genneia s.a

TRANSCRIPT

GENNEIA S.A.

Consolidated Financial Statements as of December 31, 2013, 2012 and 2011

Report of Independent Public Accountants

GENNEIA S.A.

CONSOLIDATED FINANCIAL STATEMENTS AS OF DECEMBER 31, 2013, 2012 AND 2011

Index

- Consolidated balance sheets 1

- Consolidated statements of profit and loss and other comprehensive income 2

- Consolidated statements of changes in shareholders’ equity 3

- Consolidated statements of cash flow 4

- Notes to the consolidated financial statements:

1. Background and business of the Company 5

2. Basis of preparation of the consolidated financial statements 6

3. Summary of significant accounting policies 8

4. Critical judgments in applying accounting policies 15

5. Detail of the main accounts of the consolidated financial statements 16

6. Balances and transactions with related parties 28

7. Financial instruments 30

8. Capital stock 33

9. Financing 34

10. Operating leases 38

11. Key management compensation 38

12. Major contingencies, claims, contractual commitments and other relevant agreements 38

13. Regulatory framework 44

14. Consolidated business segment information 45

15. Subsequent events 46

16. Approval of the consolidated financial statements 46

1

GENNEIA S.A.

CONSOLIDATED BALANCE SHEETS AS OF DECEMBER 31, 2013, 2012 AND 2011

(amounts expressed in thousands of Argentine pesos - Note 3.1)

2013 2012 2011

Current Assets

Cash (Note 5.a) 31,591 11,924 19,671

Investments (Note 5.b) 113,767 708 23,117

Trade receivables (Note 5.c) 476,927 313,871 207,366

Other receivables (Note 5.d) 51,466 92,467 75,702

Inventories (Note 5.e) 1,799 9,846 7,823

Other assets - - 2,006

Subtotal current assets 675,550 428,816 335,685

Assets classified as held for sale (Note 5.h) - 8,655 -

Total current assets 675,550 437,471 335,685

Non-current assets

Trade receivables (Note 5.c) 3,790 3,790 7,168

Other receivables (Note 5.d) 162,498 109,450 76,194

Inventories (Note 5.e) 31,978 18,855 5,227

Fixed assets (Note 5.f) 2,315,041 1,448,107 1,425,301

Assets under concession (Note 5.f) 20,481 23,333 19,863

Intangible assets (Note 5.f) 30,375 31,675 -

Other assets (Note 5.g) - 214 33

Total non-currents assets 2,564,163 1,635,424 1,533,786

Total assets 3,239,713 2,072,895 1,869,471

Current liabilities

Accounts payable (Note 5.i) 519,834 285,601 276,336

Loans (Note 5.j) 364,045 283,733 234,362

Salaries and social security payable (Note 5.k) 22,309 15,817 12,670

Taxes payable (Note 5.l) 32,182 14,034 7,812

Other liabilities (Note 5.ll) 18,197 18,834 15,338

Provisions (Note 5.m) 1,900 1,900 1,538

Subtotal current liabilities 958,467 619,919 548,056

Liabilities related to assets classified as held for sale (Note 5.h) - 4,772 -

Total current liabilities 958,467 624,691 548,056

Non-current liabilities

Accounts payable - 95 104

Loans (Note 5.j) 1,648,580 897,382 885,376

Taxes payable (Note 5.l) 815 1,665 1,923

Deferred income tax liability (Note 5.r) 124,454 60,227 25,491

Other liabilities - - 3,480

Total non-current liabilities 1,773,849 959,369 916,374

Total liabilities 2,732,316 1,584,060 1,464,430

Shareholders’ equity (per corresponding statements)

Attributable to owners of the Company 507,397 488,835 405,041

Attributable to non-controlling interests - - -

Total shareholders’ equity 507,397 488,835 405,041

Total liabilities and shareholders’ equity 3,239,713 2,072,895 1,869,471

Notes 1 to 16 are an integral part of and should be read in conjunction with these consolidated financial statements.

2

GENNEIA S.A.

CONSOLIDATED STATEMENTS OF PROFIT AND LOSS AND OTHER COMPREHENSIVE INCOME

FOR THE YEARS ENDED DECEMBER 31, 2013, 2012 AND 2011

(amounts expressed in thousands of Argentine pesos - Note 3.1)

2013 2012 2011

Continuing operations

Net sales (Note 5.n) 922,624 743,800 557,899

Cost of sales (Note 5.ñ) (579,339) (483,027) (384,307)

Gross profit 343,285 260,773 173,592

Selling expenses (Note 5.o) (8,748) (11,969) (5,330)

Administrative expenses (Notes 5.o) (81,047) (77,168) (54,406)

Other expenses, net (Note 5.p) (583) (17,672) (6,459)

Financial expense, net (Note 5.q) (326,405) (181,427) (102,197)

Net (loss) income before income tax (73,498) (27,463) 5,200

Income tax (Note 5.r) (41,267) (19,770) (13,442)

Net loss from continuing operations (114,765) (47,233) (8,242)

Discontinued operations

Loss from discontinued operations (Note 5.s) (4,918) (9,226) (1,717)

Net loss for the year (119,683) (56,459) (9,959)

Other comprehensive income

Translation differences (1)

138,245 55,405 26,832

Total other comprehensive income 138,245 55,405 26,832

Total comprehensive income (loss) for the year 18,562 (1,054) 16,873

(Loss) income attributable to:

Owners of the Company (119,683) (56,459) (11,103)

Non-controlling interests - - 1,144

Net loss for the year (119,683) (56,459) (9,959)

Comprehensive income (loss) attributable to:

Owners of the Company 18,562 (1,054) 15,729

Non-controlling interests - - 1,144

Total comprehensive income (loss) for the year 18,562 (1,054) 16,873

(1) Corresponds mainly to the exchange difference resulting from the conversion process to the presentation currency of

Genneia S.A. which will not be reclassified to profit and loss in future periods.

Notes 1 to 16 are an integral part of and should be read in conjunction with these consolidated financial statements.

3

GENNEIA S.A.

CONSOLIDATED STATEMENTS OF CHANGES IN SHAREHOLDERS’ EQUITY

AS OF DECEMBER 31, 2013, 2012 AND 2011

(amounts expressed in thousands of Argentine pesos – Note 3.1)

Shareholders’ contributions Retained earnings Equity attributable to:

Capital

stock

Issuance

premiums

Subtotal

Irrevocable

contributions

Capital

contributions

Total

Legal

reserve

Other

comprehensive

income

Unappropriated

retained

results

Owners

of the

Company

Non-

controlling

interests

Total

Balances as of January 1,

2011

47,100 331,505 378,605 - - 378,605 744 - 9,963(1) 389,312 17,996 407,308

As decided by the General

Ordinary and Extraordinary

Shareholders’ meeting of

June 1, 2011:

- Appropriation to legal

reserve

- - - - - - 252 - (252) - - -

Acquisition of non-

controlling interests (Note

12.4)

- - - - - - - - - - (19,140) (19,140)

Net loss for the year - - - - - - - - (11,103) (11,103) 1,144 (9,959)

Other comprehensive income

for the year

- - - - - - - 26,832 - 26,832 - 26,832

Balances as of December

31, 2011

47,100 331,505 378,605 - - 378,605 996 26,832 (1,392) 405,041 - 405,041

As decided by the Board of

Directors’ meeting of

February 2, 2012:

- Irrevocable contributions

(Note 8)

- - - 64,800 - 64,800 - - - 64,800 - 64,800

Waiver of interests from

borrowings granted by

related parties (Note 9.2.9)

- - - - 20,048 20,048 - - - 20,048 - 20,048

As decided by the General

Ordinary and Extraordinary

Shareholders’ meeting of

April 13, 2012:

- Increase in capital stock

and appropriation to

special reserve for

issuance premiums from

capitalization of

irrevocable contributions

(Note 8)

4,420 60,380 64,800 (64,800) - - - - - - - -

Net loss for the year - - - - - - - - (56,459) (56,459) - (56,459)

Other comprehensive income

for the year

- - - - - - - 55,405 - 55,405 - 55,405

Balances as of December

31, 2012

51,520 391,885 443,405 - 20,048 463,453 996 82,237 (57,851) 488,835 - 488,835

Net loss for the year - - - - - - - - (119,683) (119,683) - (119,683)

Other comprehensive income

for the year

- - - - - - - 138,245 - 138,245 - 138,245

Balances as of December

31, 2013

51,520 391,885 443,405 - 20,048 463,453 996 220,482 (177,534) 507,397 - 507,397

(1) Includes 40,743 corresponding to initial adjustment for the first time adoption of IFRS.

Notes 1 to 16 are an integral part of and should be read in conjunction with these consolidated financial statements.

4

GENNEIA S.A.

CONSOLIDATED STATEMENTS OF CASH FLOW

FOR THE YEARS ENDED DECEMBER 31, 2013, 2012 AND 2011

(amounts expressed in thousands of Argentine pesos - Note 3.1)

2013 2012 2011

Cash flows provided by operating activities

Net loss for the year (119,683) (56,459) (9,959)

Adjustments to reconcile net loss for the year to net cash flows provided by operating activities:

Fixed assets depreciation 223,972 159,578 133,314

Intangible assets depreciation - 8

Loss from sale of fixed assets - 6,174 320

Income tax 38,619 14,802 12,517

Loss arising from contractual arrangements - 32,556 -

Minority interest in subsidiary - - 1,144

Account for future investments (Note 12.3) (31,456) - -

Changes in assets and liabilities:

Trade receivables (163,056) (118,776) (67,757)

Other receivables 14,229 (34,992) (82,576)

Inventories (5,076) (15,651) (3,195)

Other assets 214 1,826 (153)

Accounts payable 234,138 152,997 (6) 12,247

Salaries and social security payable 6,492 3,148 6,869

Taxes payable 178 10,735 (1,110)

Other liabilities (637) 378 1,342

Interest payable, exchange differences and others 42,709 17,039 35,329

Net cash flows provided by operating activities 240,643(1) 173,355 (1) 38,340 (1)

Cash flows used in investing activities (4)

Acquisitions of fixed assets (439,531) (232,620) (298,886)(2)

Restricted cash (8,605) 22,118 (22,130)

Proceeds from sales of fixed assets - 10,087 (371)

Net cash flows used in investing activities (448,136) (200,415) (321,387)

Cash flows provided by financing activities

Irrevocable contributions - 64,800 -

Proceeds from notes 414,398 90,000 230,246

Payment of notes (206,178) (161,134) -

Proceeds from loans, net of commissions 212,904 43,432 100,588

Payment of loans (66,042) (41,544) (52,764)

Bank overdrafts (23,468) 23,468 -

Net cash flows provided by financing activities 331,614 19,022 278,070

Increase (decrease) in cash and equivalents (3) 124,121(5) (8,038)(5) (4,977)(5)

Cash and equivalents at the beginning of the year (3) 11,625 19,663 24,640

Cash and equivalents at the end of the year (3) 135,746 11,625 19,663

(1) It includes 214,483, 128,746 and 62,054 as interests paid for the fiscal years ended on December 31, 2013, 2012 and 2011, respectively, and 1,546, 714 and 2,373 corresponding to payments for income taxes for the fiscal years ended on December 31, 2013, 2012 and 2011, respectively.

(2) It includes 26,453 as interests paid for third parties’ financing for construction of fixed assets for the year ended on December 31, 2011.

(3) Cash plus temporary investments with a maturity of less than three months (Note 3).

(4) Main non cash investing activities during the year ended December 31, 2013 comprises the acquisition of the fixed assets of the Pinamar power plant through a financial leasing with Sullair Argentina S.A. and the partial financing of the fixed assets acquired to GR Generación Energética Argentina S.A., as it is described in Note 9.2.8, for a total amount of 57,915 and 45,920, respectively. As of Decemeber 31, 2012, comprises the acquisition of projects and investments in companies in relation to wind and thermal projects. Additionally, cash used in investing activities as of December 31, 2013 is net of 22,230 for acquisitions of fixed assets paid during the previous year. Cash used in investing activities as of Decemeber 31, 2012 includes 73,551 for acquisitions of fixed assets paid during the previous year. There were no significant non cash investing activities during the year ended December 31, 2011.

(5) Includes (3,456), (2,424) and (3,394) of cash flows used in operating activities for the years ended December 31, 2013, 2012 and 2011, respectively, and (718) and (810) of cash flows used in investing activities for the years ended December 31, 2012 and 2011, respectively, corresponding to discontinued operations.

(6) Net of cash used in acquisitions of fixed assets made during the previous year.

Notes 1 to 16 are an integral part of and should be read in conjunction with these consolidated financial statements.

5

GENNEIA S.A.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS FOR THE YEARS ENDED

DECEMBER 31, 2013, 2012 AND 2011

(Amounts stated in thousands of Argentine pesos, except where otherwise indicated – Note 3.1)

NOTE 1 – BACKGROUND AND BUSINESS OF THE COMPANY

GENNEIA S.A. (“GENNEIA” or the “Company”) (formerly EMGASUD S.A.), an Argentine corporation, was

incorporated in 1991, has a duration through November 14, 2090 and its legal address is Leandro N. Alem 928, 7th Floor,

Buenos Aires city, Argentina.

After having reoriented its business strategy and discontinued the natural gas distribution and transportation components

during 2012 (see Notes 12.6 and 12.7), and the component of construction of high pressure gas pipelines and gas

distribution networks during 2013, the main activities of GENNEIA have been defined in three business units: (i) the

electric power generation from conventional sources; (ii) the electric power generation from renewable sources; and (iii)

the deregulated natural gas trading, transportation of natural gas and electric power, currently developed through its

subsidiary Enersud Energy S.A. (“ENERSUD”).

Business units – Electric power generation from conventional sources

GENNEIA develops its power generation business from conventional sources through nine thermal power plants with a

total nominal installed capacity of 280 MW, seven of which are connected to the Argentine Interconnection System

(“Sistema Argentino de Interconexión”, “NIS”) and where originally developed under the programs “Energía Distribuída I”

and “Energía Distribuida II” of Energía Argentina S.A. (“ENARSA”) (as it is described below). Furthermore, the power

plants of Río Mayo and Gobernador Costa belong to an isolated system in the Province of Chubut, with 7 MW of installed

capacity.

The programs for the generation of distributed energy have been promoted by the National Government and by ENARSA

in the framework of Resolutions N° 220/07 and 1836/2007 of the Energy Secretariat (the “Secretariat”), which sets forth

the possibility that the holders of assets that imply an additional offer of electric power inexistent as of the moment in

which these resolutions were passed, sell -in association with ENARSA in the case of Resolution N° 1836/2007- the energy

generated by that additional offer.

As part of the Resolution N° 1836/2007 indicated above, the Company originally entered into the relevant Power Purchase

Agreements (“PPA”) GENNEIA-ENARSA for each power plant, which established among other things, (i) a three year

term as from the commercial startup of the respective power plant, (ii) granted an option to ENARSA’s to extend the

agreements for terms up to 24 months, and (iii) a monthly fixed charge denominated in US$ for the energy made available,

a variable charge in US$ for the energy effectively dispatched and a fixed monthly charge in US$ for the operation and

maintenance, which are payable in pesos.

As detailed under Note 12.3, on April 18, 2012, the Company entered into a Framework Agreement (hereinafter the

“Framework Agreement”) with the Secretariat for the renewal of the contracts originally entered with ENARSA under the

framework of Resolution N° 1836/2007, whereby the Secretariat would instruct CAMMESA to enter into PPA with

GENNEIA for each of the power plants under the framework of Resolution N° 220/2007, with similar terms to the

purchase agreements referred to in the preceding paragraph but establishing that each agreement would extend for seven

years as from the completion of the original three year term for each PPA of each power plant, so as to complete a 10 year

term as from the original commercial operation date of each power plant.

In compliance with the provisions of the Framework Agreement, CAMMESA and GENNEIA entered into the

corresponding PPA under the terms of Resolution N° 220/2007 and subject to the other guidelines provided under the

Framework Agreement for the power plants of Pinamar, Concepción del Uruguay, Paraná, Matheu, Las Armas I and

Olavarría, effective as from December 1, 2012, while the power plants of Las Armas II and Bragado will be operated

directly with CAMMESA under the terms of Resolution N° 220/2007 just after the expiration the original PPA of such

power plants on January 21, 2014 and June 16, 2014, respectively. As of the date of issuance of these consolidated financial

statements, the corresponding PPA of the Las Armas II and Bragado power plants are still pending of formalization.

Power plants Río Mayo and Gobernador Costa started commercial operations in June 2008 and September 2009,

respectively. The energy generated is sold to the province of Chubut by means of an agreement, with a term of

effectiveness until December 31, 2025. By means of this agreement, the province of Chubut has assumed the obligation to

pay monthly to GENNEIA (i) a cost for the capacity made available, and (ii) a cost for thermoelectric power generated,

which will be adjusted semiannually based on natural gas price.

6

GENNEIA S.A.

Business unit – Electric power generation from renewable sources

Law N° 26,190, enacted in 2006, established a National Promotion Regime to foster the use of renewable energy sources

for electric power generation, which is supplementary to the one set forth by Law N° 25,019 and regulations thereto,

whereby the generation of wind and solar energy had been declared of national interest. Law N° 26,190 provides (as an

energy State policy) that by the end of 2016 up to 8% of the national electric power consumption shall be supplied by

renewable energy sources.

As part of the GENREN Project, promoted by ENARSA in order to fulfill the abovementioned law, in early 2012

GENNEIA started the commercial operation of the Rawson Wind Farm with an installed power capacity of 77.4 MW,

according to the corresponding GENNEIA – ENARSA Agreements of the Rawson Project, which became effective as from

the execution of the PPA of the Rawson Project between ENARSA and CAMMESA. These Agreements, among other

matters, (i) have a term until the earlier of (a) 15 year as from the date of the commercial operation of the respective plant,

(b) the delivery of a quantity of energy dispatched that ENARSA committed to purchase (2,400 GWh for the Rawson Wind

Farm I and 1,425 GWh for the Rawson Wind Farm II), (ii) grant ENARSA the option to renew the PPA for another 18

month period, provided all of the power estimated by the respective PPA has not been delivered, in which case the PPA

will expire, and (iii) provide a fixed price in US$ payable in pesos based on the energy effectively dispatched.

Additionally to the Rawson Wind Farm, through its controlled companies GENNEIA has several wind and thermal energy

generation projects based on renewable sources already awarded for a total of 322 MW.

Business Unit – Commercialization and transportation capacity of natural gas and electricity by ENERSUD

In order to secure its position in the energy trading sector and considering the regulatory limitation it had for being a gas

sub-distributor, in 2005 GENNEIA established its subsidiary ENERSUD, whose main objective is to trade natural gas and

natural gas transport capacity for industrial or domestic use and other services, as well as trading energy.

Since 2005 ENERSUD has been granted one of the Free Agent licenses issued by the Mercado Electrónico del Gas S.A.

(Gas Electronic Market or “MEG”), which enables it to operate in the Argentinean natural gas spot market. In that same

year ENERSUD enrolled in the Registro del Mercado Mayorista de Gas Natural (Natural Gas Wholesale Market Registry)

and in the Registro de Comercializadores (Traders’ Registry). After having discontinued the gas distribution business unit,

as it is mentioned in the following paragraph, on November 7, 2013 GENNEIA enrolled in the previously mentioned

registries, which enable the Company to operate in the Argentine natural gas spot market.

Discontinued components

During 2012, the Board of Directors decided to reorient the Company’s businesses, focusing on the business units

described above and deciding to discontinue the component of natural gas distribution. Additionally, as a result of what is

mentioned in the following paragraph, during the year 2012 the Company discontinued the component of transportation

through the Patagonic Gas Pipeline. Additionally, during the year 2013, the Board of Directors decided to discontinue the

business unit of construction of high pressure gas pipelines and gas distribution networks, that already from the year 2012

were mostly developed in an outsourced manner.

Moreover, as described under Note 12.6, through Resolutions issued by the Gas Regulating Authority (“ENARGAS”)

N° I/2090 and I/2374 dated March 23 and October 22, 2012, respectively, the operation of the Patagonic Gas Pipeline has

been transferred to Camuzzi Gas del Sur S.A. since May 2012.

Also, as described in Note 12.7, in 2012 the Company entered into an agreement with Proagas S.A. for the sale of the

natural gas distribution business unit to enforce the above mentioned discontinuation.

NOTE 2 – BASIS OF PREPARATION OF THE CONSOLIDATED FINANCIAL STATEMENTS

2.1 Basis of preparation and purpose of these consolidated financial statements

The consolidated financial statements of GENNEIA and its controlled companies for the years ended December 31, 2013,

2012 and 2011 are prepared in accordance with International Financial Reporting Standard (“IFRS”), as issued by the

International Accounting Standards Board (“IASB”).

These consolidated financial statements are derived from the Company’s consolidated financial statements for the years

ended December 31, 2013 and 2012 and from the Company’s consolidated financial statements for the years ended

December 31, 2012 and 2011, originally issued and filed with the Argentine Securities Commission (“CNV”) and

originally approved by the Board of Directors of GENNEIA and authorized for issue on February 18, 2014 and March 8,

2013, respectively, and do not include certain information required by CNV regulations.

7

GENNEIA S.A.

These consolidated financial statements have been prepared only for their inclusion in the Offering Memorandum to be

prepared by the Company in connection with the Company’s proposed offering of notes under the US$ 400 million note

program, to prospective investors mainly outside of Argentina.

2.2 Applicable accounting policies

The consolidated financial statements have been prepared under the historical cost basis. Historical cost is generally based

on the fair value of the consideration given in exchange for assets.

The principal accounting policies are described in Note 3.

The preparation of these financial statements is the responsibility of the Company's Board of Directors and requires

accounting estimates and judgments of the management when applying financial standards. Areas of high complexity

which require more judgments or those in which assumptions and estimations are more significant are detailed in Note 4.

2.3 Standards and Interpretations issued

2.3.1. New standards issued

Standards and Interpretations or amendments to them, published by the IASB and endorsed by the Argentine Federation of

Professional Councils in Economic Sciences (“Federación Argentina de Consejos Profesionales de Ciencias Económicas”

or “FACPCE”) and the CNV, which have been applied by the Company as from the fiscal year ended December 31, 2013,

are the following: (i) IAS 24 (amended in 2009) “Related party disclosures”; (ii) IFRS 10 “Consolidated financial

statements”; (iii) IFRS 12 “Disclosure of interests in other entities”; (iv) IFRS 13 “Fair value measurement”; and (v)

amendments to IAS 1.

Adoption of the standards and interpretations or amendments to them mentioned in the preceding paragraph did not have a

significant impact on the consolidated financial statements of the Company for the fiscal years ended December 31, 2013,

2012 and 2011.

2.3.2. New standards issued not yet adopted

The Company did not adopt the standards and interpretations or amendments mentioned below, because its application is

not required at the end of the fiscal year ended December 31, 2013:

IFRS 9 Financial instruments 1 Amendments to IFRS 9 and IFRS 7 Mandatory effective date for application of IFRS 9 and

transition disclosures 1 Amendments to IFRS 10, 12 and IAS 27 Investments entities 2 Amendments to IAS 32 Regarding compensation of financial assets and liabilities 2

1 With indefinite deferred implementation date. 2 Effective for fiscal years beginning on or after January 1, 2014.

As of the issuance date of these consolidated financial statements, the Company is evaluating the impact that the adoption

of the standards and interpretations or amendments mentioned in the previous paragraphs will have on the consolidated

financial statements of the Company. It is probable that the changes will not have a significant impact on the consolidated

financial statements of the Company, however, it can not be reasonably determined the impact of the potential effect until a

detailed analysis is performed.

2.4 Basis of consolidation

The consolidated financial statements of GENNEIA incorporate the separate financial statements of the Company and its

controlled entities. They are considered controlled when the Company (i) has power over the investee, (ii) is exposed, or

has rights, to variable returns from its involvement with the investee and, (iii) has the ability to use its power to affect its

returns.

The main consolidation adjustments are the following:

· elimination of assets and liabilities and income and expenses of the parent with its subsidiaries, in order to disclose the balances maintained effectively with third parties; and

· elimination of interests in the equity and earnings of the controlled entities, for each period.

8

GENNEIA S.A.

The latest financial statements available as of the balance sheet date have been used and considering significant subsequent

events and transactions and/or available management information and the transactions between GENNEIA and the

controlled entity.

If necessary, financial statements of controlled entities are adjusted to bring up their accounting policies into line with those

used by the Company.

Detailed below are the controlled companies whose financial statements have been included in these consolidated financial

statements: Main activity Percentage of participation

2013 2012 2011

Subsidiaries:

Enersud Energy S.A. Industrialization, separation and trading of propane and butane gas and/or liquefied gas and trading of natural gas and transportation for industrial or residential consumption.

100% 100% 100%

Ingentis II Esquel S.A. Power generation and trading. 100% 100% 100%

IWS Energy Services S.A. Design, construction, inspection and maintenance of networks and pipelines for natural gas distribution.

100% 100% 100%

Genneia Desarrollos S.A. Production and development of renewable energies and its commercialization.

100% 100% 100%

Nor Aldyl San Lorenzo S.A. Production and development of renewable energy and its commercialization, construction of gas pipelines and networks.

100% 100% -

Nor Aldyl Bragado S.A. Production and development of renewable energy and its commercialization, construction of gas pipelines and networks.

100% 100% -

Patagonia Wind Energy Production and development of renewable energies and its commercialization.

100% 100% -

International New Energy S.A. Design, development and construction of facilities for water, gas, electricity distribution and any other form of energy generation and/or distribution.

100% 100% -

2.5 Business combinations

Acquisitions of businesses are accounted for using the acquisition method. The consideration transferred in a business

combination is measured at fair value, which is calculated as the sum of the acquisition-date fair values of the assets

transferred by the Company, liabilities incurred or assumed and the equity interests issued by the Company in exchange for

control of the acquiree. Acquisition-related costs are generally recognized in profit or loss as incurred.

At the acquisition date, the identifiable assets acquired and the liabilities assumed are recognized at their fair value at the

acquisition date, except for certain assets and liabilities measured in accordance with the corresponding accounting

policies.

The goodwill, if any, is measured as the excess of the sum of the consideration transferred, the amount of any non-

controlling interests in acquiree, and the fair value of the acquirer's previously held equity interest in the acquiree (if any)

over the net of the acquisition date amounts of the identifiable assets acquired and liabilities assumed.

During the year ended December 31, 2012 the Company has carried out the business combination mentioned in Note 12.5.

NOTE 3 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

3.1. Functional and presentation currencies and tax effects on other comprehensive income

Under IFRS the companies should define their functional currency in accordance with the criteria established by

IAS 21 "Effects of changes in foreign currency exchange rates", which may differ from their reporting currency.

Under the above mentioned rule, considering the main activities of the Company as detailed in Note 1, the Board of

Directors has defined the US$ dollar (“US$”) as the functional currency for GENNEIA and Genneia Desarrollos S.A.

As a result, the financial statements of such companies have been converted into US$ by applying the procedure

established in IAS 21. In accordance with the established procedure, monetary assets and liabilities are remeasured

into US$ at the exchange rate prevailing on the balance sheet date. Non-monetary assets, measured on a historic cost

basis, as well as income and expenses are remeasured using the exchange rate prevailing on the transaction date. Any

gain or loss arising from the remeasurement of monetary assets and liabilities into US$ is recognized in the income

statement in the period they are generated. For the other subsidiaries, Management has defined the Argentine peso as

the functional currency. In these cases, the adjustment resulting from remeasuring the financial statements of such

entities into the US$ is recognized under Other comprehensive income.

9

GENNEIA S.A.

In addition, pursuant to General Resolution 562 issued by the CNV, the Company should submit its financial

statements in pesos; hence, the amounts resulting from the process explained above should be converted into pesos by

application of the criteria established by IAS 21. As a result assets and liabilities should be translated at the exchange

rate prevailing on the balance sheet date, and income and expenses should be translated at the exchange rate prevailing

on each transaction date (or, given practical reasons and, insofar as exchange rates do not fluctuate significantly, at the

average exchange rate every month), and the resulting exchange differences are recognized under Other

comprehensive income.

Results accounted for in “Other comprehensive income” related to exchange differences arising from investments in

companies with functional currencies other than U.S. dollars and also as a result of the translation of the financial

statements of GENNEIA to its reporting currency (pesos) have no effect on the current or deferred income tax because

as of the time that such transactions were generated, they had no impact on net income nor taxable income.

3.2. Foreign currencies

In preparing the consolidated financial statements, transactions in currencies other than the Company’s functional

currency (foreign currencies) are recognized at the rates of exchange prevailing at the dates of the transactions. At the

end of each reporting year, monetary items denominated in foreign currencies are translated to functional currency at

the rates prevailing at that date. Exchange differences on monetary items are recognized in profit and loss in the year

in which they arise.

3.3. Financial assets

Financial assets include: cash, time deposits in financial entities, equity instruments of other companies, contractual

rights, or a contract which will or can be liquidated with the delivery of equity instruments of the Company.

Financial assets are classified into the following specified categories: ‘financial assets measured at fair value through

profit and loss’, ‘held-to-maturity’, ‘available for sale’, and ‘loans and receivables’. The classification depends on the

nature and purpose of the financial assets and is determined at the time of initial recognition.

Financial assets must be recognized on trade date, when the Company commits to purchase or sale an asset. The

recognition method is consistent for all purchases or sales of financial assets of the same category.

Financial assets are initially measured at fair value, plus transaction costs, except for those financial assets designated

as financial assets at fair value through profit or loss.

3.3.1 Cash and cash equivalents

Include cash, time deposits in financial entities and short-term investments with maturity up to 90 days, with low risk

of value variation and destined to cancel short-term liabilities.

2013 2012 2011

Cash 31,479 11,625 19,604

Current Investments 104,267 - 59

Cash and cash equivalents 135,746 11,625 19,663

3.3.2 Financial assets at fair value through profit and loss

The financial assets at fair value through profit and loss are stated at fair value, with any gains or losses arising on

remeasurement recognized in the consolidated statements of profit and loss and other comprehensive income. The net

gain or loss recognized in profit or loss incorporates any dividend or interest earned on the financial asset and is

included in the “Financial expense, net” caption in the consolidated statement of profit and loss and other

comprehensive income.

3.3.3 Held-to-maturity financial assets

Comprises investments over which the Company has the positive intent and ability to hold to maturity. Subsequent to

initial recognition, held-to-maturity investments are measured at amortized cost using the effective interest method

less any impairment. Revenue is recognized on an effective yield basis.

3.3.4 Loans and receivables

Loans and receivables are non-derivate financial assets with fixed or determinable payments that are not quoted in an

active market. Loans and receivables are measured at amortized cost using the effective interest method, less any

impairment.

10

GENNEIA S.A.

3.3.5 Effective interest method

The effective interest method is a method of calculating the amortized cost of a financial asset and of allocating

interest income over the relevant period. The effective interest rate is the rate that exactly discounts estimated future

cash receipts (including all taxes paid or received, transaction costs and other premiums or discounts) through the

expected life of the financial asset.

Income is recognized on an effective interest basis for financial assets other than those financial assets classified as

fair value through profit and loss.

3.3.6 Impairment of financial assets

Financial assets are assessed by the Company for indicators of impairment at the end of each year. Financial assets are

considered to be impaired when there is objective evidence that, as a result of one or more events that occurred after

the initial recognition of the financial asset, the estimated future cash flows of the financial asset have been affected.

3.3.7 Derecognition of financial assets

The Company derecognizes a financial asset only when the contractual rights to the cash flows from the asset expire,

or when it transfers the financial asset and substantially all the risks and rewards of ownership of the asset to another

party. If the Company neither transfers nor retains substantially all the risks and rewards of ownership and continues

to control the transferred asset, the Company recognizes its retained interest in the asset and an associated liability for

amounts it may have to pay. If the Company retains substantially all the risks and rewards of ownership of a

transferred financial asset, the Company continues to recognize the financial asset and also recognizes a collateralized

borrowing for the proceeds received.

3.4. Inventories

Materials and spare parts are stated at the weighted average cost reduced, if necessary, to net realizable value. The net

realizable value is the estimated price of sale less estimated selling costs. Materials and spare parts in transit have been

value at acquisition cost.

Based on Management´s analysis at December 31, 2013, 2012 and 2011 no allowance for inventory has been

recognized for materials and spare parts. Such analysis takes into consideration the conservation status, their future

use and the net realizable value of the inventories.

3.5. Fixed assets

· Lands and buildings held for use in production, supply of services or for administrative purposes, machinery and

equipment, tools, facilities, furniture and equipment and vehicles, are stated in the consolidated statement of

financial position at their cost less any subsequent accumulated depreciation (except for land which is not

depreciated) and less any recognized impairment loss.

Depreciation of buildings, machinery and equipment, tools, facilities, furniture and equipment and vehicles is

charged to expense for each year.

· Work in progress at the end of each year is carried at cost, less any recognized impairment loss. These assets are

classified in the appropriate category of fixed assets when the construction is completed and are ready for use.

Depreciation of these assets commences when the assets are ready for their intended use. The Company has

capitalized the corresponding portion of financial costs related to third parties’ financing of long-term construction

of fixed assets.

· Improvement on third party assets are stated at cost less accumulated depreciation and accumulated impairment

losses.

· Assets acquired through financial leasing agreements have been incorporated at the lower value of the cash

purchase price and the sum of discounted values of the minimum payments of the assets, calculated at the implied

interest rate of the leasing, with a counterpart in “Loans – Financial leasings” of current and non-current liabilities.

· Depreciation is recognized so as to write-off the cost or valuation of assets (other than land) less their residual

values over their useful lives, using the straight-line method. The estimated useful lives and residual values are

reviewed at each year end, with the effect of any changes in estimates being accounted for on a prospective basis.

11

GENNEIA S.A.

· An item of fixed assets is derecognized upon disposal or when no future economic benefits are expected to arise

from the continued use of the asset. Gain or loss derived of the sales proceeds disposal or retirement of an item of

fixed assets is determined as the difference between the sales proceeds and the carrying amount of the asset and it is

recognized in the consolidated statement of comprehensive income.

3.6. Assets under concession - Service concession agreements

The value of assets for the generation power plants Mayo and Costa as indicated in Note 1 (hereinafter, “the

infrastructure”) are recognized pursuant to the provisions of the IFRIC 12 “Service Concession Agreements”.

IFRIC 12 requires that certain assets being recognized in accordance with its provisions when the following

conditions are met: (i) the grantor controls or regulates the services that the Company has to provide with the

infrastructure built or to be built, to whom must provide them and at what price; (ii) the infrastructure involved in the

concession agreement is completely consumed in the concession period or the grantor controls any significant residual

interest on the infrastructure at the end of the service agreement; and (iii) the infrastructure is built or purchased by the

Company for the sole purpose of implementing the service agreement.

In this context, the Company acts as a supplier of two services: one for the construction of the power plants used to

provide electricity as a public service and another for the operation of such plants during the period of the concession.

The Company recognizes and measures revenues from construction services in accordance with the provisions set in

IAS 11 "Construction Contracts" while revenues from operating services are recognized and measured in accordance

with IAS 18 "Revenues". The consideration to be received by the Company for its services in construction is a right to

make charges to the grantor of public service that is recognized as assets under concession. That asset is measured at

the fair value at the time of initial recognition.

3.7. Intangible assets

Intangible assets include, mainly, costs of acquisition of new projects. The accounting policies for the recognition and

measurement of these intangible assets are described below.

3.7.1 – Intangible assets acquired in a business combination

Intangible assets acquired in a business combination and recognized separately from goodwill are initially recognized

at their fair value at the acquisition date (which is regarded as their cost).

Subsequent to initial recognition, intangible assets acquired in a business combination are reported at cost less

accumulated amortization and accumulated impairment losses, on the same basis as intangible assets that are acquired

separately.

3.7.2 – Derecognition of an intangible asset

An intangible asset is derecognized on disposal, or when no future economic benefits are expected from use or

disposal. Gains or losses arising from derecognition of an intangible asset, measured as the difference between the net

disposal proceeds and the carrying amount of the asset, are recognized in profit or loss when the asset is derecognized.

3.8. Impairment of tangible and intangible assets

At the end of each reporting year, the Company reviews the carrying amounts of its tangible and intangible assets to

determine whether there is any indication that those assets have suffered an impairment loss. If any such indication

exists, the recoverable amount of the asset is estimated in order to determine the extent of the impairment loss (if any).

When it is not possible to estimate the recoverable amount of an individual asset, the Company estimates the

recoverable amount of the cash-generating unit to which the asset belongs. When a reasonable and consistent basis of

allocation can be identified, corporate assets are also allocated to individual cash-generating units, or otherwise they

are allocated to the smallest group of cash-generating units for which a reasonable and consistent allocation basis can

be identified.

In the impairment assessment, the assets that do not generate independent cash flows are grouped in an appropriate

cash generating unit. The recoverable amount for such assets or the cash generating unit is measured as the higher of

its fair value (calculated by using the discounted future cash flows method) and its book value.

Recoverable amount is the higher of fair value less costs to sell and value in use. In assessing value in use, the

estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current

market assessments of the time value of money and the risks specific to the asset for which the estimates of future

cash flows have not been adjusted.

12

GENNEIA S.A.

3.9. Other assets

Correspond to costs incurred by the Company concerning the development of projects related to pipelines and electric

power generation construction activities which are measured at their acquisition cost or construction cost at each fiscal

year end, which do not exceed their estimated recoverable value, net of the corresponding allowance to reduce its

carrying amount to the probable realizable value.

3.10. Non-current assets available for sale

Non-current assets for disposal are classified as held for sale if their book value is recoverable through a sale

transaction and not through its continuous use. This condition is met only where the sale is highly probable and the

asset (or group of assets for disposal) is available for immediate sale in its current condition. Management should be

committed to the sale, which should be expected to qualify as sale completed within one year as from the

classification date.

Non-current assets classified as held for sale are measured at the lower of book value and fair value less costs to sell.

3.11. Liabilities

The Company recognizes a liability when it has a present obligation (legally enforceable as a result of the execution of

a contract or a requirement contained in a legal standard) resulting from a past event and whose amount owed can be

reliably estimated.

3.12. Financial liabilities

Financial liabilities are classified as fair value through profit or loss or as other financial liabilities.

Financial liabilities, including borrowings, initially measured at fair value, net of transaction costs, are

subsequently measured at amortized cost using the effective interest method. Interest charges are included in the

“Financial expenses, net” caption of the consolidated statement of profit and loss and other comprehensive income.

The Company derecognizes financial liabilities (or a part of them) when, and only when, the Company's obligations

are discharged, cancelled or they expired.

The difference between the carrying amount of the financial liability derecognized and the consideration paid is

recognized in profit or loss.

3.13. Other liabilities

Other liabilities have been valued at nominal value which does not significantly differ from their discounted value.

3.14. Provisions

Provisions are recognized when the Company has a present obligation (legal or constructive) as a result of a past

event, it is probable that the Company will be required to settle the obligation, and a reliable estimate can be made of

the amount of the obligation.

The amount recognized as a provision is the best estimate of the consideration required to settle the present obligation

at the end of the reporting year, taking into account the risks and uncertainties surrounding the obligation. When a

provision is measured using the cash flows estimated to settle the present obligation, its carrying amount is the present

value of those cash flows.

When some or all of the economic benefits required to settle a provision are expected to be recovered from a third

party, a receivable is recognized as an asset if it is virtually certain that reimbursement will be received and the

amount of the receivable can be measured reliably.

The Company has been sued in certain labor, civil and commercial lawsuits. Provisions for contingencies are recorded

on a risk assessment basis and when the likelihood of a loss is probable. The assessment of a loss probability is based

on the opinion of legal counsels of the Company and its Management.

3.15. Revenue recognition

The Company derives its revenues mainly from power generation and sale of energy contracts.

Revenues derived from electric power generation are measured at the fair value of the consideration received or

receivable and are recorded as sales when realized. For such purpose, they should meet the following criteria: there is

an agreement with the client, the price is fixed or determinable, the service was provided and collection is reasonably

secured.

13

GENNEIA S.A.

Interest income is recognized based on the yields calculated by the effective rate method.

3.16. Leasing

Leases are classified as finance leases whenever the terms of the lease transfer substantially all the risks and rewards

of ownership to the lessee. All other leases are classified as operating leases. There are no situations in which the

Company qualifies as a lessor.

Assets held under finance leases are initially recognized as assets of the Company at their fair value at the inception of

the lease or, if lower, at the present value of the minimum lease payments. The corresponding liability to the lessor is

included in the consolidated statement of financial position as loans.

Lease payments are recognized in profit and loss as financial expenses and reduction of the lease obligation so as to

achieve a constant rate of interest on the remaining balance of the liability.

Leases are classified as operating when the lessor does not transfer substantially all risks and rewards inherent to the

ownership of the asset upon lease.

Operating lease payments are recognized as an expense on a straight-line basis over the lease term, except where

another systematic basis is more representative of the time pattern in which economic benefits from the leased asset

are consumed.

3.17. Borrowing costs

Borrowing costs directly attributable to the acquisition, construction or production of qualifying assets, which are

assets that necessarily take a substantial period of time to get ready for their intended use or sale, are capitalized to the

cost of those assets, until such time as the assets are substantially ready for their intended use or sale.

Other borrowing costs are recognized as expenses in the period in which they are incurred.

3.18. Income tax and minimum presumed income tax

3.18.1 Income taxes – current and deferred

Income tax expenses represent the sum of the tax currently payable and the deferred tax.

3.18.1.1 Current tax

The tax currently payable is based on taxable profit for the year. Taxable profit differs from profit before

income tax as reported in the consolidated statement of profit and loss and other comprehensive income

because of items of income or expense that are taxable or deductible in other years and items that are never

taxable or deductible. The Company’s liability for current tax is calculated using tax rate that have been

enacted or substantively enacted at the end of the year. The current income tax charge is calculated on the basis

of the tax laws in force in Argentina.

3.18.1.2 Deferred tax

Deferred tax is recognized on temporary differences between the carrying amounts of assets and liabilities in

the consolidated financial statements and the corresponding tax basis used in the computation of taxable results.

Deferred tax liabilities are generally recognized for all taxable temporary differences. Deferred tax assets,

including tax loss carry forwards, are generally recognized for all deductible temporary differences to the

extent that it is probable that taxable profits will be available against which those deductible temporary

differences can be utilized.

Such deferred assets and liabilities are not recognized if the temporary difference arises from goodwill or from

the initial recognition (other than in a business combination) of other assets and liabilities in a transaction that

affects neither the taxable results nor the accounting results.

Deferred tax assets and liabilities are measured at the tax rates that are expected to apply in the period in which

the liability is settled or the asset realized, based on tax rates and tax laws that have been enacted or

substantively enacted by the end of the year. The measurement of deferred tax liabilities and assets reflects the

tax consequences that would follow from the manner in which the Company expects, at the end of the year to

recover or settle the carrying amount of its assets and liabilities.

Deferred tax assets and liabilities are offset when there is a legally enforceable right to set off current tax assets

against current tax liabilities and when they relate to income taxes levied by the same taxation authority and the

Company intends to settle its current tax assets and liabilities on a net basis.

14

GENNEIA S.A.

Under IFRS, deferred income tax assets and liabilities are classified as non-current assets and non-current

liabilities.

3.18.1.3 Current and deferred tax for the year

Current and deferred tax are recognized in profit or loss in the consolidated statement of profit and loss and

other comprehensive income, except when they relates to items that are recognized directly in equity, in which

case, the current and deferred tax is recognized directly in equity or when current tax or deferred tax arises

from the initial accounting for a business combination.

3.18.2 Minimum presumed income tax

The minimum presumed income tax complements the income tax. The Company determines the tax charge by

applying the enacted rate of 1% to the taxable assets at the end of year. The Company´s tax obligation will

coincide with the higher between the determined minimum presumed income tax and the income tax liability

determined applying the enacted 35% tax rate over the estimated taxable result of year. Nevertheless, if the

presumed income tax in a fiscal year exceeds the corresponding income tax, such excess may be computed as a

prepayment of any income tax excess over the minimum presumed income that may be generated in the next

ten years.

3.19. Shareholders’ equity accounts

Shareholders’ contributions and reserves accounts were prepared in accordance with the accounting standards in force

on the transition date to IFRS. Changes to such accounts were accounted for pursuant to the respective decisions of

the Shareholders’ Meetings, regulatory and statutory rules (Issuance premiums and Reserves) although such items

would not have existed or would have had a different balance if the IFRS have been applied in the past.

Capital stock

Includes capital contributions committed or paid in by shareholders, and includes all outstanding shares at par value.

Issuance premiums

It is the difference between the subscription price of capital increases and the corresponding par value of issued

shares.

Capital contributions

Corresponds to transactions with shareholders that, as provided by IFRS and CNV rules, and based on the substance

over form principle, are assimilated to capital contributions and, thus, their effects are directly recognized under

Shareholders’ equity.

Legal Reserve

In accordance with the provisions of Law N° 19,550, the Company is required to set up a legal reserve of at least 5%

of net income, which results from the sum of income/loss for the year, the adjustments to prior years, the transfers

from other comprehensive income and accumulated losses from prior years, until such reserve reaches 20% of the sum

of issued capital and capital adjustment accounts, if any.

Unappropriated retained results

It includes the retained earnings / losses without specific appropriation, which in case of being positive may be

distributed pursuant to a resolution by the Shareholders’ meeting, insofar as they are not subject to statutory

restrictions, as that described in the previous paragraph. Includes earnings / losses from prior years that were not

distributed, the amounts transferred from other comprehensive income and the adjustments to prior years according to

accounting standards.

In addition, pursuant to the provisions of CNV rules, when the net balance of the Other comprehensive income

account is positive, it cannot be distributed, capitalized or appropriated to absorbing accumulated losses, and when the

net balance of such account is negative, a restriction shall apply to the distribution of retained earnings by such

amount.

Under Law N° 25,063, passed in December 1998, dividends distributed, either in cash or in kind, in excess of

accumulated taxable income at the end of year immediately preceding the payment or distribution date, will be subject

to 35% as an income tax withholding as a sole and final payment. Accumulated taxable income for the purposes of

this tax includes the balance of accumulated accounting profits at year end immediately preceding the effective date of

the Law less dividends paid plus the taxable income determined from that exercise.

15

GENNEIA S.A.

Additionally, Law No. 26.893 enacted on September 20, 2013, established certain modifications to the Income Tax

Law, and determined, among other topics, a withholding tax as a sole and final payment of 10% over dividends

distributed either in cash or in kind -except in shares- to foreign beneficiaries, and to individuals resident in Argentina,

notwithstanding to the above mentioned withholding in the previous paragraph. In accordance with the Shareholders’

Agreement, the approval to distribute dividends to the shareholders requires the favorable vote of a qualified majority

of the Company´s capital stock. However, the Company is limited in the distribution of dividends by certain

restrictive covenants assumed in connection with the issuance of the negotiable obligations (Note 9).

Other comprehensive income

It includes income and expenses directly recognized under Shareholders’ Equity and the transfers of such items from

Shareholders’ Equity accounts to income for the year or retained earnings accounts, as established by IFRS.

NOTE 4 – CRITICAL JUDGEMENTS IN APPLYING ACCOUNTING POLICIES

In the application of the Company’s accounting policies, the Management and Board of Directors are required to make

judgments, estimates and assumptions about the carrying amounts of assets and liabilities that are not readily apparent from

other sources. The estimates and assumptions are based on historical experience and other factors that are considered to be

relevant. Actual results may differ from these estimates.

The estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are

recognized in the period in which the estimate is revised if the revision affects only that period or in the period of the

revision and future periods if the revision affects both current and future years.

Company’s Management make estimates, among others, in order to measure at a given moment the accruals for unbilled

receivables, allowances for uncollectable accounts, the fair value of assets and liabilities, the estimate about contingent

liabilities, the recoverable value of assets, the income tax expense, the recoverable value of deferred tax assets, cumulative

tax loss carryforwards and minimum presumed income tax credits, the useful life of fixed assets, and the functional

currency, among others.

Below is a detail of the accounting areas and items that require that management make significant judgments and estimates

in preparing these consolidated financial statements:

Functional Currency

The Company’s Management applies its professional judgment in determining its functional currency and of its controlled

entities. Judgement is basically made regarding the currency that mainly influences and determines sales prices, labor and

material costs, investments and other costs, as well as the financing and collections derived from its operating activities.

Fair value of financial assets and liabilities

In preparing its consolidated financial statements, the Company estimates the fair value of its financial assets and liabilities.

Fair value is measured as the price that would be received to sell an asset or to paid a liability in an orderly transaction

between market participants at the measurement date. If there is a quoted price available for that instrument in an active

market, fair value is calculated based on that price.

If there is no active market available for that financial instrument, its fair value is estimated on the basis of the price

established in recent transactions involving the same or similar nature instruments and, in the absence thereof, on the basis

of valuation techniques, using valuation techniques commonly used by the financial markets. The present value method is

used for estimating the fair value of financial instruments of receivables and payables including loans. Company’s

Management applies judgement in estimating expected future cash flows and the rate used to discount such expected cash

flows related with the applicable currencies.

Estimate of contingent liabilities for claims and lawsuits

The final outcome arising from litigation, claims and other contingencies, as well as the perspective given to each issue by

the Management may vary from their estimates due to different interpretations of laws, contracts, opinions and final

assessments of the amount of the claims. Changes in the facts or circumstances related to these types of contingencies can

have, as a consequence, a significant effect on the amount of the provisions for litigation and other contingencies recorded

or the perspective given by the Management.

16

GENNEIA S.A.

Recoverable value of deferred tax assets, tax loss carryforwards and credits for minimum presumed income tax

The Company recognizes tax loss carryforwards and other tax credits as deferred tax assets when it is probable its

deduction against future taxable income. To that effect, based on paragraph 26 of NIC 12, the Company considers the

projected taxable income and the reversal of temporary liability differences.

In order to determine the likelihood of realization and estimate the recoverable amount of such assets, Management projects

taxable income on the basis of several future variables, including the estimate of the Argentine currency devaluation against

the US dollar for the following years. Such estimates are periodically reviewed and their effects are recognized in the

period in which a revision is performed.

Account for future investments

As mentioned in Note 12.3, CAMMESA deducts from its monthly payments to the Company an amount appropriated to set

up an “Account for future investments” which might be used to the installation of certain power plants.

Such payments are recorded as Company’s revenues in the period of accrual based on a regulatory and legal analysis made

by Company’s management, in consultation with its legal advisors.

Recoverable value of assets

The Company generally estimates the recoverable value of fixed assets, assets under concession and intangible assets on

the basis of their economic use value, calculated as the discounted expected future cash flows generated by each asset or

group of assets under evaluation.

In order to estimate cash flows, the Company’s Management calculates revenues and future costs based on its best estimate

of the regulatory framework, tariffs, fuel costs, devaluation and inflation of the Argentine peso, salaries, wind farm

utilization factor and the rate used to discount such cash flows, among others.

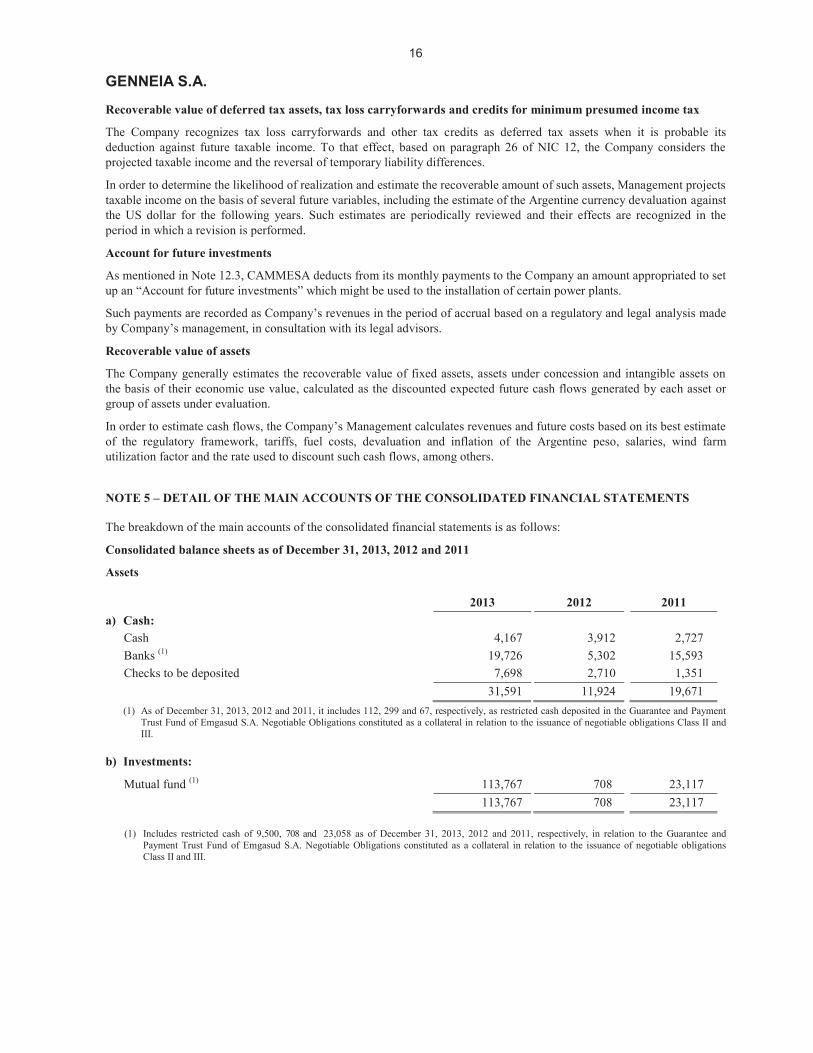

NOTE 5 – DETAIL OF THE MAIN ACCOUNTS OF THE CONSOLIDATED FINANCIAL STATEMENTS

The breakdown of the main accounts of the consolidated financial statements is as follows:

Consolidated balance sheets as of December 31, 2013, 2012 and 2011

Assets

2013 2012 2011

a) Cash:

Cash 4,167 3,912 2,727

Banks (1) 19,726 5,302 15,593

Checks to be deposited 7,698 2,710 1,351

31,591 11,924 19,671

(1) As of December 31, 2013, 2012 and 2011, it includes 112, 299 and 67, respectively, as restricted cash deposited in the Guarantee and Payment Trust Fund of Emgasud S.A. Negotiable Obligations constituted as a collateral in relation to the issuance of negotiable obligations Class II and III.

b) Investments:

Mutual fund (1) 113,767 708 23,117

113,767 708 23,117

(1) Includes restricted cash of 9,500, 708 and 23,058 as of December 31, 2013, 2012 and 2011, respectively, in relation to the Guarantee and Payment Trust Fund of Emgasud S.A. Negotiable Obligations constituted as a collateral in relation to the issuance of negotiable obligations Class II and III.

17

GENNEIA S.A.

2013 2012 2011

c) Trade receivables:

Current

Trade receivables - Electric power generation 345,938 141,491 61,459

Accruals for unbilled sales of Electric power generation 103,218 146,908 115,076

Trade receivables - Gas pipelines construction 350 10,248 5,248

Trade receivables - Sale of gas and others 20,191 13,392 24,974

Accruals for unbilled sales of gas consumption and gas

transportation 7,230 1,832 1,989

Allowance for doubtful accounts (Note 5.m) - - (1,380)

476,927 313,871 207,366

Non-current

Patagonic Gas Pipeline construction (1) 3,790 3,790 3,790

Other gas pipelines construction - - 3,378

3,790 3,790 7,168

(1) A portion of the work of the Patagonic Gas Pipeline Trust, as well as the construction of Ramales Río Pico and Corcovado, were financed

through a Financial Trust managed by Nación Fideicomisos S.A. according to Decree Nº 180/04 and Resolution MPFIPSyS Nº 185/04. As

regards to the mentioned works, the Company maintains as of December 31, 2013, 2012 and 2011, balances of aging accounts receivable past

due for 7,580, which have been measured at their estimated discounted value of 3,790 as of December 31, 2013, 2012 and 2011. As of the date of issuance

of these consolidated financial statements, GENNEIA has claimed to the Trust and to the Province of Chubut as fiduciary for the collection of

these accounts, and is taking the necessary steps for that purpose (Note 12.6).

Aging of past due but not impaired trade receivables

2013

Up to three months 168,710

Three to six months 48,392

Six to nine months 12,266

Nine to twelve months 5,291

More than one year 33,852

Balance at end of year 268,511(1)

(1) In relation to the aging for past due receivables, see Note 7.3.3.

d) Other receivables: 2013 2012 2011

Current

Related parties (Note 6) 12,587 2,180 2,048

Value added tax - 27,008 55,161

Income tax advances and withholdings and minimum presumed

income tax (net of minimum presumed income tax payable) 433

6,449

1,958

Prepaid expenses 1,648 1,066 451

Advanced payments to suppliers 1,631 2,678 1,165

Construction costs to be recovered 1,622 1,522 1,301

Accrual for unbilled construction costs 358 6,127 4,914

Receivables from insurance companies - 24,619 -

Prepaid insurance 15,088 7,532 2,778

Receivable for investment in Patagonian Pipeline (Note 12.6) 8,143 6,392 -

Rights for the reception of gas - - 1,425

Miscellaneous 9,956 6,894 4,501

51,466 92,467 75,702

18

GENNEIA S.A.

2013 2012 2011

Non-current

Account for future investments (Note 12.3) 31,456 - -

Debt Instruments – Gasoducto Loop Regional Sur Trust (1) 13,056 13,056 13,056

Value added tax 9,845 - 246

Minimum presumed income tax credit 46,933 17,832 18,628

Related parties (Note 6) 2,028 2,059 23,061

Turnover tax 4,712 6,417 7,510

Advanced payments to suppliers 7,422 24,977 11,782

Working costs to be recovered 4,768 3,537 278

Receivable for investment in Patagonian Pipeline (Note 12.6) 38,470 40,312 -

Miscellaneous 3,808 1,260 1,633

162,498 109,450 76,194

(1) It corresponds to representative debt instruments related to the construction work of Gasoducto Loop Regional Sur. At the date of issuance of

these consolidated financial statements, the gas charge corresponding to this trust is pending of enactment by the Secretariat, from which the

trust will proceed to pay the respective installments (Nota 12.8).

e) Inventories:

Current

Materials and spare parts 1,799 1,826 7,823

Work in progress for third parties - 8,020 -

1,799 9,846 7,823

Non-current

Materials and spare parts 31,978 18,855 5,227

31,978 18,855 5,227

19

GENNEIA S.A.

f) Fixed assets, assets under concession and intangible assets:

Evolution of fixed assets

2013

Cost

Main account

Accumulated

at the

beginning of

year Increases Decreases Transfers

Translation

difference

Accumulated

at the end of

the year

Land 14,617 - - - 4,765 19,382

Furniture and fixture 1,968 15 - - 628 2,611

Machinery 7,039 169 (166) - 2,264 9,306

Computer equipment 13,597 3,222 - - 4,749 21,568

Communication equipment 245 4 - - 81 330

Vehicles 6,512 - (462) - 2,004 8,054

Buildings and installations 1,651 6,628 - - 1,912 10,191

Tools 1,452 394 (146) - 474 2,174

Materials and spare parts 267 - - (240) 2 29

Pipelines 48,217 - - - (79) 48,138

Power generation equipment 1,073,633 458,557 (29,211) 67,768 460,106 2,030,853

Wind Farm 753,367 - - - 245,557 998,924

Fixed assets for gas distribution business 3,488 - (4,625) - 1,137 -

Work in progress 40,144 95,754 (110) (67,528) 20,409 88,669

Total 2013 1,966,197 564,743 (34,720) - 744,009 3,240,229

Total 2012 1,760,661 74,121 (110,814) - 242,229 1,966,197

Total 2011 1,187,847 493,056 (30,480) - 110,238 1,760,661

2013

Accumulated Depreciation

Main account

Accumulated

at the

beginning of

year % Increases Decreases

Translation

difference

Accumulated

at the end of

the year

Net book

value at

12-31-13

Net book

value at

12-31-12

Net book

value at

12-31-11

Land - - - - - - 19,382 14,617 11,607

Furniture and fixture 1,762 10% 56 - 567 2,385 226 206 149

Machinery 6,131 10% 1,264 (132) 2,043 9,306 - 908 1,553

Computer equipment 11,073 33% 1,658 - 3,719 16,450 5,118 2,524 2,648

Communication equipment 225 33% - - 89 314 16 20 11

Vehicles 3,504 20% 840 (419) 1,499 5,424 2,630 3,008 2,041

Buildings and installations 367 10% 1,594 - 187 2,148 8,043 1,284 1,112

Tools 487 10% 61 (68) 273 753 1,421 965 505

Materials and spare parts - - - - - - 29 267 316

Pipelines 13,999 3%-7% 3,231 - 14 17,244 30,894 34,218 72,795

Power generation equipment 435,483 5%-10% 160,982 (2,827) 166,886 760,524 1,270,329 638,150 646,005

Windfarm 41,571 6% 47,146 - 21,923 110,640 888,284 711,796 -

Fixed assets for gas distribution business 3,488 - - (4,625) 1,137 - - - 23,412

Work in progress - - - - - - 88,669 40,144 673,476

Total 2013 518,090 216,832 (8,071) 198,337 925,188 2,315,041

Total 2012 325,031 159,844 (23,126) 56,341 518,090 1,448,107

Total 2011 188,075 133,243 (15,934) 19,647 325,031 1,435,630

Allowance for impairment of fixed assets - - (10,329)

Total 2,315,041 1,448,107 1,425,301

20

GENNEIA S.A.

Evolution of assets under concession:

2013

Cost

Main account

Accumulat

ed at the

beginning

of year Increases Decreases Transfers

Translation

difference

Accumulated

at the end of

the year

Power generation equipment 30,487 - - 5,808 11,311 47,606

Work in progress 5,202 223 - (5,808) 383 -

Total 2013 35,689 223 - - 11,694 47,606

Total 2012 27,752 3,587 - - 4,350 35,689

Total 2011 24,721 952 - - 2,079 27,752

2013

Accumulated Depreciation

Main account

Accumulat

ed at the

beginning

of year % Increases Decreases

Translation

difference

Accumulated

at the end of

the year

Net book

value at

12-31-13

Net book value

at

12-31-12

Net book value

at

12-31-11

Power generation equipment 12,356 - 8,272 - 6,497 27,125 20,481 18,131 18,792

Work in progress - 5% - - - - - 5,202 1,071

Total 2013 12,356 8,272 - 6,497 27,125 20,481

Total 2012 7,889 3,091 - 1,376 12,356 23,333

Total 2011 4,586 2,807 - 496 7,889 19,863

Evolution of intangible assets

2013 2012 2011

Book value at the beginning of the year 31,675 - 8

Acquisitions through business combinations (Note 12.5) - 27,526 -

Translation difference 10,324 4,149 -

Depreciation - - (8)

Allowance for impairment of intangible assets (Note 5.m) (11,624) - - -

Book value at the end of the year 30,375 31,675 -

g) Other assets

Non-current

Construction of gas pipeline - Santa Fe Ruta 34 15,149 11,425 9,999

Miscellaneous - 214 33

Allowance for construction of gas pipeline - Santa Fe Ruta 34

(Note 5.m) (15,149)

(11,425) (9,999)

- 214 33

21

GENNEIA S.A.

h) Assets classified as held for sale and liabilities associated with assets classified as held for sale:

As described in Note 12.7, the Company and Proagas S.A. entered into an agreement whereby the Company sold its natural gas distribution business. The major types of assets and liabilities of the distribution business as of the fiscal year ended December 31, 2012 were the following:

2013 2012 2011

Assets classified as held for sale:

Trade receivables – Sale of gas and others - 11,998 -

Accrual for unbilled consumption of gas - 1,031 -

Allowance for doubtful accounts - (4,374) -

Fixed assets in the natural gas distribution business - 25,379 -

Allowance for impairment of fixed assets (Note 5.m) - (25,379) -

- 8,655 -

Liabilities associated with assets classified as held for sale:

ENARGAS withholdings payable – Decree N° 2067 - 4,772 -

- 4,772 -

Liabilities

i) Accounts Payable:

Current

Trade 410,629 172,583 125,949

Accrual for invoices pending to receive 106,050 101,818 148,329

Accrual for construction costs - 7,956 1,259

Advances from customers 2,870 3,031 -

Related parties (Note 6) 285 213 799

519,834 (1) 285,601 276,336

(1) Includes 94,040 past due up to three months, 17,398 from three to six months, 82,857 from six to nine months, 67,890 from nine to twelve

months and 169,166 over a year. See Note 7.3.3 in relation to the aging of past due account payables.

22

GENNEIA S.A.

2013 2012 2011

j) Loans:

Current

Negotiable obligations 172,498 189,137 85,168

Other bank and financial debts 119,504 54,089 37,102

Related parties, net of commissions (Note 6) 24,475 16,057 111,235

Financial leasings 47,568 982 857

Bank overdraft - 23,468 -

364,045 283,733 234,362

Non-current

Negotiable obligations 1,227,632 677,427 567,126

Other bank and financial debts 218,938 79,225 85,125

Related parties, net of commissions (Note 6) 174,925 139,676 232,725

Financial leasings 27,085 1,054 400

1,648,580 897,382 885,376

k) Salaries and social security payable:

Salaries, social security and withholdings payables 22,309 13,299 10,657

Social security and withholdings payables – Regularization

regime - 2,518 2,013

22,309 15,817 12,670

l) Taxes Payable:

Current

Minimum presumed income tax payable (net of advances) 9,679 13 454

Income tax payable 2,919 3,523 -

Value added tax 12,025 3,062 -

Tax withholdings payable 7,015 3,213 1,375

ENARGAS withholdings payable - Decree No. 2067

- - 3,559

Turnover tax 247 1,196 -

Taxes under regularization regime 297 380 381

Program for the rational use of energy

- 494 338

Miscellaneous - 2,153 1,705

32,182 14,034 7,812

Non-current