acquisitions. The equipment finance industry’s ability to offer and complete loans very quickly compared to other forms of finance is a significant advantage in this market.

What are the challenges?

The worst effects of the financial crisis may be well behind as the US economy is starting to steady but the North America leasing market is by no means completely out of the woods.

Back in 2011 and 2012, the main issue for leasing companies was the lack of new business, because companies were not expanding and so not buying new equipment. Most of the business that did come in was the result of companies replacing old or worn out equipment, although typically organisations held off for as long as possible before making any purchasing decision.

While the situation remained broadly the same in 2013, by 2014 it looked as if new business might be about to take off. In April, the Equipment Leasing and Finance Foundation’s (ELFF’s) Monthly Confidence Index (MCI-EFI) stood at 65.1, recording the highest index level in two years for the second consecutive month. However, by August the MCI-EFI had dipped to 58.9, easing from the previous two months’ indexes of 61.4, which were themselves below the April high.

There were fears that the drop might signal a long term trend. These seem misplaced at the start of 2015, when the previous summer’s slump was a distant memory. In March 2015, the MCI-EFI recorded its highest level in four years, at 72.1, an increase from the February index of 66.3

William Phelan, president of PayNet

GLOBAL ASSET AND AUTO FINANCE SURVEY MAY 2015

9 © A

sset

Fin

ance

Int

erna

tion

al, a

ll r

ight

s re

serv

ed.

Separately ELFA’s Monthly Leasing and Finance Index (MLFI-25) reports economic activity from 25 companies representing a cross section of the equipment finance sector. Midway through 2014 this showed their overall new business volume for July was $7.8 billion, up 8% from new business volume in July 2013. However, month over month, new business volume was down 13% from June. Year to date, cumulative new business volume increased 4% compared to 2013.

By early 2015, all the signs are that performance is starting to pick up. Latest figures from ELFA indicate a strong start in the first quarter of the year for many lenders, with business volumes 25% higher in March than they were twelve months ago, and prospects looking good for the immediate future.

The MLFI-25 shows overall new business volume for March was $8.9 billion. Volume was up 46% from $6.1 billion in February, while year to date, cumulative new business volume has increased 17% compared to 2014.

The data suggests that receivables over 30 days are creeping up a little and are now standing at 1.2%, up from 1.1% the previous month and from 1% the same period in 2014. Charge-offs were at an all-time low of 0.2% for the 13th consecutive month.

ELFA president and CEO William G. Sutton, said: ‘The March new business volume is indicative of strong capital spending, influenced by businesses taking advantage of continued low interest rates, perhaps in anticipation of reported tightening of monetary policy by the Fed. Credit quality metrics are mixed, with delinquencies edging upward counterbalanced by monthly losses remaining at historic lows.’

Separately, the ELFA’s Monthly Confidence Index (MCI-EFI) for April remained higher than throughout the whole of 2014, now standing at 70.7. However, this marks an easing from the March index of 72.1, which was the highest level in four years, suggesting that while prospects look good, lenders have their doubts.

Sutton went on to issue this caution: “The wild card, of course, is US monetary policy, with the Fed poised to raise interest rates in the not-too-distant future. While higher interest rates typically favor the fixed-rate structure of most equipment finance transactions, it remains to be seen if volume growth can be sustained going forward.”

GLOBAL ASSET AND AUTO FINANCE SURVEY MAY 2015

10 © A

sset

Fin

ance

Int

erna

tion

al, a

ll r

ight

s re

serv

ed.

Auto finance drives growth

A significant element of the growth in the leasing market is coming from the auto finance sector. As the US economy starts to strengthen and the jobs market picks up, so has country’s appetite for buying cars. New-vehicle retail and total sales in February 2015 reached their highest levels for the month since 2002, according to a monthly sales forecast developed jointly by J.D. Power and LMC Automotive. The retail seasonally adjusted annualized selling rate (SAAR) in February is 13.5 million units, 1.1 million units stronger than February 2014 and the highest retail SAAR for the month since February 2004 (13.6 million).

Source: J.D. Power and LMC Automotive

“Strength at the start of 2015 is a key factor in keeping the industry on target to surpass annual vehicle sales of 17 million units for the first time since 2001,” said Jeff Schuster, senior vice president of forecasting at LMC Automotive. “Given all the positive factors, including the economy, gas prices and fresh new products in showrooms, rain clouds are expected to stay out of the auto sales forecast for the duration of 2015.”

More sales overall is translating into greater demand for finance products, with the J. D Power figures showing lease penetration at 27.4% of retail, its highest level ever.

Melinda Zabritski, senior director at Experian Automotive, which surveys the auto lending market regularly, agrees: “From the latest data, we see that leasing remains very dominant in the marketplace. It accounts for 14% of all transactions, both new and used, and has been following an upward trend over several years.”

“A quarter (25%) of all new auto purchases are via a lease, which means one in four new vehicles, and approximately 30% of all finance transactions are leases,” Zabritski said.

After the years of austerity, booming car sales looks like a welcome development, but some commentators have started to suggest that it may bring with it the return of some very unwelcome trends.

Melinda Zabritski, senior director, Experian Automotive

GLOBAL ASSET AND AUTO FINANCE SURVEY MAY 2015

11 © A

sset

Fin

ance

Int

erna

tion

al, a

ll r

ight

s re

serv

ed.

Pre-2008, the auto lending market saw a loosening of underwriting controls which led to an increase in sub-prime loans to consumers with poor credit ratings, who were in trouble as soon as the recession started to bite. In 2015, there are some signs that the sub-prime lending sector is back on the boil.

Sub-prime worries

The Center for Responsible Lending (CRL), a not-for-profit organisation which looks at household finances, released a report in January 2015 called “Reckless Driving”: Implications of Recent Subprime Auto Finance Growth. This points out that in Q3 2014, nearly 39% of open auto loans worth $337 billion were for customers with below-prime credit. That marks an increase from $304 billion owing in the sub-prime category in 2013 and just $255 billion in 2012.

This trend has also been observed by the Federal Reserve, which stated: “The dollar value of originations to people with credit scores below 660 has roughly doubled since 2009, while originations for the other credit score groups increased by only about half.”

The Federal Reserve’s data suggests that in tandem with an increase in the number of auto loans made to borrowers with poor credit histories, more individuals are having problems with auto loans, pointing to a rise in the delinquency rate in late 2014 to 3.5%, from 3.1% in the previous quarter.

In addition, there is also a trend towards longer loans, which has been highlighted by the Office of the Comptroller of the Currency (OCC). Its research suggests lenders are now extending repayment periods up to 84 months on new and used vehicles, compared with the 60 months seen traditionally. The OCC calculates that in the past two years, the share of 73-month to 84-month loans for new cars has doubled as a percentage of the total market, from 12% to 24%. The share of long-term loans for used vehicles also doubled from 7% to 14%.

Data like this indicates growing worries that lenders are, once again, starting to flex underwriting rules in pursuit of bigger market share. However, Zabritski says that such concerns are, for the moment, likely to prove misplaced.

“Whenever there is an uptick in the number of loans to sub-prime and deep sub-prime customers, there is the potential for a ‘sky is falling’ type of reaction,” Zabritski said. “The reality is we are looking at a remarkably stable automotive loan market, in part because consumers are continuing to stay on top of their payments.”

The average credit score for leasing dipped a little in the first quarter of 2015, down from 719 to 717, but 75% of leasing occurs in either the prime or super-prime segment. The Experian figures also challenge the view that the length of the lease is going up. Two thirds of leases are in the 25 months to 36 months category, with 35 months the overall average, while a quarter run for between 37 months and 48 months. The proportion of leases longer than that is extremely small.

“There has been growth across all the risk ranges as the volume of loans increases, but it is important to note that the distribution of loans is stable,” says Zabritski. “In fact, comparing Q4 2013 to this year, there has been no change in the proportion of loans in the deep sub-prime category, which stands at 3.75%, and sub-prime has actually dropped a little. The largest volume gain is in super-prime.”

GLOBAL ASSET AND AUTO FINANCE SURVEY MAY 2015

12 © A

sset

Fin

ance

Int

erna

tion

al, a

ll r

ight

s re

serv

ed.

Moreover, the push towards securing a bigger share of the prime lending market is down to the fact that this represents the biggest area of opportunity, rather than a flight from the more problematic sub-prime segment. Indeed, so far there is little reason according to Experian to think this sector is proving particularly risky.

“The percentage of loans running at 30-day delinquencies is at 2.62% for the market as a whole, which suggests a pretty strong payment performance. And if we look at 60-day delinquencies, again the year-on-year change is very small – in fact, those are down one point at 0.72%. There’s no increase in delinquencies in the sub-prime range compared with last year,” Zabritski explained.

In contrast to those who fear that these increases mean the auto lending market is veering out of control, Zabritski is firm in her view that the stable rate of delinquencies as a percentage of the total lending is a strong indicator that lenders have not taken their foot off the brake. Delinquency balances as an overall financial total are up purely because US car sales are also on the up. However, there are those who argue that it would only take a small change in economic circumstances for delinquencies to creep up, and with them the risks to the auto lending sector.

What does the future hold?

Back in mid 2013, Choi described the views of the ELFA as “very cautiously optimistic”, putting growth at around 5% going forward, although he said the challenges of an uncertain recovery in the global economy made predictions for growth over the next year or two hard to quantify.

Since then, prospects for the leasing industry have improved markedly. The most recent research publication from the Equipment Leasing and Finance Foundation (ELFF), its Equipment & Software Investment Outlook, concludes: “The equipment finance industry started 2015 on solid footing, and industry confidence is at a multi-year high. Improved business confidence and a healing labor market are the principle bases for industry growth in 2015. Oil prices, capacity utilization, and Fed interest-rate policy are key developments to watch this year.”

The ELFF estimated growth in investment in equipment and software would rise 4.2% in 2014. Overall growth in 2014 was 5.8%, and the ELFF says it expects slightly slower growth of 5% in 2015, down from 6% growth forecast in its 2015 Annual Outlook released in December 2014.

The data shows equipment and software investment was subdued in Q4 2014, after two quarters of strong performance. Growth slowed from 10.5% in Q3 to just 1.6%. Even with a slightly slower expected pace of growth in 2015, ELFF’s report forecasts businesses will be encouraged to increase their capital spending with the overall economic expansion.

The Foundation notes that positive drivers of business investment include healthy credit markets, robust job growth, and improving business and consumer confidence, while investment headwinds include a strong dollar, with the risk that poses to exports, and low oil prices, which are likely to see reduced investment in the energy industry.

The 2015 “What’s Hot/What’s Not” Equipment Leasing Trends survey, prepared for ELFA, indicates that, for the second year in a row, construction equipment is the area where lessors are expecting the

GLOBAL ASSET AND AUTO FINANCE SURVEY MAY 2015

13 © A

sset

Fin

ance

Int

erna

tion

al, a

ll r

ight

s re

serv

ed.

biggest level of investment to occur and this market also takes first place in residual value increase. As the health of the US economy improves, so does demand for construction services

The report suggests that the trucks and trailers market will also prove strong. New truck sales increased by 19% in 2014, and new trailer orders by 50%, and sales of used vehicles in this sector are good with high resale values. Similarly, prospects for the rail sector are largely positive, along with those for the machine tools sector, where the secondary market remains buoyant.

The picture in the medical equipment market is more mixed. This industry has traditionally had a preference for leased equipment, partly as a result of the pace of technological change, but uncertainties over the impact of the new Affordable Care Act saw demand dampen for a while. After eight years tipped as the top area for investment in the ELFA study, this sector dropped to fifth place for 2015.

However, a recent survey of the sector by CIT’s corporate finance, healthcare division in early 2015 found healthcare executives are positive on the major financial metrics for 2015, including revenue, price growth and volume growth, believing that all three are likely to increase relative to the previous year. Very few expect a decrease.

Getting on for half (44%) expect their company to seek financing in the coming year, based on requirements for new hires, information technology, and construction or renovation.

William Douglass, group head and managing director of CIT corporate finance, healthcare, said: “Executives are optimistic, and while they continue to confront new challenges, they believe 2015 will be a year for growth.”

However, all lenders are only too well aware that events may move out of their control. ELFA’s 2015 survey found that the oil, gas and energy sector, which had been named as the second most likely area for major investment the previous year, had plummeted to 13th place. This decline in opportunities in the sector was a reflection of the worldwide plunge in oil prices, which has negatively affected the values of oil and gas production and hit demand for exploration equipment.

Carl Chrappa, senior managing director/asset management practice leader of the Independent Equipment Company, an Alta Group company, and the report’s author, summed up the main challenge for the equipment finance industry in 2015: “Overall, it is clear from the comments received that the biggest threat to the secondary market this year appears to come mainly from the health of the global and domestic economies.”

Rules and regulations

Patchy and volatile growth rates are only one of the challenges facing the North American leasing market. The US has taken the lead, along with several other countries around the world, in tightening up on regulation as a response to the problems uncovered when it was discovered just how poor risk management had been in some sectors of the finance industry.

Leasing companies, which have already had to cope with a raft of new rules and regulations, might have hoped that the tide had turned. Over the past few years, bank-owned lessors in particular have had to come

GLOBAL ASSET AND AUTO FINANCE SURVEY MAY 2015

14 © A

sset

Fin

ance

Int

erna

tion

al, a

ll r

ight

s re

serv

ed.

to terms with new requirements for the financial services sector at a global level, such as the changes in banking liquidity rules ushered in with Basel III. This global voluntary regulatory standard on bank capital bank adequacy means that the larger US banks, including those with significant market share in the auto and asset finance space, may be required to hold up to three times as much high quality capital as before.

Consumer Financial Protection Bureau bares its teeth

Closer to home the US auto finance industry has to assimilate and respond to a barrage of new home-grown regulatory requirements including the Truth-in-Lending Act, the Equal Credit Opportunity Act and the Fair Credit Reporting Act. However, by far the greatest cause of concern for lenders and dealers alike in this section of the leasing industry lies in meeting the requirements of the Consumer Financial Protection Bureau (CFPB).

Created as a result of changes to the financial services sector brought in under the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010, the CFPB is the first US federal agency dedicated to protecting consumers in the marketplace for financial products and services. Noncompliance with CFPB rules can result in millions of dollars in fines and penalties and even lawsuits.

Since its inception most of the focus of CFPB’s work has been on the mortgage market, and on loans to students, vulnerable older citizens and service veterans. However, the bureau has always made clear that combating discrimination in all areas of lending is high on the its agenda, and that this embraces any unequal treatment in financial affairs based on characteristics such as race or gender, and also on factors such as credit history or credit rating.

At the end of 2013, the CFPB ordered Ally Financial to pay $98 million to resolve claims that it charged approximately 235,000 minority car buyers higher interest rates than non-Hispanic white borrowers. The lender was also required to pay $18 million in penalties.

In this case the CFPB and the US Department of Justice examined some 800,000 auto loans originated from April 2011 to March 2012, with the analysis suggesting, according to the CFPB, that minority customers paid an additional $200 to $300 over the life of the average loan.

In a statement released in December 2013, Ally said it “does not engage in or condone violations of law or discriminatory practices,” and that based on its own analysis, Ally “does not believe that there is measurable discrimination by auto dealers.” In a further twist to the case, the CFPB said it was not accusing Ally of intentionally discriminating, noting that “Whether or not Ally consciously intended to discriminate makes no practical difference. In fact, we do not allege that Ally did so.”

The CFPB has since shown no let-up in its investigations into alleged discrimination, stating in a recent report it had reached confidential agreements with several other lenders to provide a total of $56 million in refunds for alleged discriminatory practices.

In 2014, the agency signalled its intention to turn up the heat on the auto loans sector. In August 2014 the CFPB fined Texas-based First Investors Financial Services Group $2.75m after concluding the auto

GLOBAL ASSET AND AUTO FINANCE SURVEY MAY 2015

15 © A

sset

Fin

ance

Int

erna

tion

al, a

ll r

ight

s re

serv

ed.

finance company had knowingly provided inaccurate information to credit reporting agencies, potentially harming the credit ratings of tens of thousands of vulnerable consumers.

The company lends primarily to sub-prime borrowers, including those who have gone through bankruptcy, both directly and via auto dealers. A CFPB investigation found it had first identified flaws in the third party computer system used to record customer details in 2011. While First Investors advised the unnamed software vendor about the problems, the company did not replace the system or take any steps to correct the inaccurate information it had supplied to Experian, TransUnion, and other credit rating agencies.

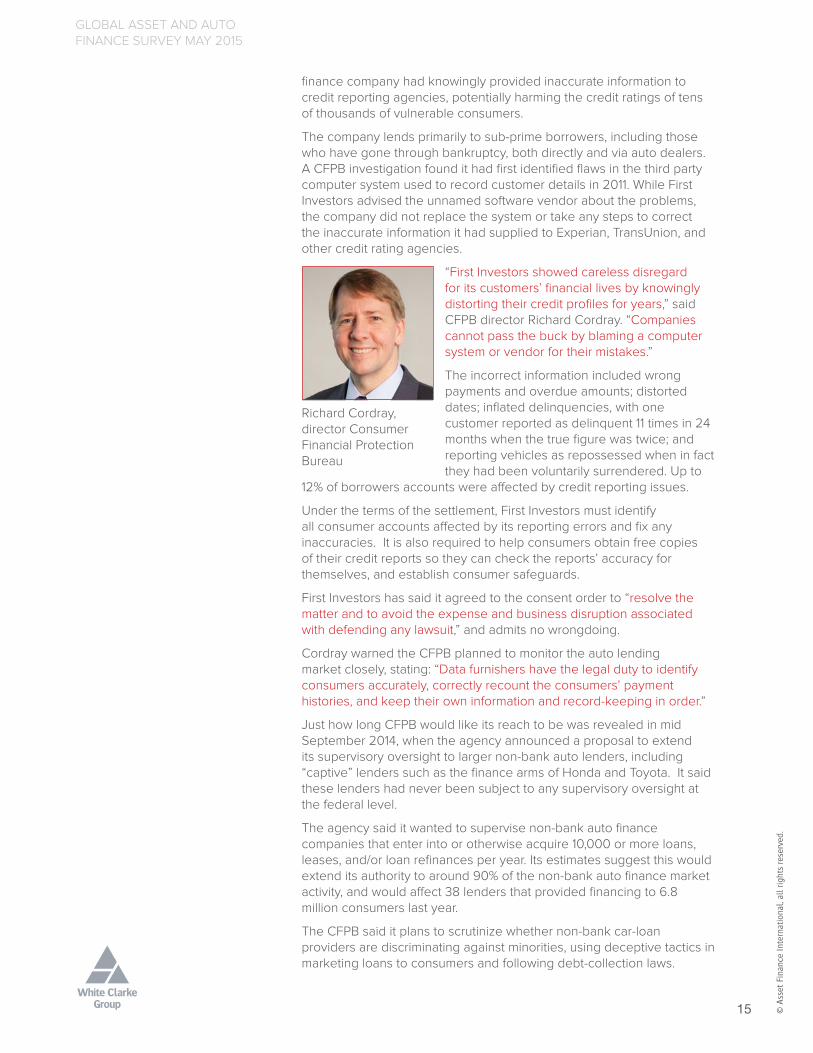

“First Investors showed careless disregard for its customers’ financial lives by knowingly distorting their credit profiles for years,” said CFPB director Richard Cordray. “Companies cannot pass the buck by blaming a computer system or vendor for their mistakes.”

The incorrect information included wrong payments and overdue amounts; distorted dates; inflated delinquencies, with one customer reported as delinquent 11 times in 24 months when the true figure was twice; and reporting vehicles as repossessed when in fact they had been voluntarily surrendered. Up to

12% of borrowers accounts were affected by credit reporting issues.

Under the terms of the settlement, First Investors must identify all consumer accounts affected by its reporting errors and fix any inaccuracies. It is also required to help consumers obtain free copies of their credit reports so they can check the reports’ accuracy for themselves, and establish consumer safeguards.

First Investors has said it agreed to the consent order to “resolve the matter and to avoid the expense and business disruption associated with defending any lawsuit,” and admits no wrongdoing.

Cordray warned the CFPB planned to monitor the auto lending market closely, stating: “Data furnishers have the legal duty to identify consumers accurately, correctly recount the consumers’ payment histories, and keep their own information and record-keeping in order.”

Just how long CFPB would like its reach to be was revealed in mid September 2014, when the agency announced a proposal to extend its supervisory oversight to larger non-bank auto lenders, including “captive” lenders such as the finance arms of Honda and Toyota. It said these lenders had never been subject to any supervisory oversight at the federal level.

The agency said it wanted to supervise non-bank auto finance companies that enter into or otherwise acquire 10,000 or more loans, leases, and/or loan refinances per year. Its estimates suggest this would extend its authority to around 90% of the non-bank auto finance market activity, and would affect 38 lenders that provided financing to 6.8 million consumers last year.

The CFPB said it plans to scrutinize whether non-bank car-loan providers are discriminating against minorities, using deceptive tactics in marketing loans to consumers and following debt-collection laws.

Richard Cordray, director Consumer Financial Protection Bureau

GLOBAL ASSET AND AUTO FINANCE SURVEY MAY 2015

16 © A

sset

Fin

ance

Int

erna

tion

al, a

ll r

ight

s re

serv

ed.

In a statement Cordray explained: “This proposal is needed to level the playing field for banks and non-banks in the auto lending market. We already supervise the auto lending practices of banks with more than $10 billion in assets, and this step would extend our supervision to the larger non-bank companies as well. It should not matter whether you get a loan or lease from a company that has a banking charter versus one that does not – every auto lender should be following the law and be subject to the same level of oversight.”

The CFPB plans have been subject to a public consultation but there has been, as yet, no confirmation of whether or not the agency will be extending its remit. However, there was a strong hint of how its role may develop from Massachusetts Senator Elizabeth Warren, a former Wall Street lawyer who was the guiding force behind the establishment of the CFPB.

In early 2015 Warren used a major public speech on financial regulation to take aim at the auto finance market, warning that: “Right now, the auto loan market looks increasingly like the pre-crisis housing market, with good actors and bad actors mixed together. The market is now thick with loose underwriting standards, predatory and discriminatory lending practices, and increasing repossessions.”

Warren called for a strengthening of the CFPB’s powers, claiming this would see some $26 billion of what she described as monies taken unfairly in commissions and other means back in consumers’ pockets. In the meantime, the agency has continued to pursue cases of alleged irregularities within the auto finance industry with some vigour.

It slapped a $8 million penalty on “buy-here, pay-here” auto dealer DriveTime, the largest such operation in the US, over claims the company made harassing debt collection calls to customers and provided inaccurate credit information to credit reporting agencies.

In its first ever action against a dealer in this sector, the CFPB ordered DriveTime to end debt collection tactics such as repeated calls to consumers’ workplaces, and make it explicitly clear how consumers can initiate “do not call” requests. Additionally, the sub-prime specialist has to fix its credit reporting practices, and arrange for harmed consumers to obtain free credit reports.

Cordray said: “DriveTime harassed and harmed countless consumers, many of whom were economically vulnerable. Our action today forces DriveTime to pay the price for its illegal debt collection tactics and for neglecting the accuracy of consumers’ credit information.”

In a statement, DriveTime executive vice president and general counsel Jon Ehlinger said the company was continuing to take steps to enhance its customer experience, and loan servicing activities, and stated: “We look forward to an ongoing relationship with the agency, and hope to establish a constructive dialogue designed to improve our customer service and compliance practices in the years ahead.”

The CFPB’s approach has itself come under attack with a coalition representing over 50 of the largest US auto finance sources claiming there is “bias and error” in the method used to determine whether an indirect auto lender’s portfolio shows evidence of unintentional discrimination in the terms offered to specific groups of consumers.

In a letter to the regulator the group, led by the American Financial Services Association (AFSA), says the CFPB should revisit its enforcement approach in the light of an independent study carried out

GLOBAL ASSET AND AUTO FINANCE SURVEY MAY 2015

17 © A

sset

Fin

ance

Int

erna

tion

al, a

ll r

ight

s re

serv

ed.

in November 2014 by Charles River Associates (CRA). This cast doubt on the reliability of many of the bureau’s findings, saying the methodology it used to analyse lending patterns overstated the impact on minorities.

The CRA study, based on 8.2 million vehicle contracts originated in 2012 and 2013, suggested that the CFPB’s method overestimates minorities by as much as 41%. While the CFPB has conducted its own analysis of its methodology, which concluded that the margin of error was around 21%, it has not explained what, if any action, it has taken to address the discrepancy.

The National Automobile Dealers Association (NADA), the American International Automobile Dealers Association (AIADA), and the National Association of Minority Automobile Dealers (NAMAD) have all pledged their support to the coalition’s campaign.

“Discrimination in the market simply cannot be tolerated,” said NADA president Peter Welch. “However, in light of the rigorous peer-review that has cast significant doubt on the CFPB’s findings, the bureau should change course – or at least hit the pause button – and address these new concerns. We applaud the courage of these organizations for speaking up.”

While there may be question marks over the methodology in use, there are no doubts that the CFPB’s push to increase its oversight of the auto lending market is part of a wider trend to bring in greater regulation.

Spotlight on loan discrimination

At the end of 2014 Honda’s US captive financing unit revealed that the CFPB and the US Department of Justice (DoJ) are set to file charges alleging it discriminates against some categories of borrowers in its pricing practices for loans made through auto dealerships.

Honda Finance said the federal agencies are seeking financial compensation for customers, and changes in the company’s pricing policies and practices, but were willing to re-consider legal action if the company co-operated with the authorities. Its disclosure followed news of a similar Securities and Exchange Commission (SEC) filing in late November from Toyota Motor Credit Corp. saying it faced enforcement action over alleged discriminatory pricing of loans to certain borrowers.

The Toyota Motor Credit Corp filing stated: “The agencies have indicated that they are seeking monetary relief and implementation of changes to our discretionary pricing practices and policies, which changes could adversely affect our business. We intend to continue to cooperate with the agencies to achieve a mutually satisfactory resolution.”

In a subsequent press statement the company said it has been working for the past two and a half years to improve its compliance with fair lending regulations.

Meanwhile, auto lender Santander Consumer USA has reached a $9.35 million settlement with the DoJ over claims the company illegally repossessed cars from members of the military on active service.

The deal, which relates to 1,112 automobile repossessions, is the largest ever levied under the Service members Civil Relief Act (SCRA).

GLOBAL ASSET AND AUTO FINANCE SURVEY MAY 2015

18 © A

sset

Fin

ance

Int

erna

tion

al, a

ll r

ight

s re

serv

ed.

The SCRA legislation protects serving personnel against certain civil proceedings that could affect their legal rights while they are in military service.

The DoJ lawsuit alleges that Santander initiated and completed 760 repossessions without court orders, which it said prevented service members from obtaining a court’s review of whether their repossessions should be delayed or adjusted in light of their military service.

The repossessions involved took place between January 2008 and February 2013 and the matter came to light following a complaint from a serving solder who told lawyers that Santander illegally repossessed his car in the middle of the night while he was at basic training.

“Those who answer this nation’s call to duty understandably have much on their minds while they are in military service,” said acting assistant attorney general Vanita Gupta of the DoJ’s civil rights division. “Whether their car will be seized and sold at auction should not be an additional worry. We will continue to vigorously pursue lenders who fail to take the simple steps necessary to determine, before repossessing a car, whether it is owned by a service member.”

Separately, JPMorgan Chase & Co revealed in an SEC filing that it is in discussions with the DoJ related to loans originating with auto dealers and financed by the bank that show “potential statistical disparities in markups charged to different races and ethnicities.”

Lease accounting uncertainty

On top of this, accounting convergence remains a critical topic for the US leasing industry, as it does globally. Companies are likely to see many more operational leases brought on balance sheet as a result of planned changes to current accounting rules (IAS 17) for leasing. The International Accounting Standards Board (IASB) and the US Financial Accounting Standards Board (FASB) issued their revised exposure draft (ED) on the proposals in 2013 and the plans have been subject to much debate, and strong criticism, in the months since.

This represents the last ongoing main convergence project in their joint attempt to harmonise US and international financial standards. Although some changes to lessor accounting are expected, lessee accounting is the area of biggest impact which will affect most companies and is likely to cause big changes to balance sheets.

Since the project originally got underway in 2008, the two regulators have published a discussion paper and two exposure drafts, changing their proposed model along the way. It is now clear that they are heading down differing accounting paths, although they continue to share one overriding goal, which is to bring leases on balance sheet. However, for some types of lease this will be carried out in two different ways, so P&L treatments will differ.

The IASB prefers a single method. Under this approach, when leases come on balance sheet there would be both a “right-of-use asset” and a lease liability initially measured at the net present value of the relevant lease payments. Two charges would then go through the income statement: amortisation of the right-of-use asset, and interest expense.

GLOBAL ASSET AND AUTO FINANCE SURVEY MAY 2015

19 © A

sset

Fin

ance

Int

erna

tion

al, a

ll r

ight

s re

serv

ed.

For its part, the FASB, is proposing a dual method whereby most existing capital/finance leases would be treated in the same way as IASB proposes (Type A, with separate amortisation and interest). Most operating leases would be classed as Type B, with a single straight line lease expense in the income statement.

After eight years of discussions, reversals and differences of opinion, IASB is now due to publish the amended lease accounting standard by Q3 2015. Whilst the equipment and auto finance industry will welcome an end to the uncertainty, no one can be sure just what impact the changes will have.

In response to concerns about cost and complexity, the boards have simplified both the measurement of lease assets and liabilities, and the reassessment requirements. In addition, the boards have clarified that a lessee can apply the requirements to a portfolio of similar leases, rather than to each individual lease.

Where cash flow presentation is concerned, a lessee would classify cash payments for the principal portion of the lease liability within financing activities and cash payments for the interest portion of the lease liability in accordance with the requirements relating to other interest paid. The boards have tentatively decided that lessor accounting will remain unchanged.

However, for some finance providers, the proposed changes to accounting for leases have served to underline how developing a new approach can lead to greater market share, by standing out from the crowd, as Jonathan Andrew, global CEO of the commercial finance business of Siemens Financial Services explains: “When considered on a global basis, the tax advantages of leasing are becoming less relevant. Innovative lessors such as Siemens are bringing to the marketplace new approaches and flexible financing solutions, creating demand based on factors beyond simply the tax advantages.”

GLOBAL ASSET AND AUTO FINANCE SURVEY MAY 2015

20 © A

sset

Fin

ance

Int

erna

tion

al, a

ll r

ight

s re

serv

ed.

EUROPE

What’s happened since the financial crisis?

While North America may be the dominant leasing market, the rest of the world was certainly not immune to the problems created by the crisis in the wider economy and a general tightening of credit.

The situation is summed up by Andrew, who explains that: “The impact of significantly reduced levels of confidence and investment at the time of the financial crisis negatively impacted the leasing market development throughout the globe.”

The situation in Europe was mixed, with the fallout from the financial crisis serving to highlight the longstanding divide between leasing activity in the southern and northern regions. Summing up what happened in the region as a whole, Servi de Vette, director strategy and geographic expansion at automotive finance specialists LeasePlan, notes a material impact in Spain, Portugal and Greece, and to a lesser extent France and Italy, with the significant decline in new car sales playing a major role.

Societe Generale Equipment Finance estimates growth in the leasing market in France came to a standstill in 2009, with a reported decline of 25%. However, in the years that followed the impact was less marked, with a decline of around 2% between 2010 and 2012.

Kai-Otto Landwehr, head of the commercial finance business of Siemens Financial Services in Germany says 2009 witnessed a sharp drop in equipment leasing investment, which was down by 20%. Since then

GLOBAL ASSET ANDAUTO FINANCE SURVEY

EUROPE

What’s happened since the financial crisis?

While North America may be the dominant leasing market, the rest of theworld was certainly not immune to the problems created by the crisis in thewider economy and a general tightening of credit.

The situation is summed up by Jonathan Andrew, global CEO of thecommercial finance business of Siemens Financial Services, who explainsthat: “The impact of significantly reduced levels of confidence and investmentat the time of the financial crisis negatively impacted the leasing marketdevelopment throughout the globe.”

The situation in Europe was mixed, with the fallout from the financial crisisserving to highlight the longstanding divide between leasing activity in thesouthern and northern regions. Summing up what happened in the region asa whole Servi de Vette, director strategy and geographic expansion atautomotive finance specialists LeasePlan, notes a material impact in Spain,Portugal and Greece, and to a lesser extent France and Italy, with thesignificant decline in new car sales playing a major role.

Société Générale Equipment Finance estimates growth in the leasing marketin France came to a standstill in 2009, with a reported decline of 25%.However, in the years that followed the impact was less marked, with adecline of around 2% between 2010 and 2012.

Kai-Otto Landwehr, head of the commercial finance business of SiemensFinancial Services in Germany says 2009 witnessed a sharp drop in equipmentleasing investment, which was down by 20%. Since then equipment leasinghas started picking up, reaching €47.2bn in 2012, though still short of the pre-crisis level of €51.1bn in 2008.

© A

sset

Fin

ance

Int

erna

tion

al, A

ll r

ight

s re

serv

ed.

14

GLOBAL ASSET AND AUTO FINANCE SURVEY MAY 2015

21 © A

sset

Fin

ance

Int

erna

tion

al, a

ll r

ight

s re

serv

ed.

equipment leasing has started picking up, reaching €47.2 billion in 2012, though still short of the pre-crisis level of €51.1 billion in 2008.

The Nordic region fared rather better than many others, with de Vette singling it out as one of the few parts of northern Europe to emerge relatively unscathed from the financial crisis, along with Switzerland, although the strength of the Swiss franc during that period created some challenges in areas such as the second hand car market.

More specifically Sjur Loen, managing director of Nordea Finance Norway, says while the Nordic region as a whole was less affected that the rest of Europe, there was some variation between the different countries, with Denmark the most affected and Norway the least.

However, since then prospects have started to improve markedly. Research published in August 2014 by Leaseurope together with specialist consultancy Invigors EMEA suggested that many of the European markets had turned the corner. The results of the biannual Leaseurope/Invigors European Business Confidence Survey confirm the optimism evident at the beginning of the year, with many of the survey’s measures showing continued improvement from the previous survey conducted in December 2013. The outlook for new business volumes over the remaining six months of 2014 was particularly positive, with 90% of those surveyed expecting new business volumes to increase, compared to just 2% who anticipated a decline. Expectations on the level of bad debt remained at a similar level to the previous survey, while over 58% of survey respondents forecast that net profits for their business will increase over the same period, again a similar percentage to that recorded last December. Industry expectations on a number of key indicators covering service levels, expenditure and staffing also indicated improvements for the second half of 2014, and over half of respondents (57%) said that their organisations are targeting expansion. Growth was focused on asset classes such as vehicles, agriculture and technology as well as geographic expansion within and outside of Europe.

European performance strengthens

After 2013’s flat performance, 2014 had all the hallmarks of a strong year for the European asset finance industry, with confidence improving markedly and the Leaseurope/Invigors survey identified strong growth and improvements in key performance indicators for many of the companies who participated.

These predictions have turned out to have considerable substance and are backed up by preliminary results from Leaseurope’s survey of the European leasing market at the start of 2015. This suggests that new leasing business in Europe expanded by 8.4% in 2014, reaching its highest annual rate of growth in volume since 2007.

Growth was observed across all main asset categories, with an especially strong performance in the auto sector, with new leasing volumes in this segment rising by 12.4% on 2013. The equipment leasing segment saw a moderate increase of nearly 1%, while real estate leasing picked up by 7.6% in 2014, witnessing the first year of growth since 2010.

GLOBAL ASSET AND AUTO FINANCE SURVEY MAY 2015

22 © A

sset

Fin

ance

Int

erna

tion

al, a

ll r

ight

s re

serv

ed.

However, the trend for growth to be uneven across all the European countries remained a challenge. Nevertheless, the survey found that most of national leasing markets saw positive results in 2014, which is an improvement compared to 2013, where just under half recorded negative performance.

Overall, the increase in new business volumes in 2014 was largely driven by Europe’s four largest economies, although some of the leasing markets in Southern Europe saw double digit growth.

What are the challenges?

The biggest challenge for all of the countries in Europe has been the eurozone crisis, which has seen countries such as Greece, Spain and Portugal forced to introduce drastic measures to tackle ballooning government debt. The consequent impact on businesses and investment in this region has been severe, with many organizations struggling to survive, let along take on new equipment or other assets. While the situation is at its most desperate in the southern parts of Europe, since there is a single market and the other countries rely on the neighbours for trade, they have also felt the effects.

Assessing market developments since 2012 Kai Ostermann, CEO of Deutsche Leasing Group, says: “The main challenge is that the current economic situation is still insecure. The overall economic environment was characterized by a downturn in the real economy which reflected the uncertainty surrounding the continuing sovereign debt crisis. In particular, the tense situation and the ongoing consolidation in the crisis countries triggered a decline in market participants’ confidence in the stability of the financial system from the spring of 2012 onwards.”

Landwehr points out that German companies have put their investment plans on ice in recent times due to falling demand from eurozone countries, which account for around 40% of German exports, and the resulting drop in manufacturing orders in 2012 and Q1 2013. Latest figures from the German leasing association suggest that new business volumes remain subdued.

It is a similar story in France. “Our business is closely linked to the ability of industries to make investments, and when this becomes difficult, or when investments stop the leasing finance sector slows down as well,” Societe Generale Equipment Finance reports.

Even in the Nordic region, which has been largely insulated from the worst of the downturn, Loen notes that in the auto finance market car dealers’ earnings, profitability and solvency are all under pressure. “Finance companies are providing wholesale solutions, demo financing as well as residual value positions. It is likely there will be some consolidation of car dealers into larger units in the Nordic region in the coming years, especially in Denmark and Norway,” he said.

Societe Generale Equipment Finance sums up the current challenges for lessors as “to continue to grow, to maintain the risk level and to adapt the prices to the capital required for our activities. To achieve these goals, the appetite for investment in France must be restarted.”

Jonathan Andrew does not underplay the potential difficulties ahead, noting that although there are positive signs of economic recovery in many parts of the world, business confidence remains fragile, and overall has yet to fully recover to pre-crisis levels. He said: “Geopolitical

GLOBAL ASSET AND AUTO FINANCE SURVEY MAY 2015

23 © A

sset

Fin

ance

Int

erna

tion

al, a

ll r

ight

s re

serv

ed.

factors continue to underpin business confidence, the world’s economies and ultimately the development of the leasing markets. Accordingly the activities of leasing players in countries grappling with a slowing or declining macro-economic outlook or an uncertain or changing political environment particularly face challenges.”

What does the future hold?

Leaseurope’s survey of members suggests the outlook for new business volumes over the first half of 2015 remains positive, with 84% of those polled expecting new business volumes to increase, while just 7% anticipate a decline. Expectations on the level of bad debt are stable at similar levels to the previous survey with the majority of participants (62%) forecasting that bad debt will remain unchanged over the coming six months.

Similarly, 52% expect no change in margins, although 31% predict that margins will decrease in their organisations, slightly above the percentage recorded in the previous survey. However, the results for net profits show a marginal improvement, with 63% of survey respondents forecasting that net profits for their business will increase over the next six months, a small increase on that recorded last June.

Industry expectations on a number of key indicators covering service levels, expenditure and staffing show either small improvements or little change for the first half of 2015, while exactly half of respondents said that their organisations are targeting expansion. Growth was focused in particular on areas such as vendor finance as well as on asset classes such as vehicles and technology. There was also interest in geographic expansion, primarily in Europe as well as in new product areas such as invoice discounting and wholesale finance.

Commenting on the figures, Leaseurope’s adviser in statistics and economic affairs, Jurgita Bucyte said: “Against the backdrop of faltering European equipment investment throughout 2014, it is particularly encouraging to see that our industry is able to gather momentum across the board. Businesses were keen to use leasing to invest in a wide range of assets, particularly in vehicles.”

“This trend supports the findings of our latest Business Confidence Survey, which demonstrates a positive sentiment in the leasing market for new business growth. While near-term European investment is likely to be subdued and some degree of economic uncertainty remains, equipment investment growth is projected to gradually pick up, which should bode well for the leasing business in 2015,” Bucyte confirmed.

Eastern European countries, now emerging from many years of centralised control and with a burgeoning middle class, are proving to be one of the leasing industry’s high spots. According to statistics from ALB, the leasing association of Romania, that country’s financial leasing market recorded a 7% increase in new business by the end of 2014 compared to performance in 2013, with the total amounting to 1,324 million euros. Of this, 76 % (1,001 million euros) was down to leasing for vehicles, 21% (282 million euros) for equipment and 3% (41 million euros) for real estate.

“We are pleased that the leasing market continues to gradually consolidate its results. The market advance this year should be seen in terms of the crisis years. Since 2009, as we have seen, financed

GLOBAL ASSET AND AUTO FINANCE SURVEY MAY 2015

24 © A

sset

Fin

ance

Int

erna

tion

al, a

ll r

ight

s re

serv

ed.

volumes have been stabilized around an annual average of 1,300 million euros. The market still has ground to recover and we shall see, most likely, the continuation of the growth dynamics also in 2015,” declared Felix Daniliuc, President of ALB.

For the future, ALB expects to see continued growth in vehicle and agricultural leasing, as well as medical equipment, but predicts that volumes will drop in construction and the energy sector.

The biggest share of the market is held by the banks’ subsidiaries, with 75% out of the total, followed by the captive companies sector with 20% and by the independent companies sector with 5%.

Eastern Europe takes the lead

Progress in the Polish leasing market was especially strong, with the Polish Leasing Association (ZLP) reporting that the market grew by 21.3% in 2014, which it pointed out was over 2.5 times higher than the average for the European market as a whole. As the Polish economy has improved so has the jobs market, which has driven strong demand for car leasing. Alongside this, up until now there has been a lot of activity in the agricultural machinery and equipment leasing sector, as a result of three years of funding from the European Union.

Looking ahead, the association forecasts that the first few months of 2015 will see lower levels of financing for light vehicles and little change in the demand for financing for fixed assets connected with heavy transport and real estate. The best prospects for the growth are identified as being within machinery and IT equipment financing.

Experienced observers of the market suggest that these predicted improvements are no mere flash in the pan, but the result of substantial regrouping and rethinking within the leasing industry. Philippe Bismut, CEO of Arval said: “The leasing industry proved itself able to weather one of the most difficult downturn periods of recent history and is now positioned to capitalise on market recoveries. Consolidated recovery will bring some long-awaited breathing room and future opportunities for industry development.”

At the start of 2015, for example, the Spanish Leasing and Renting Association (AELR) reported the number of vehicle purchases funded by leasing agreements in January reached 10,803, an increase of 41% on the same month the previous year. There was also a 28% rise in the number of new cars registered, of which over 40% purchased by companies rather than individuals. AELR suggested this showed a strengthening in the Spanish economy and that growing confidence levels were translating into business investment.

While there are clearly opportunities for improvements from a low base in some of the Southern European countries, Leaseurope’s survey highlighted the fact that some of the larger mature markets, especially the UK, are the key drivers behind overall growth. This trend is acknowledged by Rich Green, President of CIT International Finance, who pointed out that the credit crunch had drawn in new potential customers for leasing options.

“We are seeing increased opportunities to support the Small and Medium Sized Businesses (SMEs) in the UK, either through adjacent market segments or the development of new products. SMEs are looking to access funding from new sources including leasing,” Green said.

GLOBAL ASSET AND AUTO FINANCE SURVEY MAY 2015

25 © A

sset

Fin

ance

Int

erna

tion

al, a

ll r

ight

s re

serv

ed.

Figures released by the UK’s Finance & Leasing Association (FLA) show growth in asset finance new business of 13% in January 2015, compared with the same month in 2014. New business was up by the same rate in the twelve months to January 2015.

Plant and machinery finance grew by 12% in January compared with the same month a year earlier, while IT equipment finance and business equipment finance grew by 49% and by 10% respectively over the same period.

Commenting on the figures, Geraldine Kilkelly, FLA’s head of research and chief economist, said: “The asset finance market has made a good start to 2015, with growth continuing across key asset sectors. The percentage of UK investment in machinery, equipment and purchased software financed by FLA members increased from 26.2% in 2013 to 27.2% in 2014, reaching its highest level since 2011.”

Despite the slow down in business activity caused by an impending general election, and associated uncertainty about future tax changes and the possibility of a coalition government, the FLA data suggests growth in the market has a firm base. Its data indicates 12% growth in asset finance new business in February 2015, marking the market’s seventeenth consecutive month of growth. February saw strong growth in IT equipment finance and commercial vehicle finance, up by 84% and 10% respectively. Business equipment finance and car finance each grew by 5% over the same period.

Rules and regulations

France’s decision in 2013 to tighten the tax regime is not an isolated occurrence, with many of the eurozone countries taking similar steps to try to repair large government deficits. In addition to the decision taken in individual countries, changes in regulation at the EU level are also having an impact on the leasing market.

“The expanded regulatory requirements under Basel III in terms of credit institutions’ equity and liquidity have generally reduced the availability of funds. For many leasing companies this has been a big issue,” notes Ostermann. He also says that Deutsche Leasing has worked to develop its existing risk-bearing capacity concept and its risk measurement methods to comply with the requirements for modern risk management as well as current regulatory trends.

More significant for many in the leasing industry in Europe, as in the US, are planned changes to accounting for leases which are likely to see many more operational leases brought on balance sheet as a result of changes to current accounting rules (IAS17) for the leasing industry.

When the International Accounting Standards Board (IASB) and the US Financial Accounting Standards Board (FASB) issued their long-awaited exposure draft (ED) on the proposals in 2013, this drew strong criticism from organizations such as the Societe Generale Group which stated that “the conceptual basis of the proposals remains unclear and the complexity of the proposed model is still high and raising significant operational issues.”

“The current leasing accounting ED is creating uncertainty and has the potential to affect both leasing companies and companies that use leasing. It could create an immense amount of work and expense for both to implement,” CIT confirms.

GLOBAL ASSET AND AUTO FINANCE SURVEY MAY 2015

26 © A

sset

Fin

ance

Int

erna

tion

al, a

ll r

ight

s re

serv

ed.

High hopes that this fog of confusion would be lifted at the March 2014 meeting of IASB and FASB to consider responses to the ED and the way forward have been dashed by the growing view that the two standards bodies are now bound to diverge in some areas at least, with the original declared intention of creating a single global standard proving too challenging to achieve.

News that there was no agreement on several critical elements of the proposals is a major concern for multinational companies which use leasing options across their business streams in different countries and for leasing companies which operate both in the US and in Europe.

The concern for the leasing industry arises over the resulting complexity and ensuing cost in adjusting accounts to include leases of “big-ticket” items such as manufacturing facilities and aircraft, which under the single model approach would need to be accounted for in the same way as leases of office space and smaller items such as company cars and computers.

Both boards have affirmed that there would be an exemption for short-term leases, which would be accounted for in the same manner as today’s operating leases. “Short-term” would mean 12 months or less, using the same definition of the term as used elsewhere in the standard.

Although the IASB supported a recognition and measurement exemption for small assets, the FASB asked its staff to do more research on the magnitude of leases of small ticket items to get a sense of the possible impact. The boards were in agreement that there should not be specific materiality guidance as to what would qualify as a “small ticket” lease.

Past experience suggests that the increasing complexity and uncertainty around regulation will deter overseas players from making a move to acquire leasing operators in national markets such as French and Germany.

However, the prospect of an increasing tough regulatory environment may prompt mergers amongst some smaller national players. Landwehr indicated there is the potential for mergers and acquisitions amongst the 183 members of the German Leasing Association (BDL), whose numbers have already fallen from 227 in 2001, as he outlines: “More than three quarters of those in the BDL have fewer than 50 employees, and many lessors in the German market are small and medium sized companies. Just under 50% of the association’s members are manufacturer or bank-owned leasing companies, with the rest being independent businesses. Many of the smaller leasing companies were forced to exit the sector as they struggled to compete under increasing administrative costs associated with supervisory regulations. Consolidation in the industry is likely to continue.”

While agreeing that this is a potential future trend, Andrew suggests that a shortage of skilled personnel may come to represent as much of a difficulty as new regulations. “Tightening regulation continues to challenge the equipment leasing market, and as a result further structural changes are to be expected. Players are expected to nevertheless grow their businesses and portfolios, which in turn will create challenges relating to talent management – attracting, developing and retaining the best employees – particularly in those geographies where leasing is still developing,” Andrew said.

GLOBAL ASSET AND AUTO FINANCE SURVEY MAY 2015

27 © A

sset

Fin

ance

Int

erna

tion

al, a

ll r

ight

s re

serv

ed.

In addition to the long-standing concerns over the future of lease accounting, Leaseurope has joined forces with ELFA and the Canadian Finance and Leasing Association (CFLA) to raise queries about the impact of a new proposal regarding credit risk set out under the Basel framework, which is on course to become an EU-wide requirement.

Responding to the consultative document on Revisions to the Standardised Approach for Credit Risk issued by the Bank of International Settlements (BIS), the three associations are arguing there should be risk weighting treatment for commercial leases and loans backed by capital equipment. They recommend enhanced granularity and risk sensitivity, updated risk weight calibrations and better clarity on the application of the standards in order to achieve BIS’s goal of strengthening the regulatory capital standard.

The associations point out that corporate exposures consist of various types such as investment grade bonds, non-investment grade bonds, bank corporate loans, small and medium sized business loans, municipal loans and other types of debt. Each business type presents a unique risk profile that calls for treatment as specialized lending. They would like to see risk weightings on commercial leases and loans that reflect the default risk of their customers and the security offered by equipment collateral. The associations argue, and say they have supporting historical data to back up their view, that default rates are lower for equipment finance debt when compared against other forms of corporate exposures such as non-investment grade bonds or bank corporate loans.