gen ledger accounts.doc

TRANSCRIPT

8/14/2019 gen ledger accounts.doc

http://slidepdf.com/reader/full/gen-ledger-accountsdoc 1/15

General Ledger Accounts

Each different type of asset, liability, revenue, expense and owner’s equity of a business arerecorded into separate ledger accounts which show the balances and any changes in eachaccount. The general ledger contains all accounts, including control accounts, other than forindividual Accounts Receivable (debtors and Accounts !ayable (creditors which are

contained in the subsidiary ledgers. These accounts for" a detailed picture of the overallfinancial position of the business.

The ledger accounts i"ple"ent the rules of double entry# debits $ credits. Accordingly, forevery debit entry there "ust be a credit entry for the sa"e value and vice versa. The rules area very i"portant point of understanding the accounting process and need to be fullyunderstood to allow correct processing, posting and entry of individual transactions or totalsfro" %ournals. &t is also necessary to have the 'nowledge of the nature of the different accountgroups and the effect of debit and credit entries on these accounts. This can be su""arisedby the diagra" below

Increases

All %ournals are posted (totalled and the balances of each column transferred) to the generalledger. !osting the %ournal totals to the ledgers re"oves any unnecessary detail fro" theledgers. &n effect the general ledger is a su""ary of the transactions for the business, with the

Page 1 of 15

DEBIT entry (DR) CREDIT entry (CR)AccountNature

AET

LIABILITIE

OWNERS EQUITY

RE!EN"E

E#PENE

Increases Decreases

Increases

Increases

Increases

Increases

Decreases

Decreases

Decreases

Decreases

8/14/2019 gen ledger accounts.doc

http://slidepdf.com/reader/full/gen-ledger-accountsdoc 2/15

detail being previously recorded in the %ournals. Any changes to account balances arecalculated with the "ini"u" nu"ber of entries as a result of this.

Post$ng t%e &ournals to t%e ledgers

!osting to the %ournals can be done in any order as posting occurs on the one sa"e day,

usually at the end of the "onth. )o"e posting orders "ay give rise to te"porarily artificialresults, such as having a credit balance in the debtor’s control account if the cash receipts %ournal is posted first. *nce posting has been co"pleted the correct account balances willbeco"e apparent. A suggested order in which to post the %ournals is

+. general %ournal opening entry

. purchases %ournal

-. purchases returns %ournal

. sales %ournal

/. sales returns %ournal0. cash receipts %ournal

1. cash pay"ents %ournal

2. general %ournal (all the other entries.

General 'ost$ng 'rocedures

• The totals of the %ournals are posted to the relevant ledger accounts at the end of eachperiod, usually every "onth.

• Every colu"n in the %ournals should have a corresponding account in the general ledger towhich the total of the colu"n is posted.

• )ince totals of colu"ns are posted, the last date in the %ournal is used as the date of entryin the ledger accounts.

• The rules of the ledger will deter"ine which accounts are debited or credited.

• As you are using the principles of double entry accounting, the debit entries "ust equal thecredit entries.

• *nly once the %ournal is closed (around the end of the "onth are ledgers posted.

• Each sundry value is not totalled, but instead posted to the account to which it iscategorised. They will then carry the date of the transaction and not be dated the day they

are posted (end of "onth.

Page of 15

8/14/2019 gen ledger accounts.doc

http://slidepdf.com/reader/full/gen-ledger-accountsdoc 3/15

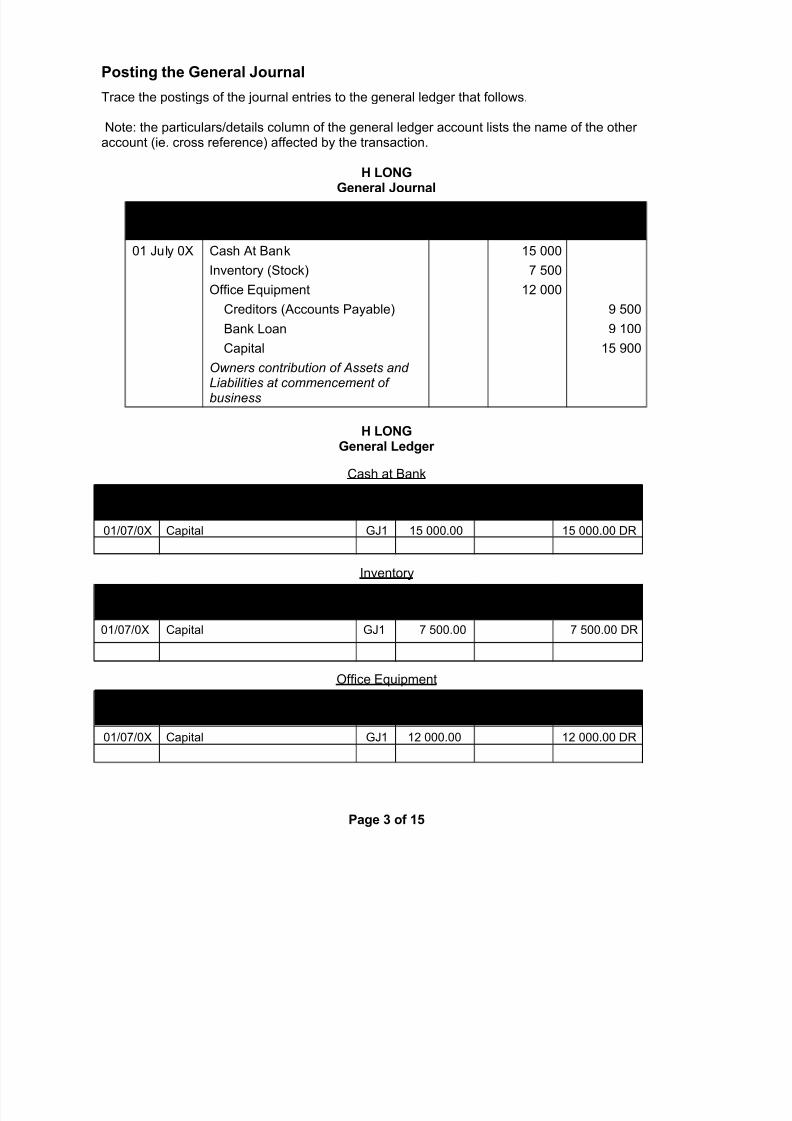

Post$ng t%e General ournal

Trace the postings of the %ournal entries to the general ledger that follows.

3ote the particulars4details colu"n of the general ledger account lists the na"e of the otheraccount (ie. cross reference affected by the transaction.

* L+NGGeneral ournal

DATE PARTIC"LAR ,+LI+ DEBIT

-

CREDIT

-

5+ 6uly 57 8ash At 9an'

&nventory ()toc'

*ffice Equip"ent

8reditors (Accounts !ayable

9an' :oan 8apital

Owners contribution of Assets andLiabilities at commencement ofbusiness

+/ 555

1 /55

+ 555

; /55

; +55+/ ;55

* L+NGGeneral Ledger

8ash at 9an'

DATE PARTIC"LAR NLRE, DEBIT-

CREDIT-

BALANCE-

5+451457 8apital <6+ +/ 555.55 +/ 555.55 =R

&nventory

DATE PARTIC"LAR NLRE,

DEBIT

-

CREDIT

-

BALANCE

-

5+451457 8apital <6+ 1 /55.55 1 /55.55 =R

*ffice Equip"ent

DATE PARTIC"LAR NLRE,

DEBIT

-

CREDIT

-

BALANCE

-

5+451457 8apital <6+ + 555.55 + 555.55 =R

Page . of 15

8/14/2019 gen ledger accounts.doc

http://slidepdf.com/reader/full/gen-ledger-accountsdoc 4/15

8reditors (Accounts !ayable

DATE PARTIC"LAR NLRE,

DEBIT

-

CREDIT

-

BALANCE

-

5+451457 8apital <6+ ; /55.55 ; /55.55 8R

9an' :oan

DATE PARTIC"LAR NLRE,

DEBIT

-

CREDIT

-

BALANCE

-

5+451457 8apital <6+ ; +55.55 ; +55.55 8R

8apital

DATE PARTIC"LAR NLRE,

DEBIT

-

CREDIT

-

BALANCE

-

5+451457 >arious Assets ? :iabilities <6+ +/ ;55.55 +/ ;55.55 8R

Note/

• general %ournals are posted directly to the accounts affected by each entry @ as

instructed by the general %ournalB.

• Total debit (=R entries (C- /55.55 are e0ual to total credit (8R entries

• (C- /55.55.

• All entries in the general ledger "ust be traceable to a %ournal, so %ournal and page

references are recorded in the %ournal reference colu"n. <6+ refers to page + of the

general %ournal.

• The date recorded in the general %ournal is the date that the entry is to be "ade in

the general ledger.

Page of 15

8/14/2019 gen ledger accounts.doc

http://slidepdf.com/reader/full/gen-ledger-accountsdoc 5/15

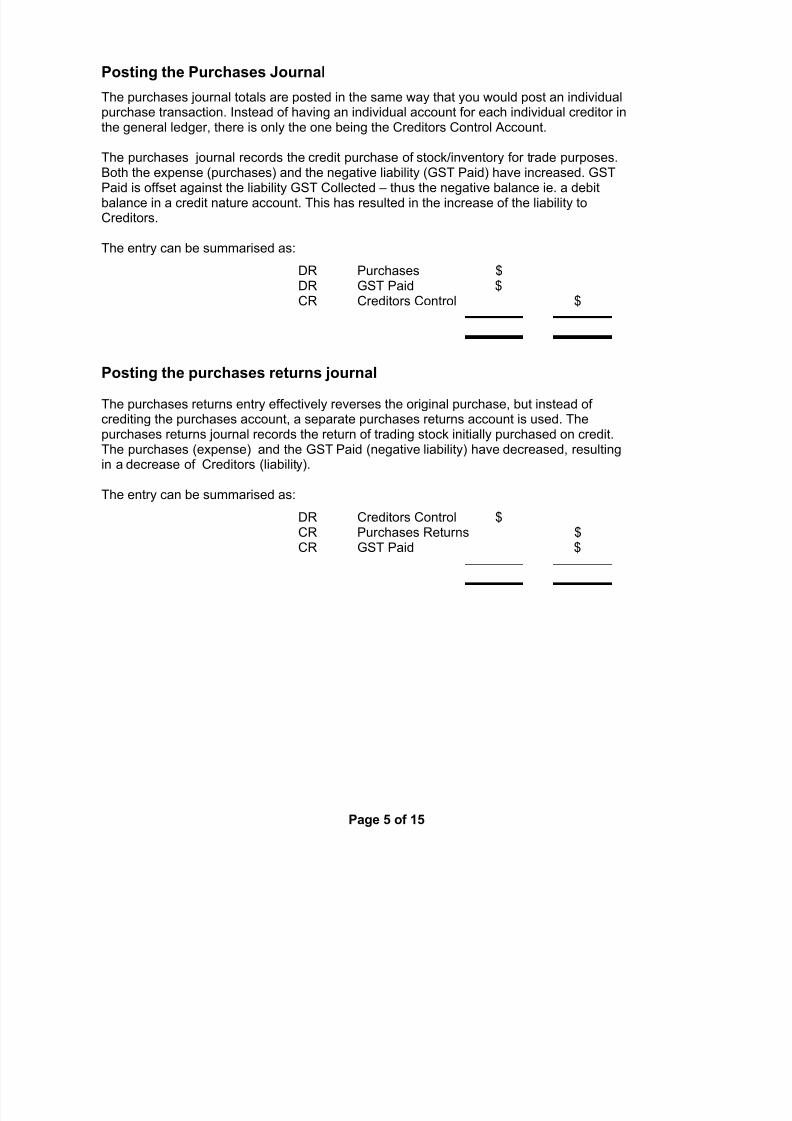

Post$ng t%e Purc%ases ournal

The purchases %ournal totals are posted in the sa"e way that you would post an individualpurchase transaction. &nstead of having an individual account for each individual creditor inthe general ledger, there is only the one being the 8reditors 8ontrol Account.

The purchases %ournal records the credit purchase of stoc'4inventory for trade purposes.9oth the expense (purchases and the negative liability (<)T !aid have increased. <)T!aid is offset against the liability <)T 8ollected @ thus the negative balance ie. a debitbalance in a credit nature account. This has resulted in the increase of the liability to8reditors.

The entry can be su""arised as

=R !urchases C=R <)T !aid C8R 8reditors 8ontrol C

Post$ng t%e 'urc%ases returns &ournal

The purchases returns entry effectively reverses the original purchase, but instead ofcrediting the purchases account, a separate purchases returns account is used. Thepurchases returns %ournal records the return of trading stoc' initially purchased on credit.The purchases (expense and the <)T !aid (negative liability have decreased, resultingin a decrease of 8reditors (liability.

The entry can be su""arised as=R 8reditors 8ontrol C8R !urchases Returns C8R <)T !aid C

Page 5 of 15

8/14/2019 gen ledger accounts.doc

http://slidepdf.com/reader/full/gen-ledger-accountsdoc 6/15

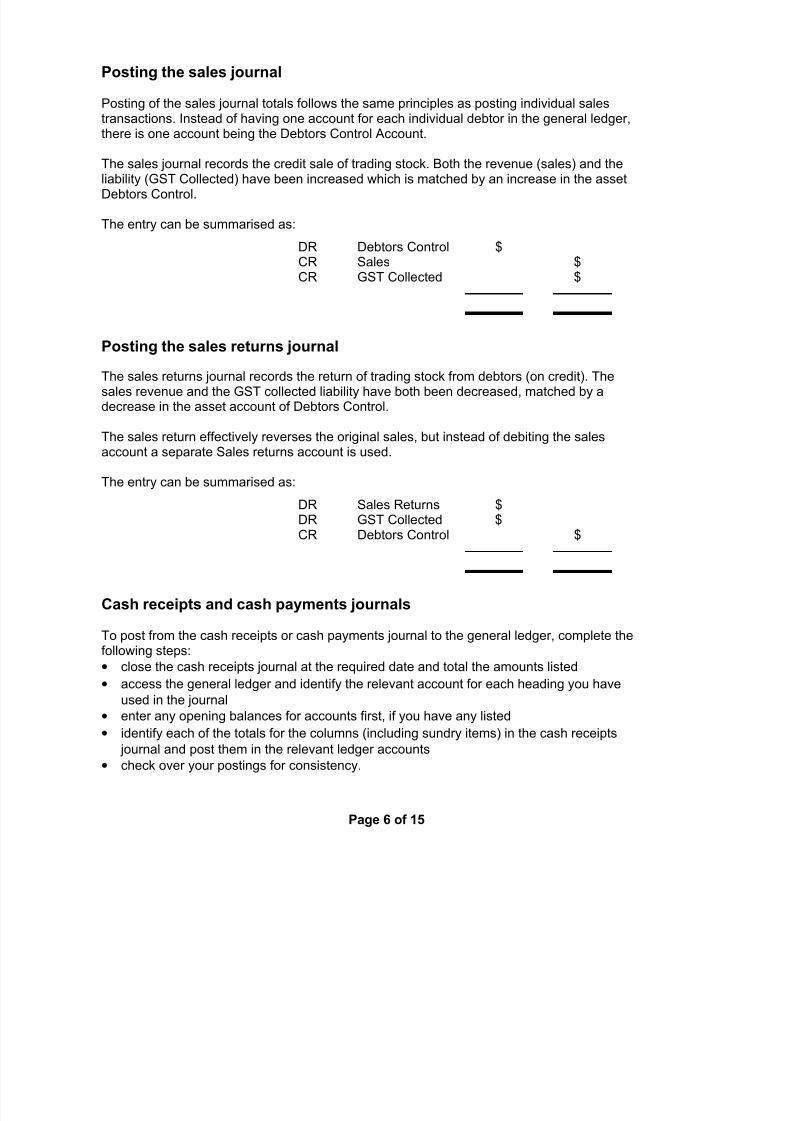

Post$ng t%e sales &ournal

!osting of the sales %ournal totals follows the sa"e principles as posting individual salestransactions. &nstead of having one account for each individual debtor in the general ledger,there is one account being the =ebtors 8ontrol Account.

The sales %ournal records the credit sale of trading stoc'. 9oth the revenue (sales and theliability (<)T 8ollected have been increased which is "atched by an increase in the asset=ebtors 8ontrol.

The entry can be su""arised as

=R =ebtors 8ontrol C8R )ales C8R <)T 8ollected C

Post$ng t%e sales returns &ournal

The sales returns %ournal records the return of trading stoc' fro" debtors (on credit. Thesales revenue and the <)T collected liability have both been decreased, "atched by adecrease in the asset account of =ebtors 8ontrol.

The sales return effectively reverses the original sales, but instead of debiting the salesaccount a separate )ales returns account is used.

The entry can be su""arised as

=R )ales Returns C=R <)T 8ollected C8R =ebtors 8ontrol C

Cas% rece$'ts and cas% 'ay2ents &ournals

To post fro" the cash receipts or cash pay"ents %ournal to the general ledger, co"plete thefollowing steps

• close the cash receipts %ournal at the required date and total the a"ounts listed• access the general ledger and identify the relevant account for each heading you have

used in the %ournal

• enter any opening balances for accounts first, if you have any listed

• identify each of the totals for the colu"ns (including sundry ite"s in the cash receipts %ournal and post the" in the relevant ledger accounts

• chec' over your postings for consistency.

Page 3 of 15

8/14/2019 gen ledger accounts.doc

http://slidepdf.com/reader/full/gen-ledger-accountsdoc 7/15

Gu$del$nes/• The corresponding entry is written in the !articulars colu"n.

• The cash receipts %ournal is crossDreferenced when posted. This is valuable where furtherinfor"ation is required fro" the cash receipts %ournal.

• =iscount expense "ay be offered to custo"ers4clients who pay their debt pro"ptly. Thispay"ent is ad%usted in the discount expense ledger and the credit is "ar'ed in the debtors

control ledger (it is not calculated in the grand total of all the other entries. This ensuresthat the debtors a"ount is reduced and recorded appropriately.

!osting to the 8ash Receipts 6ournal can be su""arised as

=R 8ash at 9an' C8R =ebtors 8ontrol C8R )ales C8R <)T 8ollected C8R )undry Accounts C

A3= A:)*, For discount expense, involving <)T

=R =iscount Expense C=R <)T 8ollected C8R =ebtors 8ontrol C

E#A4PLECas% Rece$'ts ournal

DATE PARTIC"LAR RECNo

DICE#P

DEBT+R CA*ALE

GT

-

"NDR6-

BAN7 -

+.-.57 )ales 8RR 55.55 5.55 5.55

/.-.57 )ales 8RR 055.55 05.55 005.55

;.-.5x 8o""ission +; .15 1.-5 /5.55

+.-.57 :. EdwardsDdebtor +;/ /.55 -;/.55

)ales 8RR 0/.55 0./5 + 52./5

+;.-.57 ). Gac'eyDdebtor +;0 1./5 ./5 ./5

.-.57 &nterest revenue +;1 1/.55

)ales 8RR 155.55 15.55 2/.55

2.-.57 6. !ope +;2 ./5 +1/.55 +1/.55

1588 1 8158 .588 558 .8.8 . 9:588

Page ; of 15

8/14/2019 gen ledger accounts.doc

http://slidepdf.com/reader/full/gen-ledger-accountsdoc 8/15

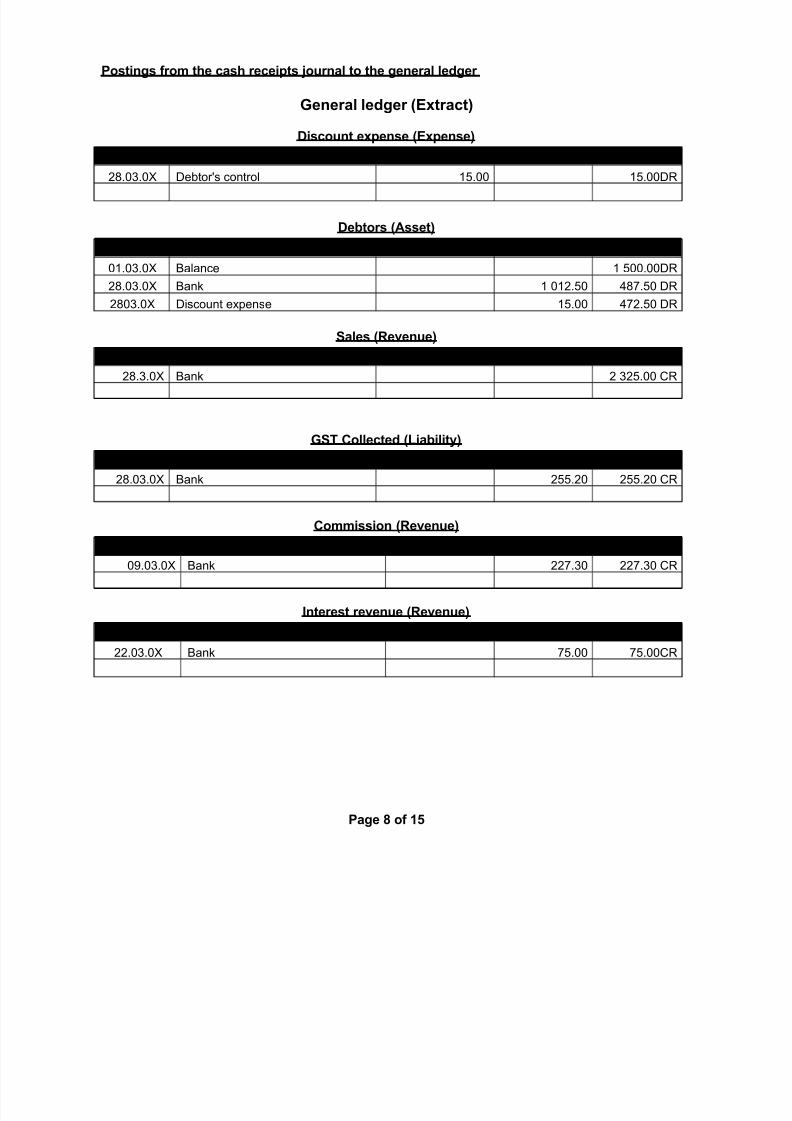

Post$ngs fro2 t%e cas% rece$'ts &ournal to t%e general ledger

General ledger (E<tract)

D$scount e<'ense (E<'ense)

DATE PARTIC"LAR DEBIT CREDIT BALANCE

2.5-.57 =ebtors control +/.55 +/.55=R

De=tors (Asset)

DATE PARTIC"LAR DEBIT CREDIT BALANCE

5+.5-.57 9alance + /55.55=R

2.5-.57 9an' + 5+./5 21./5 =R

25-.57 =iscount expense +/.55 1./5 =R

ales (Re>enue)

DATE PARTIC"LAR DEBIT CREDIT BALANCE

2.-.57 9an' -/.55 8R

GT Collected (L$a=$l$ty)

DATE PARTIC"LAR DEBIT CREDIT BALANCE

2.5-.57 9an' //.5 //.5 8R

Co22$ss$on (Re>enue)

DATE PARTIC"LAR DEBIT CREDIT BALANCE

5;.5-.57 9an' 1.-5 1.-5 8R

Interest re>enue (Re>enue)

DATE PARTIC"LAR DEBIT CREDIT BALANCE

.5-.57 9an' 1/.55 1/.558R

Page 9 of 15

8/14/2019 gen ledger accounts.doc

http://slidepdf.com/reader/full/gen-ledger-accountsdoc 9/15

Ban? (Asset)

DATE PARTIC"LAR DEBIT CREDIT BALANCE

2.5-.57 8ash receipts -2;/.55 - 2;/.55=R

ACTI!IT6

Post the entries in the cash receipts journal below to the relevant ledger accounts below.

Cas% Rece$'ts ournal

DATE PARTIC"LAR RECNo DICE#P

DEBT+R-

ALE

-

GT

-

"NDR6

-

BAN7

-

557

5+45/ )ales 8RR + 055.55 +05.55 + 105.55

5/45/ )ales 8RR 55.55 5.55 05.55

5;45/5 8o""ission +; + 555.55 + 555.55

+45/ H. RichardsDdebtor

+;/ 5.55 + /25.55

)ales 8RR /55.55 /5.55 --5.55

+;45/ 9. 6oelDdebtor +;0 -5.55 + 115.55 + 115.55

45/ &nterest revenue +;1 -55.55

)ales 8RR 255.55 25.55 - -25.55

245/ F. Avalon +;2 +5.55 155.55 155.55

Totals 3888 85888 : .8888 :.888 1 .8888 15 59888

General ledger (E<tract)

D$scount e<'ense (E<'ense)

DATE PARTIC"LAR DEBIT CREDIT BALANCE

De=tors (Asset)DATE PARTIC"LAR DEBIT CREDIT BALANCE

Page : of 15

8/14/2019 gen ledger accounts.doc

http://slidepdf.com/reader/full/gen-ledger-accountsdoc 10/15

ales (Re>enue)

DATE PARTIC"LAR DEBIT CREDIT BALANCE

GT Collected (L$a=$l$ty)

DATE PARTIC"LAR DEBIT CREDIT BALANCE

Co22$ss$on (Re>enue)

DATE PARTIC"LAR DEBIT CREDIT BALANCE

Interest re>enue (Re>enue)

DATE PARTIC"LAR DEBIT CREDIT BALANCE

Ban? (Asset)

DATE PARTIC"LAR DEBIT CREDIT BALANCE

Page 18 of 15

8/14/2019 gen ledger accounts.doc

http://slidepdf.com/reader/full/gen-ledger-accountsdoc 11/15

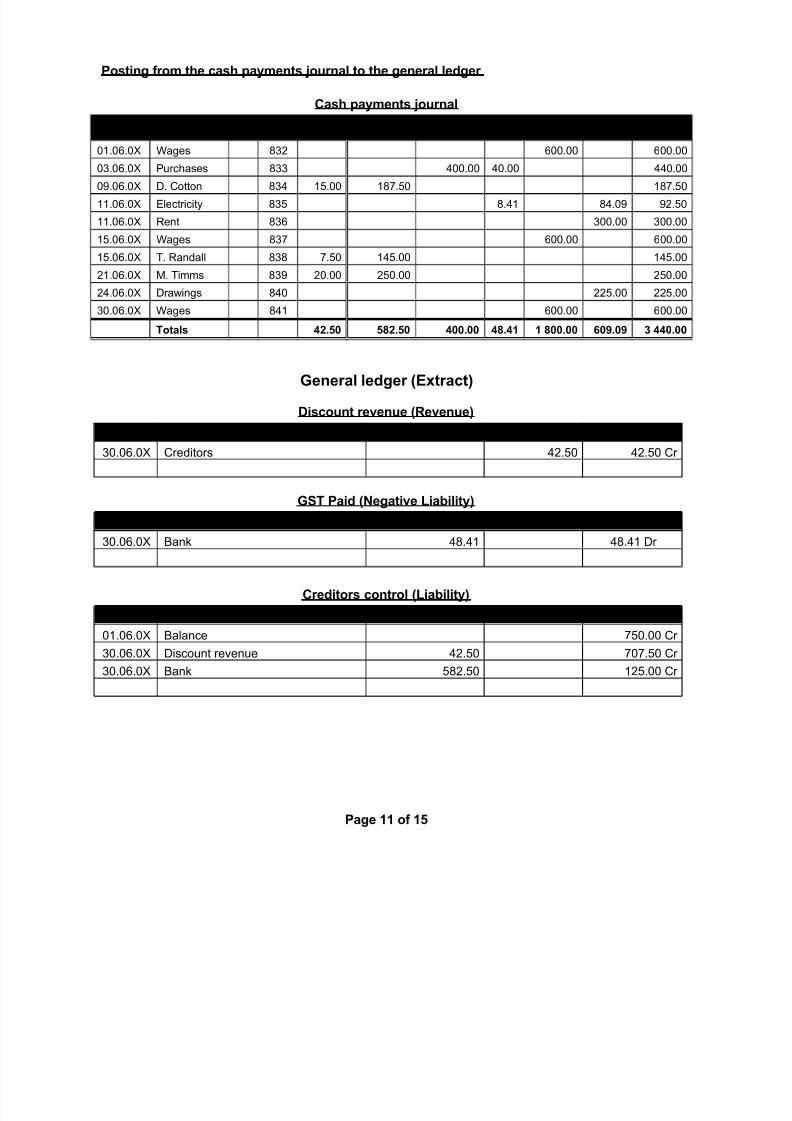

Post$ng fro2 t%e cas% 'ay2ents &ournal to t%e general ledger

Cas% 'ay2ents &ournal

DATE PARTIC"LAR ,+LI+

C*@N+

DICRE!

CREDIT+R P"RC*AE GT AGE "NDR6 BAN7-

5+.50.57 Iages 2- 055.55 055.55

5-.50.57 !urchases 2-- 55.55 5.55 5.55

5;.50.57 =. 8otton 2- +/.55 +21./5 +21./5

++.50.57 Electricity 2-/ 2.+ 2.5; ;./5

++.50.57 Rent 2-0 -55.55 -55.55

+/.50.57 Iages 2-1 055.55 055.55

+/.50.57 T. Randall 2-2 1./5 +/.55 +/.55

+.50.57 G. Ti""s 2-; 5.55 /5.55 /5.55

.50.57 =rawings 25 /.55 /.55

-5.50.57 Iages 2+ 055.55 055.55

Totals 58 5958 8888 91 1 98888 38:8: . 888

General ledger (E<tract)

D$scount re>enue (Re>enue)

DATE PARTIC"LAR DEBIT CREDIT BALANCE

-5.50.57 8reditors ./5 ./5 8r

GT Pa$d (Negat$>e L$a=$l$ty)

DATE PARTIC"LAR DEBIT CREDIT BALANCE

-5.50.57 9an' 2.+ 2.+ =r

Cred$tors control (L$a=$l$ty)

DATE PARTIC"LAR DEBIT CREDIT BALANCE

5+.50.57 9alance 1/5.55 8r

-5.50.57 =iscount revenue ./5 151./5 8r

-5.50.57 9an' /2./5 +/.55 8r

Page 11 of 15

8/14/2019 gen ledger accounts.doc

http://slidepdf.com/reader/full/gen-ledger-accountsdoc 12/15

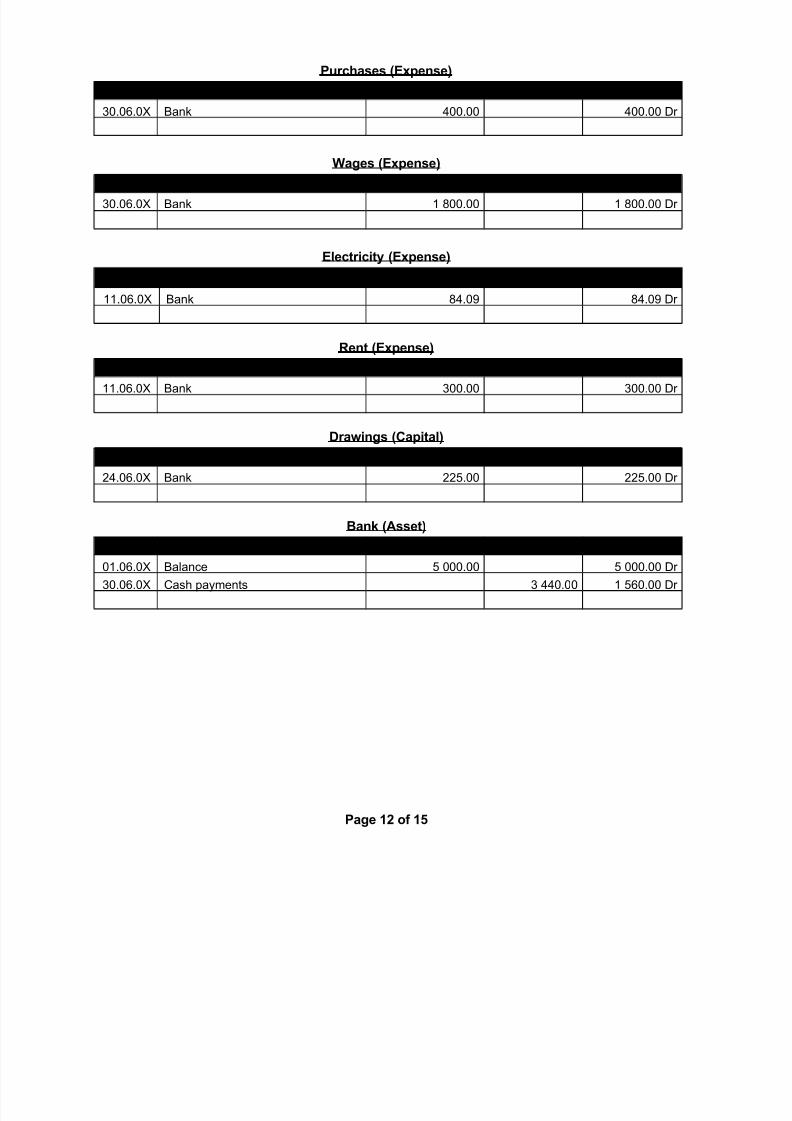

Purc%ases (E<'ense)

DATE PARTIC"LAR DEBIT CREDIT BALANCE

-5.50.57 9an' 55.55 55.55 =r

ages (E<'ense)DATE PARTIC"LAR DEBIT CREDIT BALANCE

-5.50.57 9an' + 255.55 + 255.55 =r

Electr$c$ty (E<'ense)

DATE PARTIC"LAR DEBIT CREDIT BALANCE

++.50.57 9an' 2.5; 2.5; =r

Rent (E<'ense)

DATE PARTIC"LAR DEBIT CREDIT BALANCE

++.50.57 9an' -55.55 -55.55 =r

Dra$ngs (Ca'$tal)

DATE PARTIC"LAR DEBIT CREDIT BALANCE

.50.57 9an' /.55 /.55 =r

Ban? (Asset)

DATE PARTIC"LAR DEBIT CREDIT BALANCE

5+.50.57 9alance / 555.55 / 555.55 =r

-5.50.57 8ash pay"ents - 5.55 + /05.55 =r

Page 1 of 15

8/14/2019 gen ledger accounts.doc

http://slidepdf.com/reader/full/gen-ledger-accountsdoc 13/15

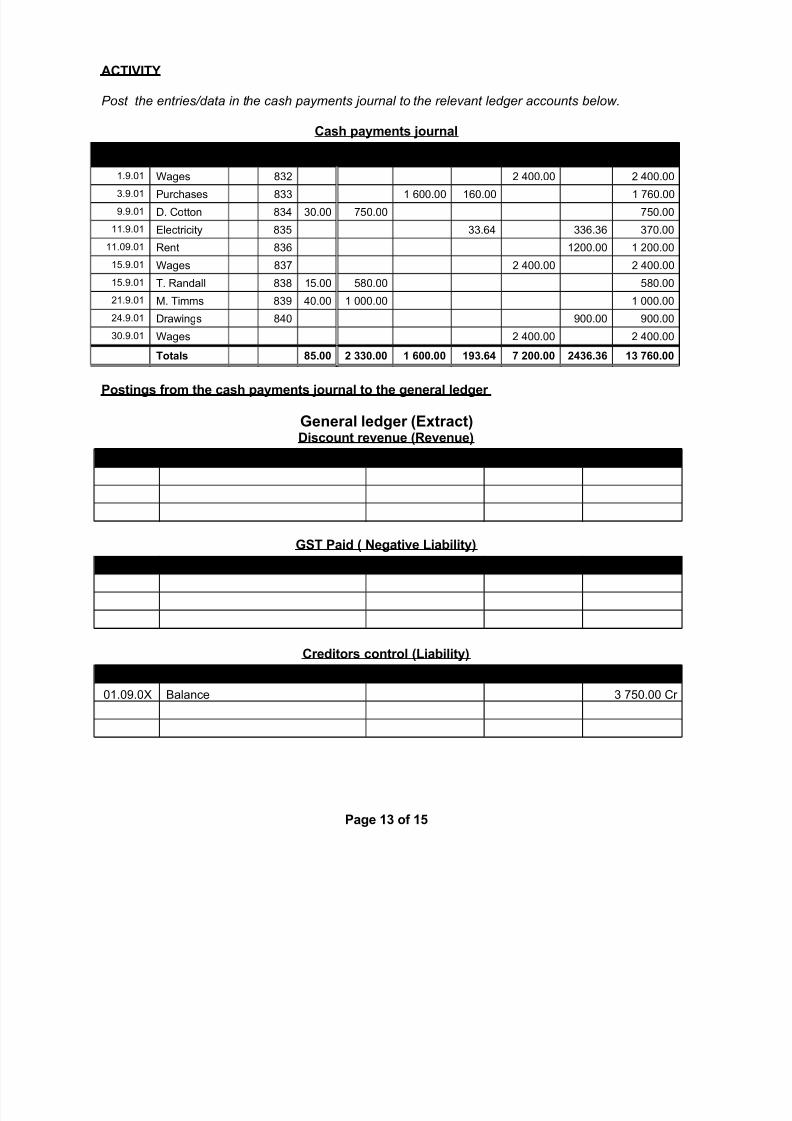

ACTI!IT6

Post the entries/data in the cash payments journal to the relevant ledger accounts below.

Cas% 'ay2ents &ournal

DATE PARTIC"LAR ,+LI+

C*@N+

DICRE!

CREDIT+ P"RC*A GT AGE "NDR6 BAN7

+.;.5+ Iages 2- 55.55 55.55

-.;.5+ !urchases 2-- + 055.55 +05.55 + 105.55

;.;.5+ =. 8otton 2- -5.55 1/5.55 1/5.55

++.;.5+ Electricity 2-/ --.0 --0.-0 -15.55

++.5;.5+ Rent 2-0 +55.55 + 55.55

+/.;.5+ Iages 2-1 55.55 55.55

+/.;.5+ T. Randall 2-2 +/.55 /25.55 /25.55

+.;.5+ G. Ti""s 2-; 5.55 + 555.55 + 555.55

.;.5+ =rawings 25 ;55.55 ;55.55

-5.;.5+ Iages 55.55 55.55

Totals 9588 ..888 1 38888 1:.3 ; 8888 .3.3 1. ;3888

Post$ngs fro2 t%e cas% 'ay2ents &ournal to t%e general ledger

General ledger (E<tract)D$scount re>enue (Re>enue)

DATE PARTIC"LAR DEBIT CREDIT BALANCE

GT Pa$d ( Negat$>e L$a=$l$ty)

DATE PARTIC"LAR DEBIT CREDIT BALANCE

Cred$tors control (L$a=$l$ty)

DATE PARTIC"LAR DEBIT CREDIT BALANCE

5+.5;.57 9alance - 1/5.55 8r

Page 1. of 15

8/14/2019 gen ledger accounts.doc

http://slidepdf.com/reader/full/gen-ledger-accountsdoc 14/15

Purc%ases (E<'ense)

DATE PARTIC"LAR DEBIT CREDIT BALANCE

ages (E<'ense)

DATE PARTIC"LAR DEBIT CREDIT BALANCE

Electr$c$ty (E<'ense)

DATE PARTIC"LAR DEBIT CREDIT BALANCE

Rent (E<'ense)

DATE PARTIC"LAR DEBIT CREDIT BALANCE

Dra$ngs (Ca'$tal)

DATE PARTIC"LAR DEBIT CREDIT BALANCE

Ban? (Asset)

DATE PARTIC"LAR DEBIT CREDIT BALANCE

5+.5;.57 9alance - +-5.55 =r

Page 1 of 15

8/14/2019 gen ledger accounts.doc

http://slidepdf.com/reader/full/gen-ledger-accountsdoc 15/15

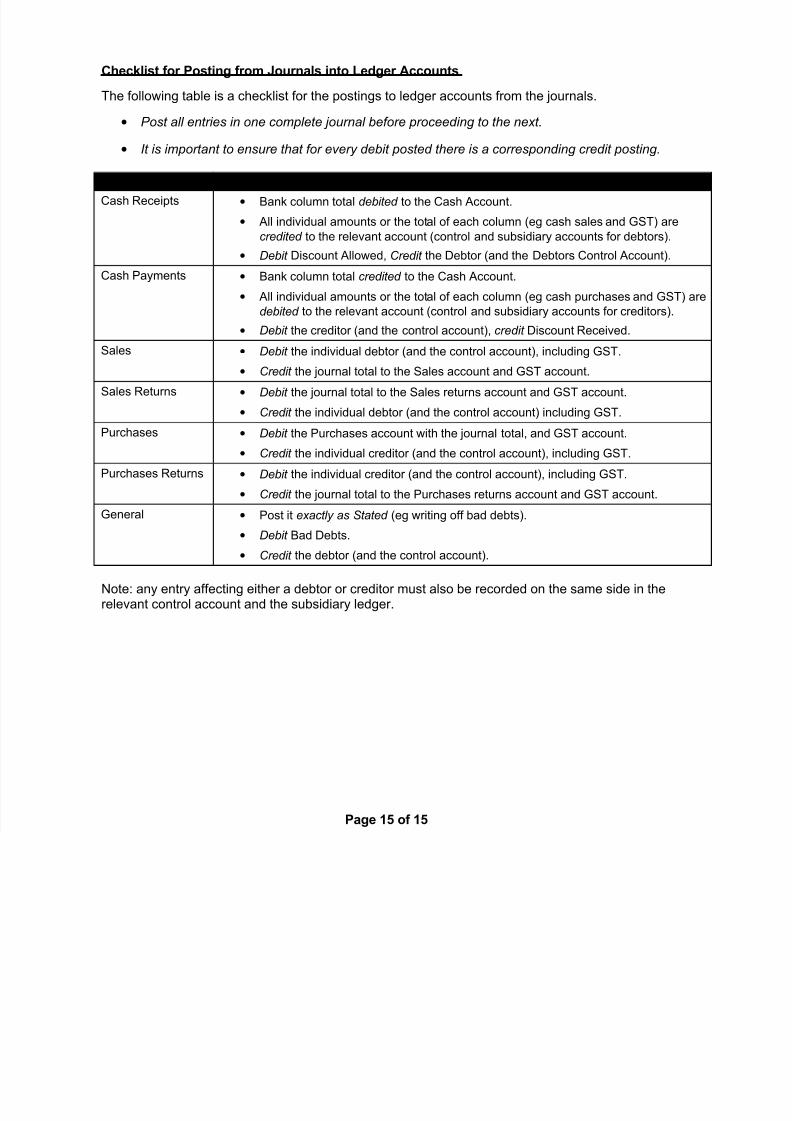

C%ec?l$st for Post$ng fro2 ournals $nto Ledger Accounts

The following table is a chec'list for the postings to ledger accounts fro" the %ournals.

• Post all entries in one complete journal before proceeding to the net.

• !t is important to ensure that for every debit posted there is a corresponding credit posting.

+"RNAL P+TING T+ T*E LEDGER

8ash Receipts • 9an' colu"n total debited to the 8ash Account.

• All individual a"ounts or the total of each colu"n (eg cash sales and <)T arecredited to the relevant account (control and subsidiary accounts for debtors.

• "ebit =iscount Allowed, #redit the =ebtor (and the =ebtors 8ontrol Account.

8ash !ay"ents • 9an' colu"n total credited to the 8ash Account.

• All individual a"ounts or the total of each colu"n (eg cash purchases and <)T debited to the relevant account (control and subsidiary accounts for creditors.

•

"ebit the creditor (and the control account, credit =iscount Received.)ales • "ebit the individual debtor (and the control account, including <)T.

• #redit the %ournal total to the )ales account and <)T account.

)ales Returns • "ebit the %ournal total to the )ales returns account and <)T account.

• #redit the individual debtor (and the control account including <)T.

!urchases • "ebit the !urchases account with the %ournal total, and <)T account.

• #redit the individual creditor (and the control account, including <)T.

!urchases Returns • "ebit the individual creditor (and the control account, including <)T.

• #redit the %ournal total to the !urchases returns account and <)T account.

<eneral • !ost it eactly as $tated (eg writing off bad debts.

• "ebit 9ad =ebts.

• #redit the debtor (and the control account.

3ote any entry affecting either a debtor or creditor "ust also be recorded on the sa"e side in therelevant control account and the subsidiary ledger.

Page 15 of 15