g10 fx weekly 4 feb 2016

DESCRIPTION

ÂTRANSCRIPT

Insights.abnamro.nl/en

G10 FX Weekly

04 February 2016

Weak US data weigh on USD

Weak US data weigh on the US dollar

Yesterday, there were two interesting market reactions. The stronger-than-expected

ADP report failed to support the US dollar. This is because currency markets are

currently biased towards negative news from the US, because this would decrease

the possibility of Fed rate hikes this year. As a result, stronger data are ignored and

weaker data have a more substantial negative impact on the US dollar. The weaker-

than-expected Markit services PMI and ISM non-manufacturing caused a dramatic

sell-off in the US dollar yesterday. EUR/USD broke the physiological level of 1.10

again and rallied to a high of 1.1146 while USD/JPY dropped to a low of 117.06

thereby fully erasing the gains after the BoJ decision last week. This morning the US

dollar has remained under pressure. The ball is now back in the court of the ECB and

the BoJ (see below). We expect the ECB cut its deposit rate in two steps (March and

June) to -0.5% and to increase its asset purchase program by 10bn in March. This is

not fully priced in by financial market.

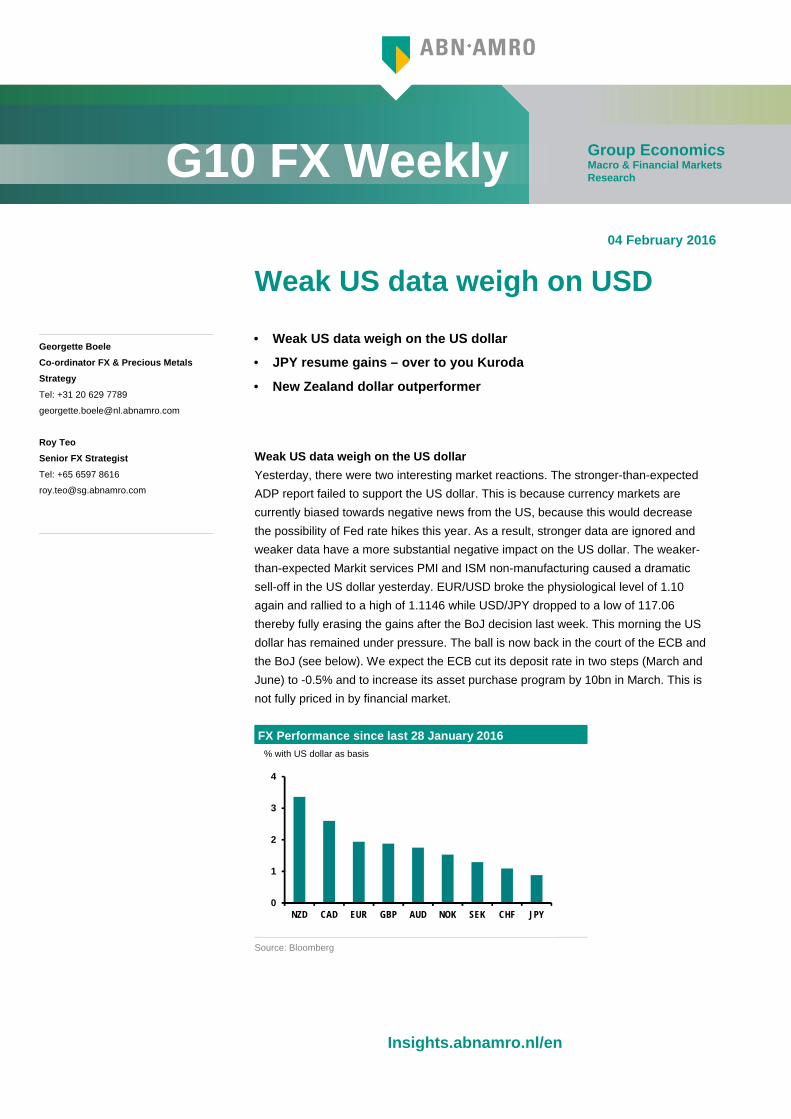

FX Performance since last 28 January 2016

% with US dollar as basis

Source: Bloomberg

0

1

2

3

4

NZD CAD EUR GBP AUD NOK SEK CHF JPY

Group EconomicsMacro & Financial MarketsResearch

Georgette Boele

Co-ordinator FX & Precious Metals

Strategy

Tel: +31 20 629 7789

Roy Teo

Senior FX Strategist

Tel: +65 6597 8616

• Weak US data weigh on the US dollar

• JPY resume gains – over to you Kuroda

• New Zealand dollar outperformer

2 G10 FX Weekly - Weak US data weigh on USD - 04 February 2016

It is likely that in the near-term, currency markets remain biased towards softer US

economic data and therefore the downward pressure on the dollar could continue.

However, improvement in investor sentiment and monetary policy divergence should

support the US dollar versus the euro and the yen during the course of this year.

JPY resume gains – over to you Kuroda

The Japanese yen (JPY) losses, after last Friday surprise move by the Bank of

Japan (BoJ) to introduce negative interest rates, were fully erased this week as safe

haven flows resumed and the US dollar fell on weak US data. Later this year, the BoJ

could increase monetary stimulus further if the yen remains resilient and continues to

weigh on the outlook for exports and inflation in Japan.

New Zealand dollar outperformer

The New Zealand dollar (NZD) was the strongest currency this week as the

unemployment rate in the last quarter of 2015 plunged from 6% to 5.3% and

employment grew 0.9% after falling 0.5% in the previous quarter. However,

weakness in the labour market remains as the labour force participation rate

recorded its third consecutive quarterly decline to its lowest level since 2013 Q2 and

there are no signs of a pick-up in wage growth. We maintain our view that the

Reserve Bank of New Zealand (RBNZ) is likely to lower the Official Cash Rate (OCR)

by 25bp to 2.25% as soon as March. Around 30% of this is priced in by financial

markets. Our year end NZD/USD forecast is 0.58.

ABN AMRO major currency forecasts

Changes in red/bold

Source: ABN AMRO Group Economics

04-Feb Close 2015 Q1 2016 Q2 2016 Q3 2016 Q4 2016 Q1 2017 Q2 2017 Q3 2017 Q4 2017

EUR/USD 1.1160 1.0866 1.05 1.00 0.95 0.90 0.92 0.96 0.98 1.00

USD/JPY 117.62 120.20 121 125 130 135 132 130 128 125

EUR/JPY 131.26 130.61 127 125 124 122 121 125 125 125

GBP/USD 1.4649 1.4734 1.40 1.32 1.23 1.22 1.28 1.37 1.44 1.52

EUR/GBP 0.7618 0.7375 0.75 0.76 0.77 0.74 0.72 0.70 0.68 0.66

USD/CHF 1.0030 0.9998 1.05 1.12 1.20 1.28 1.25 1.20 1.22 1.20

EUR/CHF 1.1193 1.0863 1.10 1.12 1.14 1.15 1.15 1.15 1.20 1.20

AUD/USD 0.7219 0.7290 0.68 0.66 0.64 0.62 0.64 0.68 0.70 0.72

NZD/USD 0.6706 0.6839 0.62 0.60 0.58 0.58 0.60 0.62 0.64 0.66

USD/CAD 1.3682 1.3828 1.44 1.46 1.47 1.48 1.40 1.38 1.35 1.30

EUR/SEK 9.3703 9.1901 9.50 9.50 9.50 9.50 9.25 9.00 8.75 8.50

EUR/NOK 9.4805 9.6178 9.50 9.25 9.00 9.00 8.75 8.50 8.25 8.00

EUR/DKK 7.4632 7.4630 7.46 7.46 7.46 7.46 7.46 7.46 7.46 7.46

3 G10 FX Weekly - Weak US data weigh on USD - 04 February 2016

Find out more about Group Economics at: https://insights.abnamro.nl/en/

DISCLAIMER

ABN AMRO BankGustav Mahlerlaan 10 (visiting address)P.O. Box 2831000 EA AmsterdamThe Netherlands

This document has been prepared by ABN AMRO. It is solely intended to provide financial and general information on economics.The information in this document is strictly proprietary and is being supplied toyou solely for your information. It may not (in whole or in part) be reproduced, distributed or passed to a third party or used for any other purposes than stated above. This document is informative in nature and does not constitute an offer of securities to the public, nor a solicitation to make such an offer.

No reliance may be placed for any purposes whatsoever on the information, opinions, forecasts and assumptions contained in the document or on its completeness, accuracy or fairness. No representation or warranty, express or implied, is given by or on behalf of ABN AMRO, or any of its directors, officers, agents, affiliates, group companies, or employees as to the accuracy or completeness of the information contained in this document and no liability is accepted for any loss, arising, directly or indirectly, from any use of such information. The views and opinions expressed herein may be subject to change at any given time and ABN AMRO is under no obligation to update the information contained in this document after the date thereof.

Before investing in any product of ABN AMRO Bank N.V., you should obtain information on various financial and other risks andany possible restrictions that you and your investments activities may encounter under applicable laws and regulations. If, after reading this document, you consider investing in a product, you are advised to discuss such an investment with your relationship manager or personal advisor and check whether the relevant product –considering the risks involved- is appropriate within your investment activities. The value of your investments may fluctuate. Past performance is no guarantee for future returns. ABN AMRO reserves the right to make amendments to this material.

© Copyright 2016 ABN AMRO Bank N.V. and affiliated companies ("ABN AMRO").