future of mobility: reinvention of the car

TRANSCRIPT

Future of Mobility: Reinvention of the Car

Introducing the Trends & Disruptive Business

Models Revolutionising Urban Mobility

Finpro ITS and MaaS Seminar, May 2016

2

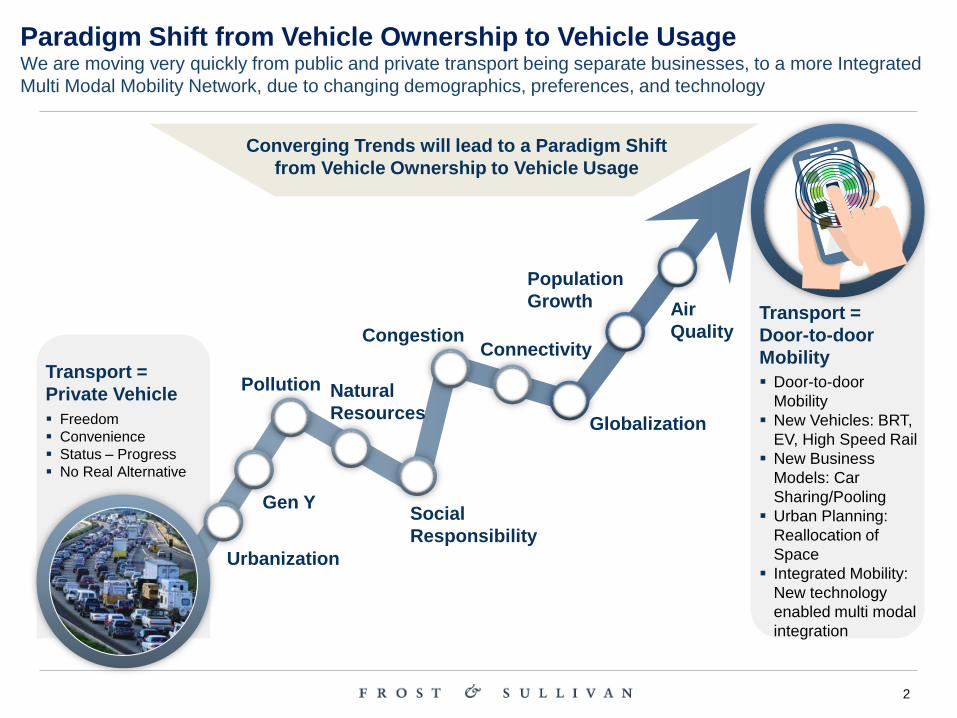

Paradigm Shift from Vehicle Ownership to Vehicle Usage We are moving very quickly from public and private transport being separate businesses, to a more Integrated

Multi Modal Mobility Network, due to changing demographics, preferences, and technology

Converging Trends will lead to a Paradigm Shift

from Vehicle Ownership to Vehicle Usage

Transport =

Private Vehicle

Freedom

Convenience

Status – Progress

No Real Alternative

Transport =

Door-to-door

Mobility

Door-to-door

Mobility

New Vehicles: BRT,

EV, High Speed Rail

New Business

Models: Car

Sharing/Pooling

Urban Planning:

Reallocation of

Space

Integrated Mobility:

New technology

enabled multi modal

integration

Gen Y

Connectivity

Population

Growth

Urbanization

Social

Responsibility

Air

Quality

Pollution

Congestion

Globalization

Natural

Resources

3

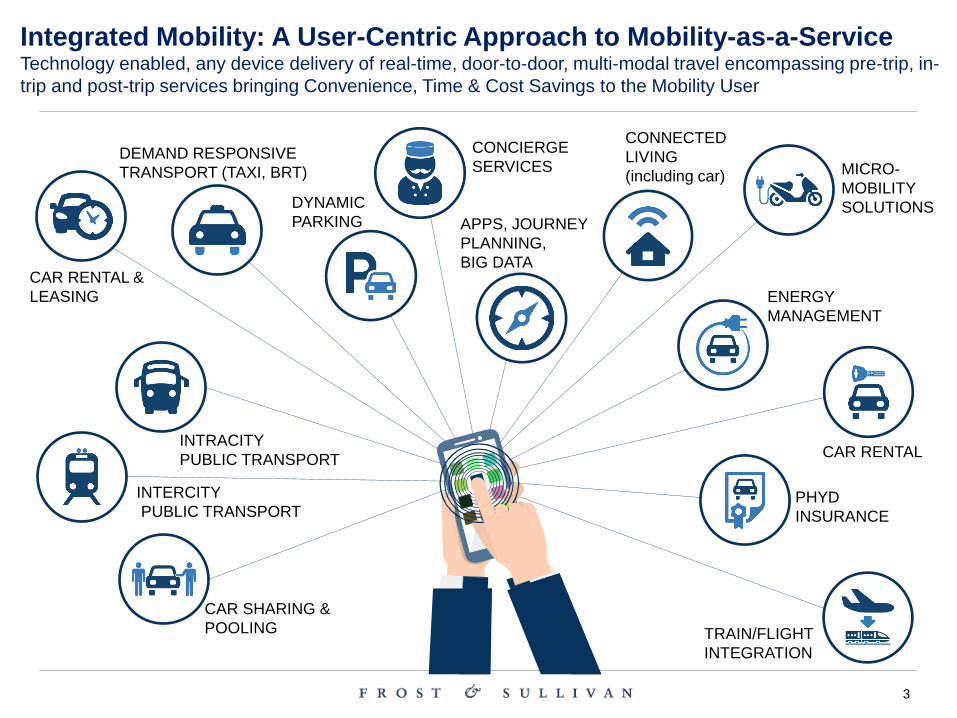

Integrated Mobility: A User-Centric Approach to Mobility-as-a-Service Technology enabled, any device delivery of real-time, door-to-door, multi-modal travel encompassing pre-trip, in-

trip and post-trip services bringing Convenience, Time & Cost Savings to the Mobility User

DEMAND RESPONSIVE

TRANSPORT (TAXI, BRT)

CONNECTED

LIVING

(including car)

INTERCITY

PUBLIC TRANSPORT

CAR RENTAL &

LEASING

CAR RENTAL

CAR SHARING &

POOLING

INTRACITY

PUBLIC TRANSPORT

PHYD

INSURANCE

DYNAMIC

PARKING

CONCIERGE

SERVICES

ENERGY

MANAGEMENT

MICRO-

MOBILITY

SOLUTIONS

TRAIN/FLIGHT

INTEGRATION

APPS, JOURNEY

PLANNING,

BIG DATA

4

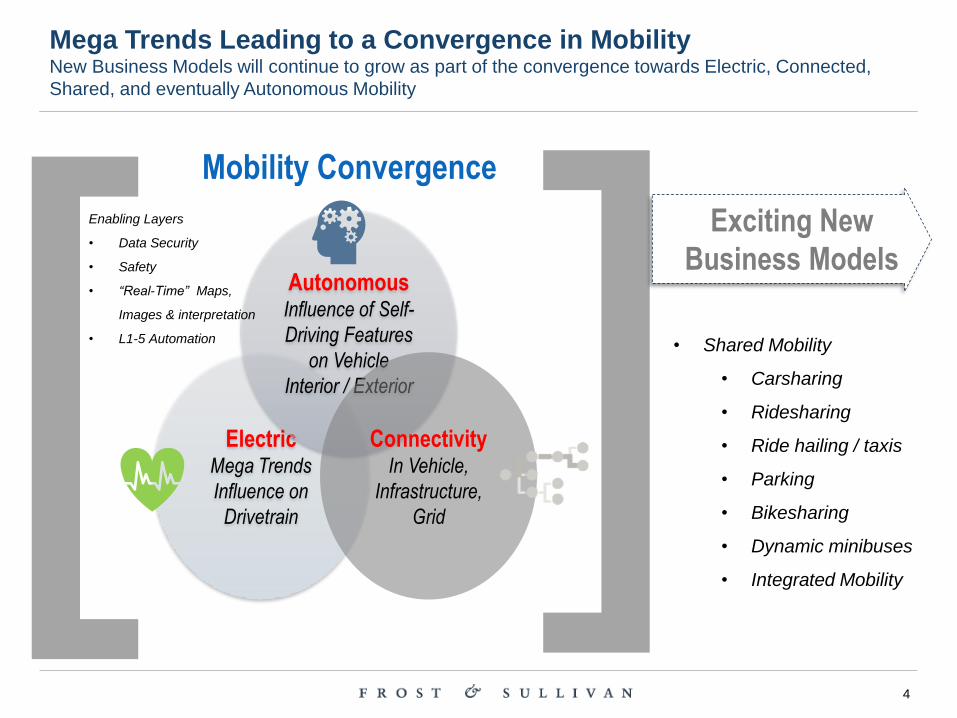

Mega Trends Leading to a Convergence in Mobility New Business Models will continue to grow as part of the convergence towards Electric, Connected,

Shared, and eventually Autonomous Mobility

Electric Mega Trends

Influence on

Drivetrain

Autonomous Influence of Self-

Driving Features

on Vehicle

Interior / Exterior

Connectivity In Vehicle,

Infrastructure,

Grid

Mobility Convergence

Exciting New

Business Models

• Shared Mobility

• Carsharing

• Ridesharing

• Ride hailing / taxis

• Parking

• Bikesharing

• Dynamic minibuses

• Integrated Mobility

Enabling Layers

• Data Security

• Safety

• “Real-Time” Maps,

Images & interpretation

• L1-5 Automation

5

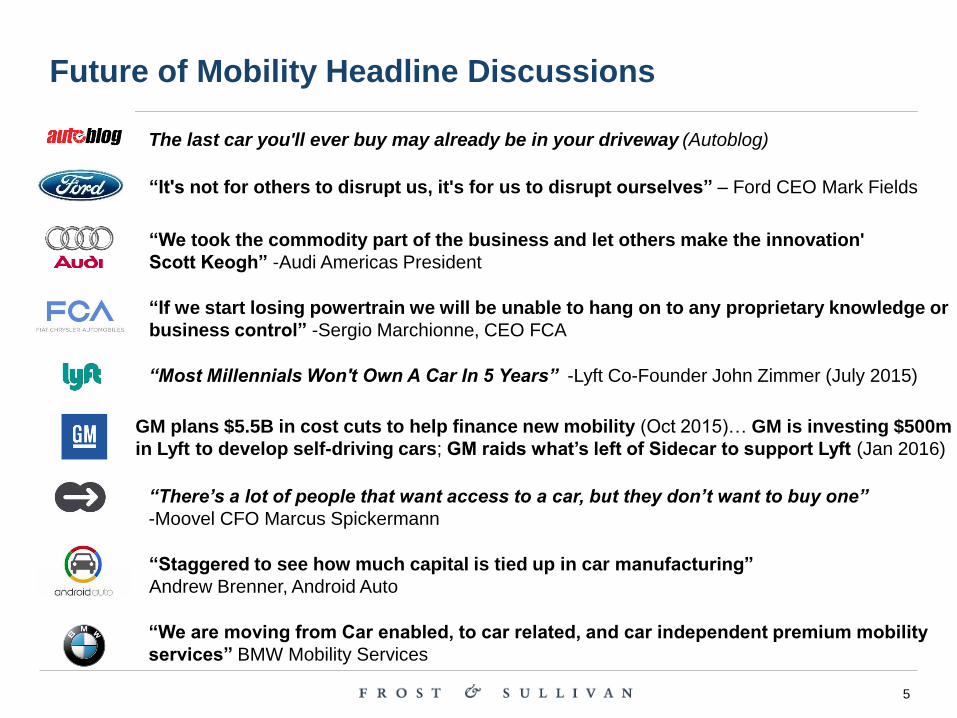

Future of Mobility Headline Discussions

The last car you'll ever buy may already be in your driveway (Autoblog)

“Most Millennials Won't Own A Car In 5 Years” -Lyft Co-Founder John Zimmer (July 2015)

“There’s a lot of people that want access to a car, but they don’t want to buy one”

-Moovel CFO Marcus Spickermann

“We are moving from Car enabled, to car related, and car independent premium mobility

services” BMW Mobility Services

“If we start losing powertrain we will be unable to hang on to any proprietary knowledge or

business control” -Sergio Marchionne, CEO FCA

“We took the commodity part of the business and let others make the innovation'

Scott Keogh” -Audi Americas President

“Staggered to see how much capital is tied up in car manufacturing”

Andrew Brenner, Android Auto

GM plans $5.5B in cost cuts to help finance new mobility (Oct 2015)… GM is investing $500m

in Lyft to develop self-driving cars; GM raids what’s left of Sidecar to support Lyft (Jan 2016)

“It's not for others to disrupt us, it's for us to disrupt ourselves” – Ford CEO Mark Fields

6

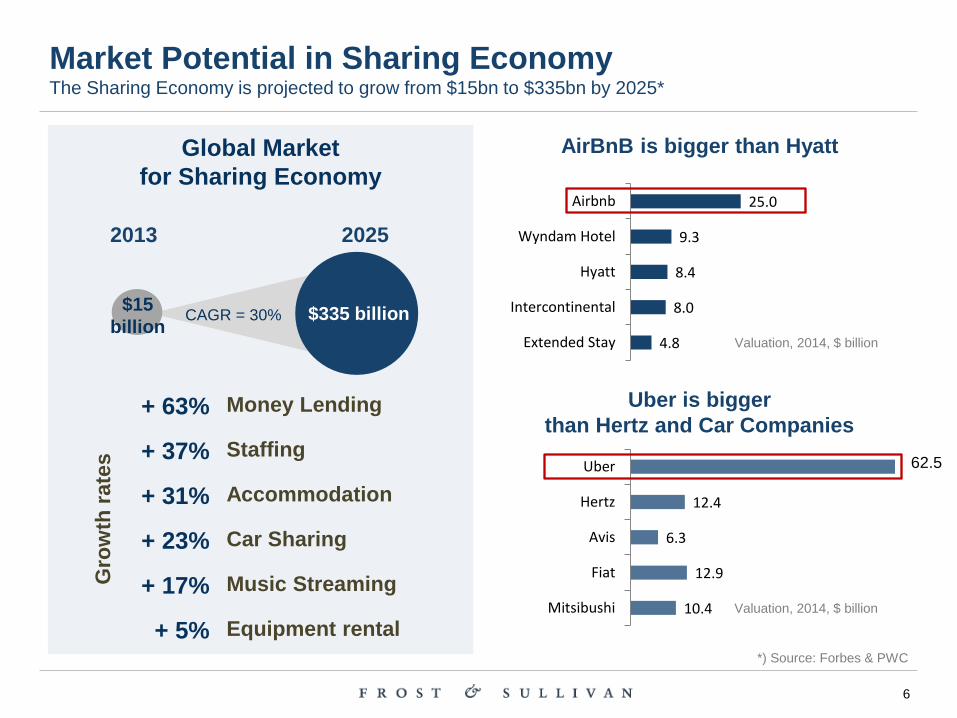

Market Potential in Sharing Economy The Sharing Economy is projected to grow from $15bn to $335bn by 2025*

Global Market

for Sharing Economy 25.0

9.3

8.4

8.0

4.8

Airbnb

Wyndam Hotel

Hyatt

Intercontinental

Extended Stay

AirBnB is bigger than Hyatt

Uber is bigger

than Hertz and Car Companies

Valuation, 2014, $ billion

$15

billion $335 billion CAGR = 30%

2013 2025

Gro

wth

ra

tes

*) Source: Forbes & PWC

+ 63% Money Lending

+ 37% Staffing

+ 31% Accommodation

+ 23% Car Sharing

+ 17% Music Streaming

+ 5% Equipment rental

12.4

6.3

12.9

10.4

Uber

Hertz

Avis

Fiat

Mitsibushi Valuation, 2014, $ billion

62.5

7

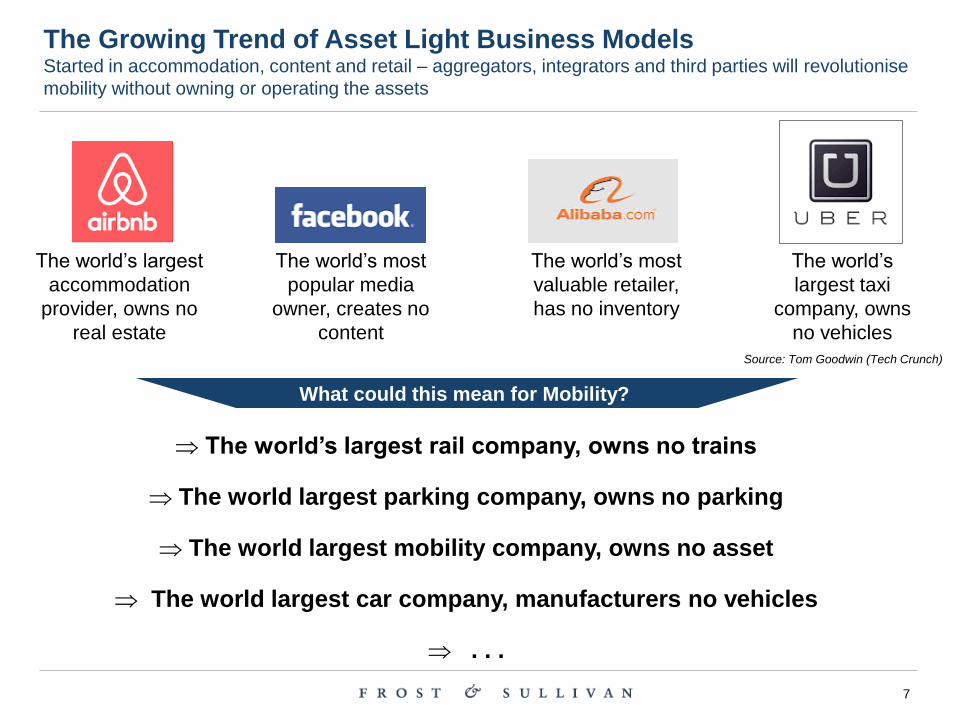

The world’s

largest taxi

company, owns

no vehicles

The world’s most

popular media

owner, creates no

content

The world’s most

valuable retailer,

has no inventory

The world’s largest

accommodation

provider, owns no

real estate

What could this mean for Mobility?

The world’s largest rail company, owns no trains

The world largest parking company, owns no parking

The world largest mobility company, owns no asset

The world largest car company, manufacturers no vehicles

. . .

Source: Tom Goodwin (Tech Crunch)

The Growing Trend of Asset Light Business Models Started in accommodation, content and retail – aggregators, integrators and third parties will revolutionise

mobility without owning or operating the assets

8

Wheels when you want them more social less media

Everyone’s private driver Your ride, On Demand

your friend with a car a ride whenever you need one

Parkatmyhouse.com the online parking marketplace

Relayrides: make money renting your car Rent the car – own the adventure

the best way from A to B moovel brings you everywhere

All transportation options, one app Search, discover, explore

Moving your way Simply. Always. Everywhere.

OurCar. YourCar. WeCar ready, set, freedom

find parking near…. parking made easy

Premium carsharing with BMW find it drive it drop it

Ideas. Focus. Solutions Innovating Fleet since 1965

Mobility Messaging – How do the key players position? In this increasingly competitive market – branding is key to understanding and adoption of new mobility

business models, reflected by the continuous dynamic nature of their messaging

Before After

9

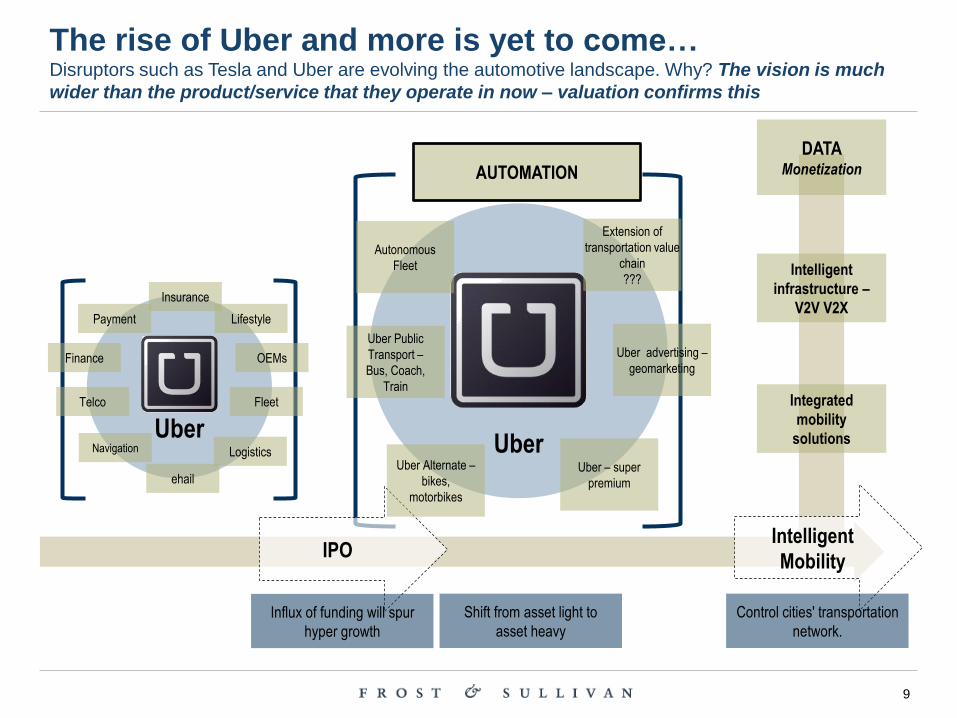

The rise of Uber and more is yet to come… Disruptors such as Tesla and Uber are evolving the automotive landscape. Why? The vision is much

wider than the product/service that they operate in now – valuation confirms this

Telco

Navigation

ehail

Logistics

Fleet

Insurance

Payment

Finance

Lifestyle

OEMs

DATA Monetization AUTOMATION

Uber Uber

Uber – super

premium

Uber advertising –

geomarketing

Uber Public

Transport –

Bus, Coach,

Train

Autonomous

Fleet

Extension of

transportation value

chain

???

IPO Intelligent

Mobility

Uber Alternate –

bikes,

motorbikes

Influx of funding will spur

hyper growth

Shift from asset light to

asset heavy

Control cities' transportation

network.

Intelligent

infrastructure –

V2V V2X

Integrated

mobility

solutions

10

Key Trends & Outlook for the Mobility Market With considerable business model innovation, investment, and public sector support, the mobility ecosystem is

set to become more integrated with existing transit networks

Integrated Mobility-as-a-

service

Increasing peer to

peer (for parking,

cars, rides, taxis)

Investment &

Partnerships from

OEMs

Dynamic Pricing

Increased Tenders

from Cities & Public

Support

Parking Reservation,

valet/automated

parking

“Car on Demand”

analytics & Big Data

Automated Driving

Source: Frost & Sullivan

11

Intelligent Mobility 2015 Video (…join us in London June 28/29th)

https://www.youtube.com/watch?v=HakdWTPAUvQ

12

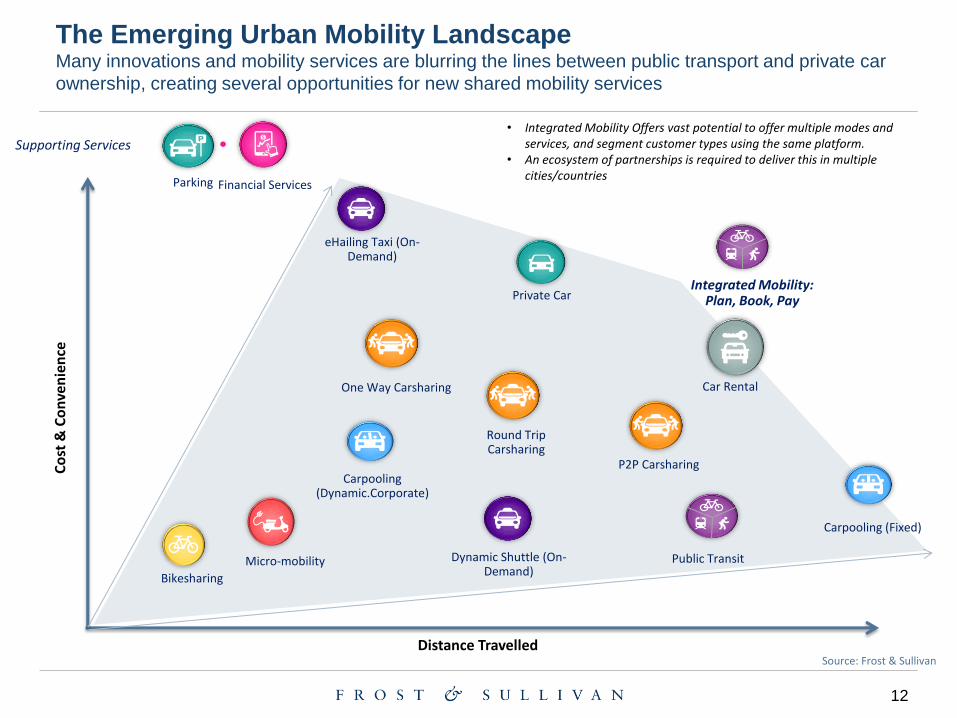

The Emerging Urban Mobility Landscape Many innovations and mobility services are blurring the lines between public transport and private car

ownership, creating several opportunities for new shared mobility services

Distance Travelled

Co

st &

Co

nve

nie

nce

Source: Frost & Sullivan

Car Rental

Micro-mobility

eHailing Taxi (On-Demand)

Bikesharing

Carpooling (Fixed)

P2P Carsharing

Integrated Mobility: Plan, Book, Pay

Dynamic Shuttle (On-Demand)

• Integrated Mobility Offers vast potential to offer multiple modes and services, and segment customer types using the same platform.

• An ecosystem of partnerships is required to deliver this in multiple cities/countries

Parking Financial Services

Round Trip Carsharing

One Way Carsharing

Public Transit

Carpooling (Dynamic.Corporate)

Supporting Services

Private Car

13

From Shared to Business Mobility in Europe New Shared Mobility models are increasingly becoming corporate, creating new use cases &

partnership potential. This is creating high growth opportunities for OEMs and commercial fleet sectors

Bike Sharing Taxi Applications Smart Parking

Carpooling / Ridesharing Car Club Models

Implications to Mobility

• Increased threat from new segments

• Agility & scalability - risk of falling behind

• Heavy technology use & increasing platforms (Asset Light)

• Cross sector partnerships & aggregation

• Increased utilisation & business potential

Actions from the Industry

• Integration of P2P, B2B, B2C to cross sell

• Partnerships for value added services

• Short term sharing/rental merging with leasing business models

• Continued investments & consolidation

€2.7bn Revenues

23m Members

1m Taxi / FHVs

139k Bikes, 430 Cities

Europe Stats

>5m Members Combined

14

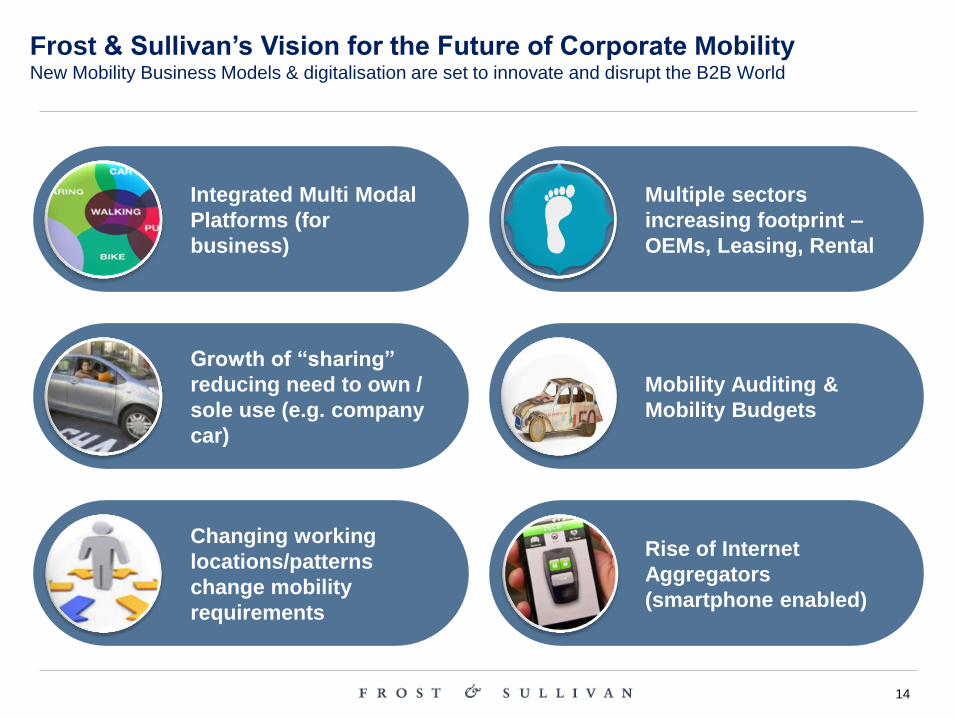

Frost & Sullivan’s Vision for the Future of Corporate Mobility New Mobility Business Models & digitalisation are set to innovate and disrupt the B2B World

Integrated Multi Modal

Platforms (for

business)

Changing working

locations/patterns

change mobility

requirements

Multiple sectors

increasing footprint –

OEMs, Leasing, Rental

Rise of Internet

Aggregators

(smartphone enabled)

Growth of “sharing”

reducing need to own /

sole use (e.g. company

car)

Mobility Auditing &

Mobility Budgets

15

Shaping Society

Building Ecosystem

1st Commercial Operators

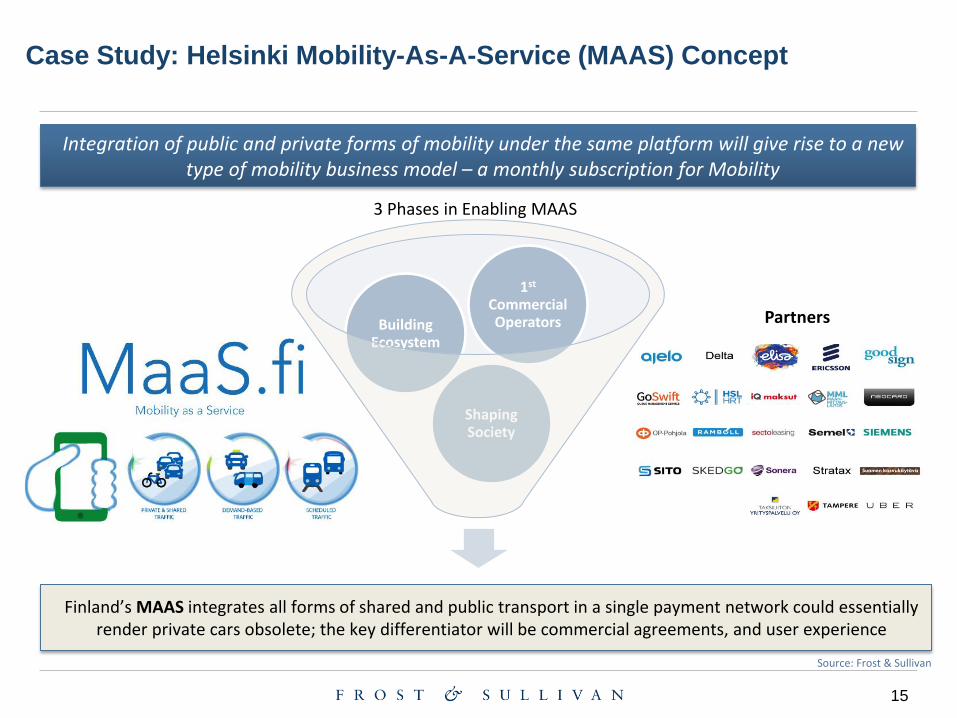

Case Study: Helsinki Mobility-As-A-Service (MAAS) Concept

Integration of public and private forms of mobility under the same platform will give rise to a new type of mobility business model – a monthly subscription for Mobility

Partners

3 Phases in Enabling MAAS

Finland’s MAAS integrates all forms of shared and public transport in a single payment network could essentially render private cars obsolete; the key differentiator will be commercial agreements, and user experience

Source: Frost & Sullivan

16

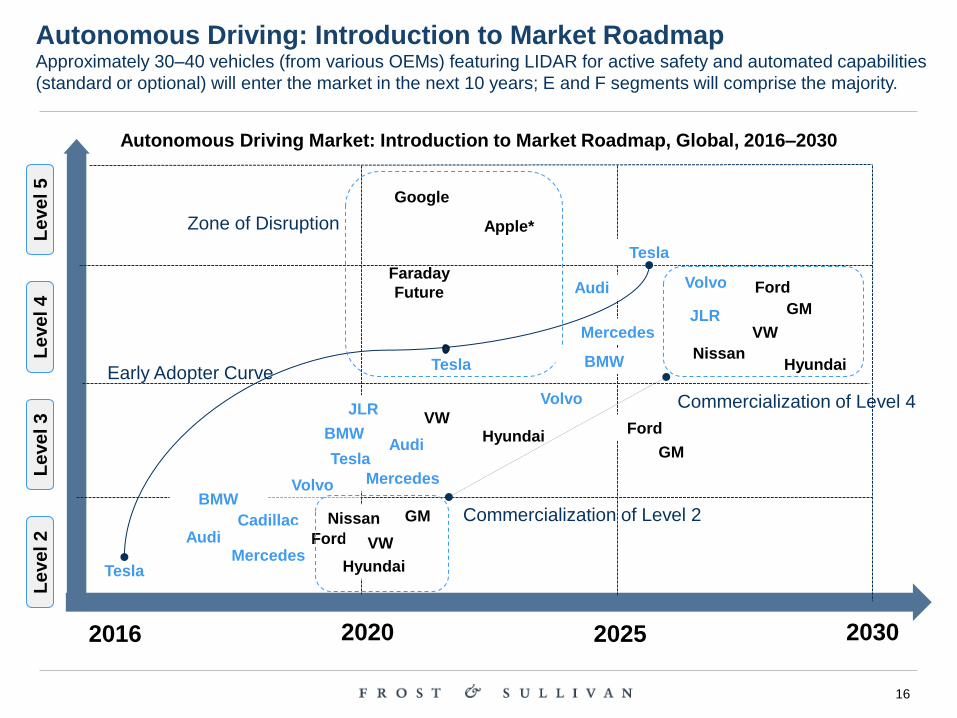

Le

ve

l 4

Le

ve

l 3

L

eve

l 2

Tesla

Le

ve

l 5

2030 2025 2020 2016

Mercedes Audi

Cadillac

Volvo

Nissan

Ford

Tesla

Tesla

Audi

Tesla

GM

Apple*

Mercedes

BMW

Volvo

Volvo

Ford

GM

Hyundai

Hyundai

Nissan

Ford

GM JLR

VW

VW

Hyundai

VW

JLR

Commercialization of Level 2

Commercialization of Level 4

Faraday

Future

Early Adopter Curve

Zone of Disruption

Audi

BMW

BMW

Autonomous Driving Market: Introduction to Market Roadmap, Global, 2016–2030

Mercedes

Autonomous Driving: Introduction to Market Roadmap Approximately 30–40 vehicles (from various OEMs) featuring LIDAR for active safety and automated capabilities

(standard or optional) will enter the market in the next 10 years; E and F segments will comprise the majority.

17

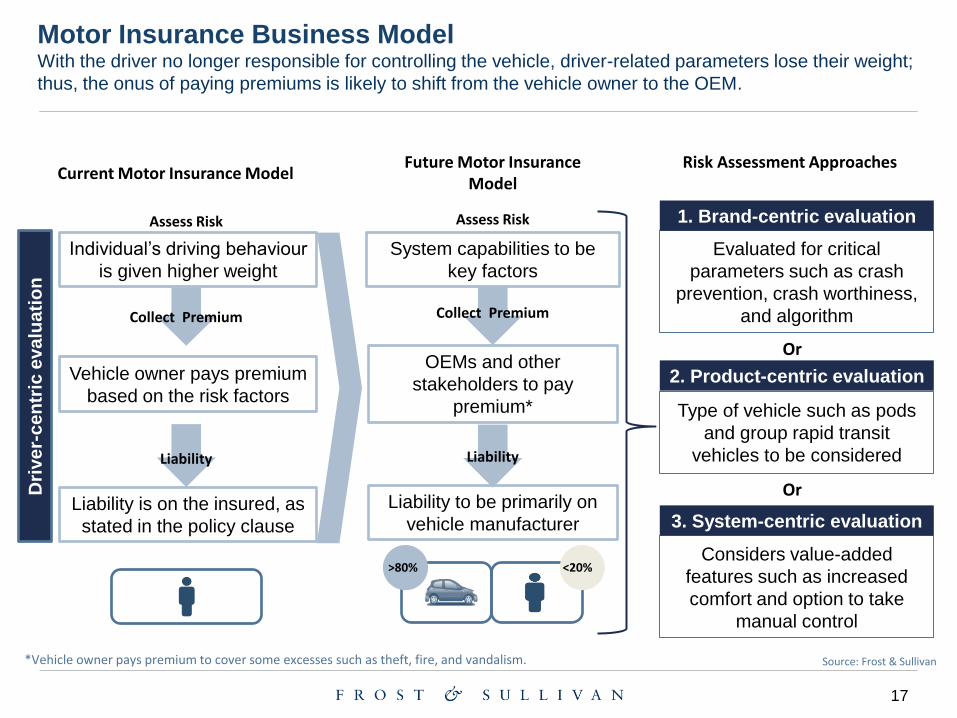

Current Motor Insurance Model Future Motor Insurance

Model

Assess Risk

Individual’s driving behaviour

is given higher weight

Vehicle owner pays premium

based on the risk factors

Liability is on the insured, as

stated in the policy clause

System capabilities to be

key factors

OEMs and other

stakeholders to pay

premium*

Liability to be primarily on

vehicle manufacturer

*Vehicle owner pays premium to cover some excesses such as theft, fire, and vandalism.

>80% <20%

Liability

Collect Premium

Assess Risk

Liability

Collect Premium

Dri

ve

r-c

en

tric

eva

lua

tio

n

Considers value-added

features such as increased

comfort and option to take

manual control

Risk Assessment Approaches

3. System-centric evaluation

Type of vehicle such as pods

and group rapid transit

vehicles to be considered

2. Product-centric evaluation

Evaluated for critical

parameters such as crash

prevention, crash worthiness,

and algorithm

1. Brand-centric evaluation

Or

Or

Motor Insurance Business Model With the driver no longer responsible for controlling the vehicle, driver-related parameters lose their weight;

thus, the onus of paying premiums is likely to shift from the vehicle owner to the OEM.

Source: Frost & Sullivan

18

Changing Role of Public Sector in Mobility As consumer habits change and technology allows innovative services, the role of the public sector is also

adapting and partnering to enable, facilitate, or restrict some of the emerging mobility business models

New Regulations for

Mobility services

Automated Driving

Carsharing Tenders,

Operations, SLA’s

Flexible scheduling &

on-demand transit

Bikesharing Tenders

Parking Supply &

Monetisation Open Data

Integrated Mobility-

As-A-Service

Source: Frost & Sullivan

19

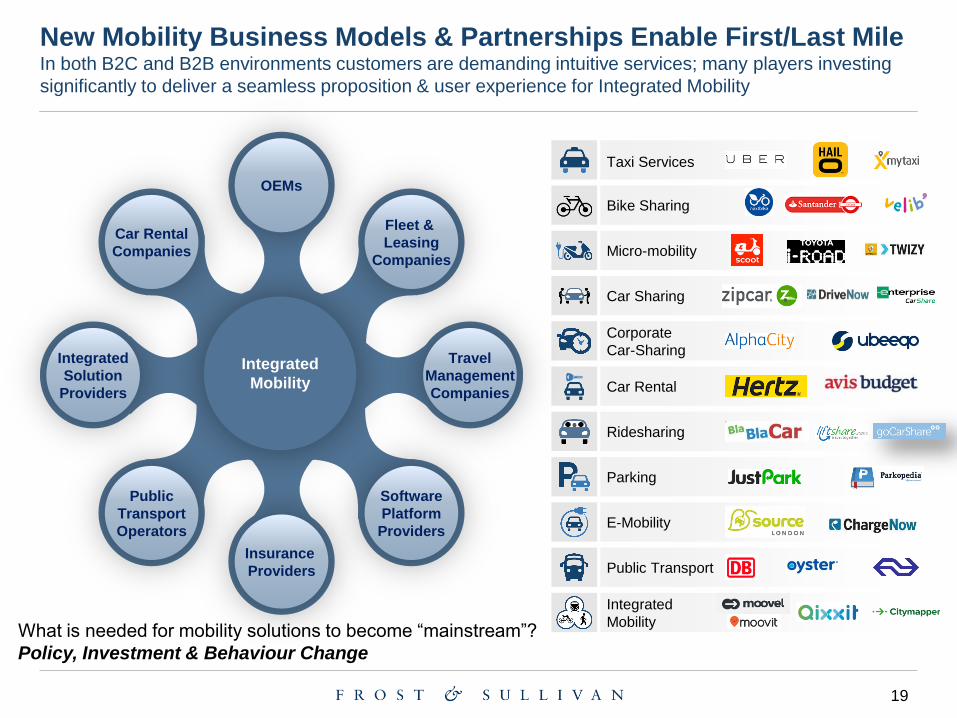

Corporate

Car-Sharing

Bike Sharing

Parking

Car Rental

Integrated

Mobility

E-Mobility

Micro-mobility

Public Transport

Car Sharing

Ridesharing

Taxi Services

New Mobility Business Models & Partnerships Enable First/Last Mile In both B2C and B2B environments customers are demanding intuitive services; many players investing

significantly to deliver a seamless proposition & user experience for Integrated Mobility

Travel

Management

Companies

OEMs

Car Rental

Companies

Public

Transport

Operators

Fleet &

Leasing

Companies

Software

Platform

Providers

Integrated

Solution

Providers

Insurance

Providers

Integrated

Mobility

What is needed for mobility solutions to become “mainstream”?

Policy, Investment & Behaviour Change

20

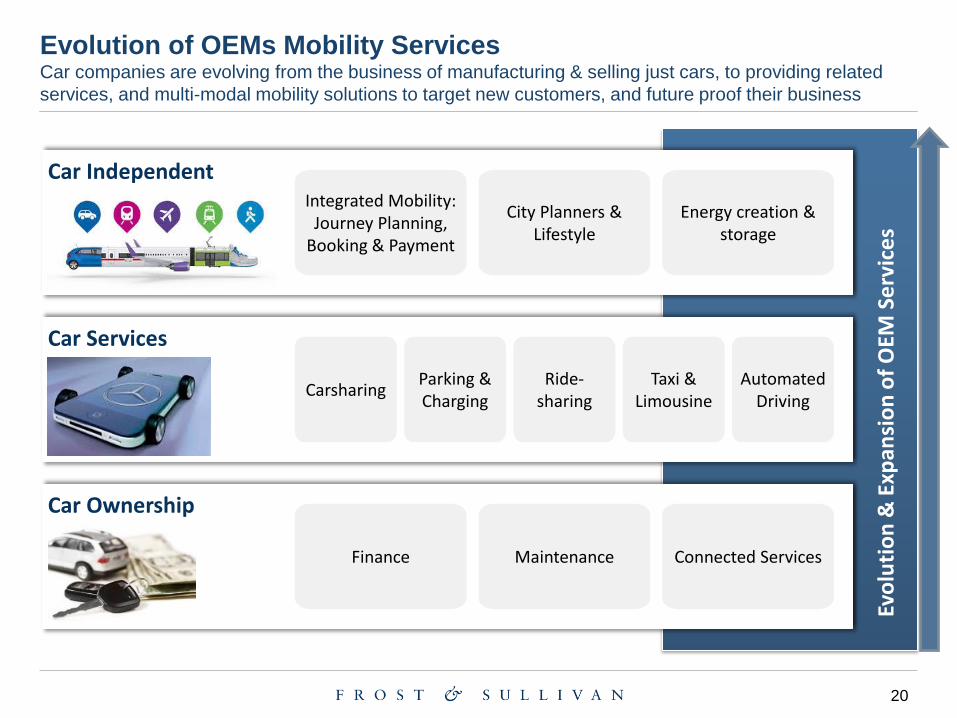

Evolution of OEMs Mobility Services Car companies are evolving from the business of manufacturing & selling just cars, to providing related

services, and multi-modal mobility solutions to target new customers, and future proof their business

Evo

luti

on

& E

xpan

sio

n o

f O

EM S

erv

ice

s

Car Independent

Car Ownership

Car Services

Integrated Mobility: Journey Planning,

Booking & Payment

City Planners & Lifestyle

Energy creation & storage

Finance Maintenance Connected Services

Carsharing Parking & Charging

Ride-sharing

Taxi & Limousine

Automated Driving

21

Conclusions & Outlook for Mobility If we shift from ownership to access of mobility services, what business models, regulation, and partnerships

are required, and how will the value chain evolve?

Mobility is becoming far more connected, asset light, and integrated – Customer

expectations are shifting from ownership to tech-enabled mobility

The lines between B2B, B2C and P2P, and public/private transport are

blurring and creating space for new players & services

What is needed for mobility services to become mainstream? A

combination of Policy, Investment, and Behaviour Change

The pace of change is accelerating – technology providers are crucial to

mobility services and can shape the evolution of MaaS

Is Finland ready to adopt Mobility-as-a-Service instead of private vehicle

ownership? Technology enables the shift from ownership to access & usage

22

Future of Mobility Video

Martyn Briggs Industry Principal, Mobility,

Direct: (+44) 2079157830

Mobile: +44 (0) 753 428 2371

Join our discussions on LinkedIn and connect

with us on @FS_automotive @BriggsMartyn

Watch our latest Video on the Future

of Mobility, filmed live at Frost &

Sullivan’s Annual Mobility Workshop

Thank You & Keep in Touch!

#IntelligentMobility

Join us in London, June 2016!