fundamental. thinking. worldwide

TRANSCRIPT

Fundamental. Thinking. Worldwide.

International Equity Review | Second Quarter 2020

HARDING LOEVNER 2

Composite PerformanceAs of June 30, 2020

1Annualized Returns; 2Inception date: December 31, 1989; 3The Benchmark Index; 4Gross of withholding taxes.The performance returns shown are preliminary. The International Equity Composite contains fully discretionary, fee-paying accounts investing in non-US equity and equity-equivalent securities and cashreserves, and is measured against the MSCI All Country World ex-US Total Return Index (Gross) for comparison purposes. Harding Loevner LP is an investment adviser registered with the Securities andExchange Commission. Harding Loevner is an affiliate of Affiliated Managers Group, Inc. (NYSE: AMG), an investment holding company with stakes in a diverse group of boutique firms. Harding Loevnerclaims compliance with the Global Investment Performance Standards (GIPS®). Harding Loevner has been independently verified for the period November 1, 1989 through March 31, 2020. Verificationassesses whether (1) the firm has complied with all composite construction requirements of the GIPS standards on a firm-wide basis and (2) the firm’s policy and procedures are designed to calculate andpresent performance in compliance with GIPS standards. The International Equity Composite has been examined for the periods January 1, 1990 through March 31, 2020. The verification and performanceexamination reports are available upon request. Performance data quoted represents past performance; past performance does not guarantee future results. Returns are presented both gross and net ofmanagement fees and include the reinvestment of all income. Net returns are calculated using actual fees. The US dollar is the currency used to express performance. For complete information on theconstruction and historical record of the International Equity Composite, please contact Harding Loevner at (908) 218-7900 or visit www.hardingloevner.com. The firm maintains a complete list anddescription of composites, which is available upon request. Please read the disclosures on the last page, which are an integral part of this presentation.

Performance (% Total Return)

3 Months YTD 1 Year 3 Years1 5 Years1 10 Years1Since

Inception1,2

HL International Equity (gross of fees) 18.82 -4.05 3.49 5.47 6.60 8.68 8.21

HL International Equity (net of fees) 18.63 -4.35 2.83 4.79 5.91 8.01 7.41

MSCI All Country World ex-US Index3,4 16.30 -10.76 -4.39 1.61 2.74 5.45 4.79

Up/Down Capture (trailing five years, annualized): 108/90

HARDING LOEVNER 3

4.5

6.6

8.8

2.4

6.6

8.5

Sales Growth Earnings GrowthCash Flow

Growth

2.9 3.3

Std Dev of ROE

12.6

9.2

13.8

10.8

5.3

12.0

Profit Margin Return on Assets Return on Equity

Quality & Growth Investment PhilosophyAs of June 30, 2020

Source: FactSet. Growth and volatility metrics are based on five-year historical data; the other ratios are based on the most recent annual data. All metrics and ratios are percentagespresented as weighted medians. Please read the disclosures on the last page, which are an integral part of this presentation.

Faster GrowthMore Profitable Lower Risk

Harding Loevner International Equity Model MSCI All Country World ex-US Index

41.6

60.2

Debt/Equity

HARDING LOEVNER 4

An Economic Recovery?

01020304050607080

Jan-

19

Feb-

19

Mar

-19

Apr

-19

May

-19

Jun-

19

Jul-

19

Aug

-19

Sep

-19

Oct

-19

Nov

-19

Dec

-19

Jan-

20

Feb-

20

Mar

-20

Apr

-20

May

-20

Jun-

20

Oil Price (Brent $ per Barrel)

2

2.2

2.4

2.6

2.8

3

3.2

Dec

-18

Jan-

19

Feb-

19

Mar

-19

Apr

-19

May

-19

Jun-

19

Jul-

19

Aug

-19

Sep

-19

Oct

-19

Nov

-19

Dec

-19

Jan-

20

Feb-

20

Mar

-20

Apr

-20

May

-20

Jun-

20

Copper NYMEX ($/lb)

Source: OECD, FactSet. The composite leading indicator (CLI) is designed to provide early signals of turning points in business cycles showing fluctuation of the economic activity around its long term potential level. CLIs show short-term economic movements in qualitative rather than quantitative terms.

April: 93.8

June: 97.1

92

94

96

98

100

102

104

OECD Composite Leading Indicator (Long-Term Average = 100)

Recession CLI

HARDING LOEVNER 5

Unprecedented Monetary and Fiscal Stimulus in Response to COVID-19

Source: IMF (chart on top), Yale School of Management (chart on bottom), IMF Classified Advanced Economies: Australia, Canada, European Union, France, Germany, Italy, Japan, Korea, Spain, Belgium, Czech republic, Denmark, Finland, New Zealand, Norway, Singapore, Sweden, Switzerland, The Netherlands, United Kingdom, United States. IMF Classified Emerging Markets: Albania, Argentina, Brazil, Bulgaria, Chile, China, Colombia, Egypt, Georgia, India, Indonesia, Kazakhstan, Mauritius, Mexico, Pakistan, Peru, Philippines, Poland, Romania, Russia, Saudi Arabia, South Africa, Thailand, Tunisia, Turkey, United Arab Emirates. IMF Classified LIDCs: Bangladesh, Ethiopia, Ghana, Guinea-Bissau, Honduras, Kenya, Nigeria, Senegal, Vietnam.

0

100

200

300

400

Cou

nt

Weekly Count of Announced Monetary Stimulus Measures

0.0 2.0 4.0 6.0 8.0 10.0 12.0

Low Income Developing Countries

Emerging Markets

G20

Advanced Economies

Percent of GDP

Summary of Fiscal Measures Since Outbreak

Loans, equity, and guarantees Additional spending and forgone revenue

HARDING LOEVNER 6

Lingering Economic Uncertainty due to COVID-19

Source: OECD Economic Outlook, June 2020

Single-hit scenario: A second wave is avoided

Double-hit scenario: A second wave of infections hits before year-end

-16

-14

-12

-10

-8

-6

-4

-2

0

ESP

FRA

ITA

GB

RCZ

EP

RT

BE

LIS

LS

VK

LTU

LVA

AR

GN

ZLR

US

EST

CHE

NLD

HU

NG

RC

PO

LCA

NFI

NB

RA

SV

ND

EUIR

LR

OU

MEX

US

AIS

RZA

FTU

RB

GR

COL

SW

ELU

XW

LDA

UT

NO

RJP

NIN

DCH

LD

NK

AU

SCR

IID

NCH

NK

OR

2020 Projected Change in GDP

Single-Hit Scenario Additional Decline in Double-Hit Scenario

HARDING LOEVNER 7

MSCI ACW ex-US Index Total Returns by Quality, Growth, and Value Rank

Source: FactSet; Data as of June 30, 2020. Please read the disclosures on the last page, which are an integral part of this presentation.

2Q20Fastest growing and most expensive stocks performed best.

Year to DateHighest quality, fastest growth, & most expensive stocks strongly outperformed.

0

5

10

15

20

25

Highest Lowest

Ret

urn

(%)

Quality Rank Quintiles

0

5

10

15

20

25

Fastest Slowest

Growth Rank Quintiles

0

5

10

15

20

25

LeastExp.

MostExp.

Value Rank Quintiles

-25

-20

-15

-10

-5

0

5

Fastest Slowest

Growth Rank Quintiles

-25

-20

-15

-10

-5

0

5

Highest Lowest

Ret

urn

(%)

Quality Rank Quintiles

-25

-20

-15

-10

-5

0

5

LeastExp.

MostExp.

Value Rank Quintiles

HARDING LOEVNER 8

Canada

Pacific ex-Japan

Middle East

Europe EMU

HL Intl Equity Composite

Emerging Markets

MSCI ACWxUS Index

Japan

Europe ex-EMU

Materials

Info Technology

Cons Discretionary

HL Intl Equity Composite

Comm Services

Industrials

Health Care

MSCI ACWxUS Index

Utilities

Financials

Cons Staples

Energy

Real Estate

Benchmark Sector/Region ReturnsSecond Quarter

Source: FactSet; Data as of June 30, 2020. Past performance does not guarantee future results. Please read the disclosures on the last page, which are an integral part of this presentation.

Sector Total Return (%) Region Total Return (%)

8.2

10.1

10.5

11.5

11.7

16.3

16.6

17.6

18.1

18.8

20.0

24.7

25.7

0.0 10.0 20.0 30.0

11.1

11.6

16.3

18.2

18.8

20.1

20.1

20.2

20.4

0.0 5.0 10.0 15.0 20.0 25.0

HARDING LOEVNER 9

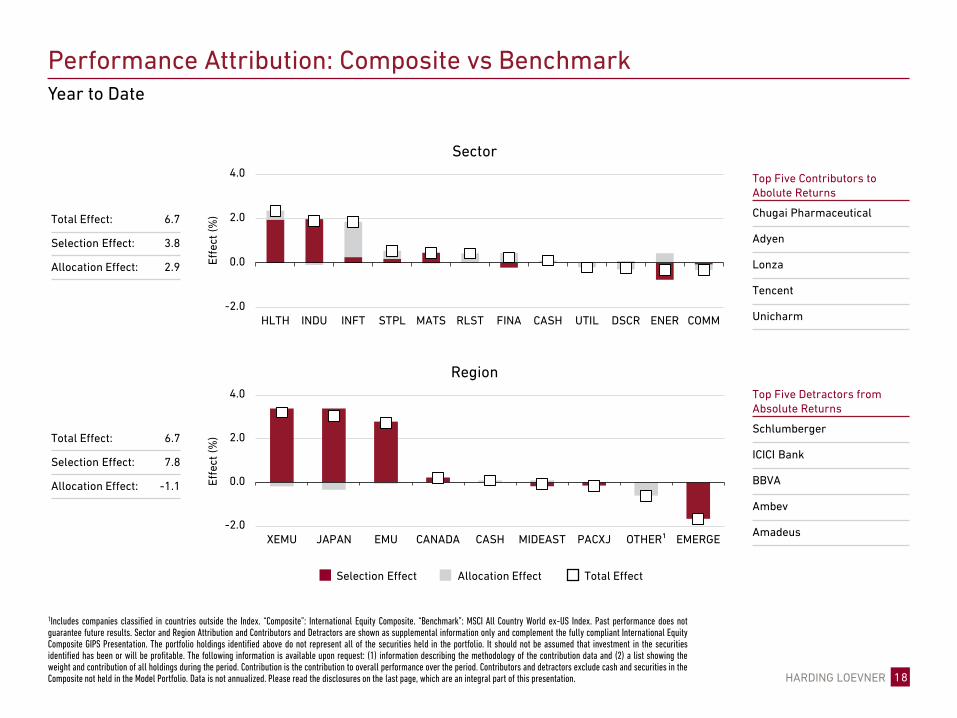

Performance Attribution: Composite vs BenchmarkSecond Quarter

1Includes companies classified in countries outside the Index. “Composite”: International Equity Composite. “Benchmark”: MSCI All Country World ex-US Index. Past performance does notguarantee future results. Sector and Region Attribution and Contributors and Detractors are shown as supplemental information only and complement the fully compliant International EquityComposite GIPS Presentation. The portfolio holdings identified above do not represent all of the securities held in the portfolio. It should not be assumed that investment in the securitiesidentified has been or will be profitable. The following information is available upon request: (1) information describing the methodology of the contribution data and (2) a list showing theweight and contribution of all holdings during the quarter. Contribution is the contribution to overall performance over the period. Contributors and detractors exclude cash and securities inthe Composite not held in the Model Portfolio. Quarterly data is not annualized. Please read the disclosures on the last page, which are an integral part of this presentation.

-1.0

0.0

1.0

2.0

3.0

INFT INDU RLST HLTH FINA UTIL ENER STPL COMM DSCR CASH MATS

Sector

Effe

ct (%

)

Top Five Contributors to Abolute Returns

Infineon Technologies

Adyen

Chugai Pharmaceutical

SAP

TSMC

Top Five Detractors from Absolute Returns

Royal Dutch Shell

China Mobile

Amadeus

Baidu

Standard Chartered-1.0

0.0

1.0

2.0

3.0

EMU JAPAN XEMU OTHER¹ CANADA MIDEAST CASH PACXJ EMERGE

Effe

ct (%

)

Region

Total Effect: 2.6

Selection Effect: 1.8

Allocation Effect: 0.8

Total Effect: 2.6

Selection Effect: 2.9

Allocation Effect: -0.3

Selection Effect Allocation Effect Total Effect

HARDING LOEVNER 10

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

Dec

-15

Mar

-16

Jun-

16

Sep

-16

Dec

-16

Mar

-17

Jun-

17

Sep

-17

Dec

-17

Mar

-18

Jun-

18

Sep

-18

Dec

-18

Mar

-19

Jun-

19

Sep

-19

Dec

-19

Mar

-20

Jun-

20

2017 2018 2019 2020 2021

Growth ExpectationsEarnings expectations collapsed for 2020, but a rebound is anticipated in 2021

Source: OECD (2019), OECD Economic Outlook, Interim Report September 2019; FactSet , Harding Loevner.

MSCI AC World ex-US Index – EPS Growth (USD)2017 – 2021 Consensus Estimates

MSCI AC World ex-US Index – EPS Growth (USD)2007 – 2011 Consensus Estimates

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

Dec

-05

Mar

-06

Jun-

06S

ep-0

6D

ec-0

6M

ar-0

7Ju

n-07

Sep

-07

Dec

-07

Mar

-08

Jun-

08S

ep-0

8D

ec-0

8M

ar-0

9Ju

n-09

Sep

-09

Dec

-09

Mar

-10

Jun-

10S

ep-1

0D

ec-1

0M

ar-1

1Ju

n-11

Sep

-11

2007 2008 2009 2010 2011

HARDING LOEVNER 11

Highest-Growth Companies Becoming More ExpensiveWe have reduced our exposure to the highest two quintiles of growth in the benchmark as those stocks appear increasingly expensive.

Source: FactSet

(10)

(5)

0

5

10

15

20

25

30

35

Mar

-16

Jun-

16

Sep

-16

Dec

-16

Mar

-17

Jun-

17

Sep

-17

Dec

-17

Mar

-18

Jun-

18

Sep

-18

Dec

-18

Mar

-19

Jun-

19

Sep

-19

Dec

-19

Mar

-20

Jun-

20

Act

ive

Wei

ght

HL International Active Weight in Top Two Quintiles of Growth

Quintile 1 Quintile 2

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

Dec

-07

Aug

-08

Apr

-09

Dec

-09

Aug

-10

Apr

-11

Dec

-11

Aug

-12

Apr

-13

Dec

-13

Aug

-14

Apr

-15

Dec

-15

Aug

-16

Apr

-17

Dec

-17

Aug

-18

Apr

-19

Dec

-19

Chea

p

R

el V

alua

tion

Expe

nsiv

e

Valuation of MSCI ACWIxUS Index by Quintiles of Growth

Quintile 1 (Fastest Growth) Quintile 2

Quintile 3 Quintile 4

Quintile 5 (Slowest Growth) MSCI ACWIxUS

HARDING LOEVNER 12

Completed Portfolio Transactions

The portfolio is actively managed therefore holdings shown may not be current. The portfolio holdings identified above do not represent all of the securities held in the portfolio. It should notbe assumed that investment in the securities identified has been or will be profitable. To request a complete list of portfolio holdings for the past year, contact Harding Loevner. Holdings areshown as supplemental information only and complement the fully compliant International Equity Composite GIPS Presentation. Please read the disclosures on the last page, which are anintegral part of this presentation.

Company Country Sector

Alcon Switzerland Health Care

Alibaba China Cons Discretionary

Positions Established Positions Sold

Portfolio Turnover (5 year annualized average): 16.8%

Company Country Sector

Amadeus Spain Info Technology

Baidu China Comm Services

Second Quarter

HARDING LOEVNER 13

3.3

4.6

2.8

6.1

7.4

11.3

11.5

15.1

19.1

18.8

1.5

2.6

4.1

5.4

7.8

13.6

14.1

14.5

15.1

21.3

0.0 5.0 10.0 15.0 20.0 25.0

Cash

Energy

ConsumerDiscretionary

Comm Services

Materials

Industrials

Health Care

Cons Staples

Financials

Info Technology

6/30/2020 6/30/2019

Sector (%)

3.3

2.7

3.4

3.1

6.4

11.4

22.8

22.8

24.1

1.5

1.5

1.5

2.2

5.1

14.9

23.0

24.7

25.6

0.0 10.0 20.0 30.0

Cash

Middle East

Other¹

Canada

Pacificex-Japan

Japan

EmergingMarkets

Europe EMU

Europeex-EMU

6/30/2020 6/30/2019

June 30, 2020 vs June 30, 2019

1Includes companies classified in countries outside the Index. Sector and Region end weights are shown as supplemental information only and complement the fully compliant InternationalEquity Composite GIPS Presentation. Please read the disclosures on the last page, which are an integral part of this presentation.

Region (%)

Portfolio Allocation Comparison

HARDING LOEVNER 14

Geography HL% ACWIxUS% (Under) / Over

Europe ex-EMU 25.6 19.7

Europe EMU 24.7 20.8

Cash 1.5 —

Other1 1.5 —

Middle East 1.5 0.4

Frontier Markets2 0.0 —

Japan 14.9 16.5

Pacific ex-Japan 5.1 7.5

Canada 2.2 6.5

Emerging Markets 23.0 28.6

Portfolio ExposuresAs of June 30, 2020

1Includes companies classified in countries outside the Index; 2Includes countries with less-developed markets outside the Index.Source: Harding Loevner International Equity Model; MSCI Inc. and S&P. Sector and region end weights are shown as supplemental information only and complement the fully compliantInternational Equity Composite GIPS Presentation. Please read the disclosures on the last page, which are an integral part of this presentation.

Sector HL% ACWIxUS% (Under) / Over

Info Technology 21.3 11.0

Cons Staples 14.5 9.9

Health Care 14.1 10.7

Industrials 13.6 11.4

Cash 1.5 —

Materials 7.8 7.6

Comm Services 5.4 7.6

Energy 2.6 4.8

Real Estate 0.0 2.8

Financials 15.1 18.1

Utilities 0.0 3.5

Cons Discretionary 4.1 12.6

(12.0) (6.0) 0.0 6.0 12.0 (12.0) (6.0) 0.0 6.0 12.0

Ten Largest Holdings – Total Weight: 32.0%

Company Country Sector Wt (%)

Infineon Technologies Germany Info Technology 3.1

Samsung Electronics South Korea Info Technology 3.1

AIA Group Hong Kong Financials 3.0

Tencent China Comm Services 2.8

Chugai Pharmaceutical Japan Health Care 2.7

83% Active Share

Company Country Sector Wt (%)

TSMC Taiwan Info Technology 4.1

Roche Switzerland Health Care 3.4

L'Oréal France Cons Staples 3.3

SAP Germany Info Technology 3.3

Atlas Copco Sweden Industrials 3.2

HARDING LOEVNER 15

Harding Loevner ProfileAs of June 30, 2020

Data as of June 30, 2020. Total AUM includes all the assets under management and is presented as supplemental information. Please read the disclosures on the last page, which are anintegral part of this presentation.

42 investment professionals International Equity portfolio management team averages 14 years at Harding Loevner

Total Assets$67B

Strategy Assets Firm Assets

Global $17.8B 27%

International (Non-US) $32.7B 49%

Emerging Markets $15.9B 24%

Frontier Emerging Markets $0.2B <1%

Global Small Companies <$0.1B <1%

International Small Companies $0.4B 1%

Research Portfolios <$0.1B <1%

Appendix

HARDING LOEVNER 17

Health Care

Info Technology

Comm Services

HL Intl Equity Composite

Cons Staples

Utilities

Materials

Cons Discretionary

MSCI ACWxUS Index

Industrials

Real Estate

Financials

Energy

Middle East

HL Intl Equity Composite

Japan

Emerging Markets

MSCI ACWxUS Index

Europe EMU

Canada

Europe ex-EMU

Pacific ex-Japan

Benchmark Sector/Region ReturnsYear to Date

Source: FactSet; Data as of June 30, 2020. Past performance does not guarantee future results. Please read the disclosures on the last page, which are an integral part of this presentation.

Sector Total Return (%) Region Total Return (%)

-32.1

-23.0

-21.5

-13.1

-10.8

-8.9

-8.8

-5.9

-5.7

-4.0

1.4

3.0

6.3

-40.0 -30.0 -20.0 -10.0 0.0 10.0

-12.9

-12.9

-12.5

-12.0

-10.8

-9.7

-6.9

-4.0

-1.5

-15.0 -10.0 -5.0 0.0

HARDING LOEVNER 18

Performance Attribution: Composite vs BenchmarkYear to Date

-2.0

0.0

2.0

4.0

HLTH INDU INFT STPL MATS RLST FINA CASH UTIL DSCR ENER COMM

Sector

Region

-2.0

0.0

2.0

4.0

XEMU JAPAN EMU CANADA CASH MIDEAST PACXJ OTHER¹ EMERGE

Total Effect: 6.7

Selection Effect: 3.8

Allocation Effect: 2.9

Total Effect: 6.7

Selection Effect: 7.8

Allocation Effect: -1.1

1Includes companies classified in countries outside the Index. “Composite”: International Equity Composite. “Benchmark”: MSCI All Country World ex-US Index. Past performance does notguarantee future results. Sector and Region Attribution and Contributors and Detractors are shown as supplemental information only and complement the fully compliant International EquityComposite GIPS Presentation. The portfolio holdings identified above do not represent all of the securities held in the portfolio. It should not be assumed that investment in the securitiesidentified has been or will be profitable. The following information is available upon request: (1) information describing the methodology of the contribution data and (2) a list showing theweight and contribution of all holdings during the period. Contribution is the contribution to overall performance over the period. Contributors and detractors exclude cash and securities in theComposite not held in the Model Portfolio. Data is not annualized. Please read the disclosures on the last page, which are an integral part of this presentation.

Top Five Contributors to Abolute Returns

Chugai Pharmaceutical

Adyen

Lonza

Tencent

Unicharm

Top Five Detractors from Absolute Returns

Schlumberger

ICICI Bank

BBVA

Ambev

Amadeus

Selection Effect Allocation Effect Total Effect

Effe

ct (%

)Ef

fect

(%)

HARDING LOEVNER 19

Completed Portfolio Transactions

The portfolio is actively managed therefore holdings shown may not be current. The portfolio holdings identified above do not represent all of the securities held in the portfolio. It should notbe assumed that investment in the securities identified has been or will be profitable. To request a complete list of portfolio holdings for the past year, contact Harding Loevner. Holdings areshown as supplemental information only and complement the fully compliant International Equity Composite GIPS Presentation. Please read the disclosures on the last page, which are anintegral part of this presentation.

PositionsEstablished

Portfolio Turnover (5 year annualized average): 16.8%

PositionsSold

3Q19 4Q19 1Q20 2Q20

Alcon

Alibaba

Amadeus

Baidu

Adyen

NITORI

Shionogi

Dentsu

HSBC

Sasol

Schlumberger

Schneider Electric

Standard Chartered

Grifols

M3

Naspers

Prosus

Prosus*

Aspen Pharmacare

BMW

Trailing 12 Months

HARDING LOEVNER 20

International vs US Relative Valuation

Source: Bloomberg; FactSet. Data as of June 30, 2020

50%

60%

70%

80%

90%

100%

110%

Jun-

96

Jun-

97

Jun-

98

Jun-

99

Jun-

00

Jun-

01

Jun-

02

Jun-

03

Jun-

04

Jun-

05

Jun-

06

Jun-

07

Jun-

08

Jun-

09

Jun-

10

Jun-

11

Jun-

12

Jun-

13

Jun-

14

Jun-

15

Jun-

16

Jun-

17

Jun-

18

Jun-

19

Jun-

20

Relative Valuation ACWIxUS vs US Avg Relative ValuationValuation as of June 30, 2020(Based on most recent annual data)

P/E P/B P/CF

ACWI ex-US 16.0 1.6 9.1

Europe 15.9 1.7 8.8

Japan 15.9 1.3 7.9

EM 16.0 1.6 10.1

US 24.3 3.7 15.8

International vs US Relative Valuation(Equal-weighted composite of relative P/E, P/B, and P/CF multiples, ACWIxUS vs US)

HARDING LOEVNER 21

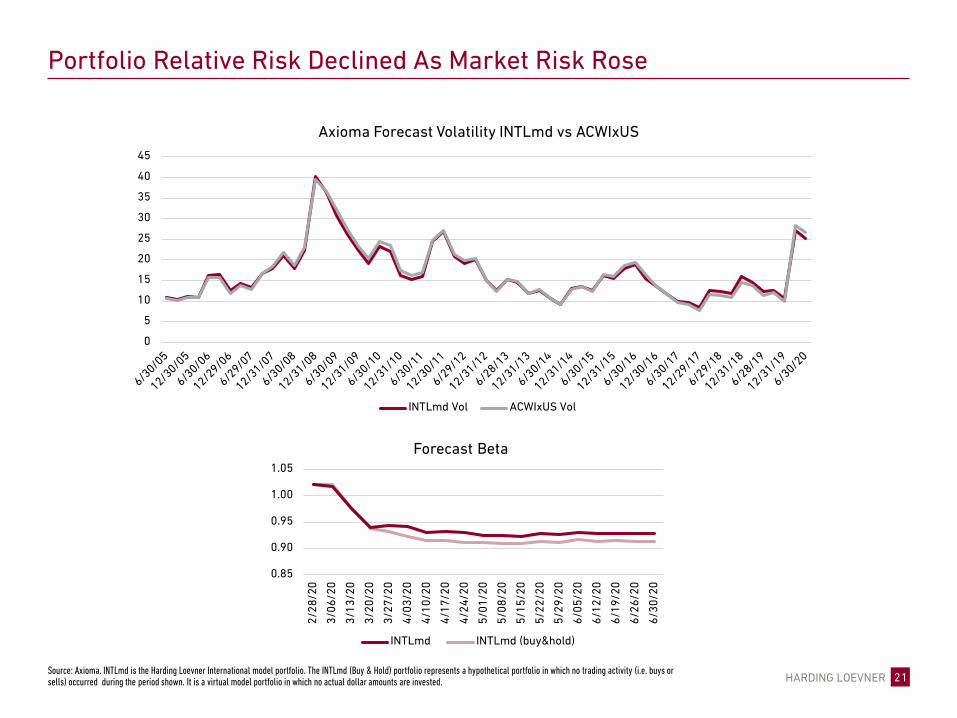

Portfolio Relative Risk Declined As Market Risk Rose

Source: Axioma. INTLmd is the Harding Loevner International model portfolio. The INTLmd (Buy & Hold) portfolio represents a hypothetical portfolio in which no trading activity (i.e. buys or sells) occurred during the period shown. It is a virtual model portfolio in which no actual dollar amounts are invested.

0.85

0.90

0.95

1.00

1.05

2/28

/20

3/06

/20

3/13

/20

3/20

/20

3/27

/20

4/03

/20

4/10

/20

4/17

/20

4/24

/20

5/01

/20

5/08

/20

5/15

/20

5/22

/20

5/29

/20

6/05

/20

6/12

/20

6/19

/20

6/26

/20

6/30

/20

Forecast Beta

INTLmd INTLmd (buy&hold)

0

5

10

15

20

25

30

35

40

45

Axioma Forecast Volatility INTLmd vs ACWIxUS

INTLmd Vol ACWIxUS Vol

HARDING LOEVNER 22

The information provided in this Presentation should not be considered a recommendation to purchase or sell a particular security. Unless otherwise stated, non-performance based criteria have been used to select the securitieslisted. The portfolio is actively managed therefore securities shown may not be current. It should not be assumed that investment in the securities identified has been or will be profitable. To request a complete list of portfolioholdings for the past year contact Harding Loevner. A complete list of holdings for the International Equity Model at June 30, 2020 is available on request.

Investing in stocks entails the risks of market volatility. The value of all types of stocks may increase or decrease over varying time periods. To the extent the investments depicted herein represent international securities, youshould be aware that there may be additional risks associated with international investing, including foreign economic, political, monetary and/or legal factors, changing currency exchange rates, foreign taxes, and differences infinancial and accounting standards.

Quality & Growth Characteristics, Investment Statistics, Benchmark Returns, Performance Attribution, Portfolio Exposures and Portfolio Transactions are shown as supplemental information only and complement the fullycompliant International Equity Composite GIPS Presentation, which is available on request.

Alpha: a measure of risk-adjusted return. Beta: a measure of the portfolio’s sensitivity to the market. R-Squared: a measure of how well a portfolio tracks the market. Standard Deviation: the statistical measure of the degree towhich an individual value in a probability distribution tends to vary from the mean of the distribution. Information Ratio: a measure of risk-adjusted return calculated by dividing the portfolio active return (i.e., portfolio returnsminus benchmark return) by the standard deviation of the active return. Sharpe Ratio: the return over the risk free rate per unit of risk. Up/Down Capture: a measure of the manager’s performance in up/down markets relative tothe market itself. Profit Margin: relationship of gross profits to net sales. Return on Assets: net income for past 12 months divided by total assets. Return on Equity: the net income divided by total common equity outstanding,expressed as a percent. Debt/Equity Ratio: total long-term debt divided by total shareholder’s equity. Sales Per Share: the total revenue earned per share over a 12-month period, net of returns, allowances, and discounts. EarningsPer Share: portion of a company’s profit allocated to each outstanding share of common stock. Cash Flow: a measure of the cash generating capability of a company calculated by adding non-cash charges (e.g. depreciation) andinterest expense to pretax income. Turnover: calculated by dividing the lesser of Purchases or Sales by Average Capital. Active Share: the proportion of holdings by weight that differ from holdings of the benchmark index.

The MSCI All Country World ex-US Index is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global developed and emerging markets, excluding the US. The Indexconsists of 48 developed and emerging market countries. The MSCI USA Index is designed to measure the performance of the large and mid cap segments of the US market. With 637 constituents, the index covers approximately85% of the free float-adjusted market capitalization in the US. You cannot invest directly in these Indexes.

All performance and data shown are in US dollar terms, unless otherwise noted.

Harding Loevner’s Quality, Growth, and Value rankings are proprietary measures determined using objective data. Quality rankings are based on the stability, trend, and level of profitability, as well as balance sheet strength.Growth rankings are based on historical growth of earnings, sales, and assets, as well as expected changes in earnings and profitability. Value rankings are based on several valuation measures, including price ratios.

The Composite and Attribution returns may show discrepancies due to the different data sources for these returns. Composite performance is preliminary and obtained from Harding Loevner’s accounting system and Attributionreturns are obtained from the FactSet portfolio analysis system. Please note returns from FactSet are not audited for GIPS compliance and are for reference only.

Source (Benchmark Performance, Performance Attribution, Contributors and Detractors): FactSet, Harding Loevner International Equity Composite; MSCI Inc.

Source (Portfolio Exposures, Portfolio Transactions, Portfolio Allocation Comparison, Quality & Growth Characteristics [Run date: July 5, 2020, based on the latest available data in FactSet on this date.]): FactSet; Harding LoevnerInternational Equity Model; MSCI Inc.

Source (Investment Statistics): eVestment Alliance; Harding Loevner International Equity Composite, based on composite returns.

MSCI Inc. and S&P do not make any express or implied warranties or representations and shall have no liability whatsoever with respect to any GICS data contained herein.

FactSet Fundamentals, Copyright 2020 FactSet Research Systems, Inc. Axioma Portfolio and Risk Analytics. All rights reserved.

Disclosures