getting to know brazil #2 (electoral conundrum)

TRANSCRIPT

8/7/2019 Getting to know Brazil #2 (electoral conundrum)

http://slidepdf.com/reader/full/getting-to-know-brazil-2-electoral-conundrum 1/13

Getting to Know Brazil

ANALYST CERTIFICATION AND REQUIRED DISCLOSURES BEGIN ON PAGE 9

BTG Pactual does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that the firm may have a conflict of interest that could affect the

objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.

Equities Research

Carlos Sequeira, CFA

Analyst

+55 21 3262 9223

Antonio Junqueira

Analyst

+55 21 3262 9278

Getting to Know Brazil

Brazil

Strategy

Sector Note

25 February 2010

#2 – The electoral conundrum

Brazil holds major elections in 2010

2010 is a major election year in Brazil. The country’s population of 190 million

inhabitants (more than 130 million voters) will elect a new president, 27 state

governors, 513 representatives of the Lower House, 54 senators and regional

congressmen across the nation. This is clearly a significant event for the country,

and may cause some market volatility due to its potential impacts on the micro

agenda (which we see as large) and the macro agenda (small).

The electoral process helps slow structural changes in the country

Brazil holds elections every two years. National and state elections are followed

and preceded by municipal elections. The small interval between elections

affects Congress’ efficiency in the second semester every two years. This

obviously impacts Brazil’s ability to make progress in key structural changes (the

so-called reforms), such as tax or public pension reforms. While we could be

tempted to think that municipal elections have low influence in Congress, the

opposite has proven to be the case.

Electoral rules lead to poor-quality voting and a distant Congress

Voting in Brazil is mandatory. At the same time, most Brazilian voters have too

little information, time, knowledge or motivation to take well-based voting

decisions. According to a poll, a remarkable 74% of Brazilians don’t even

remember who they voted for in the Lower House elections only four years

before the poll was taken. Another poll shows that 13% of Brazilian voters

admitted having switched votes in return for some personal benefit.

Pardon Montesquieu, but the powers are not balanced in Brazil

Despite enjoying really strong macroeconomic momentum, Brazil could

potentially grow faster if some key legal reforms are carried out. We don’t expect

this to happen in the next presidential term unless the government, which in

practical terms is much more powerful than Congress, decides to push these

reforms. We also don’t foresee a change in the balance of power anytime soon.

8/7/2019 Getting to know Brazil #2 (electoral conundrum)

http://slidepdf.com/reader/full/getting-to-know-brazil-2-electoral-conundrum 2/13

Getting to Know Brazil25 February 2010 page 2

Electoral process slows structural changes

We will debate our view on Brazil’s presidential candidates and their agendas in

the near future. This piece’s focus, though, is broader as we aim to shed light onBrazil’s electoral process and explain its impacts on Brazil’s legislative process

and the country’s slow pace of structural changes.

Some of the key reforms that Brazilian politicians have been clamoring to

approve for years have simply failed to get off the ground. Politically, the

changes are so tough to implement nowadays that debates such as the pension,

tax or political reforms are not even on Congress’ agenda this year.

In our view, the electoral process plays a key role in the speed of changes in

Brazil. The small interval between elections, mandatory voting, and the rules

determining who is elected to Congress are some of the reasons for poor-quality

voting and legislative agendas, in our view.

Figure 1: The 8-year electoral cycle in Brazil

Source: BTG Pactual

8/7/2019 Getting to know Brazil #2 (electoral conundrum)

http://slidepdf.com/reader/full/getting-to-know-brazil-2-electoral-conundrum 3/13

Getting to Know Brazil25 February 2010 page 3

The electoral cycle – mind the gap

Brazil holds elections every two years. National and state elections, which will

happen this year, are followed and preceded by municipal elections (the next

ones are in 2012). As senators have an eight-year term (compared to Lower

House members’ four-year term), the Senate elects 2/3 of its members in one

election (2010’s case) and the other 1/3 four years later (see figure 1 above).

In our view, the small 2-year gap between elections in Brazil explains part of

Brazil’s sloth in passing key legislative reforms (those with the potential to make

the country grow faster and healthier). Municipal elections, though considered

less relevant than major elections, also affect all parties and many congressmen

intending to become mayors of their hometowns.

The reality is that, due to the way politics works in Brazil, any politician wanting

to fly high knows that his/her chances are higher if they work for the government

instead of Congress. Being a mayor of one of Brazil’s key cities can leverage a

politician to become a state governor immediately after. In 2008’s election,

roughly 20% of Lower House members tried to become mayors of their

hometowns. And the vast majority of the remaining 80%, despite not trying to be

elected, worked towards electing its political allies in order to strengthen its

political groups and/or parties.

That said, every two years, in the second semester, Brazil’s attentions switch

from its legislative to its electoral process, reducing the scope for more important

(and discussed) changes. This is the reality this year. Even micro reforms, such

as the approval of draft bill #29 (which will allow incumbents such as Telemar

and Telesp to offer cable TV services), or the new proposed Oil Law , which will

change the current regulatory scope in Brazil’s pre-salt (affecting Petrobras and

OGX, only to mention Brazilian listed oil companies), may not be passed in an

electoral year (unless there is a big push by the government).

The electoral process – poor-quality voters and a distant Congress

Brazil’s electoral process has some factors that lead to both poor-quality voters

and a distant Congress. First of all, voting in Brazil is mandatory. And the

consequence in terms of voting quality is crystal clear – according to a Datafolha

poll in October 2008, 13% of all voters admitted having switched votes in

exchange for personal benefits (mostly cash). If 13% admitted to this, how many

other voters did the same but were afraid to admit to as much in the Datafolha

interview?

Also, the mandatory voting process forces many people who don’t follow politics,

have no interest and no information to make a decision they would rather not

take. According to another poll, published in the book “Reforma Política – Lições

da História Recente ”, published by FGV and written by Alberto Carlos Almeida,

74% of voters couldn’t even recall who they voted for in Brazil’s Lower House

elections four years prior to the year the poll was taken. Poor-quality voters

obviously lead to a poor-quality Congress.

8/7/2019 Getting to know Brazil #2 (electoral conundrum)

http://slidepdf.com/reader/full/getting-to-know-brazil-2-electoral-conundrum 4/13

Getting to Know Brazil25 February 2010 page 4

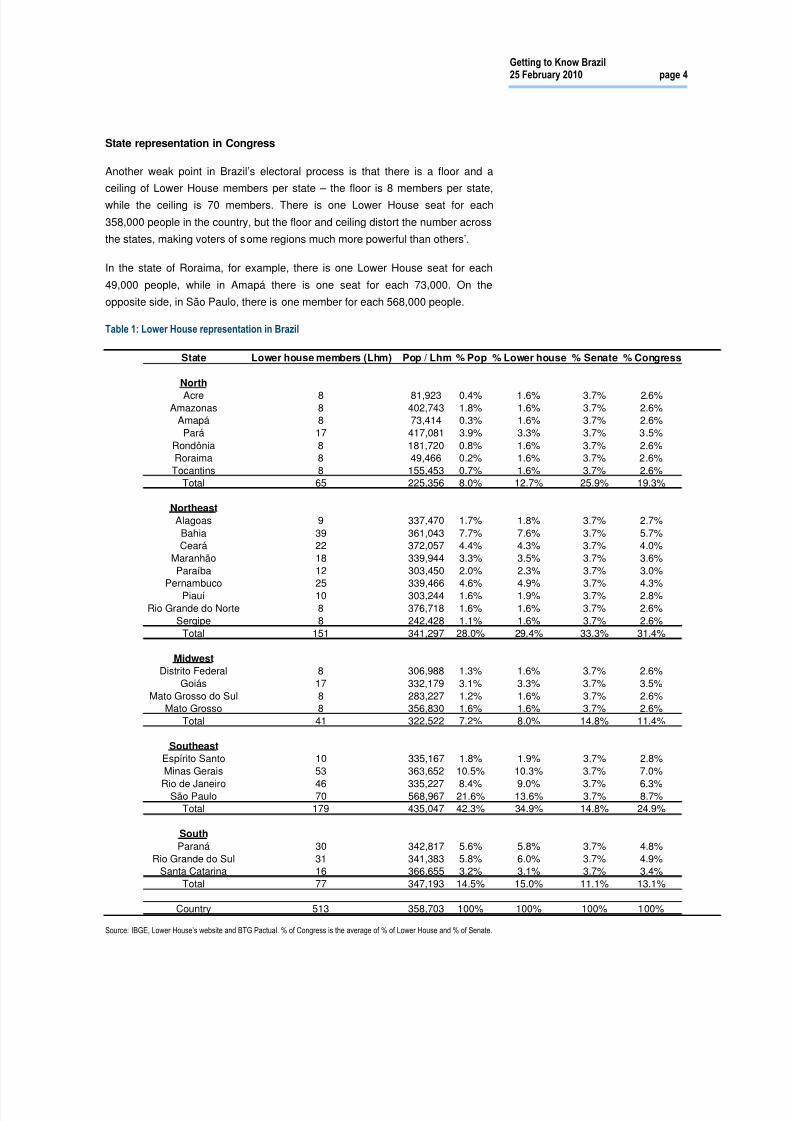

State representation in Congress

Another weak point in Brazil’s electoral process is that there is a floor and a

ceiling of Lower House members per state – the floor is 8 members per state,

while the ceiling is 70 members. There is one Lower House seat for each

358,000 people in the country, but the floor and ceiling distort the number across

the states, making voters of some regions much more powerful than others’.

In the state of Roraima, for example, there is one Lower House seat for each

49,000 people, while in Amapá there is one seat for each 73,000. On the

opposite side, in São Paulo, there is one member for each 568,000 people.

Table 1: Lower House representation in Brazil

State Lower house members (Lhm) Pop / Lhm % Pop % Lower house % Senate % Congress

North

Acre 8 81,923 0.4% 1.6% 3.7% 2.6%Amazonas 8 402,743 1.8% 1.6% 3.7% 2.6%

Amapá 8 73,414 0.3% 1.6% 3.7% 2.6%

Pará 17 417,081 3.9% 3.3% 3.7% 3.5%

Rondônia 8 181,720 0.8% 1.6% 3.7% 2.6%Roraima 8 49,466 0.2% 1.6% 3.7% 2.6%

Tocantins 8 155,453 0.7% 1.6% 3.7% 2.6%Total 65 225,356 8.0% 12.7% 25.9% 19.3%

Northeast

Alagoas 9 337,470 1.7% 1.8% 3.7% 2.7%

Bahia 39 361,043 7.7% 7.6% 3.7% 5.7%Ceará 22 372,057 4.4% 4.3% 3.7% 4.0%

Maranhão 18 339,944 3.3% 3.5% 3.7% 3.6%

Paraíba 12 303,450 2.0% 2.3% 3.7% 3.0%Pernambuco 25 339,466 4.6% 4.9% 3.7% 4.3%

Piauí 10 303,244 1.6% 1.9% 3.7% 2.8%

Rio Grande do Norte 8 376,718 1.6% 1.6% 3.7% 2.6%

Sergipe 8 242,428 1.1% 1.6% 3.7% 2.6%

Total 151 341,297 28.0% 29.4% 33.3% 31.4%

Midwest

Distrito Federal 8 306,988 1.3% 1.6% 3.7% 2.6%

Goiás 17 332,179 3.1% 3.3% 3.7% 3.5%

Mato Grosso do Sul 8 283,227 1.2% 1.6% 3.7% 2.6%Mato Grosso 8 356,830 1.6% 1.6% 3.7% 2.6%

Total 41 322,522 7.2% 8.0% 14.8% 11.4%

Southeast

Espírito Santo 10 335,167 1.8% 1.9% 3.7% 2.8%

Minas Gerais 53 363,652 10.5% 10.3% 3.7% 7.0%

Rio de Janeiro 46 335,227 8.4% 9.0% 3.7% 6.3%São Paulo 70 568,967 21.6% 13.6% 3.7% 8.7%

Total 179 435,047 42.3% 34.9% 14.8% 24.9%

South

Paraná 30 342,817 5.6% 5.8% 3.7% 4.8%

Rio Grande do Sul 31 341,383 5.8% 6.0% 3.7% 4.9%Santa Catarina 16 366,655 3.2% 3.1% 3.7% 3.4%

Total 77 347,193 14.5% 15.0% 11.1% 13.1%

Country 513 358,703 100% 100% 100% 100%

Source: IBGE, Lower House’s website and BTG Pactual. % of Congress is the average of % of Lower House and % of Senate.

8/7/2019 Getting to know Brazil #2 (electoral conundrum)

http://slidepdf.com/reader/full/getting-to-know-brazil-2-electoral-conundrum 5/13

Getting to Know Brazil25 February 2010 page 5

A rough calculation shows that each Roraima voter is 11 times more powerful

than a São Paulo voter in terms of determining the composition of Brazil’s Lower

House. The floor and ceiling levels, by trying to strengthen states in the Lower

House, approximates the Lower House concept to the Senate’s. And the

consequence of that is a Congress that doesn’t reflect the country’s

proportionality.

Considering both the Lower House and the Senate, the Northern region of Brazil,

for example, accounts for 19% of Congress, despite having only 8% of the

population. That’s an impressive 11% gap. The rich and dense Southeast region,

home to Rio and São Paulo, have 42.3% of Brazil’s population, but only 34.9% of

the Lower House and 25% of Congress.

Should voters choose parties or candidates?

In 2006, Brazil elected the current 513 Lower House members. At the time they

took office, these members came from 20 different parties. The biggest party

(PMDB) elected only 17.5% of the members, while the top 4 (PMDB, PT, PSDB

and DEM) elected 58%. Members of liberal, social, communist, republican and

workers’ parties, as well as many other fronts, gained seats in Congress.

With so many different political ideologies decently represented in Congress, one

could think that Brazil’s population has a well (and quasi-equally) diversified

political thinking. However, that’s not true. Although Brazil does have many

ideologies, the reality is that parties don’t follow a strict agenda, and share the

same views on many subjects.

That said, Brazil’s electoral law aims to strengthen the parties, and not the

candidates. Let’s take São Paulo as an example. The state has 70 Lower House

seats, but the 70 elected members weren’t the 70 that got more votes. In 2006,

the 70th

most voted candidate didn’t get in, while the 226th

did. In the 2002

elections, the discrepancy was even larger. The 634th

most voted candidate, who

got only 275 votes, was elected to Congress, while more than 560 candidates

who obtained more votes couldn’t get a seat.

But how does that happen? Rules in Brazil imply that for all the Legislative seats

in the country (except the Senate), the votes go to the parties (or coalition of

parties) instead of the candidates. In São Paulo, for example, where each

568,000 people (roughly 388,000 voters) elect one Lower House member, if one

party gets 776k votes, it is entitled to two seats (776/2 = 388). It doesn’t matter if

one of the candidates gets 775,000 votes and another one gets only 1,000 – the

party will still have two seats in the Lower House.

Although we agree with some measures that aim to strengthen parties in the

country, such as removing a politician from his/her seat when he/she decides to

change party in a specific timeframe after the elections, the above concept,

combined with the fact that Brazil has more than 20 parties, creates all types of

political distortions – the main distortion is the one mentioned above. In 2002,

each vote that the 634th

most voted candidate obtained held much more sway

than those of each and every candidate who obtained more votes.

8/7/2019 Getting to know Brazil #2 (electoral conundrum)

http://slidepdf.com/reader/full/getting-to-know-brazil-2-electoral-conundrum 6/13

Getting to Know Brazil25 February 2010 page 6

Pardon Montesquieu, but the powers are not balanced in Brazil

The Legislative is not a strong governmental force in Brazil. There are some

reasons for this, such as education and how misconduct is punished. The

electoral process, in our view, also plays a key role. The Legislative would be

stronger, we think, if the electoral process changes in a way to face the

challenges discussed in the note.

A stronger Congress would probably be able to handle more interesting agendas

and help push growth. Today most relevant changes are normally proposed and

pushed by the Executive. In other words, the country is dependent on the

government to propose an agenda with the potential to speed up Brazil’s growth.

8/7/2019 Getting to know Brazil #2 (electoral conundrum)

http://slidepdf.com/reader/full/getting-to-know-brazil-2-electoral-conundrum 7/13

8/7/2019 Getting to know Brazil #2 (electoral conundrum)

http://slidepdf.com/reader/full/getting-to-know-brazil-2-electoral-conundrum 8/13

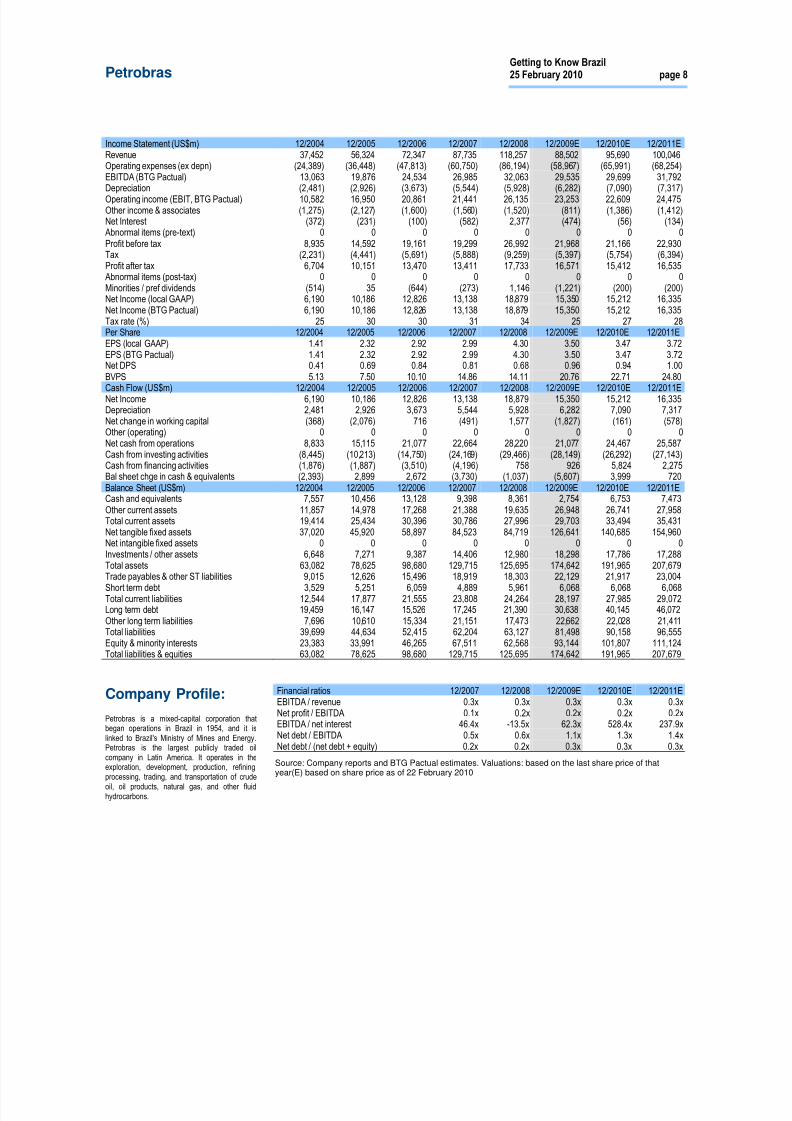

PetrobrasGetting to Know Brazil25 February 2010 page 8

Petrobras

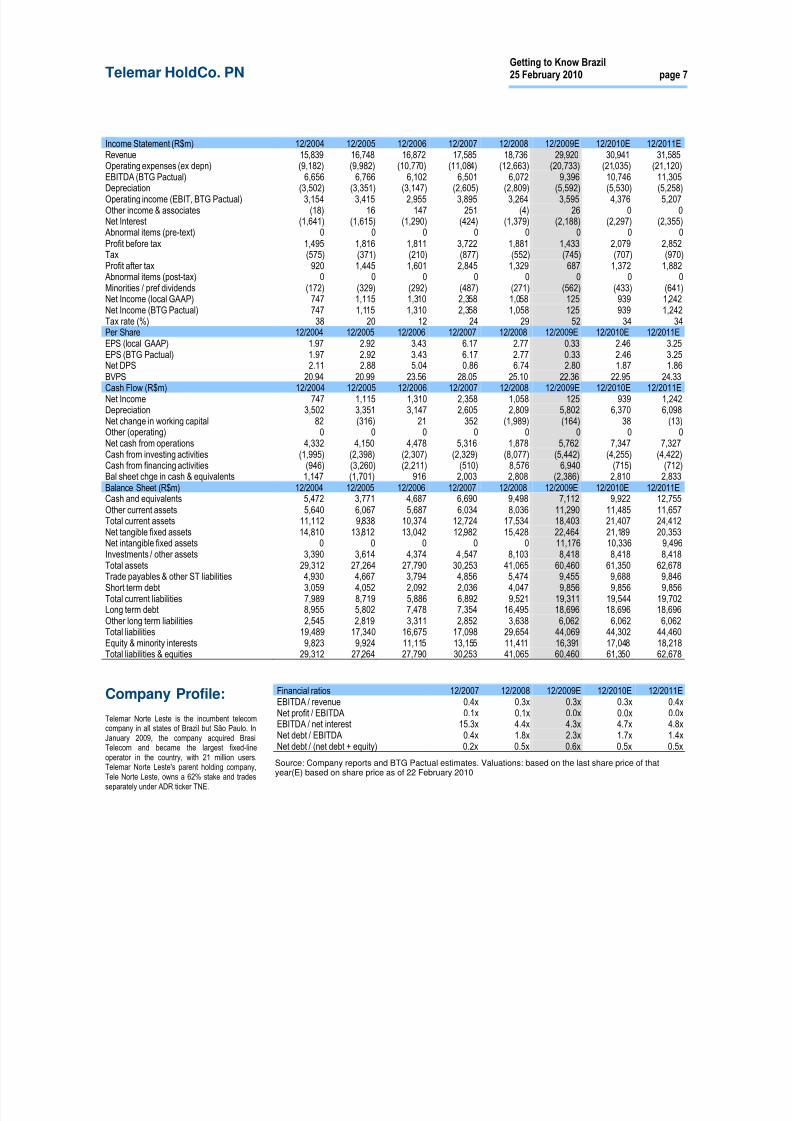

Income Statement (US$m) 12/2004 12/2005 12/2006 12/2007 12/2008 12/2009E 12/2010E 12/2011ERevenue 37,452 56,324 72,347 87,735 118,257 88,502 95,690 100,046Operating expenses (ex depn) (24,389) (36,448) (47,813) (60,750) (86,194) (58,967) (65,991) (68,254)EBITDA (BTG Pactual) 13,063 19,876 24,534 26,985 32,063 29,535 29,699 31,792Depreciation (2,481) (2,926) (3,673) (5,544) (5,928) (6,282) (7,090) (7,317)

Operating income (EBIT, BTG Pactual) 10,582 16,950 20,861 21,441 26,135 23,253 22,609 24,475Other income & associates (1,275) (2,127) (1,600) (1,560) (1,520) (811) (1,386) (1,412)Net Interest (372) (231) (100) (582) 2,377 (474) (56) (134)Abnormal items (pre-text) 0 0 0 0 0 0 0 0Profit before tax 8,935 14,592 19,161 19,299 26,992 21,968 21,166 22,930Tax (2,231) (4,441) (5,691) (5,888) (9,259) (5,397) (5,754) (6,394)Profit after tax 6,704 10,151 13,470 13,411 17,733 16,571 15,412 16,535Abnormal items (post-tax) 0 0 0 0 0 0 0 0Minorities / pref dividends (514) 35 (644) (273) 1,146 (1,221) (200) (200)Net Income (local GAAP) 6,190 10,186 12,826 13,138 18,879 15,350 15,212 16,335Net Income (BTG Pactual) 6,190 10,186 12,826 13,138 18,879 15,350 15,212 16,335Tax rate (%) 25 30 30 31 34 25 27 28Per Share 12/2004 12/2005 12/2006 12/2007 12/2008 12/2009E 12/2010E 12/2011EEPS (local GAAP) 1.41 2.32 2.92 2.99 4.30 3.50 3.47 3.72EPS (BTG Pactual) 1.41 2.32 2.92 2.99 4.30 3.50 3.47 3.72Net DPS 0.41 0.69 0.84 0.81 0.68 0.96 0.94 1.00BVPS 5.13 7.50 10.10 14.86 14.11 20.76 22.71 24.80

Cash Flow (US$m) 12/2004 12/2005 12/2006 12/2007 12/2008 12/2009E 12/2010E 12/2011ENet Income 6,190 10,186 12,826 13,138 18,879 15,350 15,212 16,335Depreciation 2,481 2,926 3,673 5,544 5,928 6,282 7,090 7,317Net change in working capital (368) (2,076) 716 (491) 1,577 (1,827) (161) (578)Other (operating) 0 0 0 0 0 0 0 0Net cash from operations 8,833 15,115 21,077 22,664 28,220 21,077 24,467 25,587Cash from investing activities (8,445) (10,213) (14,750) (24,169) (29,466) (28,149) (26,292) (27,143)Cash from financing activities (1,876) (1,887) (3,510) (4,196) 758 926 5,824 2,275Bal sheet chge in cash & equivalents (2,393) 2,899 2,672 (3,730) (1,037) (5,607) 3,999 720Balance Sheet (US$m) 12/2004 12/2005 12/2006 12/2007 12/2008 12/2009E 12/2010E 12/2011ECash and equivalents 7,557 10,456 13,128 9,398 8,361 2,754 6,753 7,473Other current assets 11,857 14,978 17,268 21,388 19,635 26,948 26,741 27,958Total current assets 19,414 25,434 30,396 30,786 27,996 29,703 33,494 35,431Net tangible fixed assets 37,020 45,920 58,897 84,523 84,719 126,641 140,685 154,960Net intangible fixed assets 0 0 0 0 0 0 0 0Investments / other assets 6,648 7,271 9,387 14,406 12,980 18,298 17,786 17,288Total assets 63,082 78,625 98,680 129,715 125,695 174,642 191,965 207,679Trade payables & other ST liabilities 9,015 12,626 15,496 18,919 18,303 22,129 21,917 23,004

Short term debt 3,529 5,251 6,059 4,889 5,961 6,068 6,068 6,068Total current liabilities 12,544 17,877 21,555 23,808 24,264 28,197 27,985 29,072Long term debt 19,459 16,147 15,526 17,245 21,390 30,638 40,145 46,072Other long term liabilities 7,696 10,610 15,334 21,151 17,473 22,662 22,028 21,411Total liabilities 39,699 44,634 52,415 62,204 63,127 81,498 90,158 96,555Equity & minority interests 23,383 33,991 46,265 67,511 62,568 93,144 101,807 111,124Total liabilities & equities 63,082 78,625 98,680 129,715 125,695 174,642 191,965 207,679

Company Profile:

Petrobras is a mixed-capital corporation thatbegan operations in Brazil in 1954, and it islinked to Brazil's Ministry of Mines and Energy.Petrobras is the largest publicly traded oilcompany in Latin America. It operates in theexploration, development, production, refining,processing, trading, and transportation of crude

oil, oil products, natural gas, and other fluidhydrocarbons.

Financial ratios 12/2007 12/2008 12/2009E 12/2010E 12/2011EEBITDA / revenue 0.3x 0.3x 0.3x 0.3x 0.3xNet profit / EBITDA 0.1x 0.2x 0.2x 0.2x 0.2xEBITDA / net interest 46.4x -13.5x 62.3x 528.4x 237.9xNet debt / EBITDA 0.5x 0.6x 1.1x 1.3x 1.4xNet debt / (net debt + equity) 0.2x 0.2x 0.3x 0.3x 0.3x

Source: Company reports and BTG Pactual estimates. Valuations: based on the last share price of thatyear(E) based on share price as of 22 February 2010

8/7/2019 Getting to know Brazil #2 (electoral conundrum)

http://slidepdf.com/reader/full/getting-to-know-brazil-2-electoral-conundrum 9/13

Getting to Know Brazil25 February 2010 page 9

Required Disclosures

This report has been prepared by Banco BTG Pactual S.A. The figures contained in performance charts refer to the past;past performance is not a reliable indicator of future results. Additional information will be made available upon request.

BTG PactualRating

Definition Coverage *1 IB Services *2

Buy Expected total return 10% above the company’ssector average.

49% 73%

Neutral Expected total return between +10% and -10%the company’s sector average.

43% 53%

Sell Expected total return 10% below the company’ssector average.

8% 50%

1: Percentage of companies under coverage globally within the 1 2-month rating category.

2: Percentage of companies within the 12-month rating category for which investment banking (IB) services wereprovided within the past 12 months.

Absolute return requirements

Besides the abovementioned relative return requirements, the listed absolute return requirements must be follo wed:

a) a Buy rated stock must have an expected total return above 15%

b) a Neutral rated stock can not have an expected total return below -5%

c) a stock with expected total return above 50% must be rated Buy

Analyst Certification

Each research analyst primarily responsible for the content of this investment research report, in whole or in part, herebycertifies that:

- all of the views expressed accurately reflect his or her personal views about those securities or issuers, and suchrecommendations were elaborated independently, including in relation to Banco BTG Pactual S.A. and/or its affiliates, asthe case may be;

- no part of his or her compensation was, is, or will be, directly or indirectly, related to the any specific recommendationsor or views contained herein or linked to the pricing of any of the securities discussed herein.

Research analysts contributing to this report who are employed by a non-US Broker dealer are not registered/qualified asresearch analysts with the NASD and NYSE and therefore are not subject to the restrictions contained in the NASD andNYSE rules on communications with a subject company, public appearances, and trading securities held by a researchanalyst account.

Other Disclaimers

Brazilian Regulation CVM 388

Each research analyst primarily responsible for the content of this investment research report, in

whole or in part, certifies that:

- all of the views expressed accurately reflect his or her personal views about those securities or

issuers, and such recommendations were elaborated independently, including in relation to Banco BTG Pactual S.A., asthe case may be;

- no relationship is maintained with any person who works for the subject companies which securities are mentioned onthis research;

- Banco BTG Pactual S.A. and/or its affiliates (including the funds, portfolios and investment clubs in securities managedby them) do not own directly or indirectly 1% or more of the total capital of the subject company(ies) NET Serviços SA,OGX Petroleo e Gas Participacoes S/A, Petroleo Brasileiro - Petrobras, Tele Norte Leste Participações SA PN, TelespFixed;

- does not hold, directly or indirectly securities of the subject companies which represent 5% or more of his or her networth, and is not involved in the acquisition , alienation or intermediation of such securities in the market;

- does not receive compensation for any services rendered or presents any commercial relationships with any of thesubject companies or person, entity or any kind of funds which represents the same interest of the subject companies;

- no part of any of the research analyst's compensation was, is, or will be directly or indirectly related to the pricing of anyof the securities issued by any of the subject companies and/or to the specific recommendations or views expressed bythe research analyst in this research although part of the analyst's compensation comes from the profits of Banco BTGPactual S.A. and/or its affiliates and, consequently, revenues arisen from transactions held by Banco BTG Pactual S.A.and/or its affiliates

- Banco BTG Pactual S.A. and/or its affiliates receive compensation for any services rendered or presents anycommercial relationships with the subject company(ies) NET Serviços SA, OGX Petroleo e Gas Participacoes S/A,Petroleo Brasileiro - Petrobras, Telesp Fixed or person, entity or any kind of funds which represents the same interest ofsubject company(ies);

- Banco BTG Pactual S.A. and/or its affiliates does not receive compensation for any services rendered or presents anycommercial relationships with the subject company(ies) Tele Norte Leste Participações SA PN or person, entity or anykind of funds which represents the same interest of subject company(ies);

- Banco BTG Pactual S.A. and/or its affiliates are not involved in the acquisition, alienation or intermediation of thesecurities of the subject company(ies) NET Serviços SA, OGX Petroleo e Gas Participacoes S/A, Petroleo Brasileiro -Petrobras, Tele Norte Leste Participações SA PN, Telesp Fixed in the market;

Statement of Risk

8/7/2019 Getting to know Brazil #2 (electoral conundrum)

http://slidepdf.com/reader/full/getting-to-know-brazil-2-electoral-conundrum 10/13

Getting to Know Brazil25 February 2010 page 10

We believe the key risks are additional competition and regulatory issues. In addition, there are potential risks inherent ininvesting in emerging market countries. Potential emerging market related risks include, but are not limited to, the volatilenature of the currency, regulatory and sociopolitical risk, and abrupt potential changes in the cost of capital and economicgrowth outlook. Valuations can also be affected by "contagion" from developments in other emerging markets.

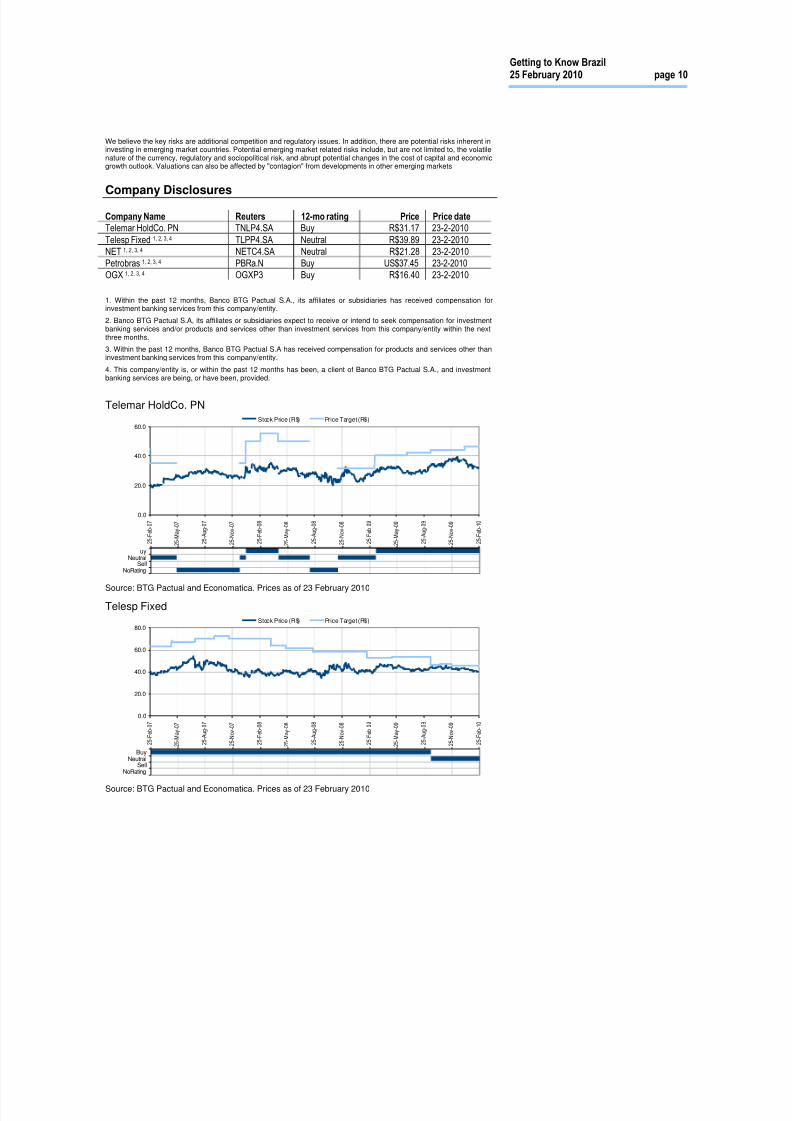

Company DisclosuresCompany Name Reuters 12-mo rating Price Price date Telemar HoldCo. PN TNLP4.SA Buy R$31.17 23-2-2010Telesp Fixed 1, 2, 3, 4 TLPP4.SA Neutral R$39.89 23-2-2010NET 1, 2, 3, 4 NETC4.SA Neutral R$21.28 23-2-2010Petrobras 1, 2, 3, 4 PBRa.N Buy US$37.45 23-2-2010OGX 1, 2, 3, 4 OGXP3 Buy R$16.40 23-2-2010

1. Within the past 12 months, Banco BTG Pactual S.A., its affiliates or subsidiaries has received compensation forinvestment banking services from this company/entity.

2. Banco BTG Pactual S.A, its affiliates or subsidiaries expect to receive or intend to seek compensation for investmentbanking services and/or products and services other than investment services from this company/entity within the nextthree months.

3. Within the past 12 months, Banco BTG Pactual S.A has received compensation for products and services other thaninvestment banking services from this company/entity.

4. This company/entity is, or within the past 12 months has been, a client of Banco BTG Pactual S.A., and investmentbanking services are being, or have been, provided.

Telemar HoldCo. PN

BuyNeutral

SellNoRating

0.0

20.0

40.0

60.0

25-Feb-07

25-May-07

25-Aug-07

25-Nov-07

25-Feb-08

25-May-08

25-Aug-08

25-Nov-08

25-Feb-09

25-May-09

25-Aug-09

25-Nov-09

25-Feb-10

Stock Price (R$) Price Target (R$)

Source: BTG Pactual and Economatica. Prices as of 23 February 2010

Telesp Fixed

BuyNeutral

SellNoRating

0.0

20.0

40.0

60.0

80.0

25-Feb-07

25-May-07

25-Aug-07

25-Nov-07

25-Feb-08

25-May-08

25-Aug-08

25-Nov-08

25-Feb-09

25-May-09

25-Aug-09

25-Nov-09

25-Feb-10

Stock Price (R$) Price Target (R$)

Source: BTG Pactual and Economatica. Prices as of 23 February 2010

8/7/2019 Getting to know Brazil #2 (electoral conundrum)

http://slidepdf.com/reader/full/getting-to-know-brazil-2-electoral-conundrum 11/13

Getting to Know Brazil25 February 2010 page 11

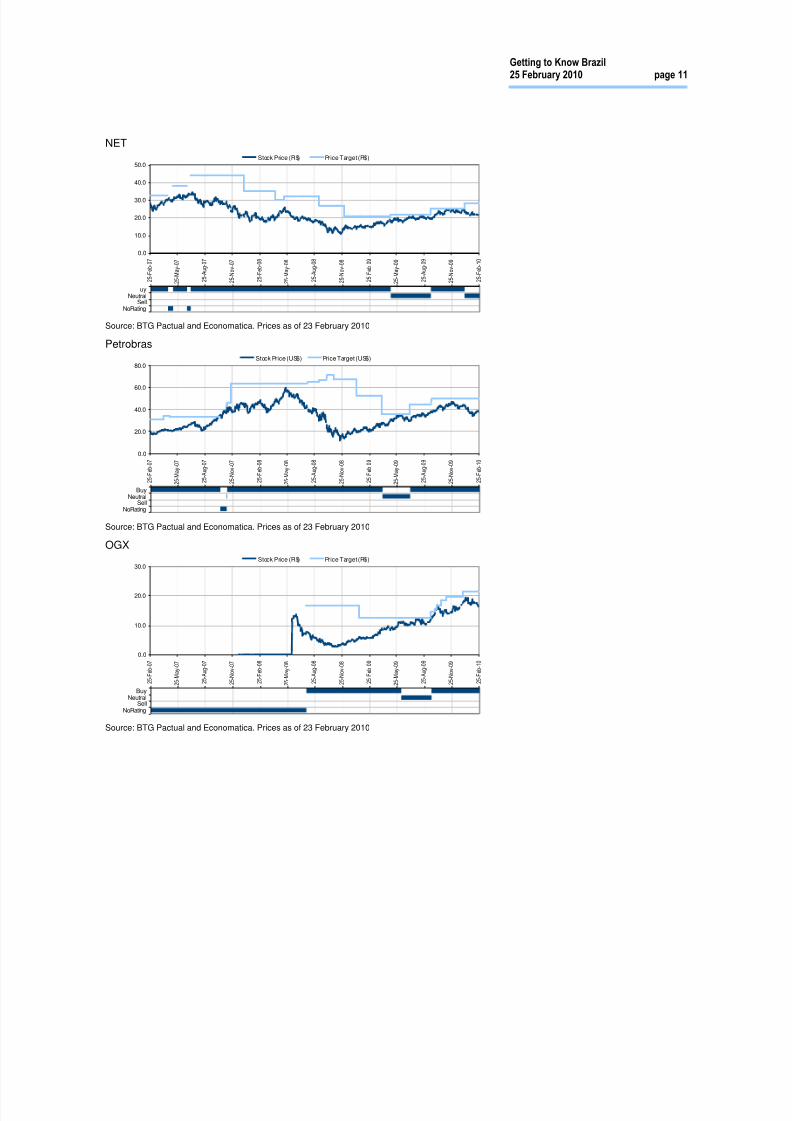

NET

BuyNeutral

SellNoRating

0.0

10.0

20.0

30.0

40.0

50.0

25-Feb-07

25-May-07

25-Aug-07

25-Nov-07

25-Feb-08

25-May-08

25-Aug-08

25-Nov-08

25-Feb-09

25-May-09

25-Aug-09

25-Nov-09

25-Feb-10

Stock Price (R$) Price Target (R$)

Source: BTG Pactual and Economatica. Prices as of 23 February 2010

Petrobras

BuyNeutral

SellNoRating

0.0

20.0

40.0

60.0

80.0

25-Feb-07

25-May-07

25-Aug-07

25-Nov-07

25-Feb-08

25-May-08

25-Aug-08

25-Nov-08

25-Feb-09

25-May-09

25-Aug-09

25-Nov-09

25-Feb-10

Stock Price (US$) Price Target (US$)

Source: BTG Pactual and Economatica. Prices as of 23 February 2010

OGX

BuyNeutral

SellNoRating

0.0

10.0

20.0

30.0

25-Feb-07

25-May-07

25-Aug-07

25-Nov-07

25-Feb-08

25-May-08

25-Aug-08

25-Nov-08

25-Feb-09

25-May-09

25-Aug-09

25-Nov-09

25-Feb-10

Stock Price (R$) Price Target (R$)

Source: BTG Pactual and Economatica. Prices as of 23 February 2010

8/7/2019 Getting to know Brazil #2 (electoral conundrum)

http://slidepdf.com/reader/full/getting-to-know-brazil-2-electoral-conundrum 12/13

Getting to Know Brazil25 February 2010 page 12

Global Disclaimer

This report has been prepared by Banco BTG Pactual S.A. (“BTG Pactual”). BTG Pactual US Capital Corp. (“BTG”), abroker-dealer registered with the U.S. Securities and Exchange Commission and a member of the Financial IndustryRegulatory Authority and the Securities Investor Protection Corporation, is distributing this report in the United States.

BTG assumes responsibility for this research for purposes of U.S. law. Any U.S. person receiving this report and wishingto effect any transaction in a security discussed in this report should do so with BTG at 212-293-4600, 623 Fifth Avenue,New York, NY 10022-6831. BTG Pactual Europe LLP (“BTG UK”), a firm regulated and authorised by the FinancialServices Authority, is distributing this report in the United Kingdom and elsewhere in the European Economic Area [deleteif not FSA-authorised].

References herein to BTG include BTG Pactual and BTG UK, as applicable.

This report is for distribution only under such circumstances as may be permitted by applicable law. This report is notdirected at you if BTG is prohibited or restricted by any legislation or regulation in any jurisdiction from making it availableto you. You should satisfy yourself before reading it that BTG is permitted to provide research material concerninginvestments to you under relevant legislation and regulations.

Nothing in this report constitutes a representation that any investment strategy or recommendation contained herein issuitable or appropriate to a recipient’s individual circumstances or otherwise constitutes a personal recommendation. It ispublished solely for information purposes, it does not constitute an advertisement and is not to be construed as asolicitation, offer, invitation or inducement to buy or sell any securities or related financial instruments in any jurisdiction.Prices in this report are believed to be reliable as of the date on which this report was issued and are derived from one ormore of the following: (i) sources as expressly specified alongside the relevant data; (ii) the quoted price on the mainregulated market for the security in question; (iii) other public sources believed to be reliable; or (iv) BTG's proprietarydata or data available to BTG. All other information herein is believed to be reliable as of the date on which this reportwas issued and has been obtained from public sources believed to be reliable. No representation or warranty, eitherexpress or implied, is provided in relation to the accuracy, completeness or reliability of the information contained herein,except with respect to information concerning BTG Pactual, its subsidiaries and affiliates, nor is it intended to be acomplete statement or summary of the securities, markets or developments referred to in the report. In all cases,

investors should conduct their own investigation and analysis of such information before taking or omitting to take anyaction in relation to securities or markets that are analyzed in this report.

BTG does not undertake that investors will obtain profits, nor will it share with investors any investment profits nor acceptany liability for any investment losses. Investments involve risks and investors should exercise prudence in making theirinvestment decisions. BTG accepts no fiduciary duties to recipients of this report and in communicating this report is notacting in a fiduciary capacity. The report should not be regarded by recipients as a substitute for the exercise of their ownjudgment. Opinions, estimates, and projections expressed herein constitute the current judgment of the analystresponsible for the substance of this report as of the date in which was issued and are therefore subject to changewithout notice and may differ or be contrary to opinions expressed by other business areas or groups of BTG as a resultof using different assumptions and criteria. Any such opinions, estimates, and projections must not be construed as arepresentation that the matters referred to therein will occur. Prices and availability of financial instruments are indicativeonly and subject to change without notice.

Research will initiate, update and cease coverage solely at the discretion of BTG Investment Bank ResearchManagement. The analysis contained herein is based on numerous assumptions. Different assumptions could result inmaterially different results. The analyst(s) responsible for the preparation of this report may interact with trading deskpersonnel, sales personnel and other constituencies for the purpose of gathering, synthesizing and interpreting marketinformation. BTG is under no obligation to update or keep current the information contained herein, except whenterminating coverage of the companies discussed in the report. BTG relies on information barriers to control the flow ofinformation contained in one or more areas within BTG, into other areas, units, groups or affiliates of BTG. Thecompensation of the analyst who prepared this report is determined by research management and senior management(not including investment banking). Analyst compensation is not based on investment banking revenues, however,compensation may relate to the revenues of BTG Investment Bank as a whole, of which investment banking, sales andtrading are a part.

The securities described herein may not be eligible for sale in all jurisdictions or to certain categories of investors.Options, derivative products and futures are not suitable for all investors, and trading in these instruments is consideredrisky. Mortgage and asset-backed securities may involve a high degree of risk and may be highly volatile in response tofluctuations in interest rates and other market conditions. Past performance is not necessarily indicative of future results.If a financial instrument is denominated in a currency other than an investor’s currency, a change in rates of exchangemay adversely affect the value or price of or the income derived from any security or related instrument mentioned in thisreport, and the reader of this report assumes any currency risk.

This report does not take into account the investment objectives, financial situation or particular needs of any particularinvestor. Investors should obtain independent financial advice based on their own particular circumstances beforemaking an investment decision on the basis of the information contained herein. For investment advice, trade executionor other enquiries, clients should contact their local sales representative. Neither BTG nor any of its affiliates, nor any oftheir respective directors, employees or agents, accepts any liability for any loss or damage arising out of the use of all orany part of this report.

Any prices stated in this report are for information purposes only and do not represent valuations for individual securitiesor other instruments. There is no representation that any transaction can or could have been effected at those prices andany prices do not necessarily reflect BTG Pactual’s internal books and records or theoretical model-based valuations andmay be based on certain assumptions. Different assumptions, by BTG Pactual or any other source, may yieldsubstantially different results.

This report may not be reproduced or redistributed to any other person, in whole or in part, for any purpose, without theprior written consent of BTG Pactual and BTG accepts no liability whatsoever for the actions of third parties in thisrespect.

Additional information relating to the financial instruments discussed in this report is available upon request.Opinions, estimates, and projections expressed herein constitute the current judgment of the analyst responsible for thesubstance of this report as of the date in which was issued and are therefore subject to change without notice and maydiffer or be contrary to opinions expressed by other business areas or groups of BTG as a result of using differentassumptions and criteria.

Because the personal views of analysts may differ from one another, BTG, BTG Pactual, its subsidiaries and affiliatesmay have issued or may issue reports that are inconsistent with, and/or reach different conclusions from, the informationpresented herein.

BTG and its affiliates have in place arrangements to manage conflicts of interest that may arise between them and theirrespective clients and among their different clients. BTG and its affiliates are involved in a full range of financial andrelated services including banking, investment banking and the provision of investment services. As such, any of BTG orits affiliates may have a material interest or a conflict of interest in any services provided to clients by BTG or suchaffiliate. Business areas within BTG and among its affiliates operate independently of each other and restrict access bythe particular individual(s) responsible for handling client affairs to certain areas of information where this is necessary inorder to manage conflicts of interest or material interests.

Any of BTG and its affiliates may: (a) have other business relationships, including investment banking relationships, withthe companies, or related entities, that are analyzed in this report; (b) be a financial adviser to the companies, or relatedentities, that are analyzed in this report, or be acting for such entities in a takeover bid by or for any of them; (c) produce

8/7/2019 Getting to know Brazil #2 (electoral conundrum)

http://slidepdf.com/reader/full/getting-to-know-brazil-2-electoral-conundrum 13/13

Getting to Know Brazil25 February 2010 page 13

this report pursuant to an agreement with any company that is analyzed in this report; (d) have disclosed this report tocompanies that are analyzed herein and subsequently amended this report prior to publication; (e) give investment adviceor provide other services to another person about or concerning any securities that are discussed in this report, whichadvice may not necessarily be consistent with or similar to the information in this report; (f) act as first purchaser,underwriter, manager or arranger and/or buy, offer, place or sell securities as principal or as agent, in relation to securitiesthat are discussed in this report; (g) trade (or have traded) for its own account (or for or on behalf of clients), have ei ther along or short position in the securities that are discussed in this report (and may buy or sell such securities), or otherwisepursue its legitimate business as a market maker or dealer (including entering into an agreement for the underwriting ofan issue of financial ins truments) in connection with the securities that are discussed i n this report; and/or (h) buy and sellunits in a collective investment scheme where it is the trustee or operator (or an adviser) to the scheme, which units mayreference securities that are discussed in this report.

Any director, employee or agent of any of BTG or its affiliates may receive remuneration that is tied to investment bankingtransactions performed by BTG or an affiliate, and/or may, although not involved in the preparation of this report, beaware of conflicts of interests of BTG or an affiliate in relation to securities or companies discussed in this report that havenot been disclosed by the individuals involved in the preparation of this report.

This report is for distribution only to persons who (i) have professional experience in matters relating to investments fallingwithin Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (as amended, the"Financial Promotion Order"), (ii) are persons falling within Article 49(2)(a) to (d) ("high net worth companies,unincorporated associations etc") of the Financial Promotion Order, (iii) are outside the United Kingdom, or (iv) arepersons to whom an invitation or inducement to engage in investment activity (within the meaning of section 21 of theFinancial Services and Markets Act 2000) in connection with the issue or sale of any securities may otherwise lawfully becommunicated or caused to be communicated (all such persons together being referred to as "relevant persons"). Thisreport is directed only at relevant persons and must not be acted on or relied on by persons who ar e not relevant persons.Any investment or investment activity to which this report re lates is available only to relevant persons and will be engagedin only with relevant persons.