functional food ingredients-7oct2005

TRANSCRIPT

1

Functional Food Ingredients A Strategic Review of the Key Challenges that are

Shaping the Industry

CASE STUDY: The Omega-3 Fatty Acid Market

Presented by: Kathy Brownlie

October 2005

Agenda

• 01: Frost & Sullivan - Introduction

• 02: Market Overview

• 03: Setting the Scene – Omega-3 Fatty Acid Market

• 04: Supply Side Analysis – Key Market Engineering Measurements: Omega-3 Fatty Acids

• 05: End-User Analysis

• 06: Consumer Analysis (proposed research)

• 07: Reviewing the Options

• 08: Summary

01: Frost & Sullivan - Introduction

4

Information for Sales Strategy

Company Core

Competencies

MarketMeasurements

& Dynamics

MarketCharacteristics

SalesStrategy

Decision Making Framework

Communication

CompanyCulture

5

Frost & Sullivan – A Holistic Approach to Research

Frost & Sullivan’s has global data collectioncapabilities for both quantitative and qualitative methods .

State-of-the-art qualitative and quantitative analysis derive deep insights into customer behaviour and attitudes.

Frost & Sullivan’s thorough knowledge of the context in which your business operates, combined with world-class Global Customer Researchcapabilities provides the insights necessary to support your growth strategy.

Frost & Sullivan’s Growth Partnership Servicesprovides a complete and comprehensive range of services, integrating demand-side and supply-side insights, to support strategic action across the value web.

6

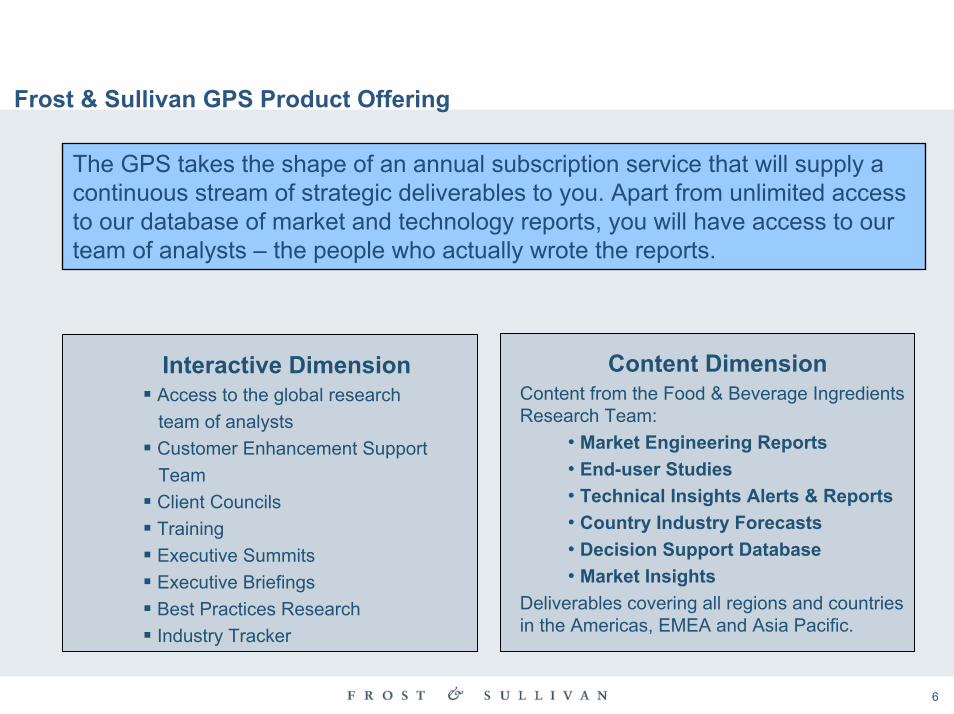

Frost & Sullivan GPS Product Offering

The GPS takes the shape of an annual subscription service that will supply a continuous stream of strategic deliverables to you. Apart from unlimited access to our database of market and technology reports, you will have access to our team of analysts – the people who actually wrote the reports.

Content DimensionContent from the Food & Beverage Ingredients Research Team:

• Market Engineering Reports• End-user Studies• Technical Insights Alerts & Reports• Country Industry Forecasts• Decision Support Database• Market Insights

Deliverables covering all regions and countries in the Americas, EMEA and Asia Pacific.

Interactive DimensionAccess to the global research team of analystsCustomer Enhancement Support TeamClient CouncilsTrainingExecutive SummitsExecutive BriefingsBest Practices ResearchIndustry Tracker

7

Research Services – Market and Customer ResearchFood Ingredients and Additives, Nutraceuticals, Animal Nutrition

Market segment analysis that provides drivers and restraints, industry challenges, forecasts and competitor analysis

Strategic SnapshotsLegislative Reviews, Opportunity Analysis, Industry Outlooks

Issue based research titles

Technical InsightsInformation on current and emerging technologies

Country Industry ForecastsDiscussion of specific industries in selected countries along with supporting

quantitative market measurements

Decision Support DatabasesKey market data, export and import data on selected industry sectors

GPS SUBSCRIPTION DELIVERABLES

8

Types of Research

Technology Assessment• Technology trends• Evaluation of existing & emerging

technologies

Market Environment• Market drivers & restraints• Industry challenges

Market Sizing & Forecasts• Demand analysis• Pricing trends• Application analysis

Competitive Profiling• Product analysis• Competitive strategies• Market share analysis

9

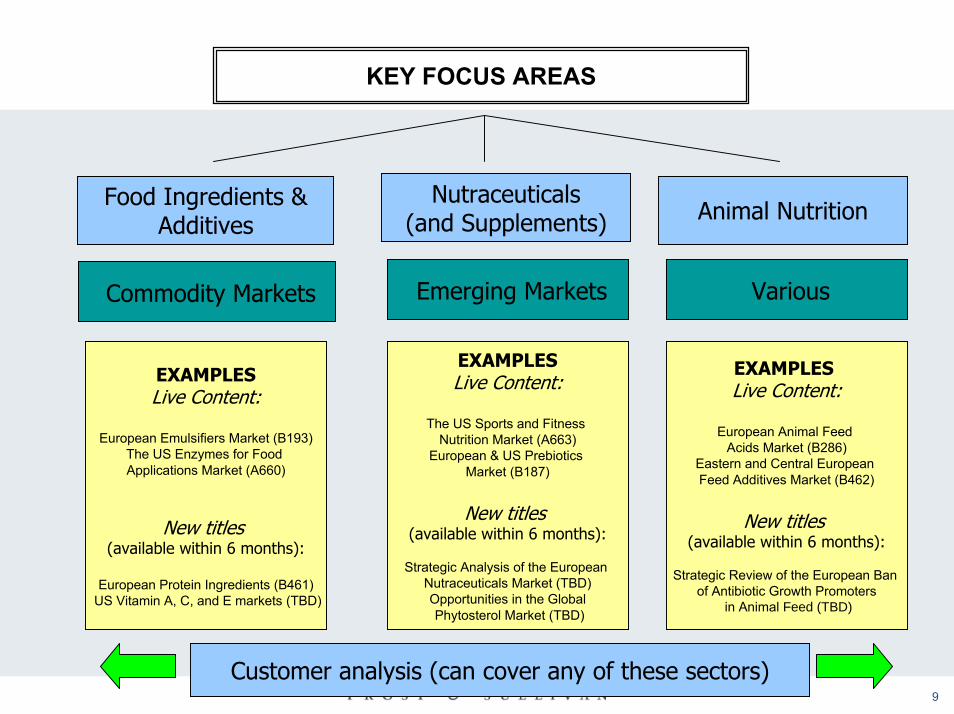

KEY FOCUS AREAS

Nutraceuticals(and Supplements)

Food Ingredients &Additives Animal Nutrition

Emerging Markets VariousCommodity Markets

EXAMPLESLive Content:

The US Sports and Fitness Nutrition Market (A663)

European & US Prebiotics Market (B187)

New titles(available within 6 months):

Strategic Analysis of the European Nutraceuticals Market (TBD)Opportunities in the GlobalPhytosterol Market (TBD)

EXAMPLESLive Content:

European Animal Feed Acids Market (B286)

Eastern and Central European Feed Additives Market (B462)

New titles(available within 6 months):

Strategic Review of the European Ban of Antibiotic Growth Promoters

in Animal Feed (TBD)

EXAMPLESLive Content:

European Emulsifiers Market (B193)The US Enzymes for Food Applications Market (A660)

New titles(available within 6 months):

European Protein Ingredients (B461)US Vitamin A, C, and E markets (TBD)

Customer analysis (can cover any of these sectors)

02: Market Overview

11

Presentation Objectives

Through a case study looking at the Omega-3 fatty acids market, this presentation will illustrate the complexities of conducting business in today’s food ingredients industry. This presentation will provide an overview of:

The challenges facing the food industry

What end-users really want from their suppliers

Examples of tools that can be used to assess various opportunities in the market

12

Food Ingredient - Key Challenges (examples)

Limited understanding oftechnology capabilities

Shelf life and other

stability issues

Achieving an acceptable flavour and taste profile

Not enough success stories in the functional food sector

Market Size and

Growth

Costly clinical development process

End-User Perceptions:

e.g. quality, safety

Uncertain RegulatoryEnvironment (health claims)

13

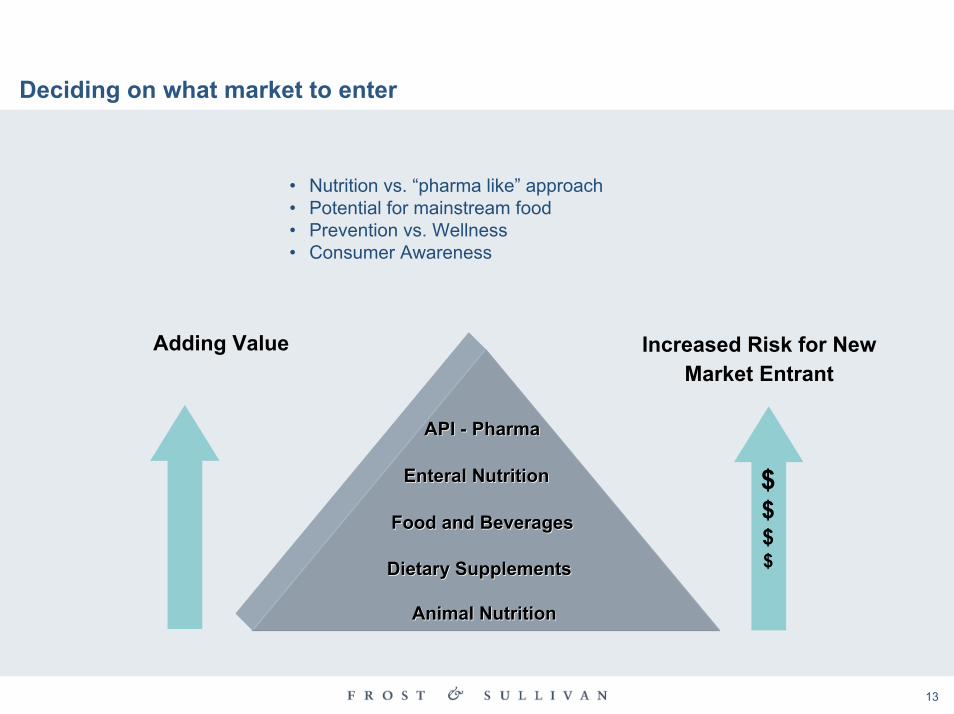

Deciding on what market to enter

• Nutrition vs. “pharma like” approach• Potential for mainstream food• Prevention vs. Wellness• Consumer Awareness

Adding Value

Enteral NutritionEnteral Nutrition

Animal NutritionAnimal Nutrition

Dietary SupplementsDietary Supplements

Food and BeveragesFood and Beverages

API API -- PharmaPharma

Increased Risk for New Market Entrant

$$$$

14

In order to achieve greatest ROI - we need to position the product within the most appropriate application

Product Positioning: Identifying the Source and Applications

• Flax Oil

• Omega-6 oils – Evening Primrose, Borage

• Low concentrates, or high concentrates

• Powder or Oil

• Branded Products

• Tuna oil vs. sardine oil vs. menhaden oil

• Animal Feed

• Pet Food

• Dietary Supplements

• Bakery Products

• Beverages

• Enteral Nutrition / Medical Food

• Pharmaceuticals

= > APPLICATION SUPPORT

• Emerging Markets: Eastern Europe

• Age Segmentation: Children, Young Woman, Elderly

• Pet Food Supplements

• Sports Nutrition

• Health Platform Segmentation: Heart Health, Joint Health

• Multivitamin Solutions

What Omega-3 source should we investigate ?

What application should we target ?

What application should we target ?

How should we position the product ?

15

Frost & Sullivan – Research Capabilities

Frost & Sullivan Analysis MARKET ENGINEERING

INDUSTRY STRUCTURE

Trader

Oil Refinery

Supplement manufacturer Food / Beverage manufacturer

CONSUMER

Ingredient Supplier

Crude Oil extractor/manufacturer

Crop grower/Fishing company

Frost & Sullivan Analysis END-USER ANALYSIS

Frost & Sullivan Analysis CONSUMER ATTITUDES

03: Setting the Scene – The Omega-3 Fatty Acid Market

17

Flax OilFlax Oil Marine OilMarine Oil Algae OilAlgae Oil

Omega-3 Fatty Acid: Sources

Adv:- LC EPA and DHA- Traditional history of use

Dis:- Sensory Profile- Quality Issues- Negative end-user

perception

Adv:- DHA only- Niche Market High Value

Applications

Dis:- High Cost- No EPA- Threat of Substitutes

Adv:- Low Cost- Contains other active components e.g. fibres

Dis:- SC Fatty Acids (ALA) –

limited nutritionalproperties

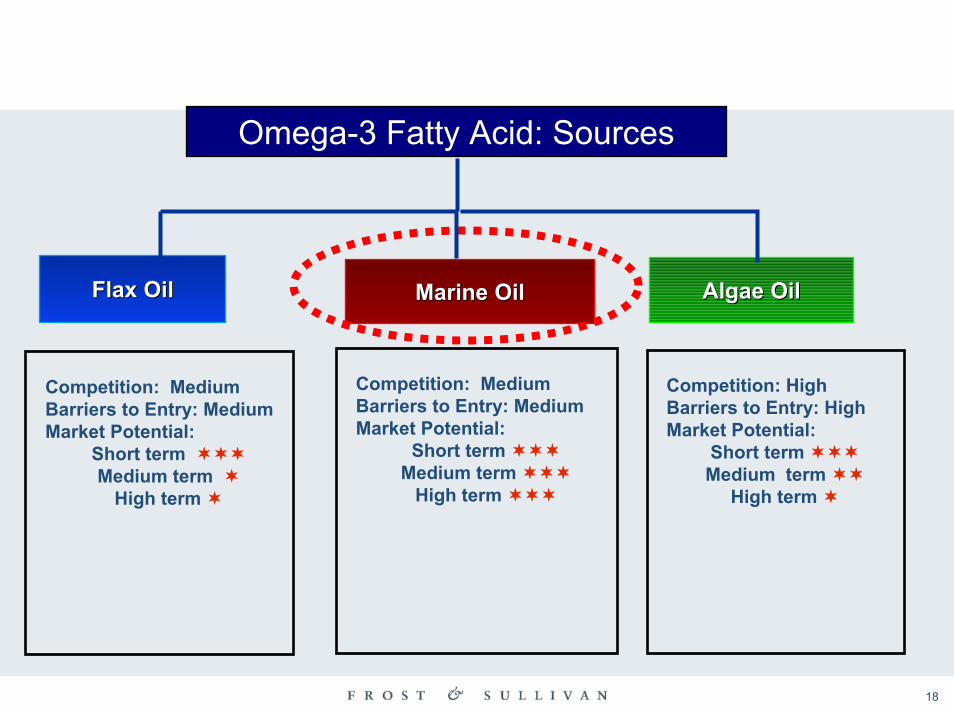

18

Flax OilFlax Oil Marine OilMarine Oil

Omega-3 Fatty Acid: Sources

Algae OilAlgae Oil

Competition: MediumBarriers to Entry: MediumMarket Potential:

Short term Medium term

High term

Competition: HighBarriers to Entry: HighMarket Potential:

Short term Medium term

High term

Competition: MediumBarriers to Entry: MediumMarket Potential:

Short term Medium term

High term

19

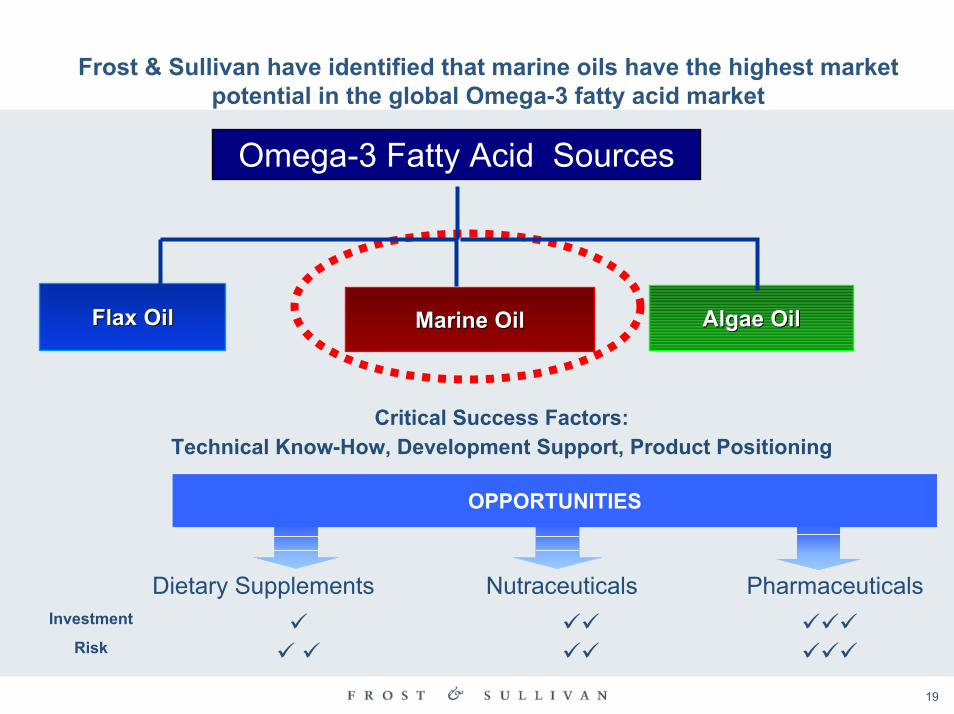

Frost & Sullivan have identified that marine oils have the highest market potential in the global Omega-3 fatty acid market

Flax OilFlax Oil Marine OilMarine Oil Algae OilAlgae Oil

Omega-3 Fatty Acid Sources

Critical Success Factors: Technical Know-How, Development Support, Product Positioning

Dietary Supplements Nutraceuticals Pharmaceuticals

Risk

Investment

OPPORTUNITIES

04: Supply Side Analysis Key Market Engineering Measurements

Omega-3 Fatty Acids

21

INDUSTRY STRUCTURE

Trader

Oil Refinery

Supplement manufacturer Food/Beverage manufacturer

CONSUMER

Ingredient Supplier

Crude Oil extractor/manufacturer

Crop grower/Fishing company

Frost & Sullivan Analysis MARKET ENGINEERING

Frost & Sullivan Analysis END-USER ANALYSIS

Frost & Sullivan Analysis CONSUMER ATTITUDES

22

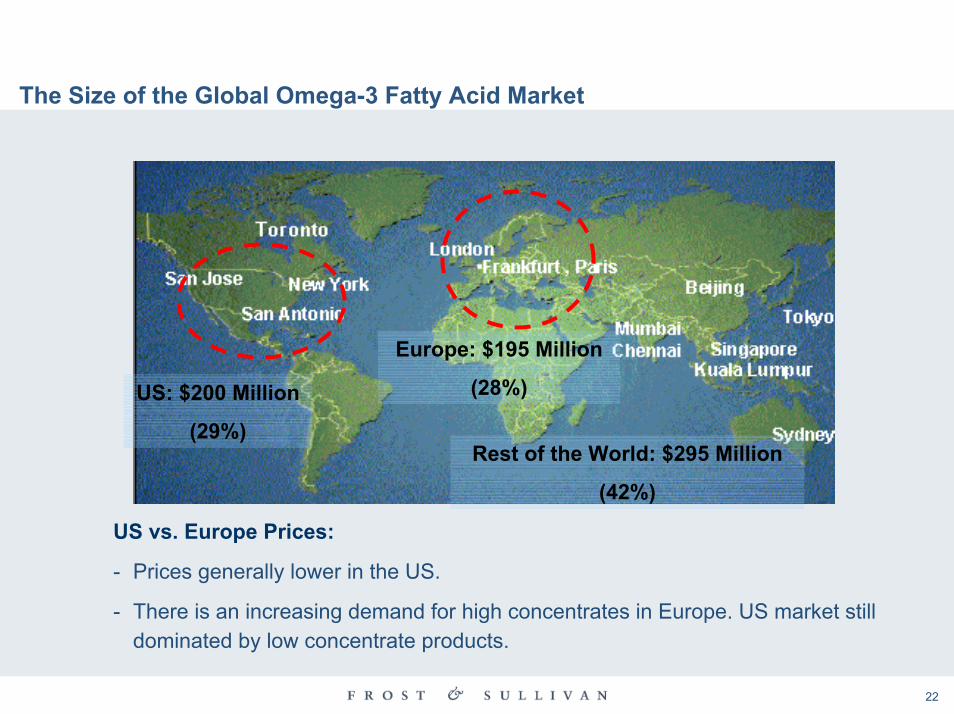

The Size of the Global Omega-3 Fatty Acid Market

Europe: $195 Million

(28%)US: $200 Million

(29%)Rest of the World: $295 Million

(42%)

US vs. Europe Prices:

- Prices generally lower in the US.

- There is an increasing demand for high concentrates in Europe. US market still dominated by low concentrate products.

23

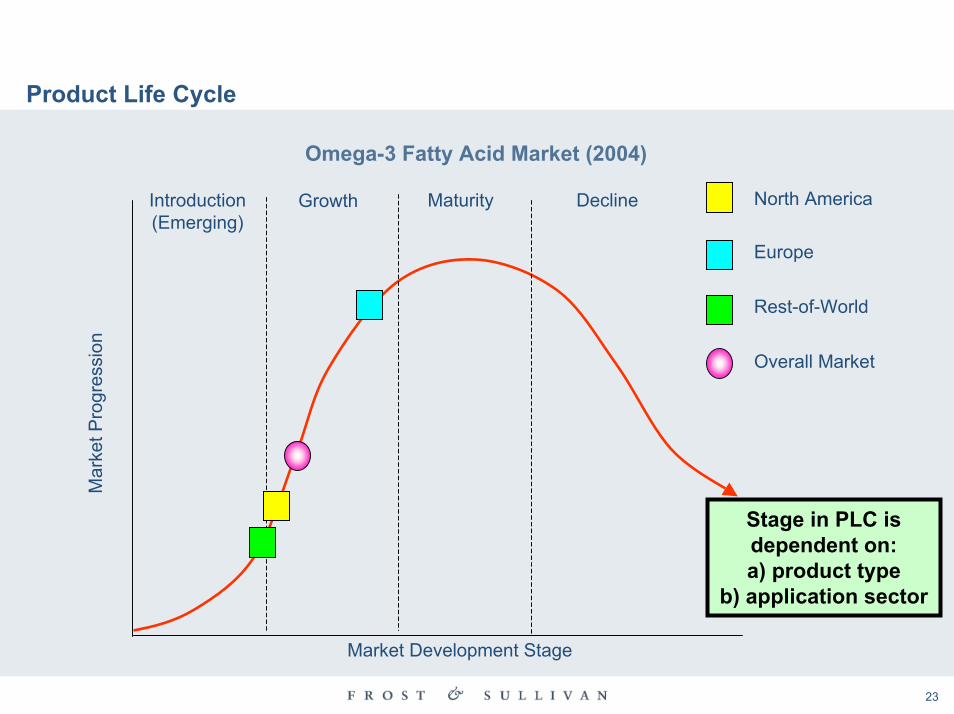

Product Life Cycle

Omega-3 Fatty Acid Market (2004)

Europe

Rest-of-World

Overall Market

Mar

ket P

rogr

essi

on

Stage in PLC is dependent on: a) product type

b) application sector

North AmericaMaturity DeclineIntroduction(Emerging)

Growth

Market Development Stage

24

Top 3 Industry Challenges:• End-User Perceptions, Uncertain Regulatory Environment, Threat of Substitution

Flax OilFlax Oil Marine OilMarine Oil Algae OilAlgae Oil

Omega-3 Oils

Marine oil Market (Europe) – Critical Data (2004) Marine oil Market (US) – Critical Data (2004)CAGR total market (value 2005-2011): 12%CAGR total market (value 2005-2010): 7 %

25

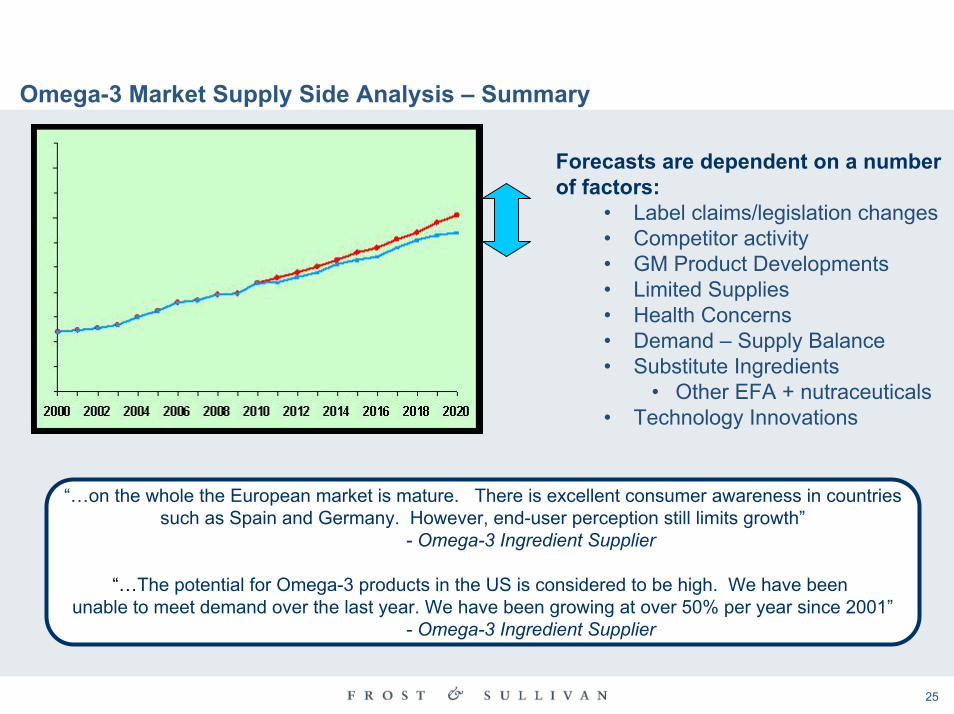

Omega-3 Market Supply Side Analysis – Summary

Forecasts are dependent on a number of factors:

• Label claims/legislation changes• Competitor activity• GM Product Developments• Limited Supplies• Health Concerns• Demand – Supply Balance• Substitute Ingredients

• Other EFA + nutraceuticals• Technology Innovations

“…on the whole the European market is mature. There is excellent consumer awareness in countriessuch as Spain and Germany. However, end-user perception still limits growth”

- Omega-3 Ingredient Supplier

“…The potential for Omega-3 products in the US is considered to be high. We have been unable to meet demand over the last year. We have been growing at over 50% per year since 2001”

- Omega-3 Ingredient Supplier

26

Global Omega-3 PUFA Marine Oil Market: Competitive Environment (2004)

Buyer power is dependent on:a) Availability of substitute

productsb) Consumer awareness of

Omega-3 benefitsCompetition from other nutraceutical ingredients.

Companies traditionally involved in the commodity market are trying to enter the value added product market.

The demand for fish oil globally has increased. However, resources are limited. The consolidated nature of the industry may make it more difficult to remain dynamic in the long term.

27

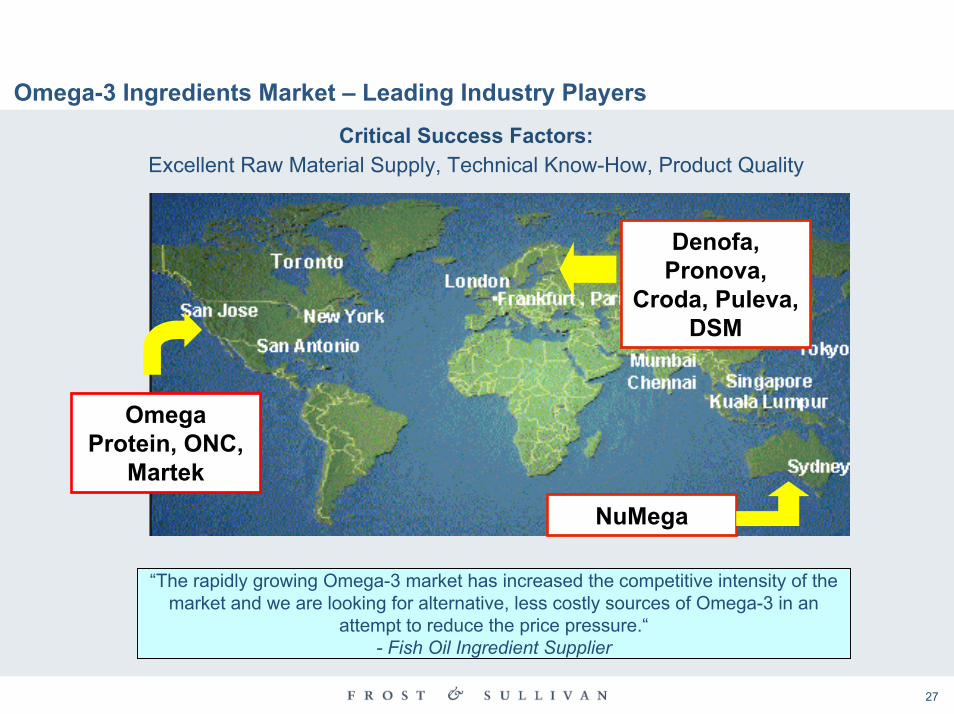

Omega-3 Ingredients Market – Leading Industry Players

Critical Success Factors:Excellent Raw Material Supply, Technical Know-How, Product Quality

Denofa, Pronova,

Croda, Puleva, DSM

Omega Protein, ONC,

Martek

NuMega

“The rapidly growing Omega-3 market has increased the competitive intensity of the market and we are looking for alternative, less costly sources of Omega-3 in an

attempt to reduce the price pressure.“- Fish Oil Ingredient Supplier

28

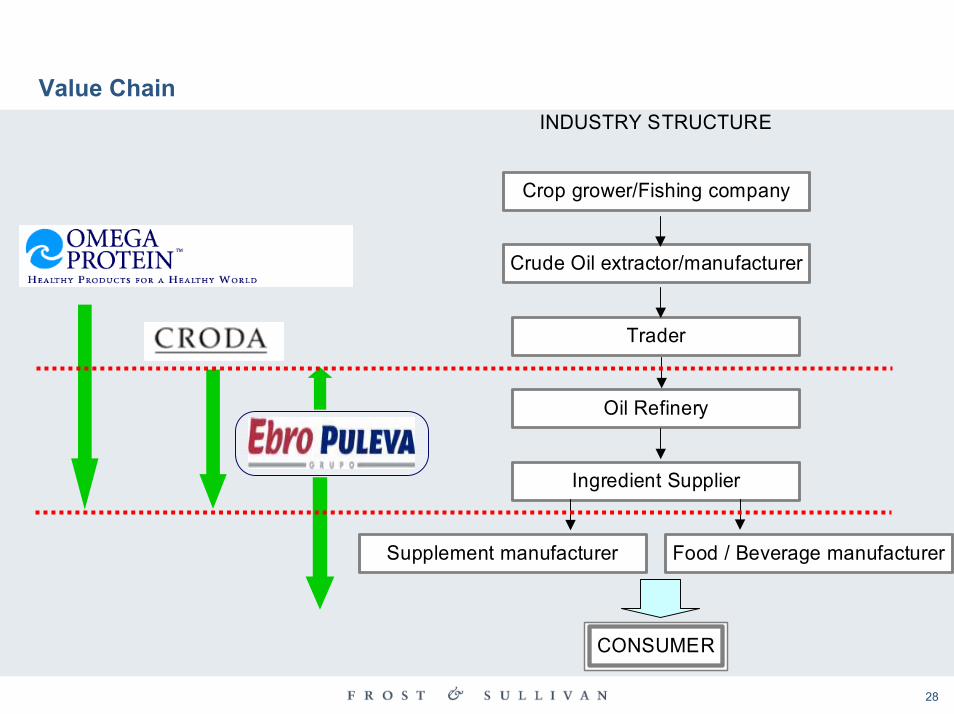

Value ChainINDUSTRY STRUCTURE

Trader

Oil Refinery

Supplement manufacturer Food / Beverage manufacturer

CONSUMER

Ingredient Supplier

Crude Oil extractor/manufacturer

Crop grower/Fishing company

06: End-User Analysis – Market Insights

1. Objectives

2. Key Findings – Purchasing

3. PUFA ingredients: Algae oil vs. Marine Oil

4. GM Issues

30

INDUSTRY STRUCTURE

Trader

Oil Refinery

Supplement manufacturer Food / Beverage manufacturer

CONSUMER

Ingredient Supplier

Crude Oil extractor/manufacturer

Crop grower/Fishing company

Frost & Sullivan Analysis MARKET ENGINEERING

Frost & Sullivan Analysis END-USER ANALYSIS

Frost & Sullivan Analysis CONSUMER ATTITUDES

31

1) Objectives

• Objective analysis of end-users’ key purchasing criteria and supplier selection process• Examples of the types of questions asked:

• How do you foresee the market development of PUFAs in the long term? • What are your key purchasing criteria?• What processes do you have in place for selecting new ingredients or

suppliers?• How much technical support do you expect from a supplier?• Would you consider using a GM PUFA ingredient ?

• Ultimately, this type of analysis will identify the key drivers for growth as seen through the eyes of the end-user

32

2) Key Findings – Product Type (examples)

• Powder vs. Oil“…final products are in liquid form, hence oils are the logical choice”

- Omega-3 ingredient supplier

• Concentration Preferred“…Omega-3 concentrations and product formulations are really dependant on our end-users and what application sectors they are active in”

- Omega-3 ingredient supplier

“…Consumers are demanding supplements with higher concentrations”- Omega-3 ingredient supplier

• Types of concentrate: Triglycerides vs. Ethyl Esters vs. Reconstituted Triglycerides. “…there is a perception in the market that triglycerides are more natural but it hasn’t been proven”

- Omega-3 ingredient supplier

33

3) Developing a PUFA Fortified Product

Have you developed your products on your own or in co-operation with your PUFA supplier ?

“Independently” 60%

By Application:

Beverage Products 50%Dairy Products 40%Bakery Products 50%Dietary Supplements 60%Clinical Nutrition 80%Infant Nutrition 60%

34

4) GM PUFA Ingredients

“….this would not suit our marketing strategy since GM food has to be declared in Germany and is not perceived as healthy food”

“…we would be interested, especially if the concept is accepted by society”“…we position our products at the health conscious consumer market. Using GM ingredients would

contradict the message we are trying to send out to consumers.”- End-Users (Food and Beverage Industry)

30% Companies said that they would consider the use of GM PUFA ingredients. Breakdown by application:

• Beverage Products 25%• Dairy Products 20%• Bakery Products 50%• Dietary Supplements 10%• Clinical Nutrition 60%• Infant Nutrition 40%

Factors that this response was dependent on include: Cost, Consumer acceptance. Regulatory restraints

Genetic modification could lead to cheaper sources of Omega-3 fatty acids. Would you be interested in these new developments or ingredients ?

35

End-User Analysis – Summary

End-users have different needs. These are dependent on: Application, previous experience

with product, existing processing facilities, local country regulations etc. Ingredient suppliers need to adapt their marketing strategy according to the end-user base

they are targeting.

• Focus on supplier support. • Still negative perception in the use of Omega-3 Ingredients in food and beverage

products

EXISTING USERS

NEW USERS

• Focus on price, and reliability of supply

07: Consumer Attitude Analysis

37

INDUSTRY STRUCTURE

Trader

Oil Refinery

Supplement manufacturer Food / Beverage manufacturer

CONSUMER

Ingredient Supplier

Crude Oil extractor/manufacturer

Crop grower/Fishing company

Frost & Sullivan Analysis MARKET ENGINEERING

Frost & Sullivan Analysis END-USER ANALYSIS

Frost & Sullivan Analysis CONSUMER ATTITUDES

38

Study Background

“…. consumers’ preference has now undergone a paradigm shifted from synthetic ingredients toward natural and organic foods, beverages and supplements. Present

day’s consumers are more informed and this could be attributed to current day media, which keeps consumers abreast of the latest scientific developments in health and wellness. Consumers are now moving toward food products that are obtained from

natural non-GMO (genetically modified organism) extracts.” – Frost & Sullivan Global Advances in Nutraceuticals (Technical Insights), 2005

Since the introduction of Genetically Modified (GM) food, consumers have been increasingly concerned about the potential health risks associated with the long term consumption of such products. Consumer perceptions vary by country but are more pronounced in Europe where the issue has received strong media coverage. These have had a profound and controversial effect on perceptions and attitudes to GM products which has fuelled, at least in some countries, much anti-GM sentiment.

39

The aim of the study is to:

• Understand consumer attitudes to GM foods and whether these have changed over recent years?

• Determine the influence of the media, government and manufacturers on consumer attitudes and behaviour.

• Identify main concerns of consumers to GM food, and establish means of overcoming any barriers to acceptance.

• Identify and measure opportunities through consumer segmentation

Study Objectives

40

Deliverables: What influences consumer attitudes towards GM foods?

TV news

Press

TV programme

Magazine article

Internet

Manufacturers

Government

Negative InfluencePositive Influence

Sample Figure Only

Reinforce messages Reassess messages

41

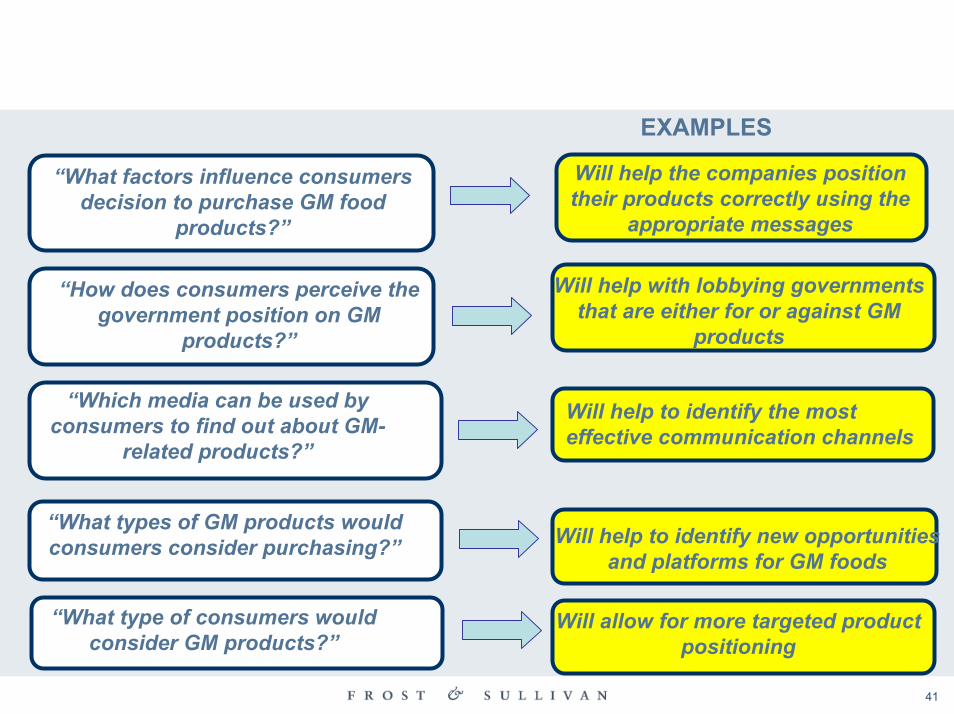

EXAMPLES

Will help the companies position their products correctly using the

appropriate messages

“What factors influence consumers decision to purchase GM food

products?”

Will help with lobbying governments that are either for or against GM

products

“How does consumers perceive the government position on GM

products?”

“Which media can be used by consumers to find out about GM-

related products?”

Will help to identify the most effective communication channels

“What types of GM products would consumers consider purchasing?” Will help to identify new opportunities

and platforms for GM foods

“What type of consumers would consider GM products?”

Will allow for more targeted product positioning

07. Reviewing the Options

43

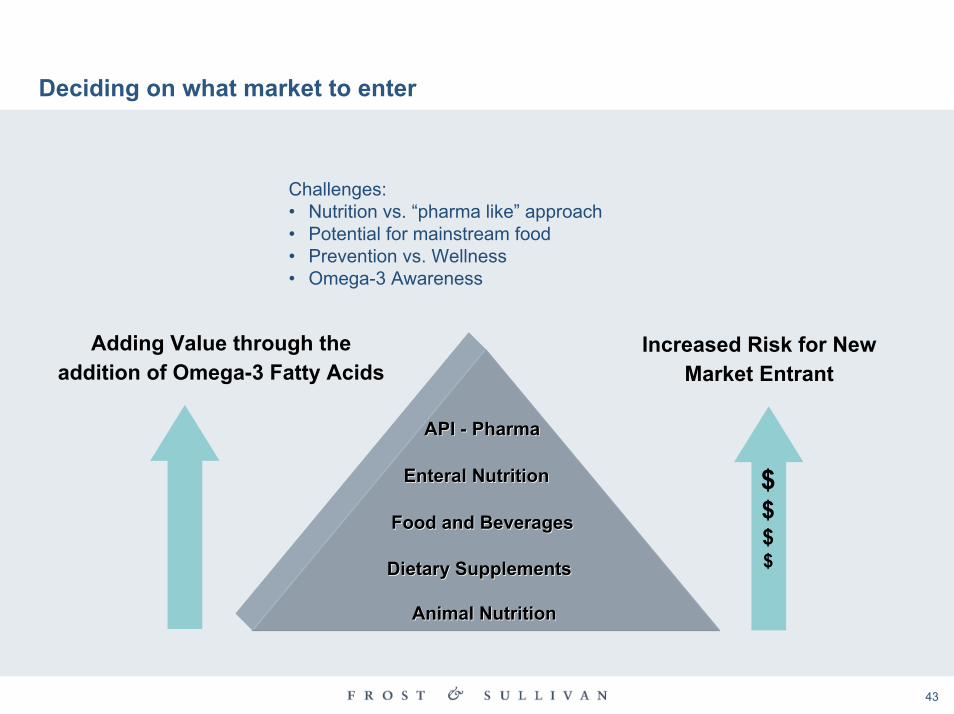

Deciding on what market to enter

Challenges:• Nutrition vs. “pharma like” approach• Potential for mainstream food• Prevention vs. Wellness• Omega-3 Awareness

Adding Value through the addition of Omega-3 Fatty Acids

Enteral NutritionEnteral Nutrition

Animal NutritionAnimal Nutrition

Dietary SupplementsDietary Supplements

Food and BeveragesFood and Beverages

API API -- PharmaPharma

Increased Risk for New Market Entrant

$$$$

44

Key Market Indicators – Omega-3 Fatty Acids

High

Competition High

Top five companies <20%

Product Life Cycle Growth

Restraints Low

Drivers High

Time to Market Short

Barriers to Entry Low

Cost of Product Low

Medium

90%

Developing

Medium

Long

CriteriaCriteria Dietary Dietary SupplementsSupplements

High

50%

Growth

Medium

High

Medium

Low

Low

NutraceuticalsNutraceuticals

High

PharmaceuticalsPharmaceuticals

High

45

Identifying the best fit product with application is crucial for successful introduction

NutraceuticalsTechnical and application support is a must for any company

considering entering this market.

CRITICAL SUCCESS FACTORSCRITICAL SUCCESS FACTORS• Development of food prototypes

with optimal taste and functional

properties

• Technology know-how

• Nutritional and clinical scientific

evidence

• Product development, process and

product launch support