function of public officers’ sworn declaration of …

TRANSCRIPT

TRA. 3031-05/N

COMPTROLLER GENERAL’S OFFICE OF THE REPUBLIC OF PERU

FUNCTION OF PUBLIC OFFICERS’ SWORN DECLARATION

OF INCOME, PROPERTY AND REVENUES AS A TOOL IN THE FIGHT AGAINST CORRUPTION

SWORN DECLARATIONS AUDIT MANAGEMENT

LIMA- PERU

October 2005

FUNCTION OF PUBLIC OFFICERS’ SWORN DECLARATION OF INCOME, PROPERTY AND REVENUES, AS A TOOL IN THE FIGHT AGAINST CORRUPTION

Table of Contents..............................................................................................................….. I Table of Figures ..................................................................................................................... II Table of Exhibits...............................................................................................................….. III

TABLE OF CONTENTS

I. Introduction............................................................................................................................. 1II. Conceptual Framework ……………………………………………………………………………. 3III. Accountability and Sworn Declarations ………………………………….....…………….…… 3IV. Legal background of sworn declarations regime in Peru ............................….............….. 4V. Sworn Declarations of Income, Property and Revenues in Peru .…………………...…….. 5 V.1 Contents .......................................................................................................................... 5 V.2 Officials obliged to submit and list of the obligors’ appointments and

contracts.......................................................................................................................... 6

V.3 Publication and timing ..................................................................................................... 6 V.4 Responsibilities of the Heads of Administration and of the Senior Officers of Budget

Items................................................................................................................………….. 7

V.5 Failure to submit sworn declarations .........................................................................…… 7 V.6 Non Compliance and Penalties ......................... .............................................……..……. 8 V.7 Auditing.............................................................................................................................. 8 V.8 Illicit Enrichment ......................................................................................................……… 9VI. Sworn Declarations Audit Management ........................................................…..………….. 9 VI.1 Structure and Organization................................................................................................ 10 VI.2 Verification Units, Registration and Filing of Sworn Declarations..........................………. 10 VI.3 Legal Advisory Unit ..............................................................................................……….. 11 VI.4 Audit Unit of Sworn Declarations....................................................................................... 12VII. Limitations to the Present System ...............................................................................……. 14VIII. Proposals for a change......................................................................................................…. 14IX. Conclusions ........................................................................................................................... 16X. List of Acronyms ...............................................................................................................…. 17XI. Bibliography............................................................................................................................ 17XII. Exhibits.................................................................................................................................... 18

(I)

TABLE OF FIGURES Figure 1 CGRP: Strategic Plan and Audit Of Sworn Declarations.................................................……………. 2Figure 2 Sworn Declarations Audit Management: Organization Chart ...............................................……….. 10Figure 3 Sworn Declarations: Verification, Registration y and Filing Processes............................................... 11Figure 4 Sworn Declarations: Auditing. Process ...........................................................................……………. 13Figure 5 Sworn Declarations Audit Management: Processes ....................................................……………… 19

(II)

TABLE OF EXHIBITS EXHIBIT 1 Sworn Declarations Audit Management: Statistics..................................................……………….... 18EXHIBIT 2 Sworn Declarations Audit Management: Processes .....................................................……….…… 19EXHIBIT 3 Sworn Declarations Audit Management : Prisma Process ..........................................……………... 19

(III)

1

I. INTRODUCTION The issue of corruption is one of the social problems, which in the last decade has gained the greatest importance in the Latin American countries. The most widely used definition of corruption is “the abuse of public power in order to obtain a private benefit”1, it is, however a phenomenon that includes a range of conducts, functions and contexts. Seeing as it is a latent threat and considering its negative consequences for society; it is agreed that it has to be dealt with urgently; either by applying preventive measures (to avoid that such acts of corruption occur or are repeated in the future), measures of detection and exposure of illicit acts or by punitive measures aimed at deterrence. This document presents the progress made and the initiatives taken by the Comptroller General’s Office of the Republic of Peru (CGRP), through the Sworn Declarations Audit Management, as part of the implementation of one of its institutional priorities defined in the 2002-2006 Multiannual Strategic Plan2 regarding the development of policies that will allow extending the coverage, quality and timeliness of the control services, within a proactive approach and the development of new coercive methods of control, based on methodological investigation work, techniques and documentation processes. The third general strategic objective (“Promoting and participating in the eradication of corruption”), seeks to fight corruption in an institutionalized framework that develops and/or strengthens the mechanisms of prevention, correction and penalty; that is why it ordered the creation of the Sworn Declarations Audit Management in January, 2004, as an organ promoting a culture of probity and transparency in the exercise of public functions. In this context, the Sworn Declaration of Income, Property and Revenues is a preventive tool against corruption; it enables us to identify whether the government employee’s conduct is honest, upright and honorable. The results to date that are presented in this document, show the efforts made by the Sworn Declarations Audit Management in its short lifespan as part of a strategy which must become “integral” and be built on the basis of a regulatory system that guarantees the application of penalties and effective compliance with the presentation of sworn declarations of income, property and revenues.

1 Source: Website: www.findarticles.com/p/articles/ mi_go2228/is_200312/ai_n6642504 - 20k – Supplementary Result. 2 The Multiannual Strategic Plan is a set of activities to be developed by a specific entity, it is inter-articulated and stated in physical and monetary units, it is expressed in a specific plan which constitutes a tool to guide the execution of resources in the fulfillment of its fundamental duties. Source : CGRP‘s 2002-2006 Strategic Sectorial Multiannual Plan.

2

Source: CGRP‘s 2002-2006 Strategic Multiannual Plan Preparation: Sworn Declarations Audit Management

Figure 1 CGRP: STRATEGIC PLAN AND AUDIT OF SWORN DECLARATIONS

Vision and Mission

“To be the State’s model institution…,

which allows the population to trust and feel secure about the adequate use of public resources by means of appropriate and

efficient control…”

Institutional Priorities “2º. Develop new coercive methods of

control, based on methodological investigation work, techniques and

documentation processing.

General Strategic Objective: 3º. To promote and participate in the eradication of corruption

Actions to address the sector’s problems:

Auditing Declarations of Income, Property and Revenues of public officers

Fighting corruption in an institutionalized framework that develops and/or strengthens the mechanisms of prevention, correction and penalty, seeking to provide greater transparency in the exercise of public service.

3

II. CONCEPTUAL FRAMEWORK This paper uses the generic definition of declaración jurada (sworn declaration). In Peru it is defined as “The Sworn Declaration of Income, Property and Revenues is a written manifestation presented by those who administer, dispose over, guard, collect and in general, under any concept, administer public goods and resources, regarding certain aspects of the situation of their personal assets and finances, taking responsibilities for the statements they make, if they are found to be false or information is omitted3.” The Spanish term “declaración jurada” (sworn declaration) is widely used in Latin America4. This term is practically synonymous to the terminology used for reports, simple declarations or records of personal financial situation. Sworn Declarations of Property contain information about the personal interests of a civil servant. III. ACCOUNTABILITY AND SWORN DECLARATIONS Transparency, accountability and the fight against corruption, are fundamental principles that should govern the performance of the State’s administration, because it contributes to consolidate society’s trust in its institutions. Transparency has a double function; on one hand, it is the support of a credible democracy, where it is strengthened insofar the citizens identify themselves with it, and plays an economic and social role, enabling the goods and services market in general, and in particular public sector entities, to function as a market economy Public officials are under the obligation to account for the administration and the use of the public resources entrusted upon them; this is directly related to the terms of transparency and responsibility. The English term “accountability” has no exact translation in Spanish, therefore it has been coined to the meaning of “rendición de cuentas”, which means the obligation all civil servants have to account for the use of the public resources they were entrusted and the results of their administration, which, undoubtedly, means conferring transparency to public acts. The trust is a legal transaction by which a person submits or more specific assets to a trustee who commits to administer or transfer them in order to fulfill a specific purpose.5 Therefore, since the public resources were entrusted to public officers and/or civil servants, the figure of a trust arises, since the public sector has been put in charge of a common asset. The sworn declaration made by the public officer, civil servant or person holding a public office entails his/her total monthly income from all public and/or private sources, as well as the revenues and property (including financial assets) he/she may own, obtained both in Peru and elsewhere, duly specified and appraised, this being the way of rendering his/her “accountability”. Publication of the sworn declaration of income, property and revenues is mandatory, enabling the citizens to know how the people the State has entrusted with its resources, have lived up or not to the trust shown to them, and thus citizens can audit them by knowing the information they have declared.

3 Source: Technical Regulations of Internal Control, approved by Comptroller General’s Office Resolution 072-98-CG dated

June 26, 1998 and modified by Comptroller General’s Office Resolution 123-2000-CG dated June 23, 2000. 4 Source: “La Corrupción Pública en América Latina: Manifestaciones y mecanismos de control” (“Public Corruption in Latin

America: Manifestations and control mechanisms”), consulted on October 05, 2005 on the website: lapaz.usembassy.gov/Corruption/corrupcion.pdf.

5 Source: “La Fiducia” (The Trust), consulted on November 7, 2005 on the website : www.fiducafe.com.co/html/body_negocios_fiduciarios.htm

4

IV. LEGAL BACKGROUND OF SWORN DECLARATIONS REGIME IN PERU A sworn declarations regime has existed in Peru since 1933. The Constitution at the time included it in its Article 22°, which literally established that, “all public, civil or military officers or employees having properties or income independent from their remunerations as such, are under the obligation of stating them expressly and specifically, in the form determined by the Law.” At the time, there was no law regulating it, but on August 17, 19636, a Supreme Decree was published outlining the first list of those under the obligation to submit such declarations. To date, the most important laws that have regulated the submission of sworn declarations of income, property and revenues are the following: (i) Supreme Decree dated August 17, 1963, established a limiting list of those under the

obligation to submit sworn declaration of income, property and revenues, issued to regulate the stipulations in Peru’s 1933 Political Constitution.

(ii) Law Decree 17095, dated November 6, 1968, by which the laws regulating an improved

submission of sworn declarations of income, property and revenues were established. Said regulations established the obligation to submit declarations at three different points in time, on taking office, leaving office and periodically every three years.

(iii) Law Decree 20475, dated December 20, 1973, by which the list of people under the obligation

to submit declarations was expanded, establishing as well the obligation to submit declarations to Personnel Management or the office serving as Personnel Management.

(iv) The 1979 Political Constitution of Peru, which includes the obligation to submit the pertinent

sworn declarations. Thus, its Article 62 established that public officers or civil servants determined by Law, or who administrate or manage State funds or funds of Organizations financed by the State, must submit a written declaration of property and income on taking and leaving office and periodically during their service.

(v) Law 24801, dated May 14, 1988, which, aside from including more people with the obligation, modified the periodic presentation from three to two years. Furthermore, it abolished the Supreme Decree dated August 17, 1963, Law Decree 17095 and Law Decree 20475.

(vi) Supreme Decree 138-88-PCM dated November 25t 1988, which established regulations for

Law 24801 and stipulated procedures, responsibilities and penalties for public officers and civil servants who had to present the Sworn Declaration of Property and Income.

(vii) 1993 Political Constitution of Peru, in force to date, which also includes said obligation in

Article 41. Furthermore, it establishes in Article 40 the obligation to publish in the official gazette any income, from any source, received by senior public officers and other civil servants stipulated by Law, and according to their positions.

(viii) Law 27482 dated June 14, 2001, which establishes the publication of Sworn Declarations by

Public Officers and Civil Servants of the State. This Law is currently in force and stipulates the three occasions when sworn declarations, today called sworn declaration of income, property and revenues, should be presented: upon taking office, leaving office and with an annual periodicity. This regulation derogated Law 27801 and its Regulations, Supreme Decree 38-88-PCM. Furthermore, it was established that CGRP would be the entity in charge of registering said sworn declarations and filing them as public instruments.

(ix) Supreme Decree 080-2001-PCM dated July 08, 2001, which approved the Regulations for Law

27482, and regulates the stipulations of Law 27482. It determines the Single Format of Sworn Declarations of Income, Property and Revenues and establishes that the Sworn Declaration of Income, Property and Revenues with annual periodicity shall be presented within the first fifteen (15) business days of January, further reducing the three years initially in force.

6 Source: Law Decree 17095, currently abolished.

5

(x) Supreme Decree 003-2002-PCM dated January, 18, 2002, modified Supreme Decree 080-2001-PCM, regarding the regularity of the annual presentation in the first fifteen business days of January. When the Supreme Decree came into force, it changed the annual presentation regarding the regularity of the annual presentation during the first fifteen business days of January to submitting it following twelve months of such administration, office or work. And if twelve months are not reached there would be no obligation to submit such declaration.

(xi) Article 22, paragraph p) of Law 27785 dated July 23, 2002, the Organic Law on the National

System of Control and the CGRP, establishes that CGRP’s powers are to ““receive, register, examine and audit the Sworn Declarations of Income, Property and Revenues, which public officers and civil servants by Law have the obligation to submit.”

(xii) Order 02-2002-CG/AC approved by Comptroller General’s Office Resolution 174-2002-CG

dated September 05, 2002, which establishes the processing and assessment of Sworn Declarations of Income, Property and Revenues of authorities, public officers and civil servants, as well as information about contracts and appointments submitted to the CGRP.

(xiii) Supreme Decree 047-2004-PCM dated June 24, 2004, by which the Single Format of Sworn

Declarations of Income, Property and Revenues was modified, and a distinction is made between the income received by public officers and civil servants from their activities in the Public Sector from those received for their activities in the Private Sector.

Evidently the issue of sworn declarations has become very important over time and has been used as a basic tool in the fight against corruption. The different amendments that have been implemented are a sign of how important this issue has been considered, in the search for the most adequate formula to regulate it. V. SWORN DECLARATIONS OF INCOME, PROPERTY AND REVENUES IN PERU Sworn declarations have evolved over the years as an instrument used in the fight against corruption. Thus, bearing in mind the wide span and complexity of the issue, the CGRP through the Sworn Declarations Audit Management, has defined its actions on the subject of Sworn Declarations of Income, Property and Revenues presented by public officers and civil servants of the State, according to the stipulations in the Regulations of Organization and Functions of the CGRP.7 It is only as of Law 27482, that the CGRP has the power to register and file, as a public instrument, public officers’ and civil servants’ sworn declarations of income, property and revenues. The legal basis for the current regime of presentation of sworn declarations is Law 27482, its regulations, approved by Supreme Decree 080-2001-PCM, and ammendments, wherein the following points are specified: V.1 Contents The contents of the sworn declaration of income, property and revenues is made up of the items income, property (immovable, movable, financial revenues, among others) and revenues of the person obliged to make declarations, both in Peru and abroad. Incomes are understood as, assets and revenues, fees and earnings obtained from leased, subleased or transferred real property, leased, subleased or transferred movable property, interests on placement of capital, royalties, life annuities, per diem allowances or similar concepts, leased movable property, savings, placements, deposits and investments in the financial system, other assets and income belonging to the declarant, credit and liabilities and anything that generates an economic benefit for the obligor8.

7 Approved by Comptroller General’s Office Resolution 110-2004-CG. 8 Source: Article 5 of Supreme Decree 080-2001-PCM, Regulations of the Law regulating the publication of sworn declarations

of income, property and revenues of public officials and civil servants of the State.

6

The CGRP issued Order 02-2002-CG/AC; on “Processing and Assessment of Sworn Declarations of Income, Property and Revenues of Authorities, Public Officers and Civil Servants, as well as information on contracts or appointments;” whose aim was to guide the officers and servants obliged to declare on how to complete such declarations. V.2 Officers obliged to submit and the list of the obligors’ appointments and contracts The public officers obliged to submit sworn declarations of income, property and revenues are senior state officers, as well as those with executive positions, decision power and/or those administrating State funds. Thus, among the obligors, specified in Article 2 of Law 27482, are: (i) President of the Republic and Vice Presidents; (ii) Members of Congress; (iii) Ministers of State and Vice Ministers; (iv) Members of the Supreme Court, Appellate Court and Judges with Special or Mixed Jurisdictions; (v) Government Attorney General, Supreme Attorney Generals, Appellate Attorney Generals and District Attorneys; (vi) members of the Constitutional Court, members of the National Council of Magistrates and the National Electoral Board; (vii) President of the Central Bank; (viii) Ombudsman; (ix) Comptroller General of the Republic; (x) Superintendent of Banking and Insurance; (xi) Mayors and Municipal Councilmen of Municipalities administrating economic resources exceeding 2000 Tax Units (UIT, Spanish acronym) per year; (xii) Ambassadors; (xiii) Regional Presidents; (xiv) Officers, Generals and Admirals of the Armed Forces; (xv) Solicitor Generals; among others. At this point it is necessary to indicate that there is a problem, which has yet to be overcome: the absence of a career line in civil service in Peru, which makes it difficult to determine the exact universe of those obliged to declare9, therefore the senior officers of each budget item are obliged to annually submit a list containing the appointments and contracts of the obligors, as well as detailed information on the total income such obligors receive for said contracts and appointments This information is submitted in January each year to the CGRP, and its purpose is to identify the universe of obligors per entity: It is pertinent to point out that the information contained in said list corresponds to December 31 of the year prior to its submission. V.3 Publication and timing of submission The obligation to publish the sworn declaration stems from Peru’s 1993 Political Constitution and it is regulated by Law 27482 and its corresponding regulations. The Regulations of Law 27482, establishes two formats of sworn declarations, the detailed format, which contains the confidential information, (i) “First Section”, which is to be submitted to the CGRP as an original hardcopy, and filed for safekeeping as a copy authenticated by the General Bureau of Administration of each entity; and (ii) “Second Section” containing information of a public nature, which is the format published in the official gazette “El Peruano.” The second section of sworn declarations with annual periodicity should be published within the first quarter of the budgetary year10 and the declarations of taking or leaving office, work or service within twenty (20) days following their submission. 9 As of October 2005 Law 28175 is in force, the Framework Law of Public Employment, which, for its due implementation,

requires the approval of certain Bills that are currently being debated by the Congress of the Republic of Peru, they are: (i) Bill proposing the “Law on the Administrative Career of Civil Servants”, (ii) Bill proposing the “Law on Public Officials and Trusted Employees”, (iii) Bill proposing the “Law on Management of Public Employment”, (iv) Bill proposing the “Law of Incompatibilities and Responsibilities of Publicly Employed Staff”, and Bill proposing the “Law on the System of Payment of Public Employees.”

10 The budgetary year is currently regulated by Article 29 of Law 28411 – General Law on the National Budget System, a law stipulating that the budgetary year includes the financial year (January 1 to December 31) and the period of regularization (whose period shall be determined by an Order from the National Bureau of the Public Budget; however, it shall under no circumstances exceed March 31 of each year).

7

With regard to the timing of submitting Sworn Declarations of Income, Property and Revenues, currently, the obligor must present them upon taking office, annually during his/her service and upon leaving office, work or service. In the case of taking or leaving office, the obligor must present the sworn declaration within fifteen (15) workdays following any of these events. The annual sworn declaration must be presented by the obligor continuing in office, during the first fifteen (15) business days after completing twelve months in office. V.4 Responsibilities of the Heads of Administration and of the Senior Officers of Budget

Items The General Bureau of Administration or the pertinent office has responsibilities as to the submission of sworn declarations of income, property and revenues of public officers and civil servants. Such responsibilities are regulated by Article 4 of Law 27428 and its Regulation, and are as follows: (i) Send to CGRP the original hardcopy of the first section of the sworn declarations within no

more than seven (7) business days following their reception and the list of obligors whose sworn declarations are being sent.

(ii) Check, before delivery, if sworn declarations are in order, and find whether they have been submitted with material errors or incomplete, so that the obligors be required to correct them.

(iii) Consider as not presented any sworn declarations that have not been corrected. (iv) File authenticated copies of sworn declarations. (v) Report to CGRP any default cases in the presentation of sworn declarations, including those

considered as not presented (those which have been presented with material errors or incomplete) within no more than seven (7) business days following the occurrence.

(vi) Report to the senior officer of the entity the information indicated in point (v) so that he will notify CGRP the penalties applied to obligors within five (5) days of their application.

(vii) Train the obligors to submit sworn declarations and the mandatory use of the Sole Form. The Senior Officer of each Budget Item shall: (i) Send to the Comptroller General’s Office, at the end of the budgetary year, a list of the

appointments or contracts of those under the obligation to present a sworn declaration, as well as detailed information of all incomes received by public officers or civil servants.

(ii) Publish in the Official Gazette El Peruano11 the sworn declarations submitted by public officers or civil servants who are under said obligation.

V.5 Failure to submit sworn declarations Article 9 of the regulation to Law 27482, as approved by Supreme Decree 080-2001-PCM, establishes penalties for public officers or civil servants who fail to submit their sworn declarations of incomes, property and revenues, depending on the labor regime they belong to. Those included in the Law of Bases of the Administration Career and remunerations to the public sector (Legislative Decree 276) shall be subject to the penalties laid down by such provisions. These include (i) verbal or written reprimand, (ii) suspension without pay for up to thirty (30) days, (iii) temporary dismissal without remuneration up to twelve (12) months, and (iv) dismissal. Those who are not under such regime may not enter into contracts with the State or perform any duties or services with public entities for one year starting from the end of periods set for the presentation of sworn declarations. Such penalties are set by the entities themselves, and shall be notified to the CGRP within seven (7) business days following their occurrence.

11 This is the State of Peru’s official journal that makes public its official information and notices.

8

V.6 Non Compliance and Penalties In addition to the penalties that entities may apply to public officers or civil servants obliged to present the Sworn Declarations of Income, Property and Revenues there are penalties established in the Regulation of Infractions and Penalties of the CGRP, approved by Comptroller General’s Office Resolution 367-2003-CG, which are applicable to Directors of Administration and/or Senior Officers of Budget Items, as the case may be. These penalties correspond to the following cases of non compliance: (i) Failing to send to the CGRP the Sworn Declarations of Income, Property and Revenues, as

well as the information regarding contracts or appointments. (ii) Failing to comply with the notices of the CGRP to correct the non submission of documents or

information as required by the various laws and regulations. (iii) Failing to deliver, present or provide other documentation or information over which there is a

legal obligation to report such documentation or information to the CGRP. In the event of point (i), the described conduct is considered a serious infraction and shall be penalized by a fine amounting from 1.5 to 5 Tax Units (UIT)12; the conducts under items (ii) and (iii) are considered slight infractions and are penalized with a fine of 0.5 to 1 Tax Units. On the other hand, Article 48 of the Infractions and Penalties Regulation states that in case slight infractions are detected, the Evaluation Body may waive the application of the penalty provided the infringer corrects the conduct that led to the infraction no later than five (5) days following the date of the notice that started the Penalizing Procedure. V.7 Audit Law 27785 dated July 23, 2002, Organic Law of the National Audit System and of the GGRP, establishes that it is the duty of the CGRP to audit the Sworn Declarations of Income, Property and Revenues that must be submitted by public officers and civil servants who are obligated according to the law. Such audit consists of a review of the information declared vs. the information obtained, taking into account how timely it has been presented, how reasonable and how consistent it is, in order to finally issue a report with the results of the process. The primordial objectives for the auditing process are, among others: (i) Determine the timeliness, that is, if the audited person presented his sworn declarations in line

with the positions he held during the audited period; and if such was done within the period established by the Law. Also, if the deadlines for delivering the original hardcopies of the Sworn Declarations of Income, Property and Revenues to the CGRP by the General Bureau of Administration, and the period for their publication in the official gazette, El Peruano, have been complied with.

(ii) Determine the reasonability of the contents of sworn declarations; checking each of its items and observing if what the audited person has declared concurs with the information obtained by the Audit Committee, both from the audited person himself and through external sources.

(iii) Determine the consistency or the correspondence between the incomes and the variation of the estate of the audited person. To such end, a comparison is made among the sworn declarations presented by the obligor, and a determination is made of the flow of funds and uses in respect of incomes, real and personal property, placements, other goods and credits (which items must be declared), from which a total of sources, a total of uses, and the difference between both is obtained.

12 The tax unit (UIT) is a reference value that can be utilized in tax rules, among others. At present, its value is [Peruvian soles

3,300 or about US$ 1000]

9

V.8 Illicit Enrichment The audit of Sworn Declarations of Income, Property and Revenues may point out, among other results, the inconsistencies between the incomes received and the variation in the estate of the public officer or civil servant during the period under analysis. If this happens, it may represent a case of Illicit Enrichment. Illicit Enrichment has a constitutional support and is directly related to the presentation of the Sworn Declarations of Income, Property and Revenues. Article 41 of said legal provision sets forth that “public officers and civil servants included in this law or who administer or manage funds of the State or agencies supported by the State must prepare a sworn declaration of properties and incomes when taking offices offices, during the time they exercise them and on leaving office. The pertinent publication is made in the Official Gazette in the form and with the conditions required by the Law. When Illicit Enrichment is presumed, the Government Attorney General, on a report from third parties or ex officio, shall file charges before the Judicial branch”. For its part, Article 401 of the Peruvian Criminal Code, as amended by Law 27482, and Act regulating the publication of Sworn Declarations of Income, Property and Revenues of public officers and civil servants of the State, and Law 28355, regulated Illicit Enrichment within its Chapter XVIII, corresponding to crimes against public administration, which sets forth that: “ Any public officer or civil servant who unlawfully increases his estate with respect to his legitimate incomes during the exercise of his duties and who cannot reasonably justify it shall be punished with loss of liberty of no less than five nor more than ten years and disqualification according to the Criminal Code, Article 36, paragraphs 1 and 2. Illicit Enrichment is suspected when the increase of the estate and/or economic expense of the public officer or civil servant with respect to his Sworn Declaration of Income, Property and Revenues is notoriously higher than what he could normally have had with his remuneration or fees, increases of capital, or incomes from any other lawful source”. VI. SWORN DECLARATIONS AUDIT MANAGEMENT Comptroller General’s Office Resolution 001-2004-CG dated January 2, 2004, approved the new Organic Structure of the CGRP, and created the Sworn Declarations Audit Management, as a Unit under the Central Development Management. Its duties were established under Comptroller General’s Office Resolution 110-2004-CG dated March 27, 2004; it is in charge of receiving, keeping, and selectively audit the truthfulness and/or reasonability of the information contained in the Sworn Declarations of Income, Property and Revenues presented by public officers obliged under the Law. In accordance with Article 53 of the Organizations and Functions Regulation of the Comptroller General’s Office, the Sworn Declarations Audit Management has as its main duties: (i) Examine, register, file and maintain in custody the Sworn Declarations of Income, Property

and Revenues sent to the CGRP. (ii) Monitor if entities are duly sending to the CGRP the information and/or documentation related

to the Sworn Declarations of Income, Property and Revenues, as determined in the pertinent regulations.

(iii) Carry out interinstitutional coordinations in order to obtain the necessary information for the performance of the Management activities.

(iv) Assess and solve inquiries on matters related to its sphere of competence. (v) Maintain updated information on implemented information systems, within its sphere of

competence.

10

VI.1 STRUCTURE AND ORGANIZATION In order to comply with the duties entrusted, the Management has as of October 2005, thirty three13 persons, between professional and technical personnel, organized as follows:

FIGURE 2:

SWORN DECLARATIONS AUDIT MANAGEMENT: ORGANIZATION CHART Note: ( ) Number of personnel at each unit Source: Manual of Procedures, Sworn Declarations Audit Management Prepared by the Sworn Declarations Audit Management VI.2 VERIFICATION UNITS, REGISTRATRION AND FILING OF SWORN DECLARATIONS The general objective of these areas is the verification, registration (digitalization and digitation), administration and filing of the Sworn Declarations of Income, Property and Revenues that are sent to the CGRP by the General Bureaus of Administration of the public entities. To this end, a team of auditors belonging to this unit assesses the sworn declarations in order to identify: (i) possible errors, (ii) remittance of photocopies, (iii) lack of signature of declarant or forms with incomplete information, among others; remarks are notified to the General Directors of Administration for processing the pertinent corrections. Subsequently, the personal data of each officer is verified through an on-line search in the database of the National Vital Statistics and Civil Registry Office (RENIEC), and then the sworn declarations database (PRISMA) is updated with the information contained in the sworn declarations through the digitalization and digitation of its contents. Finally, the sworn declarations are kept in custody classified in alphabetic order in the archives of the Sworn Declarations Audit Management.

13 Personnel as of 30 SEP 2005 as per the Report on the Compliance with the Operational Plan of the Auditing Management for Sworn Declarations, I , II and III quarter 2005.

DIGITATION (2)

SECRETARY (1)

TECHNICAL COORDINATOR(1)

SSDD VERIFICATION (2) REGISTRY & ARCHIVE (6)

ARCHIVE (3) REGISTRY (3)

DIGITALIZATION (1)

MANAGER (1)

AUDITING(20) LEGAL ADVISORY (2)

11

FIGURE 3:

SWORN DECLARATIONS: VERIFICATION, REGISTRATION AND FILING PROCESSS

Source: Verification, Registration and Filing of Sworn Declarations prepared by the Sworn Declarations Audit Management VI.3 LEGAL ADVISORY UNIT The general objective of this area is to attend written or telephonic inquiries concerning the obligation, the filling in process, appointments and contracts, among others; for the presentation of Sworn Declarations of Income, Property and Revenues by the persons who are obliged to do so under the law. It is also a supporting unit to the Sworn Declarations Management for issuing opinions on Law bills and other rules related to the Sworn Declarations of Income, Property and Revenues that are sent to the CGRP by other institutions, making suggestions and proposals to the current regulations. It also prepares and reviews the agreements with various State institutions, in order to facilitate access to the information contained in such institutions. This unit is a part of a plan to enhance a culture of probity and transparency in the public administration, by periodically scheduling training seminars to the Heads of the Institutional Control Bodies and/or General Heads of Administration in the various public institutions on procedures for the

Verification of form in force,

original, signed. Basic data declared.

On-line data verification (National Vital Statistics & Civil Registry Office - RENIEC)

Revision of

dossier, check to see if

completed, assign to audit

personnel

VERIFICATION

Request of corrections / repetitions

RECEPTION AND ASSIGNMENT

REGISTRY

Digitalization of sworn declarations

Digitation of sworn declaration contents

Filing of sworn declarations

ARCHIVO

12

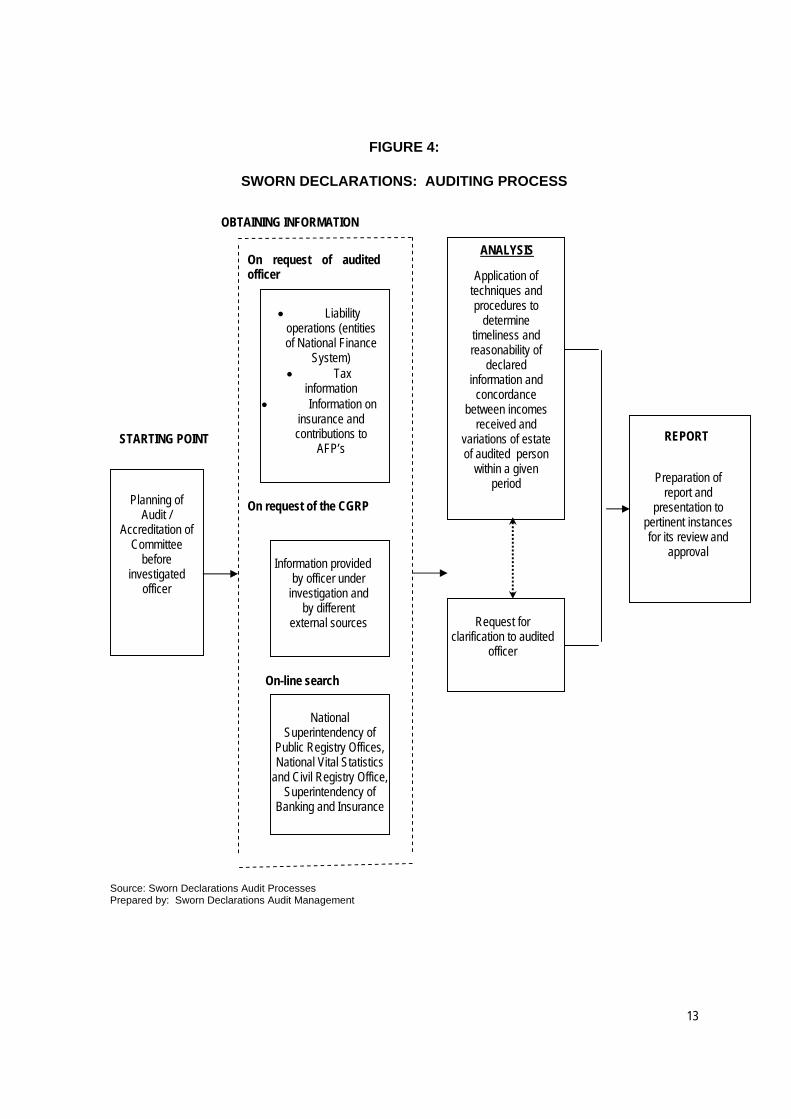

proper filling in and presentation of Sworn Declarations. In this sense, 25014 officers from several institutions were invited to the seminars scheduled at the National School of Control This unit is also responsible for attending applications for access to information on Sworn Declarations, either from citizens or miscellaneous institutions. During the first three quarters of the year 14 applications have been received.15 In addition, this area is in charge of overseeing the compliance of regulations related to Sworn Declarations, through a follow up of the duties of the General Directors of Administration and Senior Officers of Budget Items, and to apply the Regulation on Infractions and Penalties by starting the respective Penalizing Procedures, in case of non compliance. VI.4 AUDITI UNIT OF SWORN DECLARATIONS The objective of this area is to find the timeliness, reasonableness and consistency of the information contained in the Sworn Declarations presented by public officers during a certain analysis period. To such end, this unit made up by various audit committees and through the application of techniques and procedures involving the analysis of information provided from several external sources (both the persons being investigated and the public and private institutions and the Web), concerning incomes, real property, movable property, savings, deposits, placements and investments, other assets and incomes and credits and liabilities, finds if the information given is timely, reasonable and if the variation in the estate of the officer audited is in line with the incomes received during the period being analyzed, the conclusions of which are indicated in the auditing report. We should mention that for a full analysis of the estate variation, it would be necessary to have additional information, specifically as regards current expenses, which the person being audited is not obliged to record or to declare. The officers to be investigated are selected previously according to the selection criteria that involve the following aspects: (i) Alerts of the System: A process whereby a selection is made of the database containing the

information on the Sworn Declarations of Income, Property and Revenues (PRISMA System), taking into account positions with greater risk of occurrence of corruption acts in the State, entities with greater risk of occurrence of corruption, levels of patrimonial increase, among others.

(ii) On request of the obligor himself (iii) Requirements of Audit Committees. As a result of a control action, the managements in line

at CGRP attending the recommendations from the auditing committees may request the audit of an obligor in particular.

(iv) Claims: Formulated by citizens and derived to the Sworn Declarations Audit Management (v) Requirements from other instances or institutions: among which are included requirements

presented by Congress, judicial instances, among others.

14 Source: Auditing Management of Sworn Declarations: Report on the Compliance of the Operational Plan of the Auditing

Management of Sworn Declarations of I, II and III quarter 2005 15 Source: Auditing Management of Sworn Declarations: Report on the Compliance of the Operational Plan of the Auditing

Management of Sworn Declarations of I, II and III quarter 2005

13

FIGURE 4:

SWORN DECLARATIONS: AUDITING PROCESS Source: Sworn Declarations Audit Processes Prepared by: Sworn Declarations Audit Management

• Liability

operations (entities of National Finance

System) • Tax

information • Information on

insurance and contributions to

AFP’s

Application of techniques and procedures to

determine timeliness and reasonability of

declared information and

concordance between incomes

received and variations of estate of audited person

within a given period

Preparation of

report and presentation to

pertinent instances for its review and

approval Information provided

by officer under investigation and

by different external sources

Planning of

Audit / Accreditation of

Committee before

investigated officer

OBTAINING INFORMATION

Request for

clarification to audited officer

On request of audited officer

On request of the CGRP

On-line search

National Superintendency of

Public Registry Offices, National Vital Statistics

and Civil Registry Office, Superintendency of

Banking and Insurance

STARTING POINT REPORT

ANALYSIS

14

VII. LIMITATIONS TO THE PRESENT SYSTEM Within the current system of Sworn Declarations there is a series of limitations that prevent a more efficient labor so that Sworn Declarations may thoroughly comply with the purposes for which it was established. (i) Regulations: One of the most important limitations is the current regulation. At present, the CGRP is not entitled to regulate certain aspects of the law that controls the sworn declarations of Income, Property and Revenues. The regulation in force presents gaps and inaccuracies that thwart an adequate application of the stipulations. Specifically, the timing it prescribes for the presentation of the Sworn Declarations of Income, Property and Revenues generates a large number of sworn declarations with minimum variations in their items, due to the rotation of officers in several positions and/or entities along brief periods of time, within the same budgetary year. Also, the time limits specified for remittance to the CGRP are relatively short, taking into consideration that the obligor does not present his sworn declaration directly to the CGRP. Moreover, in the list of those who are under the obligation to declare there are some officers who despite having a primordial position in the institution, are not expressly obligated. This distorts the public officers segment for whom this tool was defined. Likewise, the present sole form of sworn declarations of Income, Property and Revenues is rather general, and does not allow for an accurate presentation of incomes, assets and liabilities in sufficient detail, creating doubts for the obligors. As to the audit work itself, the current Peruvian legislation is not adequate to prevent and detect illicit enrichment, among other reasons, because of all the processes involved in the lifting of banking secrecy and the tax confidentiality of the persons under investigation. Also, audits are too lengthy due to the lack of definition in maximum periods and/or penalties for the investigated officers, when they are asked for clarifications and answers. (ii) Tools: Another limitation found is the tools used for verification, registration and auditing. At present, these are insufficient to face the growing requirements of society due to the large quantity of Sworn Declarations of Income, Property and Revenues that are permanently received, because of the terms established for their presentation. To date, there are one hundred thousand (106,000) [sic] sworn declarations verified and filed in the vault of the Sworn Declarations Audit Management, and as can be seen in Figure 2, this Management has 2 auditors engaged in verification and 20 engaged in auditing. Also, as regards the audit of sworn declarations, such as mentioned above, a substantial portion of the procedures involve the search and request of information from external sources. Nonetheless, the CGRP has no legal power to demand private institutions or even the person who is being audited, that information be submitted with celerity. This, in practice, results in prolonged audits. Within this context, it is absolutely necessary to consider connections with external database in order to cross and compare on-line information and speed up the processes. VIII. PROPOSALS FOR A CHANGE The legal base requires urgent modifications in view of the limitations mentioned in the preceding paragraph Additional information should be included in the sworn declarations forms that will foresee these situations of conflicts of interest with positions held previously or currently, both by the declarant and his family constellation, among others. It is also necessary to provide a greater detail of the incomes, assets and liabilities of the declarant, his/her spouse and depending children (provenance, valuation criteria) that will facilitate their later analysis for the detection of substantial variations in the declarant’s estate.

15

In this sense, the CGRP has proposed regulations to the Executive Branch and the Legislative Branch (Congress of the Republic) seeking to obtain a proper framework for a better auditing performance. Some of these are: (i) Power to modify the contents of sworn declarations, for example: (i) include the estate of

depending children and concubine, (ii) specify the method to value each of the items to be declared, (iii) include the participations of the declarant, spouse (concubine) and dependant children in corporations, associations, foundations, etc.

(ii) Authorize the CGRP to lift the banking secret, tax confidentiality and identity discretion. (iii) Determine the infractions and penalties in connection with the presentation of sworn

declarations. (iv) Obligation to submit the sworn declarations to the CGRP directly. We are also seeking to establish interinstitutional coordinations through formal channels for transmitting information among databases, considering the scope of the sources consulted: the National Vital Statistics and Civil Registry Office (RENIEC), National Superintendency of Public Registry Offices (SUNARP), National Superintendency of Tax Administration (SUNAT), Superintendency of Banking and Insurance (SBS), Peruvian Social Security Health Insurance Institute (EsSalud), Lima Association of Notaries Public, National Institute for the Defense of Free Competition and Intellectual Property (INDECOPI), Government Attorney General’s Office, the Judiciary, Peruvian National Police (PNP), Peruvian Securities and Exchange Commission (CONASEV), General Immigration Service (DIGEMIN), Financial Intelligence Unit (UIF), among others. We have at present interinstitutional cooperation agreements with entities both in the public and the private sector, such as RENIEC, Banking Association - ASBANC, UIF, the Judiciary, the Government Attorney General’s Office and the SBS, among others. The implementations having as a goal the auditing done in a shorter time and with sufficiently effective procedures and indicators are detailed as follows: (i) PRISMA EXTERNO System This system seeks to re-design the processes and the automation of the recording and filing activities. It seeks to minimize the times and errors when entering information. The system proposes that in each entity, persons under the obligation to file their declaration enter their information while being connected to the intranet of each institution, so users responsible for the system (General Bureau of Administration) may subsequently consolidate and send through the web the sworn declarations and the printed forms previously signed. This information would be directly fed to the Management database, after it has been found that he information received through the web is consistent with the data contained in the physical forms. As of October 2005, the system is in its pilot testing stage with several institutions and it is expected to be operational in the second semester next year. (ii) Work Flow Laser Fiche The Work Flow Laser Fiche system will be shortly implemented at the Sworn Declarations Audit Management, specifically in the auditing area. This tool will seek to systematize the information flow through:

Digitalization of all documents in the audit process

Electronic “Movements” among involved persons

Generation of alerts or notices through the mail

On line procedures (approval, allocation of dossiers, conclusion, among others)

16

Automated procedure (definition of indicators, analysis and follow-up) This technology will allow a better understanding of the internal processes in auditing, on the basis of their prior standardization. The control and monitoring processes so facilitated will allow measuring the actual progress of audits, while ensuing a reduction of document processing, time and costs. (iii) Data Mining The Data Mining system seeks to extract useful information, a base for later cross information with other systems utilized by the CGRP: Governmental Auditing System (SAGU), the CGRP Integrated System (SICGRP), the Sworn Declarations System (PRISMA), among others, in order to find, for example, which officers are not complying with current legal provisions, e.g. those who could eventually be liable to pending criminal processes with the State, which would bar them from holding any public office. This system may answer questions that traditionally consume too long a time to be solved as they have to dig into databases searching for hidden or latent patters, finding predictable information that an expert would not reach because it lies beyond his expectations. IX. CONCLUSIONS Ensure that public officers will not use their jobs for their own benefit of for that of third parties is one of the main goals of the sworn declarations system. Laws and regulations are necessary conditions but not sufficient for an upright performance of public duties. We have at present a number of legal provisions concerning the time for presentation and the contents, be it on taking office, during its exercise and on leaving. However, the present mechanisms need to be complemented so that sworn declarations will be a more efficient instrument to prevent corruption, specifically in order to detect possible cases of conflicts of interest. Although the formal presentation of sworn declarations on the whole is not fully satisfactory because of non-complying officers and to repeated errors that are still being identified in the sworn declarations presented, we have anecdotic experiences that have allowed correcting wrong presentations as a result of the training programs promoted by the Sworn Declarations Audit Management that seek to make known the instructions for completing the Sworn Declarations of Income, Property and Revenues, and complying with their publication, as well as the immediate response to the said Management’s requirements. The document itself, in spite of being a signed declaration, is insufficient to guarantee the transparency and truthfulness of the information included. There is not a developed culture where what is declared is the truth. That is why verifications are required with external sources (particularly, on-line databases) in order to detect irregularities in the public officers’ estate declaration. As has been mentioned in the proposed changes, the information systems will allow detecting alerts in cases of substantial increases in the declared items. They will also reduce preparation, submission, verification and registration times with substantial savings in the pertinent costs. Being conscious of the scope of this endeavor, the CGRP will continue to encourage the changing processes by proposing modifications to regulations, the use of state-of-the-art technology, interinstitutional cooperation, promotion of a culture of transparency and probity in public administration, so that the Sworn Declarations of Income, Property and Revenues will be an efficient tool both for detecting and preventing corruption acts.

17

X. LIST OF ACRONYMS

CGRP Comptroller General’s Office of the Republic of Peru CONASEV Peruvian Securities and Exchange Commission CONATA National Council for Property Valuation DIGEMIN General Immigration Service INDECOPI National Institute for the Defense of Free Competition and

Intellectual Property PCM Presidency of the Council of Ministers PNP Peruvian National Police PRISMA Internal System for Auditing Sworn Declarations RENIEC National Vital Statistics and Civil Registry Office SAGU Government Auditing System SAT Tax Administration Service SBS Superintendency of Banking and Insurance SICGR Integrated System of the Comptroller General’s Office of the

Republic SUNARP National Superintendency of Public Registry Offices SUNAT National Superintendency of Tax Administration UIF Financial Intelligence Unit

XI. BIBLIOGRAPHY

Office of the Ombudsman. Access to public information. Thumbs down to a culture of secrecy . Lima, Peru. October 2001.

National Anticorruption Initiative. Peru without corruption. Conditions, guidelines and recommendations for the fight against corruption. Lima, Peru. 2001. This report is in the website of the Ministry of Justice. www.minjus.gob.pe

Probidad Magazine, number 016, special edition: Corruption in Peru, October-November 2001.

Peru: An alliance for educating, informing and watching - Jorge Valladares Molleda; Asociación Civil TRANSPARENCIA. Lima – Peru.

I National Conference on ANTICORRUPTION, Lima, July 2001. Pro ethics – National Consortium for Public Ethics

Klitgaard, Robert, MacLean – Abaroa, Lindsey Parris, “Corruption in cities. A practical guide for curing and preventing” May 2001.

Multiannual Sectorial Strategic Plan 2002-2006 of the CGRP

“Public Corruption in Latin America: Manifestations and Control Mechanisms”, website: lapaz.usembassy.gov/Corruption/corrupción.pdf.

La Fiducia, website: www.fiducafe.com.co/htm/body_negocios_fiduciarios.htm.

18

XII. EXHIBITS

EXHIBIT 1: SWORN DECLARATIONS AUDIT MANAGEMENT: STATISTICS CHART 1:

SWORN DECLARATIONS AUDIT MANAGEMENT: SWORN DECLARATIONS RECEIVED

Under evaluation Non obliged entities W/ objections No

objections

714 762 20,265 21,741

Year 2004 168 279 1,636 19,061 21,144

Year 2005 ** 5,475 1,989 20,261 28,418

Period

State of SSDD

Total SSDD

693

Liability *

Notes: (*) Liabilities: SSDD received between January 2001 and December 2003 (**) Year 2005: Period from January 2005 to September 2005 State of SSDD: Under evaluation: SSDD in process Non obliged entities: Budget does not exceed 2000 Tax Units (UIT) With Objections: SSDS that do not comply with regulation

CHART 2:

SWORN DECLARATIONS AUDIT MANAGEMENT - SWORN DECLARATIONS WITH OBJECTIONS

Material Error Photocopied Not signed Second Section

Abolished Form Other

38 250 54 33 125 262 762

Year 2004 292 297 147 41 798 61 1,636

Year 2005 ** 564 186 10 13 1216 2 1,989Total 894 733 211 87 2139 325 4387

% 20% 17% 5% 2% 49% 7% 100%

Period Total SSDD with

observaton

Type of Observation

Liability *

Notas: (* )Liabilities: SSDD received between January 2001 and December 2003 (**)Year 2005: Period from January 2005 to September 2005 Type of Observation of SSDD: Material Error: SSDD have mistaken data or amounts are wrongly added. Photocopied: SSDD submitted as photocopies (not originals). Not signed: SSDD forms were not signed by declarant. Second section: Form to be published in the official gazette “El Peruano”. Abolished form: SSDS forms correspond to regulations no longer in force.

1

EXHIBIT 2: SWORN DECLARATIONS AUDIT MANAGEMENT: PROCESSES FIGURE 5:

GENERAL BUREAU OF ADMINISTRATION

COPIES OF SWORN DECLARATIONS

PUBLIC OFFICER OBLIGED TO DECLARE

SWORN DECLARATION

SWORN DECLARATION

BASIC CONDITIONS: - ORIGINAL DOC. -SIGNATURE -FORM IN FORCE -DECLARED AMOUNTS

VERFICATION OF PERSONAL DATA: BASED ON THE NATIONAL VITAL STATISTICS AND CIVIL REGISTRY OFFICE

REQUEST FOR CORRECTIONS / REITERATIONS

SWORN DECLARATION

DIGITALIZATION LASERFISCHE

PRISMA SYSTEM DIGITATION

ALPHABETICAL FILING OF SWORN DECLARATIONS

VERIFICATION REGISTRY AND ARCHIVE

CROSS OF INFORMATION AND ANALYSIS

COPIAS - DECLARACIONES JURADAS

AUDIT REPORT

EXTERNAL SOURCE INFORMATION

REQUEST FOR INFORMATION AND CLARIFICATION TO AUDITED OFFICER

AUDIT COMMITTEE

STATE ENTITY AUDIT MANAGEMENT OF SWORN DECLARATIONS JURADAS- CGRP

-------------------------- TM-JC/PE 183031K5.3