gap analysis: a framework for comparing public sector...

TRANSCRIPT

Gap Analysis: A Framework for Comparing Public Sector Accounting and Auditing to International Standards Gap Analysis Diagnostic Tool is a Framework for comparing national public sector accounting and auditing standards to international standards. The main objective of this assessment is to help implement more effective Public Financial Management (PFM) in countries through better quality accounting and public audit processes and to provide greater stimulus for more cost effective outcomes of government spending. This framework was conceived, developed and piloted by the South Asia Regional Financial Management (SARFM) Unit. SARFM has completed the gap analysis for all the countries in South Asia region. Later, the accounting part of the diagnostic was tried out in Azerbaijan with slight additions/modifications. These versions have now been converged to a single framework document incorporating the lessons from the pilots and roll out studies. More specific objectives of the Gap Analysis diagnostic tool are:

• to provide the country's accounting and audit authorities and other interested stakeholders with a common well-founded knowledge as to where local practices stand against the internationally developed norms of financial reporting and auditing;

• to assess prevailing variances;

• to chart paths for improving the accordance with international standards; and

• to provide a continuing basis for measuring improvements. For conducting this assessment, a set of diagnostic questionnaires have been developed to be consistent with the context of the PEFA Framework. These can be used to gather substantial insight into country performance with regard to the PFM indicators relating to external auditing and financial statement reporting. For further information, contact P.K. Subramanian ([email protected]), tel. +1-202-473-7168 or Sanjay Vani ([email protected]), tel. +1-202-458-4885.

PUBLIC SECTOR ACCOUNTING A COMPARISON TO INTERNATIONAL STANDARDS

GUIDELINE FOR THE USE OF THE DIAGNOSTIC TOOLS Background to the Accounting Diagnostic Framework Many countries have been facing up to the problems of improving the capacities of their national accounting institutions to improve the state of public financial management and reporting. Meanwhile some developed countries have been moving to resource accounting (accounting for assets controlled and liabilities incurred by governments and government entities) based on accrual accounting and output and outcome oriented budgeting systems. Country institutions face substantial capacity problems but in many cases, programs of reform and capacity strengthening initiated by the countries themselves and those supported by the external financiers are generally continuing to produce useful results. Acceleration of these reforms is needed for many countries to absorb modern Public Financial Management (PFM)1

methods, so that, every one places greater reliance on more use of countries’ own financial systems.

Using a generally accepted set of benchmarks would aid the consistency of the development efforts and support regional reviews and cooperation in improving accounting and auditing performance. The development of the PFM Performance Measurement Framework2 by the Public Expenditure and Financial Accountability (PEFA)3 Program has opened the way for a more detailed diagnostic framework to be used that is based on the accounting standards of the International Federation of Accountants (IFAC). This approach provides valuable inputs to the details supporting the PFM indicators. The PFM performance measurement framework4

includes the following accounting performance indicators (PI):

• PI 10. Public access to key fiscal information. • PI 22. Timeliness and regularity of accounts reconciliation. • PI 23. Availability of information on resources received by delivery units. • PI 24. Quality and timeliness of in-year budget reports. • PI 25. Quality and timeliness of annual financial statements.

The International Public Sector Accounting Standards (IPSAS) are designed to apply to the general purpose financial statements of public sector entities. Public sector entities include national governments, regional governments, local governments and their dependent entities. Government Business Enterprises have to apply the International Financial Reporting Standards (IFRS).

1 Public financial management (PFM) includes all phases of the budget cycle, including the preparation of the budget, expenditure and revenue management, internal control and audit, procurement, monitoring and reporting arrangements, and external audit. 2 The PFM Performance Measurement Framework has been developed as a contribution to the collective efforts of many stakeholders to assess and develop essential PFM systems, by providing a common pool of information for measurement and monitoring of PFM performance progress, and a common platform for dialogue. 3 Public Expenditure and Financial Accountability (PEFA) Program is a partnership among the World Bank, the European Commission, the UK's Department for International Development, the Swiss State Secretariat for Economic Affairs, the French Ministry of Foreign Affairs, the Royal Norwegian Ministry of Foreign Affairs, the International Monetary Fund and the Strategic Partnership with Africa. A Steering Committee, comprising members of these agencies, is managing the Program. A Secretariat has been set up and is located in the World Bank in Washington, DC. 4 • PFM Performance Measurement Framework, PEFA Secretariat May 2006 – www.pefa.org

2

Controllers General of Accounts (CGAs)5

or their equivalent are in a good position to develop and use this diagnostic framework for comparison of accounting standards at national, regional, and local levels. The diagnostic framework will be able to identify the gaps between countries’ own official standards and international standards and the degree to which the standards are complied with in practice. The information will provide a sound basis on which each country can go forward in improving PFM so that PFM goals including service delivery to the public are improved.

Objective of the Diagnostic The outcome intended for the exercise is quicker implementation of more effective PFM through better quality accounting and public reporting processes in countries and to provide greater stimulus for more cost effective outcomes of government spending. The specific objectives of the diagnostic are: (a) to provide each country and other interested stakeholders with a common well-based knowledge as to where the countries stand against the internationally developed norms of financial reporting and audit; (b) to assess the prevailing variances; (c) to assist in charting paths for improved compliance with international standards; and (d) provide a basis for measuring interim compliance. Examples of areas where there are substantial issues (based on various diagnostics carried out by the World Bank, other donors and the countries themselves) are:

• Financial reports could be improved to increase their utility –countries are generally in need of improved annual financial reporting to a level where general purpose financial reports are prepared in compliance with international standards and made available to the legislature and the citizens in good time. The reports also need to support and reflect management’s need for detailed information for decision making.

• Need to adopt professional codes of ethics – Often, low staff salaries and an inadequate

degree of technical professionalism combined with poor systems of internal control in the government sector have made it difficult to ensure that government expenditures and service delivery accord with good work practices and are not adversely influenced by corrupt practices. The Codes of Ethics established by INTOSAI and IFAC are a useful basis for government accountants to use in enforcing appropriate behaviors through an adequate system for managing government expenditures and revenue collections.

• Need for transparent and effective benchmarking to assist reform - There is a need for a

more effective benchmark of progress in strengthening institutional arrangements for accounting that the Ministries of Finance and CGAs themselves see as acceptable and relevant to their circumstances if an active program of self improvement is likely to take root. The framework for assessing progress also has to have a capacity to recognize the relative difficulties and obstacles that need to be addressed to make progress. It needs to be able to support a program of change for the Ministry of Finance and CGA that also addresses the changes needed in other parts of the PFM accountability framework for the accounting improvement to be effective. The framework of PFM indicators will provide a reference point for these links to be identified and programmed for integrated reform.

Purposes of Applying International Standards 5 The term “Controller General of Accounts (CGA)” has been used to denote the official responsible for maintaining the national accounts. The title differs from country to country.

3

Improve government accounting and reporting and increased public access to information - Government accounting information is inadequate. The financial statements of many countries generally do not accord with relevant international accounting standards. Methodical and well-resourced steps are likely to be needed to meet the IPSAS cash accounting standard and then to identify the steps needed to move gradually to the accrual accounting favored by the IPSAS Standards. IFAC’s IPSAS-Board has developed a set of accounting standards that are considered to be appropriate for government use. The CGAs need training and other support to be equipped with the skills and capacity to support government agencies in meeting the requirements of the accounting standards. Application of the financial reporting standard will enable preparation of financial statements against which the audit can be undertaken – this will clarify and support the audit role. Application of the standards will also support the transparency, understandability and easy public access to information that are also crucial to good PFM and responses to identified deficiencies through the application of better practices. Improve internal controls over PFM and budget management - The standards of public financial management and internal control in the countries of the region need to improve to support efficient expenditure and revenue management. The CGAs need to be adequately supported to develop and oversee effective systems of internal control and internal audit throughout the public sector. Fraud and corruption need to be addressed systematically through formal financial management routines. The Ministries of Finance need to ensure the effectiveness of complementary PFM practices such as fraud control plans and management control through reporting on the management assertions required and the financial reporting rules. Use of the Assessment Questionnaires These guidelines describe the usage of the questionnaires which are used for the gathering and analysis of information necessary for a Gap Analysis Report. The tools are devised in a very similar way to the ones which are used in the process of preparation of Reports on the Observance of Standards and Codes (ROSC). The guidelines define how to use the following diagnostics, when they should be used, and what should be observed:

I Assessment of the Public Sector Accounting Environment II Assessment of Cash Basis Public Sector Accounting Standards III Assessment of Accrual Basis Public Sector Accounting Standards IV Assessment of Actual Accounting Practices V Assessment of Financial Reporting for State Owned Enterprises VI Assessment of the value to be added of adopting the various underlying concepts and

specific standards that comprise the International Public Sector Accounting Standards (IPSAS).

The tools are based on the assumption that improvements of accounting and reporting are likely to be implemented on a step-by-step basis. The main threshold levels “cash basis”, which is also reflected by the cash basis IPSAS, and “full accrual”, which is reflected by the suite of accrual IPSAS, can be observed in some instances, but most countries around the globe are more likely to be somewhere in between. Therefore an analysis only based on the two main levels would be very rough and give only limited guidance for further improvement, as the gaps identified would be very large in most instances.

4

The Diagnostic Tools are qualitative questionnaires, which are supposed to be used in interviews conducted by the preparers of the report. The preparers of the report should have a good knowledge of public sector accounting and reporting, both on a cash and accrual basis, including closely related issues such as budgeting, budget execution and government financial statistics. As the questionnaires make explicit reference to the International Public Sector Accounting Standards (IPSAS) a good knowledge of these standards is an advantage, although its main principles are reproduced throughout the questionnaire. The use of local consultant(s), with a sound knowledge both of the local situation as well as the international standards, is strongly recommended. The main interview participants are senior representatives of the organization responsible for public sector financial accounting and reporting in the country examined. In many but clearly not all instances this is the Ministry of Finance or the Treasury. In federal countries, it is very likely that different organizations are responsible at the different levels of government. In a federal setting the resources required for the interviews are substantially higher than in more centralized countries, because it is necessary to cover different systems at the same time. However, also in more centralized countries interview participants outside the organization responsible should be considered, too. These interviews are intended to help identify the actual implementation of the guidance provided by the organization responsible. However, the Diagnostic Tool takes an exploratory, entirely qualitative approach and does not include representative sampling or other quantitative techniques. Accounting Diagnostic Tool Part 1 Assessment of the Public Sector Accounting Environment This part covers the general public sector accounting environment that focuses on the statutory framework, professional education, and code of ethics for the accounting profession which underpins the quality of accounting practices. While the questionnaire is designed to assess the major gaps existing between national and International Public Sector Accounting Standards, it may not justly cover the many detailed differences that may exist between the two. The questionnaire about the Assessment of the Public Sector Accounting Environment contains sections about general themes:

I Statutory Framework II Academic Education, Professional Education, Training III Setting Accounting Standards IV Monitoring and Enforcement V Quality and Availability of Financial Reporting VI Information Technology VII Public Sector

The aim of using this Diagnostic Tool is to analyze and evaluate the current situation in a country in general as well as in the accounting profession. By answering this questionnaire a wide overview of the researched country will be given and it is important that the questions are answered not only by yes/no answers but rather also with a full descriptive answer. Accounting Diagnostic Tool Part 2 Assessment of Cash basis Accounting Standards This part of the review assesses the comparability of any national accounting standards (cash basis) that are used with International Public Sector Accounting Standards (IPSASs); and the

5

degree of actual compliance with the applicable standards. The assessment also focuses on the institutional arrangements that underpin the quality of accounting practices. Accounting Diagnostic Tool Part 3 Assessment of Accrual basis Accounting Standards This questionnaire assesses the national standards (accrual basis) in direct comparison with the IPSAS. This part of the review is conducted on a standard by standard basis, following the order in which the IPSAS have been pronounced. Diagnostic Tool II helps to identify the current public accounting situation in respect of the IPSAS. The analysis of this comparison helps to identify possible gaps and shows where public sector accounting is at a high standard already. There are basically three levels of achievement:

(i) No achievement whatsoever; (ii) National standards/regulation observed, but no compliance with IPSAS; (iii) IPSAS or national standards based on IPSAS observed.

The sections of the Diagnostic Tool are independent of each other and can be tested separately. As improvements in public sector accounting and reporting are likely to be achieved step by step, it is possible to find very different situations in the various sections. A country may, for instance, account for property in full compliance with IPSAS, but use an entirely different approach perhaps in the field of provisions. Each section starts with (i) if the specific IPSAS has been adopted as a national standard, (ii) if there are any plans to change the national standards in respect of presentation of financial statements in the near future and (iii) if there is a current regulation which addresses this issue. If the answers to questions (i) and (iii) are ‘No’, the further questions in this area do not have to be answered and the next section can be tested. Accounting Diagnostic Tool Part 4 Assessment of Actual Accounting Practices This questionnaire is designed to assess the actual accounting practices and evaluate them against the standard or rule they refer to. As those standards or rules may vary between various jurisdictions or even between various entities within one jurisdiction, a three pronged approach has been suggested. There is no separate purpose-built questionnaire for this tool. Instead, Diagnostic Tool Part 2 (cash basis IPSAS), Diagnostic Tool Part 3 (accrual basis IPSAS) or Diagnostic Tool Part 5 (IFRS/IAS) should be used for this assessment, as the questions are the same. This assessment should include organizations other than the one responsible for public sector financial accounting and reporting, even in highly centralized countries. It should also include an analysis of audited financial reports, as they may fall short from internationally accepted best practices in some cases. Accounting Diagnostic Tool Part 5 Assessment of Financial Reporting for State Owned Enterprises This part of the review enables specific attention to be given to the accounting standards and practices in state owned enterprises. It is to be used when state owned enterprises are included in the scope of the diagnostic work. This is a matter to be decided in planning the scope of the overall assessment.

6

The purpose of this questionnaire is to provide information about the differences between National Standards, and the International Financial Reporting Standards (IFRS) and International Accounting Standards (IAS) approved by the International Accounting Standards Board. The questionnaire contains the following sections:

I Framework for the Preparation and Presentation of Financial Statements II Differences between National Standards and each of the International Financial

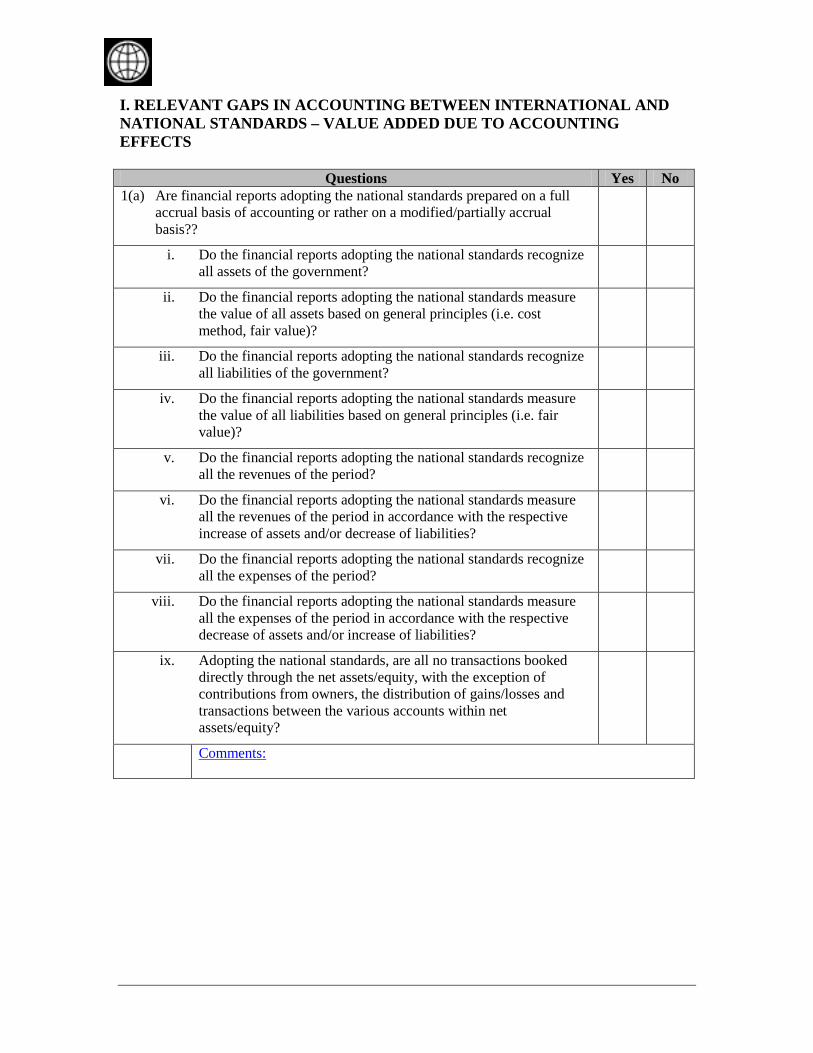

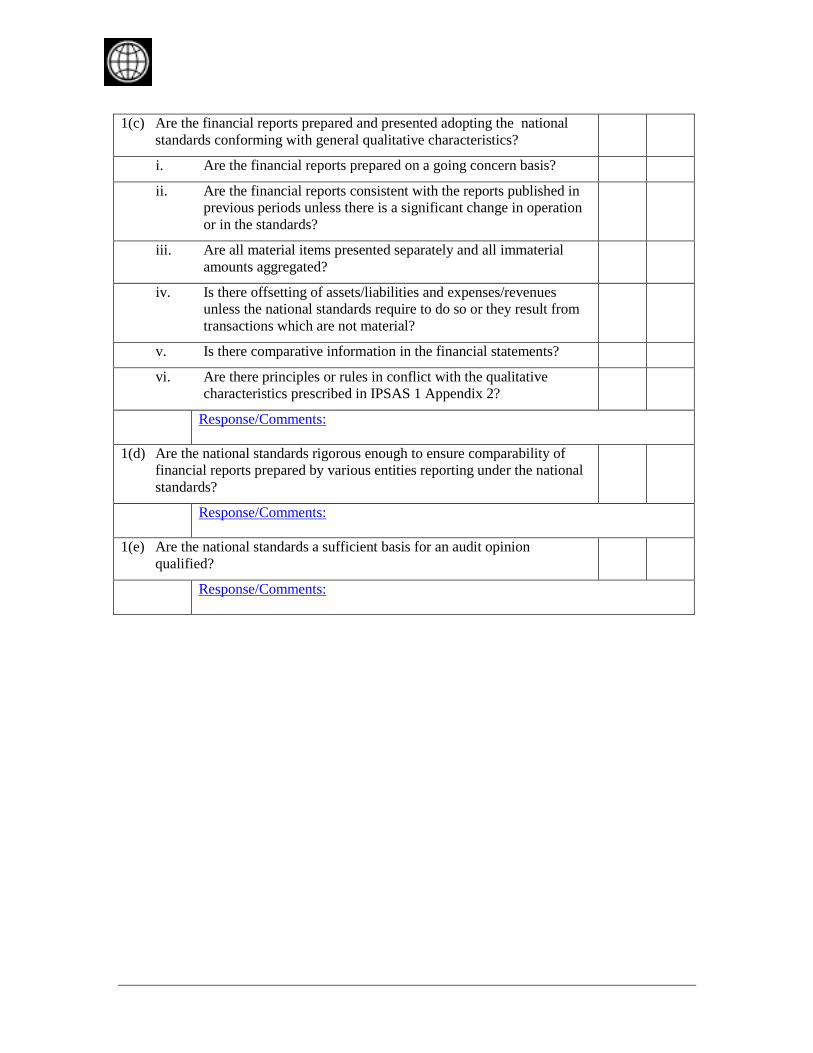

Reporting Standards or International Accounting Standards The questionnaire is to be used separately for entities that are required to use different National Standards or in practice apply the same National Standards differently (for example, as is often the case with banks, insurance entities and other financial institutions). It may also need to deal separately with legal entity and consolidated financial statements. Accounting Diagnostic Tool Part 6 Assessment of value to be added by adopting the specific standards that comprise IPSAS (or IFRS) to the extent that they are not already incorporated into the national standards This part of the review assesses the potential value to be added by an adoption of the International Public Sector Accounting Standards (IPSASs) in comparison to the National Public Sector Accounting Standards in place. The assessment identifies potential value added directly in the field of accounting, but also in respect of reputation and training of local financial management staff. While the questionnaire is designed to assess the major gaps existing between national and International Public Sector Accounting Standards, it may not fully cover the many detailed differences that may exist between the two. The questionnaire includes the following three sections:

I Relevant Gaps in Accounting between IPSAS’ and national standards – Value Added due to Accounting Effects

II Value Added due to Reputation Effects III Value Added due to Training Effects

This questionnaire is qualitative and subjective. In order, to avoid entirely personal views, making reference to other countries in similar situations or to other sectors of the economy is helpful. However, the analysis should also include obstacles or downsides, in order to avoid false expectations. Gap Analysis Report The results obtained in interviews, meetings and from available documents, laws etc. are to be used for the preparation of the Gap Analysis Report. This report includes the relevant information which was obtained from the four Diagnostic Tools. However, the content of this REPORT is structured differently from the questionnaires. The following composition was chosen:

I Introduction

7

II Institutional Framework III Accounting Standards as Designed IV Accounting Standards as Practiced V Value added Opportunities VI Recommendations

The report concentrates on the more relevant issues while summarizing the less relevant ones. It is intended to provide the user with a comprehensive picture of the issue, and should not just present the questionnaire-style preliminary results. The report should begin with an executive summary. The draft report should be discussed with the main interview participants, especially with senior representatives from the organization responsible for accounting and reporting, i.e. the Ministry of Finance/Treasury, and can benefit from a workshop on the main issues. This discussion is likely to identify substantial changes for the report, and should therefore take place well before the deadline for the final report. The feedback should be incorporated, as long as it is in accordance with the findings of the preparer. The report should be between 25 and 40 pages long.

Guideline using the Diagnostic Tools Page 1

PUBLIC SECTOR AUDITING A COMPARISON TO INTERNATIONAL STANDARDS

GUIDELINE FOR THE USE OF THE DIAGNOSTIC TOOLS

Background to the Auditing Diagnostic Framework Many countries have been working on improving the capacities of their national auditing institutions to assist with improving the state of public financial management. Country institutions face substantial capacity problems but in many cases, programs of reform and capacity strengthening initiated by the countries themselves are generally continuing to produce useful results. Acceleration of these reforms assists countries to absorb modern Public Financial Management (PFM)1

methods so that greater reliance can be placed on use of countries’ financial systems. Improvement of institutional arrangements for the Supreme Audit Institutions (SAIs) has been a continuing but slow feature of this reform. Part of the problem with increasing the speed of country implementation has been a lack of ability to focus clearly on the real progress that has been made, and greater clarity about performance improvement would assist effective monitoring.

The International Standards for SAIs (ISSAI)2

were adopted in November 2007 as a comprehensive framework of auditing standards by the International Organization of Supreme Audit Institutions (INTOSAI). This internationally accepted set of standards provides a strong benchmark to ensure consistency in SAI improvement efforts and to support consistency in regional and international cooperation to improve auditing performance. The ISSAI benchmarks provide a good reference point for relevant stakeholders to develop confidence in SAI capability. This auditing diagnostic framework is based on the ISSAI.

The PFM Performance Measurement Framework3 developed by the Public Expenditure and Financial Accountability (PEFA)4

Program includes public sector audit PFM indicators that can be incorporated into this auditing diagnostic framework so that the REPA can be helpful in the context of the overall PFM performance indicator framework.

Through their strong involvement with INTOSAI, Auditors General (AGs)5

1 Public financial management (PFM) includes all phases of the budget cycle, including the preparation of the budget, expenditure and revenue management, internal control and audit, procurement, monitoring and reporting arrangements, and external audit.

and Boards of Audit are in a good position to use this diagnostic framework for assessment of their own auditing standards and practices at national, regional, and local levels. The diagnostic framework can be used to identify the gaps between countries’ own official standards and accepted international standards, and the degree to which the standards are complied with in practice. The information will provide a sound basis on which each country can go forward in improving PFM.

2 The International Standards of Supreme Audit Institutions, ISSAI, are issued by the International Organization of Supreme Audit Institutions, INTOSAI. For more information visit www.issai.org 3 The PFM Performance Measurement Framework has been developed as a contribution to the collective efforts of many stakeholders to assess and develop essential PFM systems, by providing a common pool of information for measurement and monitoring of PFM performance progress, and a common platform for dialogue. 4 Public Expenditure and Financial Accountability (PEFA) Program is a partnership among the World Bank, the European Commission, the UK's Department for International Development, the Swiss State Secretariat for Economic Affairs, the French Ministry of Foreign Affairs, the Royal Norwegian Ministry of Foreign Affairs, the International Monetary Fund and the Strategic Partnership with Africa. A Steering Committee, comprising members of these agencies, is managing the Program. A Secretariat has been set up and is located in the World Bank in Washington, DC. 5 The term “Auditor General (AG)” has been used to denote the Head of the Supreme Audit Institution. The actual title varies across countries.

Guideline using the Diagnostic Tools Page 2

Objective of the Diagnostic The general outcome intended to be achieved by using the diagnostic framework is a report that ensures quicker implementation of more effective PFM through better quality public sector audit processes that in turn provide greater stimulus for more cost effective outcomes of government spending. The specific objectives of the REPA are: (a) to provide the SAI and other interested stakeholders with a common well-based knowledge as to where the country stands against the internationally developed norms of government audit; (b) to assess the prevailing variances; (c) to assist in charting paths for improved compliance with international standards; and (d) provide a basis for measuring interim improvements. Examples of areas where there have been substantial issues (based on various diagnostics carried out by the World Bank, other donors and the countries themselves) are:

• Financial reports could be improved to increase their utility – countries are generally in need of improved annual financial reporting to a level where audited general purpose financial reports are prepared in compliance with international standards and made available to the legislature and the citizens in good time. The reports also need to support and reflect management’s need for detailed information for decision making.

• Independence of audit needs to be enhanced – commonly, SAIs have had a direct

responsibility for providing the accounting and pre-audit functions at various levels of government, and this has diverted them from the primary SAI role of providing independent attestation to legislatures on the performance of the financial management system and the adequacy of financial reporting. The need for systematic complementary reforms can best be met under the agreed INTOSAI framework for institutional arrangements that are acceptable to host governments and the relevant bodies. The consultation between the interested parties can be improved through assessment against the relevant complementary PEFA PFM indicators for the institutions that are interacting or overlapping. The performance of SAIs can be affected by inadequacies in their institutional powers; resourcing arrangements; AG security, tenure and qualifications; access to information; and rights to report to the legislature and to report publicly. The INTOSAI ISSAI standards deal extensively in these issues.

• Need to adopt and enforce professional codes of ethics – for some SAIs, low staff salaries

and an inadequate degree of technical professionalism combined with poor systems of internal control in the government sector have made it difficult to ensure that auditors accord with good work practices and are not adversely influenced by corrupt practices. The Codes of Ethics and their enforcement regimens that have been established by INTOSAI and IFAC are a useful basis for SAIs to use in managing appropriate auditor behavior through the SAI’s internal systems for managing and supervising audits.

• Need for transparent and effective benchmarking to assist reform - there is a need for a

more effective benchmark of progress in strengthening institutional arrangements for audit that the SAIs themselves see as acceptable and relevant to their circumstances if an active program of self improvement is likely to take root. The framework for assessing progress also has to have a capacity to recognize the relative difficulties and obstacles that need to be addressed to make progress. It needs to be able to support a program of change for the SAI that also addresses the changes needed in other parts of the PFM

Guideline using the Diagnostic Tools Page 3

accountability framework for the SAI improvement to be effective. The framework of PEFA PFM indicators provides the reference point for these links to be identified and programmed for integrated reform. An important example is that there is little point to improving the SAI’s output of audit reports if the reports and their recommendations are not transmitted to the legislature, made public, and acted upon.

Purposes of Applying International Standards Improve government accounting and reporting and increased public access to information - government accounting information is inadequate in many countries. Their annual financial statements and audit certifications often do not accord with relevant international accounting standards so that their reliability and sufficiency are suspect. The SAIs need training and other support to be equipped with the skills and resourcing needed to conduct the certification and other audits and report to the legislature in a way that meets international practices established by INTOSAI. Application of internationally financial reporting standards will enable preparation of financial statements against which the audit can be undertaken confidently. Application of international standards will also support the transparency, understandability and easy public access to information that are also crucial to good PFM and responses to identified deficiencies through the application of better practices. Improve internal controls over PFM and budget management - the standards of public financial management and internal control in many countries need to improve to support efficient expenditure and revenue management. SAIs play a major role in scrutiny and improvement. The SAIs need to be equipped to audit regularity issues both from a performance perspective and from a compliance perspective to report in ways that lead to systemic improvement. Programs for improvement of public expenditure management and revenue collection need to be supported rather than constrained by audit activities which may become counter productive or ineffective by concentrating on the more trivial or occasional transgressions rather than system deficiencies. Fraud and corruption need to be addressed systematically through audit as well as through formal internal financial management routines which SAIs should scrutinize. The international standards provide benchmarks for the scope, conduct and performance of audit functions and the involvement of SAIs in routine reporting including reports on complementary PFM practices such as fraud control plans, the adequacy of the management assertions, and financial reporting rules. Improve quality of audit – in most cases, the legislative standards applied to the qualifications of auditors for commercial companies audit are more specific and at a more advanced level than those applied to government auditors. Private sector auditors are often used for State owned business enterprises and the legislative and greater public scrutiny opportunity afforded by the use of public sector auditors is denied. In some cases, public sector recruitment practices do not favor recruitment of technical specialists and auditor competence becomes a key concern as well as excess costs of unrelated training. Interchange of personnel between the public and private sectors of the accounting and auditing profession is frequently at a low level. The standards need to provide benchmarks for skills and competency requirements including ethics and discipline provisions. Improve legislative scrutiny and corrective action - The standards of legislative scrutiny are often insufficient to provide a guarantee of good PFM in government agencies. The SAI needs to have the capacity to provide the legislature with the reports and the hearings support to carry out the scrutiny and follow up processes sufficiently well to ensure that deficiencies are rectified and malpractice disciplined. The standards should provide benchmarks for the development, reporting, and follow-up of audit findings and recommendations.

Guideline using the Diagnostic Tools Page 4

The SAR PFM performance measurement framework6

includes the following performance indicators (PI) relevant to auditing:

• PI 10. Public access to key fiscal information. • PI 25. Quality and timeliness of annual financial statements. • PI 26. The scope, nature and follow-up of external audit. • PI 28. Legislative scrutiny of external audit reports.

Use of the Assessment Questionnaires These guidelines describe the usage of the three assessment questionnaires which are used for the gathering and analysis of the information necessary for a Gap Analysis Report. The tools are devised in a very similar way to those that are used for preparing Reports on the Observance of Standards and Codes (ROSC). The guidelines define how to use the following diagnostics, when they should be used, and what should be observed:

Part I Assessment of the public sector auditing environment. Part II Assessment of auditing standards and practices. Part III Assessment of the in-country value-added by adopting the various elements of the International Standards for Supreme Audit Institutions (ISSAI).

The tools enable improvements in auditing and review to be implemented on a step-by-step basis by adopting and implementing the practices embodied in the international auditing standards to the extent that national resources and conditions allow. The overall goal is certification and assessment of the annual accounts and the systems of financial controls in accordance with the auditing methodologies set out in the ISSAI framework of standards:

• Level 1: Founding Principles – Lima Declaration. • Level 2: Prerequisites for the Functioning of Supreme Audit Institutions. • Level 3: INTOSAI Auditing Standards. • Level 4: Auditing Guidelines.

These standards can be observed by countries in full in some instances but the accounting systems of many countries can make it difficult for some of the standards to be readily applied, especially where statistical sampling methods are advantageous to the audit testing processes. In these cases a lesser standard of auditing and review is attainable until accounting systems are improved - usually through some automation of record keeping and compilation. The Diagnostic Tools are qualitative questionnaires that are intended to be used in interviews conducted by the preparers of the report. The preparers of the report should have a good knowledge of public sector audit and review practices, including closely related issues such as legislative scrutiny. As the questionnaires make explicit reference to the ISSAI and the International Standards on Auditing (ISA) a good knowledge of these standards is an advantage, and the main principles of these standards are reproduced throughout the questionnaires. The use

6 PFM Performance Measurement Framework, PEFA Secretariat May 2006 – www.pefa.org

Guideline using the Diagnostic Tools Page 5

of local well-qualified consultant(s), who are members of the national professional accountancy body and have a sound knowledge both of the local public sector situation as well as the international standards, is strongly recommended. The main interview participants are senior representatives of the organization responsible for public sector financial auditing in the country examined. This is the Supreme Audit Institution. The Diagnostic Tools takes an exploratory, entirely qualitative approach and do not include representative sampling or other quantitative techniques. Audit Diagnostic Tool I Assessment of the Public Sector Auditing Environment Part I of the review assesses the potential value added that an adoption of the higher levels of the ISSAI framework would provide in comparison to the current institutional arrangements for national public sector auditing. The assessment identifies potential value added directly in the field of auditing and the preparation of audit reports. While the questionnaire is designed to assess the major gaps existing between national and international standards, it may not fully cover the many detailed differences that may exist between the two. The questionnaire about the Assessment of the Public Sector Auditing Environment contains eight sections covering the following:

I Statutory framework II Academic education, professional education, and training III Setting auditing standards IV Accountability for the SAI V Independence provided by the legislation VI Information technology VII Code of ethics VIII Country data

The aim is to develop a strong understanding of the public sector audit arrangements in the country and it is important that the questions are answered not only by yes/no answers but rather also with a full descriptive answer. Audit Diagnostic Tool II Assessment of Auditing Standards Part II of the review assesses the comparability of any written or adopted National Public Sector Auditing Standards (NPAS) with each of the ISSAI Audit Guidelines for financial audit. It also assesses the degree of actual compliance of the implementation of these national standards with the detail of the applicable ISSAI standards. The report preparer uses the results to assess the institutional arrangements that underpin the quality of auditing practices. Where ISSAI standards are still in exposure draft or not yet drafted the relevant International Standard for Auditing is used in the questionnaire for the comparison. The report preparer uses the analysis of this overall comparison to identify possible gaps. There are basically three levels of achievement:

(i) No achievement whatsoever; (ii) National standards/regulation observed, but poor compliance with ISSAI; (iii) ISSAI (or national standards substantially based on ISSAI) substantially observed.

Guideline using the Diagnostic Tools Page 6

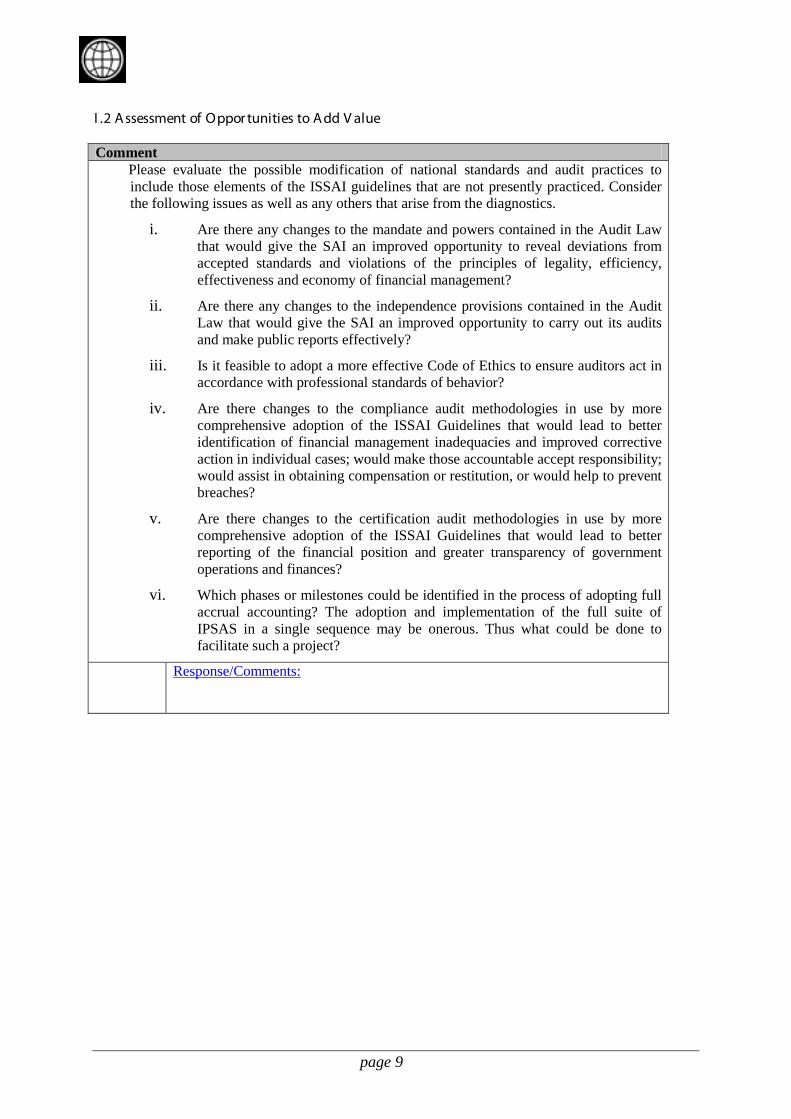

This Diagnostic Tool contains sections which refer to the current ISSAI. The sections are independent of each other and can be tested separately. As improvements in public sector auditing and review are likely to be achieved step by step, it is possible to find very different situations in the various sections. Each section starts with a summary setting out (a) if the specific ISSAI has been adopted as a national standard, (b) a brief assessment (based on the answers to the details as per (c) following) of the potential value added that adoption of the ISSAI would provide in comparison to the National Public Sector Auditing Standards (or audit practices in the absence of any particular written standards), and (c) an explanation of any differences between the national standard and the ISSAI. The main part of each section contains the main requirements of the ISSAI assessment and identifies whether audit practices in the country conform to the requirements. The answers to these requirements are to be used by the report preparer to identify the value added that can be gained by closer adherence to the ISSAI. These assessments are summarized at item (b) and further developed by the report preparer in Audit Diagnostic Tool III. This questionnaire is designed to assess the actual auditing practices and evaluate them against the standard that governs their implementation with a view to identifying where the international standards can add value to the audit processes. Audit Diagnostic Tool III Assessment of Value Added by Adopting the ISSAI Part III of the review uses the results of Parts I and II to summarize the potential value added an adoption of the ISSAI would provide in comparison to the National Public Sector Auditing Standards and/or practices applied in the country. The assessment identifies potential value added directly in the field of auditing. This diagnostic tool relies heavily on the expertise and judgement of the report preparer to form views as to the value added that can be gained by changing practices. The questionnaire includes the following three sections:

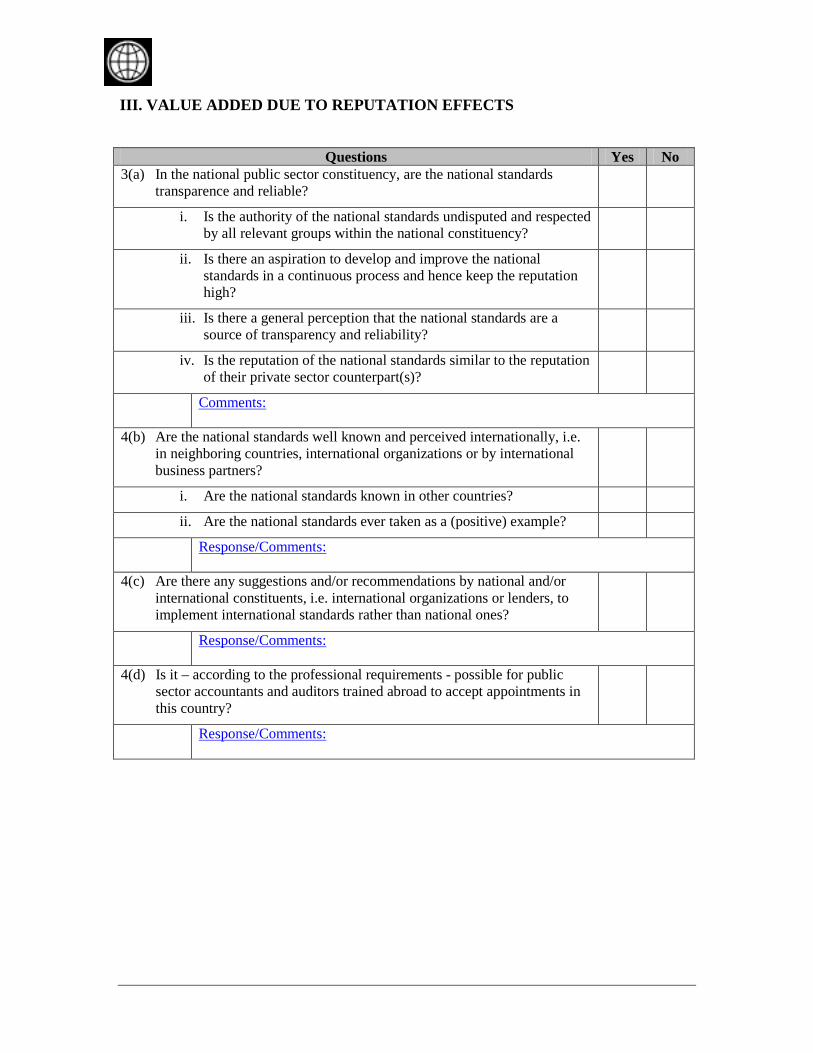

I Relevant gaps in auditing between ISSAI’s and NPSAS’s – value added due to auditing effects

II Value added due to reputation effects III Value added due to training effects

This Part includes questions for each ISSAI on the most significant requirements of the ISSAI but this is not intended to constrain the preparers of the Report. Part III is intended to be qualitative and subjective so that the perceptions that the preparers of the report gain from their survey can be translated into the best path for the country to improve its audit performance through adopting the ISSAI.. In order to avoid entirely personal views making reference to other countries in similar situations can prove to be helpful. The analysis should also include obstacles or downsides, in order to avoid false expectations and to provide realism in the projected value added. Diagnostic Report All results obtained in interviews, meetings and from available documents, laws etc. are to be used for the preparation of the Gap Analysis Report. This report is based on relevant information which was obtained through the questionnaires in the Diagnostic Tools. However, the content of this REPA is structured differently from the questionnaires as follows:

Guideline using the Diagnostic Tools Page 7

I Introduction II Institutional Framework III Auditing Standards as Designed IV Auditing Standards as Practiced V In-country Value added Opportunities VI Recommendations

The report concentrates on the more relevant issues while summarizing the less relevant ones. It is intended to provide the user with a comprehensive picture of the issue, and should not just present the questionnaire-style preliminary results. The report should begin with an executive summary. The draft report should be discussed with the main interview participants, especially with senior representatives from the organization responsible for accounting and reporting, i.e. the Supreme Audit Institution, and can benefit from a workshop on the main issues. This discussion is likely to identify substantial changes for the draft report, and should therefore take place well before the deadline for the final report. The feedback should be incorporated, as long as it is in accordance with the findings of the preparer. The report should be between 25 and 40 pages in the case of federal countries. Where audit practices differ between regions it may need to be more extensive than in a more centralized environment.

The World Bank

Public Sector Accounting: A Comparison to International Standards

Assessment of the Public Sector Accounting Environment

DIAGNOSTIC TOOL – PART 1

April, 2009

page 1

CONTENTS

Foreword ................................................................................................................................ 1I Statutory Framework .......................................................................................................... 2II Academic Education, Professional Education, Training .................................................... 4III Setting Accounting Standards ........................................................................................... 7IV Monitoring and Enforcement ............................................................................................ 9V Quality and Availability of Financial Reporting ................................................................ 9VI Information Technology ................................................................................................. 10

page 1

FOREWORD

As part of its public sector financial management reform program, the World Bank has developed a framework for assessing the variance between national and international standards in public sector accounting. This toolkit is developed for use in different countries to promote improvements in public sector financial management. This part of the review assesses the comparability of the International Public Sector Accounting Standards (IPSASs) in comparison to the National Public Sector Accounting Standards of the respective country. The assessment also covers the Public Sector accounting environment that focuses on the statutory framework, professional education, and code of ethics for the accounting profession which underpins the quality of accounting practices.

While the questionnaire is designed to assess the major gaps existing between national and International Public Sector Accounting Standards, it may not justly cover the many detailed differences that may exist between the two and that may have a material impact on financial statements.

Preparers may use the Comments box to highlight specific differences that are not covered in the tool in the questionnaire. The Diagnostic Tool Part 1 should be used in conjunction with the IPSAS 2008 Bound Volume containing all International Public Accounting Standards as of January 2008.

References to specific Standards are placed in brackets at the end of each question.

Note on Terminology Used in this Questionnaire

“Standard” refers to any applicable International Public Sector Accounting Standard issued by the International Public Sector Accounting Standards Board of IFAC.

page 2

I STATUTORY FRAMEWORK I.1. Overview over the Statutory Framework

Questions 1(a) What “legal tradition” best describes the country’s legal system (i.e. common law, written law, other)?

Answer:

1(b) Are there any fundamental principles which differ between administrative law and legislation imposed on the private sector (i.e. requirement of explicit authorization of any action taken by the government in formal piece of legislation)?

Answer:

1(c) Are there any consequences of such a legal tradition on the accounting and reporting environment? If yes, please describe.

Answer:

I.2. Public Sector Accounting Law

Questions 2(a) What is (are) the Accounting Law(s) or Act(s) which is relevant for public sector entities? What is its enacting body, enactment date and the latest amendment date? With your response to the questionnaire, please attach a copy of the Law(s) or Act(s) in the country’s official language and in English (if available).

Answer:

2(b) If there is more than one Law or Act, what are the delimitations between the various laws or acts? (i.e. indicate which ones are relevant for which level of government or for which kind of legal entity)

Answer:

2(c) Is the law also applicable to Government Business Enterprises (GBEs)? GBEs are government owned entities with the objective of selling goods or services at a profit or full cost recovery. If not, what law is applicable to GBEs.

Answer:

2(d) What are the main provisions of the Law?

Answer:

2(e) Is the presentation of government budgets covered by the same Law? If not, please name the Law or Act which is relevant for government budgets?

Answer:

2(f) Does the Law require a specific basis of accounting, either cash or accrual? If applicable, distinguish among the various kinds of entities.

Answer:

page 3

2(g) Does the Law (or the various Laws according to answer 2d) require a different basis of accounting for budgets and for financial reporting (i.e. cash basis for budgets, accrual basis for financial reporting)? If applicable, distinguish among the various kinds of entities.

Answer:

2(h) Does the Law require compliance with International Public Sector Accounting Standards (IPSAS)? If applicable, distinguish among the various kinds of entities and between separate and consolidated financial statements.

Answer:

2(i) Does the Law allow compliance with IPSAS, even if compliance is not mandated? If applicable, distinguish among the various kinds of entities and between separate and consolidated financial statements.

Answer:

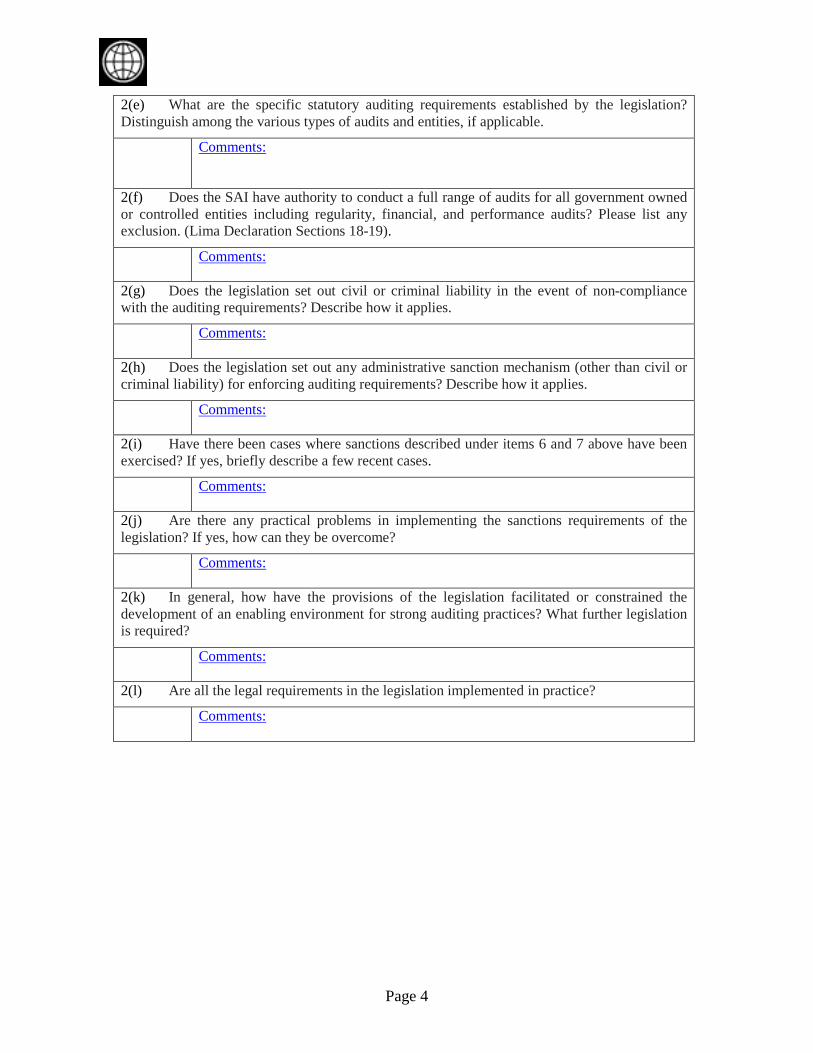

2(j) Have the provisions of the law facilitated or constrained the development of an enabling environment for strong accounting practices?

Answer:

2(k) Are all the legal requirements implemented in practice?

Answer:

2(l) Are there any practical problems in implementing the Law? If yes, how can they be overcome?

Answer:

2(m) Does the law relating to GBEs allow or require compliance with International Accounting Standards/International Financial Reporting Standards (IAS/IFRS)?

Answer:

page 4

II ACADEMIC EDUCATION, PROFESSIONAL EDUCATION, TRAINING II.1 ACADEMIC PROGRAMS

Questions 3(a) What kind of degree programs in accounting or in related areas are operational in the country? (i.e. Bachelor Science in Accounting, Master of Financial Management etc.)

Answer:

3(b) Are there any degree programs addressing public sector accounting issues in a substantial magnitude?

Answer:

3(c) Are there any non-degree programs provided by academic institutions in accounting or in related areas? (i.e. Certificate in Accounting and Auditing)

Answer:

3(d) Are there any non-degree programs provided by academic institutions addressing public sector accounting issues in a substantial magnitude? (i.e. Certificate in Public Sector Accounting)

Answer:

3(e) Please provide a rough estimate of the number of students/participants graduating from/finishing the above mentioned programs (items 3(a) through 3(d)).

Table:

3(f) Do the curriculums of the academic institutions extend to internationally recognized standards of accounting (i.e. IFRS, IPSAS)? If yes, please describe briefly how this is done. Is particular emphasis given on technical practical application of such standards?

Answer:

3(g) Are (some of) the programs internationally accredited, either by professional or academic accreditation bodies (ACCA, CPA Australia)? If yes, which kind of accreditation is in place?

Answer:

3(h) Are there minimum academic requirements for an individual seeking to begin a study/training program leading to membership in a professional accounting or auditing body? If yes, what are those requirements?

Answer:

3(i) Are there minimum academic requirements for government employees in specific positions related to accounting/auditing/financial management or above certain hierarchy levels? If yes, what are those requirements?

Answer:

II.2 PROFESSIONAL EDUCATION

page 5

Questions

4(a) Is there a professional license required for certain positions/professions in the field of accounting/auditing/financial management? Please describe briefly?

Answer:

4(b) Are there professional education requirements for an individual to obtain a professional license as an accountant/auditor or similar professions?

Answer:

4(c) Is the system of professional education/professional licenses the same in the private and public sector? If no, please highlight the differences.

Answer:

4(d) Do the entry requirements of the professional education programs comply with IFAC International Education Standards (IES 1): “at least equivalent to that required for admission into a recognized university degree program or its equivalent”? Please specify if requirements for public sector are different from their private sector counterparts.

Answer:

4(e) Do the syllabi of the professional education programs cover all areas required by IFAC International Education Standards (IES 2): “accounting, finance and related knowledge”, “organizational and business knowledge” and “information technology and competences” as defined in the standard? Please specify if requirements for public sector are different from their private sector counterparts.

Table:

4(f) Do the entry requirements of the professional education programs comply with IFAC International Education Standards (IES 5): 3 years, with not more than 12 months credited from graduate degree programs towards it? Please specify if requirements for public sector are different from their private sector counterparts.

Answer:

4(g) Is there a professional examination requirement in compliance with IFAC International Education Standards (IES 6): recorded form, reliability and validity, coverage of the syllabus, made at the end of pre-qualification program, in responsibility of professional body or regulatory authority? Please specify if requirements for public sector are different from their private sector counterparts.

Answer:

4(h) Is there a professional education/examination program which is in co-operation with international providers of such programs (i.e. CIPFA or similar)? Does it lead to the internationally recognized professional qualifications?

Answer:

page 6

II.3 CONTINUING EDUCATION

Questions 5(a) Is continuing education for professionally qualified individuals (i.e. CPAs) required and promoted by their (public sector) employers?

Answer:

5(b) Is continuing education for individuals working in the field of public sector accounting/public financial management required and promoted by their employers?

Answer:

5(c) Is there a systematic approach to continuing education programs?

Answer:

5(d) Are (some of the) continuing education programs evaluated or accredited by an independent body?

Answer:

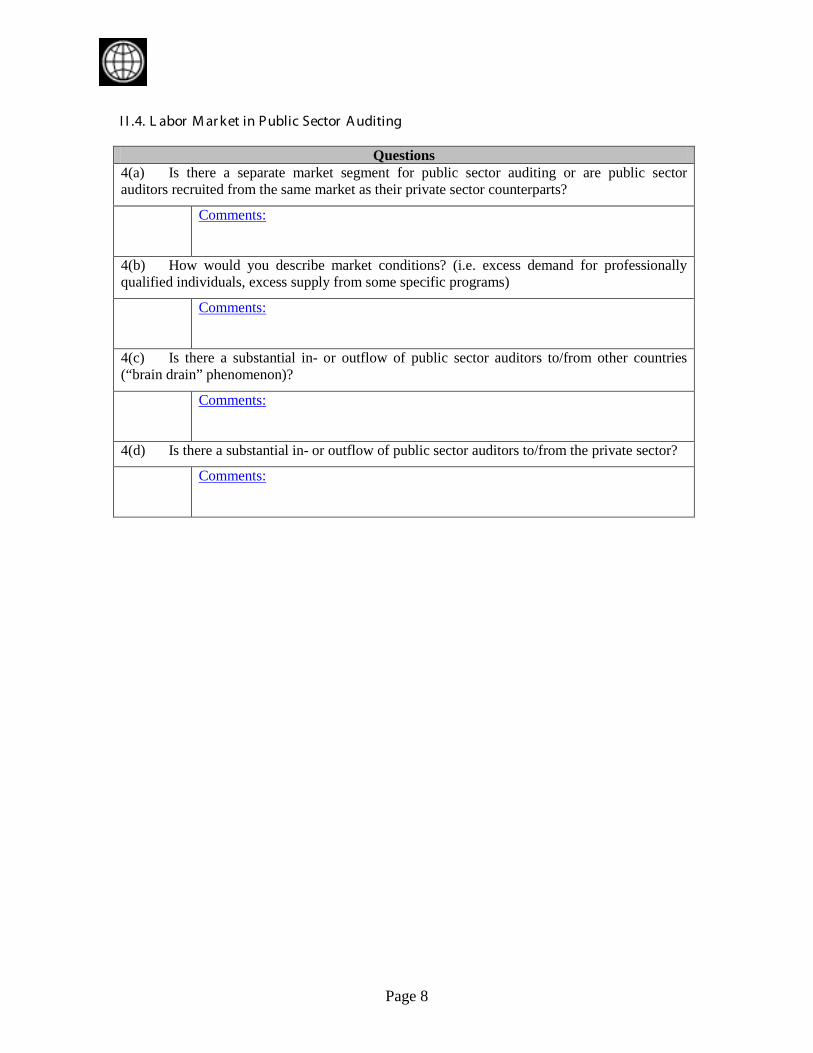

II.4 LABOUR MARKET IN THE FIELD OF PUBLIC SECTOR ACCOUNTING

Questions 6(a) Is there a separate market segment for public sector accounting or are public sector accountants recruited from the same market as their private sector counterparts?

Answer:

6(b) How would you describe market conditions? (i.e. excess demand for professionally qualified individuals, excess supply from some specific programs)

Answer:

page 7

III SETTING ACCOUNTING STANDARDS III.1 ACCOUNTING STANDARDS

Questions 7(a) Are there national accounting standards for public sector entities? If so, who is responsible for issuing those standards?

Answer:

7(b) Are the national accounting standards identical for public sector entities and for the private companies?

Answer:

7(c) What is the source of legal authority of the national standards? Is the legal authority limited?

Answer:

7(d) Is there a due process before new or revised standards are issued?

Answer:

7(e) Do the national accounting standards for public sector entities require the presentation of “general purpose financial statements” that achieve fair presentation?

Answer:

7(f) Is there any arrangement for issuance of practical implementation or interpretation guidelines? If yes, how is this arrangement accomplished?

Answer:

7(g) Have efforts been made to make national accounting standards comparable with the IPSASs?

Answer:

7(h) Highlight the main differences between national accounting standards and IPSAS?

Answer:

7(i) Are Government Business Enterprises (GBEs) following private or public sector standards?

Answer:

III.2 STANDARD SETTING BODY

Questions 8(a) Is/are there national standard setting body/ies in the field of accounting? Please name all and show the differences between their missions and legal authority? Clearly identify those which are relevant for the public sector.

Answer:

8(b) Describe the governance of those standard setting bodies which are relevant for the public sector. This should include a description of the structure and responsibilities of boards and

page 8

committees.

Answer:

8(c) What is the composition of the standard setting entities within the standard setting body? Who is nominating the individuals members of this entity? What is their qualification?

Answer:

8(d) Are the individuals responsible for standard setting tasks independent or acting as representatives on behalf of some other organizations? What is the proportion of independent members? Is independence defined in respect of preparers only or also in respect of the profession?

Answer:

8(e) Are there rules how to handle conflict of interest issues within a standard setting body or entity? (i.e. is there a requirement of abstention or suspension in specified situations?)

Answer:

8(f) Are there rules to limit the power and influence of individuals or parts of the constituency? Are there quota rules to limit the number of members from the same background? Is the term of members limited with limited possibilities of extension?

Answer:

8(g) Are there any arrangement to provide for sufficient reflection of the public interest? (i.e. is there a public interest oversight board or are there public members?)

Answer:

III.3 CODE OF ETHICS

Questions 9(a) Are public sector accountants/auditors required to adhere to a code of ethics? If yes, is the code legally enforceable? Who developed the code and when? Are there any substantial differences between the public and the private sector?

Answer:

9(b) Highlight the main differences between the national code of ethics and the revised July 2006 version of the IFAC Code of Ethics for Professional Accountants?

Answer:

page 9

IV MONITORING AND ENFORCEMENT

Questions 10(a) Is/Are there any institution/s monitoring the adoption of accounting standards and laws in the public sector? If yes, please name them. Is the capacity limited to monitoring or do these institutions have any power to enforce compliance with the standards and laws?

Answer:

10(b) Are the institutions independent from the preparers of financial statements?

Answer:

10(c) Is part of this role for public sector entities exercised by the auditors? If yes, please describe the role of the auditors in respect of monitoring and enforcement?

Answer:

10(d) Is part of this role for public sector entities exercised by institutions of the capital market, i.e. Securities Exchange? Is this limited to public sector entities issuing securities, i.e. government bonds?

Answer:

10(e) Are there any industry specific regulatory authorities for public sector entities, which are monitoring and/or enforcing accounting standards?

Answer:

V QUALITY AND AVAILABILITY OF FINANCIAL REPORTING

Questions 11(a) If IPSASs are not mandated in this country, are public sector entities allowed to publish financial reports adopting IPSAS? If yes, are they required to publish two separate sets of financial statements, one according to national standards/laws and another one adopting IPSAS?

Answer:

11(b) What are reporting deadlines for public sector entities? Are these deadlines honored by the reporting entities?

Answer:

11(c) Are financial reports publicly available? Is availability restricted somehow? Are the financial reports made available as paper copies and/or on the internet? Is there any administrative fee or price charged to those requiring a hard copy or downloading it from the internet?

Answer:

page 10

VI INFORMATION TECHNOLOGY

Questions 12(a) Provide a brief description of the IT systems in the field of accounting (hardware, software, databases) which are currently in use by the government. If necessary show differences between various units and/or levels of government.

Answer:

12(b) Is the software in use designed to cater for the needs of accrual accounting?

Answer:

12(c) If the software/databases are internationally know products (i.e. SAP, Oracle or similar), which modules/parts are implemented (i.e. FI, CO, etc.)?

Answer:

12(d) Based on a very broad and general assessment, is there a possibility for re-configuration/modification of the IT-system, if IPSAS or IPSAS-based national standards are to be adopted? Or is it rather necessary to the replace the IT-system altogether?

Answer:

VII. PUBLIC SECTOR Number Comment Levels of government Organizational entities on intermediate (e.g. provincial) level

Organizational entities on local (e.g. municipality) level

Large scale Government Business Enterprise

Name/Industry

The World Bank

Public Sector Auditing A Comparison to International Standards

Assessment of Auditing Standards

AUDIT DIAGNOSTIC TOOL - PART 2

April, 2009

CONTENTS

Foreword ................................................................................................................................................ 1General Information ............................................................................................................................... 2I. ISSAI 1210 Exposure Draft – Agreeing the Terms of Audit Engagements ....................................... 4II. ISSAI 1220 Quality Control for Audits of Historical Financial Information ................................... 6III. ISSAI 1230 Audit Documentation ................................................................................................... 8IV. ISSAI 1240 Exposure Draft - The Auditor's Responsibility Relating to Fraud in an Audit of Financial Statements ............................................................................................................................ 10V. ISSAI 1250 Exposure Draft - Considerations of Laws and Regulations in an Audit of Financial Statements ............................................................................................................................................ 12VI. ISSAI 1260 Communication of Audit Matters with those Charged with Governance .................. 15VII. ISSAI 1300 Planning an Audit of Financial Statements .............................................................. 17VIII. ISSAI 1315 Identifying and Assessing the Risks of Material Misstatements Through Understanding the Entity and its Environment .................................................................................... 20IX. ISSAI 1320 Exposure Draft - Materiality in Planning and Performing an Audit .......................... 23X. ISSAI 1330 The Auditor’s Responses to Assessed Risks ............................................................... 25XI. ISSAI 1450 Evaluation of Misstatements Identified during the Audit .......................................... 28XII. ISSAI 1500 Considering the Relevance and Reliability of Audit Evidence ................................ 30XIII. ISSAI 1530 Exposure Draft Due 2009 - Audit Sampling and Other Means of Testing ............. 32XIV. ISSAI 1550 Exposure Draft - Related Parties ............................................................................. 34XV. ISSAI 1700 Due 2009 - Reporting on Financial Statements (ISA 700) ...................................... 36XVI. ISSAI 4100 Exposure Draft – Compliance Audit for Financial Statements .............................. 39

Page 1

FOREWORD

As part of its public sector financial management reform program, the World Bank has developed a framework for assessing the variance between national and international standards in public sector auditing. This toolkit is developed for use in different countries to promote improvements in public sector auditing. This part of the review assesses the comparability of national auditing standards with the International Standards of Supreme Audit Institutions (ISSAI), auditing guidelines and the degree of actual compliance with the applicable national standards. The INTOSAI Professional Standards Committee has adopted a hierarchical four level framework of ISSAI standards:

Level 1 Founding Principles – Lima Declaration Level 2: Prerequisites for the Functioning of Supreme Audit Institutions Level 3 INTOSAI Auditing Standards Level 4: Auditing Guidelines. The standards have been progressively promulgated since January 2007 and some

of the standards have yet to be completed. It is likely that many SAIs will not yet have adopted all of the Level 4 guidelines developed to date. They are likely to have adopted the higher level standards, especially the Level 3 INTOSAI Auditing Standards, and developed in-house their own detailed audit manuals of procedures to implement these higher level standards. The status of Level 4 Auditing Guidelines as of December 2008 was:

Guidelines on financial audit – 9 endorsed by INTOSAI, 11 exposed as draft, 19 planned for 2010

Guidelines on compliance audit – 3 exposed as draft Guidelines on performance audit – 1 endorsed by INTOSAI, 1 planned for 2010. When each ISSAI Level 4 guideline is prepared by INTOSAI the text of the

corresponding International Standards for Auditing (ISA) standard is incorporated into the ISSAI. Where Level 4 guidelines are not yet endorsed or released in exposure draft for important standards, this diagnostic uses the relevant ISA.

This Diagnostic Tool Part 2 should be used in conjunction with the ISSAI published on the INTOSAI website (www.issai.org) and the IFAC IAASB 2008 Handbook of International Auditing, Assurance, and Ethics Pronouncements as of January 1, 2008.

References to specific Standards are placed in brackets at the end of each question. Note on Terminology Used in this Questionnaire

“Standard” refers to any applicable standards and implementation guidelines on financial audit and compliance audit issued as part of the ISSAI by of INTOSAI; any International Standard on Auditing (ISA) issued by the International Auditing and Assurance Standards Board of IFAC; and any International Education Guidelines (IEG) issued by IFAC.

Page 2

GENERAL INFORMATION Country:

Date of Preparation:

Individual(s) Responsible for Preparation:

Organizational Affiliation(s):

Address:

Telephone Number:

Fax Number:

E-mail Address:

1. Please identify the government entities which have to conduct audits of the financial reports or operations of government entities.

Page 3

2. Is there an official list of the differences between national auditing standards and ISSAI or ISA? If yes, please attach it to the diagnostic tool and indicate who prepared it. Please note that the existence of such a list does not alleviate the need to complete the diagnostic tool.

3. What bodies are responsible for establishing the national private sector and public sector

auditing standards? Please describe the bodies and to whom they report.

Page 4

I. ISSAI 1210 EXPOSURE DRAFT – AGREEING THE TERMS OF AUDIT ENGAGEMENTS Please refer to the whole text of ISSAI 1210. I.1 Adoption of the ISSAI

Questions Yes No 1(a) Has the Exposure Draft Agreeing the Terms of Audit Engagements been

adopted as a national standard?

Has ISSAI 1210 Agreeing the Terms of Audit Engagements been adopted as a national standard?

Comments:

1(b) If the answer to the above is NO what value would be added by adopting the standard?

Comments:

1(c) If a national standard has been adopted that differs from the international standard please set out the differences and provide a copy of the national standard.

Comments:

I.2 Establishing the Pre-conditions for the Audit Please refer to the whole text of ISSAI 1210

Questions Yes No 2(a) When establishing whether necessary preconditions for an audit are present, the financial reporting framework may often be prescribed by law and regulation. If public sector auditors determine that the framework prescribed by law and regulation is not acceptable they apply the requirements of paragraphs 6, 19 and 20 of ISA 210, and also consider informing the legislature or influencing standard setting by professional or regulatory organizations. The SAI could inform the legislature about its work program (ISSAI 1210 P5)

Comments:

2(b) The terms of an audit engagement in the public sector are normally mandated and therefore not subject to agreement with management, but the requirements in the standard are useful in establishing a common, formal understanding of the respective roles and responsibilities of management and the auditor. Since the public sector auditor is normally engaged by and reports to the legislature, agreements often need to be reached with both the legislature and management. Is there an engagement letter, and what discussions occur with management prior to the audit? (ISSAI 1210 P7)

Comments:

Page 5

I.3 Assess the Gap

Comment Please assess the differences between the audit practices and the international standard. If there is a national standard that differs from the international standard please assess to what extent, if any, the practice tends to differ from the “strict” wording of the national auditing standard(s)/regulation(s) addressing the requirements of this standard? Add a brief explanation about the reason(s) for any divergence.

Comments:

Page 6

II. ISSAI 1220 QUALITY CONTROL FOR AUDITS OF HISTORICAL FINANCIAL INFORMATION Please refer to the whole text of ISSAI 1220. II.1 Adoption of the ISSAI

Questions Yes No 1(a) Has ISSAI 1220 Quality Control for Audits of Historical Financial

Information been adopted as a national standard?

Comments:

1(b) If the answer to the above is NO what value would be added by adopting the standard?

Comments:

1(c) If a national standard has been adopted that differs from the international standard please set out the differences and provide a copy of the national standard.

Comments:

II.2 Quality Control Programs Please refer to the whole text of ISSAI 1220

Questions Yes No 2(a) Does the SAI have the quality control and assurance programs in place to ensure audit performance and results? (ISA 220 and ISSAI 1220 establish standards and provide guidance on quality control relating to the policies and procedures regarding audit work generally, and procedures regarding the work delegated to assistants on an individual audit. The standard requires that applicable quality control policies and procedures should be implemented on individual audits by the person delegated by the Auditor General to perform the audit.) Please provide a copy of any written quality control and assurance procedures.

Comments:

2(b) Do the quality control procedures cover the responsibility of the audit manager for:

• Assignment: the audit team has the appropriate capabilities, competence and

time to perform the audit. • Supervision: covering the following functions during the audit: (a) monitor

the progress of the audit, (b) become informed of and address significant accounting and auditing issues, and (c) resolve any differences of professional judgment between personnel and consider the level of consultation that is appropriate.

• Review: more experienced team members and the audit manager review work performed by less experienced team members?

Page 7

• Reporting: before the auditor’s report is issued, the audit manager, through review of the audit documentation and discussion with the engagement team, should be satisfied that sufficient appropriate audit evidence has been obtained to support the conclusions reached (IFAC ISA 220.21-220.29)

Comments:

II.3 Supervision of Auditors Please refer to the whole text of ISSAI 1220

Questions Yes No 3(a) Is there a process to record that work at each level and audit phase is properly supervised; and documented work is reviewed by a senior audit member? (INTOSAI Auditing Standards 3.0.3).

Comments:

3(b) Does the process of supervision ensure that working papers contain evidence adequately supporting all conclusions, recommendations and opinions? (INTOSAI Auditing Standards 3.0.3d)

Comments:

3(c) Does the supervision ensure that the audit report includes the audit conclusions, recommendations and opinions? (INTOSAI Auditing Standards 3.0.3f).

Comments:

3(d) Does the review process ensure that all evaluations and conclusions are soundly based and are supported by competent, relevant and reasonable audit evidence as the foundation for the final audit opinion or report? (INTOSAI Auditing Standards 3.2.4a)

Comments:

II.4 Assess the Gap

Comment Please assess the differences between the audit practices and the international standard. If there is a national standard that differs from the international standard please assess to what extent, if any, the practice tends to differ from the “strict” wording of the national auditing standard(s)/regulation(s) addressing the requirements of this standard? Add a brief explanation about the reason(s) for any divergence.

Comments:

Page 8

III. ISSAI 1230 AUDIT DOCUMENTATION Please refer to the whole text of ISSAI 1230. III.1 Adoption of the ISSAI

Questions Yes No 1(a) Has ISSAI 1230 Audit Documentation been adopted as a national

standard?

Comments:

1(b) If the answer to the above is NO what value would be added by adopting the standard?

Comments:

1(c) If a national standard has been adopted that differs from the international standard please set out the differences and provide a copy of the national standard.

Comments:

III.2 Procedures Please refer to the whole text of ISSAI 1230

Questions Yes No 2(a) Does the SAI have procedures for the confidentiality, safe custody, integrity, accessibility and retrieval of documentation covering the record of audit procedures performed, relevant audit evidence obtained, and conclusions the auditor reached? (ISSAI 1230 P6) Please describe the regulations and provide a copy of the relevant manual of procedures.

Comments:

2(b) Are there arrangements to ensure that the auditor obtains competent, relevant and reasonable evidence to support the auditor's judgment and conclusions regarding the organization, program, activity or function under audit? (INTOSAI Auditing Standards 3.5.1)

Comments:

2(c) In a Court of Accounts environment are procedures sufficient to support the requirements of the rules of evidence? (ISSAI 1230 P15)

Comments:

2(d) Are documentation procedures adequate to enable another auditor to understand and report to a scrutiny review on the significant matters arising from the audit including lack of compliance, violations of contract provisions, unauthorized expenditures, improper execution of the budget? (ISSAI 1230 P3)

Page 9

Comments:

2(e) Are there adequate procedures to ensure timely completion of the assembly of the audit file and working papers? (ISSAI 1230 P4)

Comments:

III.3 Assess the Gap

Comment Please assess the differences between the audit practices and the international standard. If there is a national standard that differs from the international standard please assess to what extent, if any, the practice tends to differ from the “strict” wording of the national auditing standard(s)/regulation(s) addressing the requirements of this standard? Add a brief explanation about the reason(s) for any divergence.

Comments:

Page 10

IV. ISSAI 1240 EXPOSURE DRAFT - THE AUDITOR'S RESPONSIBILITY RELATING TO FRAUD IN AN AUDIT OF FINANCIAL STATEMENTS Please refer to the whole text of ISSAI 1240. IV.1 Adoption of the ISSAI

Questions Yes No 1(a) Has ISSAI 1240 The Auditor's Responsibility Relating to Fraud in an

Audit of Financial Statements been adopted as a national standard?

Comments:

1(b) If the answer to the above is NO what value would be added by adopting the standard?

Comments:

1(c) If a national standard has been adopted that differs from the international standard please set out the differences and provide a copy of the national standard.

Comments:

IV.2 Management Representations Please refer to the whole text of ISSAI 1240

Questions Yes No 2(a) ISA 240 establishes standards and provides guidance on the auditor's responsibility to consider fraud and error in an audit of financial statements. Does the auditor make inquiries of management, and others within the entity as appropriate including Internal Audit, to determine whether they have knowledge of any actual, suspected or alleged fraud affecting the entity? (ISA 240.18 – ISA 240.19)

Comments: