gas to liquids - trizeninternational.comgas to liquids technology drivers to develop gtl business...

TRANSCRIPT

TRI-ZEN June 2005

GAS TO LIQUIDSGAS TO LIQUIDSThe future is gas The future is gas –– how gashow gas--toto--liquids technology becomes the liquids technology becomes the

reality that replaces oilreality that replaces oil

Presentation byPresentation byTony ReganTony Regan

TRITRI--ZEN International to ZEN International to Institute of South East Asian StudiesInstitute of South East Asian Studies

7 June 20057 June 2005

2

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

AGENDAAGENDAIntroduction to TRI-ZENIntroducing GTL

What is it?BackgroundGas to Liquids technologyDrivers to develop GTL businessWhy build GTL plants?Why is GTL attractive to a gas producer and “why now”?

GTL projectsExisting or under developmentOverview of the Qatar GTL projects“Rest of the world”

GTL products – what are they and what will they be used for?Could small be beautiful?What next - how the industry might evolve Summary & Final Note

3

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

INTRODUCTION TO TRIINTRODUCTION TO TRI--ZEN ZEN

TRI-ZEN is a consulting business focused on energy and utilities Offering a range of services focused on consulting, business development organization development & project managementWith 25 Lead Consultants across Asia and energy industry experience in:

LNG, Pipeline Gas & LPGUtilities – Power & WaterRefining & DistributionBase stocks, Lubes & Special ProductsOil Trading, Risk Management & ShippingAviation fuels marketing and operationsUpstream Oil Exploration/Production and OperationsChemicals & Industrial Gases

4

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

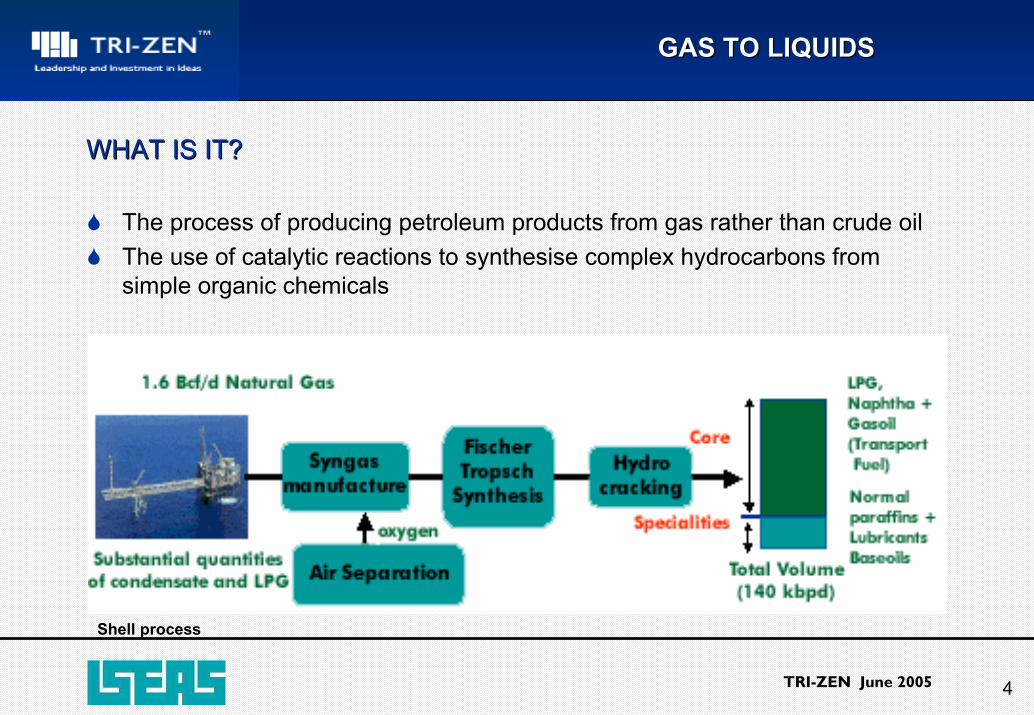

WHAT IS IT?WHAT IS IT?

The process of producing petroleum products from gas rather than crude oil The use of catalytic reactions to synthesise complex hydrocarbons from simple organic chemicals

Shell process

5

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

BACKGROUNDBACKGROUND

Basic technology developed in the 1920’s by German scientists Fischer & Tropsch Used in Germany during World War II and by Sasol in South Africa (from 1955) to convert coal to synthesis gas and then oil Mobil developed and built M-gasoline in 1985 at a New Zealand methanol to gasoline plant, but proved not commercially viable at time (cost over $30/bbl) 1993 Sasol commissioned a 25,000 barrels/day (b/d) GTL plant at Mosel Bay using coal as the feedstock1993 Shell built a 12,000 b/d GTL plant at Bintulu, Malaysia using natural gas and the Shell Middle Distillate Synthesis (SMDS) process to produce middle distillates and wax Experience gained from these projects gave the participants confidence to develop world scale commercial projects

6

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

GAS TO LIQUID TECHNOLOGYGAS TO LIQUID TECHNOLOGY

Two technologies:Direct conversion of methane to syncrude without going via syngas. Energy intensive and difficult to control. Not yet commercialised

Indirect conversion where natural gas is converted (reforming) to produce hydrogen and carbon monoxide in a ratio of 2:1 by partial oxidation or steam reforming (syngas) The syngas is then passed through a Fisher-Tropsch reactor containing an iron or cobalt catalyst and converted into straight chain waxy paraffins (syncrude) The syncrude is then passed through a conventional hydrocracker to produce high quality petroleum products

7

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

THE GTL PROCESS CONVERTS NATUTHE GTL PROCESS CONVERTS NATURRAL GAS TO EASILY AL GAS TO EASILY TRANSPORTABLE LIQUID PRODUCTSTRANSPORTABLE LIQUID PRODUCTS

GTLNaphtha

GTLFuel

GTLBase Oil

N2 to atmosphere

NaturalGas

Oxygen

O2

CH4

Syngas

H2

Fischer-Tropsch

Conversion

WaxySyncrude

Natural Gas

Reforming

Product Upgrading

CO

H2Oby-product

8

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

GAS TO LIQUID TECHNOLOGYGAS TO LIQUID TECHNOLOGY

Many variables within basic concept:Syngas can be produced by:

Steam reforming – expensive and very high hydrogen yieldPartial Oxidation – auto-thermal reforming (ATR)

Partial oxidation can be achieved using:Air. Much cheaper but produces nitrogen and a dilute syngas (Syntroleum, BP)Oxygen. Expensive, much larger plant. Purer syngas (Others)

The temperature, pressure and catalyst used to convert the syngas to products determines whether a light or heavy syncrude is produced:

High temperature process (330 deg C) produces gasoline and olefins (Sasol, Mossel Bay)Low temperature process (180-250 deg C) produces mainly diesel and waxes

Two types of FT reactor:Vertical fixed tubes containing the catalyst with several reactors in parallelSyngas is fed into bottom of reactor and moves through a slurry of liquid wax and catalyst particles. Gas is diffused and converted into more wax as it bubbles upward

9

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

Water Treating

Utilities

Gas Processing GTL Process

Air SeparationUnits

Storage

PEARL GTL, QATAR PEARL GTL, QATAR –– ONSHORE PLANT LAYOUTONSHORE PLANT LAYOUT

10

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

WHAT DOES A GTL PLANT COST?WHAT DOES A GTL PLANT COST?

Equipment cost breakdown for a 50,000 b/d plant (approx)

Syngas generation $420 millionAir Separation units $200 millionFT synthesis $180 millionOff-sites & Utilities $120 millionHydro-finishing $110 millionPower $100 millionNatural gas pre-treatment $40 millionOthers $80 millionTotal $1150 million

Add in catalyst cost, licences, labour and financing then the total cost of major full scale projects is $5-7 billion. The budget for the smaller (34 mbcd) Oryx plant currently under construction is $1bn including financing costs

ExxonMobil – Qatar GTL is its largest and most expensive single project ($7 bn)PEARL GTL – “probably the largest and most complex onshore project ever built

by Shell”

Indicative based on 2003 costs to indicate the relative cost of the components.

11

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

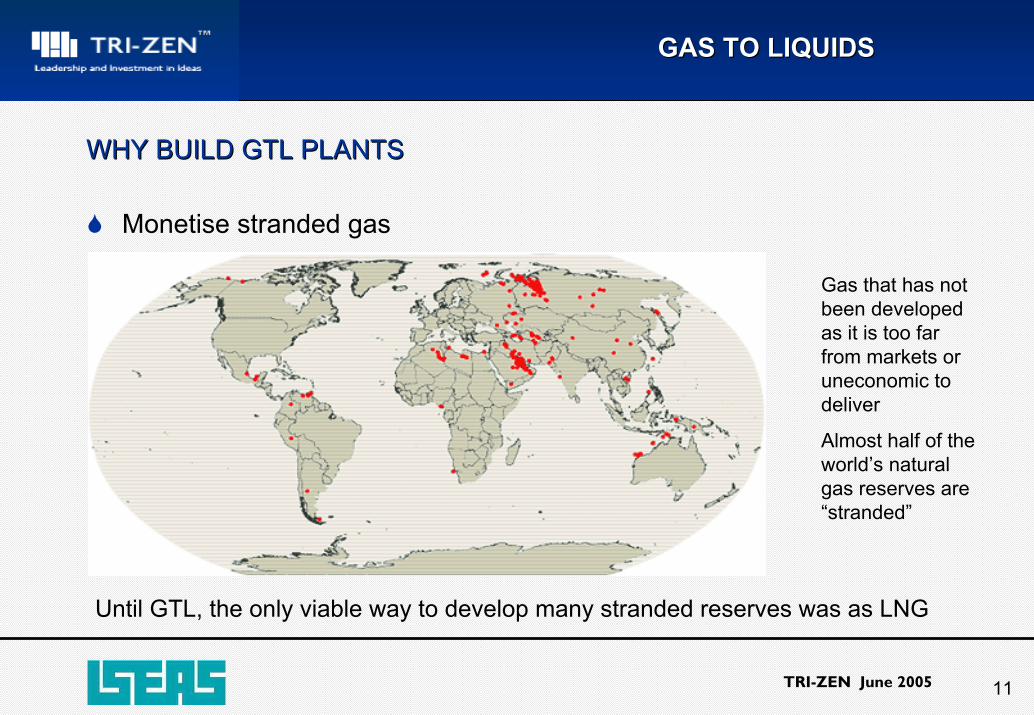

WHY BUILD GTL PLANTSWHY BUILD GTL PLANTS

Monetise stranded gas

Gas that has not been developed as it is too far from markets or uneconomic to deliver

Almost half of the world’s natural gas reserves are “stranded”

Until GTL, the only viable way to develop many stranded reserves was as LNG

12

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

MONETISING GAS RESERVESMONETISING GAS RESERVES BP Statistical Review 2005BP Statistical Review 2005

Gas consumption 2,689 bn cub mtrs in 2004 Proven gas reserves 180 trillion cub mtrs in 2004

GTL consumption –2% (to 2015)

BY 2015 GTL consumption will still only equal 2% of total

GTL – a very attractive option to producers wishing to monetise reserves

13

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

WHY IS GTL ATTRACTIVE TO A GAS PRODUCER?WHY IS GTL ATTRACTIVE TO A GAS PRODUCER?

Options:Pipeline

Most economic to about 2,000 kmsExtensive pipeline network in USA and EuropeConstrained by geography and politicsOnly 18% of natural gas crosses borders

CNGLimited application – mainly busesUsually stays within local areaNeeds dedicated vessels – very expensiveNot really commercially viable beyond 1600 kms (go for LNG)

14

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

WHY IS GTL ATTRACTIVE TO A GAS PRODUCER (2)WHY IS GTL ATTRACTIVE TO A GAS PRODUCER (2)

Options cont:LNG

Only means for gas to access distant markets (e.g. Japan)Flexible – suppliers have global reachLong lead time to develop projectsRequires specialist vessels and re-gasification terminals at destination

GTLProduction costs similar to LNGDoes not require specialist ships or receiving terminalsProduces ready for market petroleum productsFlexible product slateGlobal market for products

15

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

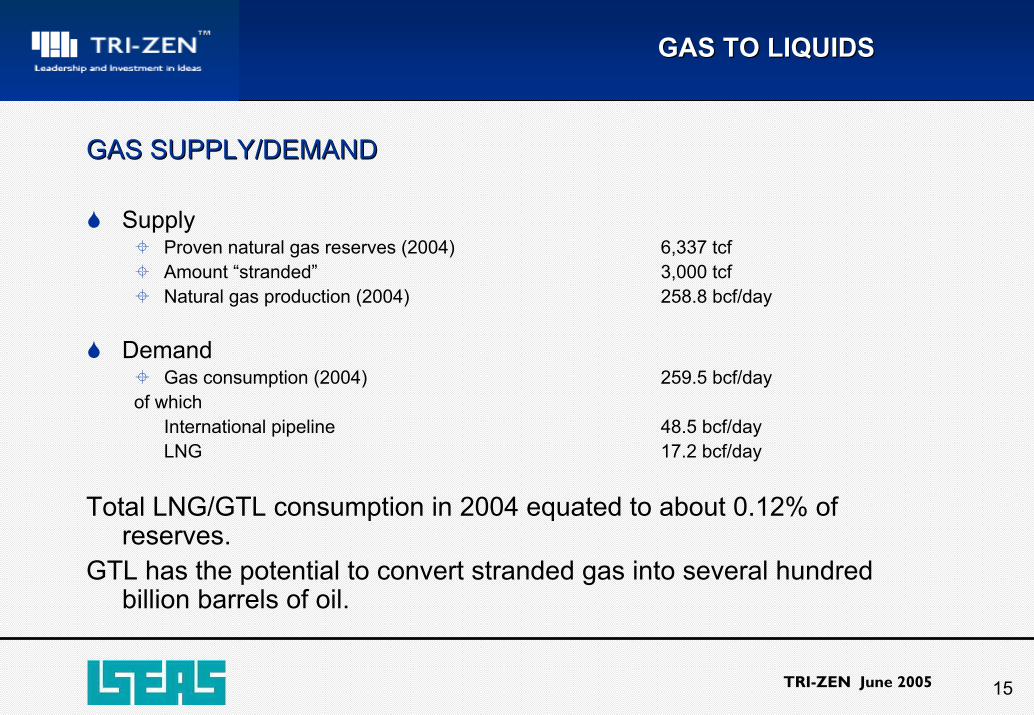

GAS SUPPLY/DEMANDGAS SUPPLY/DEMAND

SupplyProven natural gas reserves (2004) 6,337 tcfAmount “stranded” 3,000 tcfNatural gas production (2004) 258.8 bcf/day

DemandGas consumption (2004) 259.5 bcf/day

of whichInternational pipeline 48.5 bcf/dayLNG 17.2 bcf/day

Total LNG/GTL consumption in 2004 equated to about 0.12% of reserves.

GTL has the potential to convert stranded gas into several hundred billion barrels of oil.

16

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

MONETISING TECHNOLOGYMONETISING TECHNOLOGY

In the last 20 years:$2.1 bn invested in research

$4.6 bn invested in R&D (including Bintulu & S.Africademo units)

ExxonMobil holds over 500 patentsrelated to Fisher-Tropsch synthesis

Others – ConocoPhillips (120 patents)BP (75), Statoil (70)

R&D investment in GTL (Mill US$)

0500

1000150020002500

ExxonM

obil

Shell

Sasol

ChevT

exSyn

troleum

IFP/ENI

17

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

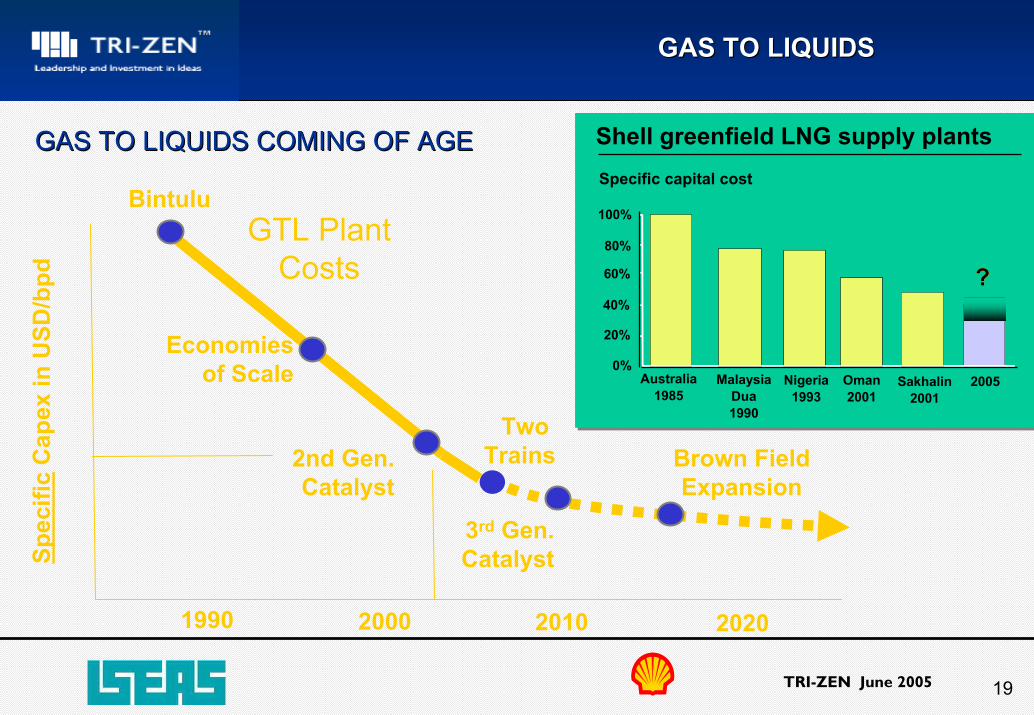

GAS TO LIQUIDS COMING OF AGEGAS TO LIQUIDS COMING OF AGE

1990 2000

Spec

ific

Cap

ex in

USD

/bpd

Economiesof Scale

2nd Gen.Catalyst

GTL Plant Costs

3rd Gen. Catalyst

2010 2020

Brown FieldExpansion

Two Trains

Bintulu

18

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

WHY NOW?WHY NOW?

Costs have come down considerablyTotal installed cost for Shell SMDS at Bintulu was about $50,000/bblTechnical advances have brought costs down to $25,000-30,000/bbl$20,000/bbl is believed to be in sight for large scale projects

Shell & ExxonMobil have declared that their Qatar projects are viable at $20/bbl oil pricesGTL very attractive at current crude pricesStrong demand for ultra low sulphur clean diesel fuel and premium baseoilsStrong petrochemical growth, particularly in Asia

Expectation of further cost reductions in the technology (air separation, Syngas, FT synthesis, wax upgrading) have suggested that $12,000/bbl is achievable – comparable with a complex refinery

19

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

1990 2000

Spec

ific

Cap

ex in

USD

/bpd

Economiesof Scale

2nd Gen.Catalyst

GTL Plant Costs

3rd Gen. Catalyst

2010 2020

Brown FieldExpansion

Two Trains

???

Shell greenfield LNG supply plantsSpecific capital cost

Australia1985

MalaysiaDua1990

Nigeria1993

Oman2001

Sakhalin2001

20050%

20%

40%

60%

80%

100%

GAS TO LIQUIDS COMING OF AGEGAS TO LIQUIDS COMING OF AGE

Bintulu

20

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

COMPARATIVE ECONOMICS LNG v GTLCOMPARATIVE ECONOMICS LNG v GTL

GTL costs have dropped to a point where they are almost similar to LNG. LNG has a disadvantage compared with GTL in that it also requires specialist ships ($300 mill each) and re-gasification terminals at the discharge ports (+$600 million) GTL and LNG are not in competition - they serve different marketsSubstantial gains to be had by integrating LNG and GTL production and using shared services

21

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

GTL PROJECTS GTL PROJECTS –– EXISTING OR UNDER DEVELOPMENTEXISTING OR UNDER DEVELOPMENT

714,200TotalHeads of Agmt.2011154,000QatarExxonMobil Qatar

EPC200934,000NigeriaSasol Chevron Nigeria

FEED phase2009140,000QatarShell/Qatar Petroleum

LOI2010?120,000QatarConocoPhillips Qatar

LOI2010130,000QatarSasol Chevron Integrated GTL

MOU200965,000QatarSasol Chevron Oryx expansion

Under construction200534,000QatarSasol/Qatar Petroleum Oryx

Under development

Operating199314,700MalaysiaShell Bintulu

Operating199122,500S. AfricaMossgas

StatusStart upCapacity b/dCountryExisting

22

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

PROPOSED GTL PROJECTS (units barrels/day)PROPOSED GTL PROJECTS (units barrels/day)

60,000USAANGTL Alaska

75,000ArgentinaShell Argentina

75,000TrinidadShell Trinidad

75,000IndonesiaShell Indonesia

75,000IranShell Iran

15,000VenezuelaPDVSA

75,000AustraliaShell Australia

30,000AustraliaSasol Chevron

50,000AustraliaAustralia Power Energy

15,000IndonesiaRentech/Pertamina

90,000BoliviaSyntroleum/Repsol

75,000EgyptShell/EGPC

10,000ChileSyntroleum

120,000QatarMarathon

1,134,000Total

36,000AlgeriaSonatrach (Tinhert GTL)

13,000RussiaSyntroleum/Yakut

20,000NigeriaDrake Synergy

5,000PeruSyntroleum Peru

10,000BoliviaGTL Bolivia

45,000OmanIvanhoe Energy

45,000EgyptIvanhoe Energy

10,000South AfricaForest Oil

35,000IranNarkanan GTL

75,000MalaysiaShell Malaysia

23

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

QATAR QATAR –– THE GLOBAL GAS CAPITALTHE GLOBAL GAS CAPITAL

24

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

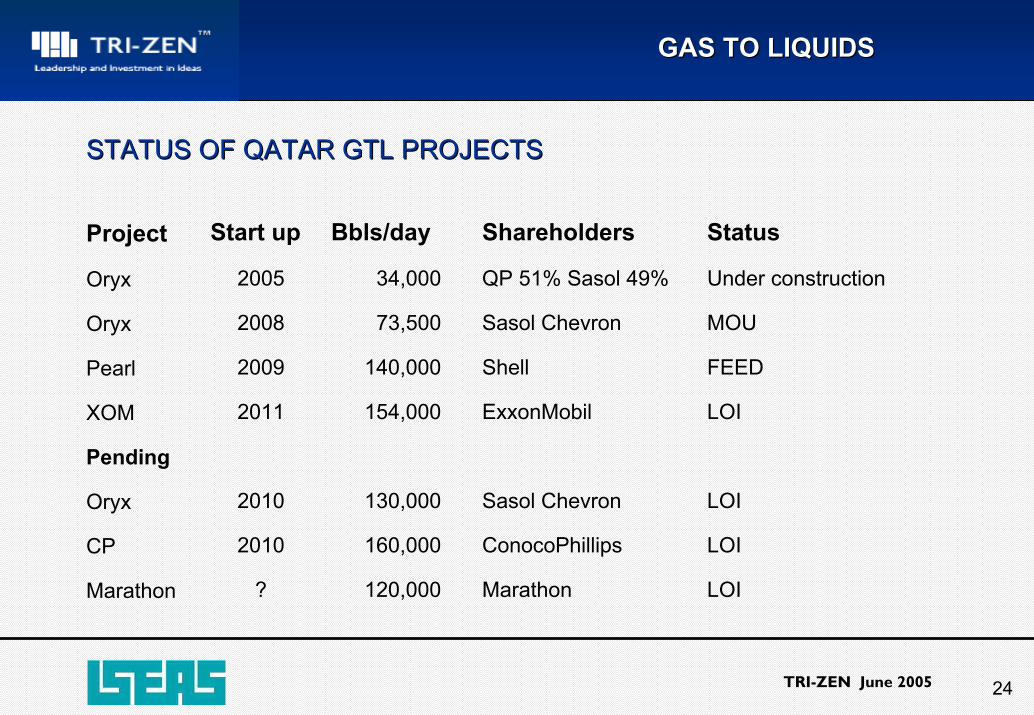

STATUS OF QATAR GTL PROJECTSSTATUS OF QATAR GTL PROJECTS

LOI Marathon120,000?Marathon

LOI ConocoPhillips160,0002010CP

LOI Sasol Chevron130,0002010Oryx

Pending

LOI ExxonMobil154,0002011XOM

FEED Shell140,0002009Pearl

MOU Sasol Chevron73,5002008Oryx

Under construction QP 51% Sasol 49%34,0002005Oryx

StatusShareholdersBbls/dayStart upProject

25

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

North Field

ORYX GTLORYX GTL

Ras Laffan

Doha

Fully integrated project: “From Reservoir to Market’

Phase 1 Qatar Petroleum 51%, Sasol 49%

330 MMscf/d well head gas

34,000 b/d GTL products

Commissioning late 2005

Phase 2. Additional 74 mbcd incl baseoil (2008) (Sasol/Chevron)

Capital costs to implement phase I ~ US$ 1 bn

EthanePropaneButaneCondensateSulphurGTL NaphthaGTL DieselWater

26

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

North Field

PEARL GTLPEARL GTL

Ras Laffan

Doha

Fully integrated project: “From Reservoir to Market’

Development & Production Sharing Agreement

1,600 MMscf/d well head gas

140,000 b/d GTL products

Substantial volumes LPG & condensate

End of decade start-up in two phases

Capital costs to implement ~ US$ 6 bn

EthanePropaneButaneCondensateSulphurGTL NaphthaGTL Fueln-ParaffinsGTL BaseoilsWater

27

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

North Field

EXXONMOBILEXXONMOBIL

Ras Laffan

Doha

Fully integrated project: “From Reservoir to Market’

Development & Production Sharing Agreement

1,800 MMscf/d well head gas

154,000 b/d GTL products

Will produce about 80 mbcd diesel fuel, 30 mbcd baseoil

Start-up in 2011

Capital costs to implement ~ US$ 7 bn

EthanePropaneButaneCondensateSulphurGTL NaphthaGTL Fueln-ParaffinsGTL BaseoilsWater

28

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

ESCRAVOS GTL PROJECTESCRAVOS GTL PROJECT

Profile of the Escravos GTL project in Nigeria

Same technology (Sasol) and size as the Oryx project in QatarDesigned to convert 300 mill cubic ft per day of gas to 34,000 b/d naphtha and dieselShareholders Chevron 75%, NNPC 25%$1.7 bn engineering, design & procurement contract awarded in April 2005 to Team JKS (Japan Gas, KBR & Snamprogetti)Commercial production planned for 2009

29

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

GTL PRODUCTS GTL PRODUCTS –– WHAT ARE THEY?WHAT ARE THEY?

Can produce LPG, naphtha, kerosene, diesel, baseoil and waxes, but typical yield is likely to be:

Naphtha 20%

Fuel (diesel) 60%

Baseoil 20%

ExxonMobil AGC-21 process

30

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

GTL PRODUCTS GTL PRODUCTS –– THE DREAM BARRELTHE DREAM BARREL

Fuel oil, 20%

Mid dists, 40%

Gasoline, 27%

LPG, 3%

Baseoil 0-30%

Mid dists, 50-75%

Naphtha 15-25%

Crude compared with GTL product yield

CRUDE GTL

Produces very high quality products

High yield of the high added value products – baseoil & waxes

Very flexible product yield – could produce 75% fuel (clean diesel)

No low margin products such as fuel oil

Can be used to upgrades other low margin products such as FCC heavy cycle oil into higher margin diesel

31

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

GTL PRODUCTS GTL PRODUCTS -- NAPHTHANAPHTHA

Characteristics – highly paraffinic with very low sulphur, naphthenes & aromatics Paraffin content typically over 95% which far exceeds the paraffin content of a typical light or full range naphthaPremium feedstock for steam crackers used to produce petrochemicals Low aromatics means product is not suitable for the production of gasoline Market

Strong growth in Asia makes this a particularly attractive market. High level of petchem investment in China/India/Middle East

32

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

Excellent quality:No sulphurHigh cetane Very low particulates & aromatics

A very clean sulphur free fuel Meets or exceeds all existing environmental specificationsCan be used in its pure form in existing engines as a low emission fuel but main use will be as blend-stock in refinery production 25-30% blends with conventional diesel give disproportionately high reduction in emissions

-12-17Cloud point deg C8171Flash point deg C

0.780.84Specific gravity<10330Sulphur ppm7445Cetane number

GTL FuelGasoil

Superior gasoil quality

Average emission benefits 100 % GTL:•Particulates 40% lower

•Nitrogen oxides 5% lower

•Hydrocarbon 60% lower

•Carbon monoxide 75% lower

GTL FUELGTL FUEL

33

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

GTL THE FUEL FOR THE MOMENTGTL THE FUEL FOR THE MOMENT -- EMISSION STANDARDS FOR NEW VEHICLESEMISSION STANDARDS FOR NEW VEHICLES

E 4E 3Euro 2Euro 1Vietnam (diesel)

Euro 4Euro 3Euro 2Euro 1Thailand

Euro 4Euro 2Euro 1Singapore

Euro 1Philippines

Euro 4Euro 2Malaysia

Euro 2Euro 1Indonesia

Euro 3Euro 2Euro 1India (others)

Euro 4Euro 3Euro 2Euro 1India (main cities)

Euro 4Euro 3Hong Kong

Euro 3Euro 2Euro 1China (Others)

Euro 4Euro 3Euro 2 Euro 1China (BJ & SH

Euro 2 Euro 1Bangladesh

Euro 5 10 ppm sulpEuro 4 50 ppm sulpEuro 3 350 ppm sulpEU

10 ppm sulp50 ppm sulp500 ppm sulpJapan

15 ppm sulp500 ppm sulpUSA

GTL diesel exceeds all proposed emission standardsGTL Fuel

20102009200820072006200520042003200220012000

34

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

GTL FUELGTL FUELGlobal diesel market 15 mill b/dLargest market Europe (3.6 mill b/d) followed by Asia Pacific (3.3 mill b/d)Demand growing at about 4% p.a & forecast to reach 22.5 mill b/d by 2020Diesel vehicle market growing strongly in EuropeGTL fuel (diesel) already being marketed in Thailand, Greece, Germany & South AfricaTotal Qatar/Nigerian GTL fuel production 400-500 mbcd – less than 4% of demand

GTL Fue l as a % of Global Diese l Demand

Diesel

GTL Diesel

Can use existing transportation & storageinfrastructure.Can be used in diesel-electric hybrid vehicles

35

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

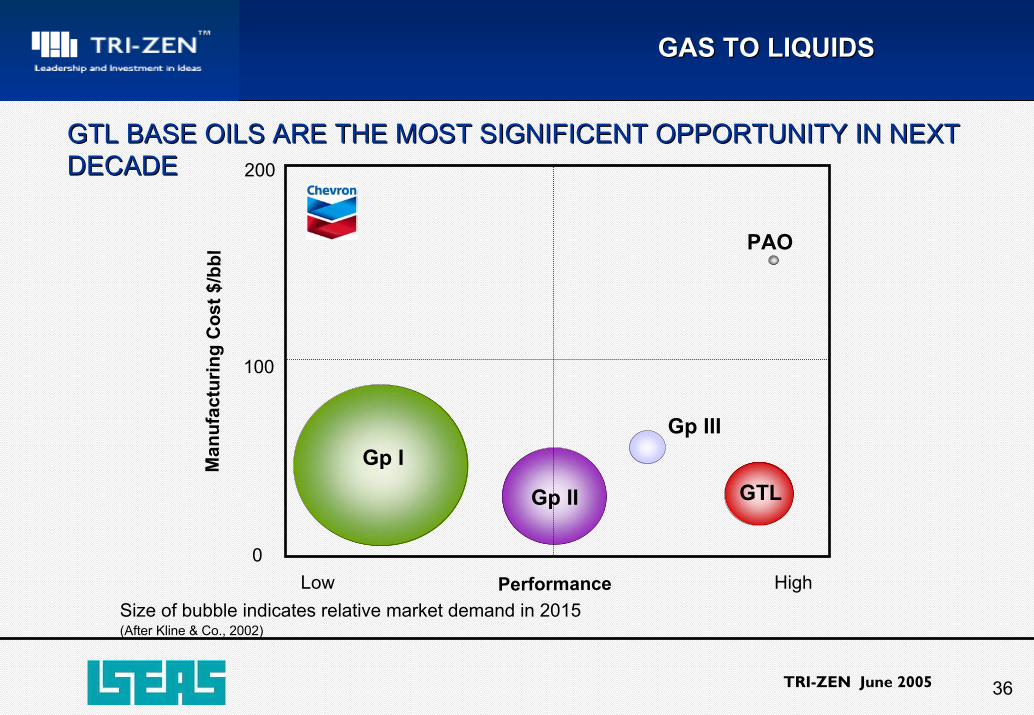

GTL BASEOILGTL BASEOIL

Extremely high quality baseoilsHigher VI than same viscosity PAOExcellent oxidation resistance – no sulphurExcellent thermal stabilityLess VI improver needed in formulations

Exceptional performance – a new generation of syntheticsSignificant volume potential – can meet all demandGTL competes directly with Group III and PAO rather than Group IIGTL based lubes offer better fuel economy, lower emissions and enable a lube marketer to offer “Fill for Life” lubes Enables zero sulphur HDEO and 5W, 0W PCMO

36

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

Man

ufac

t uri n

g C

ost $

/bbl

Performance

Gp III

PAO

0

100

200

Low High

Gp I

Gp II GTL

GTL BASE OILS ARE THE MOST SIGNIFICENT OPPORTUNITY IN NEXT GTL BASE OILS ARE THE MOST SIGNIFICENT OPPORTUNITY IN NEXT DECADEDECADE

Size of bubble indicates relative market demand in 2015(After Kline & Co., 2002)

37

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

BLENDING POWER OF GTL BASEOILSBLENDING POWER OF GTL BASEOILSV

ola

tili

ty

Group III

Group III+

PAO

GTL Base Oils

GTL Base Oils Can OUTPERFORM PAO

Low Temp Viscosity

38

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

15W-XX15W-XX

PREFERRED ENGINE OIL BLENDING COMBINATION IN THE FUTURE PREFERRED ENGINE OIL BLENDING COMBINATION IN THE FUTURE COULD BE GTL PLUS GROUP IICOULD BE GTL PLUS GROUP II

Low

Low High

Purit

y Pl

us V

isco

sity

Inde

x

High

Group IGroup I

Group IIGroup II

Group IIIGroup III

GTLGTL

0W-XX0W-XX

5W-XX5W-XX

10W-XX10W-XX

Optimal Engine Oil Blends

Optimal Engine Oil Blends

GTL and Group II can be

blended to meet equivalent

performance of Group II+

and Group III

Viscosity

39

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

GTL PRODUCTS GTL PRODUCTS –– POTENTIAL MARGINSPOTENTIAL MARGINS

GTL products can be offered at a premium to refined products due higher qualityGTL baseoils offer highest margin, but market limitedGTL fuel market unlimited and second best margin therefore most producers will probably produce 50-70% fuelStrength of naphtha premium depends on Asian demand growthKerosene can be produced but little incentive to do so unless Jet A1 specifications changeProduces excellent waxes, but market small

Potential quality premiums

01020304050

LPG Naphtha Diesel Baseoil

$ bb

l

Europe has traditionally offered the highest margin for premium baseoils followed by the USA

40

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

COULD SMALL BE BEAUTIFUL?COULD SMALL BE BEAUTIFUL?

Sasol Chevron, Shell and ExxonMobil are currently focusing on large plants where gas is plentifulBP, Syntroleum and Rentech are focusing on smaller simpler GTL plants that could monetise smaller stranded gas fields

Syntroleum uses air to produce the syngas. Removing the need for air separation units considerably reduces the cost and size of the plant Have developed a barge mounted GTL plant for quick access to small fieldsBP has built a demo plant in Alaska that also uses air to produce syngas. A radical difference with all other plants is that they have developed a compact reformer which improves conversion efficiency whilst reducing cost and plant footprint

41

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

WHAT NEXT?WHAT NEXT?

Will 30 GTL projects come to fruition – no, not in short termGTL projects are very capital intensive - $5-7 bnVery sophisticated new technology – can existing technology be scaled up?Financial community are in new territory – Oryx, the first PF GTL projectInterests of the gas producer must be aligned with the gas marketerMarket impact untestedMassive projects – very resource hungryHuge project management challenges

Focus is now on a few world class projects (+ 100 mbcd) to achieve the cost savings from scaling up. With that confidence and advances in technology it may be possible to scale down to make 30-50 mbcd projects viable Syntroleum BP & Rentech seeking to carve a niche with small, even mobile, projects

42

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

SUMMARYSUMMARY

The GTL process takes otherwise stranded (or flared) gas and converts it into high quality, high value petroleum products Could create several hundred billion barrels of petroleum productsEnables very small gas fields to be developed/monetisedIt compliments the LNG business by providing a completely different market for the gas (chemicals, transportation fuels and lubes)Its timely - technical advances and cost reductions are meeting market pullThe Fischer-Tropsch process produces products with almost no impurities opening up a whole range of new applications The initial well head treatment of the gas also produces condensate and LPGGTL naphtha can be used to provide a hydrogen source to hydrogen fuel cells Will not replace oil and refining, but compliments it and helps reduce the cost of producing high grade products

43

GAS TO LIQUIDS GAS TO LIQUIDS

TRI-ZEN June 2005

FINAL NOTEFINAL NOTEIn addition to natural gas, other feedstocks can be bio-mass, pet-coke, coal, coal waste,

and heavy residues such as asphaltenes from Canadian tar sands

Today we have discussed the GTL process and how its products will prove a significant replacement for conventionally produced oil, but GTL is only one of the processes that has come of age through a combination of research and development and higher oil prices

CTL, China is focussing on coal to gas and oil. Shell has already sold 12 coal gasification licences and Sasol is developing two 80,000 b/d projectsBTL. Bio-mass to liquids follows a similar route to producing high grade fuelsBio-oils are produced from biomass resources—agricultural residues, consumer wastes, or biomass specifically grown for energy uses

Now known collectively asXTLXTL

www.tri-zen.com