gas facilities

DESCRIPTION

oil & gasTRANSCRIPT

www.tri-zen.com

Commercial viability of FLNG projects: What does the future hold for the LNG industry

10th Asia Pacific LNG Summit, Singapore

25-26 June 2013

Tony Regan

Tri-Zen International Pte Ltd

www.tri-zen.com 2 2

Introduction to TRI-ZEN

TRI-ZEN is a consulting business focused on energy and utilities

We cover upstream & downstream, technical, commercial & financial

We offer a wide range of services:

Consulting

Strategy

Business Development

Project Management

Organizational Development

Alliances

Due diligence for M&A, project finance and IPO’s

Lead consultants located across Asia with a global extended network

Clients include the leading companies in energy and professional services based in Asia, Europe & North America

www.tri-zen.com Confidential

Engineering Associates

Uhde Energy & Power

Based in the UK and Hong Kong, Uhde Energy &Power, a member of the ThyssenKrupp Group, is a technical management consultancy providing multi-discipline technical support for major capital developments. The company has a significant track record of experience in the oil & gas, LNG and power sectors worldwide providing high quality project services to asset owners, operators and contractors in the oil, gas, LNG and renewables industries.

Core engineering design services focussed around process, facilities, utilities and structures with specialist services for due diligence and peer review, feasibility study, option appraisal, conceptual design and project management.

20 professional engineers, 20 LNG professionals

Experience gained from:

Over 30 LNG import terminals

Over 15 LNG liquefaction projects

13 Floating terminal projects (both FPSO’s and FSRU’s)

11 floating liquefaction projects (FLNG)

www.tri-zen.com Confidential 4

Drivers for FLNG

Drivers for FLNG

• Higher Gas / Energy Prices

• Cost effective way of monetising commercially challenged gas reserves

Fundamentals

• Design flexibility: re-deployable, can handle wide range of gases, can draw from multiple fields, location flexibility – offshore/inshore

• Problems with conventional LNG projects: land access, long delays getting permits, delays, cost overruns, shortage of key resources

Opportunity

• Can utilise proven technology (plenty of vendors)

Flexibility

• Potential for considerable cost savings: no offshore production & compression stations, no subsea pipeline to shore, no onshore plant/berths/utilities, and modular construction in shipyards

Financial

www.tri-zen.com Confidential

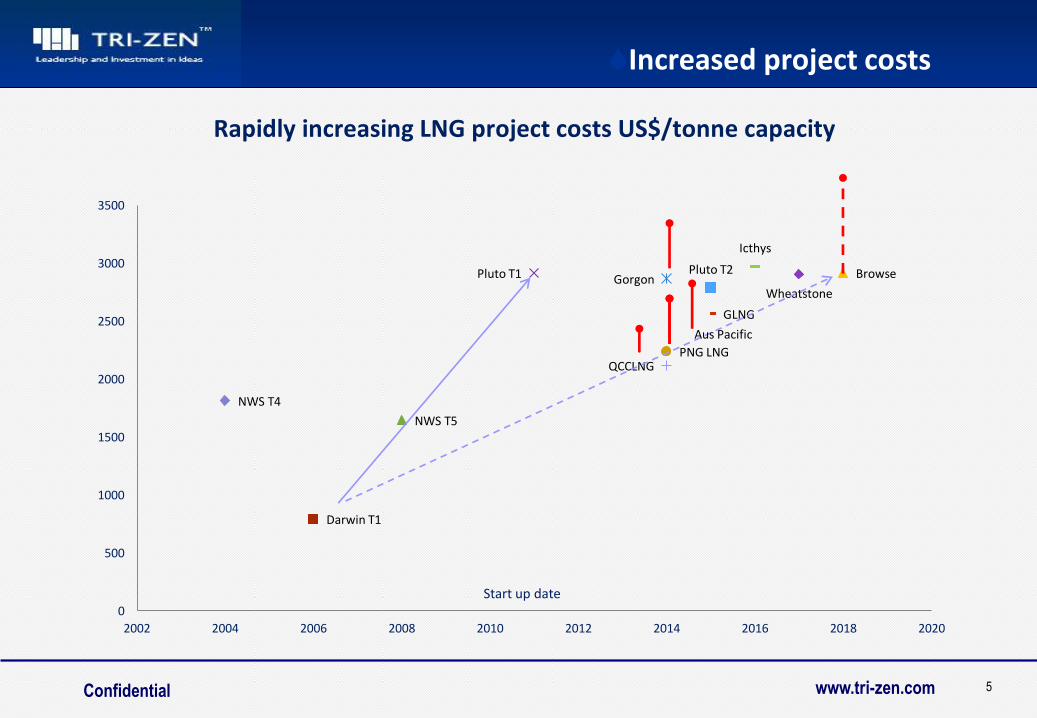

Rapidly increasing LNG project costs US$/tonne capacity

5

NWS T4

Darwin T1

NWS T5

Pluto T1 Gorgon

PNG LNG QCCLNG

GLNG

Icthys

Wheatstone

Pluto T2 Browse

0

500

1000

1500

2000

2500

3000

3500

2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Start up date

Aus Pacific

Increased project costs

www.tri-zen.com Confidential 6

The Opportunity for FLNG

Opportunity for FLNG

Capital Intensive

Costs

Land Permits

Development Time

LNG projects suffer from long project development time, high cost and substantial budget overruns. Floating LNG is an attractive concept to an LNG developer as it should enable reduced costs and substantially reduce the time taken to first LNG production

www.tri-zen.com Confidential 7

The LNG/FLNG Value Chain

The LNG Value Chain

FLNG fits neatly in the LNG chain replacing onshore

liquefaction with offshore liquefaction

Gas Production

LNG Production

LNG Shipping

Storage & Regas

www.tri-zen.com Confidential 8

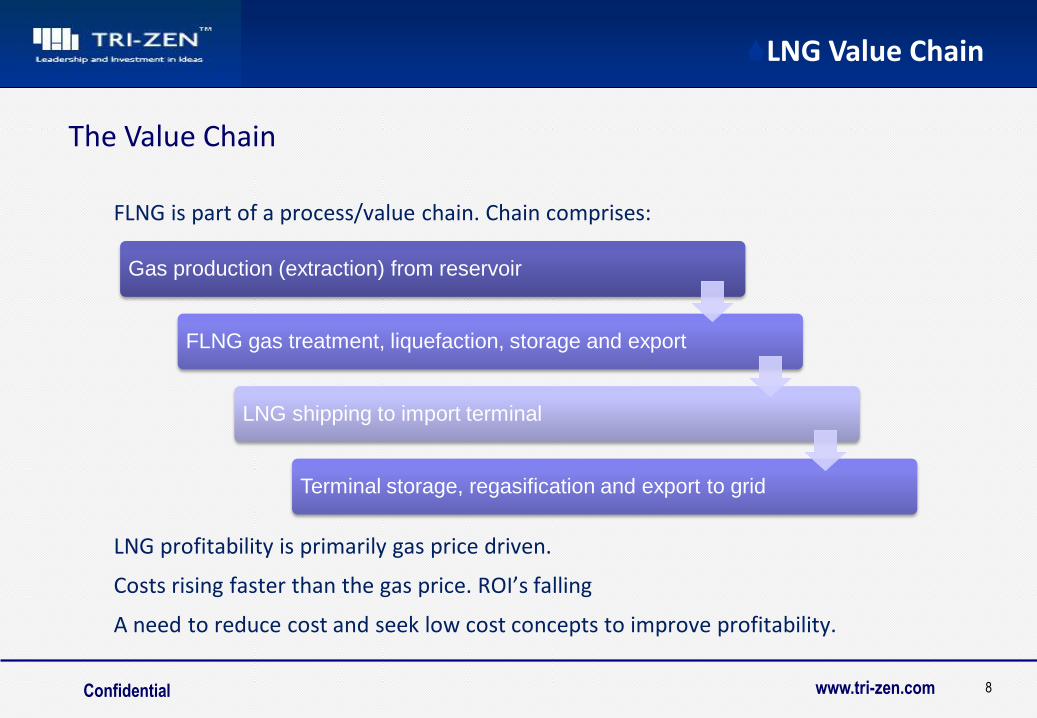

The Value Chain

LNG Value Chain

FLNG is part of a process/value chain. Chain comprises:

LNG profitability is primarily gas price driven.

Costs rising faster than the gas price. ROI’s falling

A need to reduce cost and seek low cost concepts to improve profitability.

Gas production (extraction) from reservoir

FLNG gas treatment, liquefaction, storage and export

LNG shipping to import terminal

Terminal storage, regasification and export to grid

www.tri-zen.com Confidential

Projects under construction

9

Leader Topsides LNG Hull Storage Project status Location

(Constructor) Liquefaction mtpa Containment m3 Project

Shell Technip 3.6 Barge 220,000 + FEED completed 2009 Australia

(Samsung) Shell DMR Membrane 90,000 LPG + Sanctioned May 2011 Prelude

126,000 Condensate Start Up 2017

Petronas Technip/Linde 1.2 Barge FEED completed 2012 Malaysia

(DSME) MR Membrane Sanctioned 2012 Sarawak

Start up Q4 2015

Exmar Black & Veatch 0.5 Barge 16,100 + Sanctioned 2012 Colombia

(Wison) SMR floating storage Start up Q1 2015 Pacific Rubiales

www.tri-zen.com Confidential

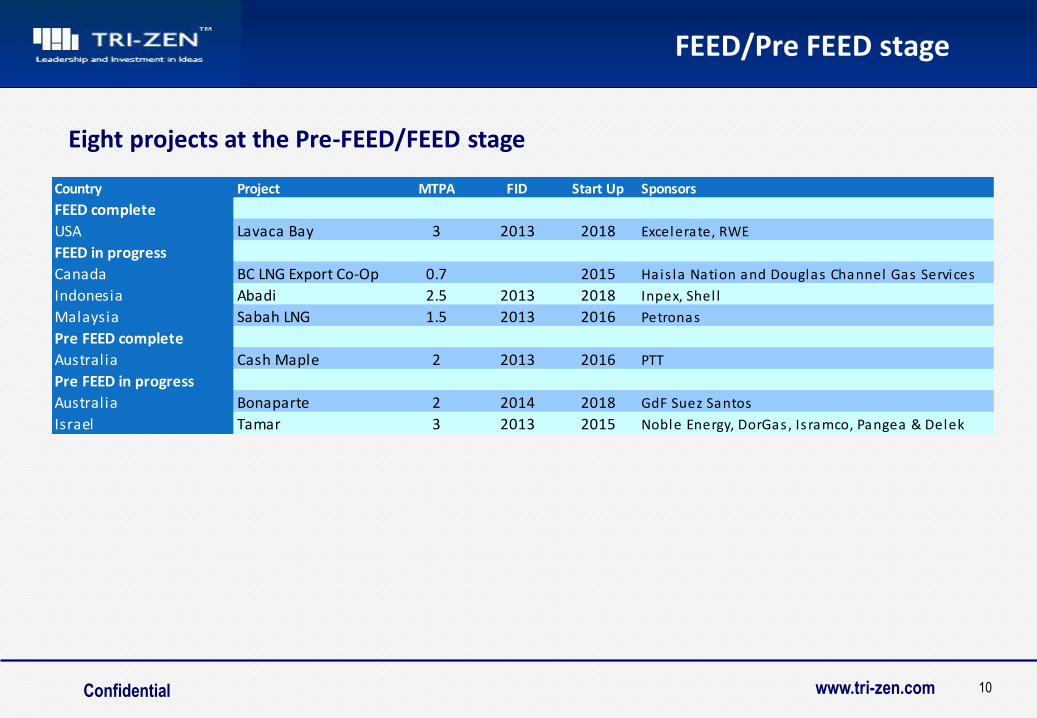

FEED/Pre FEED stage

10

Country Project MTPA FID Start Up Sponsors

FEED complete

USA Lavaca Bay 3 2013 2018 Excelerate, RWE

FEED in progress

Canada BC LNG Export Co-Op 0.7 2015 Hais la Nation and Douglas Channel Gas Services

Indonesia Abadi 2.5 2013 2018 Inpex, Shel l

Malaysia Sabah LNG 1.5 2013 2016 Petronas

Pre FEED complete

Australia Cash Maple 2 2013 2016 PTT

Pre FEED in progress

Australia Bonaparte 2 2014 2018 GdF Suez Santos

Israel Tamar 3 2013 2015 Noble Energy, DorGas , Is ramco, Pangea & Delek

Eight projects at the Pre-FEED/FEED stage

www.tri-zen.com

SBM & Golar LNG;

Considering conversions – expected to be 6-12 months shorter schedule than new build;

0.5- 2.0 mtpa LNG

Both smaller scale - probably focused towards smaller developers;

Golar – FEED being done by Keppel

3 Possible Vessel Conversions;

Contract Value of $600m Quoted;

SBM - Generic pre-FEED complete

11

Unconventional FLNG

www.tri-zen.com Confidential

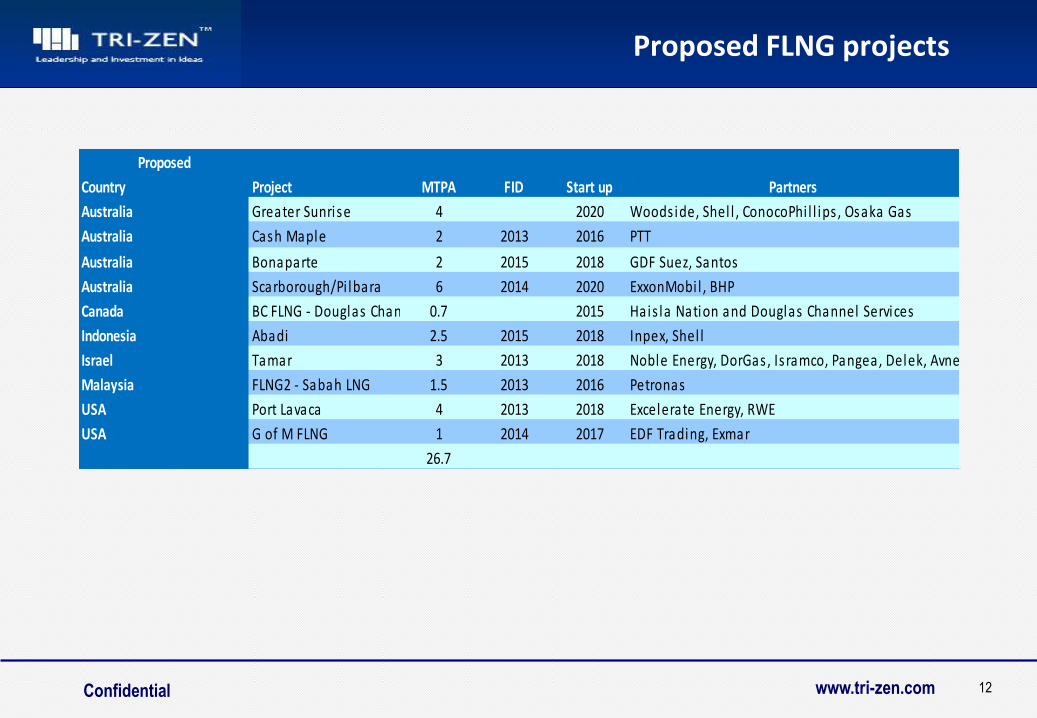

Proposed FLNG projects

12

Proposed

Country Project MTPA FID Start up Partners

Australia Greater Sunrise 4 2020 Woods ide, Shel l , ConocoPhi l l ips , Osaka Gas

Australia Cash Maple 2 2013 2016 PTT

Australia Bonaparte 2 2015 2018 GDF Suez, Santos

Australia Scarborough/Pi lbara 6 2014 2020 ExxonMobi l , BHP

Canada BC FLNG - Douglas Channel 0.7 2015 Hais la Nation and Douglas Channel Services

Indonesia Abadi 2.5 2015 2018 Inpex, Shel l

Israel Tamar 3 2013 2018 Noble Energy, DorGas , Is ramco, Pangea, Delek, Avner

Malaysia FLNG2 - Sabah LNG 1.5 2013 2016 Petronas

USA Port Lavaca 4 2013 2018 Excelerate Energy, RWE

USA G of M FLNG 1 2014 2017 EDF Trading, Exmar

26.7

www.tri-zen.com Confidential

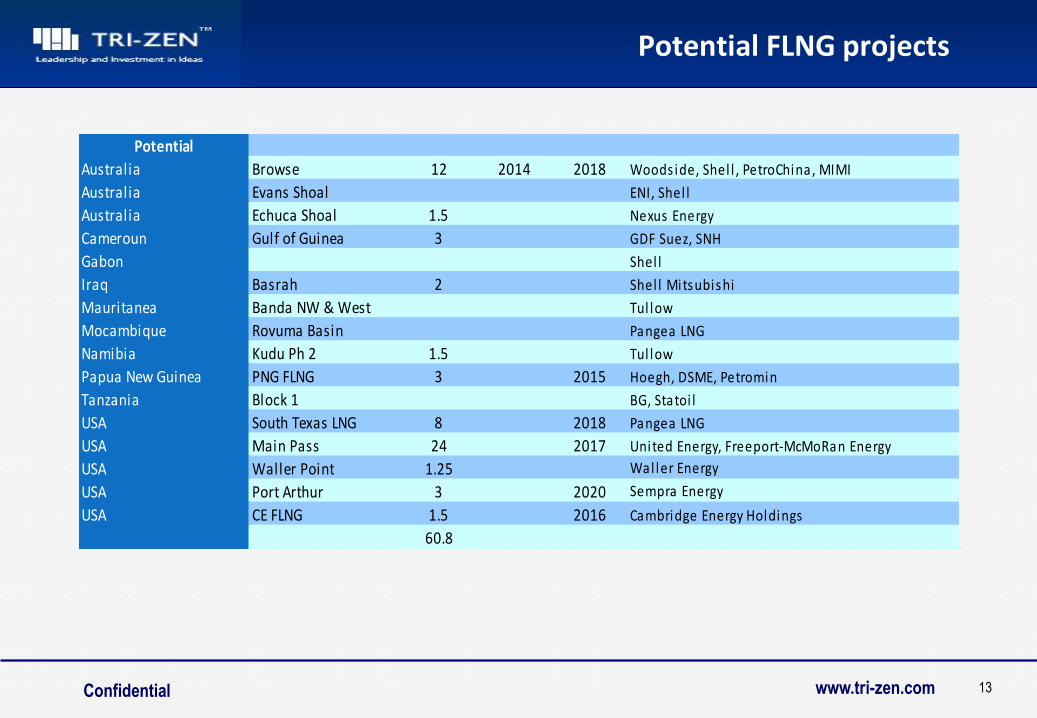

Potential FLNG projects

13

Potential

Australia Browse 12 2014 2018 Woods ide, Shel l , PetroChina, MIMI

Australia Evans Shoal ENI, Shel l

Australia Echuca Shoal 1.5 Nexus Energy

Cameroun Gulf of Guinea 3 GDF Suez, SNH

Gabon Shel l

Iraq Basrah 2 Shel l Mitsubishi

Mauritanea Banda NW & West Tul low

Mocambique Rovuma Basin Pangea LNG

Namibia Kudu Ph 2 1.5 Tul low

Papua New Guinea PNG FLNG 3 2015 Hoegh, DSME, Petromin

Tanzania Block 1 BG, Statoi l

USA South Texas LNG 8 2018 Pangea LNG

USA Main Pass 24 2017 United Energy, Freeport-McMoRan Energy

USA Waller Point 1.25 Waller Energy

USA Port Arthur 3 2020 Sempra Energy

USA CE FLNG 1.5 2016 Cambridge Energy Holdings

60.8

www.tri-zen.com

Liquefaction

Firm

Existing

Proposed

Tangguh, 7.6 mtpa

PNG LNG, 6.3 mtpa

PNG

AUSTRALIA NWS Train 1 - 5, 16.3 mtpa

Darwin, 3.7 mtpa

Greater Sunrise, 4 mtpa

Bonaparte, 2 mtpa

Ichthys, 8.4 mtpa

Prelude, 3.6 mtpa

Pluto, 4.3 mtpa

Gorgon, 15 mtpa

Scarborough, 6-7 mtpa

Wheatstone, 8.6 mtpa

Fisherman’s Landing, 1.5 mtpa

Australia Pacific, 7 mtpa

Arrow Energy 8 mtpa

Gladstone, 7.8 mtpa

Queensland Curtis, 8.5 mtpa

Echuca Shoals,

1.5 mtpa

Abadi, 2.5 mtpa

INDONESIA

TIMOR LESTE

Bontang, 23 mtpa

Cash Maple, 2 mtpa Evans Shoal,

Hoegh/Talisman, 2 mtpa

Donggi Senoro, 2 mtpa

Browse 12 mtpa

The way to go - FLNG

www.tri-zen.com Confidential

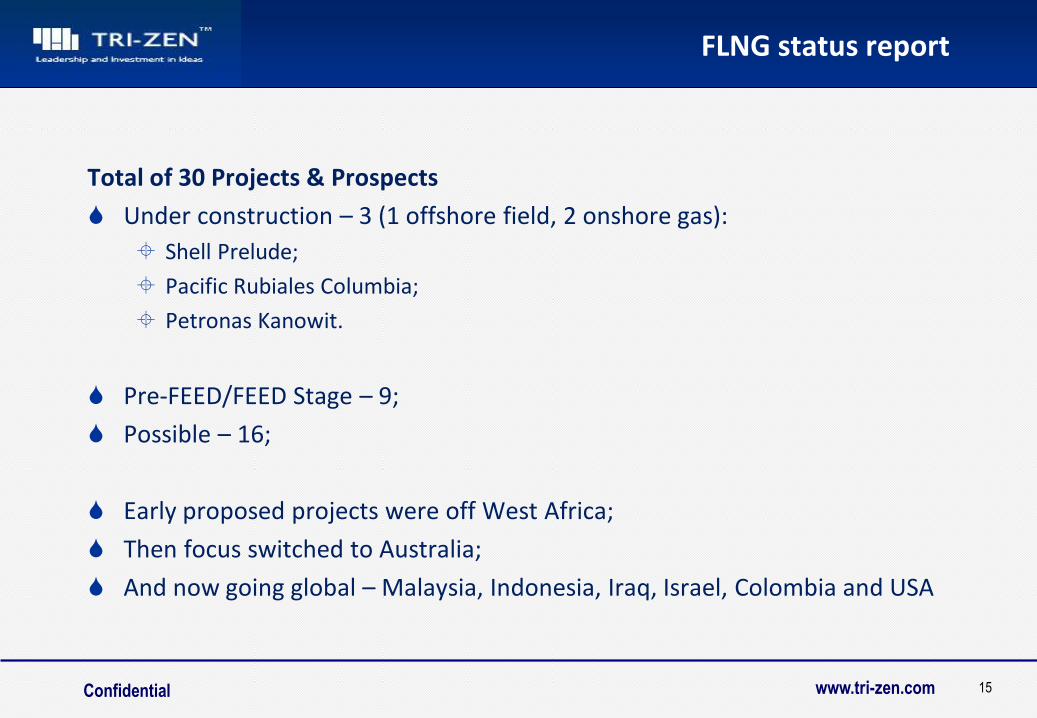

FLNG status report

Total of 30 Projects & Prospects

Under construction – 3 (1 offshore field, 2 onshore gas):

Shell Prelude;

Pacific Rubiales Columbia;

Petronas Kanowit.

Pre-FEED/FEED Stage – 9;

Possible – 16;

Early proposed projects were off West Africa;

Then focus switched to Australia;

And now going global – Malaysia, Indonesia, Iraq, Israel, Colombia and USA

15

www.tri-zen.com

R/P = 98

R/P = 265 R/P = 41

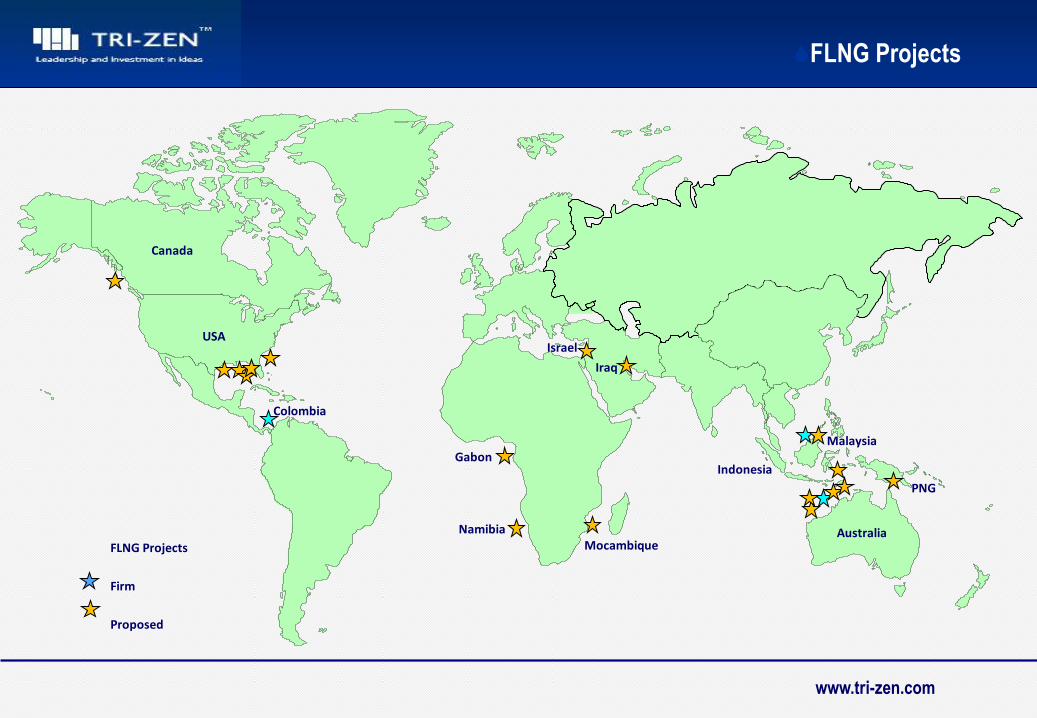

FLNG Projects

Firm

Proposed

Iraq

Canada

USA

Colombia

Gabon

Namibia Mocambique

Israel

Malaysia

Indonesia

Australia

PNG

FLNG Projects

www.tri-zen.com Confidential

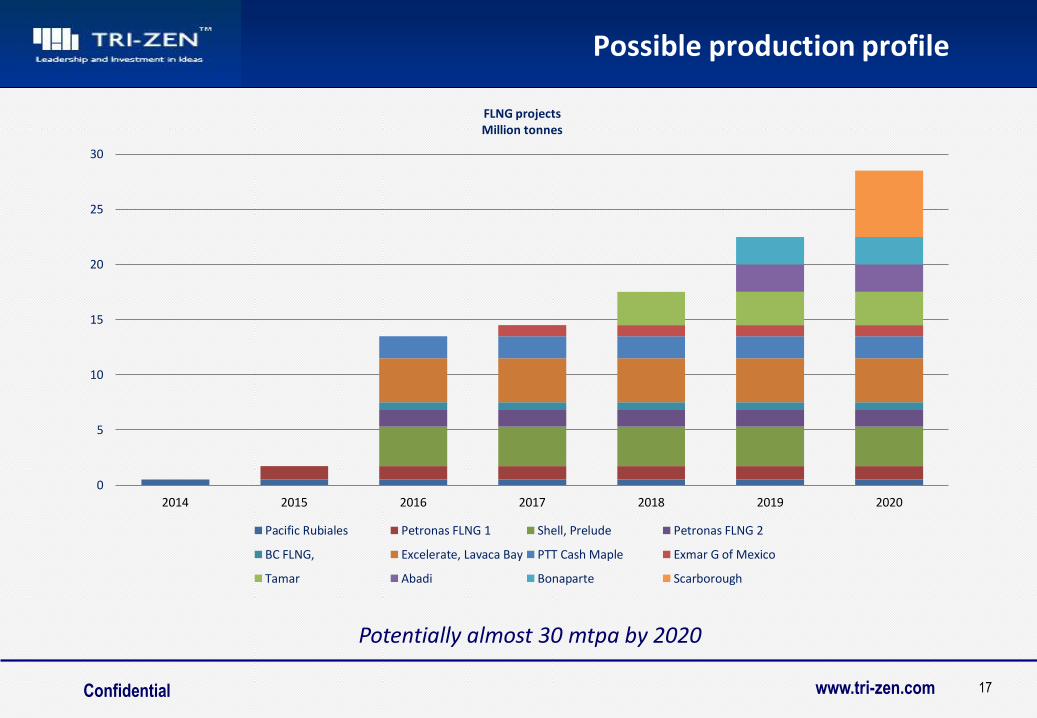

Possible production profile

17

0

5

10

15

20

25

30

2014 2015 2016 2017 2018 2019 2020

FLNG projects Million tonnes

Pacific Rubiales Petronas FLNG 1 Shell, Prelude Petronas FLNG 2

BC FLNG, Excelerate, Lavaca Bay PTT Cash Maple Exmar G of Mexico

Tamar Abadi Bonaparte Scarborough

Potentially almost 30 mtpa by 2020

www.tri-zen.com Confidential 18

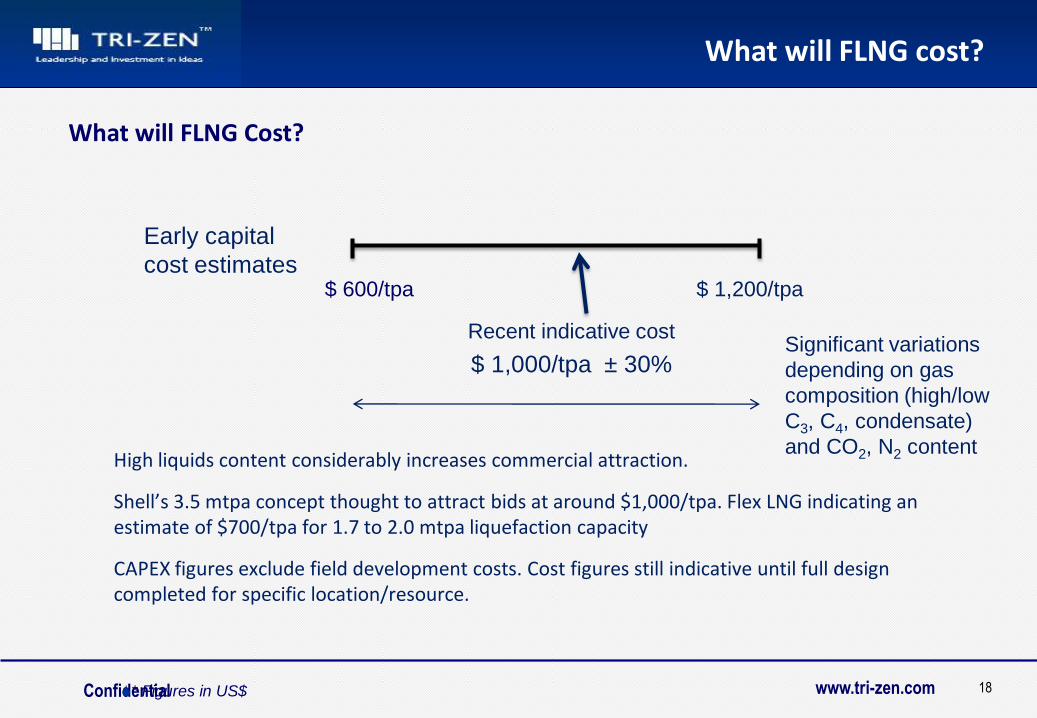

What will FLNG Cost?

What will FLNG cost?

High liquids content considerably increases commercial attraction.

Shell’s 3.5 mtpa concept thought to attract bids at around $1,000/tpa. Flex LNG indicating an estimate of $700/tpa for 1.7 to 2.0 mtpa liquefaction capacity

CAPEX figures exclude field development costs. Cost figures still indicative until full design completed for specific location/resource.

Early capital

cost estimates $ 600/tpa $ 1,200/tpa

Recent indicative cost

$ 1,000/tpa ± 30% Significant variations

depending on gas

composition (high/low

C3, C4, condensate)

and CO2, N2 content

* Figures in US$

www.tri-zen.com Confidential 19

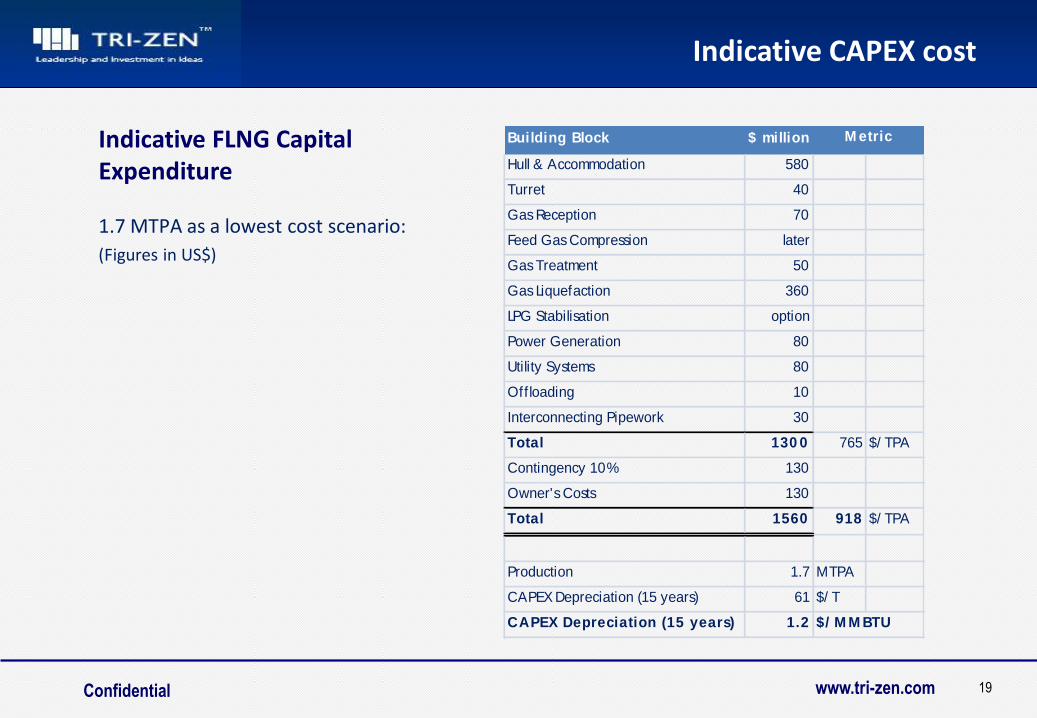

Indicative FLNG Capital Expenditure

Indicative CAPEX cost

1.7 MTPA as a lowest cost scenario:

(Figures in US$)

Building Block $ million

Hull & Accommodation 580

Turret 40

Gas Reception 70

Feed Gas Compression later

Gas Treatment 50

Gas Liquefaction 360

LPG Stabilisation option

Power Generation 80

Utility Systems 80

Offloading 10

Interconnecting Pipework 30

Total 130 0 765 $/ TPA

Contingency 10% 130

Owner's Costs 130

Total 1560 918 $/ TPA

Production 1.7 MTPA

CAPEX Depreciation (15 years) 61 $/ T

CAPEX Depreciation (15 years) 1.2 $/ M M BTU

M etric

www.tri-zen.com Confidential

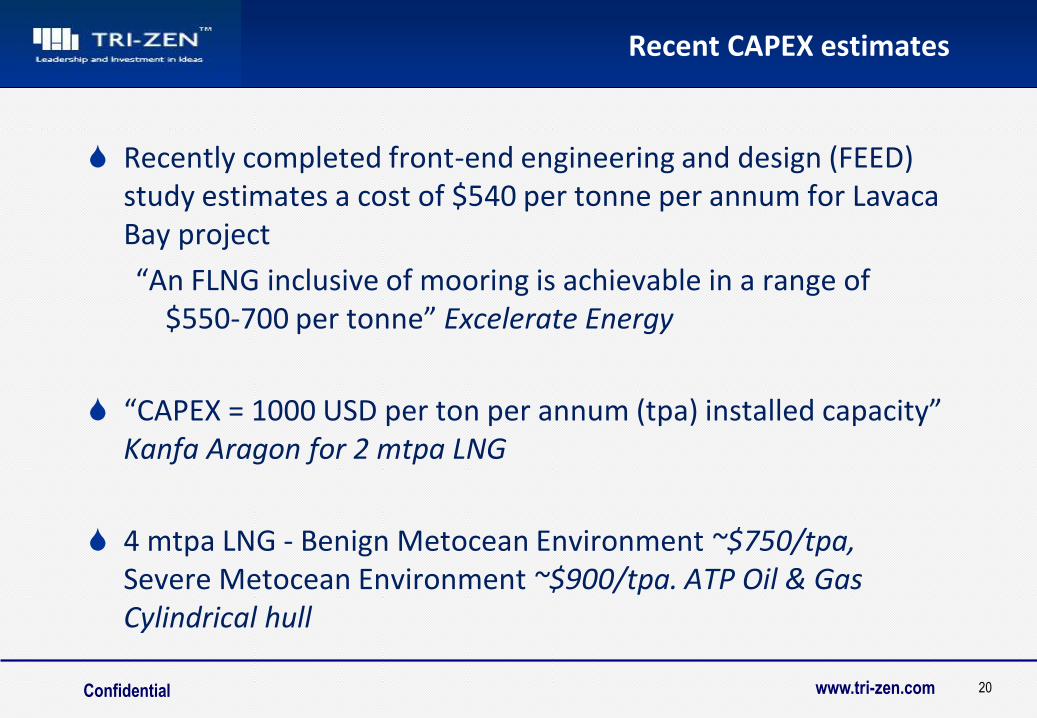

Recent CAPEX estimates

Recently completed front-end engineering and design (FEED) study estimates a cost of $540 per tonne per annum for Lavaca Bay project

“An FLNG inclusive of mooring is achievable in a range of $550-700 per tonne” Excelerate Energy

“CAPEX = 1000 USD per ton per annum (tpa) installed capacity” Kanfa Aragon for 2 mtpa LNG

4 mtpa LNG - Benign Metocean Environment ~$750/tpa, Severe Metocean Environment ~$900/tpa. ATP Oil & Gas Cylindrical hull

20

www.tri-zen.com Confidential

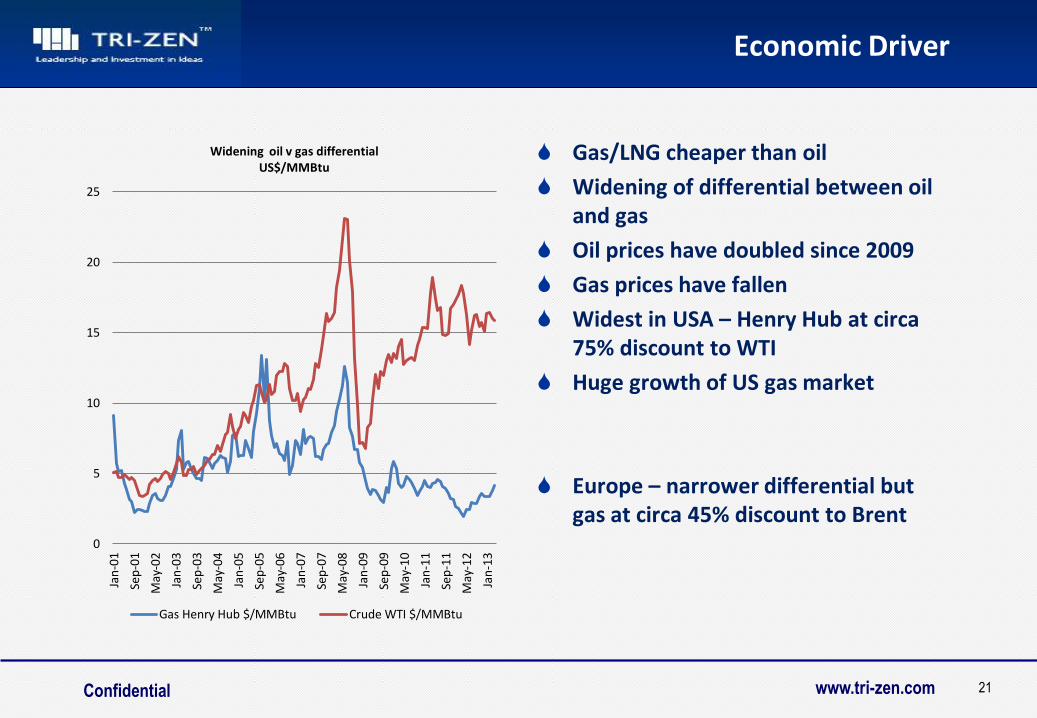

Economic Driver

Gas/LNG cheaper than oil

Widening of differential between oil and gas

Oil prices have doubled since 2009

Gas prices have fallen

Widest in USA – Henry Hub at circa 75% discount to WTI

Huge growth of US gas market

Europe – narrower differential but gas at circa 45% discount to Brent

21

0

5

10

15

20

25

Jan

-01

Sep

-01

May

-02

Jan

-03

Sep

-03

May

-04

Jan

-05

Sep

-05

May

-06

Jan

-07

Sep

-07

May

-08

Jan

-09

Sep

-09

May

-10

Jan

-11

Sep

-11

May

-12

Jan

-13

Widening oil v gas differential US$/MMBtu

Gas Henry Hub $/MMBtu Crude WTI $/MMBtu

www.tri-zen.com

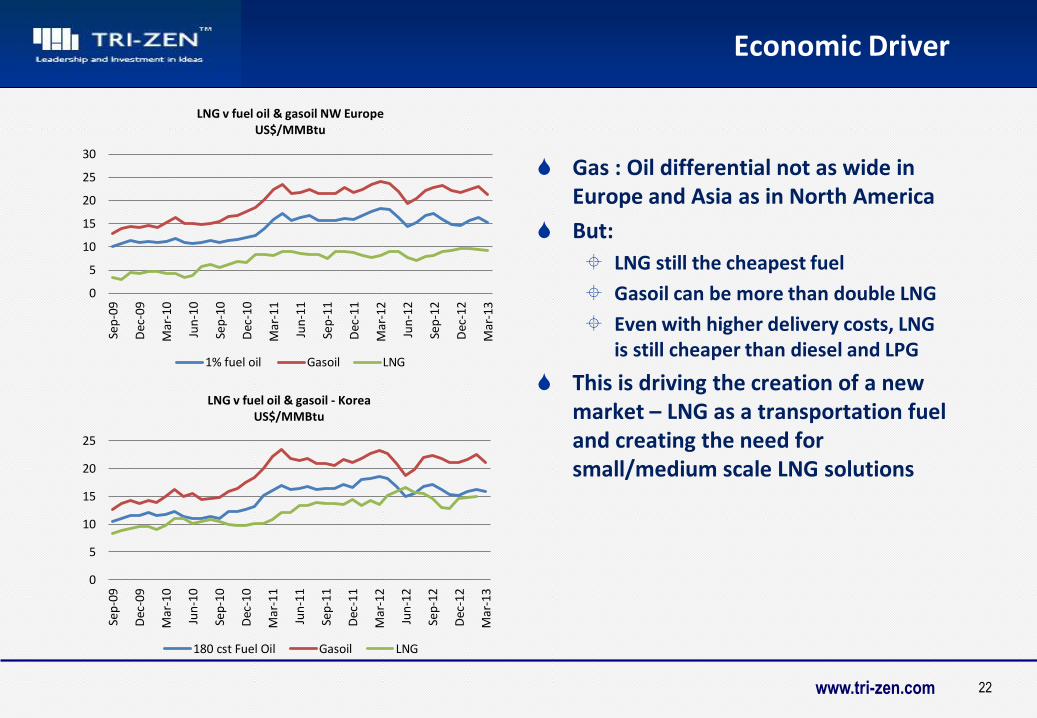

Gas : Oil differential not as wide in Europe and Asia as in North America

But:

LNG still the cheapest fuel

Gasoil can be more than double LNG

Even with higher delivery costs, LNG is still cheaper than diesel and LPG

This is driving the creation of a new market – LNG as a transportation fuel and creating the need for small/medium scale LNG solutions

22

Economic Driver

0

5

10

15

20

25

Sep

-09

Dec

-09

Mar

-10

Jun

-10

Sep

-10

Dec

-10

Mar

-11

Jun

-11

Sep

-11

Dec

-11

Mar

-12

Jun

-12

Sep

-12

Dec

-12

Mar

-13

LNG v fuel oil & gasoil - Korea US$/MMBtu

180 cst Fuel Oil Gasoil LNG

0

5

10

15

20

25

30

Sep

-09

Dec

-09

Mar

-10

Jun

-10

Sep

-10

Dec

-10

Mar

-11

Jun

-11

Sep

-11

Dec

-11

Mar

-12

Jun

-12

Sep

-12

Dec

-12

Mar

-13

LNG v fuel oil & gasoil NW Europe US$/MMBtu

1% fuel oil Gasoil LNG

www.tri-zen.com Confidential

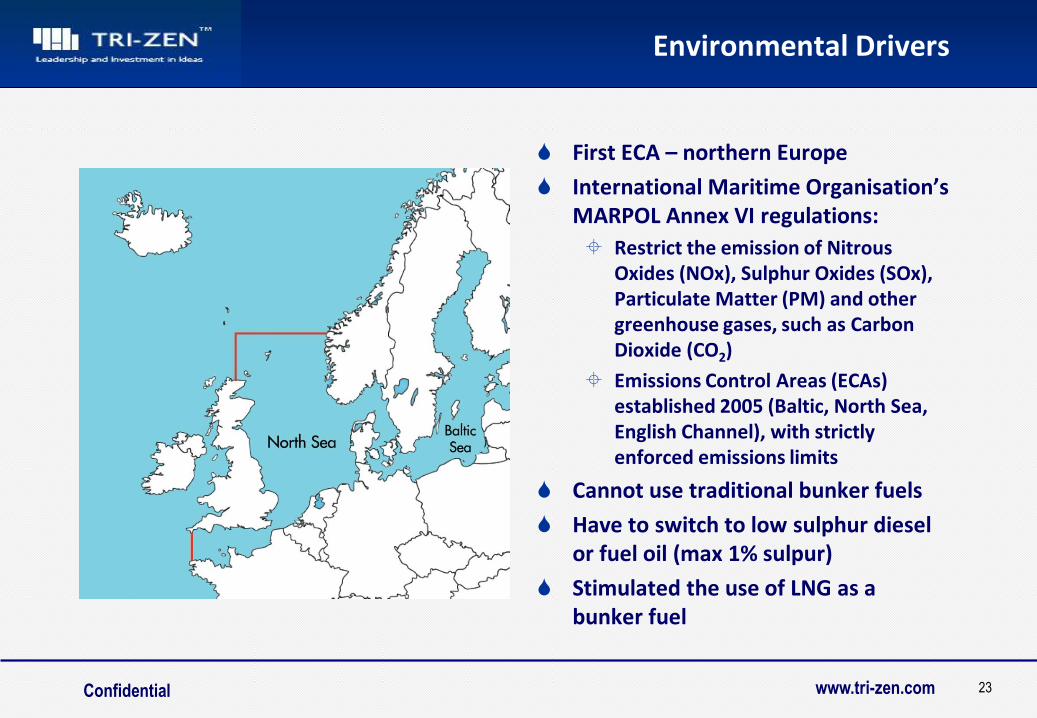

Environmental Drivers

First ECA – northern Europe

International Maritime Organisation’s MARPOL Annex VI regulations:

Restrict the emission of Nitrous Oxides (NOx), Sulphur Oxides (SOx), Particulate Matter (PM) and other greenhouse gases, such as Carbon Dioxide (CO2)

Emissions Control Areas (ECAs) established 2005 (Baltic, North Sea, English Channel), with strictly enforced emissions limits

Cannot use traditional bunker fuels

Have to switch to low sulphur diesel or fuel oil (max 1% sulpur)

Stimulated the use of LNG as a bunker fuel

23

www.tri-zen.com Confidential

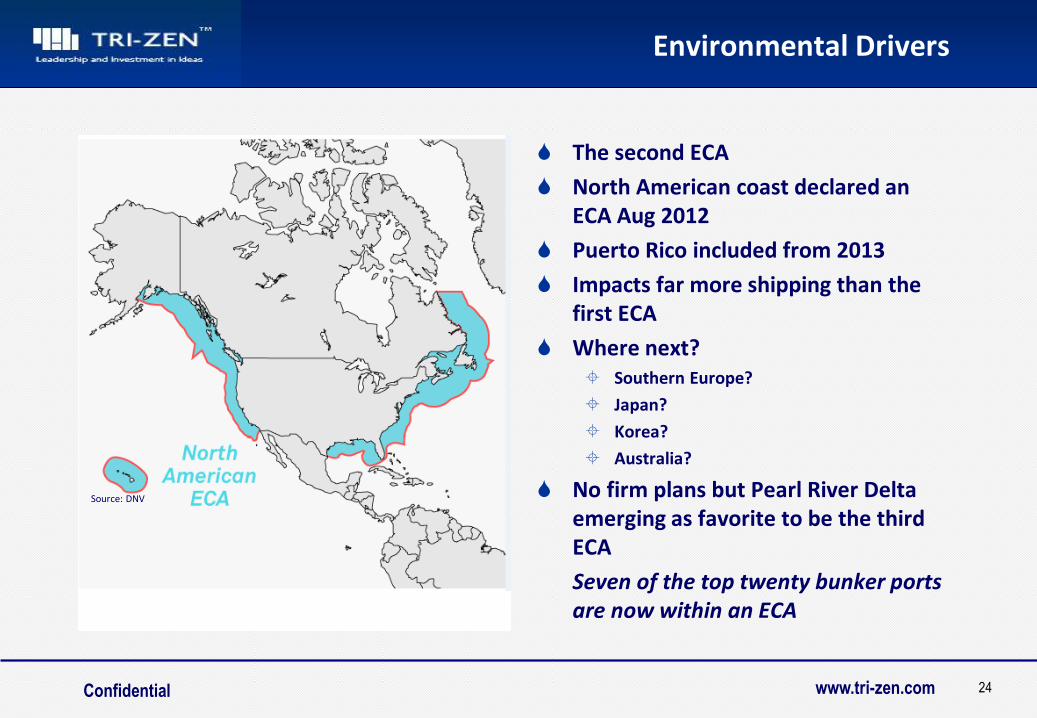

Environmental Drivers

The second ECA

North American coast declared an ECA Aug 2012

Puerto Rico included from 2013

Impacts far more shipping than the first ECA

Where next? Southern Europe?

Japan?

Korea?

Australia?

No firm plans but Pearl River Delta emerging as favorite to be the third ECA

Seven of the top twenty bunker ports are now within an ECA

24

Source: DNV

www.tri-zen.com

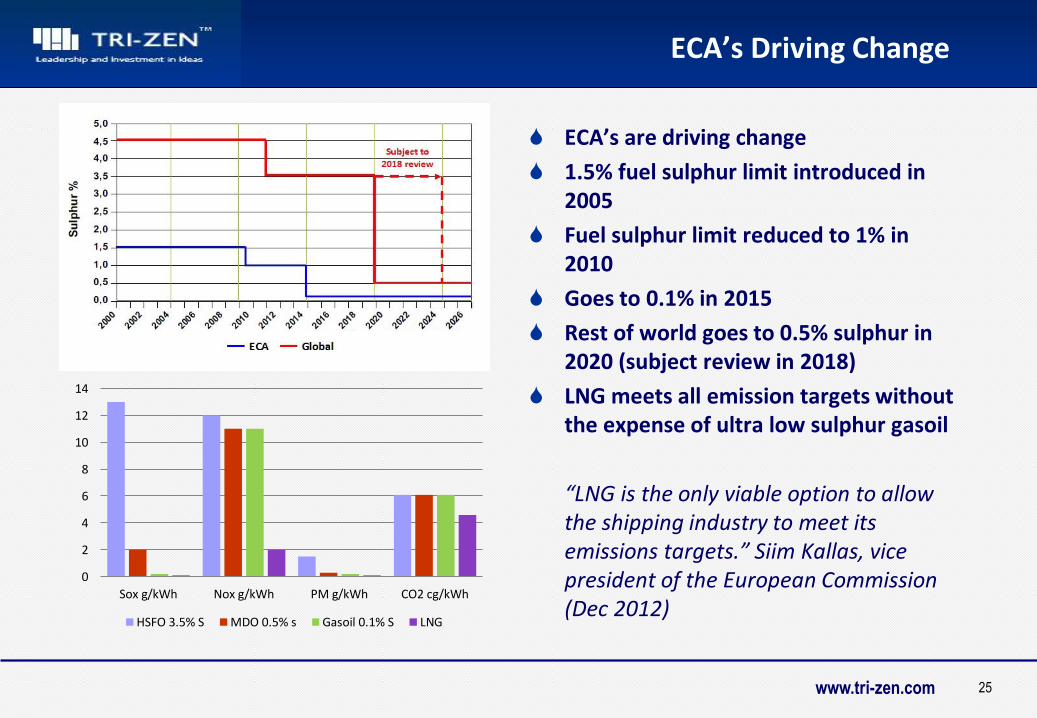

ECA’s Driving Change

ECA’s are driving change

1.5% fuel sulphur limit introduced in 2005

Fuel sulphur limit reduced to 1% in 2010

Goes to 0.1% in 2015

Rest of world goes to 0.5% sulphur in 2020 (subject review in 2018)

LNG meets all emission targets without the expense of ultra low sulphur gasoil

“LNG is the only viable option to allow the shipping industry to meet its emissions targets.” Siim Kallas, vice president of the European Commission (Dec 2012)

25

0

2

4

6

8

10

12

14

Sox g/kWh Nox g/kWh PM g/kWh CO2 cg/kWh

HSFO 3.5% S MDO 0.5% s Gasoil 0.1% S LNG

www.tri-zen.com

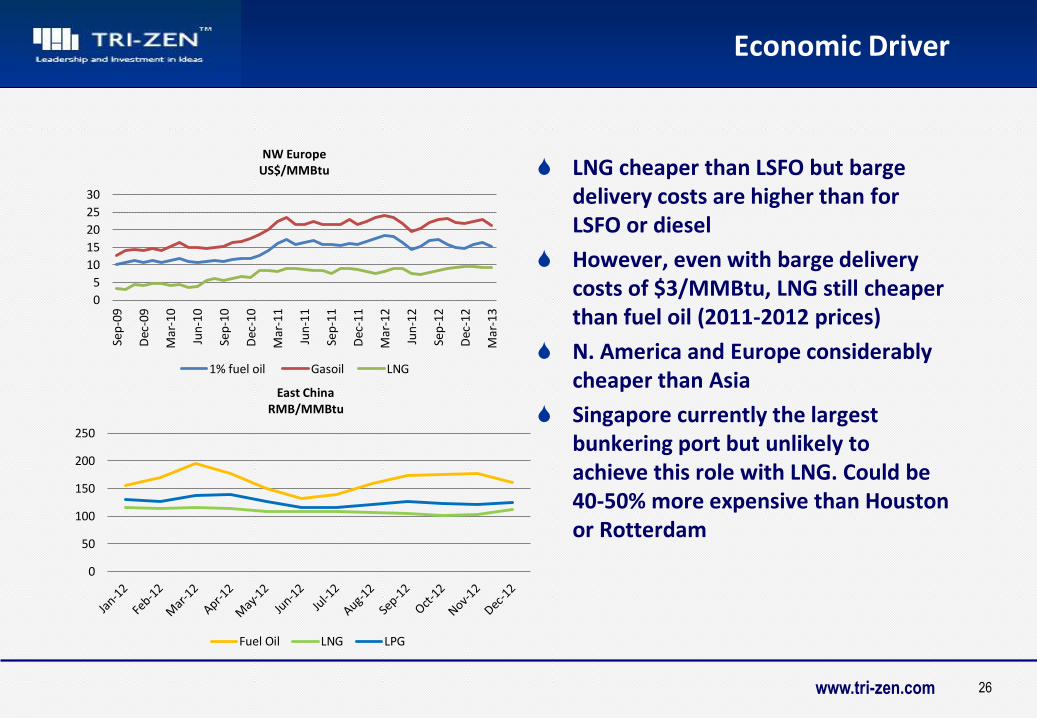

LNG cheaper than LSFO but barge delivery costs are higher than for LSFO or diesel

However, even with barge delivery costs of $3/MMBtu, LNG still cheaper than fuel oil (2011-2012 prices)

N. America and Europe considerably cheaper than Asia

Singapore currently the largest bunkering port but unlikely to achieve this role with LNG. Could be 40-50% more expensive than Houston or Rotterdam

26

0

50

100

150

200

250

East China RMB/MMBtu

Fuel Oil LNG LPG

Economic Driver

0

5

10

15

20

25

30

Sep

-09

Dec

-09

Mar

-10

Jun

-10

Sep

-10

Dec

-10

Mar

-11

Jun

-11

Sep

-11

Dec

-11

Mar

-12

Jun

-12

Sep

-12

Dec

-12

Mar

-13

NW Europe US$/MMBtu

1% fuel oil Gasoil LNG

www.tri-zen.com

America’s Natural Gas Highway

Clean Energy has opened 70 LNG fuelling stations on US highways, target of 150 by 2015

Shell and TravelCenters of America developing a U.S. nationwide network of LNG fueling centers

Shell is also developing LNG stations at Flying J truck stops in Alberta, Canada

FedEx plans to convert majority of its 90,000 vehicles to CNG/LNG

BNSF trialing LNG fuelled locomotives (rail companies second largest diesel user in US after military)

EnCana has launched mobile fuelling stations

Volvo & Shell collaborating in N. America & Europe

Shell building three small scale liquefaction plants to support fuelling network

27

North America

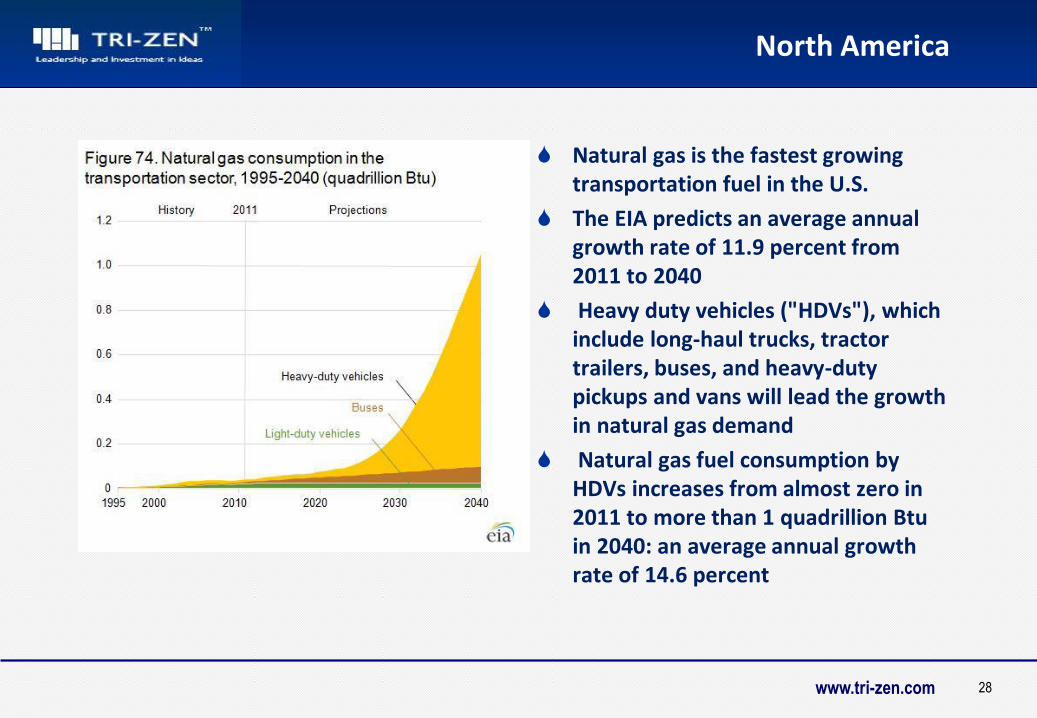

www.tri-zen.com

Natural gas is the fastest growing transportation fuel in the U.S.

The EIA predicts an average annual growth rate of 11.9 percent from 2011 to 2040

Heavy duty vehicles ("HDVs"), which include long-haul trucks, tractor trailers, buses, and heavy-duty pickups and vans will lead the growth in natural gas demand

Natural gas fuel consumption by HDVs increases from almost zero in 2011 to more than 1 quadrillion Btu in 2040: an average annual growth rate of 14.6 percent

28

North America

www.tri-zen.com Confidential

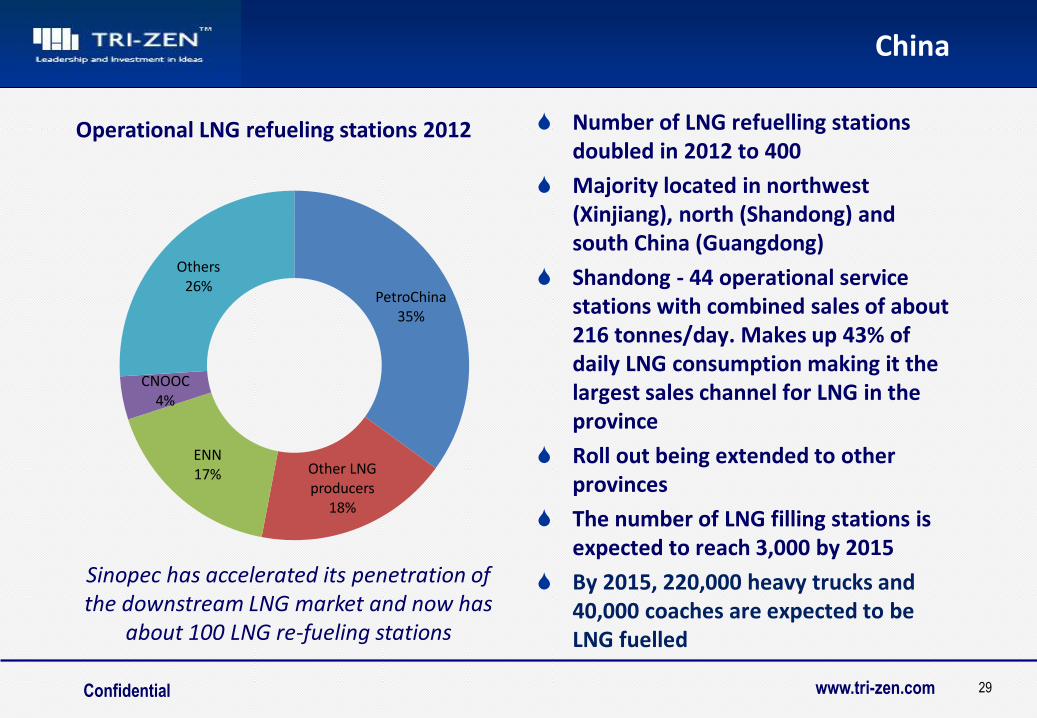

China

PetroChina 35%

Other LNG producers

18%

ENN 17%

CNOOC 4%

Others 26%

Number of LNG refuelling stations doubled in 2012 to 400

Majority located in northwest (Xinjiang), north (Shandong) and south China (Guangdong)

Shandong - 44 operational service stations with combined sales of about 216 tonnes/day. Makes up 43% of daily LNG consumption making it the largest sales channel for LNG in the province

Roll out being extended to other provinces

The number of LNG filling stations is expected to reach 3,000 by 2015

By 2015, 220,000 heavy trucks and 40,000 coaches are expected to be LNG fuelled

29

Sinopec has accelerated its penetration of the downstream LNG market and now has

about 100 LNG re-fueling stations

Operational LNG refueling stations 2012

www.tri-zen.com

First steps

Shell & BOC to install 8 LNG fuelling points in existing truck stops on busiest truck route in Australia by 2015 (Hume Highway)

EVOL LNG has opened refueling station at Caltex Wodonga, north-east of Melbourne. The first of five new stations planned for Victoria

Road trains – perfect market for LNG

Mining sector also a prime target

30

Australia

www.tri-zen.com Confidential

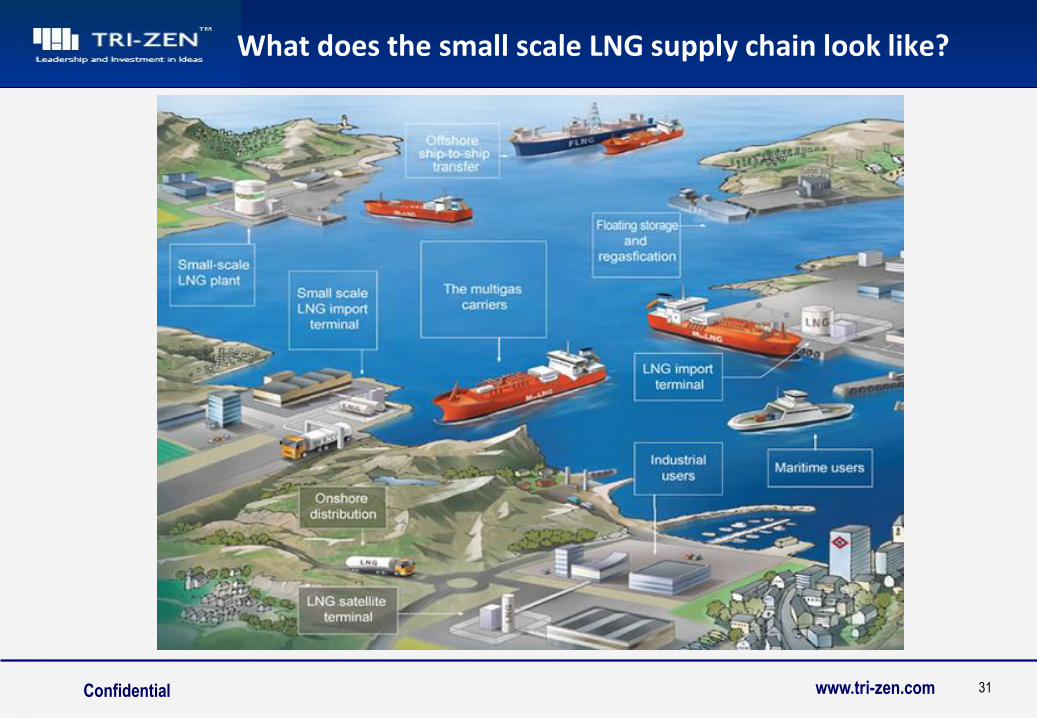

What does the small scale LNG supply chain look like?

31

www.tri-zen.com

LNG transportation fuel market being supported by local small scale LNG liquefaction plants

These liquefaction plant doesn’t have to be onshore

Why not small scale floating liquefaction?

Exmar LNG for Pacific Rubialas, Colombia – 0.5 mtpa

Should be cheaper, faster to build than onshore plants with fewer permitting issues

Indonesia – could be the perfect market for this

32

Small scale FLNG

www.tri-zen.com Confidential

How big is this market?

If all ships converted to LNG they would consume the (current) entire production of LNG

Difficult to forecast demand from bunker sector at this stage. An attempt: Base case – 653 LNG new builds by 2025 and LNG bunker demand of 24 million tonnes

High line – 1,963 LNG new builds by 2025 and LNG bunker demand of 66 million tonnes

Lloyds Register Aug 2012

Very early days – LNG as a transportation fuel taking off in China, USA and Australia. Others slower to catch on

Potentially it could be a huge market – why would any industrial plant/truck run on diesel (or LPG) if it could get LNG

Some recent estimates – Morgan Stanley estimate that LNG could displace between 1.5 and 4.5 mb/d of diesel and gasoline over next ten years.

Blue Sky scenario – 5.5 mb/d – about 225 million tonnes of LNG (global sales 2012 were 240 mill tonnes)

“The transportation fuel sector will be our largest LNG market” - PetroChina

33

www.tri-zen.com Confidential

Financing small scale FLNG projects

Can small scale LNG projects be financed?

Yes, banks generally like LNG and small scale will not be an exception

Just as with large scale LNG projects, the banks will want to see alignment:

Gas/LNG supply > production/distribution hardware > offtake agreement

The first and the last could be the biggest challenges in making small scale LNG projects “bankable”

Banks will want to be assured that there is adequate and reliable gas supply

Banks will want to be assured that there will be long term offtake agreements

Thus not going to be satisfied with spot deals. Will want to see long term supply agreements and long term offtake agreements – probably minimum ten years

34

www.tri-zen.com Confidential

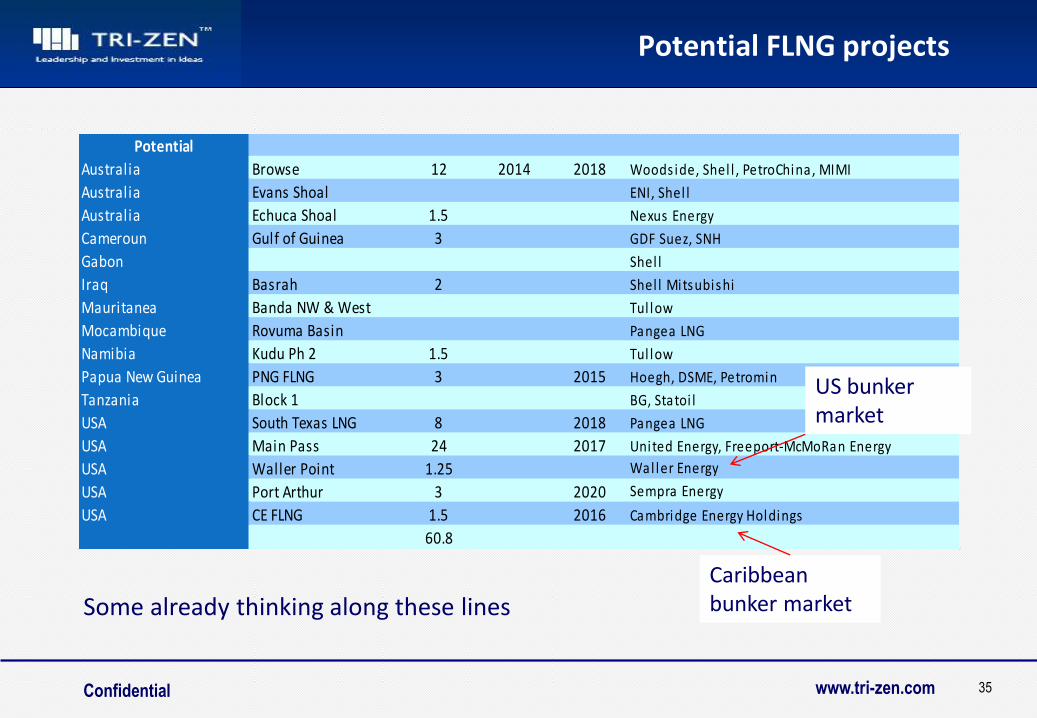

Potential FLNG projects

35

Potential

Australia Browse 12 2014 2018 Woods ide, Shel l , PetroChina, MIMI

Australia Evans Shoal ENI, Shel l

Australia Echuca Shoal 1.5 Nexus Energy

Cameroun Gulf of Guinea 3 GDF Suez, SNH

Gabon Shel l

Iraq Basrah 2 Shel l Mitsubishi

Mauritanea Banda NW & West Tul low

Mocambique Rovuma Basin Pangea LNG

Namibia Kudu Ph 2 1.5 Tul low

Papua New Guinea PNG FLNG 3 2015 Hoegh, DSME, Petromin

Tanzania Block 1 BG, Statoi l

USA South Texas LNG 8 2018 Pangea LNG

USA Main Pass 24 2017 United Energy, Freeport-McMoRan Energy

USA Waller Point 1.25 Waller Energy

USA Port Arthur 3 2020 Sempra Energy

USA CE FLNG 1.5 2016 Cambridge Energy Holdings

60.8

Some already thinking along these lines

US bunker market

Caribbean bunker market

www.tri-zen.com Confidential

Financing small scale LNG projects

Can small scale LNG projects be financed?

Yes, banks generally like LNG and small scale will not be an exception

Just as with large scale LNG projects, the banks will want to see alignment:

Gas/LNG supply > production/distribution hardware > offtake agreement

The first and the last could be the biggest challenges in making small scale LNG projects “bankable”

Banks will want to be assured that there is adequate and reliable gas/LNG supply

Banks will want to be assured that there will be long term offtake agreements

Thus not going to be satisfied with spot deals. Will want to see long term supply agreements and long term offtake agreements – probably minimum ten years

36

www.tri-zen.com Confidential

The End Users

LNG Fuelled … …

37

www.tri-zen.com 38

We add value

Strategy

Asset optimisation

Sector studies

Market studies

Forecasting

Commercial and technical studies

Commercial representation

New market entry

Detailed business cases

Project finance and management

Mergers & Acquisitions

Organisational Development

Based in Singapore with

consultants in:

Bangkok

Beijing

Hong Kong

Melbourne

Perth

London

Los Angeles

TRI-ZEN International Pte Ltd

Ocean Financial Centre 40-01, 10 Collyer Quay, Singapore 049315

Tel: 65 6254 4791 [email protected]