general presentation bruno farber ulb - …tbauler.pbworks.com/f/farber_ginko.pdfgeneral...

TRANSCRIPT

1

ULB - Green Management Module

The Ginkgo Fund

GENERAL PRESENTATION

Bruno Farber

2

INTRODUCTION THE INITIATORS & THE FUND’S STRUCTURE INVESTMENT CRITERIA AND STRATEGY INVESTMENT PROCESS PROJECTS PRESENTATION

3

Introduction Context

Today we face two crises: a deep global financial crisis and an even deeper climate and environmental crisis. There is a window of opportunity to act on the financial crisis and, at the same time, lay the foundations for a new wave of growth based on the technologies for a low-carbon economy (J. Stiglitz & N. Stern)

Towards a green recovery : there is growing consensus among policy-makers and investors around the world that sustainable investment strategies – including in urban (re)development - are a cornerstone of the revitalisation of the economy

4

Introduction Key drivers

The Fund aims to capitalise on several key drivers, in particular:

The existence of a large number of brownfields, in the context of scarcity of well-located semi-industrial, commercial and/or residential land in Europe; The recent emergence of new, more cost-efficient soil remediation techniques; Increasing European legislative pressure on (a) operators of contaminated sites to undertake expensive remedial actions, and (b) real estate developers to meet stricter energy-efficiency standards in light of the need to meet CO2 emissions reduction targets;

5

Introduction Value cycle

The Fund sees the opportunity to contribute to create a virtuous value cycle :

for investors in terms of financial value after redevelopment;

for local authorities through the restoration of tax revenues to idle and/or abandoned sites;

for communities through improvements of public health issues and other social benefits (e.g. improved neighbourhoods and higher property value)

for the environment and climate through land restoration and reduced energy

consumption in buildings.

6

Introduction Mission

The Ginkgo Fund aims to build a diversified portfolio of contaminated sites and to remediate them, before reselling them at a premium to third parties. In certain cases, after remediation the Fund will seek to maximise value through the development of “green” real estate projects. The geographical focus is Belgium and France. The Fund is targeting an IRR of 15% over an 8 year period (with two one-year additional extensions).

7

Introduction Key Positioning

The Ginkgo Fund will focus on : Sites with a pollution record – chemical or UXO - only Small to mid-size (approximately 1 to 20 ha) environmentally impaired sites showing attractive real estate potential Equity commitment between €5 and €15 million per project and prudent leverage The territories of France and Belgium Rigorous risk management Pragmatic, innovative and virtuous approach to brownfield remediation Pioneering projects with the public sector through a unique skill set in the structuring of public-private partnership A fully committed team working with the best specialist advisors

The Ginkgo Fund aims to become the largest brownfield fund in Europe and benchmark amongst its peers What the Ginkgo Fund is not :

A “socially responsible” alibi fund A high promotion/development real estate speculation fund A vehicle seeking public subsidies A procurement tool for feeding the businesses of its shareholders

8

Introduction Ginkgo’s focus on remediation : more, faster and better

Ginkgo is involved only in large/high percentile remediation operations • the pipeline average remediation budget is 800 K€ per hectare • benchmark data (Sita Remediation 2006) indicate that over 90% of remediation

projects are under the 100 K€ budget and only 1% over 600 K€ • current pipeline decontamination budget represents approx. 35% of equity

requirements Remediation and real estate development processes are interdependent and need to be

integrated • the degree of remediation is always associated with a future land use/function • soil legislation is evolving toward a risk-based approach, i.e. removing the risk for a

given use/real estate function • for many brownfield sites, development benefits do not compensate associated

costs : only a handful of redevelopment projects are economically feasible (approx. 4% of sourced pipeline) and only for investors with relevant expertise

9

Introduction Ginkgo’s focus on remediation : more, faster and better

Ginkgo adopts a vertuous but pragmatic approach towards remediation • in France, approx. 54% of the "remediation" is pollution displacement and landfilling

(source: BIPE, 2005) • Ginkgo uses landfilling only as last resort solution Ginkgo's activity brings significant ancillary societal benefits beyond soil remediation • reduction of public health issues • benefits of sustainable real estate developments • prevention of urban sprawl and revitalisation of urban areas with existing infrastructure Ginkgo provides an accelerator for public soil remediation • public entities have limited budgets and resources • public remediation approaches are often slow and sub optimal processes • Ginkgo implements innovative partnering relationship/PPP that are a catalyser for

public projects

10

INTRODUCTION THE INITIATORS & THE FUND’S STRUCTURE INVESTMENT CRITERIA AND STRATEGY INVESTMENT PROCESS PROJECTS PRESENTATION

11

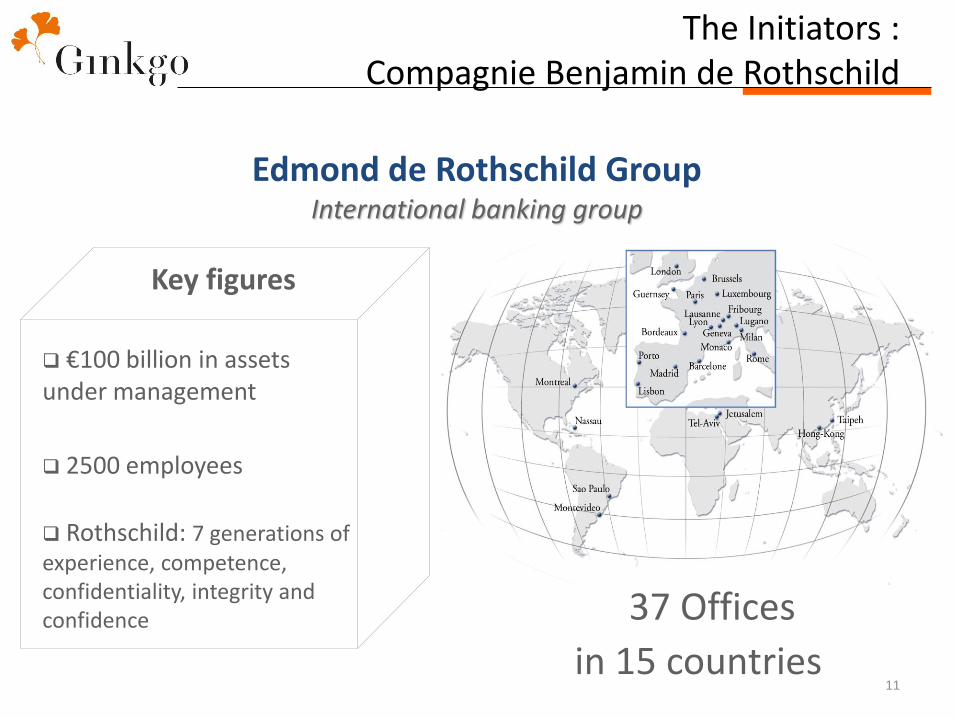

Edmond de Rothschild Group International banking group

2500 employees

€100 billion in assets under management

Rothschild: 7 generations of experience, competence, confidentiality, integrity and confidence

Key figures

37 Offices

in 15 countries

The Initiators : Compagnie Benjamin de Rothschild

12

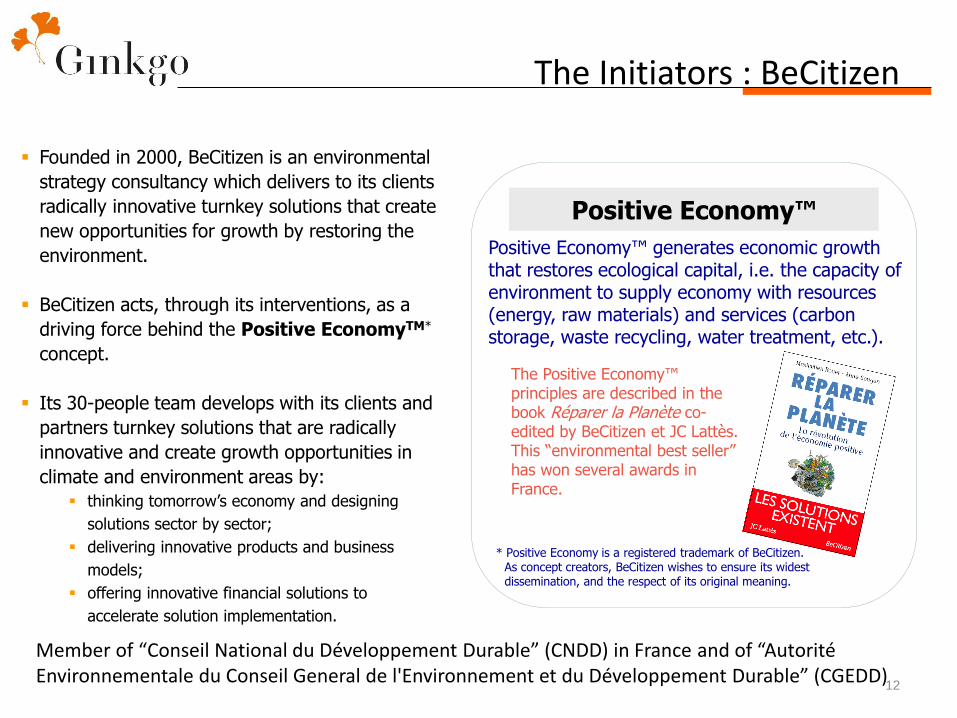

Positive Economy™

Founded in 2000, BeCitizen is an environmental

strategy consultancy which delivers to its clients

radically innovative turnkey solutions that create

new opportunities for growth by restoring the

environment.

BeCitizen acts, through its interventions, as a

driving force behind the Positive EconomyTM*

concept.

Its 30-people team develops with its clients and

partners turnkey solutions that are radically

innovative and create growth opportunities in

climate and environment areas by:

thinking tomorrow’s economy and designing

solutions sector by sector;

delivering innovative products and business

models;

offering innovative financial solutions to

accelerate solution implementation.

Positive Economy™ generates economic growth that restores ecological capital, i.e. the capacity of environment to supply economy with resources (energy, raw materials) and services (carbon storage, waste recycling, water treatment, etc.).

The Positive Economy™ principles are described in the book Réparer la Planète co-edited by BeCitizen et JC Lattès. This “environmental best seller” has won several awards in France.

* Positive Economy is a registered trademark of BeCitizen. As concept creators, BeCitizen wishes to ensure its widest dissemination, and the respect of its original meaning.

The Initiators : BeCitizen

Member of “Conseil National du Développement Durable” (CNDD) in France and of “Autorité Environnementale du Conseil General de l'Environnement et du Développement Durable” (CGEDD)

13

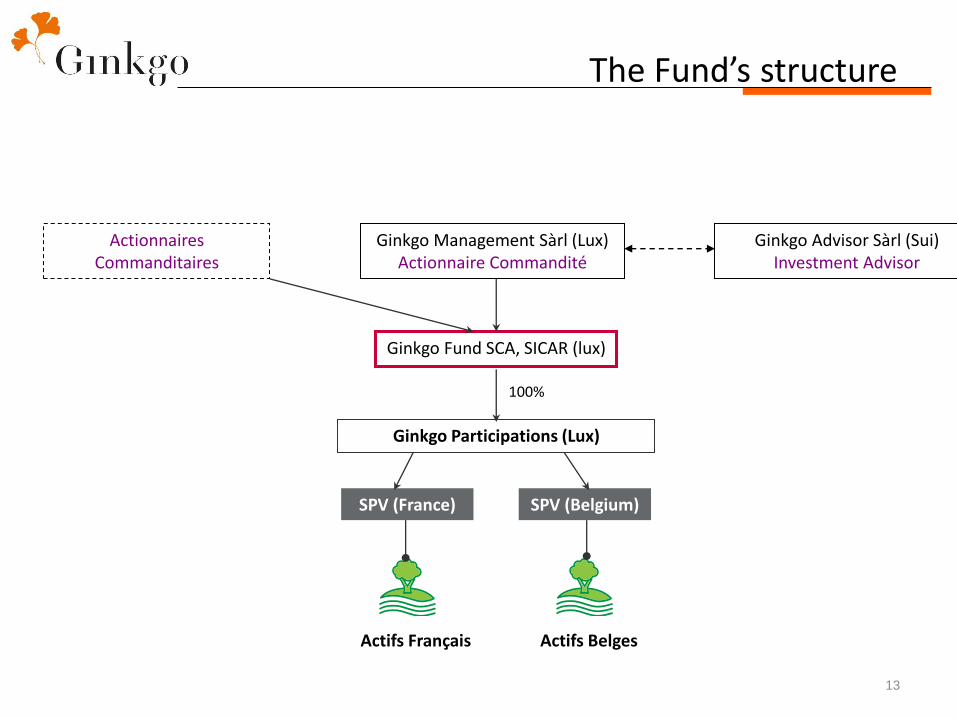

The Fund’s structure

Ginkgo Fund SCA, SICAR (lux)

Ginkgo Participations (Lux)

SPV (France) SPV (Belgium)

Actifs Français Actifs Belges

100%

Ginkgo Management Sàrl (Lux) Actionnaire Commandité

Ginkgo Advisor Sàrl (Sui) Investment Advisor

Actionnaires Commanditaires

14

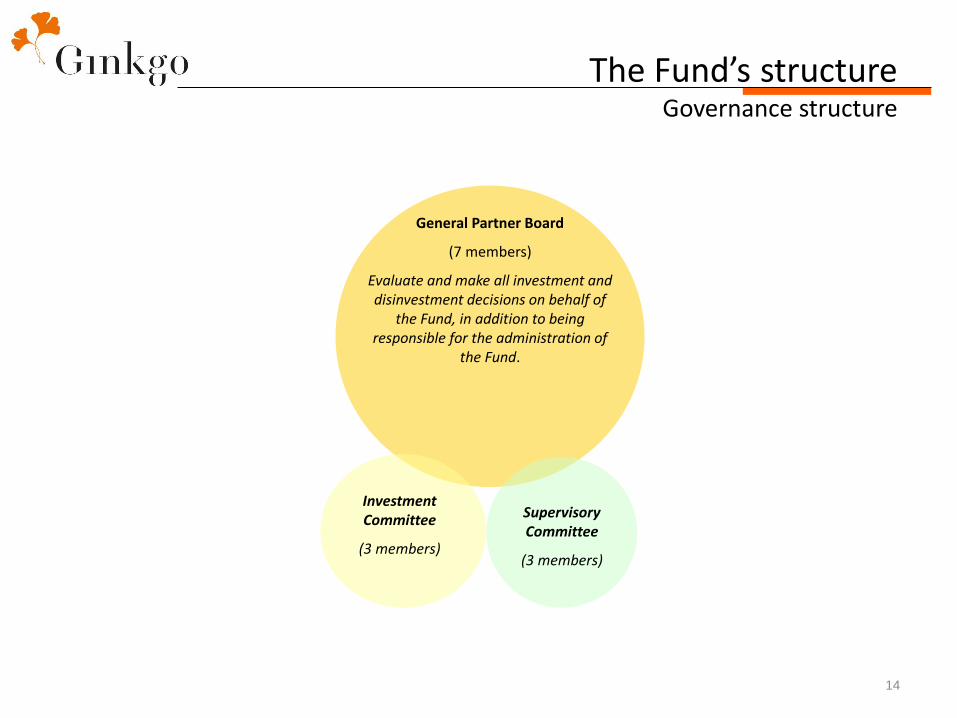

The Fund’s structure Governance structure

General Partner Board

(7 members)

Evaluate and make all investment and disinvestment decisions on behalf of

the Fund, in addition to being responsible for the administration of

the Fund.

Investment Committee

(3 members)

Supervisory Committee

(3 members)

15

The Fund’s structure Principal Investment Terms

Capital cible : 100 m€

Return cible : 15%

Commitment period : 5 ans à dater du premier closing

Durée : 8 ans plus deux extension possible de 1 an sous condition de quorum et majorité pour modification des statuts.

Management fee :

• Année 1 à 3 : 2% des commitments

• Année 4 : 1% des commitments appelés ou non appelés non investis et 2.5 % des commitments appelés et investis

• Année 5 : 0.5% des commitments appelés ou non appelés non investis et 2 % des commitments appelés et investis

• Au-delà : 2% des commitments investis

16

INTRODUCTION THE INITIATORS & THE FUND’S STRUCTURE INVESTMENT CRITERIA AND STRATEGY INVESTMENT PROCESS PROJECTS PRESENTATION

17

Investment criteria and strategy Site identification

Brownfield sites characterised using, inter alia, official national and regional databases of polluted sites ( BASOL, OVAM, IBGE, WALSOL..).

Focus on small to middle sized (approximately 1 to 20 ha) environmentally impaired sites Focus on attractive location that provide the opportunity to redevelop “landmark” projects

Size

Pollution

Location

18

Investment criteria and strategy Diversification guidelines

Aggregate Commitments for an individual project : < 20% Between €5 million and €15 million Ginkgo aims to invest in 7 to 10 Projects.

Project diversification

Geographic diversification

Real estate project

diversification

Belgium and France One country < 75% of Aggregate Commitments.

Well balanced and diversified real estate portfolio, comprised of constructable land, offices, residential units, retail and semi-industrial buildings (e.g. logistics centres) One class of real estate asset < 65% of the funded Commitments after the Commitment Period.

19

Investment criteria and strategy Leverage and SPVs

Ginkgo holds no debt The SPVs may have the possibility of being reasonably leveraged in line with the practices of debt markets with regards to the financing of these types of Projects (i.e. debt to equity ratio) Interest rate risk or currency risk will be hedged to cover potential increases in the cost of debt financing

One or more SPVs will be created for every new Project Each SPV will hold the assets and the debt Ginkgo can invest in one or more existing SPVs with ongoing brownfield remediation Projects

Leverage

SPVs

20

Investment criteria and strategy Investment Duration

The duration of the Commitment Period shall be limited to 4 years starting from the date of the Last Closing of Ginkgo

Ginkgo will not initiate investments in new projects after an investment period of 4 years

An average duration of 4 years between a Project’s initial investment and its final divestment (project’s lifecycle) will be sought

Commitment period

Investment period

Investment duration

21

Investment criteria and strategy Land Acquisition

Ginkgo will - indirectly though the SPVs - acquire full property or be granted property right (e.g. Emphyteusis or Surface area) in brownfield sites

Only sites for which a pollution record exists will be acquired by the Ginkgo.

Ginkgo will assume the structuring and negotiation of purchasing terms with the land owner (e.g. transfer or public private partnership approach with recourse to various legal mechanisms such as Emphyteusis or Surface area).

The acquisition process will generally entail the assessment of the value of the land and other assets acquired by Ginkgo by an independent evaluator.

Property right

Pollution record

Value assessment

Negotiation with the land owner

22

Investment criteria and strategy Remediation

Actions on the soil aimed at the removal, control, containment or reduction of contaminants so that the contaminated site, taking account of its current use and approved future use, no longer poses any significant risk to human health or the environment

No environmental contamination type will be excluded a priori : inorganic substances (e.g. heavy metals, asbestos), organic substances (e.g. hydrocarbures chlorinated solvents), or military/UXO pollution

Only efficient and proven remediation techniques will be used. Remediation projects will to the greatest extent possible avoid pollution transfer and landfilling, which will only be decided as a last resort. Based on a methodology taking into account societal, environmental, economic and technical criteria

The remediation process will generally entail the use of appropriate insurance policies or guaranteed fixed price remediation contracts in order to limit environmental liability and/or cap remediation expenses

The remediation process will be complemented with adequate monitoring strategies when the need arises.

Definition

Remediation techniques

Monitoring strategies

Environmental risk mitigation

Type of pollution

23

Investment criteria and strategy Development

Building development will take into account energy-efficiency criteria. Real estate Projects that do not demonstrate significant energy efficiency will not be undertaken.

Real estate development will be part of an official urban development plan/strategy : will take place only if the future use of the land has been identified and approved by the relevant competent authorities.

The construction phases will be initiated only after the securization of presale/preletting or similar forward commitment of whole or part of the buildings has been obtained in order to mitigate or neutralize market risk.

Projects of which the end-use of the property (through leasing or selling them off) falling into the following categories are explicitly excluded :

• Focus on weapons and ammunition, arms, military or police equipment or infrastructures, and equipment or infrastructure limiting people’s individual rights and freedom; • Focus on gambling and related equipment; • Focus on tobacco manufacturing, processing, or distribution; • Involve live animals insofar as compliance with the “Council of Europe’s Convention for the Protection of Vertebrate Animals used for Experimental and other Scientific Purposes” cannot be guaranteed; • May potentially cause lasting environmental damage; • May potentially restrain or reduce human rights; • May potentially lead to ethically or morally controversial disputes.

Energy efficiency

Exclusions

Market risk mitigation

Authorisation and permits

24

INTRODUCTION THE INITIATORS & THE FUND’S STRUCTURE INVESTMENT CRITERIA AND STRATEGY INVESTMENT PROCESS PROJECTS PRESENTATION

25

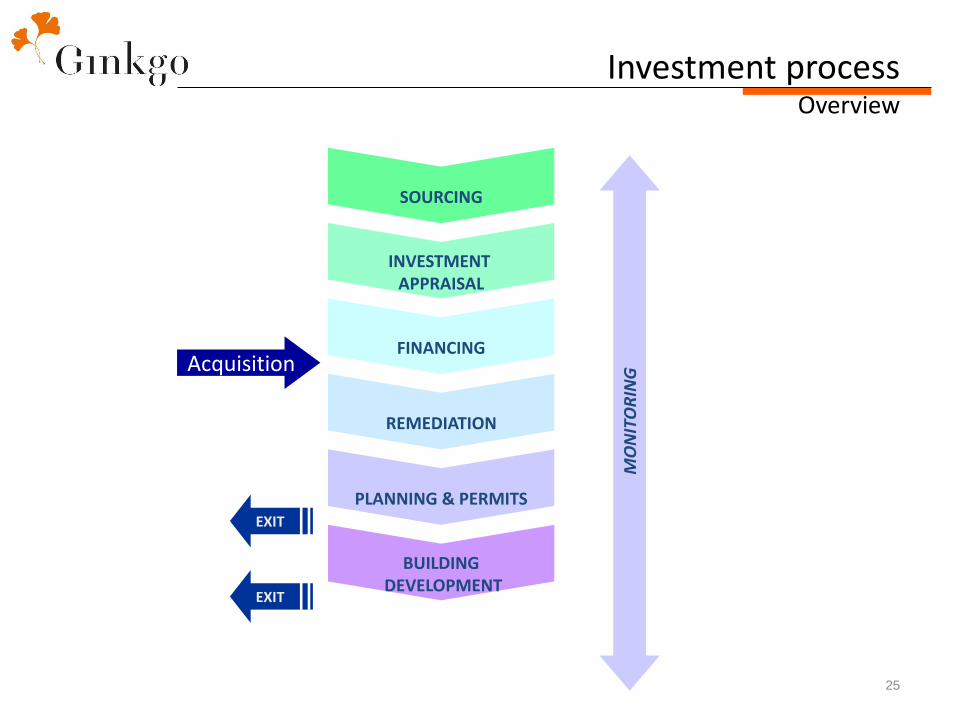

SOURCING

INVESTMENT

APPRAISAL

REMEDIATION

PLANNING & PERMITS

BUILDING

DEVELOPMENT

EXIT

EXIT

MO

NIT

OR

ING

Investment process Overview

FINANCING

Acquisition

26

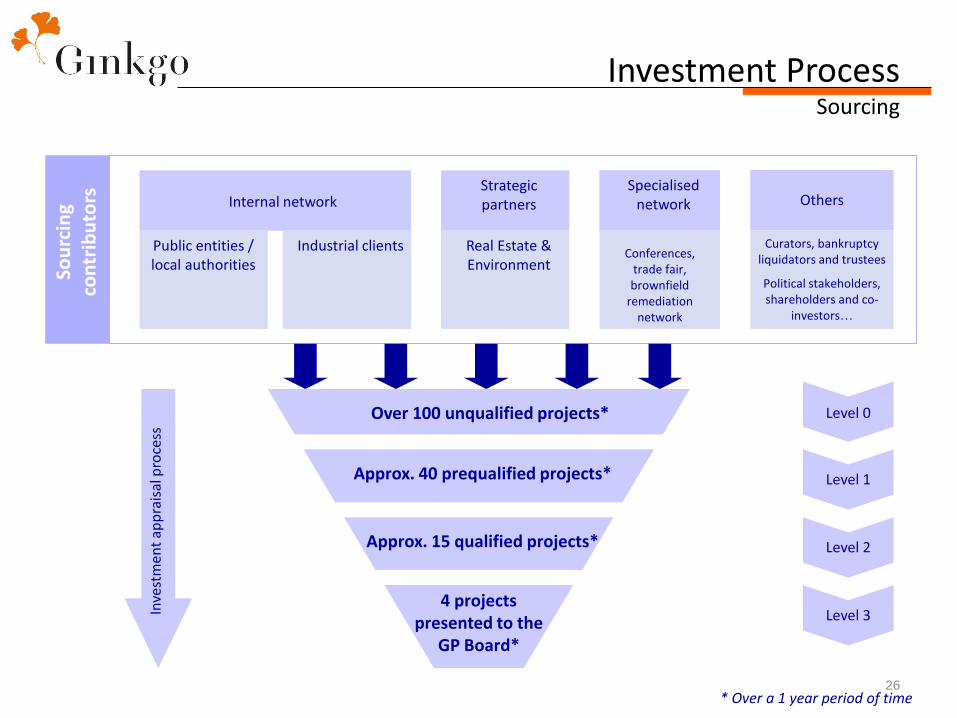

Investment Process Sourcing

Strategic partners

Curators, bankruptcy liquidators and trustees

Political stakeholders, shareholders and co-

investors…

Industrial clients

Public entities / local authorities

Internal network Specialised

network

Sou

rcin

g co

ntr

ibu

tors

Real Estate & Environment

Others

Conferences, trade fair, brownfield

remediation network

Over 100 unqualified projects*

* Over a 1 year period of time

Approx. 40 prequalified projects*

Approx. 15 qualified projects*

4 projects presented to the

GP Board*

Inve

stm

ent

app

rais

al p

roce

ss

Level 0

Level 1

Level 2

Level 3

27

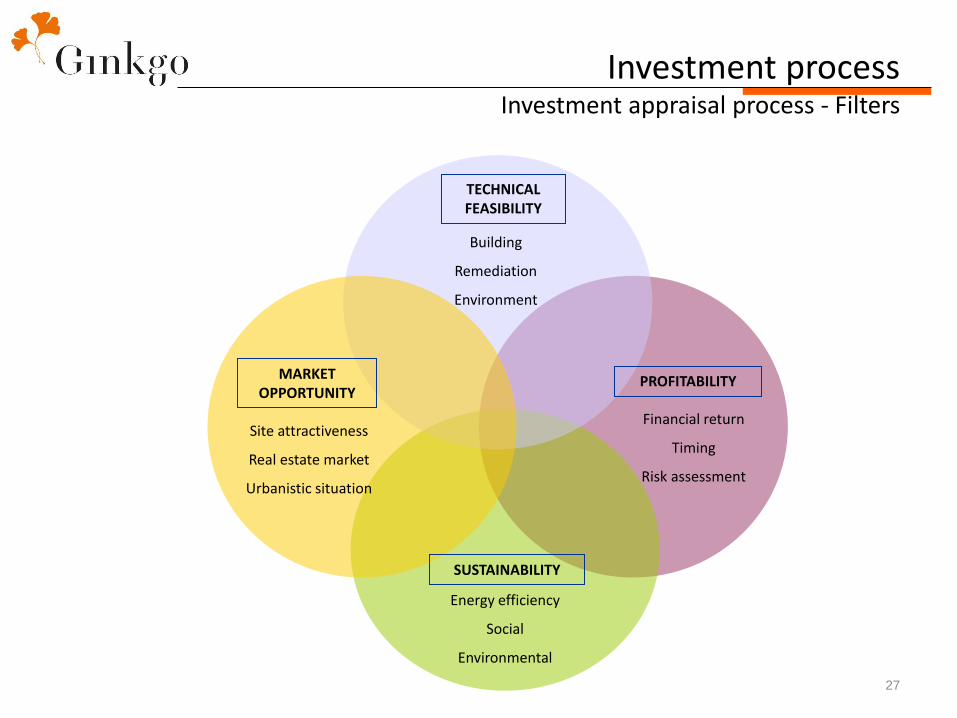

PROFITABILITY MARKET OPPORTUNITY

SUSTAINABILITY

TECHNICAL FEASIBILITY

Site attractiveness

Real estate market

Urbanistic situation

Building

Remediation

Environment

Energy efficiency

Social

Environmental

Financial return

Timing

Risk assessment

Investment process Investment appraisal process - Filters

28

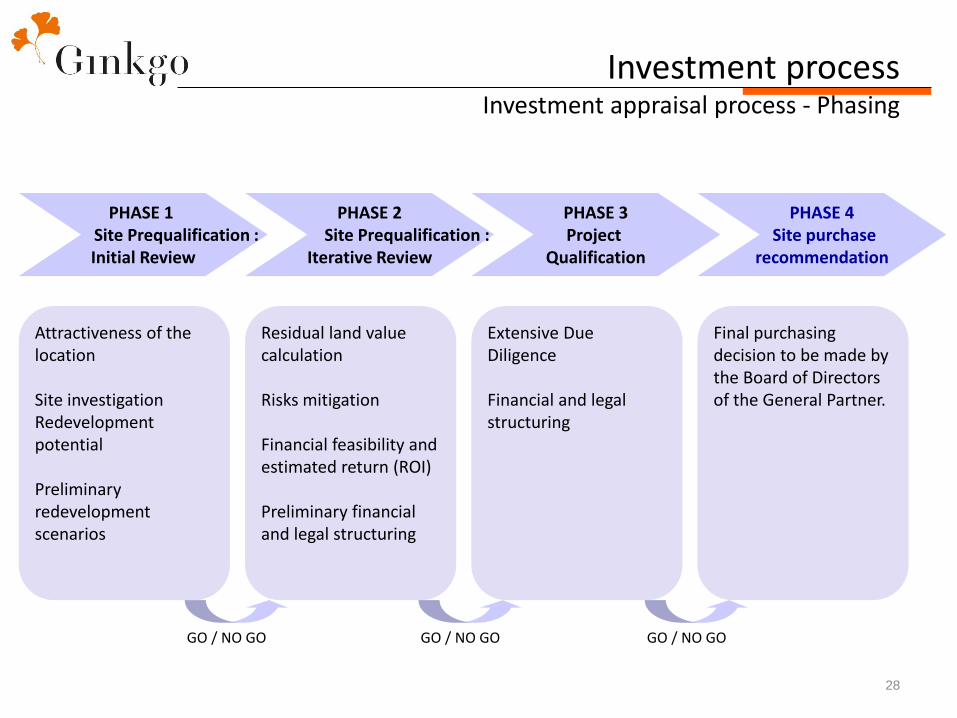

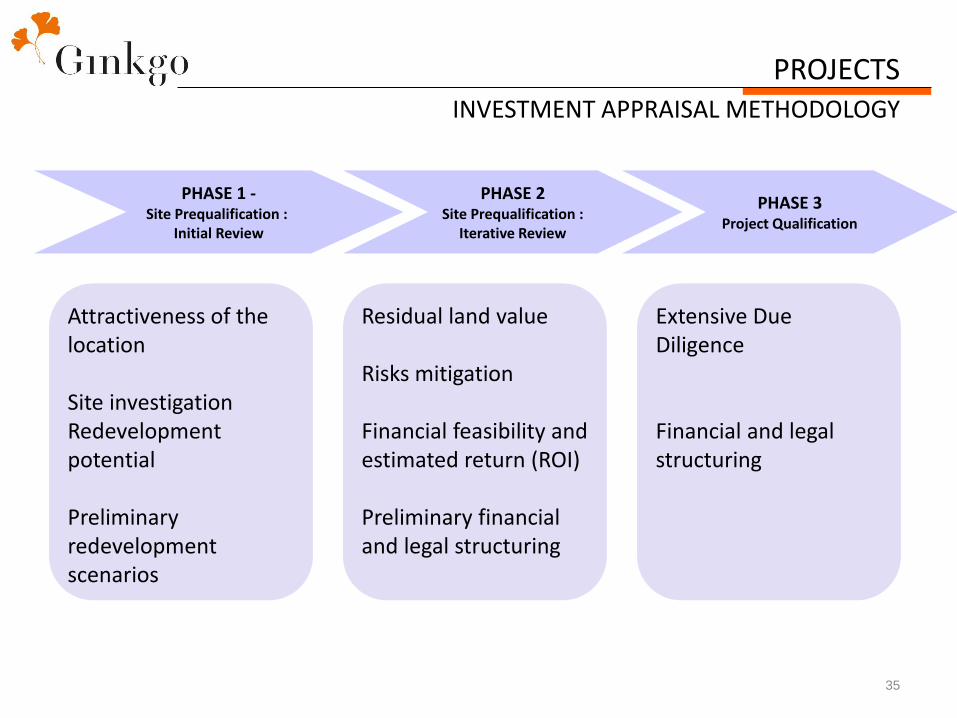

Investment process Investment appraisal process - Phasing

Residual land value calculation Risks mitigation Financial feasibility and estimated return (ROI) Preliminary financial and legal structuring

Attractiveness of the location Site investigation Redevelopment potential Preliminary redevelopment scenarios

Extensive Due Diligence Financial and legal structuring

PHASE 1 Site Prequalification :

Initial Review

PHASE 2 Site Prequalification :

Iterative Review

PHASE 3 Project

Qualification

GO / NO GO GO / NO GO

PHASE 4 Site purchase

recommendation

Final purchasing decision to be made by the Board of Directors of the General Partner.

GO / NO GO

29

Investment Process Financing

Selection of the optimum mix of financing methods in order to optimize the profit margin and of project debt financing on the best terms Project debt financing will be located at SPV level The debt to equity ratio will be conservative and in line with market practices with regards to the financing of these types of projects. The interest rate risk or currency risk will be hedged to cover potential increases in the cost of debt financing.

Optimal financing structure

Risk mitigation

Debt to equity ratio

Debt assignment

30

Investment Process Remediation

Remedial strategy design is carried out by the environmental experts of the Investment Advisor.

The Investment Advisor’s external environmental and legal advisors may provide technical assistance and support to the Investment Advisor’s environmental experts in charge of managing the brownfield remediation process.

Expertise of environmental legislation and regulatory support in the investigation and remediation process will be provided by the Investment Advisor’s legal advisors.

Illustrative steps of the remedial process : • Site reconnaissance and further soil investigations; • Descriptive investigations; • Site remediation investigations; • Technical and economic analyses for site remediation; • Laboratory feasibility tests • On-site pilot tests • Remedial design and implementation; • Geotechnical studies; • Monitoring of soil and ground water quality; • Risk evaluations and analysis; • Groundwater modelling; • Modelling of dispersion and migration of contaminants; • Risk management.

Internal and external Experts’

support

Remediation process

31

Investment Process Planning & Permits

Official contacts are made by the Investment Advisor with the authorities responsible for the granting of various appropriate permits (e.g. town planning and environmental certificate) and necessary authorizations.

If necessary, the Investment Advisor will seek the help of relevant third party experts for the application for planning permission from the competent authorities in line with their town development plans, as well as the assistance of its environmental and legal advisors. Whenever possible, Ginkgo will participate in the acquisition of brownfield land on the basis of approved (or soon to be approved) zoning which is consistent with a project development plan which has been carefully reviewed and approved in advance.

Contact with authorities

Risk mitigation

Assistance of external experts

32

Investment Process Building Development

Ginkgo expects to make its investments through SPVs, which it may set up together with other developers and partners

Ginkgo will not take direct responsibility for the management of the construction process, leaving such responsibility to a third party – for instance building developer-partner or a third party designated by it - who will act on behalf of the joint project vehicle

As a rule, several offers from various builders will be sought and, in addition to the construction management tasks performed by its building developer-partner, Ginkgo will also closely monitor the construction quality and the building progress

SPVs and partnerships

Monitoring

Construction risk mitigation

33

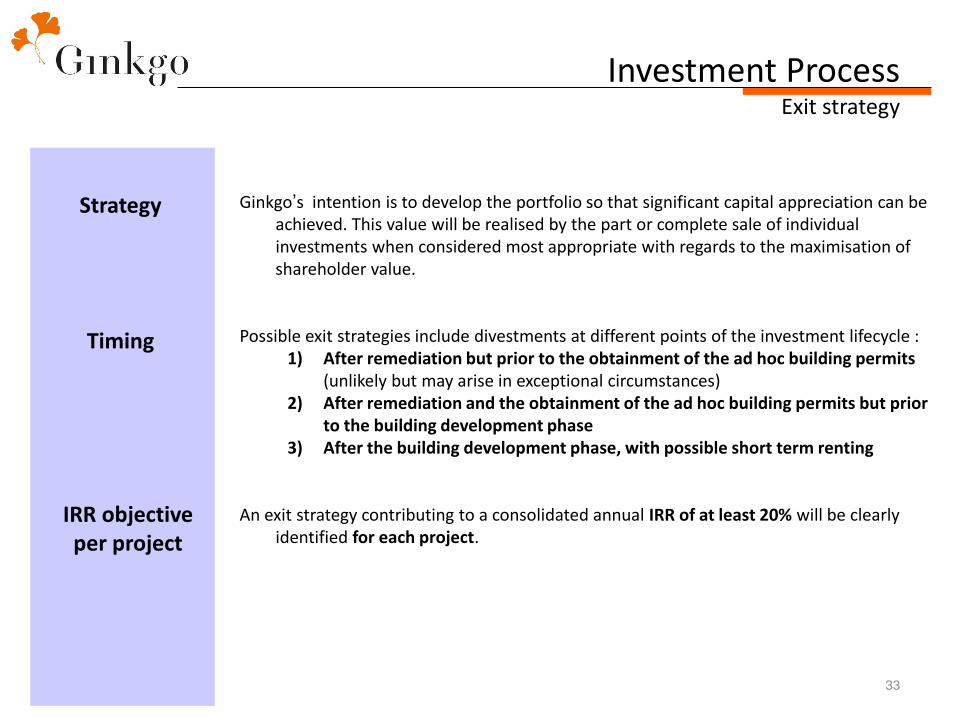

Investment Process Exit strategy

Ginkgo’s intention is to develop the portfolio so that significant capital appreciation can be achieved. This value will be realised by the part or complete sale of individual investments when considered most appropriate with regards to the maximisation of shareholder value.

Possible exit strategies include divestments at different points of the investment lifecycle :

1) After remediation but prior to the obtainment of the ad hoc building permits (unlikely but may arise in exceptional circumstances)

2) After remediation and the obtainment of the ad hoc building permits but prior to the building development phase

3) After the building development phase, with possible short term renting An exit strategy contributing to a consolidated annual IRR of at least 20% will be clearly

identified for each project.

Strategy

IRR objective per project

Timing

34

INTRODUCTION THE INITIATORS & THE FUND’S STRUCTURE INVESTMENT CRITERIA AND STRATEGY INVESTMENT PROCESS PROJECTS PRESENTATION

35

Residual land value Risks mitigation Financial feasibility and estimated return (ROI) Preliminary financial and legal structuring

Attractiveness of the location Site investigation Redevelopment potential Preliminary redevelopment scenarios

Extensive Due Diligence Financial and legal structuring

PHASE 1 - Site Prequalification :

Initial Review

PHASE 2 Site Prequalification :

Iterative Review

PHASE 3 Project Qualification

PROJECTS INVESTMENT APPRAISAL METHODOLOGY

36

“CRAEYENHOF” IN BURCHT (BELGIUM)

INVESTMENT APPRAISAL

PIPELINE

LEVEL 3 QUALIFIED PROJECT

37

OVERVIEW

Burcht - BELGIUM

Type Former petroleum storage depot located in a municipal area

Owner Craeyenhof nv (100 % SPV of ReGenius)

Location Burcht (Zwijndrecht), Belgium

Size 1.1 ha

Pollution Hydrocarbons, mineral oils, heavy metals, BTEX (benzene)

Sourcing Brocap

Status Potential Ginkgo co-investment in existing SPV

Project Residential, as part of a new Masterplan

Former petroleum storage depot site located in the center of Burcht, Zwijndrecht along the river Schelde and with proximity to Antwerp. Potential PPP with the bordering municipal land as an integrated Brownfield redevelopment.

38

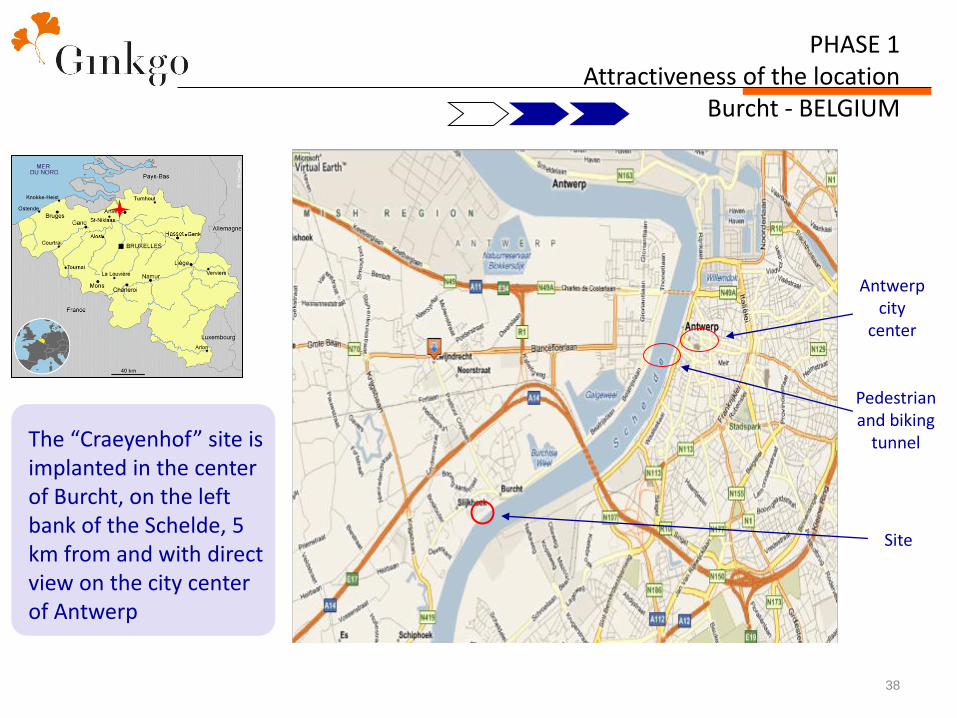

PHASE 1 Attractiveness of the location

Burcht - BELGIUM

Antwerp city

center

Site

The “Craeyenhof” site is implanted in the center of Burcht, on the left bank of the Schelde, 5 km from and with direct view on the city center of Antwerp

Pedestrian and biking

tunnel

39

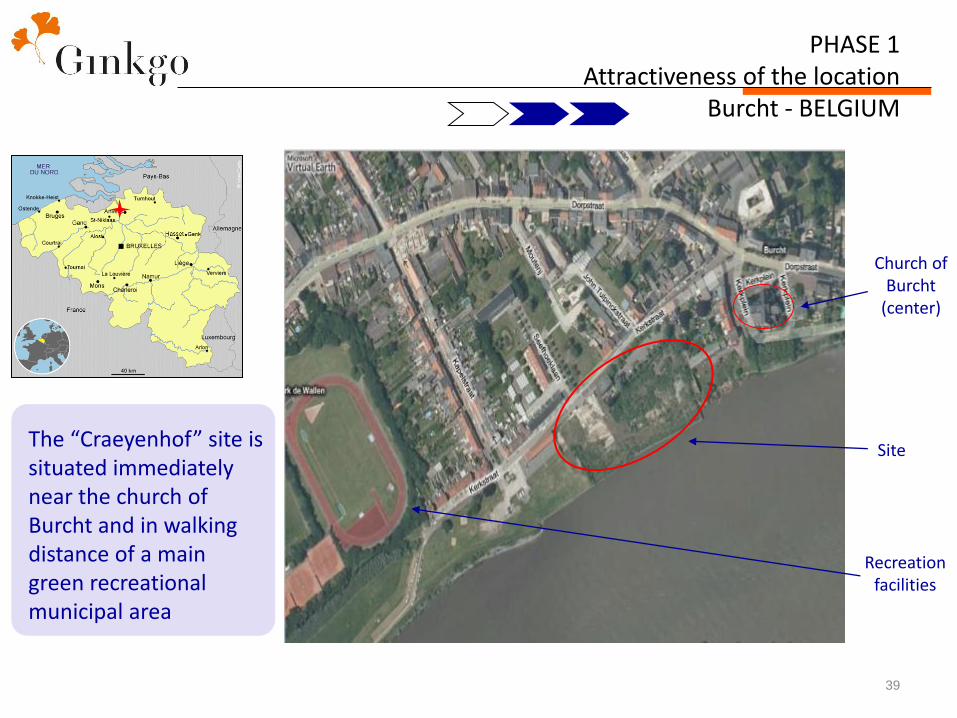

PHASE 1 Attractiveness of the location

Burcht - BELGIUM

Church of Burcht

(center)

Site The “Craeyenhof” site is situated immediately near the church of Burcht and in walking distance of a main green recreational municipal area

Recreation facilities

40

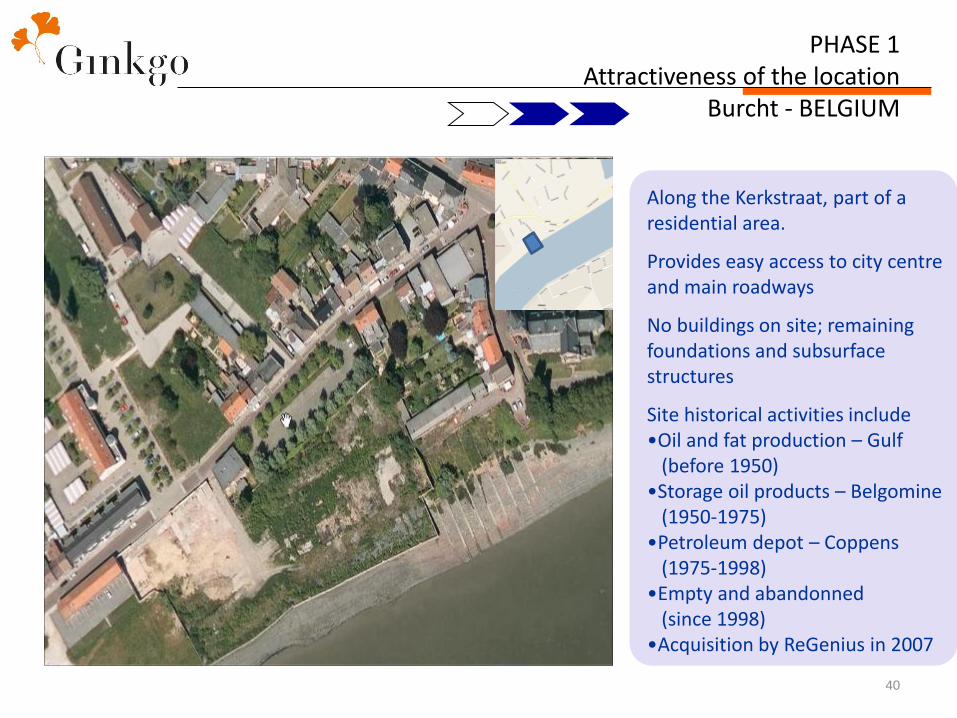

Along the Kerkstraat, part of a residential area.

Provides easy access to city centre and main roadways

No buildings on site; remaining foundations and subsurface structures

Site historical activities include •Oil and fat production – Gulf (before 1950) •Storage oil products – Belgomine (1950-1975) •Petroleum depot – Coppens (1975-1998) •Empty and abandonned (since 1998) •Acquisition by ReGenius in 2007

PHASE 1 Attractiveness of the location

Burcht - BELGIUM

41

PHASE 1 Site investigation redevelopment potential

Burcht - BELGIUM

The “Craeyenhof” site is one of the 42 listed brownfield sites selected by the Flemish Government to negotiate and sign a ‘brownfield convenant’ (application successfully filed by Brocap).

The Flemish government decree of March 30, 2007 regarding the brownfield convenants allows for:

• a convenant to be negotiated between the Flemish government and the private/public owner(s) of a brownfield site in which a mutual agreement is made about administrative procedures, timing and certain requisites to make the project feasible and realizable

• one contact point for all legislative matters concerning spatial and urban planning, the environment, permits, registration, ...

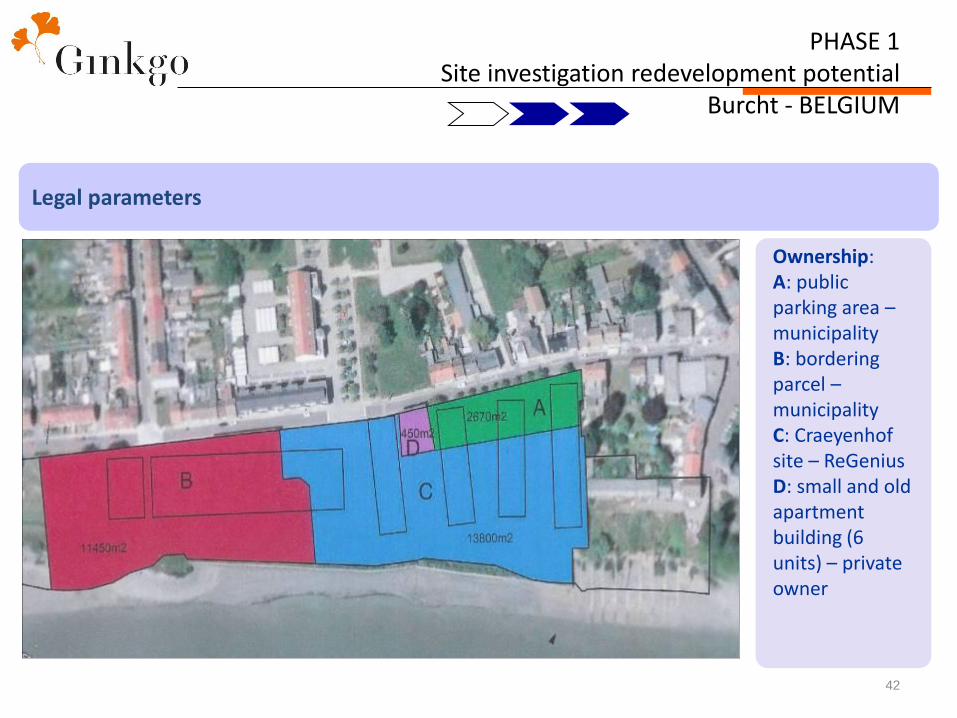

The municipality of Zwijndrecht is the owner of the bordering parcel and willing to consider a PPP in order to allow for an integrated and uniform redevelopment project along the Schelde riverbank

Legal parameters

42

PHASE 1 Site investigation redevelopment potential

Burcht - BELGIUM

Ownership: A: public parking area – municipality B: bordering parcel – municipality C: Craeyenhof site – ReGenius D: small and old apartment building (6 units) – private owner

Legal parameters

43

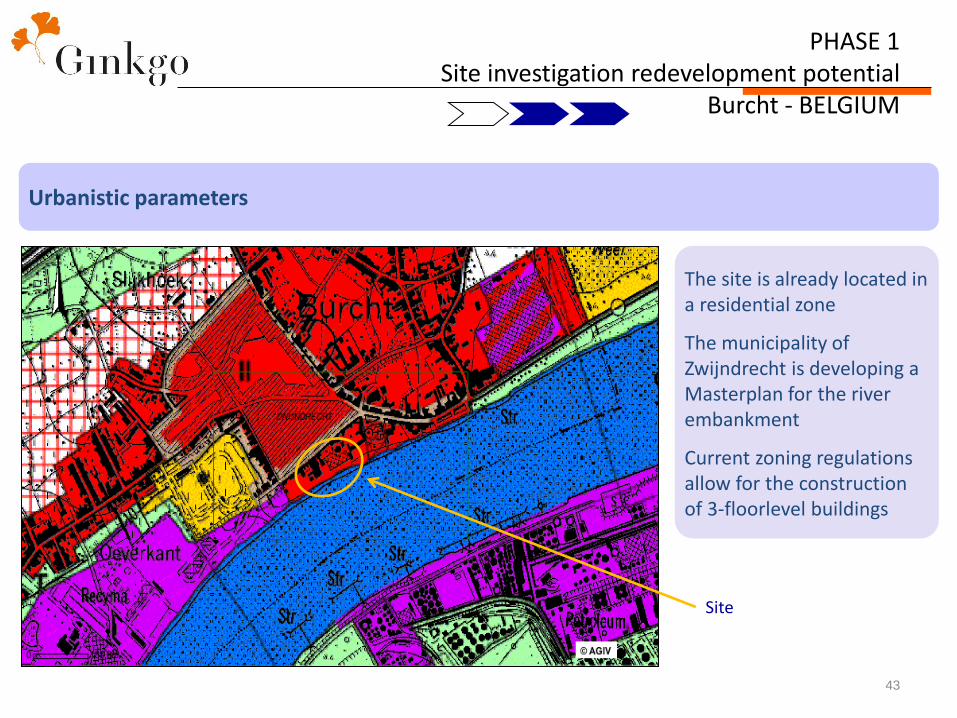

Urbanistic parameters

The site is already located in a residential zone

The municipality of Zwijndrecht is developing a Masterplan for the river embankment

Current zoning regulations allow for the construction of 3-floorlevel buildings

PHASE 1 Site investigation redevelopment potential

Burcht - BELGIUM

Site

44

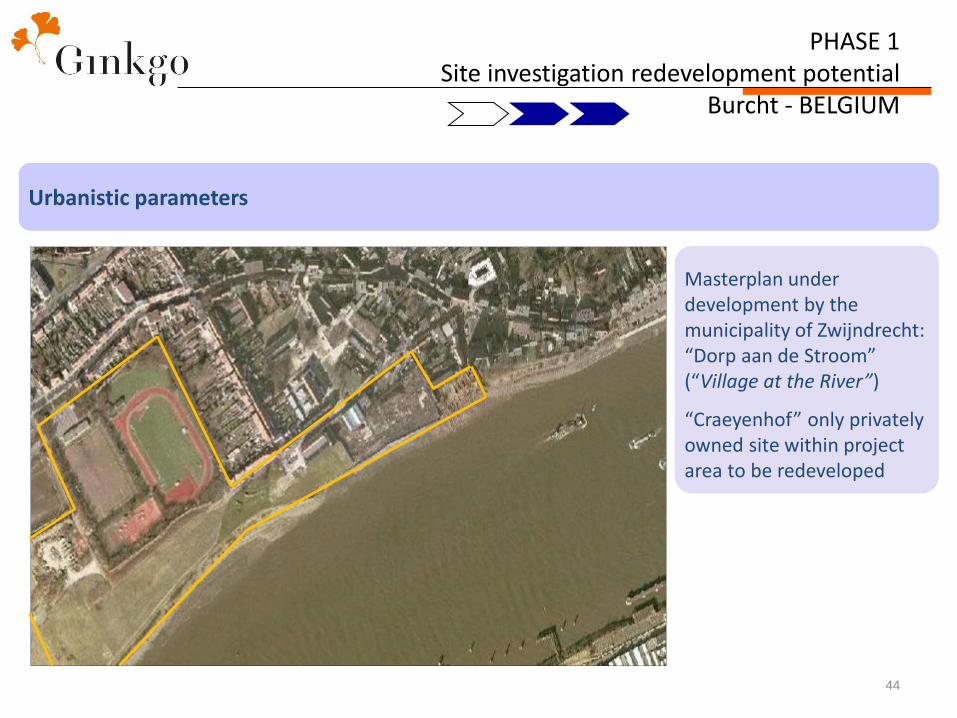

Urbanistic parameters

Masterplan under development by the municipality of Zwijndrecht: “Dorp aan de Stroom” (“Village at the River”)

“Craeyenhof” only privately owned site within project area to be redeveloped

PHASE 1 Site investigation redevelopment potential

Burcht - BELGIUM

45

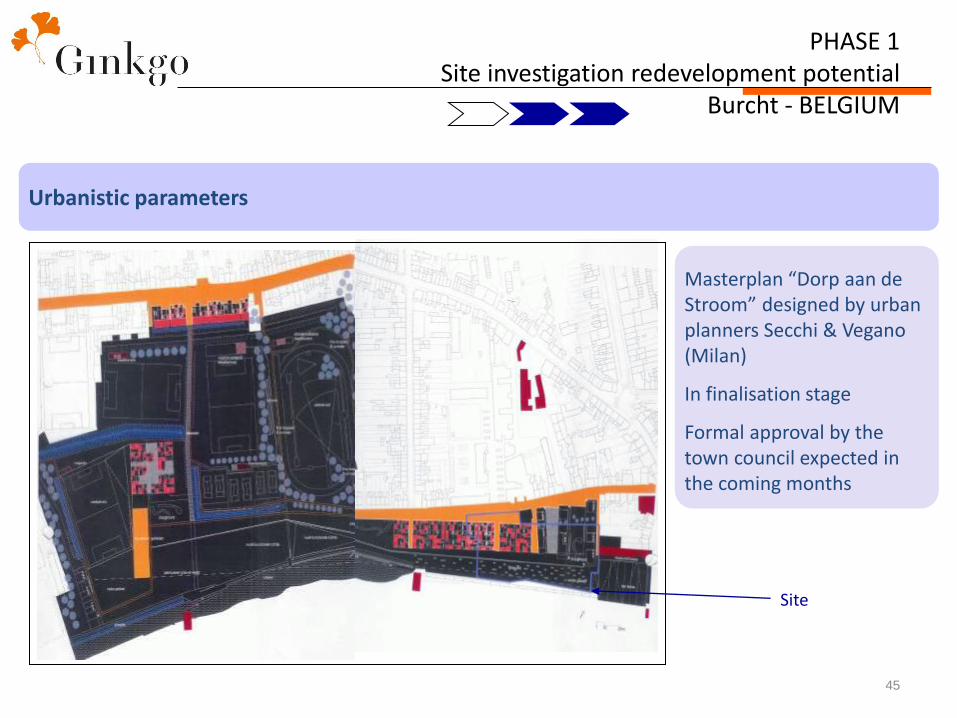

Urbanistic parameters

Masterplan “Dorp aan de Stroom” designed by urban planners Secchi & Vegano (Milan)

In finalisation stage

Formal approval by the town council expected in the coming months

PHASE 1 Site investigation redevelopment potential

Burcht - BELGIUM

Site

46

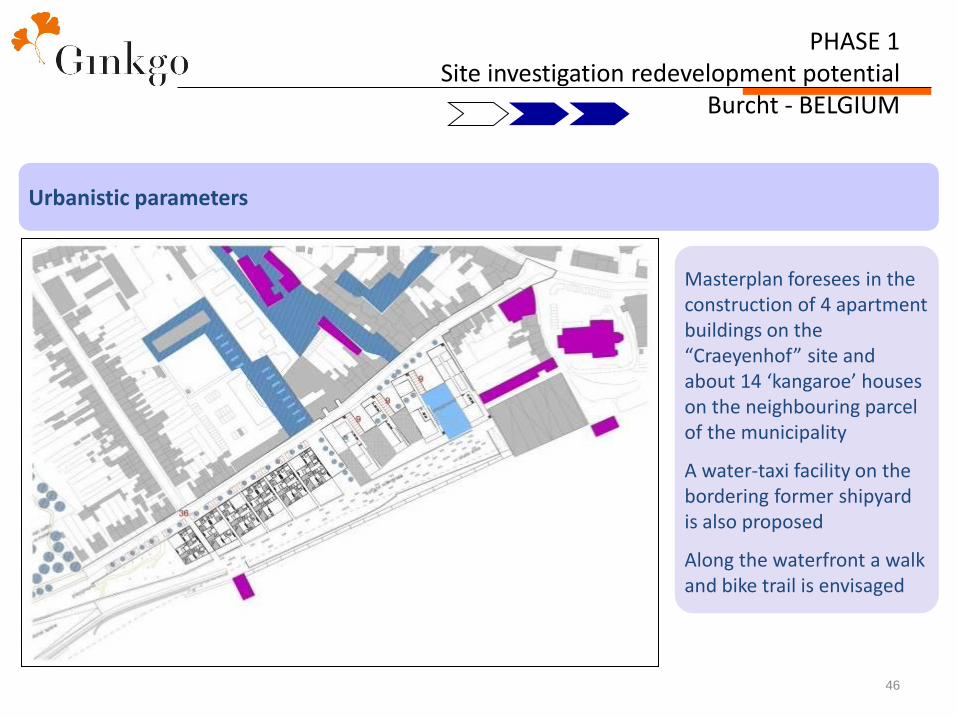

Urbanistic parameters

Masterplan foresees in the construction of 4 apartment buildings on the “Craeyenhof” site and about 14 ‘kangaroe’ houses on the neighbouring parcel of the municipality

A water-taxi facility on the bordering former shipyard is also proposed

Along the waterfront a walk and bike trail is envisaged

PHASE 1 Site investigation redevelopment potential

Burcht - BELGIUM

47

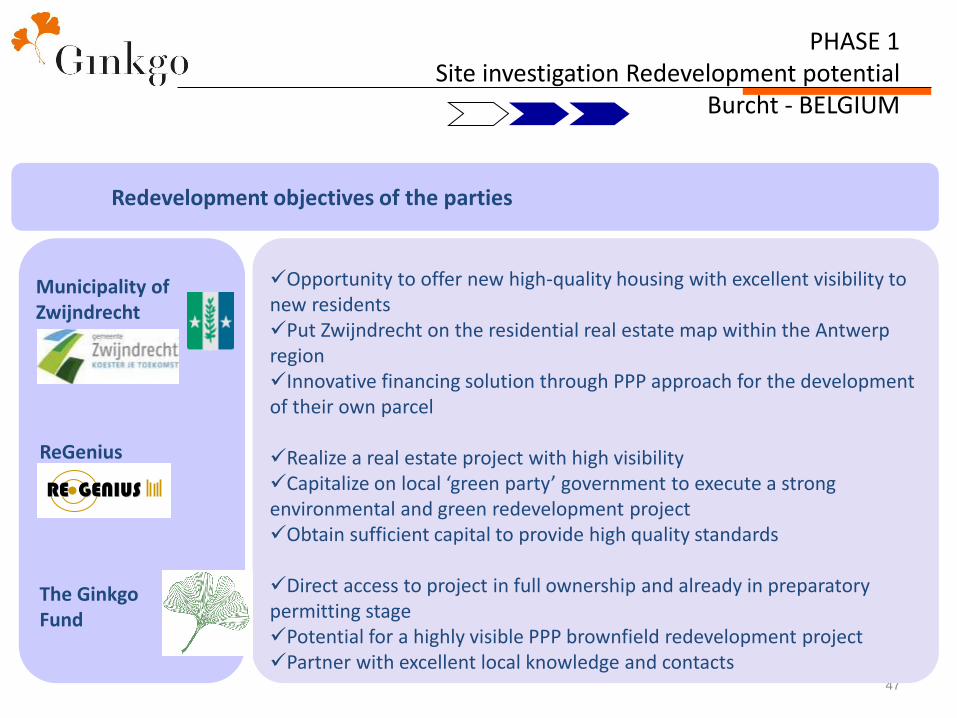

Opportunity to offer new high-quality housing with excellent visibility to new residents Put Zwijndrecht on the residential real estate map within the Antwerp region Innovative financing solution through PPP approach for the development of their own parcel Realize a real estate project with high visibility Capitalize on local ‘green party’ government to execute a strong environmental and green redevelopment project Obtain sufficient capital to provide high quality standards

Direct access to project in full ownership and already in preparatory permitting stage Potential for a highly visible PPP brownfield redevelopment project Partner with excellent local knowledge and contacts

Redevelopment objectives of the parties

PHASE 1 Site investigation Redevelopment potential

Burcht - BELGIUM

The Ginkgo Fund

Municipality of Zwijndrecht

ReGenius

REREGENIUSGENIUSRREEGGENIUSENIUS

48

The municipality of Zwijndrecht (ca. 18’000 inhabitants) wants to offer additional housing opportunities for new residents (current residential zoning potential limited)

The waterfront location, with view on the Antwerp skyline, provides a strong attractive factor

The municipality of Zwijndrecht has one of the lowest municipal taxation rates in the Flemish region

The city of Antwerp and the nearby harbour form an attractive social, cultural and professional catalyser

A market study shows that the average yearly fiscal income in Zwijndrecht and surroundings lays well above the Flemish average

Recent residential apartment sales prices in Zwijndrecht (not on the waterfront) are in the range of and slightly above 2000 Euro/sqm; similar prices on the Antwerp quays are well above the double

Real estate parameters

PHASE 1 Site investigation Redevelopment potential

Burcht - BELGIUM

49

Real estate parameters

PHASE 1 Site investigation Redevelopment potential

Burcht - BELGIUM

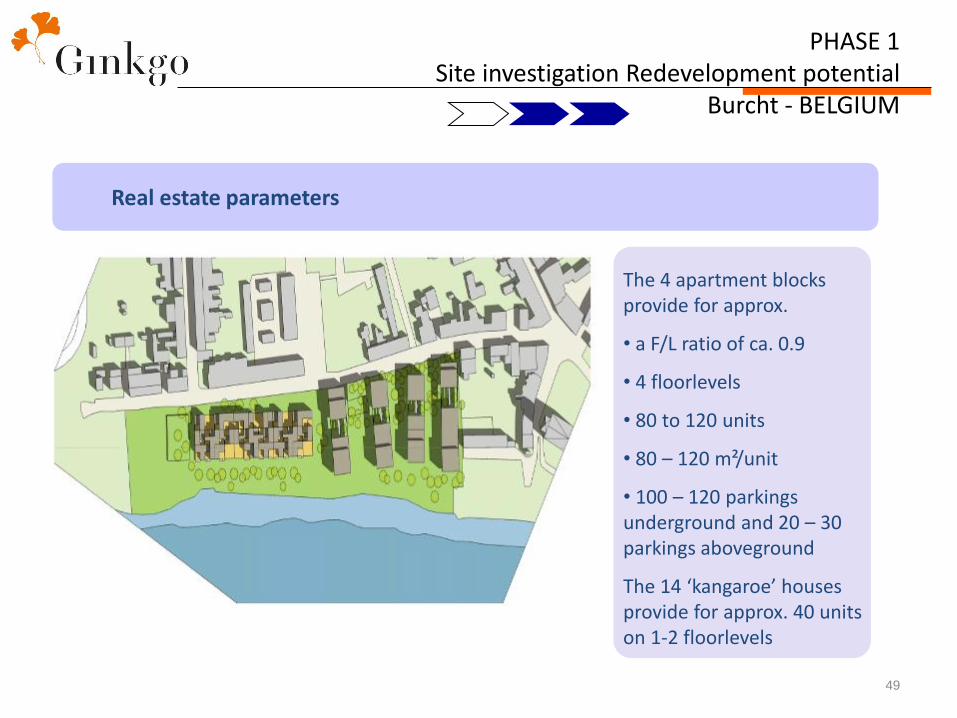

The 4 apartment blocks provide for approx.

• a F/L ratio of ca. 0.9

• 4 floorlevels

• 80 to 120 units

• 80 – 120 m²/unit

• 100 – 120 parkings underground and 20 – 30 parkings aboveground

The 14 ‘kangaroe’ houses provide for approx. 40 units on 1-2 floorlevels

50

Real estate parameters

PHASE 1 Preliminary redevelopment scenarios

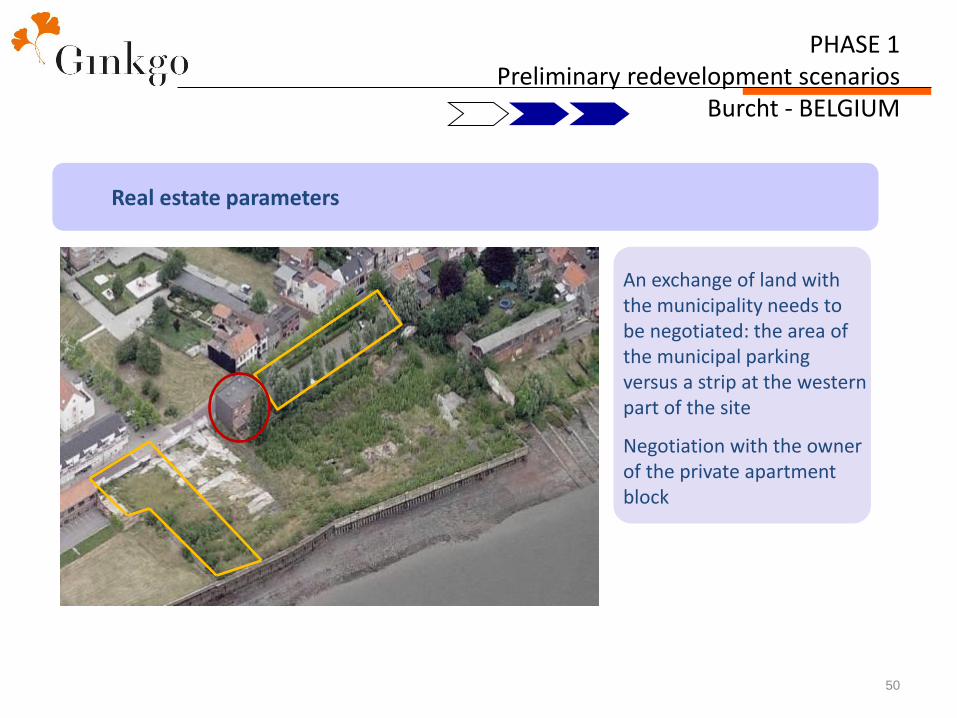

Burcht - BELGIUM

An exchange of land with the municipality needs to be negotiated: the area of the municipal parking versus a strip at the western part of the site

Negotiation with the owner of the private apartment block

51

Environmental parameters

PHASE 1 Preliminary redevelopment scenarios

Burcht - BELGIUM

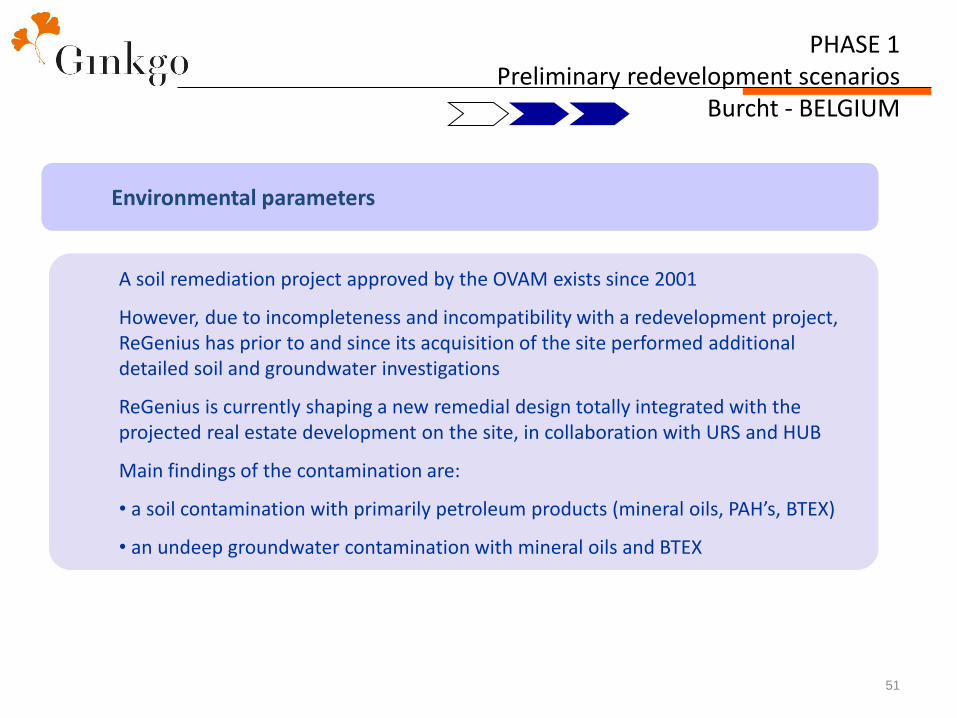

A soil remediation project approved by the OVAM exists since 2001

However, due to incompleteness and incompatibility with a redevelopment project, ReGenius has prior to and since its acquisition of the site performed additional detailed soil and groundwater investigations

ReGenius is currently shaping a new remedial design totally integrated with the projected real estate development on the site, in collaboration with URS and HUB

Main findings of the contamination are:

• a soil contamination with primarily petroleum products (mineral oils, PAH’s, BTEX)

• an undeep groundwater contamination with mineral oils and BTEX

52

Environmental parameters

PHASE 1 Preliminary redevelopment scenarios

Burcht - BELGIUM

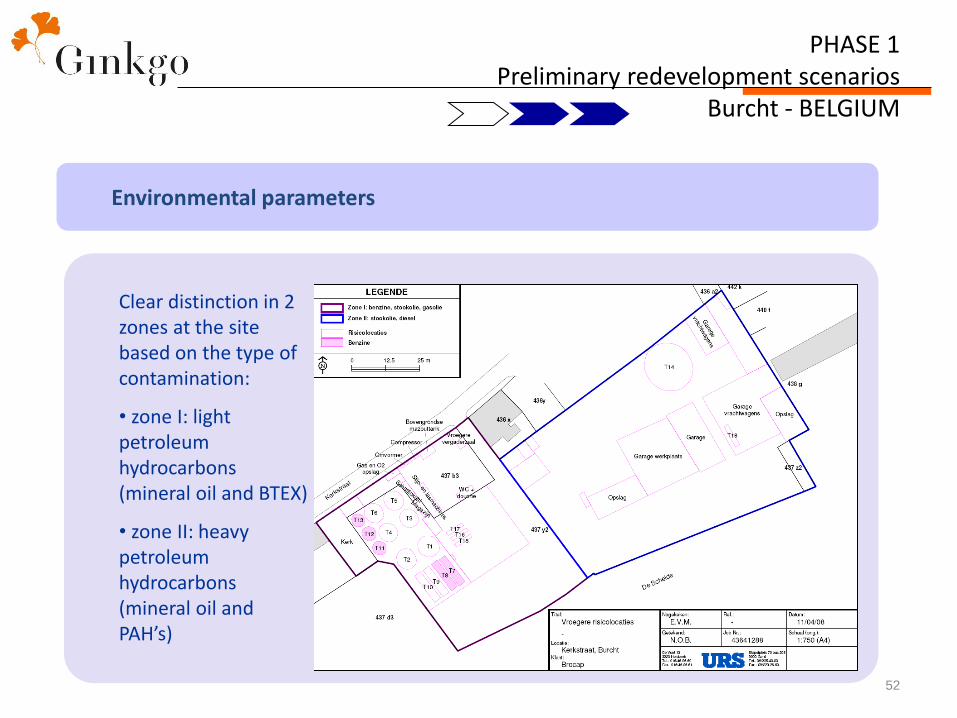

Clear distinction in 2 zones at the site based on the type of contamination:

• zone I: light petroleum hydrocarbons (mineral oil and BTEX)

• zone II: heavy petroleum hydrocarbons (mineral oil and PAH’s)

53

PHASE 1 Preliminary redevelopment scenarios

Burcht - BELGIUM

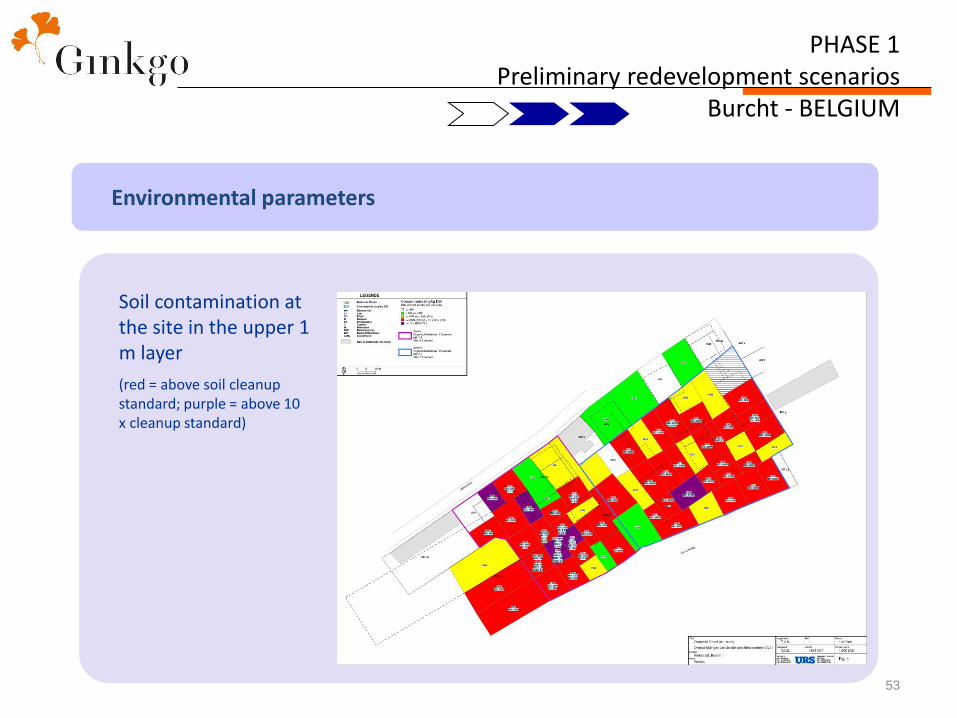

Soil contamination at the site in the upper 1 m layer

(red = above soil cleanup standard; purple = above 10 x cleanup standard)

Environmental parameters

54

PHASE 1 Preliminary redevelopment scenarios

Burcht - BELGIUM

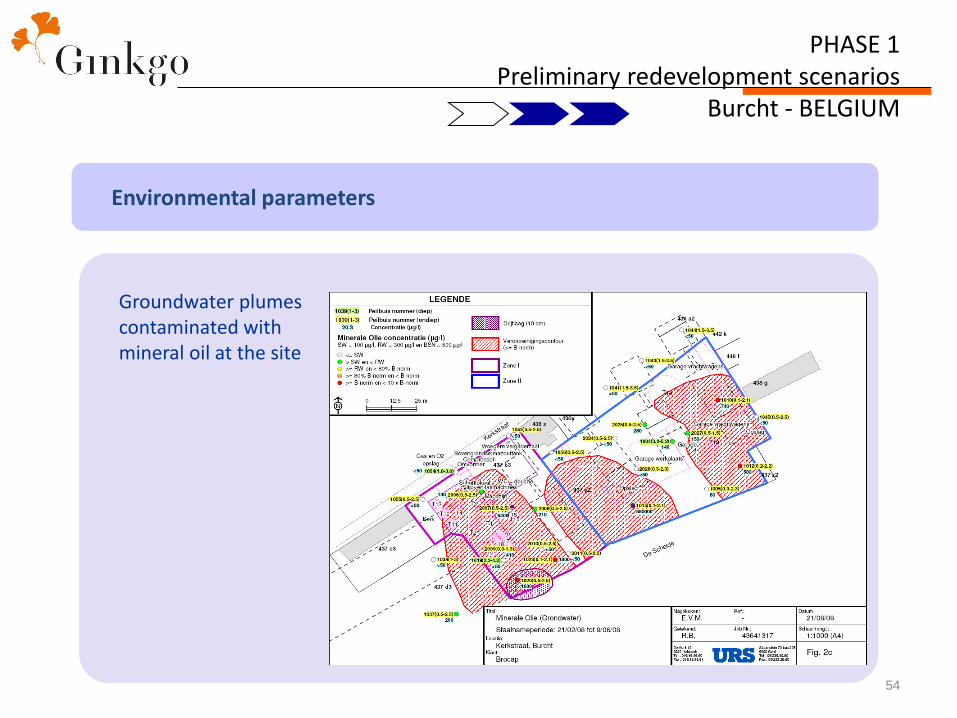

Groundwater plumes contaminated with mineral oil at the site

Environmental parameters

55

PHASE 1 Preliminary redevelopment scenarios

Burcht - BELGIUM

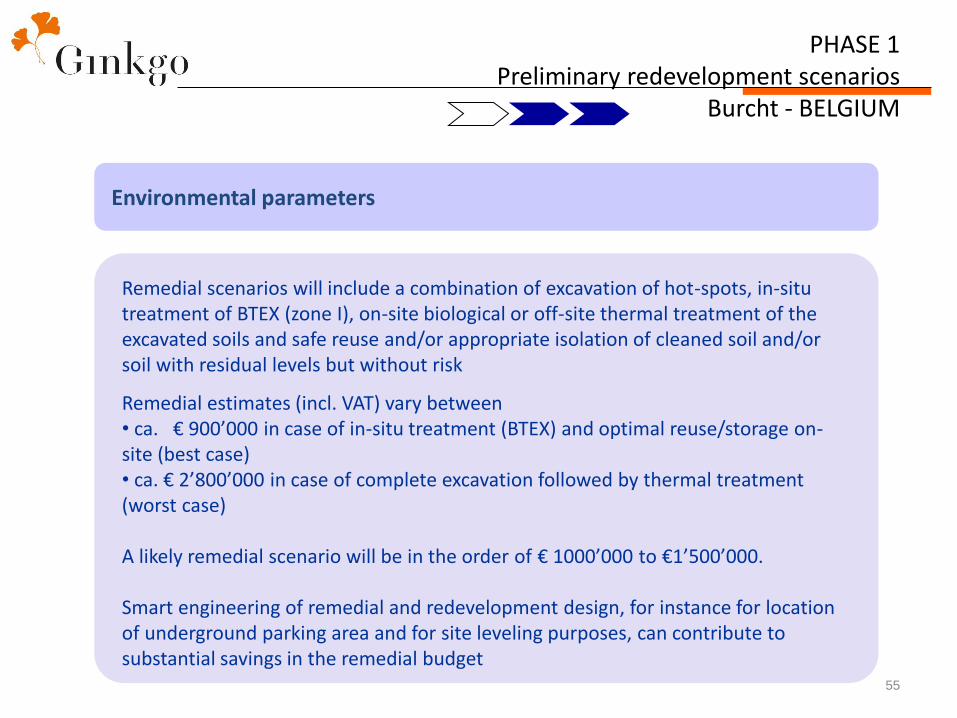

Remedial scenarios will include a combination of excavation of hot-spots, in-situ treatment of BTEX (zone I), on-site biological or off-site thermal treatment of the excavated soils and safe reuse and/or appropriate isolation of cleaned soil and/or soil with residual levels but without risk

Remedial estimates (incl. VAT) vary between • ca. € 900’000 in case of in-situ treatment (BTEX) and optimal reuse/storage on-site (best case) • ca. € 2’800’000 in case of complete excavation followed by thermal treatment (worst case)

A likely remedial scenario will be in the order of € 1000’000 to €1’500’000. Smart engineering of remedial and redevelopment design, for instance for location of underground parking area and for site leveling purposes, can contribute to substantial savings in the remedial budget

Environmental parameters

56

PHASE 1 Preliminary redevelopment scenarios

Burcht - BELGIUM

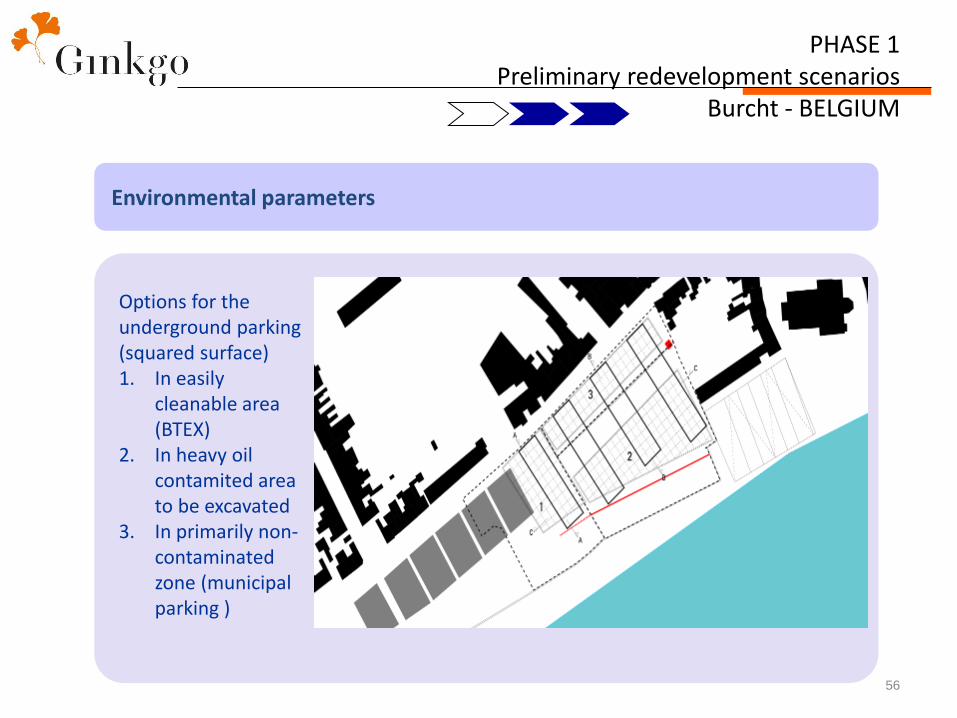

Options for the underground parking (squared surface) 1. In easily

cleanable area (BTEX)

2. In heavy oil contamited area to be excavated

3. In primarily non-contaminated zone (municipal parking )

Environmental parameters

57

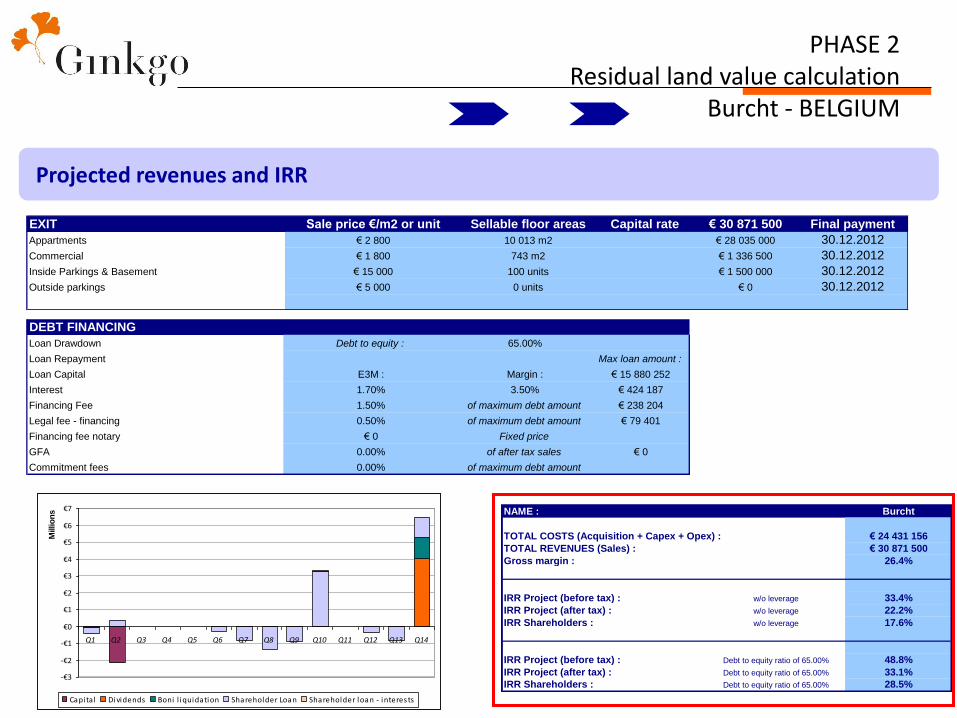

PHASE 2 Residual land value calculation

Burcht - BELGIUM

Projected costs

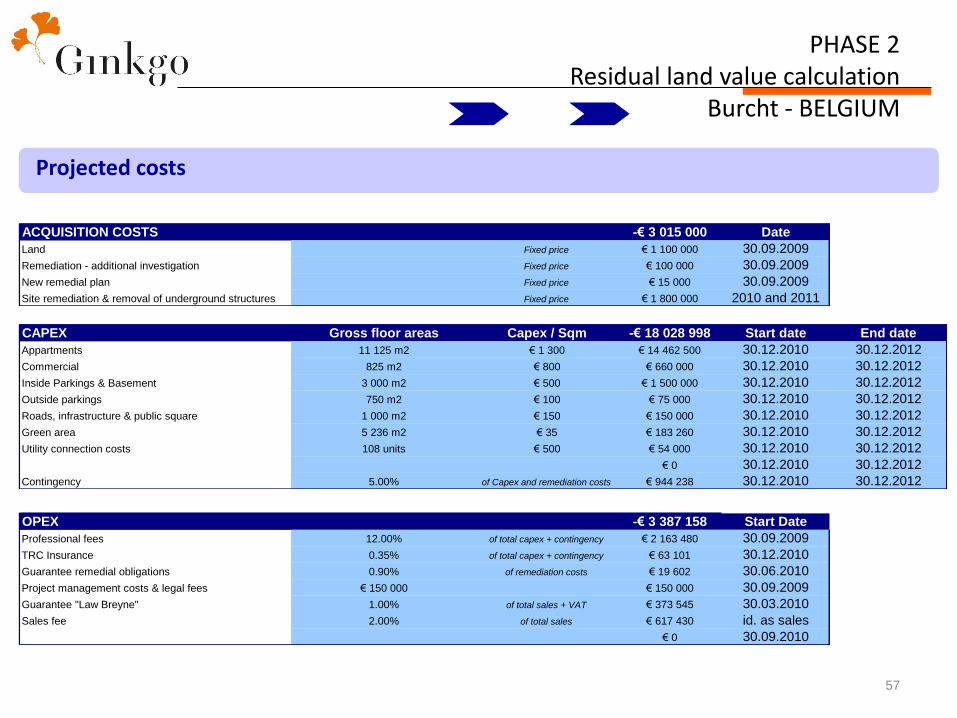

ACQUISITION COSTS -€ 3 015 000 Date

Land Fixed price € 1 100 000 30.09.2009

Remediation - additional investigation Fixed price € 100 000 30.09.2009

New remedial plan Fixed price € 15 000 30.09.2009

Site remediation & removal of underground structures Fixed price € 1 800 000 2010 and 2011

CAPEX Gross floor areas Capex / Sqm -€ 18 028 998 Start date End date

Appartments 11 125 m2 € 1 300 € 14 462 500 30.12.2010 30.12.2012

Commercial 825 m2 € 800 € 660 000 30.12.2010 30.12.2012

Inside Parkings & Basement 3 000 m2 € 500 € 1 500 000 30.12.2010 30.12.2012

Outside parkings 750 m2 € 100 € 75 000 30.12.2010 30.12.2012

Roads, infrastructure & public square 1 000 m2 € 150 € 150 000 30.12.2010 30.12.2012

Green area 5 236 m2 € 35 € 183 260 30.12.2010 30.12.2012

Utility connection costs 108 units € 500 € 54 000 30.12.2010 30.12.2012

€ 0 30.12.2010 30.12.2012

Contingency 5.00% of Capex and remediation costs € 944 238 30.12.2010 30.12.2012

OPEX -€ 3 387 158 Start Date

Professional fees 12.00% of total capex + contingency € 2 163 480 30.09.2009

TRC Insurance 0.35% of total capex + contingency € 63 101 30.12.2010

Guarantee remedial obligations 0.90% of remediation costs € 19 602 30.06.2010

Project management costs & legal fees € 150 000 € 150 000 30.09.2009

Guarantee "Law Breyne" 1.00% of total sales + VAT € 373 545 30.03.2010

Sales fee 2.00% of total sales € 617 430 id. as sales

€ 0 30.09.2010

58

PHASE 2 Residual land value calculation

Burcht - BELGIUM

Projected revenues and IRR

NAME : Burcht

TOTAL COSTS (Acquisition + Capex + Opex) : € 24 431 156

TOTAL REVENUES (Sales) : € 30 871 500

Gross margin : 26.4%

IRR Project (before tax) : w/o leverage 33.4%

IRR Project (after tax) : w/o leverage 22.2%

IRR Shareholders : w/o leverage 17.6%

IRR Project (before tax) : Debt to equity ratio of 65.00% 48.8%

IRR Project (after tax) : Debt to equity ratio of 65.00% 33.1%

IRR Shareholders : Debt to equity ratio of 65.00% 28.5%-€3

-€2

-€1

€0

€1

€2

€3

€4

€5

€6

€7

Q1 Q2 Q3 Q4 Q5 Q6 Q7 Q8 Q9 Q10 Q11 Q12 Q13 Q14

Millio

ns

Capita l Dividends Boni l iquidation Shareholder Loan Shareholder loan - interests

EXIT Sale price €/m2 or unit Sellable floor areas Capital rate € 30 871 500 Final payment

Appartments € 2 800 10 013 m2 € 28 035 000 30.12.2012

Commercial € 1 800 743 m2 € 1 336 500 30.12.2012

Inside Parkings & Basement € 15 000 100 units € 1 500 000 30.12.2012

Outside parkings € 5 000 0 units € 0 30.12.2012

DEBT FINANCING

Loan Drawdown Debt to equity : 65.00%

Loan Repayment Max loan amount :

Loan Capital E3M : Margin : € 15 880 252

Interest 1.70% 3.50% € 424 187

Financing Fee 1.50% of maximum debt amount € 238 204

Legal fee - financing 0.50% of maximum debt amount € 79 401

Financing fee notary € 0 Fixed price

GFA 0.00% of after tax sales € 0

Commitment fees 0.00% of maximum debt amount

59

PHASE 2 Risk Mitigation

Burcht - BELGIUM

Identifies significant soil and groundwater contamination on site with primarily mineral oils and BTEX. The estimated remediation budget is of €2.8 million for a worst-case scenario but should - more realistically – be of €1.0 to €1.5 million

Thorough and extensive environmental data available Detailed remedial scenario still to be selected and engineered; however integration with potential redevelopment plans and scenarios on-going Screening of biological treatment option necessary by means of external validation (Soil Treatment Center) or an on-site pilot test

Existing study

Investment Advisor assessment

Environmental parameters

60

PHASE 2 Risk Mitigation

Burcht - BELGIUM

Demonstrate a virtuous approach (i.e. more than legally required remediation approach) based on the environmental risk assessment

Negotiate an acceptable risk-based clean-up level with authorities in the framework of the brownfield convenant

Mitigation

Environmental parameters

61

PHASE 2 Risk Mitigation

Burcht - BELGIUM

Brocap assessment :

• Approval of Masterplan and consequent zoning plan recommended

• Exchange of land (municipal parking) preferable to allow for a smooth redevelopment process

Development risk

Obtain approval to start phased construction in accordance with drafted Masterplan given that the site is currently situated in a residential zone, eventually as part of the brownfield convenant to be negotiated

Negotiate exchange of land as soon as possible with municipality as part of PPP contract or brownfield convenant

Mitigation

Investment Advisor assessment

62

PHASE 2 Risk Mitigation

Burcht - BELGIUM

Brocap assessment :

• Strong local real estate market

• Phased redevelopment possible (4 blocks)

• Construction only started after sufficient pre-sales

• Strong interest and consultation by different local and national project developers to team-up or to get an option to buy

Promotion risk

Team up with project developers bearing the promotion risk Mitigation

Investment Advisor assessment

63

PHASE 2 Risk Mitigation

Burcht - BELGIUM

Change of local coalition (however unexpected)

Lack of a brownfield convenant with the Flemish government (upcoming elections in June 2009)

Political risk

Mitigation

Investment Advisor assessment

Negotiate a PPP contract or sign a convention with the municipality of Zwijndrecht regarding the land exchange (municipal parking) and a joint and integrated redevelopment project along the riverbank

Design for a feasible project even without the ‘admissions’ from the government in the brownfield convenant

64

ReGenius already fully owns the site, through its SPV “Craeyenhof” Ginkgo partners with ReGenius (joint venture) and enters into the capital of the SPV “Craeyenhof” ReGenius negotiates a brownfield convenant with the Flemish government allowing for risk-based clean-up levels and approved remedial plan

ReGenius (SPV) enters into a partnership with the municipality of Zwijndrecht in order to execute the land exchange, to obtain zoning approval and the necessary permits and to realize the integrated redevelopment along the riverbank ReGenius (SPV) teams up with one or several project developers

PHASE 2 Preliminary legal structuring

Burcht - BELGIUM

Site Acquisition

Legal / PPP steps

Capital opening

PPP and zoning

Convenant and remediation

Development

65

PHASE 3 Due diligence

Burcht - BELGIUM

Site information index card – Brocap/ReGenius

URS report “aanvullend bodemonderzoek Kerkstraat”, nov. 2008

Memorandum URS remedial scenarios brownfield site Burcht, oct. 2008

Detailed note Lydian lawyers on ‘legal issues PPP redevelopment Burcht’, sept 2007

Report Brocap – Market analysis Draft masterplan, Secchi & Vegano

Supporting documents

Environmental

Urban

Legal

Real Estate

General

66

PHASE 3 Legal structuring

Burcht - BELGIUM

Negotiation with municipality regarding land exchange (municipal parking)

Awaitening start of negotations with Flemish government coming weeks

Designing several redevelopment scenarios in line with draft Masterplan but based on findings of soil contamination

Transactions under way

Site Acquisition

Convenant

Urban

67

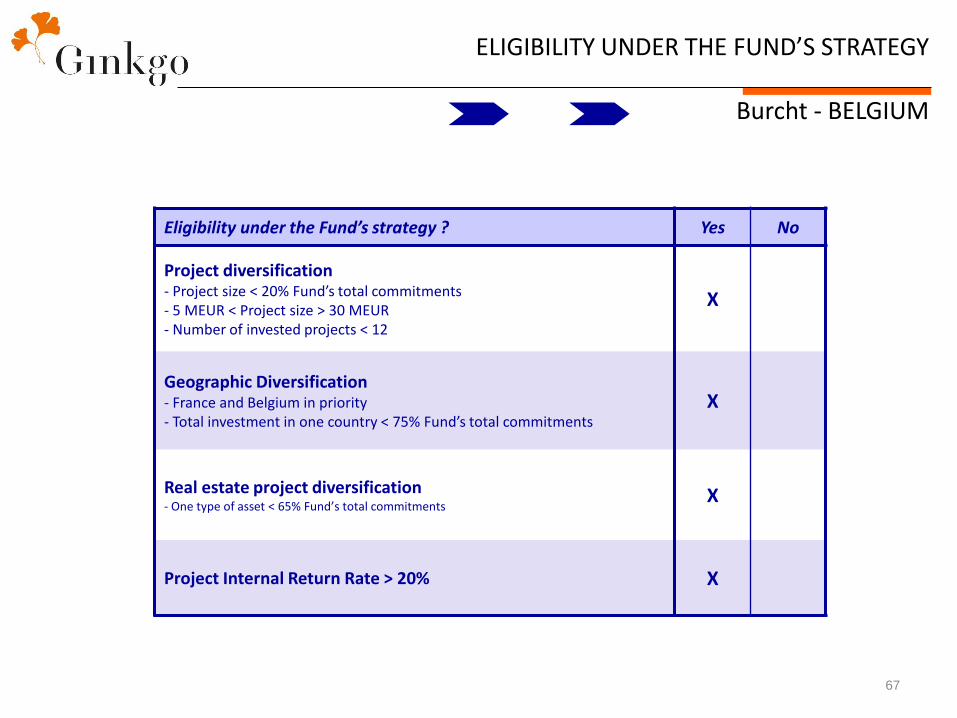

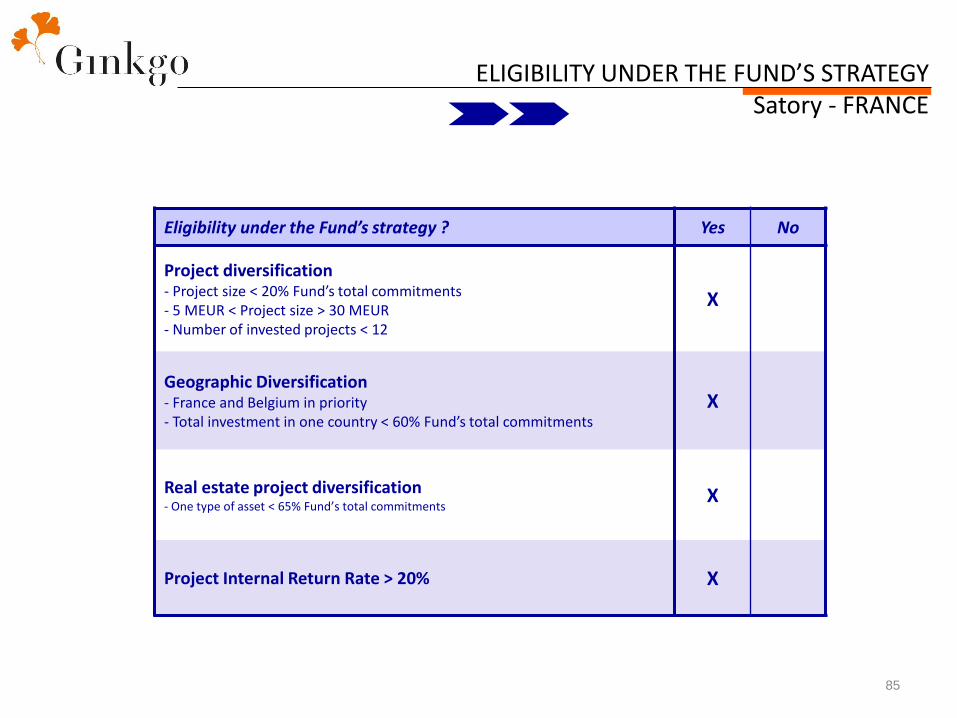

Eligibility under the Fund’s strategy ? Yes No

Project diversification - Project size < 20% Fund’s total commitments - 5 MEUR < Project size > 30 MEUR - Number of invested projects < 12

X

Geographic Diversification - France and Belgium in priority - Total investment in one country < 75% Fund’s total commitments

X

Real estate project diversification - One type of asset < 65% Fund’s total commitments

X

Project Internal Return Rate > 20% X

ELIGIBILITY UNDER THE FUND’S STRATEGY

Burcht - BELGIUM

68

VERSAILLES - SATORY (FRANCE)

INVESTMENT APPRAISAL

PIPELINE

LEVEL 3 QUALIFIED PROJECT

69

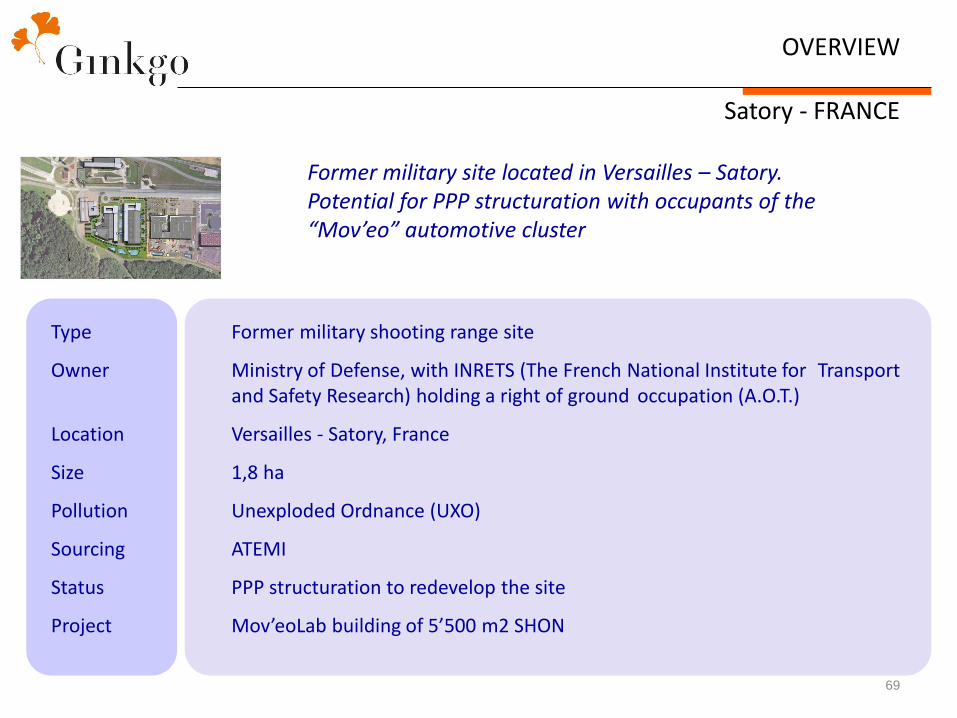

Type Former military shooting range site

Owner Ministry of Defense, with INRETS (The French National Institute for Transport and Safety Research) holding a right of ground occupation (A.O.T.)

Location Versailles - Satory, France

Size 1,8 ha

Pollution Unexploded Ordnance (UXO)

Sourcing ATEMI

Status PPP structuration to redevelop the site

Project Mov’eoLab building of 5’500 m2 SHON

Former military site located in Versailles – Satory. Potential for PPP structuration with occupants of the “Mov’eo” automotive cluster

OVERVIEW

Satory - FRANCE

70

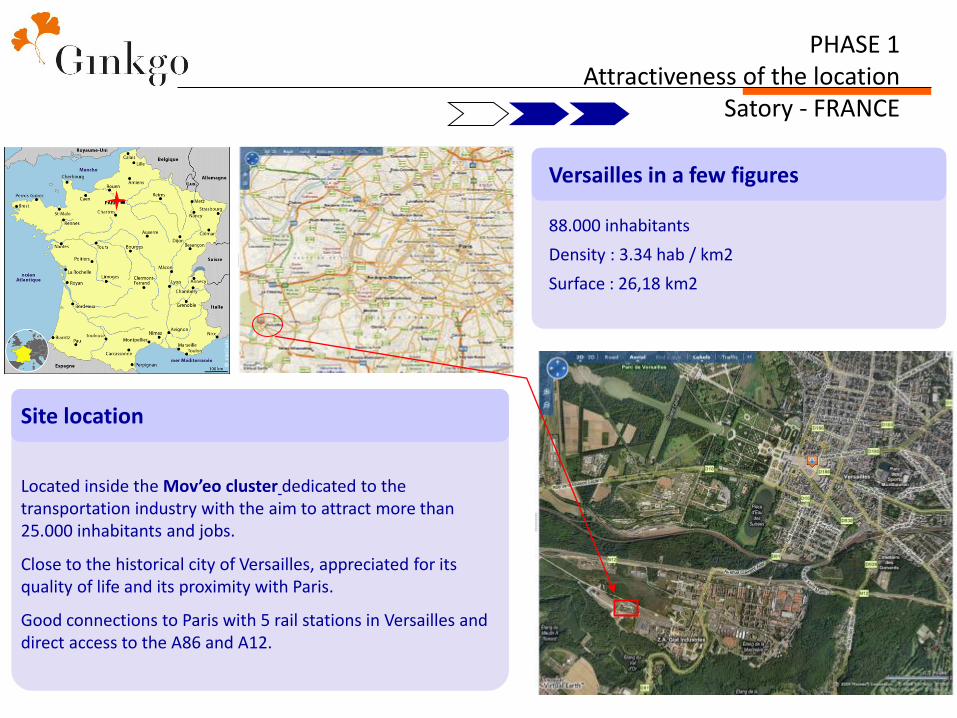

Site location

Located inside the Mov’eo cluster dedicated to the transportation industry with the aim to attract more than 25.000 inhabitants and jobs.

Close to the historical city of Versailles, appreciated for its quality of life and its proximity with Paris.

Good connections to Paris with 5 rail stations in Versailles and direct access to the A86 and A12.

Versailles in a few figures

88.000 inhabitants

Density : 3.34 hab / km2

Surface : 26,18 km2

PHASE 1 Attractiveness of the location

Satory - FRANCE

71

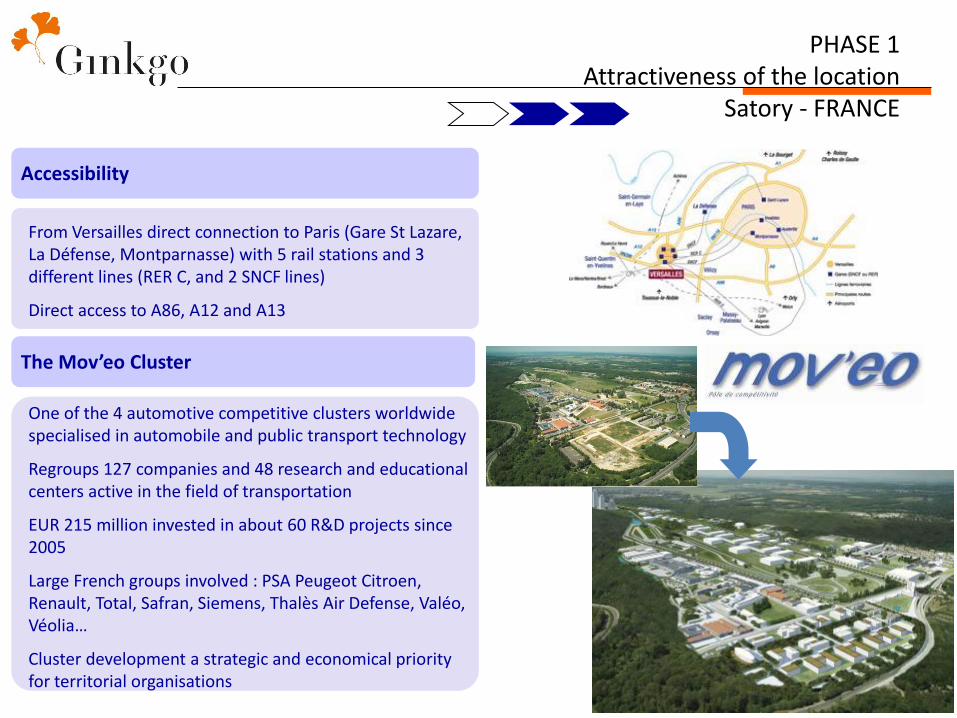

The Mov’eo Cluster

One of the 4 automotive competitive clusters worldwide specialised in automobile and public transport technology

Regroups 127 companies and 48 research and educational centers active in the field of transportation

EUR 215 million invested in about 60 R&D projects since 2005

Large French groups involved : PSA Peugeot Citroen, Renault, Total, Safran, Siemens, Thalès Air Defense, Valéo, Véolia…

Cluster development a strategic and economical priority for territorial organisations

Accessibility

From Versailles direct connection to Paris (Gare St Lazare, La Défense, Montparnasse) with 5 rail stations and 3 different lines (RER C, and 2 SNCF lines)

Direct access to A86, A12 and A13

PHASE 1 Attractiveness of the location

Satory - FRANCE

72

PHASE 1 Attractiveness of the location

Satory - FRANCE

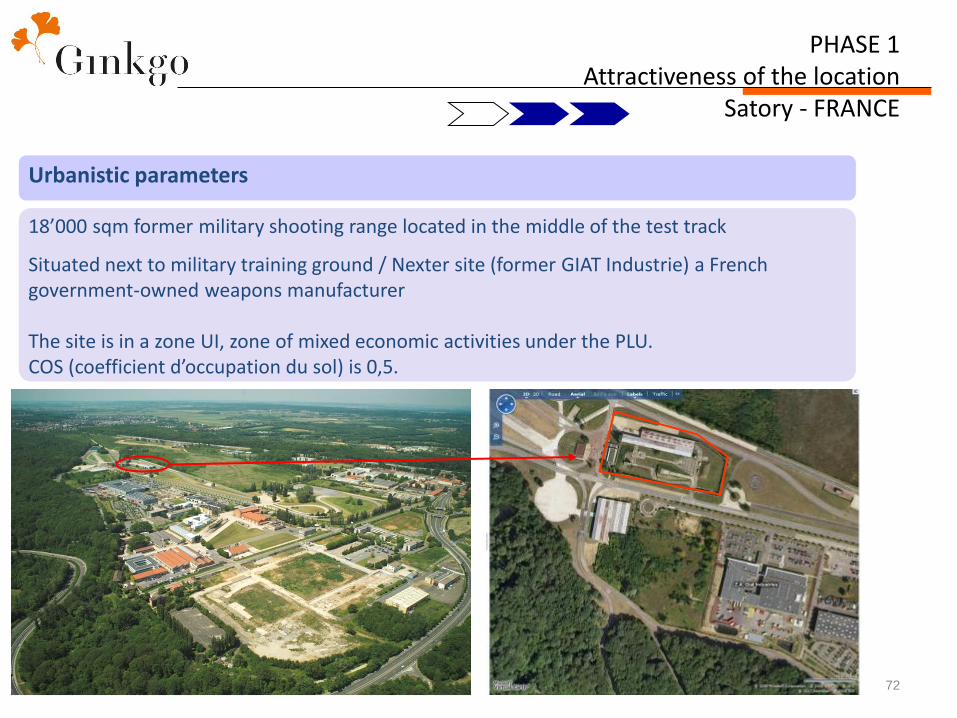

18’000 sqm former military shooting range located in the middle of the test track

Situated next to military training ground / Nexter site (former GIAT Industrie) a French government-owned weapons manufacturer The site is in a zone UI, zone of mixed economic activities under the PLU. COS (coefficient d’occupation du sol) is 0,5.

Urbanistic parameters

73

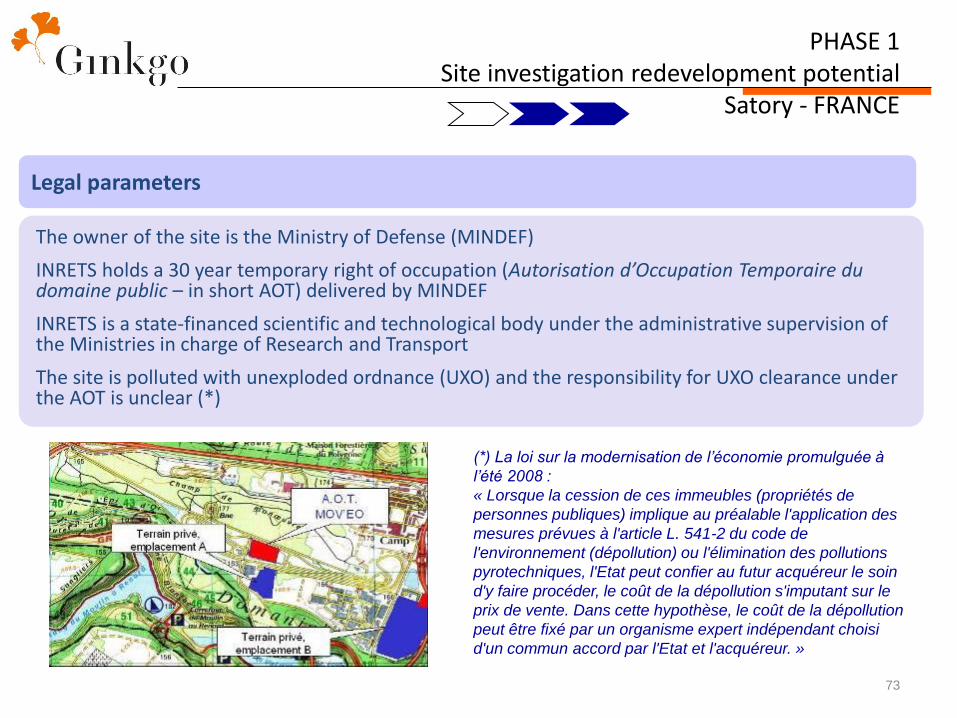

The owner of the site is the Ministry of Defense (MINDEF)

INRETS holds a 30 year temporary right of occupation (Autorisation d’Occupation Temporaire du domaine public – in short AOT) delivered by MINDEF

INRETS is a state-financed scientific and technological body under the administrative supervision of the Ministries in charge of Research and Transport

The site is polluted with unexploded ordnance (UXO) and the responsibility for UXO clearance under the AOT is unclear (*)

Legal parameters

PHASE 1 Site investigation redevelopment potential

Satory - FRANCE

(*) La loi sur la modernisation de l’économie promulguée à

l’été 2008 :

« Lorsque la cession de ces immeubles (propriétés de

personnes publiques) implique au préalable l'application des

mesures prévues à l'article L. 541-2 du code de

l'environnement (dépollution) ou l'élimination des pollutions

pyrotechniques, l'Etat peut confier au futur acquéreur le soin

d'y faire procéder, le coût de la dépollution s'imputant sur le

prix de vente. Dans cette hypothèse, le coût de la dépollution

peut être fixé par un organisme expert indépendant choisi

d'un commun accord par l'Etat et l'acquéreur. »

74

Acceleration of site clearance & development for the Mov’eoLab project (2011 deadline) – see real estate parameters Innovative financing solution through PPP approach Rapid implementation of the first elements of the Mov’eo cluster

Positionning as precursor and leader PPP brownfield redevelopment insuring French Public Sector visibility Identification of a strong financial counterparty

Redevelopment objectives of the parties

PHASE 1 Site investigation Redevelopment potential

Satory - FRANCE

The Ginkgo Fund

Mov’eo partners

French public sector representatives

75

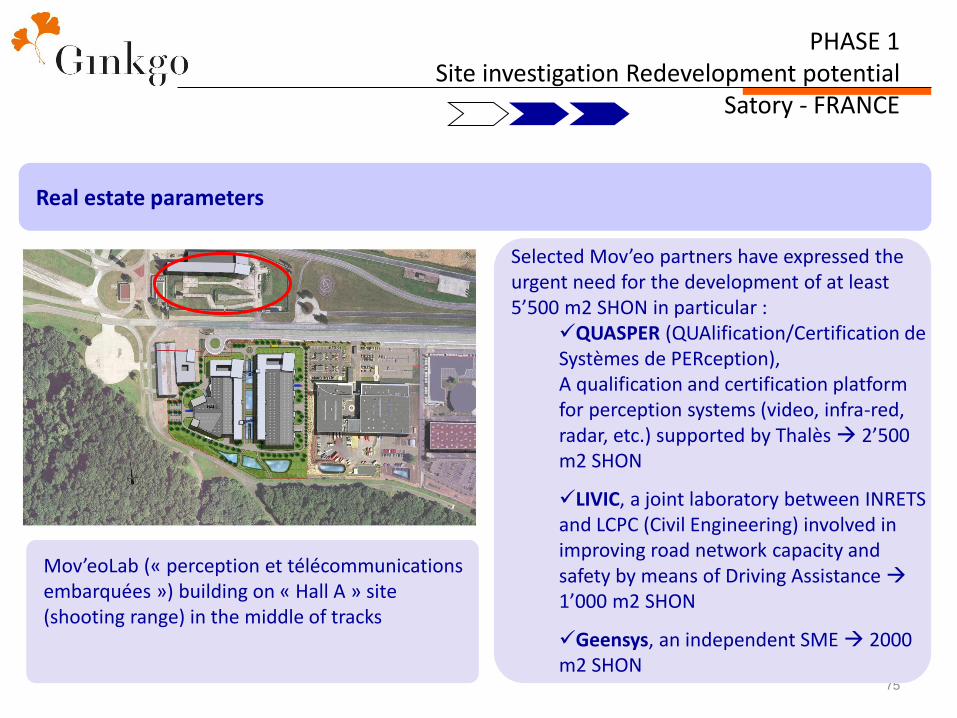

Selected Mov’eo partners have expressed the urgent need for the development of at least 5’500 m2 SHON in particular :

QUASPER (QUAlification/Certification de Systèmes de PERception), A qualification and certification platform for perception systems (video, infra-red, radar, etc.) supported by Thalès 2’500 m2 SHON

LIVIC, a joint laboratory between INRETS and LCPC (Civil Engineering) involved in improving road network capacity and safety by means of Driving Assistance 1’000 m2 SHON

Geensys, an independent SME 2000 m2 SHON

Real estate parameters

PHASE 1 Site investigation Redevelopment potential

Satory - FRANCE

Mov’eoLab (« perception et télécommunications embarquées ») building on « Hall A » site (shooting range) in the middle of tracks

76

Real estate parameters

PHASE 1 Site investigation Redevelopment potential

Satory - FRANCE

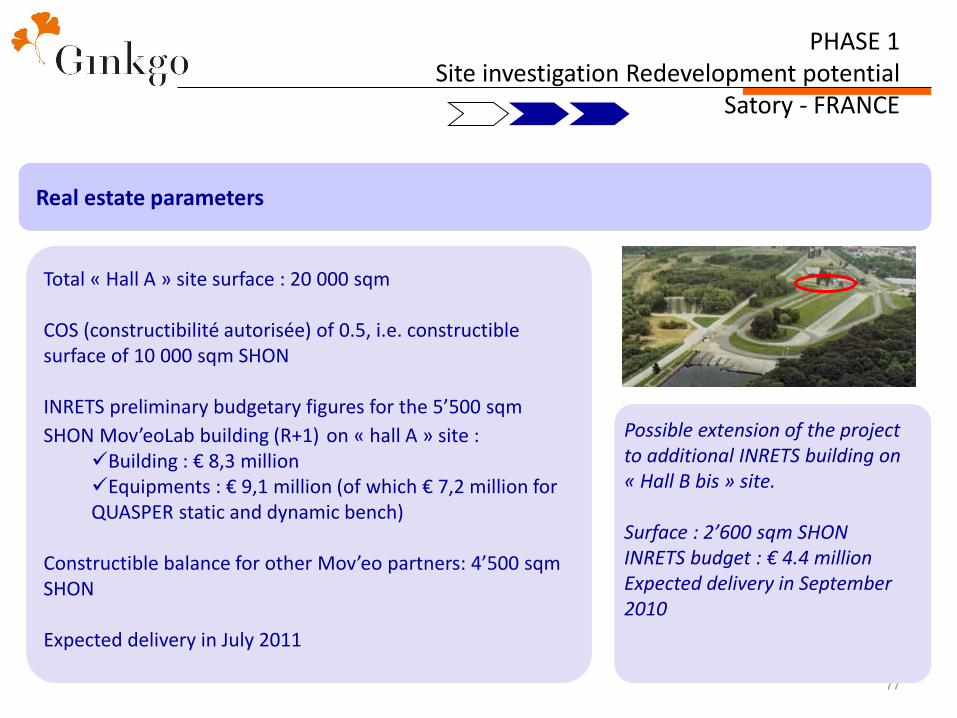

Other real estate projects on Satory site:

ESTACA and MOVEOTRONICS on SOGARIS land Construction of a second building next to new INRETS building (« Hall B ») for both INRETS and other MOVEO partners

77

Real estate parameters

PHASE 1 Site investigation Redevelopment potential

Satory - FRANCE

Total « Hall A » site surface : 20 000 sqm COS (constructibilité autorisée) of 0.5, i.e. constructible surface of 10 000 sqm SHON INRETS preliminary budgetary figures for the 5’500 sqm

SHON Mov’eoLab building (R+1) on « hall A » site : Building : € 8,3 million Equipments : € 9,1 million (of which € 7,2 million for QUASPER static and dynamic bench)

Constructible balance for other Mov’eo partners: 4’500 sqm SHON Expected delivery in July 2011

Possible extension of the project to additional INRETS building on « Hall B bis » site. Surface : 2’600 sqm SHON INRETS budget : € 4.4 million Expected delivery in September 2010

78

Environmental parameters

PHASE 1 Preliminary redevelopment scenarios

Satory - FRANCE

Unexploded ordnance (UXO) present in the subsoil – no depollution from the Army Historically a shooting range comprising sand pits for GIAT (middle to large caliber machine gun and Leclerc battle tanks and ammunition) There are currently no official study or assessment for the “hall A” site.

79

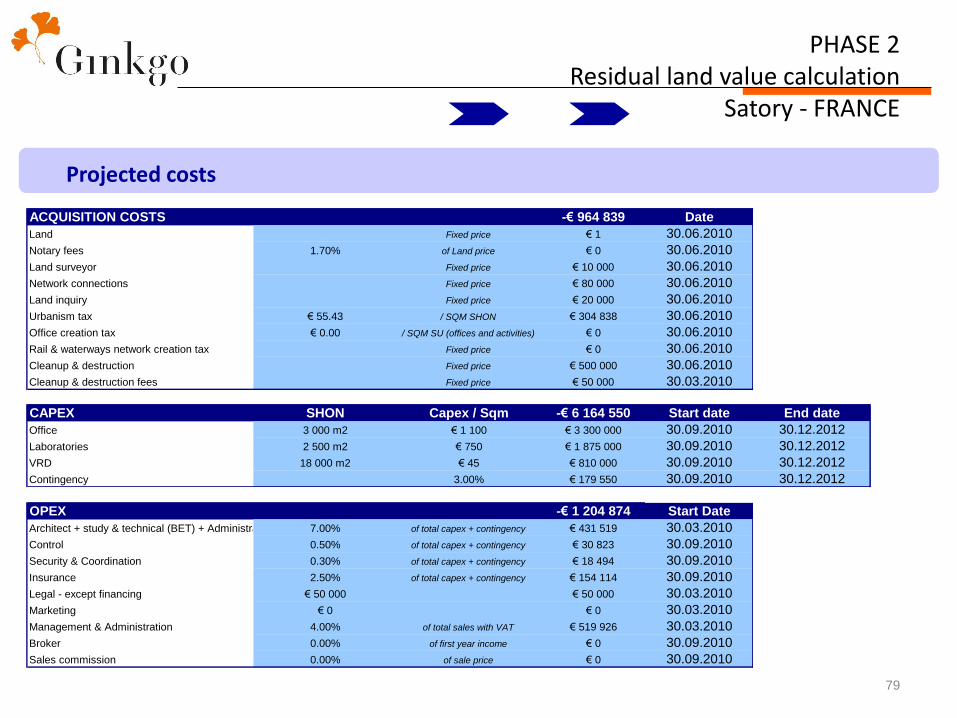

PHASE 2 Residual land value calculation

Satory - FRANCE

Projected costs

ACQUISITION COSTS -€ 964 839 Date

Land Fixed price € 1 30.06.2010

Notary fees 1.70% of Land price € 0 30.06.2010

Land surveyor Fixed price € 10 000 30.06.2010

Network connections Fixed price € 80 000 30.06.2010

Land inquiry Fixed price € 20 000 30.06.2010

Urbanism tax € 55.43 / SQM SHON € 304 838 30.06.2010

Office creation tax € 0.00 / SQM SU (offices and activities) € 0 30.06.2010

Rail & waterways network creation tax Fixed price € 0 30.06.2010

Cleanup & destruction Fixed price € 500 000 30.06.2010

Cleanup & destruction fees Fixed price € 50 000 30.03.2010

CAPEX SHON Capex / Sqm -€ 6 164 550 Start date End date

Office 3 000 m2 € 1 100 € 3 300 000 30.09.2010 30.12.2012

Laboratories 2 500 m2 € 750 € 1 875 000 30.09.2010 30.12.2012

VRD 18 000 m2 € 45 € 810 000 30.09.2010 30.12.2012

Contingency 3.00% € 179 550 30.09.2010 30.12.2012

OPEX -€ 1 204 874 Start Date

Architect + study & technical (BET) + Administration (MOEX) + acoustician7.00% of total capex + contingency € 431 519 30.03.2010

Control 0.50% of total capex + contingency € 30 823 30.09.2010

Security & Coordination 0.30% of total capex + contingency € 18 494 30.09.2010

Insurance 2.50% of total capex + contingency € 154 114 30.09.2010

Legal - except financing € 50 000 € 50 000 30.03.2010

Marketing € 0 € 0 30.03.2010

Management & Administration 4.00% of total sales with VAT € 519 926 30.03.2010

Broker 0.00% of first year income € 0 30.09.2010

Sales commission 0.00% of sale price € 0 30.09.2010

80

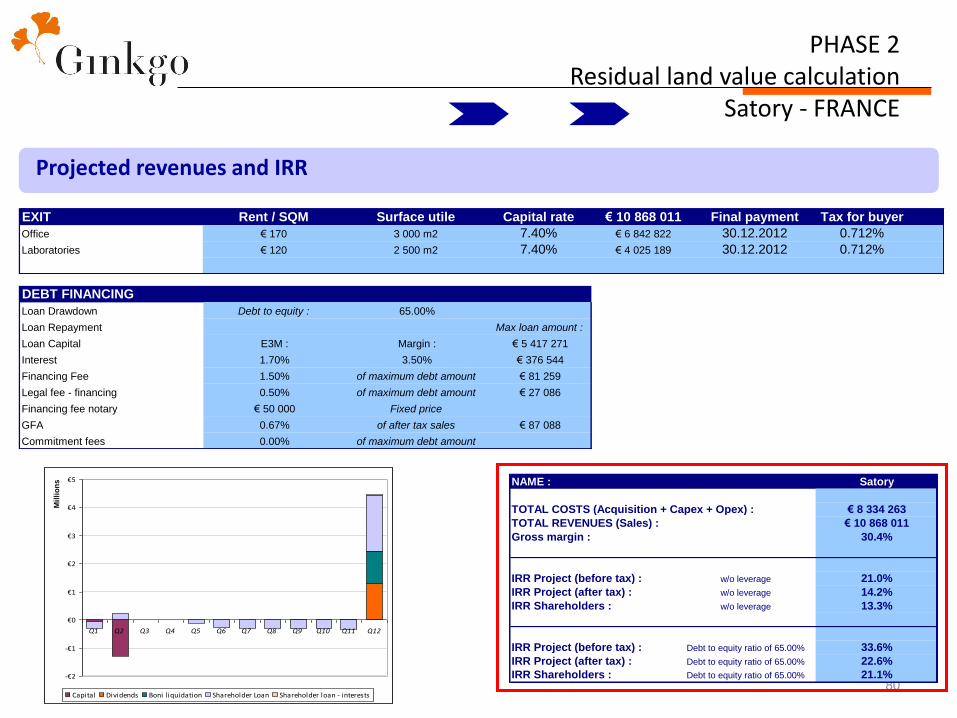

PHASE 2 Residual land value calculation

Satory - FRANCE

Projected revenues and IRR

EXIT Rent / SQM Surface utile Capital rate € 10 868 011 Final payment Tax for buyer

Office € 170 3 000 m2 7.40% € 6 842 822 30.12.2012 0.712%

Laboratories € 120 2 500 m2 7.40% € 4 025 189 30.12.2012 0.712%

DEBT FINANCING

Loan Drawdown Debt to equity : 65.00%

Loan Repayment Max loan amount :

Loan Capital E3M : Margin : € 5 417 271

Interest 1.70% 3.50% € 376 544

Financing Fee 1.50% of maximum debt amount € 81 259

Legal fee - financing 0.50% of maximum debt amount € 27 086

Financing fee notary € 50 000 Fixed price

GFA 0.67% of after tax sales € 87 088

Commitment fees 0.00% of maximum debt amount

NAME : Satory

TOTAL COSTS (Acquisition + Capex + Opex) : € 8 334 263

TOTAL REVENUES (Sales) : € 10 868 011

Gross margin : 30.4%

IRR Project (before tax) : w/o leverage 21.0%

IRR Project (after tax) : w/o leverage 14.2%

IRR Shareholders : w/o leverage 13.3%

IRR Project (before tax) : Debt to equity ratio of 65.00% 33.6%

IRR Project (after tax) : Debt to equity ratio of 65.00% 22.6%

IRR Shareholders : Debt to equity ratio of 65.00% 21.1%-€2

-€1

€0

€1

€2

€3

€4

€5

Q1 Q2 Q3 Q4 Q5 Q6 Q7 Q8 Q9 Q10 Q11 Q12

Mil

lio

ns

Capital Dividends Boni l iquidation Shareholder Loan Shareholder loan - interests

81

PHASE 2 Risk Mitigation

Satory - FRANCE

No existing study for unexploded ordnance (UXO)

Remote investigation by visual interpretation of available historical aerial photographs or combination of geophysical and survey methods with modern electromagnetic and magnetic detectors (magnetometer probes) providing digital mapping of UXO contamination

geotechnical data detection to better target subsequent excavations, reducing the cost of digging on every metallic contact and speeding the clearance process

Recent assessments of neighboring sites indicate approx. 25 UXO magnetic anomalies per 1’000 sqm between 0 and 1 meter preliminary UXO clearance budget can be estimated at 550 K€ Next step : exploratory UXO assessment and budget taking into account specific real estate project

Environmental risk

Existing study

Investment Advisor assessment

Mitigation

82

PHASE 2 Risk Mitigation

Satory - FRANCE

ATEMI assessment : PPP project only

Development/promotion risk

Development of MoveoLab facilities through long term contract with INRETS – see PPP structuration

Mitigation

Investment Advisor assessment

83

PHASE 2 Risk Mitigation

Satory - FRANCE

French government : Satory constitutes an « Opération d’intérêt national (OIN) » along with the development of the SACLAY plateau. Strong local support from Communauté d’Agglomération de Saint-Quentin-en Yvelines, Chambre de Commerce et d’Industrie (CCI) de Versailles, Conseil Général des Yvelines, Conseil Régional d’Ile-de-France, City of Versailles… But risk of a multiplicity of stakeholders

Political risk

Mitigation

Investment Advisor assessment

Step by step pragmatic approach Strategic partnership with Caisse des Dépôts – Direction territoriale Yvelines et Hauts-de-Seine

84

INRETS, holder of the temporary right of occupation (AOT) and acting as public contractor, launches a bid for the structuring, designing, financing, UXO clearance and building of the Mov’eoLab facility.

Note : The legislation imposes standards of freedom of access, equal treatment of candidates and procedural objectivity and requires a published request for proposals (RFP) but is less stringent/faster than the “contrat de partenariat”

Ginkgo, through a dedicated SPV bids for the contract and is awarded the bid INRETS transfers its AOT to the dedicated SPV The dedicated SPV which contracts banking debt (70% by assumption) finances and manages the UXO clearance and the design and construction of the building

The SPV transfers a « convention de mise à disposition » (CMD) of the building occupants (QUASPER, LISIC, Geentech) versus the payment of rent over a long period (e.g. 30 years) guaranteed by INRETS

PHASE 2 Preliminary legal and financial structuring

Satory - FRANCE

PPP preliminary structuring

85

Eligibility under the Fund’s strategy ? Yes No

Project diversification - Project size < 20% Fund’s total commitments - 5 MEUR < Project size > 30 MEUR - Number of invested projects < 12

X

Geographic Diversification - France and Belgium in priority - Total investment in one country < 60% Fund’s total commitments

X

Real estate project diversification - One type of asset < 65% Fund’s total commitments

X

Project Internal Return Rate > 20% X

ELIGIBILITY UNDER THE FUND’S STRATEGY Satory - FRANCE

86

NIVELLES (BELGIUM)

INVESTMENT APPRAISAL

PIPELINE

LEVEL 2 REJECTED PROJECT

87

OVERVIEW

Nivelles - BELGIUM

Type Industrial site located in an periurban area

Owner Industrial group (paper)

Location Nivelles (Wallonia), Belgium

Size 24 ha

Pollution Hydrocarbons, mineral oils, heavy metals and PCB’s

Sourcing BroCap

Status Bidding procedure abandonned

Project Mixed redevelopment

Industrial site located in Nivelles with proximity to future RER train station to Brussels.

88

PHASE 1 Attractiveness of the location

Nivelles - BELGIUM

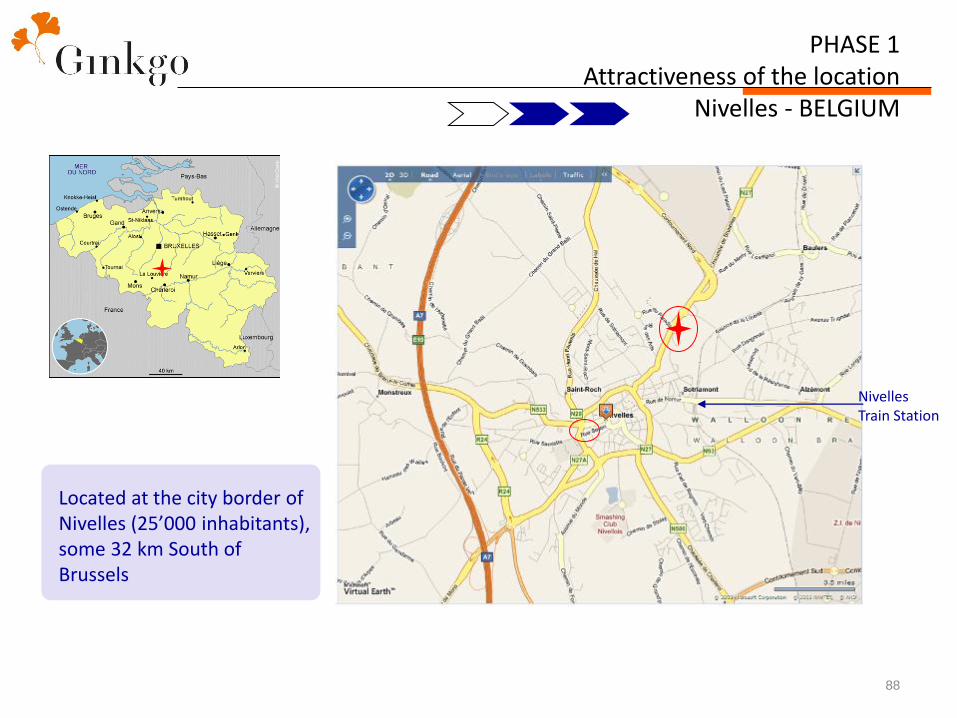

Located at the city border of Nivelles (25’000 inhabitants), some 32 km South of Brussels

Nivelles Train Station

89

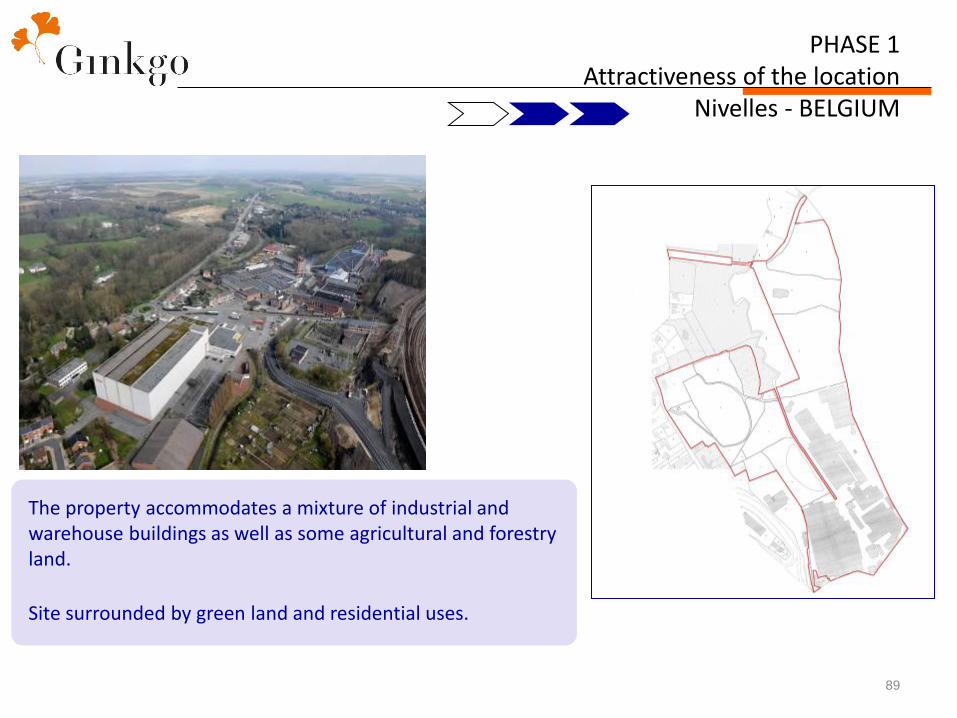

The property accommodates a mixture of industrial and warehouse buildings as well as some agricultural and forestry land.

Site surrounded by green land and residential uses.

PHASE 1 Attractiveness of the location

Nivelles - BELGIUM

90

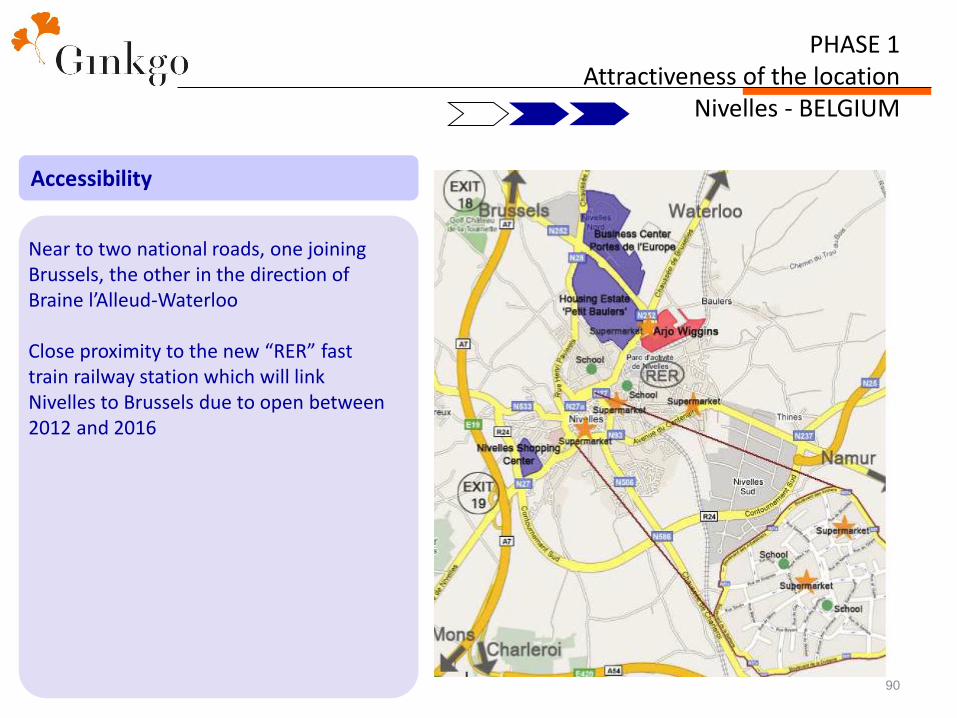

Near to two national roads, one joining Brussels, the other in the direction of Braine l’Alleud-Waterloo Close proximity to the new “RER” fast train railway station which will link Nivelles to Brussels due to open between 2012 and 2016

PHASE 1 Attractiveness of the location

Nivelles - BELGIUM

Accessibility

91

PHASE 1 Site investigation redevelopment potential

Nivelles - BELGIUM

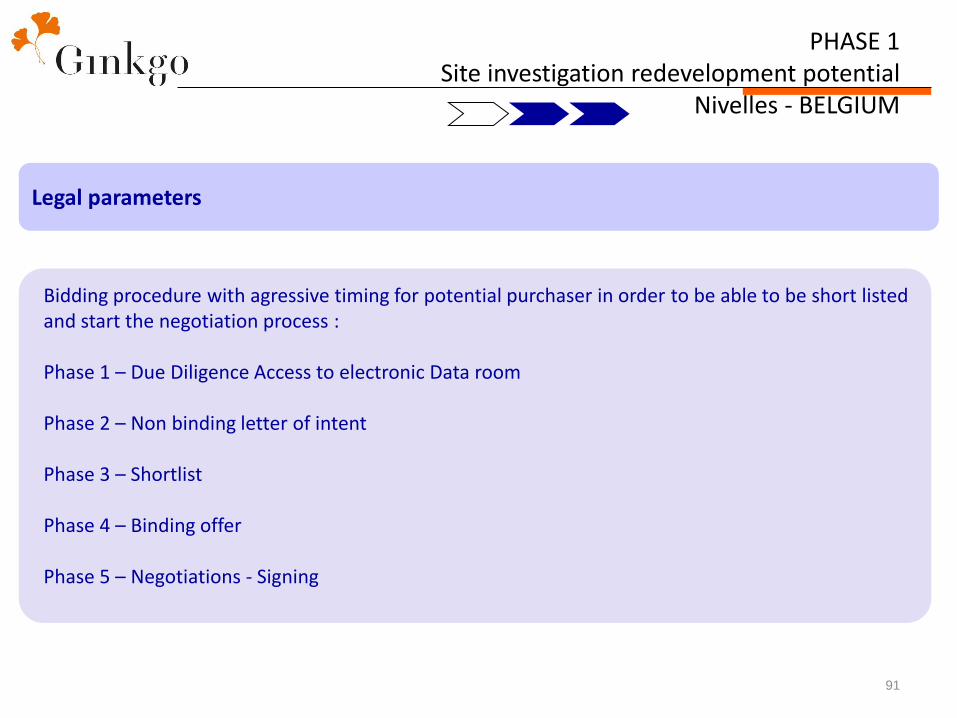

Bidding procedure with agressive timing for potential purchaser in order to be able to be short listed and start the negotiation process : Phase 1 – Due Diligence Access to electronic Data room Phase 2 – Non binding letter of intent Phase 3 – Shortlist Phase 4 – Binding offer Phase 5 – Negotiations - Signing

Legal parameters

92

Urbanistic parameters

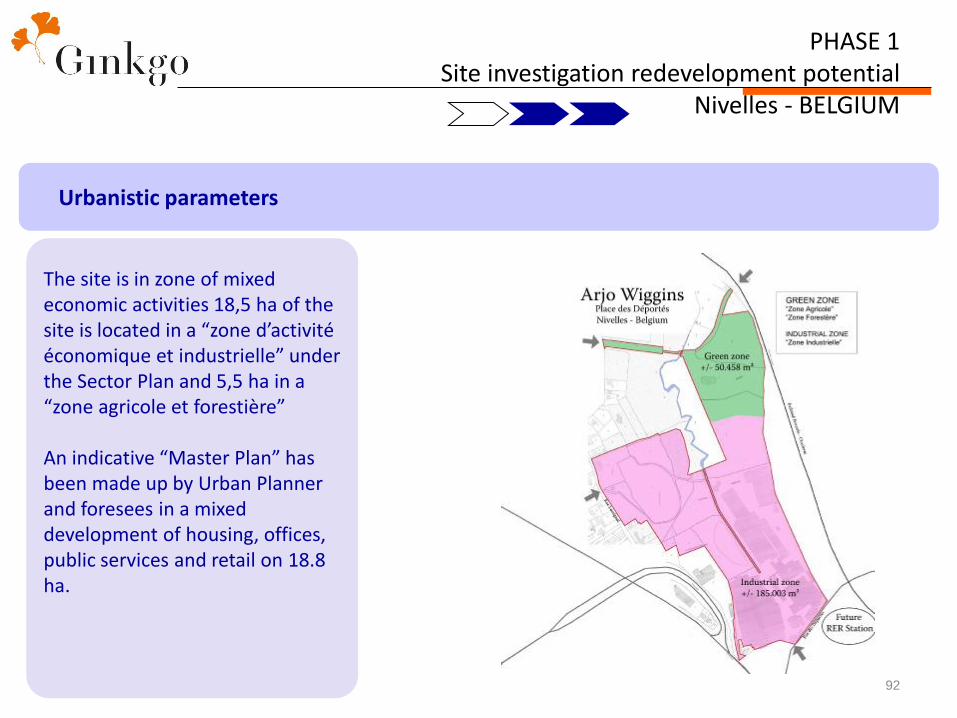

The site is in zone of mixed economic activities 18,5 ha of the site is located in a “zone d’activité économique et industrielle” under the Sector Plan and 5,5 ha in a “zone agricole et forestière” An indicative “Master Plan” has been made up by Urban Planner and foresees in a mixed development of housing, offices, public services and retail on 18.8 ha.

PHASE 1 Site investigation redevelopment potential

Nivelles - BELGIUM

93

Maximise the short term benefits - upfront cash for the sale of the land - at the expense of the long term risks (has indicated its willingness to shoulder a significant amount of environmental risk) Encouraged by its real estate advisor King Sturge (probably paid based on the sale price that has a large access to traditional real estate developers and promoters and little understanding of remediation issues). Large scale site allowing a mixed redevelopment project not too far from Brussels Potentially attractive location for housing and residencies due to the planned nearby RER station with direct access to the centre of Brussels Important environmental liability that is partly or entirely retained by the current owner; if not, a significant reduction in the acquisition price can be negotiated Support of the city of Nivelles for the preliminary draft masterplan and interest for public engagements (school, library)

Redevelopment objectives of the parties

PHASE 1 Site investigation Redevelopment potential

Nivelles - BELGIUM

The Ginkgo Fund

Owner

94

Probable unsufficient polarity to enable the development of 160 000 m2 (Master Plan). The site redevelopment in 1’400 new residential houses, compared with a population of 25 000 people, is to ambitious restrict project density Reasonable accessibility near to two national roads. Access to ringroad easy but not immediate. Train station at 1km/10minutes walking distance. Nivelles City center at 2km/20 walking distance Not quite the city advantages nor the bucolic surrounding Limited potential for commercial development : the N27 national road axis in the direction of Waterloo-Brussels is underdevelopped but commercial units need to be located on the axis itself.

Real estate parameters

PHASE 1 Site investigation Redevelopment potential

Nivelles - BELGIUM

Spatial density

Accessibility

Attractiveness of the trade area

95

A recent business park exists at 400m « Portes de l'Europe » and is nearly vacant. Numerous recent residential developments near the site are under way, e.g. a 800 residential unit project– of which 150 units are authorised already - at 400m of the site (over a 15- to 20-year period).

Constructible land is available nearby around station.

Real estate parameters

PHASE 1 Site investigation Redevelopment potential

Nivelles - BELGIUM

State of the local real estate market

96

Environmental parameters

PHASE 1 Preliminary redevelopment scenarios

Nivelles - BELGIUM

Various soil & groundwater investigation have been carried out in 2006, 2007 and 2008 by URS (industrial area – built zone) and TAUW (industrial area – green land) on behalf of the owner. A succession of uncoordinated technical reports states the presence of hydrocarbons, mineral oils, heavy metals and PCB’s in the soil and groundwater. The URS document Evaluation des coûts d’assainissement indicates a remediation budget range between €0,9 million (pumping, treatment and containment of decantation muds) and €13,4 million (total excavation and treatment) TAUW concludes that the soil and groundwater quality at the green land does not require any further investigation. Owner estimates of remediation cost comprised between 185 K€ and 4,350 K€

97

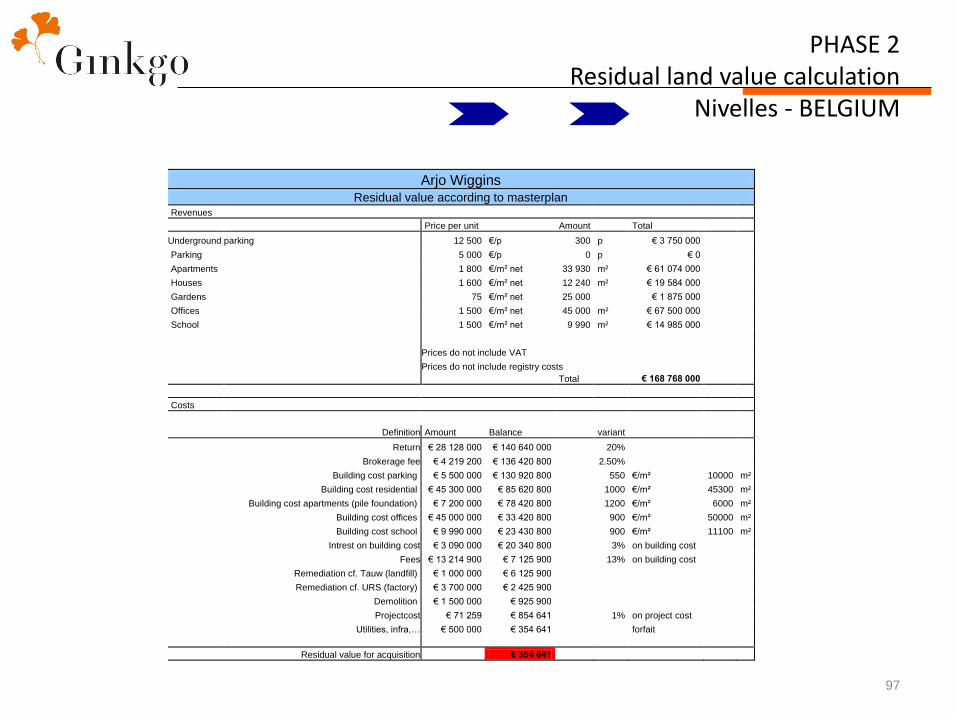

Arjo Wiggins Residual value according to masterplan

Revenues

Price per unit Amount Total

Underground parking 12 500 €/p 300 p € 3 750 000

Parking 5 000 €/p 0 p € 0

Apartments 1 800 €/m² net 33 930 m² € 61 074 000

Houses 1 600 €/m² net 12 240 m² € 19 584 000

Gardens 75 €/m² net 25 000 € 1 875 000

Offices 1 500 €/m² net 45 000 m² € 67 500 000

School 1 500 €/m² net 9 990 m² € 14 985 000

Prices do not include VAT

Prices do not include registry costs

Total € 168 768 000

Costs

Definition Amount Balance variant

Return € 28 128 000 € 140 640 000 20%

Brokerage fee € 4 219 200 € 136 420 800 2.50%

Building cost parking € 5 500 000 € 130 920 800 550 €/m² 10000 m²

Building cost residential € 45 300 000 € 85 620 800 1000 €/m² 45300 m²

Building cost apartments (pile foundation) € 7 200 000 € 78 420 800 1200 €/m² 6000 m²

Building cost offices € 45 000 000 € 33 420 800 900 €/m² 50000 m²

Building cost school € 9 990 000 € 23 430 800 900 €/m² 11100 m²

Intrest on building cost € 3 090 000 € 20 340 800 3% on building cost

Fees € 13 214 900 € 7 125 900 13% on building cost

Remediation cf. Tauw (landfill) € 1 000 000 € 6 125 900

Remediation cf. URS (factory) € 3 700 000 € 2 425 900

Demolition € 1 500 000 € 925 900

Projectcost € 71 259 € 854 641 1% on project cost

Utilities, infra,… € 500 000 € 354 641 forfait

Residual value for acquisition € 354 641

PHASE 2 Residual land value calculation

Nivelles - BELGIUM

98

PHASE 2 Risk Mitigation

Nivelles - BELGIUM

Identifies soil and groundwater contamination with polycyclic aromatic hydrocarbons, heavy mineral oils, benzene and PCB’s. Estimated remediation & demolition budget is unconclusive, anywhere between € 2.5 and € 15 million

URS and TAUW data and approach largely incomplete (nature of contaminants on site, the pollution under the buildings and geotechnic data ) and risk model largely theoretical/black box (Crap In Crap Out) Additionnal worries include pollution spilling from the green area (TAUW) zone to neigboring zones and an unknown degree of contamination below 10m (unsufficient soil boring).

Environmental risk

Existing study

Investment Advisor assessment

Remediation budget is currently unknown and needs to take into account the projected real estate project and requires much more exhaustive soil and groundwater data and studies

Investment Advisor remedial costs rough estimates are: € 3 million for the built zone and €4-5 million for green land : NO IDENTIFIED ENVIRONMENTAL MITIGATION APPROACH DEAL REJECTED

Mitigation

99

PHASE 2 Risk Mitigation

Nivelles - BELGIUM

Given the state of the local real estate market (other developments under completion nearby, vacant offices, …) and even taking into account a lower density project, development risk appears important in the short-mid term.

Development/promotion risk

NO IDENTIFIED REAL ESTATE MITIGATION APPROACH DEAL REJECTED

Mitigation

Investment Advisor assessment

100

PHASE 3 Due diligence

Nivelles - BELGIUM

74 documents have been consulted in the electronic data room : general, environmental, legal, real estate.

Supporting documents

101

PHASE 3 Financial and legal structuring

Nivelles - BELGIUM

Original non-binding offer submitted

Modification of the scope of the transaction including the sale of an additional warehouse bordering the site

No modified non-binding offer submited

Short-listed as potential purchaser with approval to contact authorities and urban planner

Ginkgo declined to submit binding offer for year-end deadline

Because of environmental uncertainties, bidding procedure still pending today

Walloon government decided to order an additional environmental study from SARSI (société d'assainissement et de rénovation des sites indutriels) Willingness from the Region to invest in the remediation but only if potential benefits, i.e. PPP approach

Deal summary

102

Nous n’héritons pas de la terre de nos ancêtres, nous l’empruntons à nos enfants

Antoine de Saint Exupéry