general sales tax - ma-acc.comma-acc.com/files/laws/general sales taxes 11-1991.pdf · 2 medhat...

TRANSCRIPT

1

MMeeddhhaatt GGhhaallyy && AAllbbeerrtt EEddwwaarrdd –– CChhaarrtteerreedd AAccccoouunnttaannttss AAuuddiittss && CCoonnssuullttaanncciieess FFiirrmm -- EEggyypptt

General Sales Tax

Law No(11) of the year 1991

On promulgation of the General Sales Tax Law

In the name of the people,

The President of the Republic,

The People's Assembly has passed the following Law, and it has been issued:

Article(1)

The General Sales Tax shall be governed by the provisions of the attached Law.

Article (2)

Law No (133) of the year 1981 on Consumption Tax shall hereby be repealed.Also any other provision(s) inconsistent with the provisions herein shall be repealed.

Article(3)

The name Consumption Tax Department shall, wherever stated in the applicable laws, decrees and regulations be replaced by the name Sales Tax Department

Article(4)

The provisions of this Law shall not prejudice the exemptions established by the agreements concluded between the Egyptian Government and foreign countries or international and regional organizations, or by virtue of petroleum and mining agreements.

Article (5)

This Law shall be published in the Official Gazette and shall come into force as of the next day of publication.

The Minister of Finance shall, within one month of enforcement, issue the executive regulations hereof.

This Law shall receive the seal of the State and shall come into force as one of the State Laws.

The Presidency of the Republic on 13th of. Shawal , 1411 AH corresponding, 28 th of.April, 1991.

Hosni Mubarak

Cairo:

Tel & Fax: +202 39 26 231 / 39 59 150 Abdel Khalek Tharwat St. – 4th Floor - Egypt

E-mail: [email protected]

Sharm El-Sheikh: Tel & Fax: 069 36 02 035

Sharm Trade Center - Naama Bay – Egypt [email protected]

Web site: www.ma-acc.com

2

MMeeddhhaatt GGhhaallyy && AAllbbeerrtt EEddwwaarrdd –– CChhaarrtteerreedd AAccccoouunnttaannttss AAuuddiittss && CCoonnssuullttaanncciieess FFiirrmm -- EEggyypptt

General Sales Tax Law

Chapter 1

Preliminary Provision

Article (1)

In application of the provisions of this Law, the following shall mean:

The Minister :

The Minister of Finance.

The Commissioner:

The Commissioner of the Sales Tax Department.

The Department :

The Sales Tax Department.

The Tax :

The General Sales Tax.

Taxable person:

The natural or juridical person required to collect and pay the Tax to the Department whether said person is a manufacturer, a trader or a supplier of a taxable service(s) whose sales reach the registration threshold specified herein.Also each and every importer of a taxable commodity or service for commercial purposes regardless of his/her annual turnover.

Commodity :

Each and every manufactured product(s) whether locally manufactured or imported.

In defining commodity,the remarks and provisions stated in the sections and chapters of Customs Tariff shall be taken as guide.

Service:

Each service stated in Table No(2)attached hereto.

Sale:

The transfer of ownership of commodity or the supply of service from the seller, even if he/she is an importer, to the purchaser for the purposes of this Law.The following shall, in application of the provisions of this Law, be deemed sale whichever occurs first:

Cairo:

Tel & Fax: +202 39 26 231 / 39 59 150 Abdel Khalek Tharwat St. – 4th Floor - Egypt

E-mail: [email protected]

Sharm El-Sheikh: Tel & Fax: 069 36 02 035

Sharm Trade Center - Naama Bay – Egypt [email protected]

Web site: www.ma-acc.com

3

MMeeddhhaatt GGhhaallyy && AAllbbeerrtt EEddwwaarrdd –– CChhaarrtteerreedd AAccccoouunnttaannttss AAuuddiittss && CCoonnssuullttaanncciieess FFiirrmm -- EEggyypptt

• Issuance of invoice. • Delivery of commodity or supply of service. • Payment of consideration for the commodity or service whether fully or partially,

or payment of a down payment or as settlement of accounts or on credit or any other form of payment in accordance with any of the terms and conditions of payment.

Manufacture :

Conversion of material, whether organic or inorganic, manually, mechanically or by any other means, into a new product, or changing the size or shape or components or nature or kind thereof.

Assembling parts of equipment, packing and repacking, preservation in boxes, parcels, bottles or any other containers shall be deemed manufacture.

However, packing of unprocessed agricultural products as they are and / or packing by retailers when directly selling to consumer and installing of machinery and equipment for construction purposes , shall not be deemed manufacture.

Manufacturer:

All and every natural or juridical person, regularly or accidentally and whether as principal or agent who carries on any manufacturing process.

Service Supplier:

All and every natural or juridical person who supplies a taxable service.

Importer:

All and every natural or juridical person who imports taxable goods or services for commercial purposes.

Registrant:

The taxable person registered at the Sales Tax Department under the provisions of this Law.

Tax invoice:

The invoice prepared in accordance with the form prescribed in a decree by the Commissioner.

Month :

The calendar month.

Cairo:

Tel & Fax: +202 39 26 231 / 39 59 150 Abdel Khalek Tharwat St. – 4th Floor - Egypt

E-mail: [email protected]

Sharm El-Sheikh: Tel & Fax: 069 36 02 035

Sharm Trade Center - Naama Bay – Egypt [email protected]

Web site: www.ma-acc.com

4

MMeeddhhaatt GGhhaallyy && AAllbbeerrtt EEddwwaarrdd –– CChhaarrtteerreedd AAccccoouunnttaannttss AAuuddiittss && CCoonnssuullttaanncciieess FFiirrmm -- EEggyypptt

The Fiscal Year :

Twelve months starting and expiring with the fiscal year of the taxable person.

The wholesaler :

All and every natural or juridical person who sells taxable commodities to others who sell or manufacture such purchases.

The Retailer:

All and every natural or juridical person who sells his / her taxable purchases as they are to the final consumer.

The Additional Tax:

A sales tax of 0.5 % of the unpaid tax per week or part thereof allover the period succeeding last due date of G.S.T payment.

Input Tax :

The Tax previously charged on the intermediary goods used in manufacturing taxable goods.

Exempted goods :

The goods included in the exemption lists.

Phases of Tax application:

Phase 1:

In which a manufacturer and / or an importer and / or a service supplier are required to collect and pay the tax to the Department.

Phase 2:

In which the manufacturer and / or the importer and / or the service supplier as well as the wholesaler are required to collect and pay the Tax to the Department.

Phase 3:

In which the manufacturer and /or the importer and /or the service supplier and / or the wholesaler as well as the retailer are required to collect and pay the Tax to the Department.

Cairo:

Tel & Fax: +202 39 26 231 / 39 59 150 Abdel Khalek Tharwat St. – 4th Floor - Egypt

E-mail: [email protected]

Sharm El-Sheikh: Tel & Fax: 069 36 02 035

Sharm Trade Center - Naama Bay – Egypt [email protected]

Web site: www.ma-acc.com

5

MMeeddhhaatt GGhhaallyy && AAllbbeerrtt EEddwwaarrdd –– CChhaarrtteerreedd AAccccoouunnttaannttss AAuuddiittss && CCoonnssuullttaanncciieess FFiirrmm -- EEggyypptt

Chapter 2

Imposition and Liability of Tax

Article (2)

General Sales Tax ( G.S.T) shall be levied on locally manufactured goods or imported goods except goods exempted by a special provision.

The Tax shall also be levied on services stipulated in table (2) attached hereto.

Goods and services exported shall be subject to a zero rate in accordance with terms and conditions specified in the Executive Regulations hereof.

Article (3)*

Standard tax rate levied on commodities shall be 10 %, except commodities stipulated in table (1) attached hereto where applicable tax rate shall be that specified for each therein.

Tax rate(s) on services shall be those specified in table (2) attached hereto.

*The third article is amended by virtue of law No.2 of 1997 published in the Official Gazette,edition No.4(bis) on 29-1-1997.Before amendment the article stipulated the following:

The standard tax rate levied on commodities shall be 10%, except commodities stipulated in Table(1) attached hereto where applicable tax rate shall be that specified for each therein.Tax rate(s) on services shall be that specified in Table(2) attached hereto

The President of the Republic may, by a decree, exempt certain goods from tax and may amend tax rate on certain goods.

The President of the Republic may amend Tables(1) and (2) attached hereto.In all cases the Presidential decree shall be presented to People's Assembly within 15 days as of date of publication of such decree in case the People's Assembly is in session.Otherwise, the decree shall be presented to the People's Assembly in the first session thereof.In case the decree is not passed by the People's Assembly, the decree shall not be in effect but is not effective as to the period from date of publication of such decree to the date of the said session.

Cairo:

Tel & Fax: +202 39 26 231 / 39 59 150 Abdel Khalek Tharwat St. – 4th Floor - Egypt

E-mail: [email protected]

Sharm El-Sheikh: Tel & Fax: 069 36 02 035

Sharm Trade Center - Naama Bay – Egypt [email protected]

Web site: www.ma-acc.com

6

MMeeddhhaatt GGhhaallyy && AAllbbeerrtt EEddwwaarrdd –– CChhaarrtteerreedd AAccccoouunnttaannttss AAuuddiittss && CCoonnssuullttaanncciieess FFiirrmm -- EEggyypptt

Article (4)

Phase (1) of the application of the General Sales Tax shall be in effect as of the date of enactment of this Law.Concerning collection of the Tax on some commodities, the President of the Republic may, by a presidential decree, allow the move to phase (2) or phase (3) therefor.

Article (5)

Taxable persons shall collect the Tax, state the amounts thereof in a return to be filed to the Department accompanied with payment of such amounts on the dates prescribed herein.

Article (6)

The Tax shall be due at the point of sale of a commodity or the supply of a service by a taxable person in accordance with the provisions of this Law.

Using goods or making use of service by taxable persons for private or personal purposes or any legal disposal shall be deemed sale.

The Tax shall be due on imported goods at their release from Customs.For such commodities the taxable point shall be same of Customs , and G.S.T.shall be collected in accordance with the procedures stated thereto.

In the absence of provisions stipulated in this Law, the rules stipulated in Customs Law shall be applied to such imported goods.

Article (7)

Goods or services exported by the businesses of free zones and free cities and free shops shall be subject to zero rate.

With the exception of automobiles, imported goods or services by such businesses for carrying out the licenced activities thereof shall not be taxed.

The Tax shall not be due on transit goods provided that such transit is made under the control of Customs in accordance with the procedures and conditions and guarantees specified in the Executive Regulations.

Article (8)

Without prejudice to the provision of the second paragraph of article (7) and in accordance with the provisions of this law, the Tax shall be due on the taxable goods or services imported to free zones and free cities and free shops for domestic consumption therein.

Import for trading purposes in free zones, forming a whole city, shall be deemed domestic consumption.

Cairo:

Tel & Fax: +202 39 26 231 / 39 59 150 Abdel Khalek Tharwat St. – 4th Floor - Egypt

E-mail: [email protected]

Sharm El-Sheikh: Tel & Fax: 069 36 02 035

Sharm Trade Center - Naama Bay – Egypt [email protected]

Web site: www.ma-acc.com

7

MMeeddhhaatt GGhhaallyy && AAllbbeerrtt EEddwwaarrdd –– CChhaarrtteerreedd AAccccoouunnttaannttss AAuuddiittss && CCoonnssuullttaanncciieess FFiirrmm -- EEggyypptt

Except as provided in the two prior paragraphs of this article and in accordance with the provisions of this Law the Tax shall be due on the taxable goods and services imported from free zones and free cities and free shops to local markets.

Services or goods manufactured in the businesses of free zones and free cities shall be dealt with in the same way as imported goods withdrawn for local consumption.

Executive Regulations shall specify the limits and organizing rules of the enactment of this article and article(7).

Article (9)

In case of termination or liquidation of a taxable business, the Tax shall be due on the goods in possession of the registrant at time of disposal unless the successor is a registrant or applied for registration under the provisions of this Law.

Article (10)

Without prejudice to the penalties provided for in this Law, unreported sales and sales made in violation of the rules stated herein shall be subject to the tax rates in effect at the date of such crime or offense.

If such date is unidentified such sales shall be subject to the tax rates effective in time of seizure or discovery of offense.

Chapter (3)

Value assessment

Article (11)

The value to be reported in the return and taken as a basis for tax calculation shall be the consideration ACTUALLY PAID for taxable goods sold and / or taxable services rendered by a registered to an independent person in normal circumstances.Otherwise the consideration for such goods and / or services shall be the market price thereof in normal circumstances in accordance with the rules stipulated in the Executive Regulations hereof.

Value of imported goods shall be the value for Customs purposes at time of release from Customs plus the Customs duties and any other taxes, duties and levies thereon.

The Minister may, after agreement with the competent minister, issue price lists for certain goods or services to be taken as a base for tax calculation.

Cairo:

Tel & Fax: +202 39 26 231 / 39 59 150 Abdel Khalek Tharwat St. – 4th Floor - Egypt

E-mail: [email protected]

Sharm El-Sheikh: Tel & Fax: 069 36 02 035

Sharm Trade Center - Naama Bay – Egypt [email protected]

Web site: www.ma-acc.com

8

MMeeddhhaatt GGhhaallyy && AAllbbeerrtt EEddwwaarrdd –– CChhaarrtteerreedd AAccccoouunnttaannttss AAuuddiittss && CCoonnssuullttaanncciieess FFiirrmm -- EEggyypptt

Article (12)

Without prejudice to any other procedures provided for herein if the value of sales of the registrant proved to be different from that reported in his /her return at any taxable period, the Department may amend the taxable value.

In all cases, the registrant may appeal against the assessment of the Department in accordance with measures and procedures specified in this Law.

Article (13)

The value of the tax shall be added to the price of goods or services including price-fixed and profit-determined goods and services.

At time of imposition of Tax or at time of amending rates thereof, prices included in contracts whose party or parties are registered persons may be accordingly amended so as to consider such burden of tax or of tax amendments.

Chapter (4)

Invoices,Returns, Notifications,

Books and Records

Article (14)

The registrant shall issue a tax invoice when supplying taxable goods and /or services in accordance with the provisions of this Law.

The Executive Regulations shall specify rules and procedures that guarantee the regularity of invoices and facilitate the control and check thereof.

Article (15)

The registrant shall keep regular accounting books and records to regularly record the transactions made.The registrant shall keep such records and copies of invoices mentioned above in the previous article for three years following the end of the fiscal year during which entries were made therein.

The Executive Regulations shall specify limits, rules, and procedures to be followed and records and documents to be kept by the registrant as well as data to be recorded therein.

Article (16)

All and every registrant shall submit to the Department a monthly return stating the tax due on the form prepared therefor within thirty days following the end of the taxable month.

Cairo:

Tel & Fax: +202 39 26 231 / 39 59 150 Abdel Khalek Tharwat St. – 4th Floor - Egypt

E-mail: [email protected]

Sharm El-Sheikh: Tel & Fax: 069 36 02 035

Sharm Trade Center - Naama Bay – Egypt [email protected]

Web site: www.ma-acc.com

9

MMeeddhhaatt GGhhaallyy && AAllbbeerrtt EEddwwaarrdd –– CChhaarrtteerreedd AAccccoouunnttaannttss AAuuddiittss && CCoonnssuullttaanncciieess FFiirrmm -- EEggyypptt

The Minister may, by a decree , extend the 30 day period as may be convenient*.

The registrant shall file said return even if no taxable supplies were made within the taxable month.

Without prejudice to criminal impeachment, if the registrant failed to file the return stipulated herein the Department is entitled to assess the tax due on the accounting period thereof, such assessment shall include bases thereof.

*This period was extended by virtue of the ministerial decree no 190 of 1991 published on 20/6/91 in the Official Gazette no 140 to the effect that the monthly return shall be filed and the due tax shall be paid within the two months following the taxable month with the exception of Table 1 commodities manufacturers who are still committed to the old 30 day period.

The ministerial decree no 651 of 1994 was issued adding to the ministerial decree no 190 of 1991the following paragraph:

Tax return of April shall be filed and the due tax shall be paid not later than the 15 th of June

Article (17)*

The Department may amend the return provided for in the previous article. The registrant shall be notified of such amendment by a registered letter with a return receipt within three years as of the date of submitting the return to the Department.

The registrant may appeal to the Commissioner within thirty days as of the date of receiving the notification. If such appeal is refused or not settled within sixty days, the registrant may apply for referring such dispute to reconciliation committees stipulated herein within the sixty days following the notification of the registrant of refusing the appeal thereof by a registered letter with a return receipt or within the sixty days following the expiry of the period stipulated herein for deciding on the appeal.

In case such appeal is not made or the application for reconciliation is not submitted within the dates mentioned above, the assessment made by the Department shall be final.

A registrant may object to the assessment of the Department before first instance court within thirty days of being final.

Cairo:

Tel & Fax: +202 39 26 231 / 39 59 150 Abdel Khalek Tharwat St. – 4th Floor - Egypt

E-mail: [email protected]

Sharm El-Sheikh: Tel & Fax: 069 36 02 035

Sharm Trade Center - Naama Bay – Egypt [email protected]

Web site: www.ma-acc.com

10

MMeeddhhaatt GGhhaallyy && AAllbbeerrtt EEddwwaarrdd –– CChhaarrtteerreedd AAccccoouunnttaannttss AAuuddiittss && CCoonnssuullttaanncciieess FFiirrmm -- EEggyypptt

* Amended on 30-3-2005 by Law No.9 of 2005 .

Chapter 5

registration

Article (18)

All and every manufacturer whose total value of sales of locally manufactured taxable and exempt goods during the 12 months preceding date of enactment of this Law reached or exceeded L.E 54000, AND all and every supplier of taxable service(s) whose value of supplies reached or exceeded said amount in same period SHALL, within the period determined by the Minister, apply for registration of his / her name and details on the form prepared therefor.

For the purposes of this Law, each and every productive family registered in the records of the Ministry of Social Affairs shall be deemed A MANUFACTURER in accordance with provisions agreed upon with the Ministry of Social Affairs.

The Minister may amend the above mentioned registration threshold.

After enactment of this Law, all and every natural or juridical person who becomes taxable under each phase of application and whose value of supplies in any fiscal year or part thereof reached or exceeded the registration threshold SHALL, within the period determined by the Minister, apply for registration on the above-mentioned form and shall be subject to the provisions of this Law as of the beginning of the month following that in which the total value of his / her supplies reached or exceeded the registration threshold.

All and every importer and distribution agent of taxable persons shall apply for registration.

The Executive Regulations shall specify the application form and the information to be included therein as well as terms and conditions and rules of registration.

Article (19)

The natural or juridical person who does not reach the registration threshold may apply to the Department for registration in accordance with terms and conditions and procedures specified in the Executive Regulations.In such case, such person shall be taxable and shall be subject to all provisions of this Law.

Cairo:

Tel & Fax: +202 39 26 231 / 39 59 150 Abdel Khalek Tharwat St. – 4th Floor - Egypt

E-mail: [email protected]

Sharm El-Sheikh: Tel & Fax: 069 36 02 035

Sharm Trade Center - Naama Bay – Egypt [email protected]

Web site: www.ma-acc.com

11

MMeeddhhaatt GGhhaallyy && AAllbbeerrtt EEddwwaarrdd –– CChhaarrtteerreedd AAccccoouunnttaannttss AAuuddiittss && CCoonnssuullttaanncciieess FFiirrmm -- EEggyypptt

Article (20)

The Department shall keep a registration record including all details thereof after ensuring authenticity of such details and shall issue a registration a certificate for each registrant.

The Executive Regulations shall specify terms and conditions, rules and procedures concerning registration certificates and information included therein.

Article(21)

Each and every registrant shall notify the Department in writing of any changes that may occur to details previously presented in the application for registration within twenty one days of occurrence of such changes.

Article (22)

The Commissioner may cancel the registration in cases stipulated in the Executive Regulations, in accordance with terms and conditions thereof.

Chapter 6

Tax Credit, Exemption, and Refund

Article (23)

When calculating amounts of Tax due the registrant may, according to the limits and terms and conditions stipulated in the Executive Regulations, deduct tax previously paid or charged on his inputs and tax on returned goods as well as deducting tax paid or charged at every stage of distribution from tax due on his sales of goods.

The deduction referred to herein shall not be applicable to commodities listed in table No (1) attached hereto.

In case of exportation, when the deductible Tax exceeds Tax due on sales, the Department shall refund the discrepancy in accordance with terms and conditions and procedures specified in the Executive Regulations within a period not exceeding three months from date of applying for such refund.

Article (23 bis)*

When calculating the tax due, a registrant may deduct from the tax amount due on his / her sales of goods and services the tax previously paid on machines, equipment, parts, and accessories thereof used in manufacturing a taxable commodity or performing a taxable service except for motor vehicles for the transport of persons and motor cars, unless such vehicles and cars are used for carrying out the licensed activity of the of the business.

Cairo:

Tel & Fax: +202 39 26 231 / 39 59 150 Abdel Khalek Tharwat St. – 4th Floor - Egypt

E-mail: [email protected]

Sharm El-Sheikh: Tel & Fax: 069 36 02 035

Sharm Trade Center - Naama Bay – Egypt [email protected]

Web site: www.ma-acc.com

12

MMeeddhhaatt GGhhaallyy && AAllbbeerrtt EEddwwaarrdd –– CChhaarrtteerreedd AAccccoouunnttaannttss AAuuddiittss && CCoonnssuullttaanncciieess FFiirrmm -- EEggyypptt

Tax credit shall be made within the amounts of tax due. The amount that is not deducted shall be carried forward to the following tax period(s) until exhausting such amount in full.

The minister of finance shall set rules for the payment of tax charged on machinery and equipment.

* Added on 30-3-2005 by Law No.9 of 2005 .

Article (24)

On reciprocity basis and within the limits of such treatment and in accordance with the information of the Ministry of Foreign Affairs, the following shall be exempted from Tax:

• Purchases and imports for personal use by foreign members of diplomatic and consular corps ( non honorary) listed in tables issued by the Ministry of Foreign Affairs, and purchases and imports for personal use of their spouses and minors.

• Purchases and / or imports for official use by non-honorary embassies, legations and consulates except food, spirits and tobacco.Vehicles exempted under items (1) and (2) shall be one car for personal use, five cars for official use of each embassy or legation and two cars for official use of each consulate.The Minister may, in accordance with agreement with the Minister of Foreign Affairs, raise such limits.

• Imported baggage, furniture and home appliances as well as only one used car for every foreign official person working in such Diplomatic or Consular Missions who does not benefit from exemptions stipulated in item (1) of this article, provided that importing such items occurs within six months from the arrival date of the beneficiary. The Minister may, by an agreement with the Minister of Foreign Affairs, extend such six month period.

The exemptions referred to in this Article shall be effective after the approval of the Head of Diplomatic or Consular Mission, as the case may be, being granted on exemptions application and ratification thereof by the Ministry of Foreign Affairs.

Article (25)

Items exempted under the previous article shall not be disposed of for purposes other than those they were exempted for within five years of such exemption unless the Department is notified and the Tax due on such items is paid according to the state and value thereof and the effective tax rate on the date of payment and unless reciprocity principle requires otherwise.

The Executive Regulations shall stipulate rules and procedures therefor.

Cairo:

Tel & Fax: +202 39 26 231 / 39 59 150 Abdel Khalek Tharwat St. – 4th Floor - Egypt

E-mail: [email protected]

Sharm El-Sheikh: Tel & Fax: 069 36 02 035

Sharm Trade Center - Naama Bay – Egypt [email protected]

Web site: www.ma-acc.com

13

MMeeddhhaatt GGhhaallyy && AAllbbeerrtt EEddwwaarrdd –– CChhaarrtteerreedd AAccccoouunnttaannttss AAuuddiittss && CCoonnssuullttaanncciieess FFiirrmm -- EEggyypptt

Article (26)

the Minister may, by a decree, and in agreement with the Minister of Foreign Affairs, exempt imports by distinguished foreign persons for personal use as a comity of nations.

Article (27)

The following shall , within the limits, terms and conditions prescribed in the Executive Regulations, be exempted:

1. Samples consumed in analysis purposes in the governmental laboratories. 2. Non-commercial personal effects such as decorations, medals and prizes

for scientific or sport distinction. 3. Imported supplies, with no compensation for damage or loss, in

consignments previously supplied or rejected and for which full tax was then paid after verification by Customs.

4. Personal luggage of travelers arriving from abroad. 5. Tax – paid goods that were previously exported and re-imported, in the

same state after verification by the Customs.

Article (28)

The Minister may, by a decree, and in agreement with the competent minister, exempt certain goods in each of the following:

1. Gifts, donations and presents to the State Administration or municipalities. 2. Imports for scientific, educational and cultural purposes by scientific,

educational bodies and scientific research institutes.

Article (29)*

All taxable commodities, equipment, machinery and services necessary for armament purposes of defense and national security, as well as raw materials, production prerequisites and components thereof, shall be exempted.

The minister may, by a decree, determine the goods and services to be exempted by virtue of the above-mentioned paragraph.

* Amended on 30-3-2005 by Law No.9 of 2005 .

Article (30)

Tax exemptions set forth in other laws and decrees shall not be applicable to G.S.T.unless explicitly provided for.

Cairo:

Tel & Fax: +202 39 26 231 / 39 59 150 Abdel Khalek Tharwat St. – 4th Floor - Egypt

E-mail: [email protected]

Sharm El-Sheikh: Tel & Fax: 069 36 02 035

Sharm Trade Center - Naama Bay – Egypt [email protected]

Web site: www.ma-acc.com

14

MMeeddhhaatt GGhhaallyy && AAllbbeerrtt EEddwwaarrdd –– CChhaarrtteerreedd AAccccoouunnttaannttss AAuuddiittss && CCoonnssuullttaanncciieess FFiirrmm -- EEggyypptt

Article (31)

In accordance with terms, conditions and limits prescribed in the Executive Regulations , and at a date not exceeding three months following date of applying for refund , Tax shall be refunded in each of the following:

• Tax previously collected on goods exported in its same state or as components in other exported goods;

• Tax collected by error on the receipt of an application by the person concerned.

Chapter 7

Tax Collection

Article (32)

In accordance with rules and regulations set forth in the Executive Regulations, the registrant shall regularly pay the tax to the Department with the monthly return at the date stipulated in article (16) of this Law.

Tax on imported goods shall be paid at release thereof from Customs and according to procedures followed at payment of Customs duties, such goods shall NOT be finally released before payment of the whole tax dues.

In case of non-payment of Tax at due date(s), the Additional Tax shall be due and collected with the tax under the same rules and regulations.

Article (33)

For the services of continuous nature stipulated in the Executive Regulations, issuance of invoice by the supplier of service shall be deemed the taxable act according to the provisions of this Law.

Article (34)

Tax and other amounts due to the Department according to this Law shall be granted a lien on all the property of debtors or taxable persons charged with collecting and remitting such tax and amounts to the Department by virtue of the Law.Said tax-dues shall be preferential over all other debts with the exception of juridical expenses.

Cairo:

Tel & Fax: +202 39 26 231 / 39 59 150 Abdel Khalek Tharwat St. – 4th Floor - Egypt

E-mail: [email protected]

Sharm El-Sheikh: Tel & Fax: 069 36 02 035

Sharm Trade Center - Naama Bay – Egypt [email protected]

Web site: www.ma-acc.com

15

MMeeddhhaatt GGhhaallyy && AAllbbeerrtt EEddwwaarrdd –– CChhaarrtteerreedd AAccccoouunnttaannttss AAuuddiittss && CCoonnssuullttaanncciieess FFiirrmm -- EEggyypptt

Chapter(8)

Reconciliation

Article (35)*

In exception to the provisions of law no. 7 of 2000 on formation of reconciliation committees for settling certain disputes that ministries and public judicial persons are parts thereof, in case of a dispute with the Department regarding value, kind or quantity of good(s) or service(s) or regarding amount of tax due and the person

concerned applied for referring such dispute to reconciliation committees at the date stipulated in article (17) herein, the Commissioner or his / her legal representative shall within fifteen days of being notified of the application for reconciliation submit the dispute, as preliminary stage to the afore-mentioned committee. The reconciliation committee shall consist of two members one thereof shall be appointed by the Department and the other by the person concerned.

In case of concurrence by both, their decision shall be final.

In case of non- conclusion of preliminary stage either because of failure by the person concerned to nominate a representative thereof or failure by the two members to reach an agreement, the dispute shall be submitted to the committee of appeals constituted of a permanent delegate member other than the employees of the Department appointed by the Minister as a chairman thereof, a representative of the Department appointed by the Commissioner and the person concerned or his/ her representative. Award shall be rendered by majority after hearing the two members of the reconciliation committee, in case the preliminary stage was held. The Committee also may, up to its convenience, hear from experts and technicians.

The award of such committee shall be served to the person concerned and the Department within fifteen days from date of issue by registered letters with return receipt. The award shall come into force and shall define the party committed to bear the costs of appeal.

In all cases the person concerned may object to the award of the committee of appeals before first instance court within thirty days of being notified of the award of appeal.

The Minister shall determine the number and geographical locations and competences of the reconciliation committees and shall decide on the costs of reconciliation as well as the remunerations of members thereof.

*Amended on 30-3-2005 by Law No.9 of 2005 .

Cairo:

Tel & Fax: +202 39 26 231 / 39 59 150 Abdel Khalek Tharwat St. – 4th Floor - Egypt

E-mail: [email protected]

Sharm El-Sheikh: Tel & Fax: 069 36 02 035

Sharm Trade Center - Naama Bay – Egypt [email protected]

Web site: www.ma-acc.com

16

MMeeddhhaatt GGhhaallyy && AAllbbeerrtt EEddwwaarrdd –– CChhaarrtteerreedd AAccccoouunnttaannttss AAuuddiittss && CCoonnssuullttaanncciieess FFiirrmm -- EEggyypptt

Article (36)*

Reconciliation shall not be heard unless accompanied with an evidence of payment of tax as reported in the monthly return stipulated in article (16) herein.

In case the arbitration award is not in the registered person’s favour, the tax and the total amount of discrepancies between the amount paid according to his/ her return and the amount due according to reconciliation shall be paid plus the additional tax on such discrepancies for the period from the date of payment according to the return to the date of payment according to reconciliation.

*Repealed on 6/1/2001 by virtue of the judgement pronounced by the High Constitutional Court.

Article (37)

Concerning imported goods subject to Customs control, provisions and procedures of reconciliation set forth in the Customs Law shall be applicable.

Chapter 9

Department employees

And their duties

Article (38)

For the purposes of enactment of this Law and the executive decrees hereof , The Department Officers, whose jobs are determined by a decree from the Minister of Justice in agreement with the Minister, may have the capacity of Law Officers.

Such officers may, by a written warrant from the Commissioner or any person so authorized, inspect the laboratories, factories, warehouses, shops and firms dealing in taxable goods and services and such Officers may, in case of sequestration, seek assistance from other authorities if necessary.

Article (39)*

The Department Officers who have the capacity of Law Officers may view whatsoever papers, documents, books, records, invoices and instruments related to the application of provisions herein and seize same in the presence of an evidence for an offence against the provisions of this Law. Such Officers may, by a written warrant from the Commissioner or any person so authorized, take specific samples from goods for analysis or inspection.

Cairo:

Tel & Fax: +202 39 26 231 / 39 59 150 Abdel Khalek Tharwat St. – 4th Floor - Egypt

E-mail: [email protected]

Sharm El-Sheikh: Tel & Fax: 069 36 02 035

Sharm Trade Center - Naama Bay – Egypt [email protected]

Web site: www.ma-acc.com

17

MMeeddhhaatt GGhhaallyy && AAllbbeerrtt EEddwwaarrdd –– CChhaarrtteerreedd AAccccoouunnttaannttss AAuuddiittss && CCoonnssuullttaanncciieess FFiirrmm -- EEggyypptt

Exchange of data and information amongst revenue authorities of the Ministry of Finance, in accordance with the regulating rules set by a decree of the Minister, shall not be considered a disclosure of confidential information.

*Amended on 30-3-2005 by Law No.9 of 2005 .

Chapter 10

Control

Article (40)

The Executive Regulations shall define the control measures, methods and systems required to implement the provisions of this Law.

Chapter 11

Crimes and Penalties

Article (41)

With the exception of tax evasion acts set forth herein , whomsoever violates the procedures or regulations prescribed in this Law and the Executive Regulation hereof shall be fined a minimum of L.E.100 up to a maximum of L.E.2000 plus the tax due and the additional tax.

The following cases shall be deemed violation of the provisions of this Law:

• Failure to file the return and to pay the tax within the period specified in article (16) herein for a period not exceeding 60 days thereof.*

• Submission of false data regarding sales of taxable goods or services if the excess proved to be not more than 10% over what was stated in the return.

• Violation of the provisions set forth in article (15) of this Law. • In case of shortage or surplus in the goods deposited in the free zones and

shops, not exceeding 10% for justifiable reasons. • Failure to notify the Department of changes occurred in data of the application for

registration form within the period determined. • Obstructing Department Officers from carrying out their duties or exercising their

competences in control and inspection and examination and audit and request and review of documents.

Cairo:

Tel & Fax: +202 39 26 231 / 39 59 150 Abdel Khalek Tharwat St. – 4th Floor - Egypt

E-mail: [email protected]

Sharm El-Sheikh: Tel & Fax: 069 36 02 035

Sharm Trade Center - Naama Bay – Egypt [email protected]

Web site: www.ma-acc.com

18

MMeeddhhaatt GGhhaallyy && AAllbbeerrtt EEddwwaarrdd –– CChhaarrtteerreedd AAccccoouunnttaannttss AAuuddiittss && CCoonnssuullttaanncciieess FFiirrmm -- EEggyypptt

*Amended by Law NO 91 of 1996 published in the Official Gazette NO 25 r. on the 30 th of June , 1996. Before amendment the item stipulated the following:

"Failure to file the return and to pay the tax within the period specified in article ( 16 ) herein for a period not exceeding 30 days thereof".

Article (42)

The Minister or any person so authorized may effect reconciliation regarding the violations stipulated in the preceding article in return for payment of tax and additional tax if due as well as a compensation within the limits of the fine stipulated in the preceding article.

In consequence of reconciliation the criminal action shall be dropped , legal action shall be ceased and all the subsequences thereof shall be annihilated.

Article (43)

:Without prejudice to any heavier penalty provided for in any other Law , attempt or commitment of tax evasion shall be penalized by imprisonment for a term not less than one month and / or a fine not less than L.E 1000 and not exceeding L.E 5000.

Perpetrators and partners shall be sentenced to jointly pay the Tax and The Additional Tax and a compensation not exceeding same amount of tax*.

In case of recommitment of tax evasion, such penalty and compensation may be doubled.Cases of evasion shall be expeditiously heard when submitted to court.

*Amended by Law no. 91 of 1996 published in the Official Gazette no. 25 (bis) on 30/6/1996 Before amendment the article stipulated the following:

Without prejudice to any heavier penalty provided for in any other law, attempt or commitment of tax evasion shall be penalized by imprisonment for a term not less than six months and / or a fine not less than L.E.1000 and not exceeding L.E. 5000. Perpetrators and partners shall be sentenced to jointly pay the Tax and the Additional Tax and a compensation not exceeding three times of the amount of tax. In case assessment of tax is not possible the court shall decide the amount of compensation provided that such compensation shall not exceed L.E.50000.

Article (44)

The following shall be deemed tax evasion penalized by the penalties provided for in the previous article.

Cairo:

Tel & Fax: +202 39 26 231 / 39 59 150 Abdel Khalek Tharwat St. – 4th Floor - Egypt

E-mail: [email protected]

Sharm El-Sheikh: Tel & Fax: 069 36 02 035

Sharm Trade Center - Naama Bay – Egypt [email protected]

Web site: www.ma-acc.com

19

MMeeddhhaatt GGhhaallyy && AAllbbeerrtt EEddwwaarrdd –– CChhaarrtteerreedd AAccccoouunnttaannttss AAuuddiittss && CCoonnssuullttaanncciieess FFiirrmm -- EEggyypptt

• Failure to apply for registration in the prescribed date(s). • Sale or importation of goods and / or supply of service without including the same

in the return accompanied with payment of tax due. • Unjustifiable deduction of tax, fully or partially, in violation of rules and limits of

credit. • Unjustifiable refund or claim of tax refund, fully or partially. • Filing false or fabricated documents or records or data for the purpose of evading

payment of Tax fully or partially. • Underreporting sales if the excess proved to be more than 10% of the amount of

tax reported in the return. • Discovery of shortage or surplus in commodities deposited in free zones and

shops exceeding 10%. • Non- issuance of invoice by the registrant for his / her sales of taxable goods and

/ or services. Non- inclusion of self- supplies in the return. • Failure to file the return and pay the tax for a period exceeding 60 days. • Issue of tax invoice(s) by non- registrants.

*Amended by Law no. 91 of 1996 published in the Official Gazette no. 25 (bis) on the 30th of June , 1996.Before amendment the article stipulated the following:

"Failure to file the return and to pay the tax for a period exceeding 30 days".

Article (45)

Regarding tax evasion crimes, prosecution shall not be submitted to court, nor action shall be set in motion, except by a warrant from the Minister or any person so authorized.

The Minister or any person so authorized may reconcile in said crimes before the delivery of final judgement in return for payment of tax due and Additional Tax as well as a compensation equals same amount of tax *.

In case of delivery of judgement and before being final the Minister or any representative so authorized may reconcile in return for payment of tax and the Additional Tax as well as a compensation equals three times the amount of tax.In case of recurrence of evasion, compensation may be doubled.

Reconciliation, shall terminate the Criminal action and annihilate effects thereof including penalties delivered by the court

The second paragraph in article (45) was amended by Law no. 91 of 1996, before amended the paragraph stipulated the following :

Cairo:

Tel & Fax: +202 39 26 231 / 39 59 150 Abdel Khalek Tharwat St. – 4th Floor - Egypt

E-mail: [email protected]

Sharm El-Sheikh: Tel & Fax: 069 36 02 035

Sharm Trade Center - Naama Bay – Egypt [email protected]

Web site: www.ma-acc.com

20

MMeeddhhaatt GGhhaallyy && AAllbbeerrtt EEddwwaarrdd –– CChhaarrtteerreedd AAccccoouunnttaannttss AAuuddiittss && CCoonnssuullttaanncciieess FFiirrmm -- EEggyypptt

The Minister or any person so authorized may reconcile in said crimes before the delivery of final judgement in return for payment of tax due and Additional Tax as well as a compensation equals two times the amount of Tax.

Article (46)

In case an act of tax evasion is committed by a juridical person, the responsible for such an act shall be the acting partner or the managing director or the delegated member or the chairman of board of directors, whoever actually takes the responsibility of management as the case may be.

Chapter 12

Transitional Provisions

Article (47)

The provisions of this Law shall apply to the commodities of table No (1) attached hereto, without contradiction to the provisions set forth in such table and to the following provisions:

• The tax shall be due at the first point of sale of the domestic commodity or at the Customs tax point for the imported commodities.

The tax shall only be levied again when the state of commodity is changed.

• In case of taxing a commodity or raising the tax rate imposed on certain commodities, importers and wholesalers and semi-wholesalers and distributors and retailers shall submit to the Department a report of stock of such commodities on the day preceding the date on which the above-mentioned taxing or raising is in force within fifteen days from said date.This tax shall be due at the time of submitting such report and shall be paid to the Department within the period determined by the Commissioner, not later than six months from the date of tax maturity.

• The Department may, if necessary, take samples of certain goods to be analyzed and consult competent experts.The person concerned may ask for re-analysis on his own expense and the Minister shall issue a decree determining the methods and procedures of taking samples.

• Any plant or laboratory for producing any of such commodities shall not be established or operated except after receiving a license from the competent administrative body according to the terms and conditions decided by the competent minister in agreement with the Minister.

• Every manufacturer of such commodities shall, in case of total or partial discontinuance of business for any reason, notify the Department and shall notify

Cairo:

Tel & Fax: +202 39 26 231 / 39 59 150 Abdel Khalek Tharwat St. – 4th Floor - Egypt

E-mail: [email protected]

Sharm El-Sheikh: Tel & Fax: 069 36 02 035

Sharm Trade Center - Naama Bay – Egypt [email protected]

Web site: www.ma-acc.com

21

MMeeddhhaatt GGhhaallyy && AAllbbeerrtt EEddwwaarrdd –– CChhaarrtteerreedd AAccccoouunnttaannttss AAuuddiittss && CCoonnssuullttaanncciieess FFiirrmm -- EEggyypptt

the Department promptly after expiry of period of discontinuance in accordance with arrangements and periods prescribed by a decree from the Commissioner.

• The manufacturer or importer of such goods shall, regardless of his / her turnover or value of production, apply to the Department for registration in accordance with the rules and procedures prescribed in the Executive Regulations.

• The beneficiary, whether owner or tenant, of a property designated wholly or partly to carry out a business related to a taxable commodity shall, within a period of three months from the effective date of this Law, notify the Department of the places where the business is carried out and the name of beneficiary, whether owner or tenant.

Regarding places occupied or leased after the effective date of this Law, a notification shall be submitted within a month as of the date of occupation or lease. A notification shall be submitted within a month from date of waiver or expiry of the lease. The beneficiary shall be responsible for the notification.

• Without prejudice to provisions of article (44) herein, judgement (by the court) shall in all cases include confiscation of smuggled goods and, if unseized, shall include payment of value thereof. Judgement may include confiscation of all means of transport as well as equipment and materials used in smuggling except ships and aircraft unless specially rented or prepared for smuggling such goods.

• Regarding Table (1) commodities and without prejudice to tax evasion acts afore-mentioned in article (44) of this Law, the following acts shall be deemed tax evasion acts and shall be penalized by the penalties prescribed in such article:

• Possession of taxable goods for trading purpose with cognizance that such goods are smuggled.

Such cognizance shall be presumed in case the possessor fails to submit the documents proving payment of tax.

• Operating plants and/ or laboratories producing such goods without notifying the Department.

• Putting false and fabricated marks or seals to avoid, wholly or partially, payment of tax.

The Executive Regulations shall determine the amounts to be collected by the Department as a consideration for printed materials, banderole stamps and distinguishing marks, seal stamping, analysis expenses or fees for services rendered by the Department officers as well as remunerations for work done for persons concerned during non-official work hours.Such amounts shall not be included in scope of exemptions or tax refund stipulated in this Law.

Cairo:

Tel & Fax: +202 39 26 231 / 39 59 150 Abdel Khalek Tharwat St. – 4th Floor - Egypt

E-mail: [email protected]

Sharm El-Sheikh: Tel & Fax: 069 36 02 035

Sharm Trade Center - Naama Bay – Egypt [email protected]

Web site: www.ma-acc.com

22

MMeeddhhaatt GGhhaallyy && AAllbbeerrtt EEddwwaarrdd –– CChhaarrtteerreedd AAccccoouunnttaannttss AAuuddiittss && CCoonnssuullttaanncciieess FFiirrmm -- EEggyypptt

Chapter 13

General Provisions

Article (48)

Without prejudice to the special provisions stated in this Law, disposal of any goods exempted from tax or use of such goods in purposes other than those for which they were exempted within five years following the exemption except after notifying the Department and paying the tax due according to the value of such goods and the effective tax rate thereon at the date of disposal shall not be allowed.

In all cases, the tax due shall not exceed the amount of previous tax exemption.

Said disposal, without notification of the Department and payment of tax due, shall be deemed a tax evasion act and shall be penalized by the penalties prescribed in this Law.

Article (49)

In accordance with the rules specified in the Executive Regulations, the Department may dispose of seized goods and equipment used in smuggling and means of transport confiscated by judgement.

Provisions and rules prescribed in Customs Law regarding sale and disposal of seized goods shall apply to imported goods.

The Department may, before the delivery of judgement, dispose of seized goods liable to damage, decrease or perishment.The Department may, after consulting the competent technical authorities, destroy the goods prohibited to be circulated or harmful to public health or feared, if sold, to affect security and safety of citizens.

Article (50)

Taxable imported goods unreleased from Customs shall be subject to provisions of offences and evasion set forth in Customs Law.

Article (51)

Debts due to the Department by registrant may be written - off in the following cases:

• If the registrant was finally sentenced to bankruptcy and the case of bankruptcy was closed.

• If the registrant left the country for ten years without leaving funds. • If the debtor proved to be out of funds to be seized. • If the registrant died leaving no inheritance.

Cairo:

Tel & Fax: +202 39 26 231 / 39 59 150 Abdel Khalek Tharwat St. – 4th Floor - Egypt

E-mail: [email protected]

Sharm El-Sheikh: Tel & Fax: 069 36 02 035

Sharm Trade Center - Naama Bay – Egypt [email protected]

Web site: www.ma-acc.com

23

MMeeddhhaatt GGhhaallyy && AAllbbeerrtt EEddwwaarrdd –– CChhaarrtteerreedd AAccccoouunnttaannttss AAuuddiittss && CCoonnssuullttaanncciieess FFiirrmm -- EEggyypptt

Debt writing-off shall be the competence of committees formed by a ministerial decree and the recommendations of such committees shall be approved by the Commissioner. The decision on writing -off debts

Article (52)*

The minister of finance may, after having the consent of the cabinet , set one or more systems for rewarding employees of Sales Tax Department in accordance with work performance rates and achievement levels thereof without being restricted to any other system . The minister may allocate sums of money for contribution in social cooperative funds, provident funds, mutual funds and sports clubs of the Department employees.

* Added on 30-3-2005 by Law No. 9 of 2005

Article (53)*

The person concerned, who wants to make a transaction that entails consequences related to the general sales tax, may submit an application to the comunissioner or his / her legal representative requesting the issuance of a statement declaring the department point of view concerning application of the previsions herein on such transaction.

The application submitted shall include all aspects and various phases of the transaction the issuance of the statement is requested therefor.

The commissioner shall issue the requested statement within sixty days as of the date of submission of the application to the Department. The commissioner may demand additional data about the transaction within the same period. The statement issued by the Commissioner shall be binding to the Department unless any other aspects of the transaction are revealed and are not presented to the department prior to issuance of the statement .

In all cases non- issuance of the statement requested within the period referred to be herein shall be considered a rejection of the request.

Cairo:

Tel & Fax: +202 39 26 231 / 39 59 150 Abdel Khalek Tharwat St. – 4th Floor - Egypt

E-mail: [email protected]

Sharm El-Sheikh: Tel & Fax: 069 36 02 035

Sharm Trade Center - Naama Bay – Egypt [email protected]

Web site: www.ma-acc.com

24

MMeeddhhaatt GGhhaallyy && AAllbbeerrtt EEddwwaarrdd –– CChhaarrtteerreedd AAccccoouunnttaannttss AAuuddiittss && CCoonnssuullttaanncciieess FFiirrmm -- EEggyypptt

Table No. (1)

Tax on imported goods Tax on domestic goods Serial No. Item Collection

Unit Tax rate L.E. Collection Unit Tax rate L.E.

Tea(A) Unsubsidized tea (Gomhoria) Net Ton 766.262 Net Ton 766.262

(B) Tea distributed by ration cards Net Ton 144.756 Net Ton 144.756

(C) Imported tea in normal packages Net Ton 1051.262 Net Ton 1051.262

(D) Imported tea in deluxe packages Net Ton 1166.662 Net Ton 1166.662

1

(E) Others Net Ton 1166.662 Net Ton 1166.662 Solid beet sugar and cane sugar, other kinds of solid sugar, condensed sugar syrups not containing added odoriferous or additional colouring matters: (A) Sugar distributed by ration cards Net Ton 43.600 Net Ton 43.600

2

(B) Unsubsidized sugar:

(1) Crystallized sugar

(2) Cubic sugar

(3) Sugar lump

(4) Others

Net Ton

Net Ton

Net Ton

Net Ton

55.600

57.600

58.600

58.600

Net Ton

Net Ton

Net Ton

Net Ton

55.600

57.600

58.600

58.600 Beer*13

(1) Alcoholic Value

100 % with minimum amount of L.E. 200 per hectoliter

Value

100 % with minimum amount of L.E. 200 per hectoliter

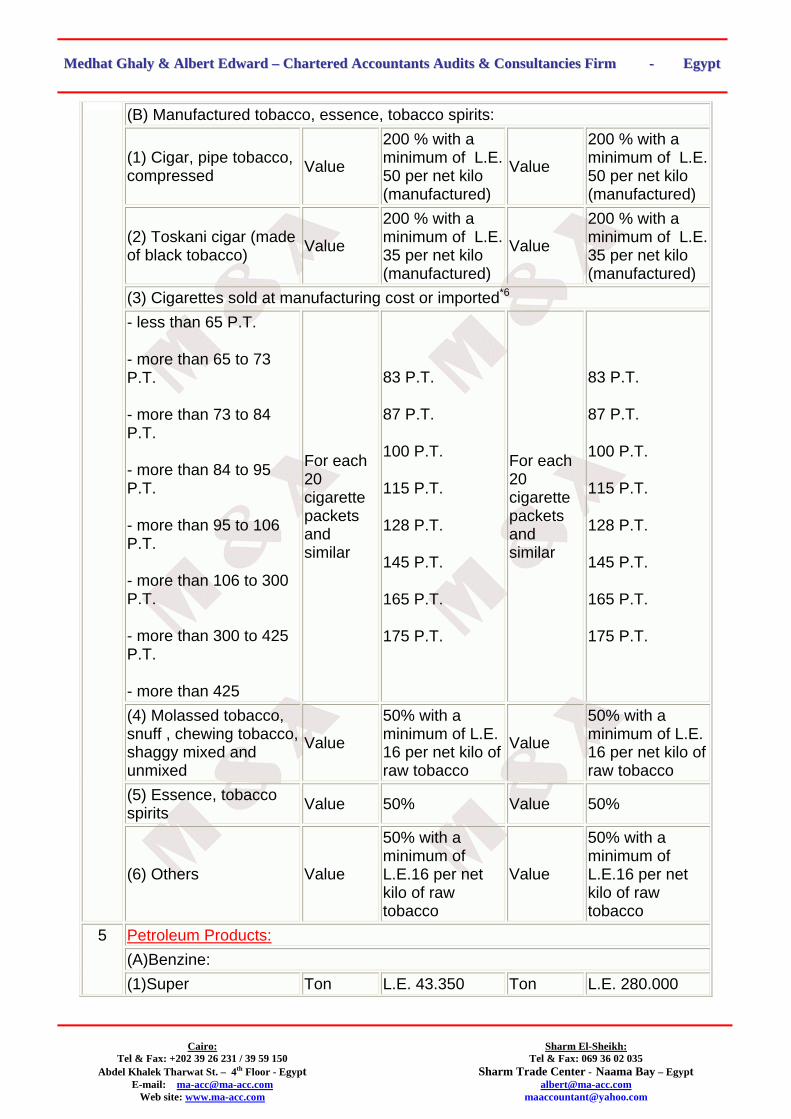

Tobacco:(A) Raw or unmanufactured tobacco and refuse:

1) Persian tobacco for narghiles Value

100 % with a minimum of L.E. 40 per net kilogram

4

2) Others *2.3 Value 75 % with a minimum of L.E. 16 per net kilo

Cairo:

Tel & Fax: +202 39 26 231 / 39 59 150 Abdel Khalek Tharwat St. – 4th Floor - Egypt

E-mail: [email protected]

Sharm El-Sheikh: Tel & Fax: 069 36 02 035

Sharm Trade Center - Naama Bay – Egypt [email protected]

Web site: www.ma-acc.com

25

MMeeddhhaatt GGhhaallyy && AAllbbeerrtt EEddwwaarrdd –– CChhaarrtteerreedd AAccccoouunnttaannttss AAuuddiittss && CCoonnssuullttaanncciieess FFiirrmm -- EEggyypptt

(B) Manufactured tobacco, essence, tobacco spirits:

(1) Cigar, pipe tobacco, compressed Value

200 % with a minimum of L.E. 50 per net kilo (manufactured)

Value

200 % with a minimum of L.E. 50 per net kilo (manufactured)

(2) Toskani cigar (made of black tobacco) Value

200 % with a minimum of L.E. 35 per net kilo (manufactured)

Value

200 % with a minimum of L.E. 35 per net kilo (manufactured)

(3) Cigarettes sold at manufacturing cost or imported*6

- less than 65 P.T.

- more than 65 to 73 P.T.

- more than 73 to 84 P.T.

- more than 84 to 95 P.T.

- more than 95 to 106 P.T.

- more than 106 to 300 P.T.

- more than 300 to 425 P.T.

- more than 425

For each 20 cigarette packets and similar

83 P.T.

87 P.T.

100 P.T.

115 P.T.

128 P.T.

145 P.T.

165 P.T.

175 P.T.

For each 20 cigarette packets and similar

83 P.T.

87 P.T.

100 P.T.

115 P.T.

128 P.T.

145 P.T.

165 P.T.

175 P.T.

(4) Molassed tobacco, snuff , chewing tobacco, shaggy mixed and unmixed

Value

50% with a minimum of L.E. 16 per net kilo of raw tobacco

Value

50% with a minimum of L.E. 16 per net kilo of raw tobacco

(5) Essence, tobacco spirits Value 50% Value 50%

(6) Others Value

50% with a minimum of L.E.16 per net kilo of raw tobacco

Value

50% with a minimum of L.E.16 per net kilo of raw tobacco

Petroleum Products:(A)Benzine:

5

(1)Super Ton L.E. 43.350 Ton L.E. 280.000

Cairo:

Tel & Fax: +202 39 26 231 / 39 59 150 Abdel Khalek Tharwat St. – 4th Floor - Egypt

E-mail: [email protected]

Sharm El-Sheikh: Tel & Fax: 069 36 02 035

Sharm Trade Center - Naama Bay – Egypt [email protected]

Web site: www.ma-acc.com

26

MMeeddhhaatt GGhhaallyy && AAllbbeerrtt EEddwwaarrdd –– CChhaarrtteerreedd AAccccoouunnttaannttss AAuuddiittss && CCoonnssuullttaanncciieess FFiirrmm -- EEggyypptt

(2)Ordinary Ton L.E. 43.350 Ton L.E. 250.000 (B) White Spirits Liter L.E. 1.750 Liter L.E. 1.750 (C) Kerosene Liter L.E. 0.010 Liter L.E. 0.010 (D) Gas Oil (Solar) Liter L.E. 0.010 Liter L.E. 0.010 (E) Diesel Oil Liter L.E. 0.008 Liter L.E. 0.008 (F) Fuel Oil (Mazot) Ton L.E. 0.500 Ton L.E. 0.500 (G) Lubricating oil Ton L.E. 11.000 Ton L.E. 11.000 (H) Lubricating preparations (Oil-based metal lubricants)

Ton L.E. 9.000 Ton L.E. 9.000

(A) Pure Ethyl alcohol undenatured of any alcoholic degree*5

Pure Liter 7.5 Pure Liter 7.5

(B) Denatured alcohol of any alcoholic degree for fuel

Liquid Liter 0.150 Liquid

Liter 0.15

(C) Wine of fresh grapes, grape must with fermentation arrested by the addition of alcohol including vermouths, mistella and other kinds of wine, fermented beverages

Value

100% with a minimum of L.E. 7.5 per liquid liter

Value

100% with a minimum of L.E. 7.5 per liquid liter

(D) Spirits and alcoholic beverages with sugar, odoriferous, other alcoholic beverages, compound alcoholic preparations, natural distillations

6

Value

100% with a minimum of L.E. 7.5 per liquid liter

Value

100% with a minimum of L.E. 7.5 per liquid liter

7

Medicine except those exempted by a ministerial decree in agreement with the Minister of Health

Value 1.625 Value 5%

8

Automatic wheeled chairs, its spare parts and its separate components, and other artificial human organs listening system for the deaf, and other system equipments or limbs worne or borne or

Exempt Exempt

Cairo:

Tel & Fax: +202 39 26 231 / 39 59 150 Abdel Khalek Tharwat St. – 4th Floor - Egypt

E-mail: [email protected]

Sharm El-Sheikh: Tel & Fax: 069 36 02 035

Sharm Trade Center - Naama Bay – Egypt [email protected]

Web site: www.ma-acc.com

27

MMeeddhhaatt GGhhaallyy && AAllbbeerrtt EEddwwaarrdd –– CChhaarrtteerreedd AAccccoouunnttaannttss AAuuddiittss && CCoonnssuullttaanncciieess FFiirrmm -- EEggyypptt

transplanted in human body to compensate for any mayhem or deformation or unfitness or handicapping

9*6Unsubsidized vegetable edible oils, fixed, fluid, solid, refined or purified

Net Ton 37.400 Net Ton 37.400

10*6

Animal or vegetable oils and fats, wholly or partly hydrogenated or solidified or hardened or purified by other process whether or not refined but not further prepared

Net Ton 40.000 Net Ton 40.000

11*6

Hydraulic cement of all kinds and agglomerated unground cement (clinikers) whether or not coloured

Ton 1.400 Ton 2.500

(1) Amended as of 30/3/2005 by Law NO (9) of 2005.

(2) Importers shall notify the Department of purchasers of tobacco or of any other disposals of imported quantity of tobacco within fifteen days following the month of sale .

(3) In case such item is an input of a domestic product, tax collected on such item shall be deducted from tax due on such domestic product amended as of 29.7.1997 replaced by Law NO (2) of 1997 .

(4) Amended by Law No 164 of 2002 promulgated on 20 / 7 / 2002.

Again, this item was amended by law no. 164 of 2002 .

(5) Producers and importers shall notify the Department of purchasers of such item and of any other disposal of quantities sold thereof within fifteen days following the month of sale . ( item 6 was amended as of 5.3.1992 by Law NO( 2 ) of the year 1997 ) .

(6)Items 10 & 11 were added to Table (1) by the presidential decree NO (180) of the year 1991 as of 4.5.1991. Such amendment is included in table (B) attached to Law No 2 of 1997.

Cairo:

Tel & Fax: +202 39 26 231 / 39 59 150 Abdel Khalek Tharwat St. – 4th Floor - Egypt

E-mail: [email protected]

Sharm El-Sheikh: Tel & Fax: 069 36 02 035

Sharm Trade Center - Naama Bay – Egypt [email protected]

Web site: www.ma-acc.com

28

MMeeddhhaatt GGhhaallyy && AAllbbeerrtt EEddwwaarrdd –– CChhaarrtteerreedd AAccccoouunnttaannttss AAuuddiittss && CCoonnssuullttaanncciieess FFiirrmm -- EEggyypptt

Table No.(2)

Taxable Services

Serial No. Item* Collection

Unit Tax Rate

11The Services of hotels and tourist restaurants other than the free services rendered by such bodies to the workers thereof .

value of invoice 10%

21 Services of tourist transportation companies. value of invoice 10%

3 Telex and Fax Services2 Value of receipt 10%

4 Air conditioned means of transportation between Governorates ( buses, railway)

Value of ticket 5%

5 Sound and Light show services Service fees 10% 6 Use of sound and Light companies utilities Service fees 10%

7 Artistic Agent services in public and private parties Value of contract 5%

81The services of fixed phones, local telegram to the public, government cabins … etc, other than mobile phones.

The value of invoice 5%

91

Other Communication services

a)Communication services either national or international by mobile phones either by invoice, prepaid card or any means of collection.

b)Services of international communications , telegram, information communication and international telephone calls by fixed phones .

The value of invoice

The value of invoice

15%

10%

10 Services of installation of telephone connections and fittings, wire and wireless and others

Value of receipt 10%

11 Processing for a third party3 Service fees 10% 12 Hiring private cars services Service fees 10% 13 Express mail services Value 10% 14 Services of cleanliness and private security companies Value 10%

15 Using of highways4 Duty value 10% at least 25

P.T.

16 Intermediary in sale of real estate Value of service 10%

17 Intermediary in the sale of cars Value 10%

Cairo:

Tel & Fax: +202 39 26 231 / 39 59 150 Abdel Khalek Tharwat St. – 4th Floor - Egypt

E-mail: [email protected]

Sharm El-Sheikh: Tel & Fax: 069 36 02 035

Sharm Trade Center - Naama Bay – Egypt [email protected]

Web site: www.ma-acc.com

29

MMeeddhhaatt GGhhaallyy && AAllbbeerrtt EEddwwaarrdd –– CChhaarrtteerreedd AAccccoouunnttaannttss AAuuddiittss && CCoonnssuullttaanncciieess FFiirrmm -- EEggyypptt

*Items 8-11 were added to this table as of 5.3.1992 by law No 2 of the year 1997.

*Items 12-15 were added to this table as of 29.7.1993 by law No 2 of the year 1997 .

*Items 16-17 were added to this table as of 14-2-1994 by law No 2 of the year 1997 .

1. Tax rates charged on items 1,2,8,9 were amended by virtue of law no.89 of 2004 as of 20/5/2004.

2. This item was amended as of 5.3.1992 by law No ( 2 ) of the year 1997 . 3. Law no. 11 of 2002 was promulgated on interpreting the phrase "Processing for a

third party". 4. This item was amended as of 6.8.1993 by law No ( 2 ) of the year 1997 .

Table (A)* annexed to law No (2) of the year 1997

First:The following commodities shall be subject to Sales Tax at rate of 5%:

1- Coffee, whether or not roasted or decaffeinated, coffee husks and skins, coffee substitutes containing coffee in any proportion.

2- All flour products and sweets made of pastry except all kinds of fixed price bread.

3- Soap and detergents for home use purposes.

4- Fertilizers.

5- Disinfectants, insecticides, fungicides, herbicides, anti-sprouting, rat poisons, for agricultural purposes.

6- Gypsum.

7- Wood sawn in sheets lengthwise, sliced or peeled. and sheets for plywood and reconstituted wood and fiberboard but not further manufactured .

8-Bars and rods from iron for building ; waste and scrap metal of iron or steel ; blooms and billets**.

*This table was effective as of 4.5.1991

**Added as of 29.5.1991 by the law No (2) of the year 1997 .

Cairo:

Tel & Fax: +202 39 26 231 / 39 59 150 Abdel Khalek Tharwat St. – 4th Floor - Egypt

E-mail: [email protected]

Sharm El-Sheikh: Tel & Fax: 069 36 02 035

Sharm Trade Center - Naama Bay – Egypt [email protected]

Web site: www.ma-acc.com

30

MMeeddhhaatt GGhhaallyy && AAllbbeerrtt EEddwwaarrdd –– CChhaarrtteerreedd AAccccoouunnttaannttss AAuuddiittss && CCoonnssuullttaanncciieess FFiirrmm -- EEggyypptt

Table No (c)*

Attached to Law No (2) of the year 1997

-Goods exempted from General Sales Tax-

1- Dairy products and products from milk produced by substitution of one or more of its natural elements.

2- Subsidized vegetable edible oils, fixed, fluid, solid, refined or purified.

3- Products of the milling industry except imported fine flour or fermented flours.

4- Meat preparations and kinds preserved or manufactured.

5- Fish preserved or prepared, except caviar and caviar substitutes and smoked fish.

6- Vegetables, fruits, legumes, cereals, salt and spices prepared and packaged or canned whether fresh, or frozen or preserved except such imported thereof.

7- Sweet made of sesame-seed meat and thick sauce made of sesame oil**.

8- Foods produced and sold by untouristic restaurants or shops directly to final consumer.

9- Subsidized bread in all kinds ***

10- Natural gas and butane gas even if collected in prepared pipes for retail sale

11- Residues and wastes of food industries. Foods prepared for animals, birds and fishes (forage) except such used for feeding cats, dogs and ornamental fish.

12- Subsidized clothes distributed by Ministry of Supply and Interior Trade.

13- Paper pulp, waste paper and paperboard, scrap articles of paper and of paperboard, fit only for use in paper making.

14- Newsprint paper and printing and writing paper.

15- Books and academic lectures printed ****

16- Newspapers and magazines****.

17-Macaroni produced from ordinary flours.

18-Gold ores, item 12-871 in Harmonized customs Tariff issued by presidential decree No (38) of the year 1994***** .

Cairo:

Tel & Fax: +202 39 26 231 / 39 59 150 Abdel Khalek Tharwat St. – 4th Floor - Egypt

E-mail: [email protected]

Sharm El-Sheikh: Tel & Fax: 069 36 02 035

Sharm Trade Center - Naama Bay – Egypt [email protected]

Web site: www.ma-acc.com

31

MMeeddhhaatt GGhhaallyy && AAllbbeerrtt EEddwwaarrdd –– CChhaarrtteerreedd AAccccoouunnttaannttss AAuuddiittss && CCoonnssuullttaanncciieess FFiirrmm -- EEggyypptt

19-Civil aircraft vehicles, engines, parts and components thereof as well as spare parts and equipment necessary for use thereof

also services applied to said vehicles in the customs zone, whether planes or engines or parts or components or spare parts or

equipment or services rendered thereto were imported or local, all above in consistency with rules and provisions stipulated in the

agreement on trade of civil aircraft issued by Presidential Decree No 414 of 1983****** .

20-Molasses*******.

21-Herring smoked fish*******.

22-All kinds of bread.***

� * Effective as of 4.5.1991 by virtue of law No.2 of 1997.

**the cabinet rectification - the official Gazette, issue No. 18 ( bis) A on 4-5-1991 .

*** Bread of all kinds ( subsidized and unsubsidized ) is now exempted as of 30-3-2005 by virtue of law No.9 of 2005 .

**** Amended as of 29-7-1993 by virtue of law No.2 of 1997 .

***** Added as of 1-10-1996 by virtue of law No.2 of 1997 .

****** Exempted as of 23-12-1997 by virtue of law No. 161 of 1997 .

******* Exempted as of 14-6-1998 by virtue of law No. 163 .

Table No. (F)

Annexed to Law No (2) of 1997

Second:The following commodities shall be subject to Sales Tax rate of 25%:

1- Coloured T.V. more than 16 inch whether or not incorporated in any other set or equipment.

2- Refrigerators and Refrigerating equipment of capacity more than 12 feet for private home use and display refrigerators for shops

and hotels and all such equipment used in other places.

3- Deep freezes of capacity 10 feet or more.

4- Sound recorders and reproducers, image and sound recorders and or reproducers (video)

5- Air-condition units and its separate units (split).

6- Cameras and parts thereof.

7- Perfumery, Cosmetics or Toilet preparations and products prepared for care of hair and skin.

8- Chandeliers and parts thereof.

9- Tapes for recording image and sound (video tapes)

10-Motor cars of cylinders` capacity more than 1600 cc. or motor cars of rotary engines, motor vehicles for the transport of goods

and persons, Jeep motor vehicles and caravans for trips and camping trailers*

11- Non-alcoholic beer.**

12- Aerated water, odoriferous with or without sugar.***

* Amended as of 23.2.1995 by presidential decree No.65 of 1995 replaced by article (8) of

Law No (2) of the year 1997 which provided that G.S.T rates on all automobiles regardless

of Cylinder Capacity and cars with rotary engines and motor vehicles for transportation of

Cairo:

Tel & Fax: +202 39 26 231 / 39 59 150 Abdel Khalek Tharwat St. – 4th Floor - Egypt

E-mail: [email protected]

Sharm El-Sheikh: Tel & Fax: 069 36 02 035

Sharm Trade Center - Naama Bay – Egypt [email protected]

Web site: www.ma-acc.com

32

MMeeddhhaatt GGhhaallyy && AAllbbeerrtt EEddwwaarrdd –– CChhaarrtteerreedd AAccccoouunnttaannttss AAuuddiittss && CCoonnssuullttaanncciieess FFiirrmm -- EEggyypptt

goods and persons and Jeep motor vehicles and caravans for trips and camping trailers

shall be raised by 5%

Again it was amended as of 1.10.1996 by Article 291 of the Law (2) of the year 1997 which

provided that G.S.T rates on motor vehicles subject to 160% customs duties shall be raised

by 15% .

**Amended as of 30/3/2005 by law no. (9) of 2005. Value of bottles returned to factories

shall be factories shall be included in elements of value taken as a base for taxation

according to depreciation ratios determined by a ministerial decree in agreement with the

competent minister. However, value of unreturned bottles or containers shall be included in

elements of value taken as a base for taxation.

*** Amended as of 30/3/2005 by law no. (9) of 2005. Value of bottles returned to factories

shall be factories shall be included in elements of value taken as a base for taxation

according to depreciation ratios determined by a ministerial decree in agreement with the

competent minister. However, value of unreturned bottles or containers shall be included in

elements of value taken as a base for taxation .

Aerated water prepared in public shops by post mix machines shall be subject to the same

tax rate and the tax shall be collected in advance from companies producing syrup used in

such machines according to the amounts produced of aerated water determined by

measures set by competent technical bodies.

In agreement with competent minister, the minister shall issue price lists of aerated water

taken as a base for taxation.

Cairo:

Tel & Fax: +202 39 26 231 / 39 59 150 Abdel Khalek Tharwat St. – 4th Floor - Egypt

E-mail: [email protected]

Sharm El-Sheikh: Tel & Fax: 069 36 02 035

Sharm Trade Center - Naama Bay – Egypt [email protected]

Web site: www.ma-acc.com