fundamentals of the us payments environment -...

TRANSCRIPT

FUNDAMENTALS OF THE PAYMENTS ENVIRONMENTENVIRONMENT

P t d b Ch l GPresented by Cheryl GurzManaging DirectorBank Segment ManagerBNY Mellon

June 4, 2013

Information Security Identification: Confidential

CONTENTS

1. U.S. Payment Environment

2. U.S. Payment Systems

3. Key Trends and Issues in Payment Systems

Q4. Questions

Information Security Identification: Confidential2

1. U.S. PAYMENT ENVIRONMENT

THE GLOBAL PAYMENTS MARKETPLACE

REGIONCAGR

(‘08 ’11)CAGR

(‘11 ’12 )GROWTH(‘11 ’12 )

NUMBER OF WORLDWIDE NON-CASH TRANSACTIONS (IN BILLIONS), BY REGION, 2008-2012e

212720

25

266285

312339

280

350

REGION (‘08-’11) (‘11-’12e) (‘11-’12e)

GLOBAL 8.1% 8.8%

REST OF ASIA 19.7% 24.4%

20.6%CEMEA 26.3% 25.5%

elop

ing

22 26 3035

4119

2426

2934

1114

1721

1214

17247

266

210

280LATAM 15.8% 14.3%

MATUREAPAC

16.5% 16.8%

EUROPE (INCLUDING 4 3% 1 3%

Dev

e

73 75 7982 83

1405.4%

(INCLUDING EUROZONE)

4.3% 1.3%

Mat

ure

111 113 117 124 130

0

70

2008 2009 2010 2011 2012E

NORAM 3.7% 4.8%

Information Security Identification: Confidential4

Source:Capgemini Analysis, 2012; ECB Statistical Data Warehouse, 2010 figures released November 2011; Bank for International Settlements Red Book, 2010 figures released December 2011; Central Bank Annual Reports, 2010

PAYMENT SYSTEMS IN THE UNITED STATES

SVPCO

The Clearing House

The FederalEPN Check and ACHSVPCOCheck Image Exchange (TCH)

The Federal Reserve Bank System

EPNElectronic Payments Network (TCH)

Check and ACHSettlement

• The four main interbank payment clearing systems in the United States are Fedwire, The Clearing House Interbank Payments System (CHIPS), Automated Clearing House (ACH) and check clearing. Th Cl i H d Th F d l ll th i t t f b k i th U it d St t• The Clearing House and The Fed clear all these instruments for banks in the United States.

Information Security Identification: Confidential5

U.S. PAYMENTS – 2009 FEDERAL RESERVE PAYMENTS STUDY

U.S. PAYMENTS GROWTH RATE 2006-2009, BASED UPON PAYMENT TYPE AND VOLUME (IN BILLIONS)

2006 2009 CAGR

TOTAL VOLUME(ALL PAYMENT TYPES)

95.2 109.0 4.6%35

40

S)

-7.1%CAGR

14.8%CAGR

20

25

30

ME

(IN

BIL

LIO

NS

9.4%CAGR

-0.2%CAGR

10

15

20

21.5%CAGR

VO

LUM

0

5

CHECKS ACH CREDIT DEBIT CARD PREPAID

Information Security Identification: Confidential6

CHECKS (PAID)

ACH CREDIT CARD

DEBIT CARD PREPAID CARD

2006 2009

PAPER TO ELECTRONIC – A JOURNEY

DISTRIBUTION OF NON-CASH PAYMENTS IN 2009

PAYMENT TYPE AS A PERCENTAGE VALUE OF PAYMENT TYPE AS A PERCENTAGE

15%

4% 0%

PAYMENT TYPE AS A PERCENTAGE VALUE OF PAYMENT TYPE AS A PERCENTAGE

32%

44%

51%

23%

51%

26%

CHECKS PAID DEBIT CARD CREDIT CARD

2%3%

CHECKS PAID DEBIT CARD CREDIT CARD

Information Security Identification: Confidential7

ACH PREPAID CARD* ACH PREPAID CARD*

Source: The Federal Reserve 2009 Payments Study; Internal analysis * Pre-paid includes EBT

CASH IS MOST USED INSTRUMENT – CHECK AND ACH DOMINATE BY VALUE

AVERAGE ANNUAL PERCENTAGE GROWTH IN TRANSACTION VOLUME (2000-2009)

CURRENCY IN CIRCULATION SOARS

18 4%18.4%

13.5%

3 7%3.7%

DEBITCARD

ACHCREDITCARD

CHECK

Debit card and ACH use have grown dramatically,

-5.8%

CARDCARD

Information Security Identification: Confidential8

Debit card and ACH use have grown dramatically, while check volume has dropped.

Source: Federal Reserve Bank of San Francisco 2012 Annual Report (both charts)

2. U.S. PAYMENT SYSTEMS

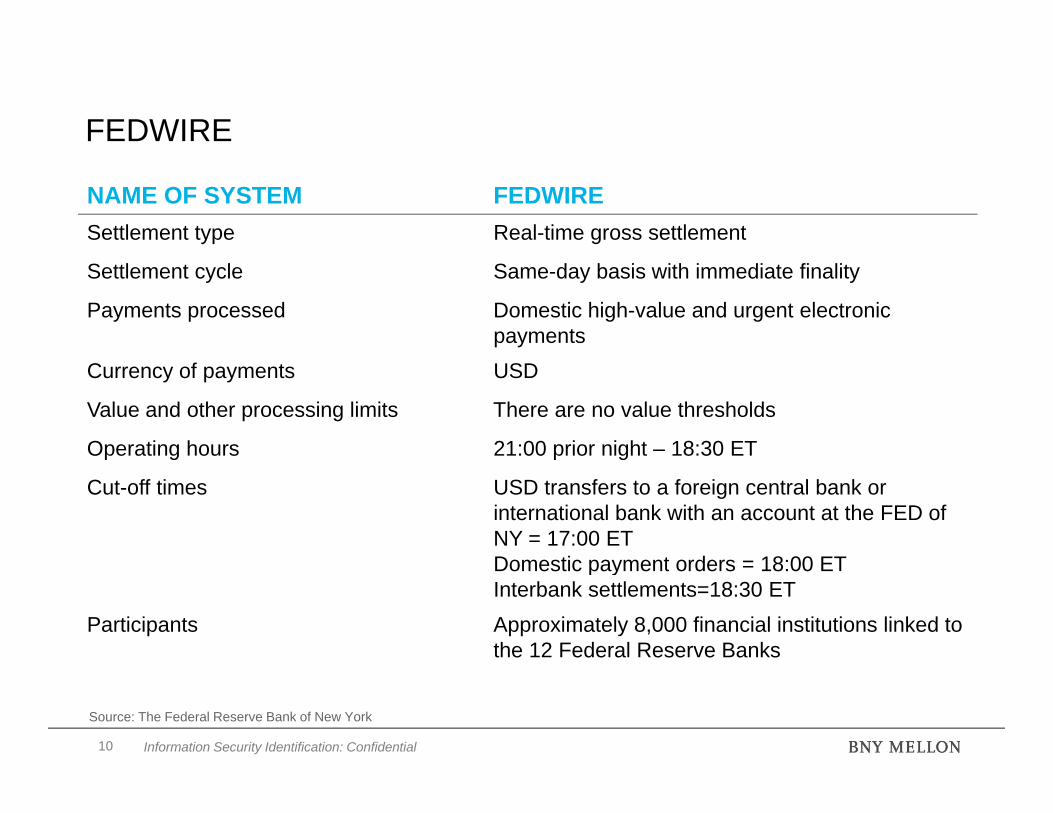

FEDWIRE

NAME OF SYSTEM FEDWIRESettlement type Real-time gross settlement

Settlement cycle Same-day basis with immediate finality

Payments processed Domestic high-value and urgent electronicpayments

Currency of payments USD

Value and other processing limits There are no value thresholds

Operating hours 21:00 prior night – 18:30 ETp g p g

Cut-off times USD transfers to a foreign central bank or international bank with an account at the FED of NY = 17:00 ETDomestic payment orders = 18:00 ETDomestic payment orders = 18:00 ETInterbank settlements=18:30 ET

Participants Approximately 8,000 financial institutions linked to the 12 Federal Reserve Banks

Information Security Identification: Confidential10

Source: The Federal Reserve Bank of New York

THE CLEARING HOUSE INTERBANK PAYMENTS SYSTEM

NAME OF SYSTEM CHIPSSettlement type Real-time net settlement

Settlement cycle Same-day basis with immediate or end-of- day finality

Payments processed Domestic high-value and urgent electronicpayments both domestic and cross borderpayments, both domestic and cross-border

Currency of payments USD

Value and other processing limits There are no value thresholds

Operating hours 21:00 prior night – 17:00 ET

Cut-off times 17:00 ET

Participants 50 direct participants. Non-direct participants may send transfers through a CHIPS via a direct member.

Information Security Identification: Confidential11

Source: The Clearing House

AUTOMATED CLEARING HOUSE

NAME OF SYSTEM ACHSettlement type Multilateral net settlement

Settlement cycle Debits settle on a next-day basis at 11:00 ETCredits settle on a two-day basis at 08:30 ET

Payments processed Low value and non urgent electronic paymentsPayments processed Low-value and non-urgent electronic payments

Currency of payments USD

Value and other processing limits There are no value thresholds

Operating hours 03:00 to 17:00 ET

Cut-off times Dependent upon operator

Participants Approximately 20,000 institutionsp pp y ,

Information Security Identification: Confidential12

Source: The Clearing House

CHECKS

NAME OF SYSTEM PAPER CHECKSSettlement type Multilateral net settlement

Settlement cycle Depends upon presentment – direct exchange, correspondent bank or Federal Reserve

Payments processed Paper checks via images

Currency of payments USD

Value and other processing limits There are no value thresholds

Operating hours Depends upon bankp g p p

Cut-off times Dependent upon bank

Participants Multiple ABA’s

Information Security Identification: Confidential13

PAYMENT RISK FACTORS

ASPECT DESCRIPTIONMITIGATIONSTRATEGIES

1) Fraud Payments executed with the consent or authorization of the payer due to deliberate criminal actions such as counterfeiting,alteration of instruments or deception

• KYC• Fraud review• AML• BSA• SARs• SARs

2) Operations Systems or operations failure due to natural or man-made causes, preventing the timely, accurate execution of payments

• Business continuity• Disaster recovery• Resilient IT design• Regular testing of plansRegular testing of plans

3) Credit/Settlement Failure of a counterparty to a payment transaction or participant in a payment scheme to fulfill gross or net settlement obligations

• Underwriting• Exposure limits• Exposure monitoring• Nettingg g• Collateralization• Linked settlement

4) Compliance Civil, criminal and market sanctions resulting from failure to comply with laws,

• AML• OFAC

Information Security Identification: Confidential14

rules, regulations or codes of conduct • Capital/liquidity requirements• Consumer protection

THE ABC’s OF REGULATION

REGULATION NAMEPAYMENT INSTRUMENTS IMPACTED

Reg B Consumer Credit Protection Act Cards

Reg B Electronic Fund Transfer Act ACH

Reg B Federal Reserve Act, Expedited Funds Availability Act, Check Clearing for the 21st Century Act (Check 21) Checks/Wire Transfers

Reg O Federal Deposit Insurance Act of 1991 Cardsg p

Reg P Gramm-Leach-Billey Act Checks, ACH, Wire Transfers, Cards

Reg S Right to Financial Privacy Act Wire Transfers

Reg Z Truth in Lending Act CardsReg Z Truth in Lending Act Cards

Reg AA Federal Trade Commission Act Cards

Reg CC Expedited Funds Availability Act, Check Clearing for 21st Century Act Checks

Reg DD Truth in Savings Act Checks, ACH, Wire Transfers

Reg FF 15 U.S.C 168 1b Cards

Reg GG Unlawful Gambling Enforcement Act Checks, ACH, Wire Transfers, Cards

Information Security Identification: Confidential15

UFC Uniform Commercial Code Checks, ACH, Wire Transfers

Source: The U.S. Treasury, Office of the Comptroller of the Currency

3. KEY TRENDS AND ISSUES IN PAYMENT SYSTEMS

CORPORATE PRIORITIES FOR PAYMENTS

PAYMENTS INITIATIVES IN PRIORITY ORDER (AFP SURVEY, MAY 2011):1. Same-day ACH2. Industry standard for account opening/maintenance docs3. Account owner verification for ACH4. Remittance standards harmonization5. Small business (trading partners) electronification6. Cross-Border ACH 7. Wire transfer ERI and notification

Information Security Identification: Confidential17

Source: The Association of Financial Professionals, Payments Survey, May 2011

PAYMENT METHOD COMPARISONS

SERVICE BENEFITS CHALLENGESACH ACH is cost effective when compared to other

electronic paymentsWithout lifting fees, beneficiaries will receive the full value of the payment

Lack of standardization, with each country employing its own set of standards and rulesRegulations affecting local clearing systems are constantly evolvingvalue of the payment

Increased control over value date of the paymentconstantly evolvingLack of common standards in terms of format and communication methodsLimitation on payment value varies country to country

TRANSFER Standard global payment format Higher cost for issuers and beneficiaries:TRANSFER Standard global payment format Can generally be repaired up frontSame Day/Next Day delivery for time critical paymentsRemittance information can travel with the paymentNo limitation on payment value

Higher cost for issuers and beneficiaries:– Transaction cost for issuer– Lifting fees

Varied degrees of self-servicing capabilities

p y

CHECKS Complete beneficiary bank details not required

Less possibility for returns

No limitation on payment value

Access to float

Higher cost for issuers, including check printing costsDelivery time varies dramatically between countries and takes longerIncreased exposure to fraud riskStop and Payment Recall rules vary and can be p y ycumbersome country to country

CARDS Eliminates paper

Ability to develop robust analytics around spend

Improve working capital management

Higher cost for vendors/suppliers as a result of interchange fees

Acceptance as a payment method may vary country to country

Information Security Identification: Confidential

Rebate opportunity Increased exposure to fraud risk

Potentially less control over spend

4. QUESTIONS

FOR MORE INFORMATION

CHERYL GURZManaging DirectorBank Market Segment ManagerBank Market Segment ManagerBNY Mellon Treasury Services101 Barclay Street, 19th FloorNew York, NY 10286212 815 5313212 815 [email protected]

Information Security Identification: Confidential20

DISCLOSURESBNY MELLON IS THE CORPORATE BRAND OF THE BANK OF NEW YORK MELLON CORPORATION AND MAY ALSO BE USED AS A GENERIC TERM TO REFERENCE THE CORPORATION AS A WHOLE OR ITS VARIOUS SUBSIDIARIES GENERALLY. PRODUCTS AND SERVICES MAY BE PROVIDED UNDER VARIOUS BRAND NAMES AND IN VARIOUS COUNTRIES BY SUBSIDIARIES, AFFILIATES, AND JOINT VENTURES OF THE BANK OF NEW YORK MELLON CORPORATION WHERE AUTHORIZED AND REGULATED AS REQUIRED WITHIN EACH JURISDICTION, AND MAY INCLUDE THE BANK OF NEW YORK MELLON, ONE WALL STREET, NEW YORK, NEW YORK 10286, A BANKING CORPORATION ORGANIZED AND EXISTING PURSUANT TO THE LAWS OF THE STATE OF NEW YORK AND OPERATING IN ENGLAND THROUGH ITS BRANCH AT ONE CANADA SQUARE, LONDON E14 5AL, ENGLAND. REGISTERED IN ENGLAND AND WALES WITH FC005522 AND BR000818 AND AUTHORIZED AND REGULATED BY THE FINANCIAL SERVICES AUTHORITY IN THE UK. NOT ALL PRODUCTS AND SERVICES ARE OFFERED AT ALL LOCATIONS.

THE MATERIAL CONTAINED IN THIS PRESENTATION, WHICH MAY BE CONSIDERED ADVERTISING, IS FOR GENERAL INFORMATION AND REFERENCE PURPOSES ONLY AND NOT INTENDED TO PROVIDE LEGAL, TAX, ACCOUNTING, INVESTMENT, FINANCIAL OR OTHER PROFESSIONAL ADVICE ON ANY MATTER, AND IS NOT TO BE USED AS SUCH. THIS PRESENTATION IS A FINANCIAL PROMOTION. THIS PRESENTATION, AND THE STATEMENTS CONTAINED HEREIN, ARE NOT AN OFFER OR SOLICITATION TO BUY OR SELL ANY PRODUCTS (INCLUDING FINANCIAL PRODUCTS) OR SERVICES MENTIONED AND SHOULD NOT BE CONSTRUED AS SUCH. THIS PRESENTATION IS NOT INTENDED FOR DISTRIBUTION TO, OR USE BY, ANY PERSON OR ENTITY IN ANY JURISDICTION OR COUNTRY IN WHICH SUCH DISTRIBUTION OR USE WOULD BE CONTRARY TO LOCAL LAW OR REGULATION SIMILARLY THIS PRESENTATION MAY NOT BE DISTRIBUTED OR USED FOR THE PURPOSE OF OFFERS OR SOLICITATIONS IN ANY JURISDICTION OR IN ANYREGULATION. SIMILARLY, THIS PRESENTATION MAY NOT BE DISTRIBUTED OR USED FOR THE PURPOSE OF OFFERS OR SOLICITATIONS IN ANY JURISDICTION OR IN ANY CIRCUMSTANCES IN WHICH SUCH OFFERS OR SOLICITATIONS ARE UNLAWFUL OR NOT AUTHORIZED, OR WHERE THERE WOULD BE, BY VIRTUE OF SUCH DISTRIBUTION, NEW OR ADDITIONAL REGISTRATION REQUIREMENTS. PERSONS INTO WHOSE POSSESSION THIS PRESENTATION COMES ARE REQUIRED TO INFORM THEMSELVES ABOUT AND TO OBSERVE ANY RESTRICTIONS THAT APPLY TO THE DISTRIBUTION OF THIS DOCUMENT IN THEIR JURISDICTION. THE INFORMATION CONTAINED IN THIS PRESENTATION IS FOR USE BY WHOLESALE CLIENTS ONLY AND IS NOT TO BE RELIED UPON BY RETAIL CLIENTS. ANY DISCUSSION OF TAX MATTERS CONTAINED IN THIS PUBLICATION IS NOT INTENDED OR WRITTEN TO BE USED, AND CANNOT BE USED, FOR THE PURPOSE OF AVOIDING PENALTIES UNDER THE INTERNAL REVENUE CODE OR PROMOTING, MARKETING OR RECOMMENDING TO ANOTHER PARTY ANY TRANSACTION OR MATTER. THIS MATERIAL MAY NOT BE REPRODUCED OR DISSEMINATED IN ANY FORM WITHOUT THE EXPRESS WRITTEN PERMISSION OF BNY MELLON BNY MELLON DOES NOT GUARANTEE THE ACCURACY OF ANY INFORMATION CONTAINED HEREIN AND CANNOT BE HELD LIABLE FORWRITTEN PERMISSION OF BNY MELLON. BNY MELLON DOES NOT GUARANTEE THE ACCURACY OF ANY INFORMATION CONTAINED HEREIN AND CANNOT BE HELD LIABLE FOR ANY ERRORS IN OR RELIANCE UPON THIS INFORMATION. PRIOR RESULTS DO NOT GUARANTEE A SIMILAR OUTCOME. THIS IS NOT AN OFFER OR SOLICITATION TO BUY OR SELL ANY FINANCIAL PRODUCT OR TO PARTICIPATE IN ANY PARTICULAR STRATEGY. THE INVESTMENT PRODUCTS AND SERVICES MENTIONED HERE ARE NOT INSURED BY THE FDIC (OR ANY OTHER STATE OR FEDERAL AGENCY), ARE NOT DEPOSITS OF OR GUARANTEED BY ANY BANK, AND MAY LOSE VALUE.

ALL REFERENCES TO ASSETS UNDER MANAGEMENT, ASSETS SERVICED, ASSETS UNDER CUSTODY AND ADMINISTRATION, GLOBAL PAYMENTS PROCESSED AND EMPLOYEES ARE SOURCED FROM BNY MELLON AND CORRECT AS OF SEPTEMBER 30, 2012, UNLESS OTHERWISE NOTED.

TO LEARN MORE ABOUT BNY MELLON, SEE OUR LATEST ANNUAL REPORT ON FORM 10-K, PROXY STATEMENT, QUARTERLY REPORTS ON FORM 10-Q AND CURRENT REPORTS ON FORM 8-K FILED WITH THE SEC. IT IS ALSO POSSIBLE TO LEARN MORE ABOUT US AND OUR INDUSTRY THROUGH A VARIETY OF PUBLIC MATERIALS AND THROUGH OUR WEBSITE, LOCATED AT WWW.BNYMELLON.COM. OTHER MATERIALS WE HAVE FILED WITH THE SEC ARE AVAILABLE THROUGH ITS WEBSITE AT WWW.SEC.GOV.

TRADEMARKS AND LOGOS BELONG TO THEIR RESPECTIVE OWNERS.

Information Security Identification: Confidential

© 2013 THE BANK OF NEW YORK MELLON CORPORATION. ALL RIGHTS RESERVED.

21