garage basics - jjins.com · garage basics - training for agents © western heritage insurance...

TRANSCRIPT

Garage BasicsTraining for Agents

Garage Basics Training for Agents

Learner Guide

Garage Basics—Training for Agents

Designed 01/2013

Last Revision Date 02/13/2013

© 2013 Western Heritage Insurance Company

Notice This publication is protected by copyright and is licensed for individual users only.

It is illegal to reproduce these materials or any part of them in any way, to share these materials, or to lease or rent them to anyone else.

Garage Basics - Training for Agents

© Western Heritage Insurance Company February 2013 iiii

Table of Contents

Introduction ..................................................................................................... 1

Overview and Objectives............................................................................... 1

Course Overview ....................................................................................... 1

Learning Objectives .................................................................................... 1

Benefits of Garage Products ............................................................................. 2

Comparing CGL and Garage .......................................................................... 2

Key Question ............................................................................................. 2

All-in-One Approach .................................................................................. 2

Garage Coverages and Exposures .................................................................... 3

Section I—Covered Autos .............................................................................. 3

Symbols ..................................................................................................... 3

Section II—Liability Coverage ........................................................................ 4

Liability—CGL as Compared to Garage....................................................... 4

Liability—Exclusions ................................................................................... 5

Liability—Limits of Insurance ...................................................................... 5

Liability—Coverages That Can Be Added by Endorsement .......................... 6

Liability—Med Pay ..................................................................................... 6

Section III—Garagekeepers Coverage............................................................. 7

Garagekeepers—Garage as Compared to Other Options ............................ 7

Garagekeepers—Comp as Compared to SCL .............................................. 7

Garagekeepers—Collision Coverage ........................................................... 7

Garagekeepers—Exclusions ........................................................................ 8

Garagekeepers—Limits of Insurance and Deductibles ................................. 8

Section IV—Physical Damage Coverage ......................................................... 9

Physical Damage—Comp as Compared to SCL ........................................... 9

Physical Damage—Collision Coverage ........................................................ 9

Physical Damage—Exclusions ................................................................... 10

Physical Damage—Limits of Insurance ...................................................... 11

Physical Damage—Premium Basis ............................................................ 11

Garage Basics - Training for Agents

© Western Heritage Insurance Company February 2013 iiiiiiii

Physical Damage—Deductible .................................................................. 11

Section VI—Definitions ................................................................................ 12

Important Definitions ............................................................................... 12

Knowledge Check ........................................................................................ 13

Instructions ............................................................................................... 13

Scenario ................................................................................................... 13

Questions ................................................................................................. 13

Risks That Belong on a Garage Form ............................................................. 17

Risks Eligible and Not Eligible for the Garage Coverage Form ....................... 17

Eligible and Ineligible Risks ....................................................................... 17

Knowledge Check ........................................................................................ 18

Instructions ............................................................................................... 18

Questions ................................................................................................. 18

Identifying Information for a Garage Application .......................................... 20

Information to Gather .................................................................................. 20

All Exposures ............................................................................................ 20

Auto Dealers Liability ............................................................................... 20

Auto Dealers Physical Damage ................................................................. 21

Nondealers Liability .................................................................................. 21

Garagekeepers ......................................................................................... 21

Conclusion ..................................................................................................... 22

Review of Learning Objectives ..................................................................... 22

Learning Objectives .................................................................................. 22

Garage Basics - Training for Agents

© Western Heritage Insurance Company February 2013 1111

Introduction

Overview and Objectives

Often agents shy away from requesting a garage policy simply because they feel they do not understand the coverage. This course will illustrate some of the similarities and differences between the garage form and the commercial general liability (CGL) coverage form and further define some of the unique coverages the garage form can provide.

As a result of this training, agents will be able to:

1. Explain the benefits of garage products.

− Distinguish between the general liability and garage products.

2. Discuss the coverages and exposures that are involved in a garage risk.

− Identify the main coverages on the garage form (liability, garagekeepers, physical damage).

− Explain the auto coverage symbols.

− Identify premises and products completed operations.

− Identify the auto exposure on a garage risk.

3. Identify risks that belong on a garage form.

− Identify risks that do not belong on a garage form.

4. Identify information to gather when underwriting a garage risk.

Additional notes:

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Course Overview

Learning Objectives

Garage Basics - Training for Agents

© Western Heritage Insurance Company February 2013 2222

Benefits of Garage Products

Comparing CGL and Garage

When determining if a risk would be better on the CGL coverage form or on a garage coverage form, the first question that should be asked is:

“Is there an auto exposure to this risk?”

The benefit of a garage policy form is that it provides liability coverage for both premises and products plus provides liability for “autos.”

Unlike a CGL policy, it can also include a variety of physical damage coverages like:

� Garagekeepers coverage—the care, custody, and control (C,C,C) of nonowned autos

� Dealer’s physical damage coverage – the physical damage coverage for dealer’s autos.

Autos used for personal, service, or commercial use also can be specifically scheduled under the garage coverage form.

Additional coverages can be added to the garage coverage form such as:

� Uninsured/underinsured motorist

� Personal injury protection

� Broadened coverage

With all of these options available the garage coverage form offers an all-in-one approach to cover your premises, products, and autos.

Additional notes:

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Key Question

All-in-One Approach

Garage Basics - Training for Agents

© Western Heritage Insurance Company February 2013 3333

Garage Coverages and Exposures

Section I—Covered Autos

Symbols shown on the Declaration page designate which “autos” are covered under the policy.

Symbol Description Of Covered Auto Designation Symbols

21 Any "Auto"

22 Owned "Autos" Only Only those "autos" you own (and for liability coverage any "trailers" you don't own while attached to power units you own). This includes those "autos" you acquire ownership of after the policy begins.

23 Owned Private Passenger "Autos" Only

Only the private passenger "autos" you own. This includes those private passenger "autos" you acquire ownership of after the policy begins.

24 Owned "Autos" Other Than Private Passenger "Autos" Only

Only those "autos" you own that are not of the private passenger type (and for liability coverage any "trailers" you don't own while attached to power units you own). This includes those "autos" not of the private passenger type you acquire ownership of after the policy begins.

25 Owned "Autos" Subject To No-Fault

Only those "autos" you own that are required to have no-fault benefits in the state where they are licensed or principally garaged. This includes those "autos" you acquire ownership of after the policy begins provided they are required to have no-fault benefits in the state where they are licensed or principally garaged.

26 Owned "Autos" Subject To A Compulsory Uninsured Motorists Law

Only those "autos" you own that because of the law in the state where they are licensed or principally garaged are required to have and cannot reject uninsured motorists coverage. This includes those "autos" you acquire ownership of after the policy begins provided they are subject to the same state uninsured motorists requirement.

27 Specifically Described "Autos"

Only those "autos" described in Item Nine of the Declarations for which a premium charge is shown (and for liability coverage any "trailers" you don't own while attached to a power unit described in Item Nine).

28 Hired "Autos" Only Only those "autos" you lease, hire, rent, or borrow. This does not include any "auto" you lease, hire, rent, or borrow from any of your "employees," partners (if you are a partnership), members (if you are a limited liability company), or members of their households.

29 Nonowned "Autos" Used In Your Garage Business

Any "auto" you do not own, lease, hire, rent, or borrow used in connection with your garage business described in the Declarations. This includes "autos" owned by your "employees" or partners (if you are a partnership), members (if you are a limited liability company), or members of their households while used in your garage business.

Table continued on next page

Symbols

Garage Basics - Training for Agents

© Western Heritage Insurance Company February 2013 4444

Symbol Description Of Covered Auto Designation Symbols

30 "Autos" Left With You For Service, Repair, Storage Or Safekeeping

Any customer's land motor vehicle or trailer or semitrailer while left with you for service, repair, storage, or safekeeping. Customers include your "employees," and members of their households, who pay for the services performed.

31 Dealers "Autos" (Physical Damage Coverages)

Any "autos" and the interests in these "autos" described in Item Seven of the Declarations.

Additional notes:

___________________________________________________________________

___________________________________________________________________

Section II—Liability Coverage

The CGL form offers:

� Coverage A—Bodily Injury and Property Damage Liability

The garage form offers:

� “Garage Operations”—Other Than Covered “Autos”—Liability—This covers “bodily injury” and “property damage” caused by an “accident” and resulting from “garage operations” other than the ownership, maintenance, or use of a covered “auto.”

� “Garage Operations”—Covered “Autos”—In addition to providing the premises and products liability, the garage form also provides “bodily injury” and “property damage” caused by an “accident” and resulting from “garage operations” involving the ownership, maintenance, or use of a covered “auto.”

Additional notes:

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Liability—CGL as Compared to Garage

Garage Basics - Training for Agents

© Western Heritage Insurance Company February 2013 5555

Exclusions on the garage form Liability section include:

� Expected or intended injury

� Contractual

� Workers’ compensation

� Property of others (C,C,C)

� Pollution

� Leased autos—Any covered "auto" while leased or rented to others. But this exclusion does not apply to a covered "auto" you rent to one of your customers while their "auto" is left with you for service or repair.

� Racing—“Covered "autos" while used in any professional or organized racing or demolition contest or stunting activity, or while practicing for such contest or activity. This insurance also does not apply while that covered "auto" is being prepared for such a contest or activity.”

� Work you performed—“Property damage” to “work you performed” if the “property damage” results from any part of the work itself or from the parts, materials, or equipment used in connection with the work.

Limits on the garage form Liability section include:

� Aggregate Limit of Insurance —“Garage Operations”—Other Than Covered “Autos”

� Limit of Insurance—“Garage Operations”—Covered “Autos”

Additional notes:

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Liability—Exclusions

Liability—Limits of Insurance

Garage Basics - Training for Agents

© Western Heritage Insurance Company February 2013 6666

Coverages that can be added to the garage form Liability section by endorsement include:

� Broadened coverage, which adds eight additional coverages:

1. Personal and advertising injury

2. Host liquor liability

3. Damage to rented premises

4. Incidental medical malpractice

5. Nonowned watercraft

6. Additional persons insured

7. Automatic liability coverage—newly acquired garage businesses (90 days)

8. Limited worldwide liability

� Uninsured/underinsured motorist, which provides compensatory damages to the insured (the damages must result from the ownership, maintenance, or use of an uninsured or underinsured motor vehicle)

� Personal injury protection, which usually covers all medical expenses, a percentage of work loss, and replacement services

On the garage form, med pay can be endorsed to cover:

� Premises —Covers medical expenses when the bodily injury occurs at a covered location

� Auto—Covers medical expenses when the bodily injury occurs while the insured is occupying an auto or occurs to a pedestrian hit by an auto

� Combined—Provides medical expenses for both premises and auto

Additional notes:

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Liability—Coverages That Can Be Added by Endorsement

Liability—Med Pay

Garage Basics - Training for Agents

© Western Heritage Insurance Company February 2013 7777

Section III—Garagekeepers Coverage

Legal liability or direct primary

� The garage form is written such that the insured must legally be liable for the loss to the customer’s auto while the insured is attending, servicing, repairing, parking, or storing it in the insured’s "garage operations.”

� Most companies offer a coverage option for direct primary for an increased premium, which states that the loss will be considered without regard to the insured’s legal liability.

Comprehensive (comp) coverage or specified causes of loss (SCL) coverage:

� Comp coverage—from any cause except:

(1) The "customer's auto's" collision with another object; or

(2) The "customer's auto's" overturn.

� SCL coverage—caused by:

(1) Fire, lightning, or explosion;

(2) Theft; or

(3) Mischief or vandalism.

Collision coverage—caused by:

(1) The "customer's auto's" collision with another object; or

(2) The "customer's auto's" overturn.

Additional notes:

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Garagekeepers—Garage as Compared to Other Options

Garagekeepers—Comp as Compared to SCL

Garagekeepers—Collision Coverage

Garage Basics - Training for Agents

© Western Heritage Insurance Company February 2013 8888

Exclusions on the garage form Garagekeepers section include:

� Contractual obligations

� Theft

� Defective parts

� Faulty work

� Additional exclusions that apply to:

− Tape decks or other sound reproducing equipment

− Tapes, records, and other sound reproducing devices

− Sound receiving equipment

− Radar detectors

− War

On the garage form Garagekeepers section:

� Limits—Limits are subject to each location.

� Deductibles—Sometimes to settle a claim or "suit," all or any part of the deductible will be paid. If this happens, the insured reimburses the company for the deductible or that portion of the deductible that we paid.

Additional notes:

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Garagekeepers—Exclusions

Garagekeepers—Limits of Insurance and Deductibles

Garage Basics - Training for Agents

© Western Heritage Insurance Company February 2013 9999

Section IV—Physical Damage Coverage

Comp coverage or SCL coverage:

� Comp coverage—from any cause except:

(1) The covered "auto's" collision with another object; or

(2) The covered "auto's" overturn.

� SCL coverage—caused by:

(1) Fire, lightning, or explosion;

(2) Theft;

(3) Windstorm, hail, or earthquake;

(4) Flood;

(5) Mischief or vandalism; or

(6) The sinking, burning, collision, or derailment of any conveyance transporting the covered "auto."

Collision Coverage—caused by:

(1) The covered "auto's" collision with another object; or

(2) The covered "auto's" overturn.

Additional notes:

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Physical Damage—Comp as Compared to SCL

Physical Damage—Collision Coverage

Garage Basics - Training for Agents

© Western Heritage Insurance Company February 2013 10101010

Exclusions on the garage form Physical Damage section include:

� Nuclear hazard

� War or military action

� Any covered "auto" leased or rented to others unless rented to one of your customers while their "auto" is left with you for service or repair

� Any covered "auto" while used in any professional or organized racing or demolition contest or stunting activity, or while practicing for such contest or activity

− We will also not pay for "loss" to any covered "auto" while that covered "auto" is being prepared for such contest or activity

� Your expected profit, including loss of market value or resale value

� "Loss" to any covered "auto" displayed or stored at any location not shown in Item Three of the Declarations if the "loss" occurs more than 45 days after your use of the location begins

� False pretense—We will not pay for "loss" to a covered "auto" caused by or resulting from:

a. Someone causing you to voluntarily part with it by trick or scheme or under false pretenses; or

b. Your acquiring an "auto" from a seller who did not have legal title.

Additional notes:

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Physical Damage—Exclusions

Garage Basics - Training for Agents

© Western Heritage Insurance Company February 2013 11111111

Key points about Limits of Insurance on the garage form Physical Damage section are:

� The most we will pay for "loss" to any one covered "auto" is the lesser of:

a. The actual cash value of the damaged or stolen property as of the time of "loss"; or

b. The cost of repairing or replacing the damaged or stolen property with other property of like kind and quality.

� An adjustment for depreciation and physical condition will be made in determining actual cash value in the event of a total "loss."

� If a repair or replacement results in better than like kind or quality, we will not pay for the amount of the betterment.

Dealer’s physical damage coverage can be written using either:

� Quarterly or monthly reporting premium basis

− Whichever method is used, the amount paid at the time of loss will be based on a 100% coinsurance limit.

� Nonreporting premium basis

Unlike the garagekeepers deductible, the dealer’s physical damage deductible is a first-party deductible. This means the amount of damages paid to the insured will be reduced by the amount of the deductible.

Additional notes:

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Physical Damage—Limits of Insurance

Physical Damage—Premium Basis

Physical Damage—Deductible

Garage Basics - Training for Agents

© Western Heritage Insurance Company February 2013 12121212

Section VI—Definitions

� Accident—includes continuous or repeated exposure to the same conditions resulting in "bodily injury" or "property damage."

� Auto—means a land motor vehicle, "trailer," or semitrailer.

� Bodily Injury—means bodily injury, sickness, or disease sustained by a person including death resulting from any of these.

� Customer’s auto—means a land motor vehicle, "trailer," or semitrailer lawfully within your possession for service, repair, storage, or safekeeping, with or without the vehicle owner's knowledge or consent. A "customer's auto" also includes any such vehicle left in your care by your "employees" and members of their households, who pay for services performed.

� Garage operations—means the ownership, maintenance, or use of locations for garage business and that portion of the roads or other accesses that adjoin these locations. "Garage operations" includes the ownership, maintenance, or use of the "autos" indicated in Section I of this coverage form as covered "autos." "Garage operations" also include all operations necessary or incidental to a garage business.

� Products—includes:

1. The goods or products you made or sold in a garage business; and

2. The providing of or failure to provide warnings or instructions.

� Property damage—means damage to or loss of use of tangible property.

� Work you performed—includes:

1. Work that someone performed on your behalf; and

2. The providing of or failure to provide warnings or instructions.

Additional notes:

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Important Definitions

Garage Basics - Training for Agents

© Western Heritage Insurance Company February 2013 13131313

Knowledge Check

Answer the following questions to check your knowledge of garage coverages and exposures. In some cases, there will be more than one correct answer; select all that apply. Be prepared to share your answers.

One Stop Auto Inc. is a used auto dealer and also provides warranty service work for the autos sold. Outside of the warranty work, One Stop has a full-service repair shop and a car wash for use by the business and its customers. One Stop also owns a tow truck used to pick up cars at auction and autos for the repair shop.

1. For liability, what symbols would be needed?

a. 22

b. 22 and 29

c. 23, 30, and 29

d. 22, 29, and 27

2. While washing his car, a customer slips and falls in the soapy water due to poor drainage and breaks his arm. What coverage would apply to this loss?

a. “Garage Operations”—Covered “Autos”

b. “Garage Operations”—Other Than Covered “Autos”

c. Uninsured Motorist

d. Garagekeepers

Additional notes:

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Instructions

Scenario

Questions

Garage Basics - Training for Agents

© Western Heritage Insurance Company February 2013 14141414

3. What symbol would apply to the loss described in Question 2.?

a. 22

b. 21

c. None

d. 27

4. While driving a scheduled 2008 flat bed to pick up a customer’s auto and bring it back to the shop to repair, the insured runs a stop sign and hits another vehicle. From Question 1., we know the policy has the symbols 22, 27, and 29 for liability. Which symbol applies to this auto?

a. 22

b. 27

c. 29

d. None, this is not a covered auto

5. One Stop provides a loaner auto from the sales lot to a customer while her car is being repaired. What coverages apply to this auto?

a. Liability only

b. Dealer’s physical damage only

c. Both liability and dealer’s physical damage

d. None, it is excluded under the leased autos exclusion

Additional notes:

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Garage Basics - Training for Agents

© Western Heritage Insurance Company February 2013 15151515

6. A customer brings in a race bike to have a performance adjustment. The next day when the customer is racing, the bike’s engine stalls causing an accident. What coverages apply to this auto?

a. Liability only

b. Garagekeepers only

c. Both liability and garagekeepers

d. None, it is excluded under the racing exclusion

7. After replacing a battery and installing new battery cables in a customer’s auto, the customer drove the auto home. Within several hours, the customer sees his auto on fire. The cause of loss is determined to be that the insured improperly installed the battery. What is covered under this loss?

a. No coverage since the auto is no longer in the insured’s care, custody, or control

b. Coverage for the entire loss as it was the insured’s faulty work that caused the loss

c. No coverage since it was the insured’s faulty work that caused the loss

d. None of the above

8. When storing customer autos overnight, our insured locks the autos in a building with a central station burglar alarm. One night someone breaks in and steals an auto before the police can respond. Our insured’s policy has garagekeepers legal liability, SCL, and collision coverages. Will this loss typically be covered?

a. No, this was written on a legal liability basis

b. Yes, theft is a covered cause of loss under the garagekeepers coverage

c. No, theft would only be covered under comp coverage

Additional notes:

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Garage Basics - Training for Agents

© Western Heritage Insurance Company February 2013 16161616

9. Two autos are held for sale at One Stop’s lot. They are taken to a separate location to be detailed. The cars will not be ready until the next day, so they are left at the second location overnight. When the insured returns in the morning, the autos have been stolen. The insured files a claim against the dealer’s physical damage coverage. The policy is written with comp and collision coverages and has symbol 31. Will this be covered?

a. Yes, theft is covered under comp coverage

b. No, this location is not scheduled on the policy

c. No, it was not the insured’s fault

d. Yes, the loss occurred less than 45 days after the use of the location began

10. One Stop purchases a used vehicle at auction and is notified by the police

a few days later that this is a stolen auto. The police impound the vehicle and One Stop files a claim under the dealer’s physical damage comp coverage for the amount paid for the auto. Is this covered?

a. No, this is not a SCL

b. No, it is excluded under false pretense

c. Yes, comp coverage only excludes collision or overturn 11. One Stop insures its dealer’s physical damage at a limit of $100,000. A

hail storm hits and damages three autos for a total of $10,000. The examiner investigates and finds that the lot had $200,000 in autos. One Stop’s policy has a $500 deductible with a maximum of $2,500. How much will be paid on this loss?

a. $9,500 ($10,000 minus the $500 deductible)

b. $7,500 ($10,000 minus the maximum deductible of $2,500)

c. $3,500 ($10,000 times the coinsurance penalty of .50, minus the $500 deductible for each auto)

d. $8,500 ($10,000 minus the $500 deductible for each auto) Additional notes:

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Garage Basics - Training for Agents

© Western Heritage Insurance Company February 2013 17171717

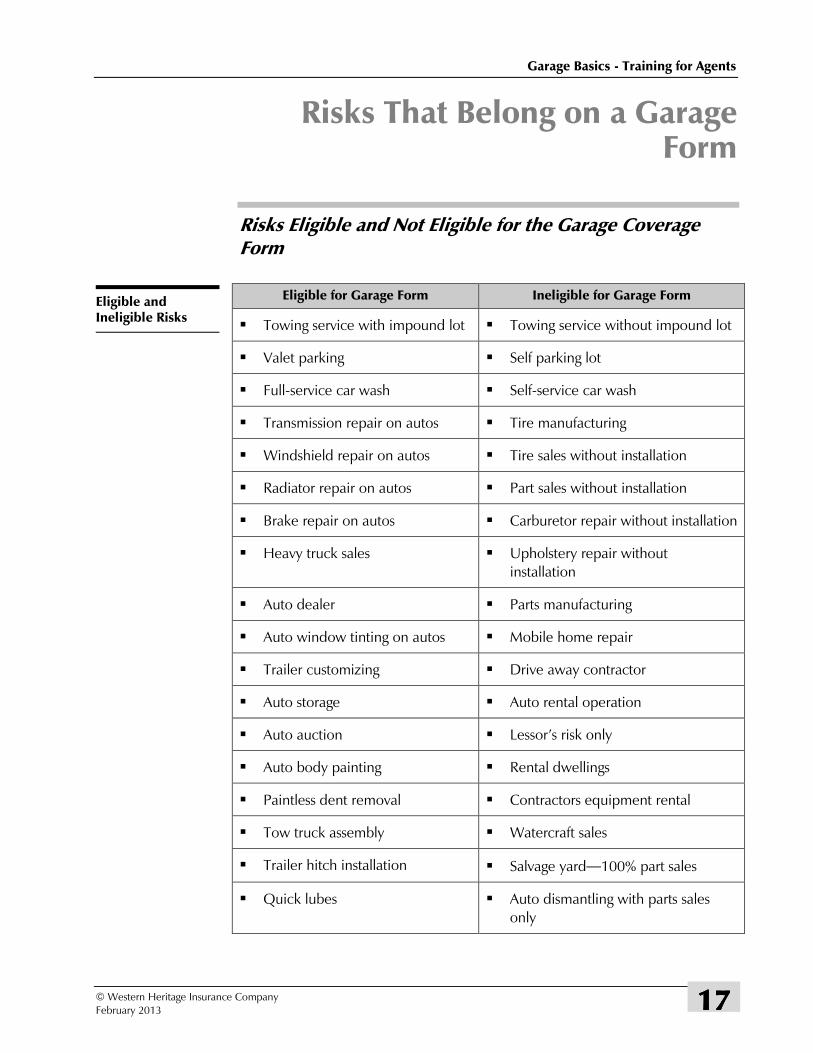

Risks That Belong on a Garage Form

Risks Eligible and Not Eligible for the Garage Coverage Form

Eligible for Garage Form Ineligible for Garage Form

� Towing service with impound lot � Towing service without impound lot

� Valet parking � Self parking lot

� Full-service car wash � Self-service car wash

� Transmission repair on autos � Tire manufacturing

� Windshield repair on autos � Tire sales without installation

� Radiator repair on autos � Part sales without installation

� Brake repair on autos � Carburetor repair without installation

� Heavy truck sales � Upholstery repair without installation

� Auto dealer � Parts manufacturing

� Auto window tinting on autos � Mobile home repair

� Trailer customizing � Drive away contractor

� Auto storage � Auto rental operation

� Auto auction � Lessor’s risk only

� Auto body painting � Rental dwellings

� Paintless dent removal � Contractors equipment rental

� Tow truck assembly � Watercraft sales

� Trailer hitch installation � Salvage yard—100% part sales

� Quick lubes � Auto dismantling with parts sales only

Eligible and Ineligible Risks

Garage Basics - Training for Agents

© Western Heritage Insurance Company February 2013 18181818

Knowledge Check

Answer the following questions to check your knowledge of risks that are eligible and ineligible for the garage form. In some cases, there will be more than one correct answer; select all that apply. Be prepared to share your answers.

1. Which one of the following would be best written on a garage form?

a. Tire sales only without installation

b. Transmission repair with installation

c. Engine repair without installation

2. Which one of the following would be best written on a CGL policy?

a. Full-service car wash

b. Auto auction

c. Carburetor manufacturer without installation

3. Which of the following would be best written on a garage form?

a. Farm equipment repair

b. Alarm installation on vehicles

c. Fuel tank manufacturing

Additional notes:

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Instructions

Questions

Garage Basics - Training for Agents

© Western Heritage Insurance Company February 2013 19191919

4. Which one of the following would be best written on a garage form?

a. Heavy truck sales

b. Towing service without impound lot or repair

c. Salvage yard with only part sales

5. Which one of the following would be best written on a garage form?

a. Self-service car wash

b. Transmission repair without installation

c. Auto auction

Additional notes:

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Garage Basics - Training for Agents

© Western Heritage Insurance Company February 2013 20202020

Identifying Information for a Garage Application

Information to Gather

Gathering this information before sending an application to the general agent will expedite the quote process:

� Name

� Address

� Names and ages of all individuals driving covered autos

� Years in business/related experience

� Handling of any flammables

� Pick up or delivery of autos

� Three-year prior carrier and loss history

� Total number of employees: full time and part time

� Description of garage operations

� Description of premises

� Radius of operations

� Premises conditions: fire/burglar protection

� Coverages requested

� Any commercial or service vehicles

Gather this information for auto dealers liability:

� Names and ages of all employees and family members who drive covered autos

� Their use of autos

� Customer test-driving procedures

� Number of autos sold per year

� Number of dealer plates

� Where autos are purchased

� Other operations not related to garage

� Whether they repossess autos

� Auto transport to/from point of purchase

� Types of autos sold

Additional notes:

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

All Exposures

Auto Dealers Liability

Garage Basics - Training for Agents

© Western Heritage Insurance Company February 2013 21212121

Gather this information for auto dealers physical damage:

� Types of autos sold

� Customer test-driving procedures

� Average value per auto sold

� Maximum number of autos on premises

� Maximum value of all autos on premises

� Theft barriers

� Key control procedures

� Auto transport to/from point of purchase

� Ownership of autos being sold

Gather this information for nondealers liability:

� Experience of technicians

� Breakdown of operations conducted

� Self-service operations

� Welding

Gather this information for garagekeepers:

� Vehicle storage and theft precautions

� Key control procedures

� Average number of vehicles kept in care, custody, and control

� Whether there is an approved paint booth

� Whether there is on-hook exposure

� Maximum number of vehicles kept in care, custody, and control

Additional notes:

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Auto Dealers Physical Damage

Nondealers Liability

Garagekeepers

Garage Basics - Training for Agents

© Western Heritage Insurance Company February 2013 22222222

Conclusion

Review of Learning Objectives

As a result of this training, agents will be able to:

1. Explain the benefits of garage products.

− Distinguish between the general liability and garage products.

2. Discuss the coverages and exposures that are involved in a garage risk.

− Identify the main coverages on the garage form (liability, garagekeepers, physical damage).

− Explain the auto coverage symbols.

− Identify premises and products completed operations.

− Identify the auto exposure on a garage risk.

3. Identify risks that belong on a garage form.

− Identify risks that do not belong on a garage form.

4. Identify information to gather when underwriting a garage risk.

Additional notes:

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

___________________________________________________________________

Learning Objectives