full slides 2016: the current & future state of independent contractor compliance & usage

TRANSCRIPT

DENIS S. KENNY ATTORNEY, SCHERER SMITH & KENNY LLP

2016: THE CURRENT & FUTURE STATE OF INDEPENDENT

CONTRACTOR COMPLIANCE & USAGE

AGENDA • Effects and implications of U.S. Department of

Labor Administrator’s Interpretation No. 2015-1 • Misconceptions that lead to misclassifications: “on

demand companies” in the “sharing” or “gig” economy

• Consequences and ways to reduce risks of misclassification

• Prognostication for 2016 and beyond. . .

EVOLVING & DIVERSE LEGAL STANDARDS No Single Federal or California Test Federal Tests

Federal Common Law Test NLRA IRS Test FICA/FUTA, IRCA Economic Realities Test FLSA/ADEA/Title VII/ADA Hybrid Test Title VII EEOC Test Title VII, ADA, ADEA California Tests

California Borello Test CA FEHA, CA Family Rights Act, CA Labor Code, CA Workers Comp Act, Agricultural Labor Relations Act

California Common Law Test California UI, SDI, FTDI, Payroll Tax

Employment Development Department (EDD) Test California UI, SDI, FTDI, Payroll Tax

Tests in Other States

IRS Test 24 states and District of Columbia ABC Rule 19 states

NEW WAGE & HOUR ADMINISTRATOR’S INTERPRETATION

• On July 15, 2015, United States Department of Labor, Wage and Hour Administrator issued Administrator’s Interpretation No. 2015-1 (“Interpretation”).

• Interpretation’s message is clear: most workers are employees under FLSA, not independent contractors.

INTERPRETATION (cont’d) • Test for Employee/Independent Contractor still

the same: o (a) FLSA defines “employ” broadly to include “to suffer or

permit to work”* o (b) Multi-factor “economic realities” test *Note: “to suffer or permit” encompasses workers that might be beyond common law control of employer

INTERPRETATION (cont’d) • Six-Factor economics realities test: This test looks to whether

worker is economically dependent on or independent of the hiring company (the “Company”). Factors: o Extent to which work performed is an integral part of the Company’s

business; o Worker’s opportunity for profit or loss depending on worker’s

managerial skill; o Extent of the relative investments of the Company and worker; o Whether the work performed requires special skills and initiative; o Permanency of the relationship; and o Degree of control exercised or retained by the Company.

• Courts looks to economic reality rather than technical concepts.

EXAMPLE – INTERNET & CABLE INSTALLERS Scantland v. Jeffry Knight, Inc., 721 F.3d 1308 (11th Cir. 2013)

• Claim: FLSA overtime claim by current and former internet and cable

installers alleging they were misclassified as ICs.

• Trial and Appellate courts applied the same economic reality test with differing results. o Trial court found installers were ICs, finding that the relationship is a

typical outsourcing arrangement. (Scantland v. Jeffry Knight, Inc. (M.D. Fla. March 29, 2012) 2012 WL 1080361.)

o Appellate Court held 4 factors weighed strongly in favor of employee status and 2 factors weighed only very slightly in favor of IC status; thus, finding IC misclassification.

SCANTLAND (cont’d) APPELATE COURT ANALYSIS

“[P]oints strongly toward employee status” Facts Control Installers were required to report arrival and departure from assigned jobs, received

constant site checks, could not decline jobs without threat of termination, and were subject to uncontestable fines.

Opportunity for Profit or Loss Company determined rates the installers were paid. Permanency and Duration One-year terms, automatically renewed, and terminable with 30-day notice. Integral Part of Company’s Business Company was in the installation and repair service business, and the installers provided

that service. “Weakly” Favors IC Status Facts Investment in Equipment or Materials Installers required to have vehicles, auto insurance, tools and safety equipment, and

commercial general liability insurance, but most installers already had own vehicles and purchased specialty tools directly from the Company via “payroll” deductions.

Special Skills Installers were skilled workers, but Company provided those skills via unpaid trainings and unpaid ride-alongs.

MISCONCEPTIONS • “The worker wants to be an independent contractor.” • “The worker created a LLC or S-Corp to do business

with us.” • “We have a written contract.” • “The worker only performs occasional services for us.” Reality: Classification is a legal determination that parties cannot displace by a written contract. “Form over substance” will not be allowed.

WHY IS THIS TOPIC IMPORTANT RIGHT NOW? Shifting Focus • Historically misclassification has not been a huge area of focus • Recession resulting in more businesses using ICs • Tax deficit at state and federal level • Estimated tax loss due to underreporting of employment taxes is $54B with an estimated over

$2.7B due to misclassification (Treasury Inspector General 2013 Report). RESULT: Focus on misclassification and enforcement • Increased legislation at federal and state level

• In California in 2011, SB 459 “deputized” state EDD, WCAB, UIAB, etc. (Labor Code §§ 226.8, 2753 regarding sliding scale of penalties for “willful” misclassifications).

• Inter-agency (state and federal) cooperation is growing. • Upsurge of audits

• Each budget since 2011 submitted to Congress has included $10M for DOL to distribute to state agencies and almost $4M for DOL enforcement.

• For FY 2016, one of DOL’s Wage and Hour Division’s “Key Enforcement Initiatives” will be “Addressing the Fissured Workplace,” i.e., IC relationships and other business models.

LESSONS FROM THE UBER & LYFT CLASS ACTIONS

Nature of Claims • Class of thousands of drivers from both ridesharing

start-ups claim they should have been classified as W-2 employees rather than 1099 independent contractors (“ICs”) and, in turn, claim they are owed overtime, vacation/sick leave, healthcare insurance and other employee-related rights and benefits (including workers’ compensation insurance).

THE UBER & LYFT CLASS ACTIONS: THE FACTS & ANALYSIS

“On Demand” companies in the “Sharing Economy” • Both Uber and Lyft allow drivers to make themselves available for work whenever they want and allow

them to accept or reject rides once they have been selected – both factors that favor IC status. • On the other hand, both companies expressly reserve the right to terminate the drivers’ relationship or to

terminate their use of the company app if a driver’s customer ratings are deemed unacceptably low or for any reason at all. Both courts noted that this factor is a key one favoring employee status.

• U.S. District Judge Edward Chen, who heard the Uber suit, voiced skepticism about the firm’s claims that it wasn’t an employer, but rather a technology company that licenses its app to drivers given that Uber sets fares and screens and fires drivers.

• U.S. District Judge Vince Chhabria, who heard the Lyft case, said that the current employment test for classifying workers is “woefully outdated” when applied to app-enabled firms such as Lyft; consequently, misclassification “will often be for juries to decide.”

LYFT LITIGATION

• On January 26, 2016, Lyft and its drivers reached a preliminary settlement, subject to Court approval: $12.25M settlement for estimated reimbursement claims, among nonmonetary components, but the preliminary settlement did not address the classification issue.

• On April 7, 2016, Judge Chhabria rejected the preliminary settlement because the monetary settlement short-changed the drivers.

• “[N]othing in this agreement would prevent the California Legislature (or Congress) from offering a legislative solution to the problem of how to classify workers in the ‘gig economy.’”

UBER LITIGATION

• Settlement imminent in California litigation! • As of April 21, 2016, subject to Judge Chen’s approval, the settlement provides

that Uber will pay $84M to the plaintiffs PLUS $16M if Uber goes public and valuation increases 1.5x of Dec. 2015 valuation within 1st year of IPO, and drivers remain ICs, not employees, among other provisions.

• Repeat: Drivers remain independent contractors. • Comment: This proposed settlement is not binding on pending lawsuits in states

like Arizona, Florida, and Pennsylvania, but could signal a win for the “gig economy.”

CONSEQUENCES OF MISCLASSIFICATION Everyone is a potential adversary if you misclassify a worker as an independent contractor. • Government agencies • Plaintiff lawyers • Customers • Unions • Workers’ compensation carrier • Contractors themselves • New! National Labor Relations Board (“NLRB”)

• On April 18, 2016, Los Angeles office issued an unfair labor practice complaint against Intermodal Bridge Transport, alleging NLRA violations for misclassification.

CONSEQUENCES OF MISCLASSIFICATION What Triggers an Audit Unemployment, Worker’s Comp, Discrimination/Harassment/Retaliation claims • A W-2 and 1099 issued for the same worker by the same company in the same

year

• Unmatched 1099 to individual income tax reporting

• “Disgruntled Worker” can anonymously request a misclassification review (IRS Form SS-8)

• Class action lawsuits

• IRS “Whistleblower” Awards Program: Tax Relief and Health Care Act of 2006, 26 USC Section 7623(b)

POSSIBLE PENALTIES & COLLATERAL DAMAGES Overview of Possible Penalties and Collateral Damages • Total of Unpaid Taxes • Penalties • Fines • Punitive Damages • Compensatory Damages • Liquidated Damages • Equitable Relief • Back-Pay • Reinstatement • Expenses including attorneys’ fees and costs (even a “win” will be costly!)

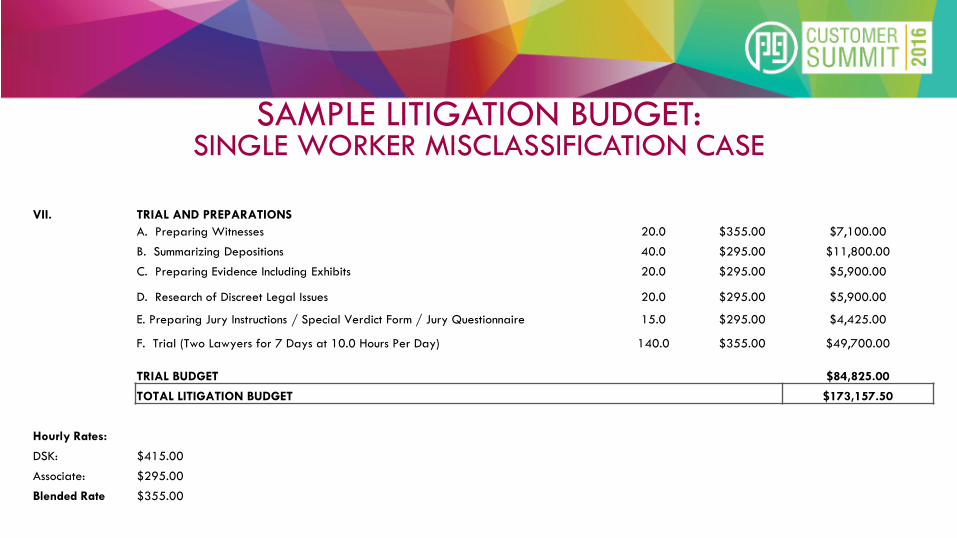

SAMPLE LITIGATION BUDGET: SINGLE WORKER MISCLASSIFICATION CASE

PRETRIAL TASKS: Hours Rate Total I. PLEADINGS

A. Answer to Complaint 1.5 $355.00 $532.50 II. PRE-TRIAL DISCOVERY

A. Draft and Respond to Written Discovery 45.0 $295.00 $13,275.00

10.0 $415.00 $4,150.00 B. Depositions > Plaintiff 15.0 $355.00 $5,325.00 > Plaintiff Co-Worker(s) 15.0 $355.00 $5,325.00 > Defend Owner 15.0 $355.00 $5,325.00 > Defend "Supervisor" 15.0 $355.00 $5,325.00 C. Other Analysis of Discovery and Summary 15.0 $355.00 $5,325.00

III. DISPOSITIVE MOTIONS A. Possible Motion for Summary Judgment / Summary Adjudication 50.0 $295.00 $14,750.00

10.0 $415.00 $4,150.00 IV. EXPERT FEES TBD V. MEDIATION

A. Including Brief, Preparation, and Mediation 30.0 $355.00 $10,650.00 VI. MISCELLANEOUS

A. Attend Status Conferences; Status Calls and Letters; Telephone Calls; Review and Analysis of Case-related Documents/Correspondence.

40.0 $355.00 $14,200.00

PRE-TRIAL BUDGET $88,332.50

SAMPLE LITIGATION BUDGET: SINGLE WORKER MISCLASSIFICATION CASE

VII. TRIAL AND PREPARATIONS A. Preparing Witnesses 20.0 $355.00 $7,100.00

B. Summarizing Depositions 40.0 $295.00 $11,800.00

C. Preparing Evidence Including Exhibits 20.0 $295.00 $5,900.00

D. Research of Discreet Legal Issues 20.0 $295.00 $5,900.00

E. Preparing Jury Instructions / Special Verdict Form / Jury Questionnaire 15.0 $295.00 $4,425.00

F. Trial (Two Lawyers for 7 Days at 10.0 Hours Per Day) 140.0 $355.00 $49,700.00

TRIAL BUDGET $84,825.00

TOTAL LITIGATION BUDGET $173,157.50

Hourly Rates:

DSK: $415.00

Associate: $295.00

Blended Rate $355.00

MITIGATING YOUR RISKS

Basic Steps for Engaging Independent Contractors • Review your IC agreements

• Refine your benefit plans

• Use specific “exclusion” clauses

• Educate your company as to methods of correct

classification

THE PRICE TO PAY FOR “VICTORY” Suing the U.S. Dep’t of Labor – Gate Guard Services, L.P. v. Perez, 792 F.3d 554 (5th Cir. 2015). • Facts: Company contracts with oil companies to provide gate attendants for remote drilling sites

and classified these gate attendants as ICs. DOL was obstructionist and unprofessional in how it investigated this matter and litigated this case.

• Lawsuit: Company sued DOL seeking declaration that it is complying with FLSA in classifying its gate guards as ICs. DOL filed a counter-action for misclassification-related back wages and injunctive relief.

• District Court concluded that government’s position that gate attendants are employees (not ICs) was “not substantially justified,” finding for employer and awarding over $565K in attorney’s fees.

• Appellate Court awarded heightened fees because DOL’s conduct and ignorance of controlling precedent demonstrated DOL “acted in bad faith, vexatiously, wantonly, or for oppressive reasons”; DOL settled for $1.5M.

MITIGATING YOUR RISKS How to Evaluate: Proving conduct is not “willful”

• Create a consistent, centralized process for evaluating IC status o Evaluate everyone o Use consistent standards o Develop questionnaires for both managers and workers to complete o Document your analysis of why the work and the worker are

suitable for IC classification • Consult with experienced labor and employment counsel

PROGNOSTICATION: WHAT MIGHT THE FUTURE HOLD

The California 1099 Self-Organizing Act (AB 1727) • California State Assemblywoman Lorena Gonzalez (D-San Diego) has authored AB

1727, which allows ICs who provide services through hosting platform(s) to have certain rights enjoyed by employees.

• Examples: right to organize, negotiate with hosting platforms, or engage in activities for group negotiations or other mutual aid or protections.

• Status: On April 20, 2016, AB 1727 has been referred to the Assembly Judiciary Committee.

PROGNOSTICATION: WHAT MIGHT THE FUTURE HOLD

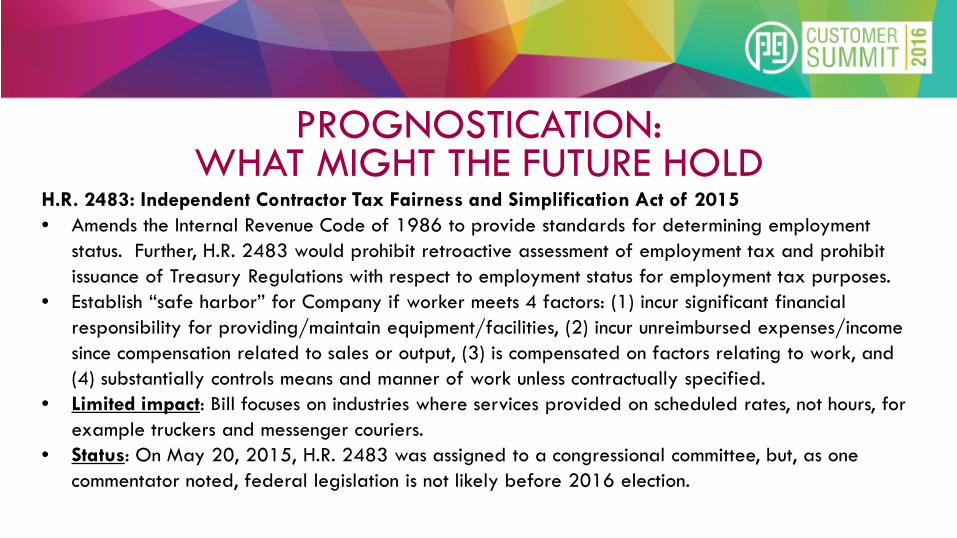

H.R. 2483: Independent Contractor Tax Fairness and Simplification Act of 2015 • Amends the Internal Revenue Code of 1986 to provide standards for determining employment

status. Further, H.R. 2483 would prohibit retroactive assessment of employment tax and prohibit issuance of Treasury Regulations with respect to employment status for employment tax purposes.

• Establish “safe harbor” for Company if worker meets 4 factors: (1) incur significant financial responsibility for providing/maintain equipment/facilities, (2) incur unreimbursed expenses/income since compensation related to sales or output, (3) is compensated on factors relating to work, and (4) substantially controls means and manner of work unless contractually specified.

• Limited impact: Bill focuses on industries where services provided on scheduled rates, not hours, for example truckers and messenger couriers.

• Status: On May 20, 2015, H.R. 2483 was assigned to a congressional committee, but, as one commentator noted, federal legislation is not likely before 2016 election.

QUESTIONS?

Please feel free to email or call me with any follow-up questions or comments

about this presentation.

Thank you, Denis Sullivan Kenny

(415) 433-1099 140 Geary Street, 7th Flr., San Francisco, CA 94108