gibraltar - pkf international · there is no capital gains tax in gibraltar. the commissioner of...

TRANSCRIPT

2016/17

Gibraltar

PKF Worldwide Tax Guide 2016/17 1

FOREWORD A country's tax regime is always a key factor for any business considering moving into new markets. What is the corporate tax rate? Are there any incentives for overseas businesses? Are there double tax treaties in place? How will foreign source income be taxed? Since 1994, the PKF network of independent member firms, administered by PKF International Limited, has produced the PKF Worldwide Tax Guide (WWTG) to provide international businesses with the answers to these key tax questions. As you will appreciate, the production of the WWTG is a huge team effort and we would like to thank all tax experts within PKF member firms who gave up their time to contribute the vital information on their country's taxes that forms the heart of this publication. The PKF Worldwide Tax Guide 2016/17 (WWTG) is an annual publication that provides an overview of the taxation and business regulation regimes of the world's most significant trading countries. In compiling this publication, member firms of the PKF network have based their summaries on information current on 30 April 2016, while also noting imminent changes where necessary. On a country-by-country basis, each summary such as this one, addresses the major taxes applicable to business; how taxable income is determined; sundry other related taxation and business issues; and the country's personal tax regime. The final section of each country summary sets out the Double Tax Treaty and Non-Treaty rates of tax withholding relating to the payment of dividends, interest, royalties and other related payments. While the WWTG should not to be regarded as offering a complete explanation of the taxation issues in each country, we hope readers will use the publication as their first point of reference and then use the services of their local PKF member firm to provide specific information and advice. Services provided by member firms include: Assurance & Advisory;

Financial Planning / Wealth Management;

Corporate Finance;

Management Consultancy;

IT Consultancy;

Insolvency - Corporate and Personal;

Taxation;

Forensic Accounting; and,

Hotel Consultancy. In addition to the printed version of the WWTG, individual country taxation guides such as this are available in PDF format which can be downloaded from the PKF website at www.pkf.com

Gibraltar

PKF Worldwide Tax Guide 2016/17 2

IMPORTANT DISCLAIMER This publication should not be regarded as offering a complete explanation of the taxation matters that are contained within this publication. This publication has been sold or distributed on the express terms and understanding that the publishers and the authors are not responsible for the results of any actions which are undertaken on the basis of the information which is contained within this publication, nor for any error in, or omission from, this publication. The publishers and the authors expressly disclaim all and any liability and responsibility to any person, entity or corporation who acts or fails to act as a consequence of any reliance upon the whole or any part of the contents of this publication. Accordingly no person, entity or corporation should act or rely upon any matter or information as contained or implied within this publication without first obtaining advice from an appropriately qualified professional person or firm of advisors, and ensuring that such advice specifically relates to their particular circumstances. PKF International Limited (PKFI) administers a family of legally independent firms. Neither PKFI nor the member firms of the network generally accept any responsibility or liability for the actions or inactions of any individual member or correspondent firm or firms. PKF INTERNATIONAL LIMITED JUNE 2016 © PKF INTERNATIONAL LIMITED All RIGHTS RESERVED USE APPROVED WITH ATTRIBUTION

Gibraltar

PKF Worldwide Tax Guide 2016/17 3

STRUCTURE OF COUNTRY DESCRIPTIONS A. TAXES PAYABLE

COMPANY TAX CAPITAL GAINS TAX BRANCH PROFITS TAX VALUE ADDED TAX CUSTOMS AND EXCISE DUTIES FRINGE BENEFITS TAX GENERAL RATES STAMP DUTY CAPITAL DUTY GAMING TAX OTHER TAXES

B. DETERMINATION OF TAXABLE INCOME

INDIVIDUALS INDIVIDUAL ORDINARY RESIDENT CORPORATIONS STOCK OPTIONS CAPITAL ALLOWANCES CAPITAL GAINS AND LOSSES DIVIDENDS INTEREST DEDUCTIONS WITHHOLDING TAX – PAYMENTS TO SUBCONTRACTORS LOSSES FOREIGN SOURCED INCOME INCENTIVES DEDUCTION OF APPROVED EXPENDITURE ON PREMISES DEVELOPMENT AID

C. FOREIGN TAX RELIEF D. CORPORATE GROUPS E. RELATED PARTY TRANSACTIONS F. EXCHANGE CONTROL G. PERSONAL INCOME TAX

CHARGE TO TAX TAX INCENTIVES SOCIAL SECURITY CONTRIBUTIONS

H. TREATY AND NONE-TREATY WITHHOLDING TAX RATES

Gibraltar

PKF Worldwide Tax Guide 2016/17 4

MEMBER FIRM For further advice or information please contact: City Name Contact Information Gibraltar Joseph Canilla +350 200 71876 [email protected] BASIC FACTS Full name: Gibraltar Capital: Gibraltar Main language: English, Spanish, Llanito Population: 32,194 (2015 estimate) Major religion: Christianity Monetary unit: Gibraltar Pound (GIP) Internet domain: .gi Int. dialling code: +350 KEY TAX POINTS • A company is taxed on profits which accrue, or are derived, in Gibraltar for a financial year at a

rate of 10% (although the rate can be 20% in some cases). • Profits of foreign companies are taxed at the same rate as resident companies. • There is no capital gains tax or VAT in Gibraltar. • For individuals and partnerships, the tax year runs from 1 July to 30 June and tax is payable on

the actual taxable profits for the year. For tax purposes, individuals can elect between the Allowance and Gross Income Based Systems. The standard rate of tax for individuals is 20%.

A. TAXES PAYABLE COMPANY TAX The standard rate of Gibraltar corporation tax is 10%. For utility companies & companies that abuse a dominant position there is a higher rate of tax applied which is 20%. The utility companies are classified as Telecommunications, Petroleum, Water and Sewage. Companies are taxed on profits for the financial year on income accrued or derived in Gibraltar. CAPITAL GAINS TAX There is no capital gains tax in Gibraltar. The Commissioner of Income Tax will refer to case law to judge whether a benefit is of a capital or trading nature. BRANCH PROFITS TAX Profits of foreign companies are taxed at the same rate as resident companies. VALUE ADDED TAX There is no VAT in Gibraltar. Derogation from implementing VAT: Although Gibraltar joined the EU alongside the United Kingdom at the time of the United Kingdom’s accession Gibraltar was granted derogation from

Gibraltar

PKF Worldwide Tax Guide 2016/17 5

implementing VAT. Therefore there is no VAT in Gibraltar. CUSTOMS AND EXCISE DUTIES Goods imported into Gibraltar from outside are, with some exceptions, generally subject to import duty at the applicable rate of 6% or 12%. FRINGE BENEFITS TAX Perquisites or benefits in kind are taxed as gains from employment. There is specific detailed legislation on how to tax benefits and also the allowances available, particularly with respect to: Expense payments; vouchers and credit tokens; Living accommodation; removal benefits and expenses; Cars, vans and related expenditure; Loans to: employees, directors, shadow directors or connected persons. The Commissioner for Income Tax has the ability to tax benefits not specifically covered in the legislation. Where the benefits are less than £250 in total for any year of assessment no tax is payable in respect of those benefits. The employer may opt to pay the tax on the benefits on behalf of an employee. When the annual value of these benefits is between £250 and £15,000 the tax under this Schedule shall be paid at the rate of 20%. When the annual value of the benefit is above £15,000 tax shall be paid at the rate of 29%. GENERAL RATES General rates are levied on all properties in Gibraltar. STAMP DUTY Stamp Duty is payable on the transfer or sale of any Gibraltar real estate or shares in a company owning Gibraltar real estate (on an amount based on the market value of the said real estate) at the following guidance rates: First or second time buyers as defined by section 19A the Act: Value of property Stamp Duty First £260,000; 0% From £260,000 to £350,000 5.5% From £350,000 3.5% Non- qualifying Purchasers Not exceeding £200,000 0% £200,000 to £350,000 5.5% £350,000 to first £350,000 3.0% Above £350,000 3.5% Stamp Duty is also payable on mortgages secured on Gibraltar real estate at the following rates: Mortgages up to £200,000 0.13% Mortgages over £200,000 0.20% CAPITAL DUTY Capital duty of £10 is payable on the nominal share capital or any increase thereof Limited liability companies. GAMING TAX Gaming tax is levied at 1% of the gaming income. The tax paid is subject to a minimum of £85,000

Gibraltar

PKF Worldwide Tax Guide 2016/17 6

and maximum of £425,000 per annum. OTHER TAXES There are no capital gains, wealth, inheritance or gift taxes in Gibraltar B. DETERMINATION OF TAXABLE INCOME INDIVIDUALS An individual who is ordinary resident in Gibraltar is chargeable to tax on his/her worldwide income. INDIVIDUAL ORDINARY RESIDENT A person who is resident in Gibraltar for a period (or accumulated period) totalling at least 183 days in any year of assessment or is present in Gibraltar in any year of assessment which is one of three consecutive years in which the total of the days on which the individual is present in Gibraltar exceeds 300 days. Non-residents who undertake activities in Gibraltar which are ancillary to their employment or self-employment elsewhere and the duration of the activity is less than 30 days in aggregate in any year of assessment or such other number of days that the commissioner may by prior written agreement in his discretion allow, will not be liable to income tax in Gibraltar. This also covers directors’ fees. CORPORATIONS A company is taxed on profits which accrue or are derived in Gibraltar. The Act defines accrued or derived by reference to the activities that generate the profit. A company is considered ordinarily resident in Gibraltar if management and control as defined is exercised in Gibraltar. STOCK OPTIONS The granting of an option or share to an employee is an event which is taxable. When the option is exercised and there is a disposal of the shares capital gains arises and the capital gain is not taxable on the individual as there is no capital gain tax in Gibraltar. CAPITAL ALLOWANCES 100% First year allowances: The first £30,000 of qualifying expenditure on fixtures & fittings plant and machinery acquired in a year of assessment. The first £50,000 of Computer equipment acquired in a year of assessment. Annual allowances: There is an additional annual allowance on the surplus balance of the pooled amount at the rate of 15% per annum on a reducing balance basis. Motor vehicles not qualifying as plant and machinery there is an allowance at the rate of 15% per annum on a reducing balance basis. Unincorporated entities and companies on the higher 20% rate of income tax there is a 20% allowance on the pooled balance. Capital allowances on Entertainment centres, hotel, mill, factory or other similar premises (excluding the cost of the land). There is an allowance at the rate of 4% per annum on a straight line basis. CAPITAL GAINS AND LOSSES Capital gains are not subject to tax therefore capital losses are not allowable deductions.

Gibraltar

PKF Worldwide Tax Guide 2016/17 7

DIVIDENDS There is no charge to tax on the receipt by a Gibraltar company of dividends from any other company, whether it is a Gibraltar resident or non-resident. There is no tax on a dividend paid by a Gibraltar company to a non-resident of Gibraltar. There is also no withholding tax on dividends paid, but when a dividend is declared to a Gibraltar resident person, individual or company, a dividend return must be filed with the tax authorities. INTEREST DEDUCTIONS There is no withholding tax on interest payments. WITHHOLDING TAX – PAYMENTS TO SUBCONTRACTORS Payments made to subcontractors (in the construction industry) without a valid tax exemption certificate issued by the Commissioner of Income Tax are subject to 25% withholding tax on that portion of the payment which is not for materials used in construction. LOSSES A trading loss incurred can be carried forward and set off against future trading profit. Non trading losses are not allowable deductions. If within any period of three years there is both a change in ownership of a company and there is a major change in the nature or conduct of a trade carried on by the company no relief shall be given in respect of any losses brought forward from the period beginning before the change of ownership against any profits or gains. There is no provision for the carrying back of losses. FOREIGN SOURCED INCOME Income tax is charged on income accruing in or derived from Gibraltar. Residents of Gibraltar are taxed on their world-wide income. INCENTIVES DEDUCTION OF APPROVED EXPENDITURE ON PREMISES Resident taxpayers whether Individuals or companies (although there is a different approach to each category) who have an interest in a building situated in Gibraltar, have a special allowance for approved expenditure on the repair or enhancement of the façade of the building. This allowance is in addition to any normal allowance given. The taxpayer will have to comply with the requirement contained within the special provisions in order to be able to reap its advantages. Individuals whose assessable income is based on the gross income based system the allowance is restricted to £6,000 per annum. DEVELOPMENT AID The development Aid Act is aimed at private development in Gibraltar. There are conditions to be met in order to take advantages of the incentives offered. Application for development aid must be made to the Minister responsible. C. FOREIGN TAX RELIEF Any person ordinarily resident in Gibraltar can claim unilateral tax relief on tax paid abroad subject to providing the necessary evidence of the payment to the Commissioner of Income Tax, the taxpayer is

Gibraltar

PKF Worldwide Tax Guide 2016/17 8

entitled to a tax credit equivalent to the lesser of the tax payable on that income in Gibraltar; or the tax payable abroad in respect of that income. If relief from the double taxation has to be made abroad then the relief allowed is reduced accordingly. D. CORPORATE GROUPS There is no group relief available in Gibraltar. E. RELATED PARTY TRANSACTIONS Anti-avoidance provision The 2010 Income tax Act introduced a number of anti-avoidance clauses which can be invoked to set aside arrangements that can be seen to be fictitious or artificial. Also the promoters of a tax planning schemes have to notify the Commissioner of Income Tax within 30 days of any schemes which result in the payment of less tax. There are a number of clauses that specifically consider and address anti avoidance arrangements that can lead to the reduction or elimination of tax payable as follows: Thin capitalisation rules This is aimed at shareholder or connected persons and refers to interest paid on a loan by a company to related parties (which is not itself a company) or loans where security is provided by related parties and where at any time in an accounting period the loan capital to equity ratio is greater than 5 to 1. The interest paid will be deemed to be a dividend by the company and received by the connected part and not deductible on the company in computing the profits for the period. Transactions with connected persons When it appears that transactions with connected persons in the course of the business are arranged with a view to make no profit or reduce profits or increase losses any excess will be deemed to be a dividend paid and not deductible on the company in computing the profits for the period. When expenses incurred in favour of a connected person the expense allowed shall be the least of the expense incurred; 5% of the gross turnover of the person for the accounting period or 75% of the pre-expense net of profit of the person for the accounting period. Non-deductibility of interest paid on certain secured loans This refers to interest payable and back to back loans. Where a loan is made by a lender at an arm’s length and all or part of the loan is secured by a cash deposit or an investment as defined by the Act of any connected person over which the lender has taken security the loan interest will not be deductible when computing the profit or gain. Chargeability of dual employment contracts Where an employee of an employer ordinarily resident in Gibraltar has one or more other contracts with that or another employer whether resident in Gibraltar or elsewhere who is a connected person to the employer ordinary resident in Gibraltar the income derived shall be subject to tax. If it can be proved to the Commissioner that the purpose of the transactions is not to avoid tax this is a mitigation circumstance that will be considered. Transfer of assets abroad This is to prevent the transfer of assets abroad by an ordinary resident individual with the purpose of avoiding taxation in Gibraltar and the income becomes payable by persons resident outside Gibraltar. When the person affected can demonstrate to the Commissioner that the intention is not to avoid tax the provisions do not apply. F. EXCHANGE CONTROL There are no exchange controls in Gibraltar.

Gibraltar

PKF Worldwide Tax Guide 2016/17 9

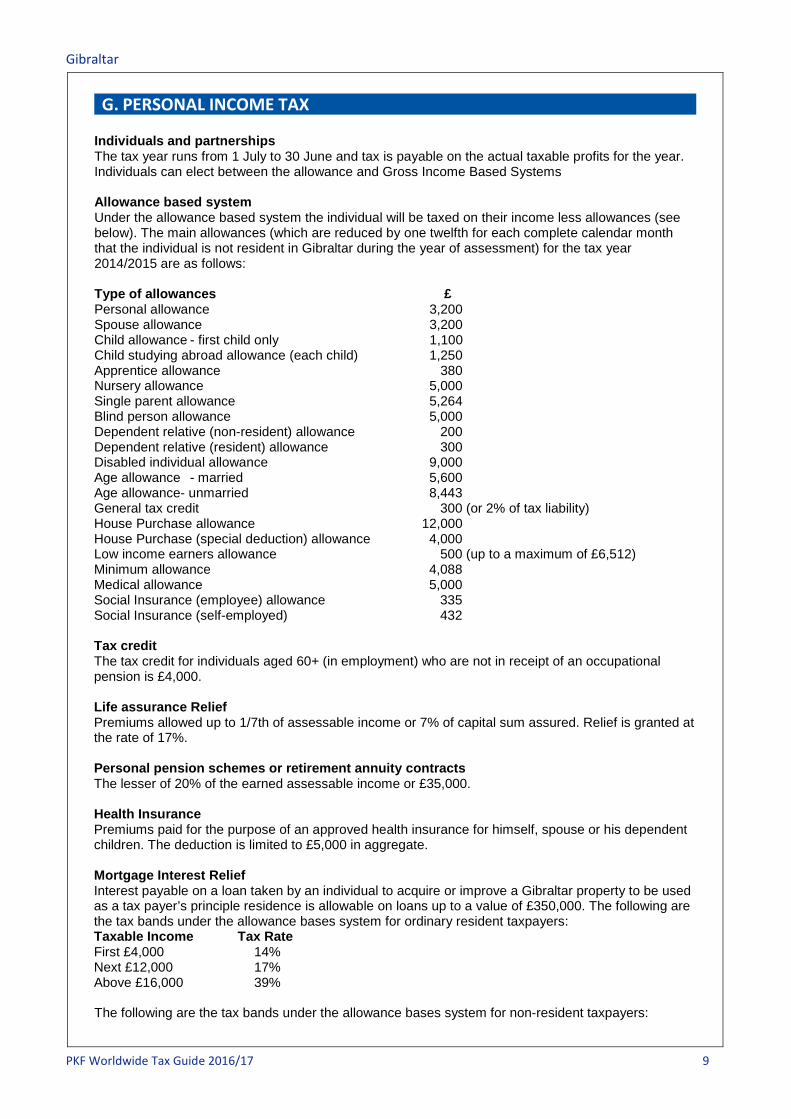

G. PERSONAL INCOME TAX Individuals and partnerships The tax year runs from 1 July to 30 June and tax is payable on the actual taxable profits for the year. Individuals can elect between the allowance and Gross Income Based Systems Allowance based system Under the allowance based system the individual will be taxed on their income less allowances (see below). The main allowances (which are reduced by one twelfth for each complete calendar month that the individual is not resident in Gibraltar during the year of assessment) for the tax year 2014/2015 are as follows: Type of allowances £ Personal allowance 3,200 Spouse allowance 3,200 Child allowance - first child only 1,100 Child studying abroad allowance (each child) 1,250 Apprentice allowance 380 Nursery allowance 5,000 Single parent allowance 5,264 Blind person allowance 5,000 Dependent relative (non-resident) allowance 200 Dependent relative (resident) allowance 300 Disabled individual allowance 9,000 Age allowance - married 5,600 Age allowance- unmarried 8,443 General tax credit 300 (or 2% of tax liability) House Purchase allowance 12,000 House Purchase (special deduction) allowance 4,000 Low income earners allowance 500 (up to a maximum of £6,512) Minimum allowance 4,088 Medical allowance 5,000 Social Insurance (employee) allowance 335 Social Insurance (self-employed) 432 Tax credit The tax credit for individuals aged 60+ (in employment) who are not in receipt of an occupational pension is £4,000. Life assurance Relief Premiums allowed up to 1/7th of assessable income or 7% of capital sum assured. Relief is granted at the rate of 17%. Personal pension schemes or retirement annuity contracts The lesser of 20% of the earned assessable income or £35,000. Health Insurance Premiums paid for the purpose of an approved health insurance for himself, spouse or his dependent children. The deduction is limited to £5,000 in aggregate. Mortgage Interest Relief Interest payable on a loan taken by an individual to acquire or improve a Gibraltar property to be used as a tax payer’s principle residence is allowable on loans up to a value of £350,000. The following are the tax bands under the allowance bases system for ordinary resident taxpayers: Taxable Income Tax Rate First £4,000 14% Next £12,000 17% Above £16,000 39% The following are the tax bands under the allowance bases system for non-resident taxpayers:

Gibraltar

PKF Worldwide Tax Guide 2016/17 10

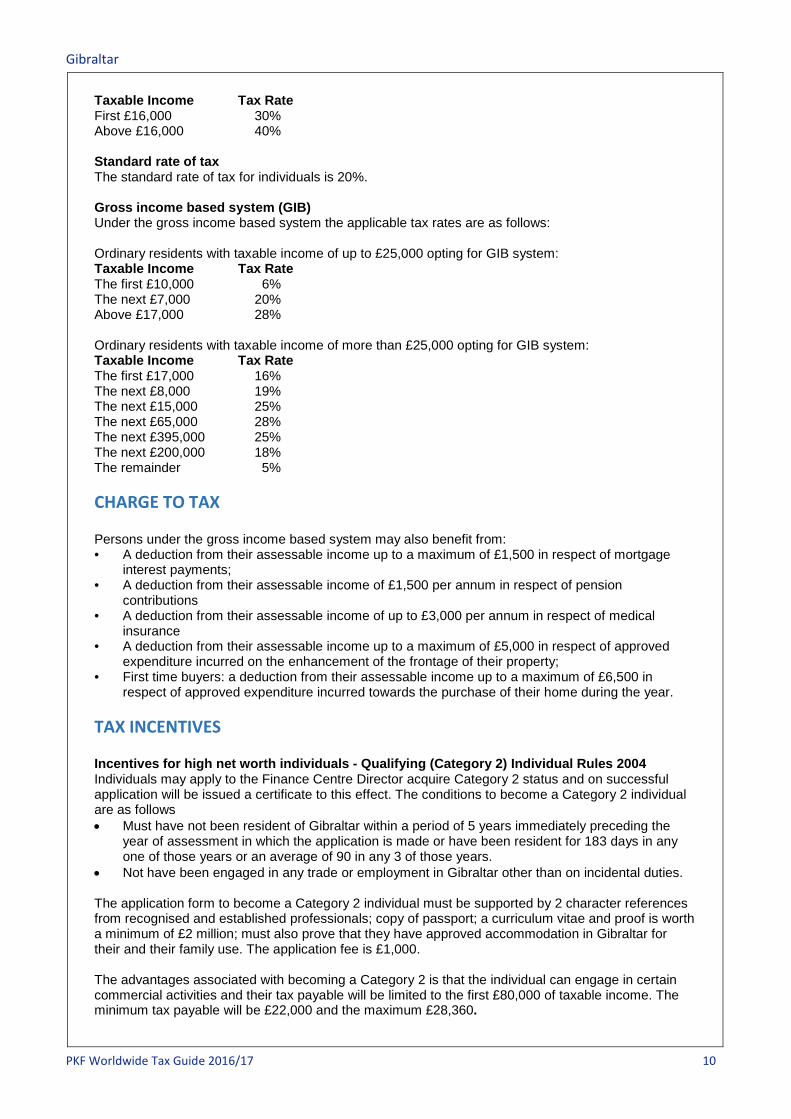

Taxable Income Tax Rate First £16,000 30% Above £16,000 40% Standard rate of tax The standard rate of tax for individuals is 20%. Gross income based system (GIB) Under the gross income based system the applicable tax rates are as follows: Ordinary residents with taxable income of up to £25,000 opting for GIB system: Taxable Income Tax Rate The first £10,000 6% The next £7,000 20% Above £17,000 28% Ordinary residents with taxable income of more than £25,000 opting for GIB system: Taxable Income Tax Rate The first £17,000 16% The next £8,000 19% The next £15,000 25% The next £65,000 28% The next £395,000 25% The next £200,000 18% The remainder 5% CHARGE TO TAX Persons under the gross income based system may also benefit from: • A deduction from their assessable income up to a maximum of £1,500 in respect of mortgage

interest payments; • A deduction from their assessable income of £1,500 per annum in respect of pension

contributions • A deduction from their assessable income of up to £3,000 per annum in respect of medical

insurance • A deduction from their assessable income up to a maximum of £5,000 in respect of approved

expenditure incurred on the enhancement of the frontage of their property; • First time buyers: a deduction from their assessable income up to a maximum of £6,500 in

respect of approved expenditure incurred towards the purchase of their home during the year. TAX INCENTIVES Incentives for high net worth individuals - Qualifying (Category 2) Individual Rules 2004 Individuals may apply to the Finance Centre Director acquire Category 2 status and on successful application will be issued a certificate to this effect. The conditions to become a Category 2 individual are as follows • Must have not been resident of Gibraltar within a period of 5 years immediately preceding the

year of assessment in which the application is made or have been resident for 183 days in any one of those years or an average of 90 in any 3 of those years.

• Not have been engaged in any trade or employment in Gibraltar other than on incidental duties. The application form to become a Category 2 individual must be supported by 2 character references from recognised and established professionals; copy of passport; a curriculum vitae and proof is worth a minimum of £2 million; must also prove that they have approved accommodation in Gibraltar for their and their family use. The application fee is £1,000. The advantages associated with becoming a Category 2 is that the individual can engage in certain commercial activities and their tax payable will be limited to the first £80,000 of taxable income. The minimum tax payable will be £22,000 and the maximum £28,360.

Gibraltar

PKF Worldwide Tax Guide 2016/17 11

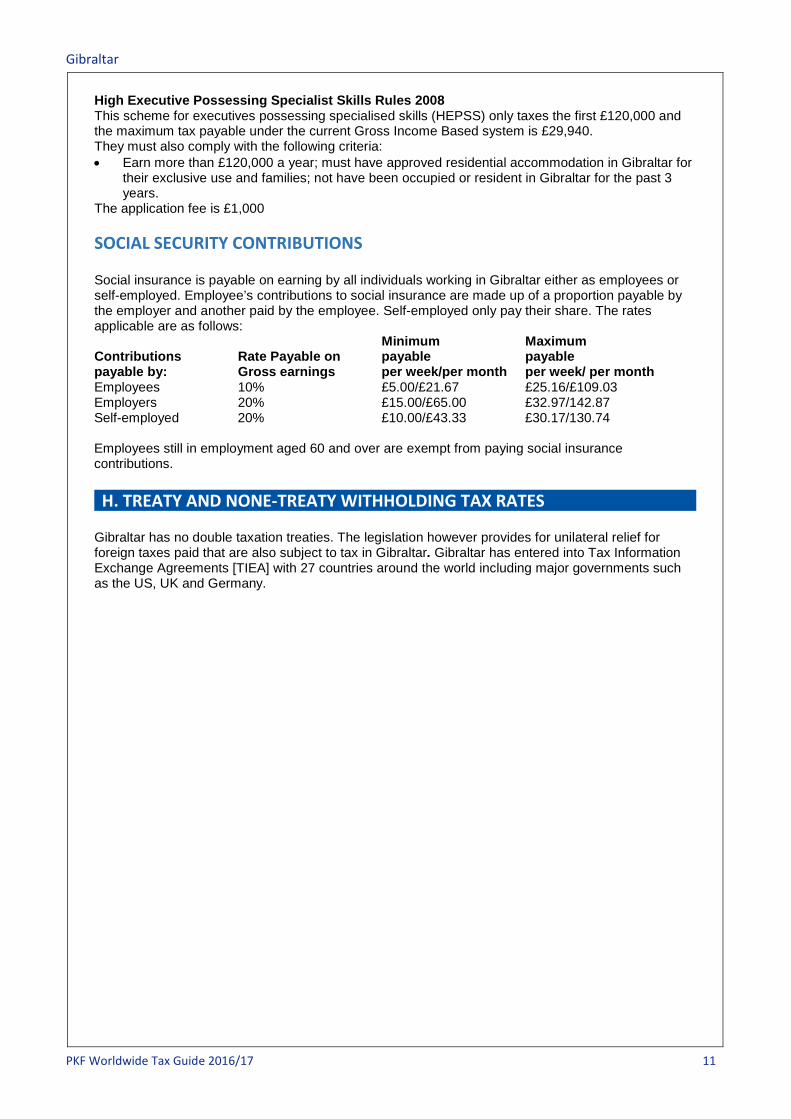

High Executive Possessing Specialist Skills Rules 2008 This scheme for executives possessing specialised skills (HEPSS) only taxes the first £120,000 and the maximum tax payable under the current Gross Income Based system is £29,940. They must also comply with the following criteria: • Earn more than £120,000 a year; must have approved residential accommodation in Gibraltar for

their exclusive use and families; not have been occupied or resident in Gibraltar for the past 3 years.

The application fee is £1,000 SOCIAL SECURITY CONTRIBUTIONS Social insurance is payable on earning by all individuals working in Gibraltar either as employees or self-employed. Employee’s contributions to social insurance are made up of a proportion payable by the employer and another paid by the employee. Self-employed only pay their share. The rates applicable are as follows: Minimum Maximum Contributions Rate Payable on payable payable payable by: Gross earnings per week/per month per week/ per month Employees 10% £5.00/£21.67 £25.16/£109.03 Employers 20% £15.00/£65.00 £32.97/142.87 Self-employed 20% £10.00/£43.33 £30.17/130.74 Employees still in employment aged 60 and over are exempt from paying social insurance contributions. H. TREATY AND NONE-TREATY WITHHOLDING TAX RATES Gibraltar has no double taxation treaties. The legislation however provides for unilateral relief for foreign taxes paid that are also subject to tax in Gibraltar. Gibraltar has entered into Tax Information Exchange Agreements [TIEA] with 27 countries around the world including major governments such as the US, UK and Germany.