g. investor day - wbl print final - air liquide · quick connector easy identification altop albee...

TRANSCRIPT

Ambition2015 Objectives

December 13, 2010

Business linesto meet the challenge

Ambition2015 Objectives

December 13, 2010

Business linesto meet the challenge

Industrial Merchant

Jean-Baptiste RIPARTVice-President, World Business LineIndustrial Merchant

Air Liquide, world leader in gases for industry, health and the environment Investor Day – December 2010 3

Largest Industrial Gas Market

Growth > industrial production

€ 24 bn

2009 Market

Industrial Merchant

Business Model

Local density

Logistics

Premium through Innovation

Contracts:

Mid-term

Rental income

Price indexation

AdvancedEconomies

68%

DevelopingEconomies

32%

Air Liquide, world leader in gases for industry, health and the environment Investor Day – December 2010 4

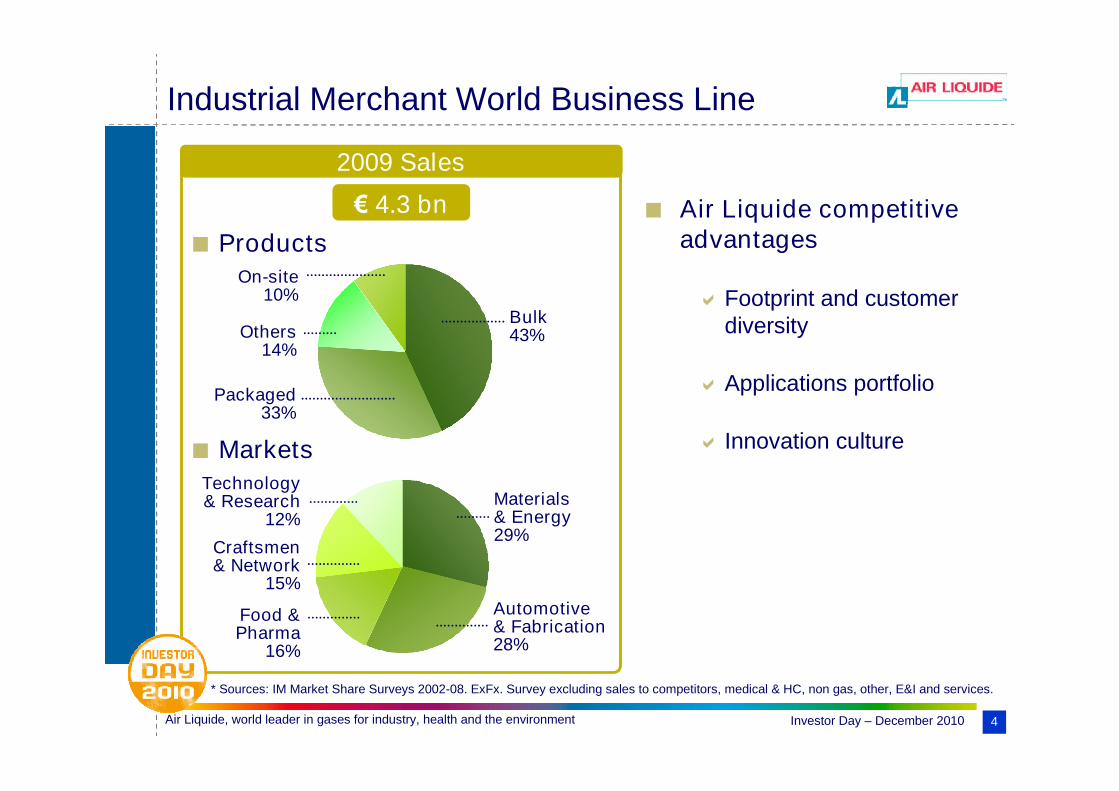

Industrial Merchant World Business Line

2009 Sales

ProductsOn-site

10%

Packaged33%

Others14%

Bulk43%

MarketsTechnology& Research

12%

Automotive& Fabrication28%

Craftsmen& Network

15%

Materials& Energy29%

Food &Pharma

16%

€ 4.3 bn

* Sources: IM Market Share Surveys 2002-08. ExFx. Survey excluding sales to competitors, medical & HC, non gas, other, E&I and services.

Air Liquide competitiveadvantages

Footprint and customerdiversity

Applications portfolio

Innovation culture

Air Liquide, world leader in gases for industry, health and the environment Investor Day – December 2010 5

Acceleration in developing economies

Technology evolution:

New Markets: H2 based mobility, LED fabrication

Green trends

New applications: water-treatment, food freezing, modifiedatmosphere preservation, window insulation, small cylinders, etc…

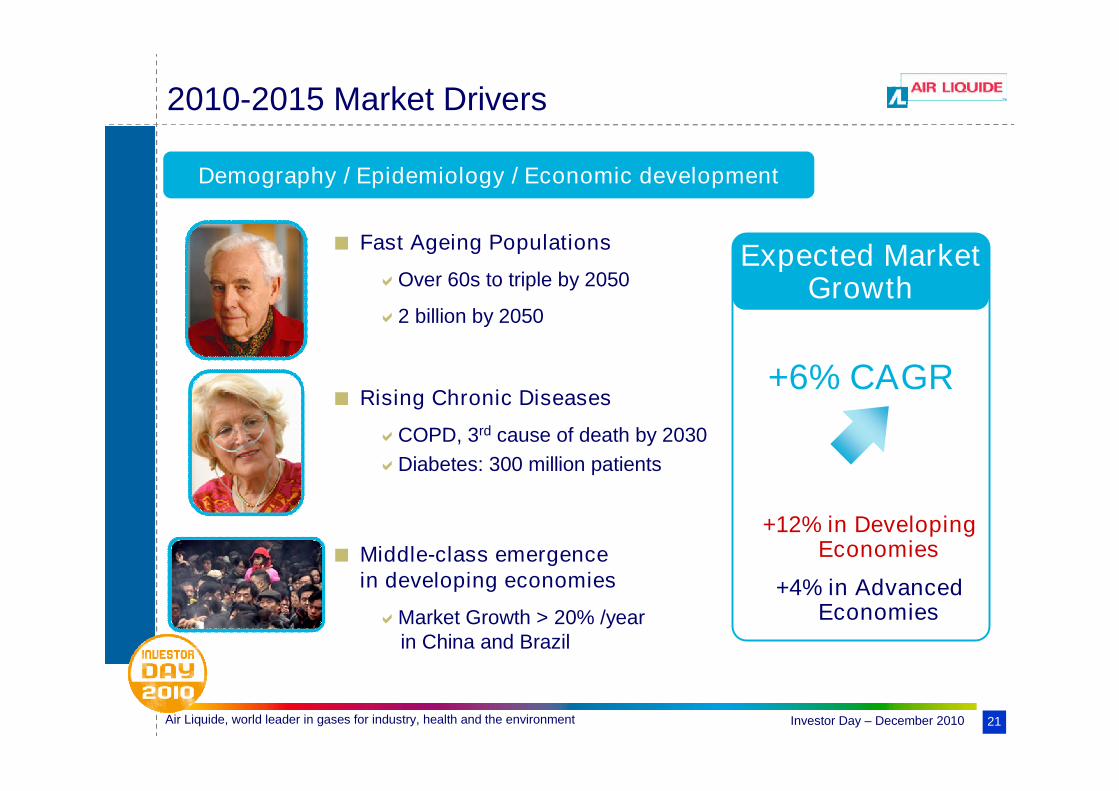

2010-2015 Market Drivers

* Source: IM Market Assessment 2009, Excluding Equipment & Installation, constant prices.

+6% CAGR

Gas Market*

€ 24 bn € 35 bn

2009 2015

Developing +11%

Advanced +3%

68%32% 57%43%

Air Liquide, world leader in gases for industry, health and the environment Investor Day – December 2010 6

Medium Term Objectives

Acquisitions

Applications roll-out

New offers

New markets

Industrial optimization

PERFORM TRANSFORM

Spread best practices:

Safety

Customer focus

Innovation cycle

Safety best practice everywhere

Value-added applications across geographies

Further logistics efficiency

Objectives

Examples of initiatives & projects:

Air Liquide, world leader in gases for industry, health and the environment Investor Day – December 2010 7

Listening to customers > New offers

Listening to customers…

Light cylindersVolume indicator

Safe to useValue for money

Quick connector

Easy identification

Altop Albee

New offers

Smartop

Quality

Air Liquide, world leader in gases for industry, health and the environment Investor Day – December 2010 8

2015 Objectives

GroupCAGR

+8 to +10%*

CAGR: +6 to +9%Industrial Merchant 2015

Large Industries 2015

Healthcare 2015Healthcare 2015

Electronics 2015

* In a normal environment

Ambition2015 Objectives

December 13, 2010

Large Industries& Engineering

Business linesto meet the challenge

Ron LABARREGroup Vice PresidentLarge Industries - World Business Line

Air Liquide, world leader in gases for industry, health and the environment Investor Day – December 2010 10

Large Industries

2009 Market

€ 10 bn*

Business Model

Air Liquide ownershipand operation of units

Industrial basins and networks

Investment model and strongcash flow

Contracts: Long term Price indexation Uptake commitments Clear risk definition

Mainly Air Gases and HyCOCogen not included in markets figures

AdvancedEconomies

70%

DevelopingEconomies

30%

Air Liquide, world leader in gases for industry, health and the environment Investor Day – December 2010 11

Large Industries World Business Line

2009 Sales

HyCO

27%

Products

Air Gases51%

Air Liquide competitiveadvantages:

Worldwide Large Industriesleadership

In house Engineering andproprietary technologies

Rigorous project selectionand strong execution

Largest pipeline networkand basin development

€ 3.2 bn

Cogen

& Other

22%

Markets

Metal20% Chemical

39%

Energy

29%

Elec & Other12%

Air Liquide, world leader in gases for industry, health and the environment Investor Day – December 2010 12

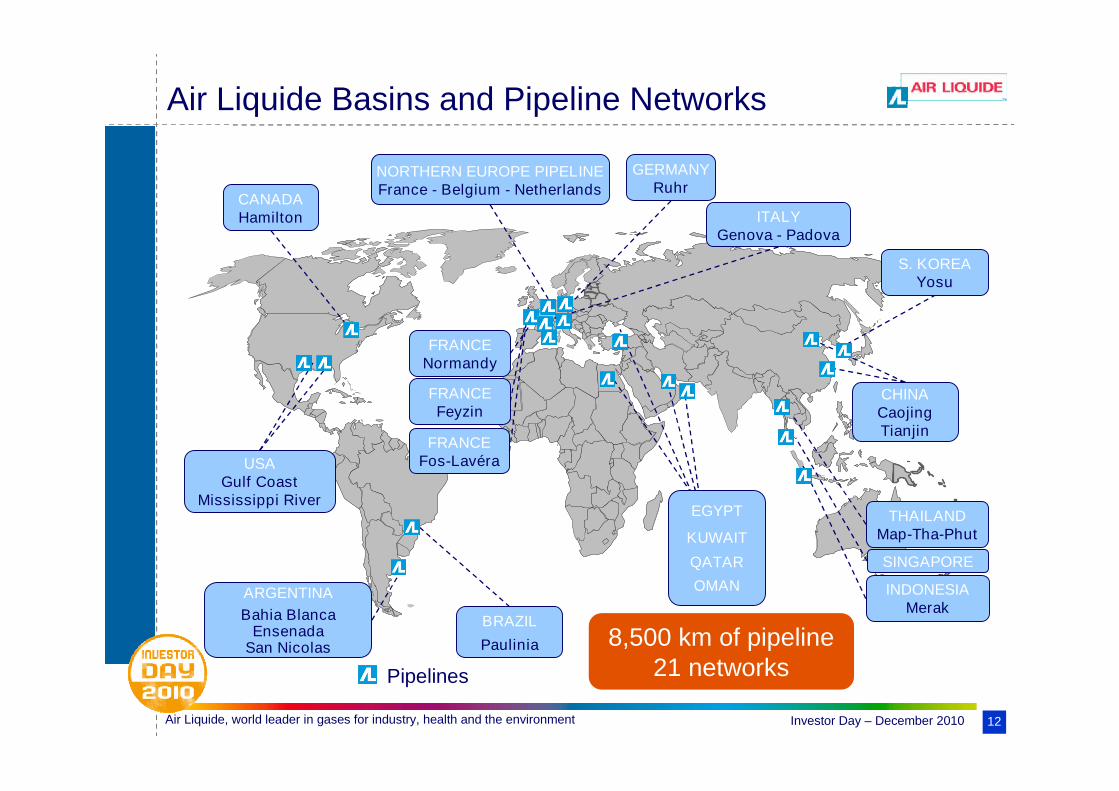

Air Liquide Basins and Pipeline Networks

NORTHERN EUROPE PIPELINEFrance - Belgium - Netherlands

CANADAHamilton

GERMANYRuhr

FRANCENormandy

FRANCEFos-Lavéra

FRANCEFeyzin

ITALYGenova - Padova

S. KOREAYosu

CHINACaojingTianjin

THAILANDMap-Tha-Phut

SINGAPORE

BRAZIL

Paulinia

ARGENTINA

Bahia BlancaEnsenada

San Nicolas

INDONESIAMerak

Pipelines

USAGulf Coast

Mississippi River

8,500 km of pipeline21 networks

EGYPT

KUWAIT

QATAR

OMAN

Air Liquide, world leader in gases for industry, health and the environment Investor Day – December 2010 13

Engineering & Construction

Business Model

Advanced ProprietaryTechnologies

Air Gases, HyCO

Gasification

Refining/Chemicals

Biofuels

Amplified by Lurgi acquisition

Competitiveness

Design to cost

Low cost countrymanufacturing

Execution

Strong project management

International breadth

Markets

Orders in Hand (2009)

Infrastructure investmentsin Developing geographies

Energy market growth

Emerging environmental focus

€ 4.4 bn

Air Gases

51%Traditional

17%

Alternative

10%

HyCO

18%

Renewable

4%

Fuels

Air Liquide, world leader in gases for industry, health and the environment Investor Day – December 2010 14

Growth in Outsourcing

35% of O2 production today

20% of H2 production today

New capacities in developing markets

80% of expected market growth

Renovation in advanced markets

Green technologies

2010-2015 Market Drivers

+9% CAGR

Over the Fence Gas Market (Excluding cogeneration. At constant price.)

€ 10 bn € 18 bn

2009 2015

Developing +20%

Advanced +4%

70%30% 55%45%

Air Liquide, world leader in gases for industry, health and the environment Investor Day – December 2010 15

Medium Term Objectives

Process SafetyManagement

Reliability

Standard & ModularPlants

Expanded Offer

PERFORM TRANSFORM

Account managementfocus on futureleading customers

Recruit, train, retainin Developingmarkets

Grow faster than the market

Enhance Competitiveness through internal and customer processes

Objectives

Examples of initiatives & projects:

Air Liquide, world leader in gases for industry, health and the environment Investor Day – December 2010 16

OBERHAUSEN

Basin development: Ruhr Valley

New 2,300 tpdASU decidedin Oberhausen

Acquisition ofhydrogenpipeline

Extension of H2business &connection toOXEA

Messer acquisition Takeover ofOXEA syngasplant

1999 2001-04 2004 2008 2010

RuhrRuhr

Ruh

ein

DÜSSELDORF

ESSEN DORTMUND

DUISBURG

GELSENKIRCHEN

LEVERKUSEN

UERDINGEN

H2 N2O2Syngas

Steam

AirLiquide

RuhrPipeline

now supplies:MARL

Air Liquide, world leader in gases for industry, health and the environment Investor Day – December 2010 17

2015 Objectives

CAGR: +6 to +9%Industrial Merchant 2015

Large Industries 2015

Healthcare 2015Healthcare 2015

Electronics 2015

CAGR: +9 to +11%

* In a normal environment

GroupCAGR

+8 to +10%*

Ambition2015 Objectives

December 13, 2010

Business linesto meet the challenge

Healthcare

Pascal VINETVice-President, Healthcare WorldBusiness Line and Operations

Air Liquide, world leader in gases for industry, health and the environment Investor Day – December 2010 19

Healthcare

€ 4 bn Medical gases

€ 9 bn Homecare

+ Hygiene estimated at € 8 bn

€ 13 bn

2009 Market

AdvancedEconomies

87%

DevelopingEconomies

13%

Business Model

Steady growth

Medical and regulatory obligations, and multiple stakeholders

Health System pricing pressure, compensated by productivity

Low capital intensity

Air Liquide, world leader in gases for industry, health and the environment Investor Day – December 2010 20

Healthcare World Business Line

2009 Sales

Markets

Air Liquide competitiveadvantages

European leadership

Replicable homecaremodel: 600,000 patientstoday

New capacity fromIndustrial Merchant

Innovation portfolio

Proprietary IT systems

Homecare43%

Chronic patients:O2 Therapy,Ventilation,Sleep Apnea,Diabetes

Hygiene20%

AntisepticsDisinfectants

Hospital37%

Gaseous drugs &related servicesfor hospitals

€ 1.8 bn

Air Liquide, world leader in gases for industry, health and the environment Investor Day – December 2010 21

+6% CAGR

+12% in DevelopingEconomies

+4% in AdvancedEconomies

Demography / Epidemiology / Economic development

Fast Ageing Populations

Over 60s to triple by 2050

2 billion by 2050

Rising Chronic Diseases

COPD, 3rd cause of death by 2030

Diabetes: 300 million patients

Middle-class emergencein developing economies

Market Growth > 20% /yearin China and Brazil

2010-2015 Market Drivers

Expected MarketGrowth

Air Liquide, world leader in gases for industry, health and the environment Investor Day – December 2010 22

Medium Term Objectives

Geographic andoffer expansion

Acquisitions

Innovation

Efficiency

PERFORM TRANSFORM

Anticipateregulatorycompliance

Enhance medicalexpertise

#1 in Medical Oxygen

1,000,000 patients in Homecare in 2015

Objectives

Examples of initiatives & projects:

Air Liquide, world leader in gases for industry, health and the environment Investor Day – December 2010 23

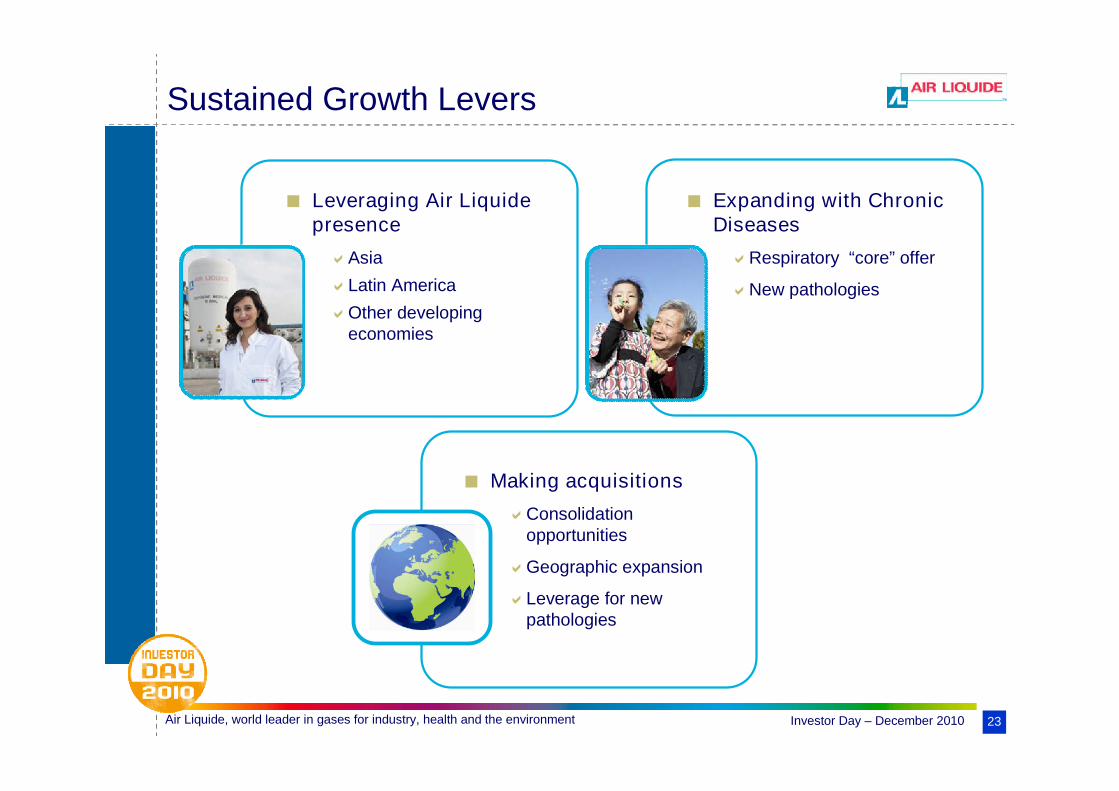

Sustained Growth Levers

Leveraging Air Liquidepresence

Asia

Latin America

Other developingeconomies

Expanding with ChronicDiseases

Respiratory “core” offer

New pathologies

Making acquisitions

Consolidationopportunities

Geographic expansion

Leverage for newpathologies

Air Liquide, world leader in gases for industry, health and the environment Investor Day – December 2010 24

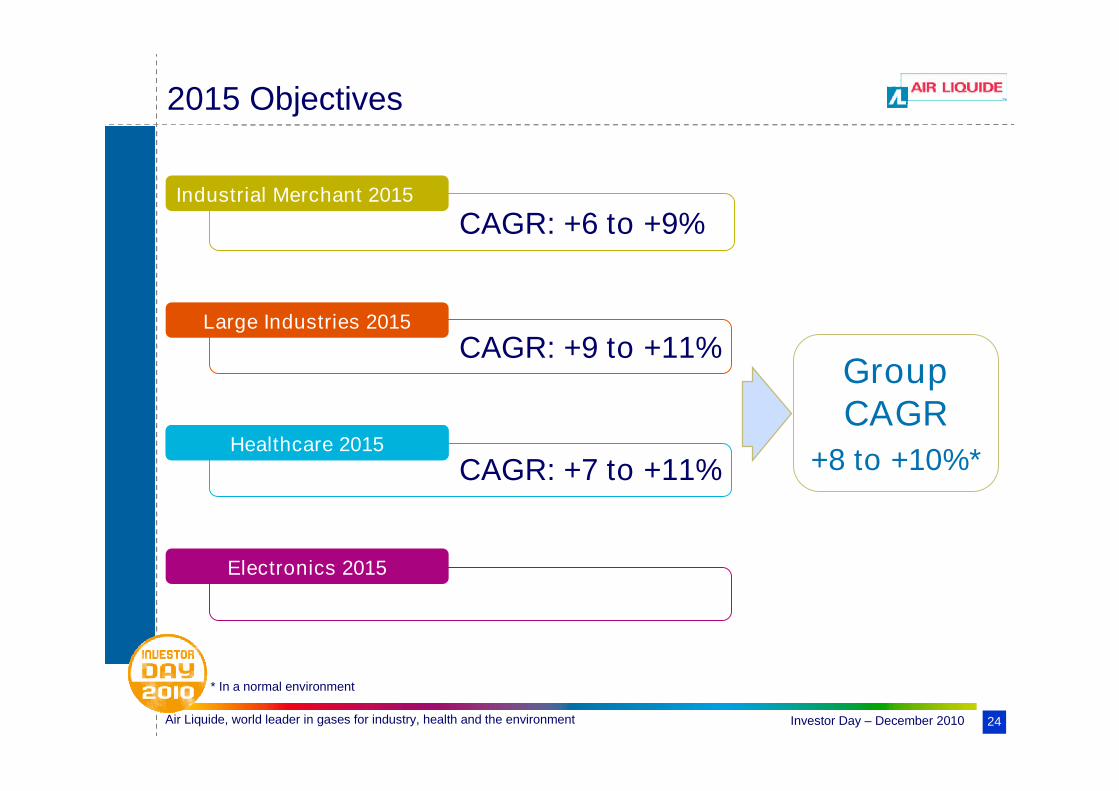

2015 Objectives

CAGR: +6 to +9%Industrial Merchant 2015

Large Industries 2015

CAGR: +9 to +11%

Healthcare 2015

CAGR: +7 to +11%Healthcare 2015

Electronics 2015

* In a normal environment

GroupCAGR

+8 to +10%*

December 13, 2010

Business linesto meet the challenge

Electronics

Francisco MARTINSVice-President, World Business LineElectronics

Ambition2015 Objectives

Air Liquide, world leader in gases for industry, health and the environment Investor Day – December 2010 26

> 80% in Asia

Semiconductors (SC)~ +8%/year

Flat Panel Display (FPD)> +10%/year

Solar Photovoltaic (PV)> +20%/year

Cyclical customer demand.

Electronics

€ 3.7 bn

2009 Market

Business Model

Long-term contracts for Carrier Gas supply

Growing volume requirements for Specialty Gases

Technology road maps driving new molecules

Markets

SC 69%FPD 24%

PV 7%

FPD24%

Geography

Taiwan24%

USA 10%

China 9%

Japan 20%

Europe 6%

Korea26%

Sing. 4%

Air Liquide, world leader in gases for industry, health and the environment Investor Day – December 2010 27

Markets

Semi-conductors81%

Flat Panel

Displays

11%

Photovoltaic

8%

Electronics World Business Line

2009 Sales

AL competitive advantages

Co-leader in Electronics

Early player & leader in PV

R&D in Japan, Europeand US

New molecules development

Silane production

Products

ESGs

26%

CarrierGases39%

Services

14%

Equipment &

Installation

21%

€ 0.9 bn

Air Liquide, world leader in gases for industry, health and the environment Investor Day – December 2010 28

2010-2015 Market Drivers

New growth cycle driven by:

Mobility

Increasing standard of living

Dynamic Solar energy demand

Production focused in Asia

Gas Market*

€ 3.3 bn

41%59%

€ 5.4 bn

2010 2015

32%68%

Developing +12%

Advanced +4%

(excluding Equipment & Installation, Chemicals. At constant price.)

+10% CAGR

Air Liquide, world leader in gases for industry, health and the environment Investor Day – December 2010 29

Medium Term Objectives

Further strengthen positions in Asia

Differentiate through innovative Molecule offers

Objectives

PERFORM

Capture PV growth

Improve ESG efficiency

Intensify ALOHATM(1)

initiative

TRANSFORM

Expand relationswith industry leaders

Strengthen E&I

organization

(1) Advanced materials used for thin-film deposition in SC & PV manufacturing processes

Examples of initiatives & projects:

Air Liquide, world leader in gases for industry, health and the environment Investor Day – December 2010 30

2015 Objectives

CAGR: +6 to +9%Industrial Merchant 2015

Large Industries 2015

CAGR: +9 to +11%

Healthcare 2015

CAGR: +7 to +11%Healthcare 2015

Electronics 2015

CAGR: +8 to +10%

* In a normal environment

GroupCAGR

+8 to +10%*