gb wholesale market summary september 2021

TRANSCRIPT

GB Wholesale Market SummarySeptember 2021

Published October 2021

2Source: Aurora Energy Research

Aurora offers power market forecasts and market intelligence spanning Europe’s key markets, the US and Australia

Bespoke forecasts

Aurora can provide power market forecasts upon request

Comprehensive Power Market Services

✓ ✓

✓

✓

✓

✓

✓

✓

Market forecast reports

Forecast data in Excel

Global energy market forecast reports

Strategic insight reports

Regular subscriber group meetings

Policy updates

Bilateral workshops

Analyst support✓

Power MarketForecast Reports

Power market forecast reports

Forecast data in Excel

Analyst support

✓

✓

✓

3

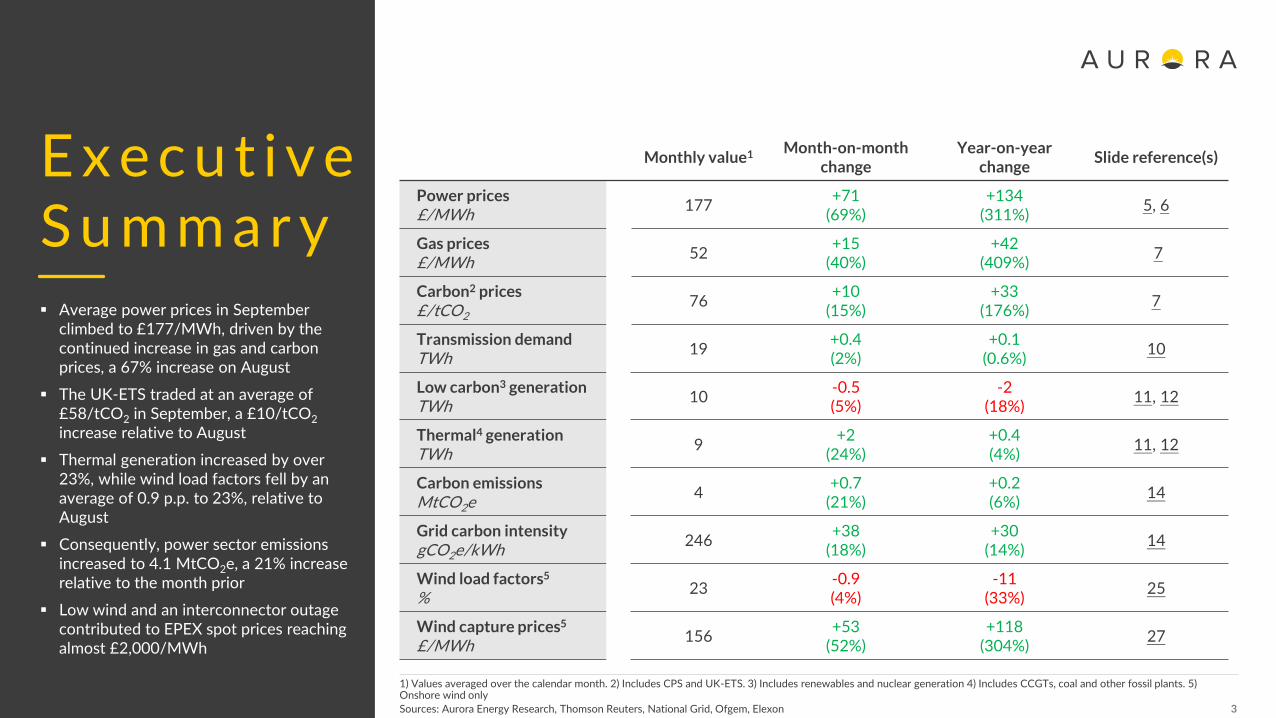

E x e c u t i v e S u m m a r y▪ Average power prices in September

climbed to £177/MWh, driven by the continued increase in gas and carbon prices, a 67% increase on August

▪ The UK-ETS traded at an average of £58/tCO2 in September, a £10/tCO2

increase relative to August

▪ Thermal generation increased by over 23%, while wind load factors fell by an average of 0.9 p.p. to 23%, relative to August

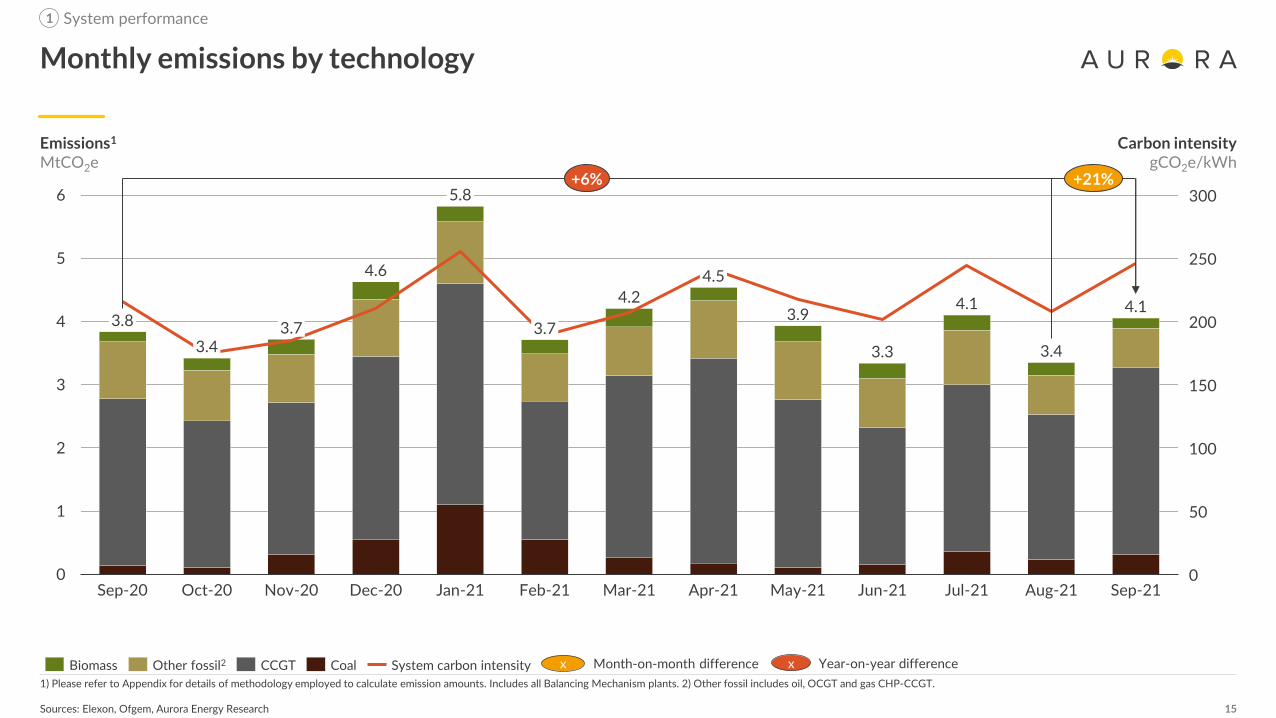

▪ Consequently, power sector emissions increased to 4.1 MtCO2e, a 21% increase relative to the month prior

▪ Low wind and an interconnector outage contributed to EPEX spot prices reaching almost £2,000/MWh

Sources: Aurora Energy Research, Thomson Reuters, National Grid, Ofgem, Elexon

1) Values averaged over the calendar month. 2) Includes CPS and UK-ETS. 3) Includes renewables and nuclear generation 4) Includes CCGTs, coal and other fossil plants. 5) Onshore wind only

Monthly value1 Month-on-month change

Year-on-year change

Slide reference(s)

Power prices£/MWh

177+71

(69%)+134

(311%)5, 6

Gas prices£/MWh

52+15

(40%)+42

(409%)7

Carbon2 prices£/tCO2

76+10

(15%)+33

(176%)7

Transmission demandTWh

19+0.4(2%)

+0.1(0.6%)

10

Low carbon3 generationTWh

10-0.5(5%)

-2(18%)

11, 12

Thermal4 generationTWh

9+2

(24%)+0.4(4%)

11, 12

Carbon emissionsMtCO2e

4+0.7

(21%)+0.2(6%)

14

Grid carbon intensitygCO2e/kWh

246+38

(18%)+30

(14%)14

Wind load factors5

%23

-0.9(4%)

-11(33%)

25

Wind capture prices5

£/MWh156

+53(52%)

+118(304%)

27

4

Agenda

I. System performance

II. Company performance

III. Plant performance

5

EPEX spot price1

£/MWh

Sources: Aurora Energy Research, Thomson Reuters

Half-hourly EPEX spot price for September

1) Half-hourly EPEX is the volume-weighted reference price over that half-hour interval, as provided by EPEX Spot

System performance1

13-Sep0

600

200

400

800

1,200

1,000

1,400

1,600

1,800

2,000

06-Sep 20-Sep 27-Sep

Monthly average price in September 2021:£177/MWh

6

Average EPEX spot price1

£/MWh

Sources: Aurora Energy Research, Thomson Reuters

Historic monthly average EPEX spot price

1) Average monthly EPEX is the average over the month of the volume-weighted reference prices for each half-hour interval.

System performance1

40

50

80

140

20

160

60

70

150

30

90

100

110

170

120

130

180

Sep-17

Sep-20

Sep-10

Sep-12

Sep-11

Sep-15

Sep-13

Sep-16

Sep-18

Sep-19

Sep-21

Sep-14

+311%

+67%

Average monthly spot price Annual average spot price x Month-on-month difference x Year-on-year difference

7

Gas/Coal price£/MWh

Sources: Aurora Energy Research, Thomson Reuters

Historic fuel pricesGas, Coal and Carbon daily prices

1) Includes CPS and EU-ETS until 18th of May 2021, and from 19th of May onwards, includes CPS and UK ETS

System performance1

Jul-21

10

Jan-21

90

15

Nov-200

Sep-20

80

20

Oct-20

65

Dec-20

95

Feb-21 Mar-21

30

Apr-21

55

Sep-21May-21 Jun-21 Aug-21 Oct-210

70

20

30

40

50

60

510

25

70

35

4045

50

60

75

85

Total GB carbon price1

£/tCO2

+89%

+14%

Gas Coal CO2 Monthly averages x Month-on-month difference

8Sources: Aurora Energy Research, ICE Futures, Bank of England

Historic UK ETS and EU ETS Prices

30

35

40

45

50

55

60

65

70

75

14-Jun31-May03-May 26-Jul17-May 28-Jun 12-Jul 09-Aug 23-Aug 06-Sep 20-Sep

Monthly UK ETS averageEU ETS UK ETSWeekly average EU and UK ETS prices £/tCO2

-10

0

10

20

30

40

03-May 17-May 31-May 14-Jun 28-Jun 12-Jul 26-Jul 09-Aug 23-Aug 06-Sep 20-Sep

Relative difference between UK and EU ETS prices %

On the first day of trading, UK ETS prices traded at 5% above the EU ETS

Week commencing

Week commencing

UK ETS began trading on the 19th of May at a price of £45/tCO2

System performance1

The UK ETS traded at an average of £58.2/tCO2 in September

9Sources: Elexon, National Grid, Thomson Reuters, Aurora Energy Research

Half-hourly spot prices against half-hourly system margins for September

1) Half-hourly EPEX is the volume-weighted reference price over that half-hour interval, as provided by EPEX Spot. 2) Margins are calculated as the difference between MEL and Demand for each half-hour period. Demand data presented here is Initial Transmission System Demand Out-Turn, and does not include embedded demand. MEL is calculated as the sum of all transmission BM units reporting MEL values in each half-hour. Where a BMU gives multiple values in a half-hour, only the least is taken.

System performance1

EPEX spot price1

£/MWh

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

0 5,000 10,000 15,000 20,000 25,000 30,000 35,000

Margins2

MW

10

25

20

10

0

5

35

30

15

40

45

50

55

W ThTh SaF SaSu WTuM W F MSu M Tu W Th F Sa FSu Tu W Th Sa Su M Tu Th

Sources: National Grid, Aurora Energy Research

Daily September max and min demandRelative to historic September max and min demand since 20101

1) Data from previous years is matched to the nearest weekday within the current month, to maintain the weekly demand pattern. 2) Demand data presented here is Initial Transmission System Demand Out-Turn, and does not include embedded demand.

System performance1

Demand2

GW

Daily range Historic maximum/minimum

11Sources: National Grid, Aurora Energy Research

Monthly historical demand on the transmission system

1) Demand data presented here is Initial Transmission System Demand Out-Turn, and includes station transformer load, pumped storage demand and interconnector demand, but does not include embedded demand.

System performance1

Total demand1

TWh

26

16

28

18

20

22

24

30

32

34

Sep-17

Sep-10

Sep-11

Sep-12

Sep-13

Sep-14

Sep-18

Sep-15

Sep-21

Sep-16

Sep-19

Sep-20

+2%+3%

Total monthly demand Annual average demand x Month-on-month difference x Year-on-year difference

12

Output1

TWh

Sources: Elexon, Sheffield Solar, National Grid, Aurora Energy Research

Monthly fuel mix breakdown

20

0

16

14

2

4

6

8

18

12

10

1.4

Other fossil2

1.9

Onshore Wind

0.4

19%

TotalCCGT Nuclear Coal

9%

Other renewables3

8%

7.5

Solar

2%

40%

100%

10%

1.2

Offshore Wind

6%

1.7

3.6

1.018.7

5%

Load factor%

System performance

1) Includes outputs from generators registered as BM Units as well as embedded wind and solar PV assets. All numbers are rounded to 0.1 TWh which means that subtotals may not sum to total value. 2) Other fossil includes oil, CHP-CCGT and OCGT. 3) Other renewables includes biomass and hydro.

1

38 54 27 19 27 28 11 9

13

Output1

% of total

Sources: Elexon, Sheffield Solar, National Grid, Aurora Energy Research

Historical fuel mix breakdown

System performance

17% 19%25% 24%

20%24% 27% 27% 25% 24%

18% 19%

28%28%

45%41%

35%23%

45%37%

15%18%

27%

29%

37% 33%

23%29%

32%

40%

10%

5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Sep-20

Sep-10

Sep-11

Sep-15

Sep-12

Sep-13

Sep-14

4%

Sep-16

5%

Sep-17

6%

Sep-18

1%

Sep-19

1%

9%

6%

8%

2%

Sep-21

Other renewables3Nuclear Other fossil2CCGTCoal Onshore Wind Offshore Wind Solar Imports

1) Includes outputs from generators registered as BM Units as well as embedded wind and solar PV. 2) Other fossil includes oil, CHP-CCGT and OCGT. 3) Other renewables includes biomass and hydro.

1

14

Flow1

MW

Sources: Elexon, National Grid, Aurora Energy Research

Monthly interconnector flow duration curveFlow in each half-hour for GB interconnectors

1) Positive flow is imports into GB, negative flow is exports.

System performance

200

0

1,000

1,400

2,000

-800

-600

-400

-200

400

600

800

1,200

1,600

1,800

I/C France 2

I/C France I/C Rep. IrelandI/C Netherlands

I/C N. Ireland I/C Belgium

1

TimeHalf-hours

15

Emissions1

MtCO2e

Sources: Elexon, Ofgem, Aurora Energy Research

Monthly emissions by technology

1) Please refer to Appendix for details of methodology employed to calculate emission amounts. Includes all Balancing Mechanism plants. 2) Other fossil includes oil, OCGT and gas CHP-CCGT.

System performance

0

1

2

3

4

5

6

200

150

100

50

250

0

300

4.1

Nov-20Sep-20 Oct-20 Dec-20 Jan-21

3.4

Feb-21

4.2

Apr-21 May-21 Jun-21 Jul-21 Aug-21 Sep-21

3.8 3.7

4.6

3.7

4.5

3.9

5.8

3.3

4.1

3.4

Mar-21

+6% +21%

CCGTOther fossil2Biomass System carbon intensityCoal

1

Carbon intensitygCO2e/kWh

x Month-on-month difference x Year-on-year difference

16

Agenda

I. System performance

II. Company performance (Subscriber Only)

III. Plant performance

17

Agenda

I. System performance

II. Company performance

III. Plant performance

18

Load factor1

%

Sources: Aurora Energy Research, Elexon, BEIS

Plant utilisation – load factors by plant

1) Represents 60 plants with highest capacity according to the Balancing Mechanism (BM) database, as well as aggregated data for wind and solar. Capacity of each plant represents the sum of capacities of all its generators that have been active at least once in the last three months. Please refer to Appendix for a detailed description of the data used and categories presented

Plant Performance

Capacity, GW

3

Column width reflects capacity

10

64

30

50

60

80

90

58 665654 620

50

100

444038 483634 7032262422 52

40

20 681816 423012 14

20

4 6 462

60

280 728

70

10

Ø 32

Hydro

Gas CHP-CCGT

Biomass Onshore Wind

CCGT

Coal

Interconnector Pumped Storage

Nuclear

OCGT

Offshore Wind

Oil

Solar

19

Full load hours1

% of total for the period

Sources: Aurora Energy Research, Elexon

CCGT plant utilisation – by plant

1) Includes all CCGT plants of the presented companies that report to the Balancing Mechanism

Plant Performance

Capacity, GW

3

Column width reflects capacity

Plant Names: 1. Enfield Energy, 2. Langage, 3. Marchwood, 4. Pembroke, 5. Cottam Dvpt Centre, 6. Great Yarmouth, 7. Kings Lynn, 8. Carrington, 9. Staythorpe, 10. West Burton B, 11. DidcotB, 12. Seabank 1, 13. Damhead Creek, 14. Seabank 2, 15. Spalding, 16. Keadby, 17. Rocksavage, 18. Connahs Quay, 19. South Humber Bank, 20. Little Barford, 21. Rye House, 22. Coryton, 23.Shoreham, 24. Corby, 25. Killingholme 2, 26. Peterborough, 27. Medway, 28. Killingholme 1, 29. Sutton Bridge, 30. Glanford Brigg, 31. Peterhead, 32. Severn, 33. Baglan Bay.

10

30

20

90

100

40

10 250

60

30

5 15

70

50

200

80

174 16

63

.6

58

.0

1024

22 2526

27 29 30 31 32

80

.6

78

.9

21

77

.6

74

.0

71

.66

9.9

60

.4

56

.6

20

43

.2

41

.4

33

.9

32

.7

22

.6

17

.2

16

.5

15

.5

7.3

4.8

0.02

.4

2.0

0.0

0.0

0.0

0.0

18 191312 15 2328

6

0.0

5

54

.0

3 8 921

2.1

7

45

.2

3311

37

.1

14

3.2

RWECalon EDF IntergenCentrica Drax EPH ESB Munich Re SSE Uniper

20

Full load hours1

% of total for the period

Sources: Aurora Energy Research, Elexon

Coal plant utilisation – by plant

1) Includes all coal plants of the presented companies that report to the Balancing Mechanism

Plant performance

Capacity, GW

3

Column width reflects capacity

Plant Names: 1. Ratcliffe, 2. West Burton, 3. Uskmouth, 4. Fiddlers Ferry, 5. Drax Coal.

2

10

0

20

40

50

40

70

30

6

90

80

100

60

0.00.0

1 2 3

24.0

4

0.5

5

0.0

SSEDrax EDF UniperSIMEC

21

Average load factor1

%

Sources: Aurora Energy Research, Elexon, Crown Estate

Monthly load factors by technology

1) Includes outputs from generators registered as BM Units as well as embedded wind and solar PV

Plant performance

34 40 42 41 3650

3923 26 21 15 23 22

60

0

40

20

Mar-21Sep-20 Oct-20 Nov-20 Dec-20 Jan-21 Feb-21 Apr-21 May-21 Jun-21 Jul-21 Aug-21 Sep-21

4156 52 52 48

5945

28 31 23 2131 27

60

20

0

40

Jul-21Dec-20Sep-20 May-21 Sep-21Oct-20 Nov-20 Jan-21 Feb-21 Mar-21 Apr-21 Jun-21 Aug-21

126 4 2 3

69

17 15 16 1612 11

0

5

15

10

20

Apr-21Sep-20 Oct-20 Nov-20 Feb-21Dec-20 Jan-21 Mar-21 May-21 Jun-21 Jul-21 Aug-21 Sep-21

Solar AverageSolarOffshore Wind Offshore Average

3

Onshore Wind Onshore Average

22

Load factor1

%

Sources: Aurora Energy Research, Elexon, Crown Estate

Wind farm utilisation – load factor by wind farm

1) Represents UK wind farms reporting Balancing Mechanism Unit data. Figures presented reflect Final Physical Notification (FPN) expectations reported to the grid, which are not always representative of actual production

Plant performance

100

70

40

90

50

30

60

10

0

80

20

10030 9010 10720 40 80

109

70 111108 110

60501

Offshore Wind Onshore Wind

3

Plant Names: 1. Halsary Windfarm, 2. Whiteside Hill, 3. Galloper, 4. Aikengall 2, 5. Beatrice, 6. Dunmaglass, 7. Westermost Rough, 8. Dudgeon, 9. Hornsea 1 , 10. Moray East, 11. Brockloch Rig 2, 12. Corriegarth, 13. Andershaw, 14. Beinn an Tuirc III , 15.Carraig Gheal, 16. Crystal Rig, 17. Cour, 18. Farr, 19. Humber, 20. East Anglia One, 21. Hywind Scotland, 22. Stronelairg, 23. Rampion, 24. Fallago Rig, 25. An Suidhe, 26. Lincs, 27. Race Bank, 28. Bad a Cheo, 29. Beinneun, 30. Kilbraur, 31. West of DuddonSands, 32. Rothes Extension, 33. Aberdeen, 34. Sanquhar Community, 35. Dorenell, 36. Blackcraig, 37. Auchrobert, 38. Walney Extension, 39. Gordonbush, 40. Hill of Glaschyle, 41. Greater Gabbard, 42. Edinbane, 43. London Array, 44. Bhlaraidh, 45.Baillie, 46. Camster, 47. Berry Burn, 48. Gordonstown, 49. Kilgallioch, 50. Gwynt y Mor, 51. Assel Valley, 52. A Chruach, 53. Robin Rigg, 54. Freasdail, 55. Harburnhead, 56. Beinn Tharsuinn, 57. Millennium, 58. Walney, 59. Strathy North, 60. BurboExtension, 61. Minsca, 62. Clyde, 63. Coire Na Cloiche, 64. Mid Hill, 65. Burn of Whilk, 66. Kype Muir, 67. Afton, 68. Thanet, 69. Gunfleet Sands, 70. Braes of Doune, 71. Corriemoillie, 72. Clashindarroch, 73. Tullymurdoch, 74. Ormonde, 75. Glen App, 76.Barrow, 77. Embedded Wind, 78. Pen y Cymoedd, 79. Glens of Foudland, 80. Dersalloch, 81. Hare Hill Extension, 82. Dalswinton, 83. Toddleburn, 84. Lochluichart, 85. Burbo Bank, 86. Ewe Hill, 87. Beinn An Tuirc , 88. Griffin, 89. Sheringham Shoals, 90. Hillof Towie, 91. Middle Muir, 92. Moy, 93. Goole Fields, 94. Tullo, 95. Whitelee, 96. Tullo Extension, 97. Craig, 98. Minnygap, 99. Dun Law Extension, 100. Arecleoch, 101. Hadyard Hill, 102. Mark Hill, 103. Harestanes, 104. Glenchamber, 105. Black Law, 106.Clachan Flats, 107. Airies, 108. Keith Hill, 109. Kincardine, 110. Galawhistle, 111. Brownieleys.

23

Baseload and capture price1,2

£/MWh

RES capture price versus baseload price

1) Baseload price is the average monthly EPEX price; 2) Wind capture price is the load-weighted monthly average EPEX price across all wind Balancing Mechanism plants for all half-hourly periods. 3) Negative values represent capture prices above the baseload price while positive values represent capture prices below the baseload price

Plant performance

Sources: Aurora Energy Research, Elexon, Thomson Reuters

3

Mar-21Feb-21

15

Jun-21Apr-21-10

-5

0

5

10

Sep-20 Oct-20 Jul-21Nov-20 Dec-20 Jan-21 May-21 Aug-21 Sep-21

Technology capture discount2,3 to baseload%

Apr-21Feb-21 Mar-21

100

0Aug-21Sep-20 Oct-20 Nov-20

200

Dec-20 Jan-21 May-21 Jun-21 Jul-21 Sep-21

50

150

+262%

+49%

Baseload Offshore WindOnshore Wind Average wind x Month-on-month difference (average wind) x Year-on-year difference (average wind)

24

▪ Output values used in this summary reflect the sum of Final Physical Notifications (FPN) submitted by all BM Units of a given plant that have been active over the last three months.

▪ Capacity values used in this summary reflect the sum of capacities of individual BM Units, as reported to the Balancing Mechanism, that have been active over the last three months. They reflect long-term capacities and exclude temporary fluctuations due e.g. to plant failures or scheduled maintenance.

▪ Prices used in this summary are the EPEX half-hourly Reference Prices for half-hourly, two-hourly and four-hourly spot products.

Data used

▪ Full-load hours represent the plants’ load factors, calculated as the ratio of the output produced in a given month to the maximum possible output given the plants’ capacity.

▪ Running hours represent the proportion of time in a given month when a plant has been active, i.e. when at least one of its BM Units produced output greater than zero.

▪ Capture prices (or average output-weighted prices) are calculated as an average of EPEX half-hourly prices per MWh weighted by the plants’ corresponding half-hourly outputs for all periods.

▪ Average gross margins are calculated as a sum of the uplift and inframarginal rent. Uplift is calculated as the difference between the EPEX price and the system marginal cost (SMC). SMC is the maximum marginal cost of all the plants with at least one generator producing above 80% of its installed capacity in a given half-hour.

▪ Emissions are calculated as plant output divided by electrical efficiency, multiplied by theoretical carbon content of the fuel input. The carbon content of fuel inputs is sourced from BEIS’s Greenhouse gas reporting – Conversion factors 2016. System carbon intensity is calculated as the total emission divided by total electricity generated.

Categories presented

Source: Aurora Energy Research

Appendix

25

General DisclaimerThis document is provided "as is" for your information only and no representation or warranty, express or implied, is given by Aurora Energy Research Limited and itssubsidiaries Aurora Energy Research GmbH and Aurora Energy Research Pty Ltd (together, "Aurora"), their directors, employees agents or affiliates (together, Aurora’s"Associates") as to its accuracy, reliability or completeness. Aurora and its Associates assume no responsibility, and accept no liability for, any loss arising out of your useof this document. This document is not to be relied upon for any purpose or used in substitution for your own independent investigations and sound judgment. Theinformation contained in this document reflects our beliefs, assumptions, intentions and expectations as of the date of this document and is subject to change. Auroraassumes no obligation, and does not intend, to update this information.

Forward-looking statementsThis document contains forward-looking statements and information, which reflect Aurora’s current view with respect to future events and financial performance. Whenused in this document, the words "believes", "expects", "plans", "may", "will", "would", "could", "should", "anticipates", "estimates", "project", "intend" or "outlook" or othervariations of these words or other similar expressions are intended to identify forward-looking statements and information. Actual results may differ materially from theexpectations expressed or implied in the forward-looking statements as a result of known and unknown risks and uncertainties. Known risks and uncertainties include butare not limited to: risks associated with political events in Europe and elsewhere, contractual risks, creditworthiness of customers, performance of suppliers andmanagement of plant and personnel; risk associated with financial factors such as volatility in exchange rates, increases in interest rates, restrictions on access to capital,and swings in global financial markets; risks associated with domestic and foreign government regulation, including export controls and economic sanctions; and otherrisks, including litigation. The foregoing list of important factors is not exhaustive.

CopyrightThis document and its content (including, but not limited to, the text, images, graphics and illustrations) is the copyright material of Aurora, unless otherwise stated.This document is confidential and it may not be copied, reproduced, distributed or in any way used for commercial purposes without the prior written consent of Aurora.

Disclaimer and Copyright