fstep%20islamic_treasury_operation

TRANSCRIPT

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 1/89

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 2/89

1. Overview

2. Objectives of Treasury

3. Development of Malaysia Financial Markets

4. Islamic Money Market

5. Islamic Financial Instruments6. Islamic Derivatives Instruments

7. Islamic Foreign Currency

8. FOREX Trading

9. FOREX Transactions in Islamic Banking Operations

CONTENTS

Table of Contents

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 3/89

1Overview

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 4/89

• Islamic Treasury involves activities that are carriedout in ways that do not conflict with the conscience

of Muslims and the religion of Islam.• It represents an assertion on religious law that

prohibits the following transactions:

• Usury (riba)• Gambling (maisir)

• Ambiguity (gharar)

Overview

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 5/89

2

Objectives of Treasury

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 6/89

Objectives of Treasury

• Ensure liquidity is available to meet all current andfuture obligations,

• Maximize return on investment portfolio managed,• Ensure bank is funded in the most appropriate and

cost efficient manner,

• Identify and mitigate financial risk that could erodebank’s financial standing.

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 7/89

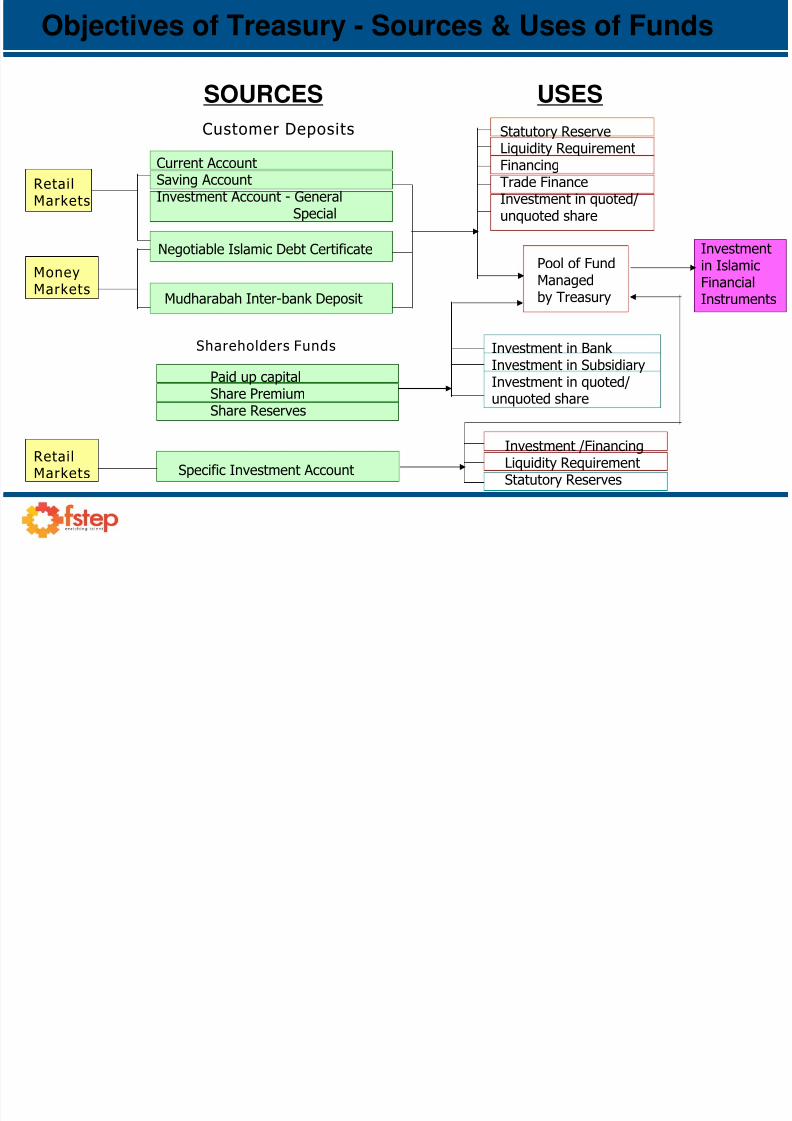

• Primarily responsible to manage a pool of bank’sexcess fund. This fund comprises of:

• Customers Deposits (CD),• Inter-bank Deposits (ID),

• Shareholders Fund (SHF) and

any other sources approved by the bank . . .

• after being utilized on statutory requirements,financing and investment.

Objectives of Treasury - Sources & Uses of Funds

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 8/89

Negotiable Islamic Debt Certificate

Mudharabah Inter-bank Deposit

Specific Investment Account

Investment /FinancingLiquidity Requirement

Statutory Reserves

Pool of Fund

Managedby Treasury

RetailMarkets

Money

Markets

Customer Deposits

Current AccountSaving Account

Investment Account - GeneralSpecial

Paid up capitalShare PremiumShare Reserves

Investment in Bank Investment in Subsidiary

Investment in quoted/unquoted share

SOURCES USES

Investmentin Islamic

FinancialInstruments

Retail

Markets

Objectives of Treasury - Sources & Uses of Funds

Shareholders Funds

Statutory ReserveLiquidity RequirementFinancingTrade FinanceInvestment in quoted/unquoted share

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 9/89

3

Development of MalaysianFinancial Markets

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 10/89

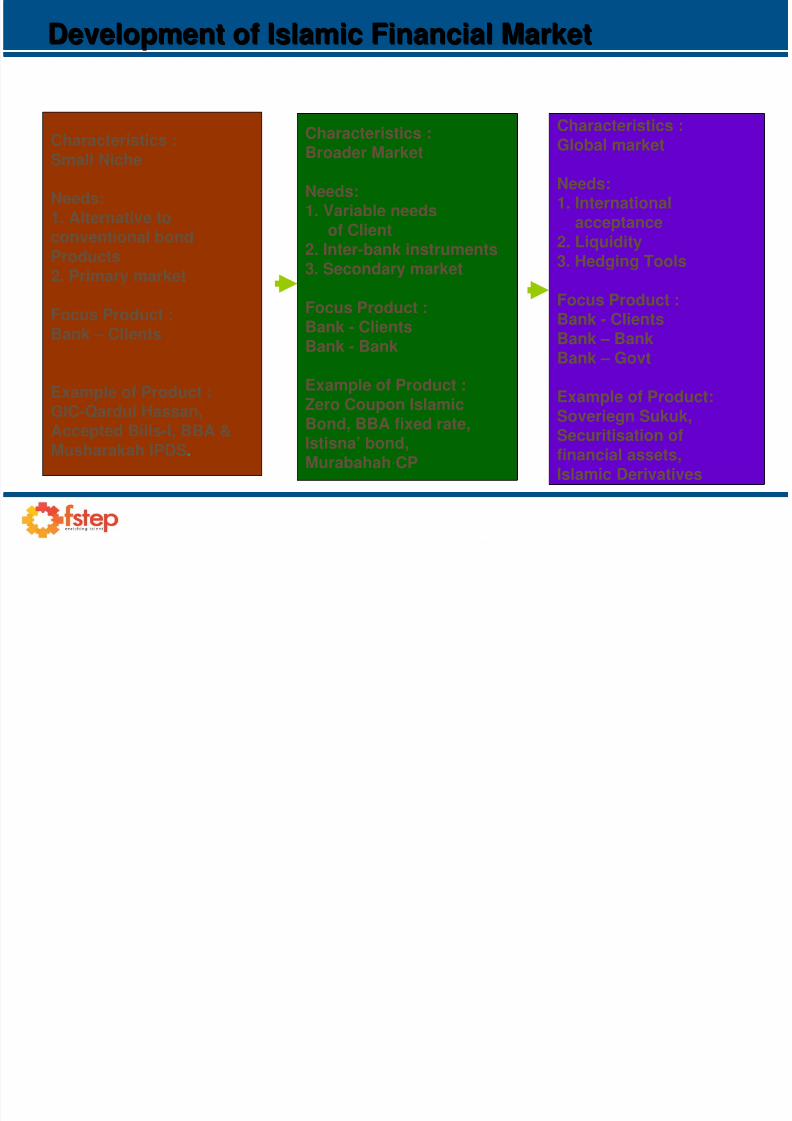

Development of Islamic Financial MarketDevelopment of Islamic Financial Market

Characteristics :Small Niche

Needs:1. Alternative toconventional bondProducts2. Primary market

Focus Product :Bank – Clients

Example of Product :GIC-Qardul Hassan,Accepted Bills-I, BBA &Musharakah IPDS.

Characteristics :Broader Market

Needs:1. Variable needs

of Client2. Inter-bank instruments3. Secondary market

Focus Product :Bank - ClientsBank - Bank

Example of Product :Zero Coupon IslamicBond, BBA fixed rate,Istisna’ bond,Murabahah CP

Characteristics :Global market

Needs:1. International

acceptance2. Liquidity3. Hedging Tools

Focus Product :Bank - ClientsBank – BankBank – Govt

Example of Product:Soveriegn Sukuk,Securitisation offinancial assets,

Islamic Derivatives

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 11/89

Early Stage (1983-1992)

Small Niche

After 11 years (1992-2000)Broader Market

After 18 years (2000 and beyond)Global Market

Development of Islamic Financial MarketDevelopment of Islamic Financial Market

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 12/89

Development of Islamic Financial MarketDevelopment of Islamic Financial Market

Early Stage (1983-1992)Small niche

• Malaysian Government issuance of GIC

• Bank Islam issued Accepted Bills - Islamic• Shell Malaysia issued BBA Fixed rate bond• Sarawak Shell issued Musharakah bond

• Primary markets only

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 13/89

Development of Islamic Financial MarketDevelopment of Islamic Financial Market

• Islamic Money Market in Malaysia

• Petronas issued Zero Coupon bond• Cagamas issued Sanadat Mudharabah bond• KLIA issued 2.2 billion BBA Fixed Rate bond

• Moccis issued Murabahah Islamic Commercial Paper

• Khazanah issued Benchmark bond

After 11 years (1992-2000)Broader Markets

• Evolution of Secondary market

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 14/89

Development of Islamic Financial MarketDevelopment of Islamic Financial Market

• Guthrie issued USD150 milion Sukuk Al Ijarah• Malaysian Govt issued USD500 million Sukuk

• Issuance of IPDS by Supranational Institutions• Bank Islam introduced FX Forward & Swap• Introduction of Commodity Murabahah Products

• Standard Chartered introduced Islamic Profit RateSwap, Cross Currency Swap & Forward

After 18 years (2000 and beyond)Global Markets

Global Recognition of Islamic Financial Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 15/89

4 Islamic Money Market

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 16/89

• Introduced by BNM in January 3, 1994

• Defined as:• Activities guided by Syariah principle

• Wholesale transactions

• Liquid and low risk instruments

• Less than 1 year

• Market players are Islamic banks and commercial andinvestment banks with Islamic window.

• The activities include:• Inter-bank Mudharabah

• BNM Wadiah Tender

• Trading of Islamic Financial Instrument

Islamic Money MarketIslamic Money Market

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 17/89

• Inter-bank Mudharabah (IBM)• A system where a Islamic bank obtains investment from

another Islamic bank on the basis of Mudharabah to

source, invest and square their short term fund.• Mudharabah is a joint venture between two parties i.e one

party with fund and the other party who is the entrepreneur.

• Both parties will then negotiate and agree on the amount,tenor of investment and profit sharing ratio. Any loss mustbe borne by the investor.

• IBM is an alternative to the conventional money market,

the activities are based on profit sharing principle; asopposed to interest on borrowing / lending activities in theconventional money market.

Islamic Money MarketIslamic Money Market

I l i M M kI l i M M k t

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 18/89

• The period of investment ranges from over night to 12months.

• The minimum amount of investment is RM50,000.00

• The rate of return shall be based on the gross profitbefore distribution for investment of 1 year of thereceiving bank .

• The profit of IBM is calculated based on the followingformula :

Profit = prt(k)

36500where :p = Principal investmentr = Gross Profit Rate of the Receiving FIt = Number of Day Invested

k = Profit Sharing Ratio of the Investing FI

Islamic Money MarketIslamic Money Market

I l i M M k tI l i M M k t

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 19/89

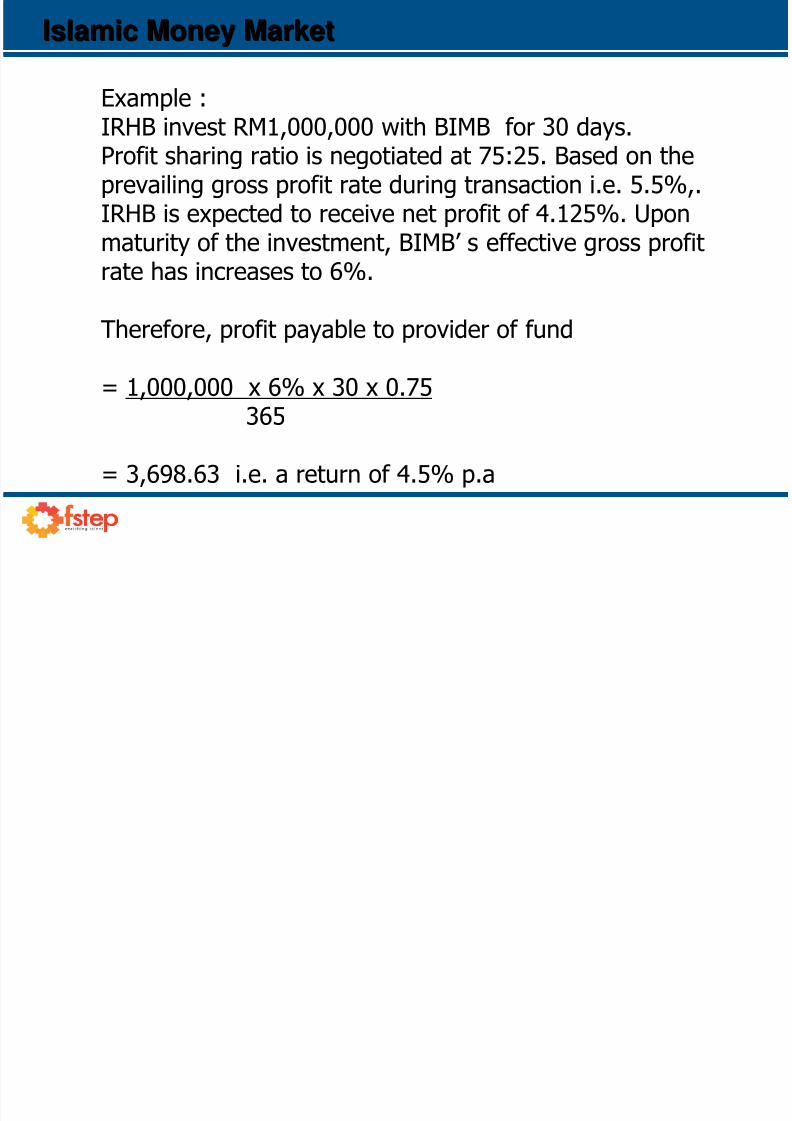

Example :IRHB invest RM1,000,000 with BIMB for 30 days.Profit sharing ratio is negotiated at 75:25. Based on the

prevailing gross profit rate during transaction i.e. 5.5%,.IRHB is expected to receive net profit of 4.125%. Uponmaturity of the investment, BIMB’ s effective gross profitrate has increases to 6%.

Therefore, profit payable to provider of fund

= 1,000,000 x 6% x 30 x 0.75365

= 3,698.63 i.e. a return of 4.5% p.a

Islamic Money MarketIslamic Money Market

I l i M M k tI l i M M k t

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 20/89

• BNM Wadiah Placement

• BNM accept placement of fund from the money marketunder the concept of Wadiah.

• Under Wadiah contract, BNM undertake to safeguard thefund placed with them and will refund the same amount onmaturity date.

• Islamic banks will place excess fund with BNM for safekeeping.

• The period of placement range for overnight only.

• Profit (if any) is paid based on discretion of BNM.

Islamic Money MarketIslamic Money Market

Islamic Money MarketIslamic Money Market

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 21/89

• BNM Wadiah Tender

• Similar approach with Wadiah placement.

• The information of tender is being disseminated earlymorning of the Wadiah issuance through FAST.

• The period of placement ranges from 1 week to 3 months.

• The amount tendered will be prorated with issuance sizeand successful tender is based on their bid size.

• Profit (if any) is paid based on discretion of BNM.

Islamic Money MarketIslamic Money Market

Islamic Money MarketIslamic Money Market

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 22/89

• Trading of Islamic Financial Instruments• IMM creates a secondary market where participants trade

all the available Islamic financial instruments.• The market allows:

• Easy access to Islamic Instruments

• Provide liquidity in the market for the financialinstruments

• Trading and Arbitraging

• between instruments with same tenor

• between tenor of the same class of instruments

• Each instrument is different from one another in terms ofrisk profile, yield, tenor, marketability and liquidity.

Islamic Money MarketIslamic Money Market

Islamic Money MarketIslamic Money Market

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 23/89

Risk Spectrum

Financial Institutions(less risky, less volatile,

reasonable return

Sovereign Papers(risk free, less volatile

low return)

Increased risk and volatility

Reduced yield on investment

Corporate Papers(riskier, more volatile

high return)

Islamic Money MarketIslamic Money Market

Islamic Money MarketIslamic Money Market

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 24/89

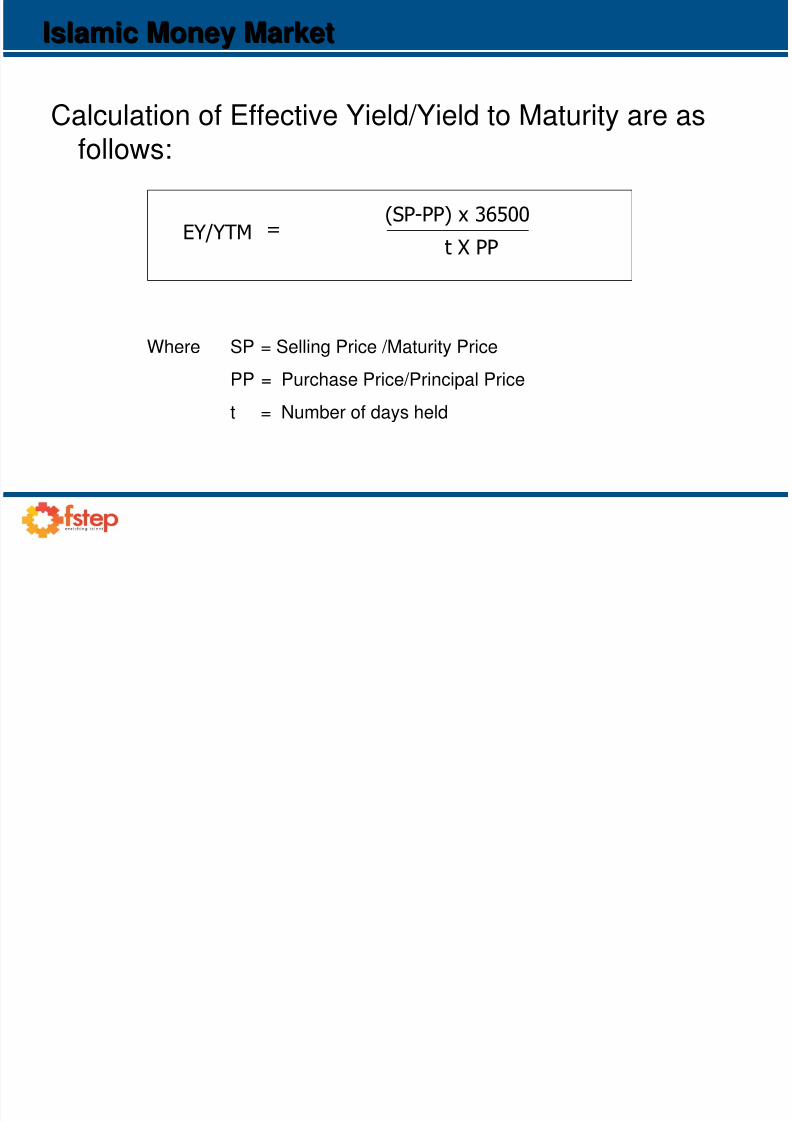

Calculation of Effective Yield/Yield to Maturity are asfollows:

EY/YTM

Where SP = Selling Price /Maturity Price

PP = Purchase Price/Principal Pricet = Number of days held

=(SP-PP) x 36500

t X PP

Islamic Money MarketIslamic Money Market

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 25/89

5Islamic Financial Instruments

Islamic Financial InstrumentsIslamic Financial Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 26/89

Bank Negara Monetary Notes - i (BNMN-i)

BNMN-i is a liquidity management tool issued by BNM to

manage liquidity in the Islamic Money Market. BNMN-i was introduced by BNM on December 8, 2006 to

replace Bank Negara Monetary Notes.

Issued under the Islamic principle of Bai al Enah, thetransaction involved a for forward sale (principal plusprofit) of assets owned by BNM and the corresponding

spot purchase (immediate delivery) of the said assets. Minimum standard amount is RM5 million.

Islamic Financial InstrumentsIslamic Financial Instruments

Islamic Financial InstrumentsIslamic Financial Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 27/89

• Bank Negara Monetary Notes-i (BNMN-i)• The issuance of BNMN-i is on tender basis to principal

bidder with information of the issuance being published

through FAST a few days before the issue date.• The bidding proceed is based on the following formula :

Proceed = Face Value of Tender x 1 – ((r x t)/36500)where r = discounting rate

t = tenor of issue• The successful bidder is the market participant who

tendered for the highest price for the asset offered by

BNM.• Debt created from the Bai al Enah contract is traded in

the secondary market under Bai Al Dayn concept.

Islamic Financial InstrumentsIslamic Financial Instruments

Islamic Financial InstrumentsIslamic Financial Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 28/89

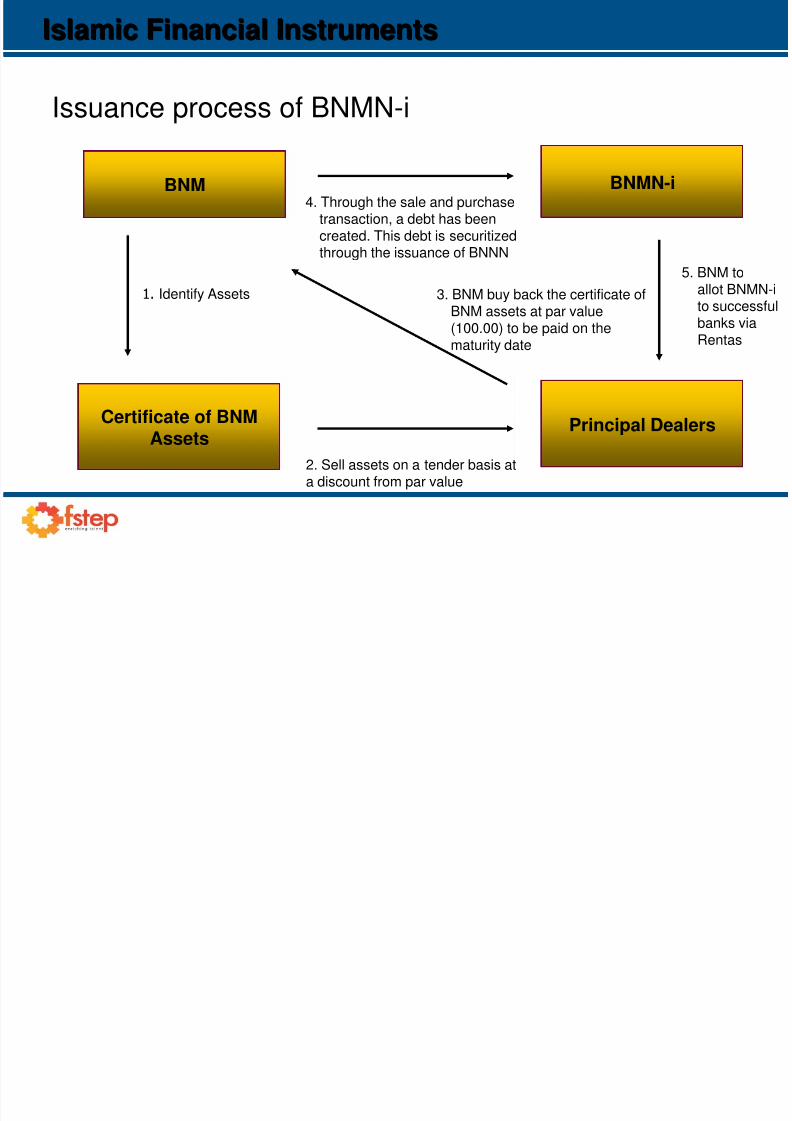

Issuance process of BNMN-i

Certificate of BNMAssets

BNM

Principal Dealers

BNMN-i

1. Identify Assets

2. Sell assets on a tender basis at

a discount from par value

3. BNM buy back the certificate ofBNM assets at par value(100.00) to be paid on thematurity date

4. Through the sale and purchasetransaction, a debt has beencreated. This debt is securitizedthrough the issuance of BNNN

Islamic Financial InstrumentsIslamic Financial Instruments

5. BNM to

allot BNMN-ito successfubanks viaRentas

Islamic Financial InstrumentsIslamic Financial Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 29/89

Bank Negara Malaysia Sukuk Ijarah (BNMSI)

BNMSI is another short term money market instrumentissued by BNM under the Islamic principle of Ijarah.

Under Ijarah contract, BNM undertake to sell an asset to anSPV who will issue BNMSI to finance the purchase price.SPV will lease back the asset to BNM with agreed rentalwhich will be further paid to BNMSI holders. On the expiry

of lease, BNM will purchase back the asset from SPV andthe sukuk will be redeemed.

Tenor of BNMSI ranges from 1 year to 3 years with

quarterly rental payment. The tender is based on the rental rate and the successful

bidder is the one who tendered for the lowest rental rate for

the BNMSI.

Islamic Financial InstrumentsIslamic Financial Instruments

Islamic Financial InstrumentsIslamic Financial Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 30/89

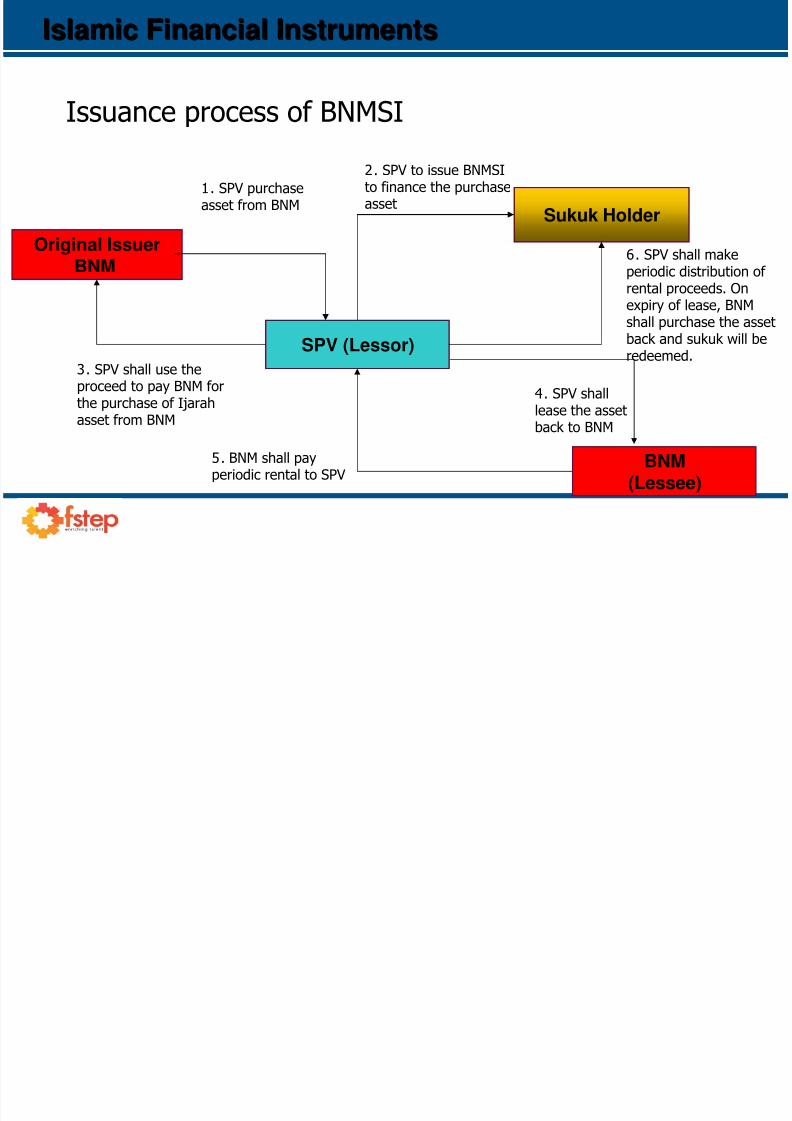

Issuance process of BNMSI

SPV (Lessor)

Original IssuerBNM

BNM

(Lessee)

Sukuk Holder

1. SPV purchaseasset from BNM

2. SPV to issue BNMSIto finance the purchaseasset

6. SPV shall makeperiodic distribution of

rental proceeds. Onexpiry of lease, BNMshall purchase the assetback and sukuk will beredeemed.

3. SPV shall use the

proceed to pay BNM forthe purchase of Ijarahasset from BNM

5. BNM shall payperiodic rental to SPV

4. SPV shalllease the assetback to BNM

Islamic Financial InstrumentsIslamic Financial Instruments

Islamic Financial InstrumentsIslamic Financial Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 31/89

Malaysia Islamic Treasury Bills (MITB)

MITB is a short term money market instrument issued by

the Government under the Islamic principle of Bai al Enah. Under Bai al Enah contract, the Government will

undertake to sell identified asset to successful FI’s on

cash basis at a discount and subsequently buy back thesame asset at par on deferred payment.

MITB’s tenor, issuance process and trading in the

secondary market is similar to BNMN-i.

Islamic Financial InstrumentsIslamic Financial Instruments

Islamic Financial InstrumentsIslamic Financial Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 32/89

Issuance process of MITB

Certificate of GOMAssets

Government of

Malaysia

Principal Dealers

MITB

1. Identify Assets

2. Sell assets on a tender basis at

a discount from par value

3. GOM buy back the certificate ofGOM assets at par value(100.00) to be paid on thematurity date

4. Through the sale and purchasetransaction, a debt has beencreated. This debt is securitizedthrough the issuance of MITB

5. GOM thru

BNM toallot MITBto successfubanks viaRentas

Islamic Financial InstrumentsIslamic Financial Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 33/89

Government Investment Issues (GII)

Issued by law under the Government Investment Act 1982(amended 1990)

Investment in GII constitutes an investment to the

government based on the principle of Bai Al Inah. Under Bai al Enah contract, the Government undertake to

sell identified asset to successful FI’s on cash basis and

subsequently buy back the same asset plus profit ondeferred payment.

Islamic Financial InstrumentsIslamic Financial Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 34/89

Government Investment Issues (GII)

Tenor ranges from 3 years to 10 years. Issuance of GII is on tender basis to principal bidder

with information of the issuance being published through

FAST a few days before the issue date. Tendering procedure for GII is similar to instruments

issued by Government or BNM.

Pricing of GII in the secondary market is based on thenormal bond market pricing convention.

Islamic Financial InstrumentsIslamic Financial Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 35/89

Issuance process of GII

Certificate of GOMAssets

Government of

Malaysia

PrincipalDealers

GII

1. Identify Assets

2. Sell assets on a tender basiseither on discount or par value

3. GOM buy back the certificate ofGOM assets (principal plusprofit) to be paid on the maturitydate

4. Through the sale and purchasetransaction, a debt has beencreated. This debt is securitizedthrough the issuance of GII

5. GOM thru

BNM toallot MITBto successfubanks viaRentas

Islamic Financial InstrumentsIslamic Financial Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 36/89

• Accepted Bills – Islamic (AB-i)• AB-i is a bill of exchange which is either:

• drawn by the Bank and accepted by the

importer/purchaser – underlying syariah concept isMurabahah

• drawn by the exporter/seller and accepted by theBank – underlying syariah concept is Dayn

• The bill constitutes a debt owed to the Bank, thuseligible for trading in the secondary market.

• The underlying Shariah transaction for trading in the

secondary market is known as Bai Al-Dayn (debt trading)• The rate of discounting of AB-i shall reflect the current

market standing

Islamic Financial InstrumentsIslamic Financial Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 37/89

• Accepted Bill - Islamic (AB-i)

• Calculation of proceeds of AB-i is derived at as follows:

Proceed

Where FV = Face Value

r = Discounting rate (in %)

t = Number of remaining days to maturity

= FV r x t

3651 -( )

Islamic Financial InstrumentsIslamic Financial Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 38/89

• Islamic Commercial Papers

• ICP are debts issued by corporation to fund their capitalrequirement on short term, roll over basis.

• It is issued under the concept of Murabahah.

• Prior to issuance of ICP the rated by rating agency.

• Corporation must obtain approval from SecuritiesCommission (SC)

• Types of ICP:• Murabahah Notes Issuance Facility (MUNIF)

• Islamic Revolving Underwritten Facility (IRUF)

• Guaranteed Revolving MUNIF (GRUNIF)

Islamic Financial InstrumentsIslamic Financial Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 39/89

Issuance process of ICP

Assets

Corporation

Tender PanelMembers

ICP

1. Identify Assets

2. Sell assets on a tender basiseither on discount or at par value

3. Corporation buy the assets(principal plus profit) to be paidon the maturity date

4. Through the sale and purchasetransaction, a debt has beencreated. This debt is securitizedthrough the issuance of ICP

5. Lead

arranger toallot ICPto successfubanks

Islamic Financial InstrumentsIslamic Financial Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 40/89

• Islamic Commercial Papers

• Calculation of proceeds of Islamic Commercial Papers isderived at as follows:

Proceed

Where FV = Face Value

r = Discounting rate (in %)

t = Number of remaining days to maturity

= FV r x t

3651 -( )

Islamic Financial InstrumentsIslamic Financial Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 41/89

• Negotiable Islamic Debt Certificate (NIDC)

• NIDC is the Shariah-compliant alternative to the NegotiableInstrument of Deposit (NID) currently offered by the

conventional banks.• The underlying Shariah transaction for the creation of

NIDC is Bai Bithaman Ajil – BBA (Deferred payment sale).

• NIDC is issued to the customer as an evidence of theBank’s debt to the customer.

• The debt is tradable in the secondary market under theconcept of Bai Al-Dayn.

• NIDC certificate is a security items that must be kept bythe customer’s authorized custodian which is usually theissuing bank.

Islamic Financial InstrumentsIslamic Financial Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 42/89

Formula to calculate price of NIDC, with maturity less than1 year:

Price

RV

T x Y

Where RV = Redemption value per RM100 nominal value

T = No. of days from settlement date to maturity date

Y = Yield / Profit rate

=

365001 + ( )

[Price are rounded up to 4 nearest decimal point]

Islamic Financial InstrumentsIslamic Financial Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 43/89

Formula to calculate price of NIDC, with maturity exceeding 1 year:

Price RV

Yld

Where RV = Redemption value per RM100 nominal value

Yld = Yield in % p.a.

DSC = No. of days from settlement date next quasi coupon

date (as if the instrument pay semi annual profit)DCC = No. of days in quasi coupon period

n = No. of remaining quasi coupon profit period

m = No. of dividend payment per year

=

m1 +( )

n-1+DSC/DCC

Islamic Financial InstrumentsIslamic Financial Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 44/89

• Commodity Murabahah Program (CMP)• CMP is a universally accepted trade transaction

structured as a money market instruments under the

contract of Murabahah.• The trade involve a spot purchase of Syariah approved

commodities for immediate delivery and a forward sale

on deferred payment term.• There are three types of CMP:• Commodity Murabahah Deposit

• Commodity Murabahah Investment

• BNM Commodity Murabahah Tender

• Profit on CMP is calculated based on the simple interestformula i.e. Principal x Rate x Tenor

Islamic Financial InstrumentsIslamic Financial Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 45/89

Commodity Murabahah Deposit

Counter Party

BIMB, as Principal

BIMB,Acting as Agent

Trader 2

Trader 1

2

3

1

C/party appointsBIMB as its agent tobuy commodity from

London Metal

Exchange (LME).BIMB buys the

commodity by cashvia Trader 1.

$

$

Deferred$

Commodity

Commodity

Commodity C/party then sells thecommodity to BIMB viadeferred payment. TheSale Price representsthe return from deposit

for BIMB.

BIMB sells thecommodity at LME via

Trader 2 for cash.

Islamic Financial InstrumentsIslamic Financial Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 46/89

Commodity Murabahah Investment

Counter Party

$ Commodity Deferred$

BIMB

1

BIMB as Agent

Trader 1

Trader 2

2

3

Commodity

Commodity

$

BIMB then sells the commodity toC/party. Sale Price representsBIMB’s expected return from

investment and will be paid byC/party via deferred payment.

C/party then appoints BIMas agent to sell the

Commodity at LME by casvia Trader 2. The cash

belongs to C/party,

representing investmentproceeds.

BIMB buys aCommodity at

LME by cash viaTrader 1

Islamic Financial InstrumentsIslamic Financial Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 47/89

Cagamas Islamic Bond (CIB) CIB are bonds issued by Cagamas Berhad under the Islamic

principle to raise funds for their operations.

Cagamas business includes purchase of Islamic mortgage, hirepurchase and other asset classes from financial institutions

Bond issuance range between 1 to 7 years with profit payable semiannual basis

From purchases of asset with recourse, Cagamas has expanded itbusiness to include outright purchases of financial assets

There are 3 types of Cagamas Islamic Bond:

1. Sanadat Murabahah Cagamas

2. Cagamas Bai Bithaman Ajil Islamic Securities (BAIS)

3. Cagamas Islamic Residential Mortgage Backed Securities

Islamic Financial InstrumentsIslamic Financial Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 48/89

1Grant Islamic

financing

2Pay monthly

instalment

9Pay

coupon

7Appoint Approved Sellers as servicer

Pre-saleDuring sale

Post-sale

Overview of Cagamas Structure

ApprovedSellers3

Sell Islamic debts

4Receive cash

6Receive

cash

5IssueCIB8

Remit Cagamas instalment

Customers

Cagamas

Principal Dealers/Investors

Islamic Financial InstrumentsIslamic Financial Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 49/89

1. Cagamas Mudharabah Bond (CMB)

Based on the concept of Al Mudharabah CMB allows thebondholders and Cagamas to share profit generated fromthe issuer operation in purchasing financial assets from

Islamic financial institutions. Both parties agree to share the profit derived from the

venture based on an agreed profit sharing ratio.

The bondholder will bear any loss of diminution in theprincipal amount of the bond

Islamic Financial InstrumentsIslamic Financial Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 50/89

2. Cagamas Bai Bithaman Ajil Islamic Securities(BAIS)

Introduced to replace SMC with its first issuance in

August 2004.

Issued based on the principle of Bai al Inah.

Under Bai al Enah contract, Cagamas undertake to sellidentified asset to successful investors on cash basisand subsequently buy back the same asset at par ondeferred payment basis.

The profit rate is fixed and paid twice a year.

Calculation of proceed is similar with coupon bearingbonds calculation.

Islamic Financial InstrumentsIslamic Financial Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 51/89

3. Cagamas Islamic Residential Mortgage BackedSecurities (RMBS-i)

First issued on August 8, 2005.

Issued based on the principle of Musyarakah, Cagamasand bondholders enter into a joint venture to fund theissuer operation in purchasing financial assets from

Islamic financial institutions. Profit is shared by both Cagamas and bondholders

based on an agreed profit sharing ratio.

Both Cagamas and bondholder will bear any lossarising from the bond issuance according to the ratioagreed by both parties.

Islamic Financial InstrumentsIslamic Financial Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 52/89

•.

• Islamic Bond (IB)/ Islamic Debt Securities (IDS)• IB’s are debts issued by the multinational or big

corporation to raise funds for their operations.

• Typically issued for long term capital expenditurerequirements and project financing for concessionaires,infrastructures and utilities.

• The tenor of issuance of IB’s ranges between minimum

period of 3 years and maximum of 20 years.• SC approval is required prior to any bond issuance and

must be rated (except for quasi government issuance) .

• There are two types of IB:1.Zero Coupon Islamic Bond

2.Fixed Rate Islamic Bond

Islamic Financial InstrumentsIslamic Financial Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 53/89

1. Zero Coupon Islamic Bond• Issued at a discount from the face value.

• This bond does not have any inward cash flow in

term of profit payable every semi annual and bondholder only received the face value upon maturityof the bond.

• The few Syariah contracts used as underlyingtransaction include:a. Murabahah - Khazanah Bond

b. Bai Bithaman Ajil – SILK & Encorp

b. Qardh Al Hassan - Petronas Dagangan & Petronas Gas

Islamic Financial InstrumentsIslamic Financial Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 54/89

Price of Bond is calculated based on the following formula:

P = Price of Bond

FV = Face value per RM100 nominal value

i = Yield to maturity

m = Number of coupon payment per year

n = Number of years to maturity

D = Number of days from value date to next coupon date (as if the bond pays semi annual coupon)

E = Number of day in coupon period

NV = Nominal Value of bond

P = FV

1 + i mn-1+D/E

Proceed = NV x PB

m

100

Islamic Financial InstrumentsIslamic Financial Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 55/89

2. Coupon Islamic Bond• Issued at nominal value which is equivalent to the face

value (amount payable upon maturity).

• A series of coupon (annual or semi annual ) is paid basedon fix agreed rate.

• The underlying Syariah concept is Bai Bithaman Ajil Ijarah,

Mudharabah and Musyarakah.• The few Syariah contracts used as underlying transaction

for Coupon Islamic Bond include :

a. Bai Bithaman Ajil – KLIA Bond, SAJ, TNBb. Ijarah - Segari Energy Venture. Silterra, KL Kepong

c. Mudharabah – PG Municipal Council, Mukah Power, OCBC Sub Debt

b. Musyarakah – KL Sentral, PLUS, Rantau Abang

Islamic Financial InstrumentsIslamic Financial Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 56/89

Where P = Price of Bond per RM100 nominal valueFV = Face Value per RM100 nominal valueI = Yield to maturitym = Number of coupon payment per yearn = Number of years to maturityc = Coupon rate per annum

A = Number of days from last coupon payment to value dateD = Number of days from value date to next coupon dateE = Number of days in current dividend period

NV = Nominal value of bond transacted

P = mn c/m x 100 + FV -

Σ

t = 1 (1 + i/m) (1 + i/m )

100 x c x Am E

Proceed = NV x PB + NV c x A

100 2 E

t-1+D/E mn-1+D/E

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 57/89

6Islamic Derivatives Instruments

Islamic Derivatives Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 58/89

• Starting from middle of 2005, the Islamic financial markethas started to explore application of derivatives in Islamicfinance.

• Basic building blocks of derivatives:

• Swap

• Forward

• Options

• Futures

• National Syariah Council has approved FX Forward/Swapand Islamic Profit Rate Swap and with more research

undertaken by the market there will be more derivativesinstruments endorsed by the council thus opening up thedevelopment of Islamic structured products in the nearfuture.

3 IPRSIslamic Derivatives Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 59/89

3 IPRS

1. Islamic Profit Rate Swaps (IPRS)

Main objective of IPRS is to assist banks and corporate inthe management of profit rate risk.

An agreement to exchange a series of profit/return/ coupon

rates between two counterparties (normally consist of aFixed Rate Party and a Floating Rate Party);

Implementation is by the execution of a series of underlying

Murabahah contracts on commodities.

IPRS (cont ’d)

Islamic Derivatives Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 60/89

BIMBIPRS

Counterparty

Pays Fixed Rate

Receives Floating Rate

Financial Liability

FinancialAsset

Receives Fixed

Returns

Pays Floating

Obligations

I

P

R

S

IPRS (cont d)

IPRS (cont ’d)

Islamic Derivatives Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 61/89

Bank Islam

• IPRS Stage 1: Fixed Profit Rate Leg

Broker

CParty sells commodity to Bank Islam

at FIXED price (costPlus - Deferred)1 2

IPRSCounterparty

Broker

CParty buys commodity from

broker through Bank Islam asAgent

Bank Islam sells commodity to

broker3

1

2

3

Commodity Flow

Funds Flow

IPRS (cont d)

Bank Islam as Agent

IPRS (cont ’d)

Islamic Derivatives Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 62/89

BIMB

broker

BIMB sells commodity to CParty at

FLOATING price (costPlus - Deferred)1 2

IPRSCounterparty

broker

CParty sells commodity

to broker through Bank Islam as Agent

BIMB buys commodity from broker

3

1

2

3

Commodity Flow

Funds Flow

IPRS (cont d)

IPRS Stage 2: Floating Profit Rate Leg

Bank Islam as Agent

Islamic Derivatives Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 63/89

2. Islamic Forward Rate Agreement (IFRA )

Main objective of IFRA is to assist banks and corporate inthe management of profit rate risk.

An agreement to exchange profit/return/ coupon rates

between two counterparties at a single specified period Implementation is by the execution of a single Murabahah

contracts on commodities.

IFRA can also be structured to hedge a series of amortizedcashflow.

Islamic Derivatives Instruments

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 64/89

3. Islamic Cross Currency Swaps (ICCS)

ICCS enables counter-party to switch their asset or liability

from one currency to another to : Hedge currency risk

Profit rate risk

The agreement to exchange currency between two counter-parties can be between fixed profit rate to fixed profit rate,fixed to floating or floating to floating.

Implementation is by the execution of a series of underlyingMurabahah contracts on commodities.

Islamic Derivatives Instruments

I iti l E h f P i i l d P i di P fit P t

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 65/89

MalaysianCorporate BIMB1. MYR Principal

1.USD Principal

MYR Financing

USSubsidiary

1. USD

Principal

1. MYR Principal

I

C

C

S

2.USD Profit

Payment

2.MYR ProfitPayment

2.MYR Profit Payment

2.USD Profit Payment

Initial Exchange of Principal and Periodic Profit Payment

Islamic Derivatives Instruments

Exchange of Principal on Maturity Date

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 66/89

MalaysianCorporate BIMB

3. MYR Principal

3.USD Principal

MYR Financing

USSubsidiary

3. USD

Principal

3. MYR Principal

I

C

C

S

Exchange of Principal on Maturity Date

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 67/89

7Islamic Foreign Currency

Islamic Foreign Currency

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 68/89

• Treasury operation also involves activities related to foreignexchange which conform to Syariah. The activities include :• Commercial transactions

• Inter-bank trading (Proprietary Trading)

• Forms of foreign exchange transactions include spot, swapand forward.

• Exchange of one currency against another is permissible inIslam under the concept of Al Sarf. However suchtransaction must be under the following conditions• involving two different currencies

• delivery of currencies must be done concurrently

Islamic Foreign Currency

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 69/89

• Inter-bank trading which account to more than 90% of thetotal foreign exchange volume worldwide can be classified

as follows:i. Investment - Fundamental / Long term in nature

ii. Speculation - Technical / Short term in nature

iii. Gambling - No basis / information

• Transaction acceptable is for investment and speculation.

• Trading is subject to the net open position permissible byBNM and internal approved daylight and overnight

exposure of the respective financial institution.

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 70/89

• Prices of the underlying concept for FX Forward and Swap

is Waad Mulzim (Unilateral Promise)• This is to facilitate settlement process and satisfy market

convention for a forward contract where the delivery of theexchange is done at a specified future date.

• In other word, Wa’ad is made on the transaction date andthe Sarf akad is perform on settlement date.

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 71/89

8FOREX Trading

FOREX TRADING

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 72/89

• Front Line Operations

• Back Office Operations

FOREX TRADING

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 73/89

Front Line Operations:

• Corporate Forex

• Proprietary Trading

• Funding

FOREX TRADING

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 74/89

Corporate Forex:

• Provides quotations to corporate customers

• Provides advisory services to corporatecustomers

• Daily branch FX counter rates

• Marketing

FOREX TRADING

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 75/89

Proprietary Trading:

• Trading on the inter-bank market• Taking position for the bank

• Guided by limits imposed by bank• ‘Squaring off’ corporate positions

FOREX TRADING

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 76/89

Funding:

Placing of excess foreign currency funds(borrowing of shortage currency funds) indeposits/trading of excess funds

FOREX TRADING

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 77/89

Back Office Operations:

• Settlement of transactions• Confirmation of transactions

• Limit monitoring

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 78/89

9FOREX Transactions in IslamicBanking Operations

OVERVIEW

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 79/89

• A marketplace where one currency (e.g. MYR) is exchangedwith another currency (e.g. USD) at a price determined by

market forces

• Operates in Over The Counter (OTC) market• Global foreign exchange (FX) market is the biggest market

in the world

• Average global daily turnover in foreign exchangetransactions is more than USD1.5 trillion.

• Operates in a 24 hour market.

OVERVIEW

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 80/89

Corporations:•Trade•Investment

Individuals:•Investments•Personal use

Commercial Banks:•Provide services to corporations

and individuals•Trading for own accounts

Central Bank:•Managing reserves/intervention•Provide direction to otherparticipants

Brokers:Middlemen

OVERVIEW

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 81/89

Factors Affecting FX Rates:• Economic Factors:

Gross Domestic Product (GDP), Consumer PriceIndex (CPI), Money Supply, Balance of Payment

(BOP), Capital Flows

• Government and Central Bank Policies

Fiscal/monetary policies

External debt, budget deficits/surpluses

Current account deficits/surpluses

OVERVIEW

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 82/89

Fac tors Affec ting FX Rates:

Centra l Bank’s ac tion and polic ies

Spec ula tive position

Political

Tec hnic a lSeasona l demand, yea r-end fac tors

Market information and rumours

Foreign Exchange Trading Policies

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 83/89

• Bank Negara Malaysia’s Exchange ControlNotices

• Exchange Control Act 1953

• Rules on Ringgit Operations Monitoring

System (RIMS)

Bank Negara Malaysia’s Exc hange Control Notic es

Foreign Exchange Trading Policies

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 84/89

• ECM 2: Dea lings in Gold & Foreign Currenc y

• ECM 3: Externa l Ac c ounts

• ECM 4: Genera l Payments• ECM 5 : Export of Goods

• ECM 6: Cred it Fac ilities to Non-Residents

• ECM 7: Foreign Currenc y Ac c ounts• ECM 8: Domestic Cred it Fac ilities to Non-Resident Controlled

Companies

• ECM 9: Investment Ab road• ECM 10: Foreign Currenc y Cred it Fac ilities & Ring g it

Bank Negara Malaysia’s Exc hange Control Notic es

Foreign Exchange Trading Policies

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 85/89

• ECM 12: Sec urities

• ECM 13: Import & Export of Currenc y Notes, Bills of Exc ha nge,

Assuranc e Polic ies, etc .• ECM 14: Dea ling s with Spec ified Persons and In Restric ted

Currencies

• ECM 15: Labua n Interna tiona l Offshore Fina nc ia l Centre

• ECM 16: Ap proved Opera tiona l Headquarters

Types of FX Instruments:

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 86/89

• Spot

• Forward

• Swap• Futures

• Non-Deliverable Forward (NDF)

• Options

• Struc tured Produc ts/ Derivatives

OVERVIEW

V i T f FX T i d V l D

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 87/89

FX Contrac ts

Various Types of FX Transac tions and Value Dates

Immed iate Contrac ts

Forward Contrac ts

OVERVIEW

V i T f FX T ti d V l D t

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 88/89

Various Types of FX Transac tions and Value Dates

Immed iate Contrac ts

Va lue Today (TOD) Va lue Tomorrow(TOM)

Va lue Spot

FINANCIAL SECTOR TALENT ENRICHMENT PROGRAMME

8/7/2019 FSTEP%20islamic_treasury_operation

http://slidepdf.com/reader/full/fstep20islamictreasuryoperation 89/89

Thank you