future opportunities in paper based packaging markets in paper-based packaging... · us global...

TRANSCRIPT

Future Opportunities in

Paper Based Packaging

MarketsMarketsPrepared for

2011 ICE Conference

By

Frank PerkowskiBusiness Development Advisory

April 7, 2011

�Sustainability focus has changed the game

�Historic share losses to film have stabilized paper demand at a base level

� Improved paper supply chain dynamics

Why Paper Based Packaging Materials Warrant a Second Look

2

�Paper process / product improvements have opened the door to new markets

�Raw material costs reflect improved value proposition versus film and other materials

�Predictions by some for continued high growth for plastic materials questionable.

� Paper Industry Overview

� Paper Packaging Markets and Grades

� Growth Opportunities and Challenges in Paperboard Packaging Markets

Presentation Outline

3

Paperboard Packaging Markets

� Growth Opportunities and Challenges in LWT Paper Packaging Markets

� Paper Converter Opportunities and Implications

� US paper industry is mature with overall volume flat to declining in certain segments

� Industry returns have fallen short of its cost of capital in 16 of the past 20 years

� US Industry has undergone significant consolidation and mill

Paper Industry Overview

4

� US Industry has undergone significant consolidation and mill rationalizations in the past 15 years

� Industry investment has shifted dramatically to lower cost developing countries

� US global competitiveness has declined, assets are aging, and current investment levels are well below depreciation levels.

� US decline being driven by electronic substitution in printing / publishing markets, plastic substitution in some packaging markets, and a shift to lower cost production facilities in Asia and Latin America

� Recessionary periods driving use of lower cost substitutes

� New growth opportunities emerging in energy (bio refineries and renewable energy), globalization, sustainability, new

Paper Industry Overview - Continued

5

and renewable energy), globalization, sustainability, new fibers, value added papers.

� New business models emerging:

� Global focus within selected markets� More consolidated supply base with market leverage� Bankruptcy followed by leaner organizations� Increased focus on outsourced operations � Forward integration into converting / related

businesses

Paper Based Packaging

6

Packaging Overview

� Paper demand in packaging markets has kept pace with

GDP growth overall

� Shift to overseas manufacturing has been major source of

volume loss for paper mills and converters

� Displacement by plastics in some applications has also

resulted in capacity reductions is certain segments

Paper Based Packaging Industry Overview

7

resulted in capacity reductions is certain segments

� Containerboard / corrugated business is still world class

despite relatively flat demand

� Folding cartons and boxboard markets are stable and

threats are minimal

� New growth opportunities exist for lightweight papers.

� Higher concentration levels across every segment has led to higher /

more stable price levels and cycles

� Financial buyers, fewer mills, and historically low returns have led to

increased discipline within the industry in recent years

� No new capacity - many machines being shutdown or re-focused

� Producers / mills have become more focused on a limited number of

Paper Based Packaging Supply Base Trends

8

� Producers / mills have become more focused on a limited number of

grades and markets

� Commodity grades being increasingly supplied by low cost, pulp

integrated mills with large scale paper machines

� More specialized grades provided by smaller, non integrated mills with

broader paper machine capabilities (but much higher costs)

� Mid level machines continue to be repositioned to compete with smaller

machines that eventually get shutdown.

Broad Array of Paper Based Packaging Grades and Applications

Major Paper Grade Primary Packaging

Product

Approx Tons

(millions)

CAGR %

(2010-

2014)

Comments

Containerboard (Linerboard /

Medium)

Corrugated boxes 21.5 0.4% Little substitution threat

White Top Linerboard Graphic corrugated 2.2 1.5% Expanded applications

Uncoated Recycled Board Cores / tubes /

backing

1.5 0.4% Stable / low value business

Coated Recycled Board Folding cartons 2.5 0.4% Sustainability is main driver

Coated Unbleached Kraft Carrier cartons 2.1 0.7% High strength

Major Packaging Paper / Board Grades

9

Coated Unbleached Kraft Carrier cartons 2.1 0.7% High strength

Bleached Board (SBS) Folding cartons 2.4 0.6% Premium positioning

Total Paperboard 32.2 0.5%

Label Facestock Labels 0.6 2.1% Still high growth but maturing

Release Base / Liner Labels 0.7 2.2% Follows label demand

Kraft Papers Multiwall and kraft

bags

1.5 -0.8% Still in decline but recovering

Packaging Papers Product wraps / bags

/ covers

0.9 1.5% Well positioned in flexible

packaging

Bristol papers Tags 0.2 1.2% Niche applications

Foodservice / Processing

Papers

Sandwich /food

wraps

0.5 1.6% Little substitution threat

Total Paper 4.4 1.3%

Paper Raw Material Prices Have Lagged Plastic Raw Material Prices

140

150

160

170

US

Pri

ce In

de

x (

20

01

= 1

00

)

Raw Packaging Material Price Trends

Plastic resins and

materials

Woodpulp

1

0

80

90

100

110

120

130

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 YTD

US

Pri

ce In

de

x (

20

01

= 1

00

)

Aluminum sheet

/ plate / foil

All commodities

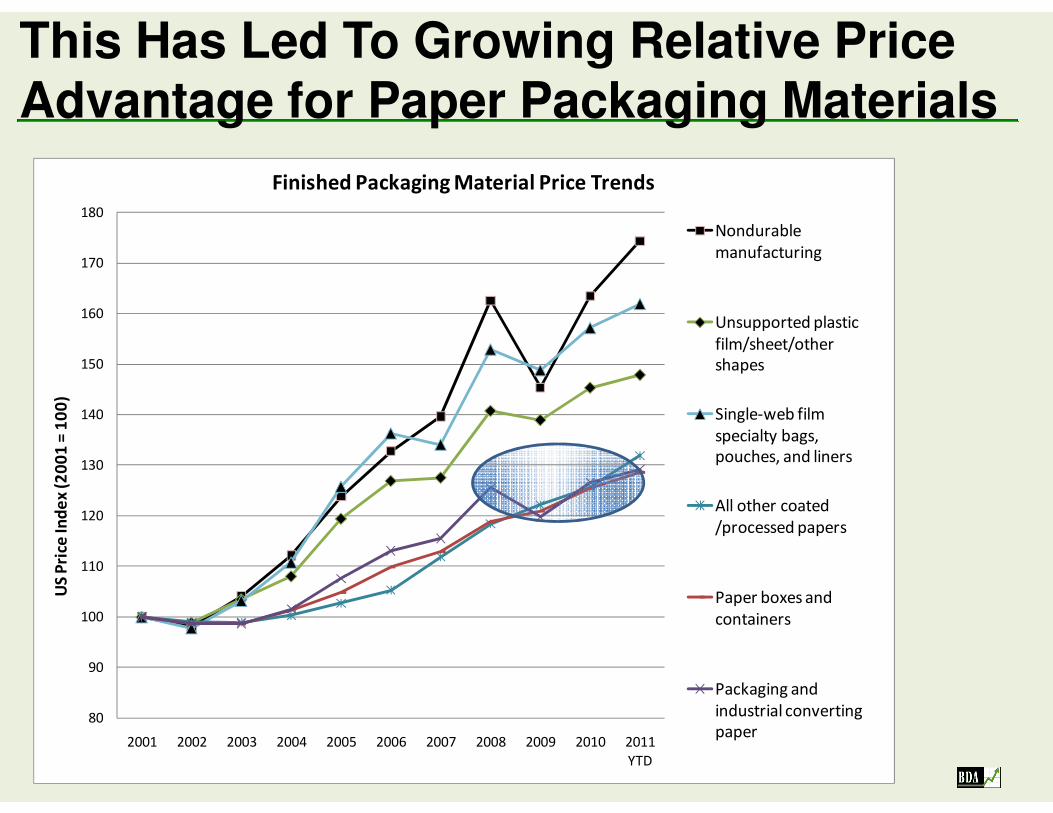

This Has Led To Growing Relative Price Advantage for Paper Packaging Materials

140

150

160

170

180

US

Pri

ce In

de

x (

20

01

= 1

00

)

Finished Packaging Material Price Trends

Nondurable

manufacturing

Unsupported plastic

film/sheet/other

shapes

Single-web film

1

1

80

90

100

110

120

130

140

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

YTD

US

Pri

ce In

de

x (

20

01

= 1

00

)

Single-web film

specialty bags,

pouches, and liners

All other coated

/processed papers

Paper boxes and

containers

Packaging and

industrial converting

paper

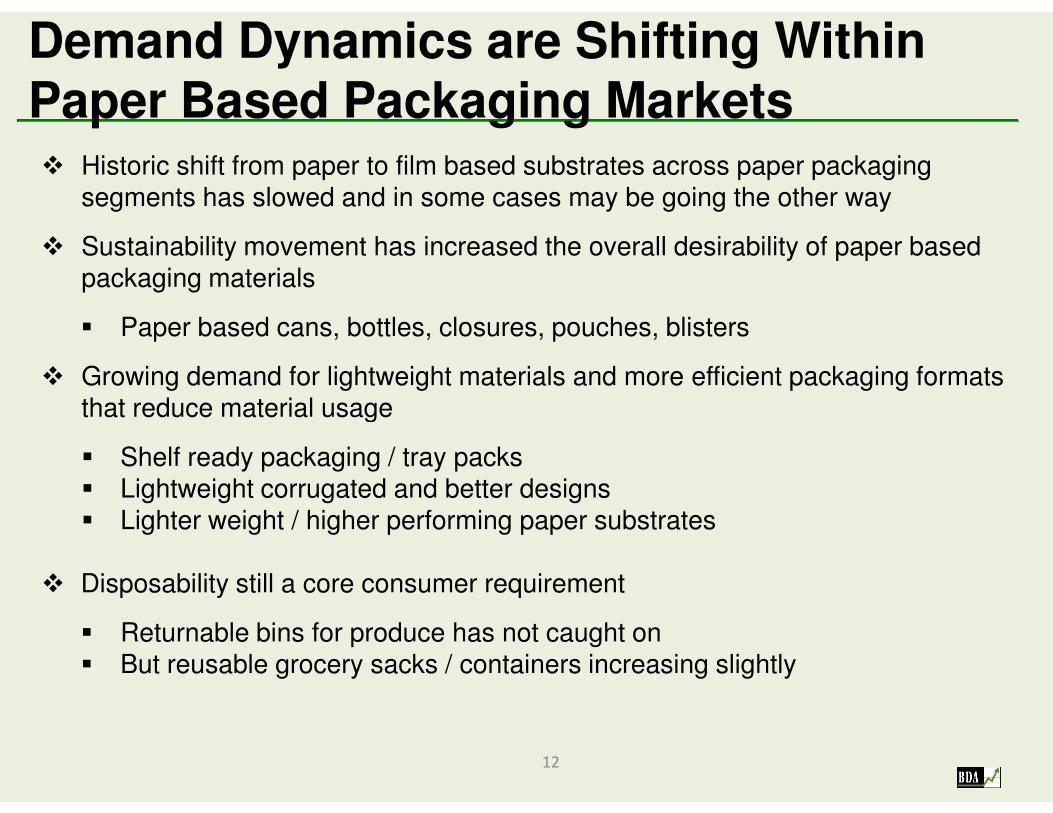

� Historic shift from paper to film based substrates across paper packaging

segments has slowed and in some cases may be going the other way

� Sustainability movement has increased the overall desirability of paper based

packaging materials

� Paper based cans, bottles, closures, pouches, blisters

� Growing demand for lightweight materials and more efficient packaging formats

that reduce material usage

Demand Dynamics are Shifting Within Paper Based Packaging Markets

12

that reduce material usage

� Shelf ready packaging / tray packs

� Lightweight corrugated and better designs

� Lighter weight / higher performing paper substrates

� Disposability still a core consumer requirement

� Returnable bins for produce has not caught on

� But reusable grocery sacks / containers increasing slightly

Major Gaps / Unmet Needs

• More environmentally

friendly packaging

• Security features that

reduce counterfeiting

Paper Packaging Offers Solutions That Meet Emerging Customer Needs

Paper Solutions

• High recycled content, certified paper,

exotic fibers, chlorine free, low impact

processes, cradle to cradle

• Watermarks, embedded fibers,

laminations, printing solutions

13

• Packaging with additional

functional benefits

• Smart / intelligent

packaging features

• More efficient supply

chains

• Durable substrates, exotic surfaces /

finishes, functional coatings, reusability,

high impact features

• Chemical sensors / reactors, embedded

chips, battery inserts, nano materials

• Better information systems, increased

responsiveness, forward integrated

processes, broad-based solutions.

Paperboard Packaging

14

Packaging Overview

Paperboard Packaging Markets Will Undergo Significant Shifts in Future

� More concentrated supply chains will result in a more healthy, stable supply

base

� In corrugated, volume / demand will be impacted by light weighting

initiatives, more efficient packaging designs, retail ready packaging, and

increased use of pallet wraps and trays to replace standard corrugated

boxes

� Improved print surfaces and technologies will fuel continued share

15

� Improved print surfaces and technologies will fuel continued share

growth in retail applications

� In folding cartons, bleached board, recycled board and coated unbleached

board will continue to trade business but with no major volume shift overall

� But some traditional folding carton applications will continue to shift

to mini flute corrugated and flexible packaging solutions that better

meet performance / sustainability needs.

� Major growth opportunities exist to displace metal and other rigid

containers for sustainability / cost benefits.

Recent / Developing Innovations in Paperboard Packaging Materials

Retail ready

packaging /

high graphics

Metal can

replacement

Molded fiber

bottles

16

Bag in Box

cartons/ glass

replacement

Mini flutes /

wax

replacement

Laminated /

barrier

treated

cartons

Plastic

clamshell

replacement

Lightweight Packaging

17

Packaging Papers

Overview

LWT Packaging Paper Product Overview

17%

14%

10%

9%

5%4% 4%

2009 US Packaging Paper Demand by Major Application Category

Release base

papers

Label papers

Product packaging

papers - 1 ply

Kraft bag papers

Multiwall bag

18

13%

13%

11%

10% Multiwall bag

papers

Product packaging

papers -M ply

Industrial wrapping

papers

Foodservice papers

Tag packaging

papers

Food processing

papersSource: BDA NA Packaging Paper Study

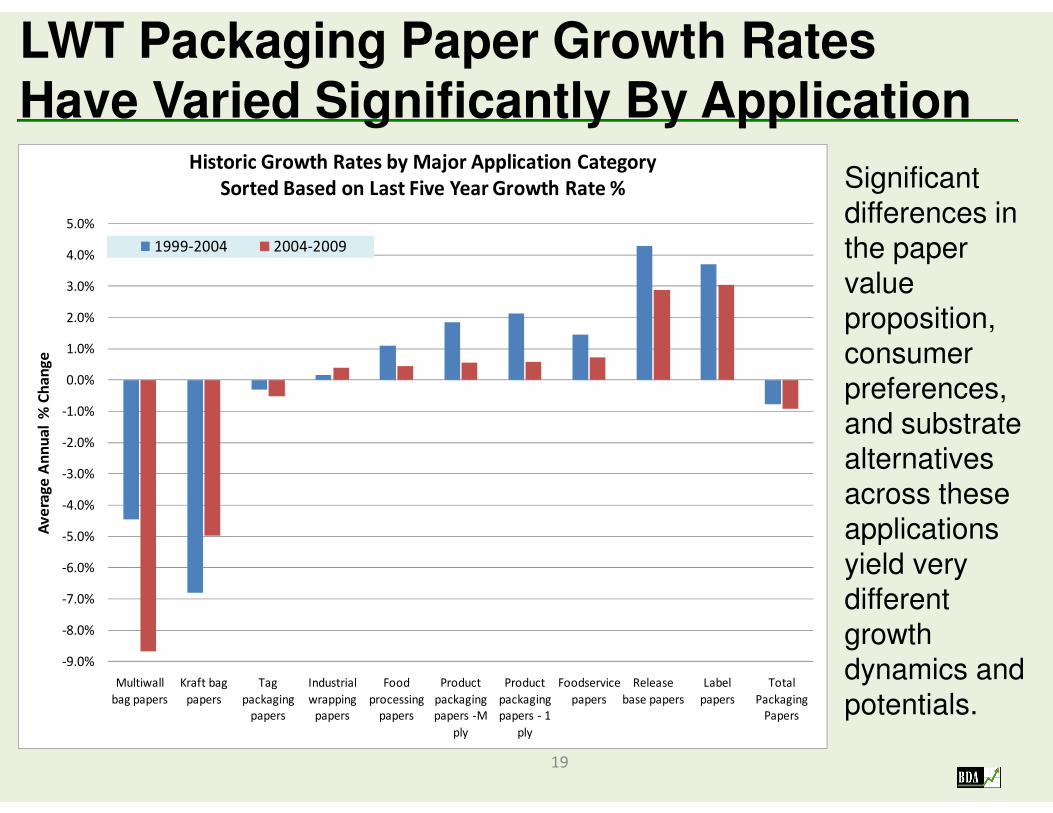

Significant

differences in

the paper

value

proposition,

consumer

preferences,

LWT Packaging Paper Growth Rates Have Varied Significantly By Application

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

Av

era

ge

An

nu

al

% C

ha

ng

e

Historic Growth Rates by Major Application Category

Sorted Based on Last Five Year Growth Rate %

1999-2004 2004-2009

19

and substrate

alternatives

across these

applications

yield very

different

growth

dynamics and

potentials.

-9.0%

-8.0%

-7.0%

-6.0%

-5.0%

-4.0%

-3.0%

-2.0%

-1.0%

Multiwall

bag papers

Kraft bag

papers

Tag

packaging

papers

Industrial

wrapping

papers

Food

processing

papers

Product

packaging

papers -M

ply

Product

packaging

papers - 1

ply

Foodservice

papers

Release

base papers

Label

papers

Total

Packaging

Papers

Av

era

ge

An

nu

al

% C

ha

ng

e

Packaging Papers Account for About 25% of the US Flexible Packaging Market

46%45%

43%

27%30%

35%

40%

45%

50%

8.0

10.0

12.0

14.0

Bil

lio

ns

of

Fle

xib

le P

ack

ag

ing

Co

sts

US Paper Packaging Share of Major Flexible Packaging Materials

Billions of Finished Packaging Material Costs

20

Retail Food Instit FoodRetail

Nonfood

Institutional

Nonfood

Consumer

Products

Industrial

Products

Medical /

PharmaRetail bags

Composite / Other 2.4 0.2 0.1 0.1 0.3 0.1 0.4 0.0

Film 6.9 1.3 1.2 0.4 1.6 1.7 1.2 1.4

Paper 2.4 1.9 1.2 0.8 1.0 0.7 0.7 0.6

Paper % Total 15% 46% 45% 43% 27% 22% 22% 23%

15%

22% 22%23%

0%

5%

10%

15%

20%

25%

0.0

2.0

4.0

6.0

8.0

Bil

lio

ns

of

Fle

xib

le P

ack

ag

ing

Co

sts

Paper Converters Add Different Levels of Value Depending on Application

72%

65% 65%

60%

70%

45%

80%

45%

55%

50%

60%

70%

80%

90%

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

20

09

Est

ima

ted

US

Pa

cka

gin

g C

ost

s ($

00

0)

Paper Material Cost as % of Total Packaging Cost

By Major Paper Packaging Paper Segment

21

Grocery/

foodservice

bags

Multiwall

bag

Industrial

wrapping /

interleaving

Foodservice

wraps /

papers

Food

processing

papers

Label

facestock

Release

base

papers

(labels)

Paper tags

Product

packaging

papers -

Multi ply

Product

packaging

papers -

Single ply

Other Costs 145,342 207,274 166,027 158,037 62,551 1,064,077 931,162 39,732 562,667 480,042

Paper Material Cost 373,736 384,937 308,336 237,055 145,953 598,544 761,860 158,928 460,364 586,718

Paper % Total 72% 65% 65% 60% 70% 36% 45% 80% 45% 55%

36%

45%

0%

10%

20%

30%

40%

50%

-

200,000

400,000

600,000

800,000

1,000,000

20

09

Est

ima

ted

US

Pa

cka

gin

g C

ost

s ($

00

0)

About 70% of Packaging Paper Volume is Coated or Laminated in Some Way

Uncoated

29%Clay Coated only

17%

Laminated / Coated

7%

Laminated / Uncoated

3%

Lightweight Packaging Papers

Most Common Surface Finishing

22

Barrier / Other

Coating only

26%

Clay + Barrier

Coatings

18%

BDA 2010 Packaging Paper Study

Examples of Recent / Developing Innovations in Packaging Papers

New / safer

barrier

treatments

Embedded /

printed

electronics

Folding

carton

replacement

Improved /

digital print

surfaces

2

3

Windowed

packaging /

cellophane

laminations

Smart /

reactive

papers &

labels

surfaces

New pulp –

based films

Paper

pouches

Concerns About Plastic’s Impact on the Environment Growing

24

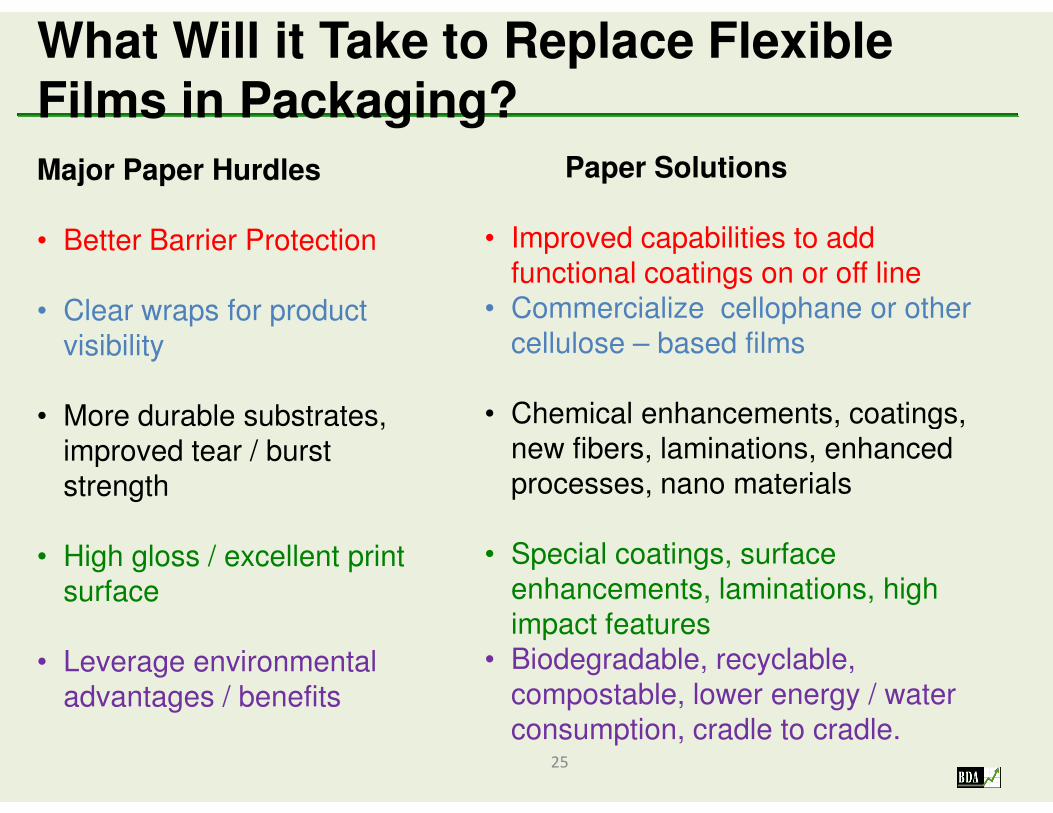

Major Paper Hurdles

• Better Barrier Protection

• Clear wraps for product

visibility

• More durable substrates,

What Will it Take to Replace Flexible Films in Packaging?

Paper Solutions

• Improved capabilities to add

functional coatings on or off line

• Commercialize cellophane or other

cellulose – based films

• Chemical enhancements, coatings,

25

• More durable substrates,

improved tear / burst

strength

• High gloss / excellent print

surface

• Leverage environmental

advantages / benefits

• Chemical enhancements, coatings,

new fibers, laminations, enhanced

processes, nano materials

• Special coatings, surface

enhancements, laminations, high

impact features

• Biodegradable, recyclable,

compostable, lower energy / water

consumption, cradle to cradle.

Paper Based Materials Positioned To Gain in Flexible Packaging Markets

� Paper still remains the preferred material in many

applications

� Historic plastic share growth at the expense of paper has

slowed

� Paper is perceived by most to be a more sustainable

26

� Paper is perceived by most to be a more sustainable

material

� Sustainability weaknesses (energy and water usage) are

less apparent and more difficult to demonstrate

� Major CPG’s are seriously considering paper based options

to reduce plastic exposure

� Improved barrier treatments, print surfaces, and

environmental profiles for paper relative to film.

Final Thoughts and

27

and Implications

Future Paper Packaging Solutions Will Focus More On Higher Value Offerings

High Growth Low Growth

Barrier treated paper Kraft and multiwall bags

"High sustainability" paper substrates Standard weight paper / board substrates

Digital print compatible surfaces Standard / commodity grades of paper

Wax / PFOA replacement barriers

Paper Based Packaging Materials - High and Low Growth Segments

28

Wax / PFOA replacement barriers

Smart packaging features

Security packaging features

Lightweight / high strength substrates

Laminated substrates

Retail ready packaging

Graphic corrugated

Dual function package designs

High performance labels and release liners

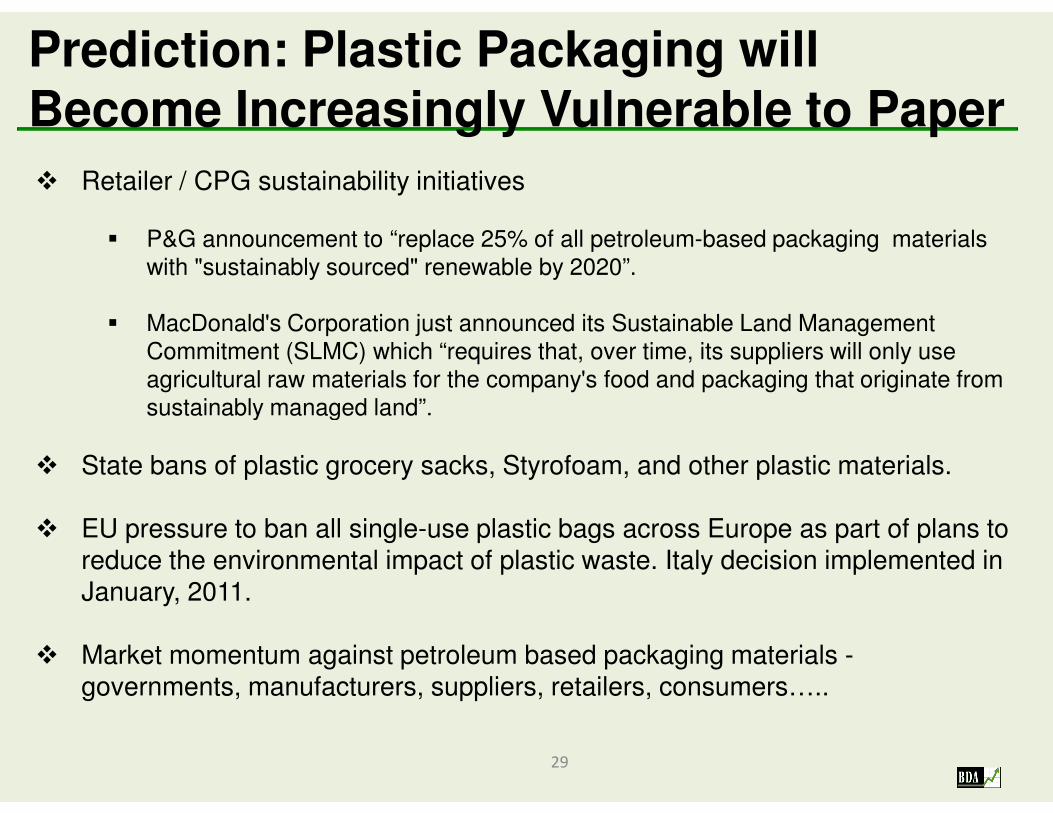

� Retailer / CPG sustainability initiatives

� P&G announcement to “replace 25% of all petroleum-based packaging materials with "sustainably sourced" renewable by 2020”.

� MacDonald's Corporation just announced its Sustainable Land Management Commitment (SLMC) which “requires that, over time, its suppliers will only use agricultural raw materials for the company's food and packaging that originate from sustainably managed land”.

Prediction: Plastic Packaging will Become Increasingly Vulnerable to Paper

29

sustainably managed land”.

� State bans of plastic grocery sacks, Styrofoam, and other plastic materials.

� EU pressure to ban all single-use plastic bags across Europe as part of plans to

reduce the environmental impact of plastic waste. Italy decision implemented in

January, 2011.

� Market momentum against petroleum based packaging materials -

governments, manufacturers, suppliers, retailers, consumers…..

But Several Factors Will Reduce Demand for Paper Packaging and Threaten Growth

� Continued manufacturing outsourcing to overseas locations

� Historic preference for flexible / clear films in pouches, bags, and wraps (which should continue but growth may slow)

� Increasing demand for higher barrier and durable materials (film substrates) to protect food and freshness

30

� Existing installations of lower cost converting / filling systems for film based packaging materials

� Increased availability of lighter weight, more durable, PLA based, high impact film based substrates

� Limited paper industry R&D efforts and associated investments

� High cost, non integrated specialty paper mills must differentiate themselves

and capture more revenue dollars / ton. One way to do this is forward

integration

� Forward integration business model within paper industry has been very

successful where implemented:

� Retail and commercial tissue

� Corrugated and folding cartons

More Integrated Paper Supply Chains Will Develop – Implications???

31

� Corrugated and folding cartons

� Release liners

� Opportunity for industry to streamline the supply chain and reduce total costs

through forward integration, converter consolidation, strategic supply

agreements

� Backward integration by converters provides opportunity to secure a more

reliable / consistent paper supply, reduce total supply chain costs, and exert

more control over the product development process

� Increased paper price stability, fewer supply options,

stronger suppliers, better but higher cost materials

� Need to regularly review your paper supply strategy and

supplier performance / plans to ensure a strong capability fit

� Important to align yourselves with mills that are well

Other Implications For Packaging Converters

32

� Important to align yourselves with mills that are well

positioned in their markets with sustainable business

models

� Make an effort to develop preferred supplier agreements

that commit volumes via long –term contracts

� Consider investment / strategic partnerships which can

provide competitive advantages to both parties.

� Identify / leverage paper sustainability benefits to provide

added value to customers

� Pursue strategic partnerships (backward integration?) with

paper suppliers to reduce supply chain costs and strengthen

your value proposition

Flexible Packaging Converter Next Steps Relative to Paper

33

� Identify / focus on paper suppliers that can offer real

sustainability benefits / solutions (e.g., high recycled content,

FSC / SFI certified pulp, chain of custody, renewable energy

sources, sustainable chemicals, waste collection systems,

etc)

� Pursue closed loop, collection, process, and material

changes within your operation that reduce packaging waste.

• Growth development consulting firm

focused on paper and packaging markets

• Based in Marietta, GA

• Contact:

Who is BDA?

34

• Contact:

Frank [email protected]