frozen food in europe key trends and …wabel.com/sites/default/files/frozen food in europe...2017...

TRANSCRIPT

FROZENFOODINEUROPEKeyTrendsAndDevelopments

28th March2018

DanielLojo,FoodAnalyst

©Euromonitor International

2

EUROMONITORINTERNATIONAL

FROZENFOODINEUROPE- KEYTRENDSANDDEVELOPMENTS

OVERVIEW

©Euromonitor International

3

OVERVIEWOFFROZENFOODINEUROPE

GROWTHDRIVERSANDOPPORTUNITIES

KEYTAKEAWAYS

©Euromonitor International

4

Europeleadstheglobalexpenditureinfrozenfood

OVERVIEWOFFROZENFOODINEUROPE

Market size - 2017

RetailValueRSP|USDmillion|ConstantPrices|FixedExchangeRates

Global retail value sales of frozen food

©Euromonitor International

5

PositivebutmodestgrowthacrossEurope

OVERVIEWOFFROZENFOODINEUROPE

§ CAGRof1%between2012and2017

§ Drivenbyhealthandwellnesstrendsandconvenience

§ Fastestgrowthinmeatsubstitutes

Retail value sales of frozen food in Europe (2012-2017)

RetailValueRSP|USDmillion|ConstantPrices|FixedExchangeRates

©Euromonitor International

6

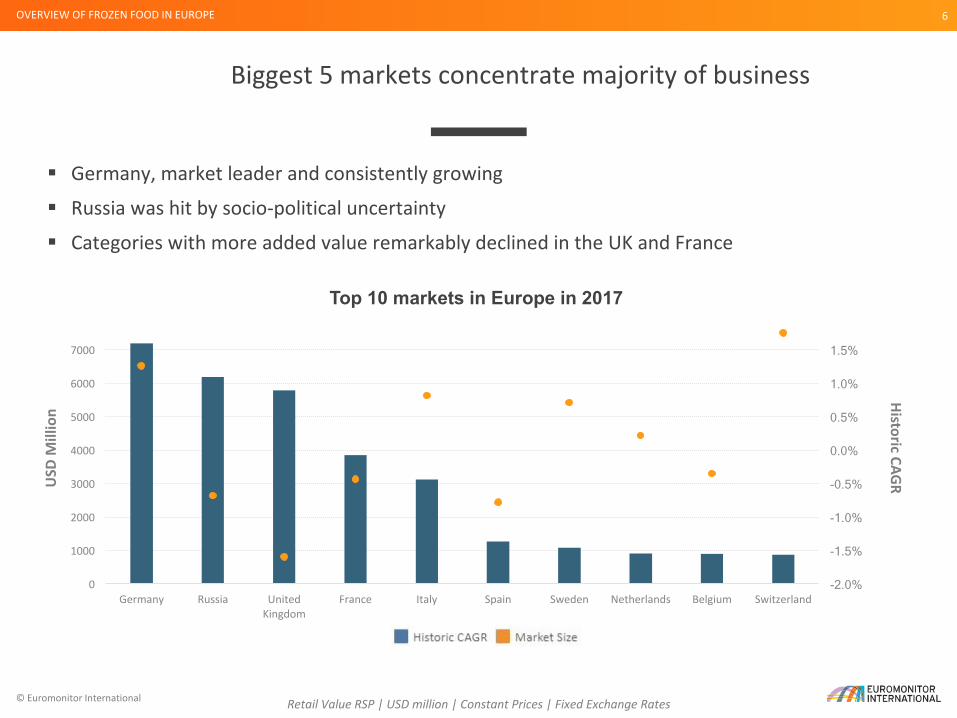

Biggest5marketsconcentratemajorityofbusiness

OVERVIEWOFFROZENFOODINEUROPE

§ Germany,marketleaderandconsistentlygrowing

§ Russiawashitbysocio-politicaluncertainty

§ CategorieswithmoreaddedvalueremarkablydeclinedintheUKandFrance

Top 10 markets in Europe in 2017

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

0

1000

2000

3000

4000

5000

6000

7000

8000

Germany Russia UnitedKingdom

France Italy Spain Sweden Netherlands Belgium Switzerland

USD

Million

HistoricCAG

R

RetailValueRSP|USDmillion|ConstantPrices|FixedExchangeRates

©Euromonitor International

7

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

8.0%

2013 2014 2015 2016 2017

ModestgrowthinWesternEurope,wavesinEasternEurope

OVERVIEWOFFROZENFOODINEUROPE

Top 5 markets performance

§ PizzaandreadymealsdrovegrowthinGermany§ RecessionhitRussia§ MeatandseafoodbehindUK’sweakperformance

RetailValueRSP|USDmillion|ConstantPrices|FixedExchangeRates

©Euromonitor International

8

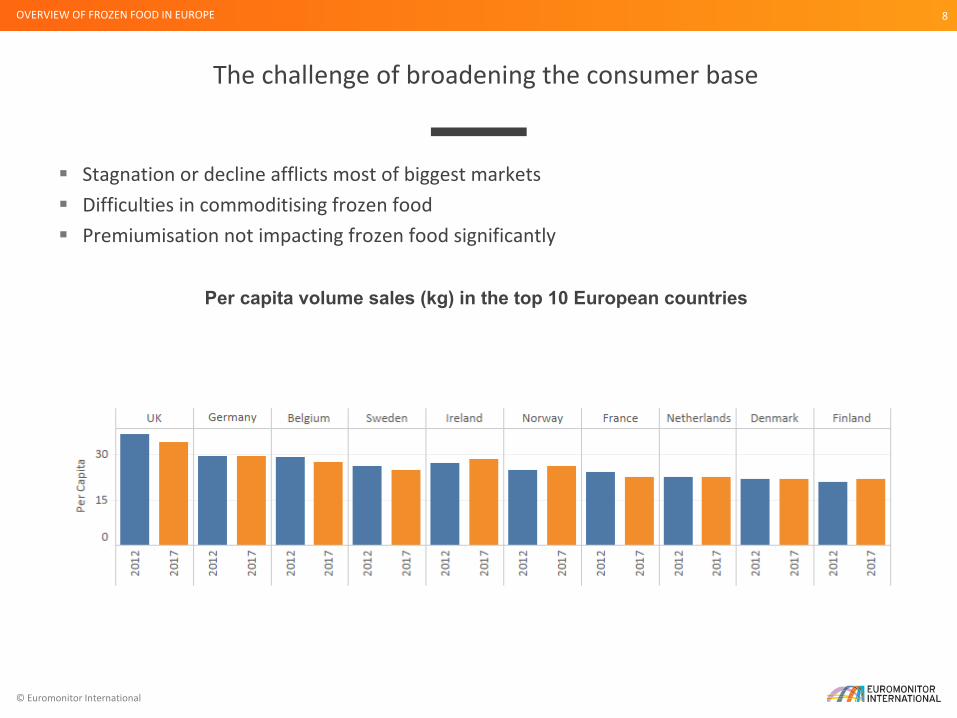

Thechallengeofbroadeningtheconsumerbase

OVERVIEWOFFROZENFOODINEUROPE

§ Stagnationordeclineafflictsmostofbiggestmarkets§ Difficultiesincommoditisingfrozenfood§ Premiumisationnotimpactingfrozenfoodsignificantly

Per capita volume sales (kg) in the top 10 European countries

©Euromonitor International

9

PrivatelabelisstillunbeateninWesternEurope

OVERVIEWOFFROZENFOODINEUROPE

Retail value sales top 5 markets in 2017

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Italy

France

UnitedKingdom

Russia

Germany

PrivateLabel BrandedProducts

RetailValueRSP|USDmillion|ConstantPrices|FixedExchangeRates

©Euromonitor International

10

0%

2%

4%

6%

8%

10%

2012 2013 2014 2015 2016 2017

TightandinvariablecompetitivelandscapeinEurope

OVERVIEWOFFROZENFOODINEUROPE

§ Fiercecompetitiveenvironmenttogainshare

§ OnlyOetker-Gruppe recordednoticeablepositivegrowth

§ Privatelabelmaintainsitsattractiveness

Valueshares

Top 5 branded players

RetailValueRSP|USDmillion|ConstantPrices|FixedExchangeRates

OVERVIEW

©Euromonitor International

11

OVERVIEWOFFROZENFOODINEUROPE

GROWTHDRIVERSANDOPPORTUNITIES

KEYTAKEAWAYS

©Euromonitor International

12

Growthdriversandvalue-addingopportunitiesinfrozenfood

GROWTHDRIVERSANDOPPORTUNITIES

Vegetarianandveganalternatives

Healthandwellnessattributes

Organicandnaturalingredients

Sustainabilityandcleanlabel

Connectingwithdigitalconsumers

Multi-channelopportunities

©Euromonitor International

13

Easypreparationiskey

GROWTHDRIVERSANDOPPORTUNITIES

Feb2018- Spain

Pescanova – Tartar

€4.85– 150g

o Positionedasgourmet

o Ethniccuisine

o InformationviaQRcode

Convenient Connected

©Euromonitor International

14

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

0

10

20

30

40

50

60

70

80

2013 2014 2015 2016 2017

Brandsales Marketshare

Casestudy:Young’sGastro

GROWTHDRIVERSANDOPPORTUNITIES

§ Launchedin2013,sawoutstandinggrowth

§ Keycompetitorsfollowedsimilarstrategies

USD

Million

Gastro performance in the UK – Frozen Processed Seafood

y-o-ygrowth

©Euromonitor International

15

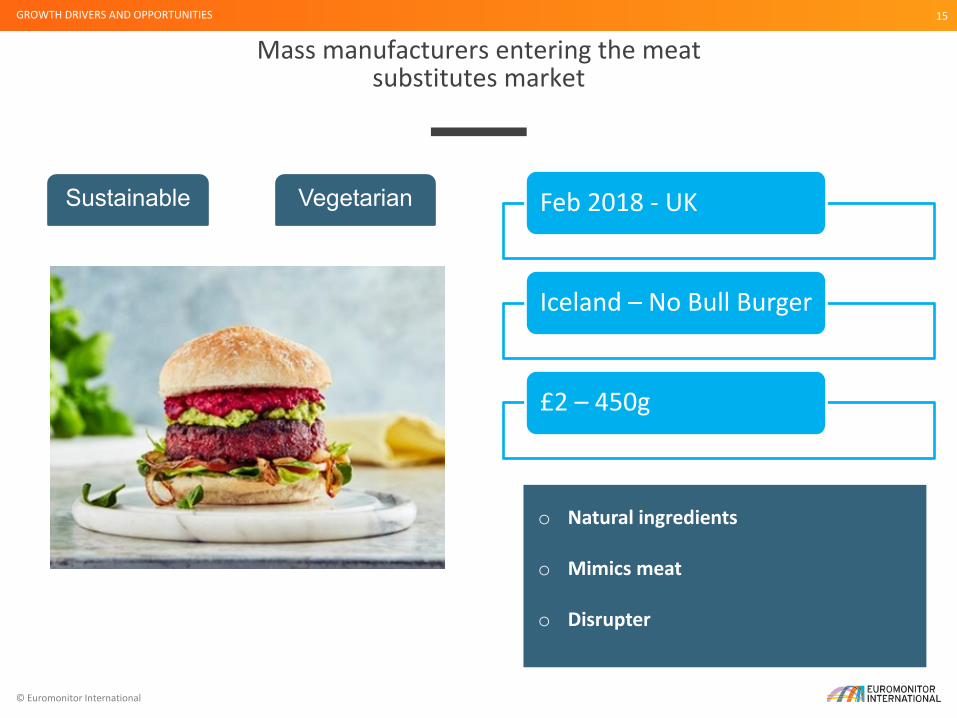

Massmanufacturersenteringthemeatsubstitutesmarket

GROWTHDRIVERSANDOPPORTUNITIES

Feb2018- UK

Iceland– NoBullBurger

£2– 450g

o Naturalingredients

o Mimicsmeat

o Disrupter

Sustainable Vegetarian

©Euromonitor International

16

0%

1%

2%

3%

4%

5%

6%

7%

0

100

200

300

400

500

600

700

2017 2018 2019 2020 2021 2022

Marketsize y-o-ygrowth

Meatsubstituteswillgainoutstandingconsumerattention

GROWTHDRIVERSANDOPPORTUNITIES

§ FrozenmeatsubstitutesstillneedtomakeanappearanceinEasternEurope

§ Morechallengingforprivatelabeltoenterthismarket

USD

Million

Frozen meat substitutes in Europe

y-o-ygrowth

RetailValueRSP|USDmillion|ConstantPrices|FixedExchangeRates

©Euromonitor International

17

Greenoptions,healthyandprofitable

GROWTHDRIVERSANDOPPORTUNITIES

o Convenientduetosmallpack

o Sustainable

o Positionedashealthy

Organic Vegetarian Feb2017- Norway

Pizzabakeriet GrilledeGrønnsaker Økologisk

NOK70– 400g

©Euromonitor International

18

Differentiationthroughorganicproducts

GROWTHDRIVERSANDOPPORTUNITIES

§ Greatestimportanceinbiggestmarkets

§ Privatelabelrangesarealreadypopularinsomecountries

USD

Million

Organic frozen meat, seafood, fruit and vegetables in Europe

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

0

50

100

150

200

250

300

350

400

2017 2018 2019 2020 2021 2022

Marketsize y-o-ygrowth

y-o-ygrowth

RetailValueRSP|USDmillion|ConstantPrices|FixedExchangeRates

©Euromonitor International

19

Naturalingredientsarebackandherestay

GROWTHDRIVERSANDOPPORTUNITIES

March2017- Belgium

Iglo Linzen Lentilles

€3.99– 400g

o Naturalingredients

o Ethniccuisine

o Sourceofproteins

Convenient Vegetarian

©Euromonitor International

20

-2.5%

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

2017 2018 2019 2020 2021 2022

Marketsize y-o-ygrowth

Frozenreadymealswillbenefitfrombusierlifestyles

GROWTHDRIVERSANDOPPORTUNITIES

§ Increaseofsinglehouseholdswillhaveapositiveimpactinreadymealssales

§ Higherqualityandhomemaderecipeimitationswillincreasereadymealsvaluesales

USD

Million

Frozen ready meals in Europe

y-o-ygrowth

RetailValueRSP|USDmillion|ConstantPrices|FixedExchangeRates

©Euromonitor International

21

Growthdriversandopportunities

ADDINGVALUEBYCONNECTINGWITHCONSUMERS

Ensures traceability

Showcases provenance

Pushes for green diets

Improves off and online image

Health advice

Tips to cook

OVERVIEW

©Euromonitor International

22

OVERVIEWOFFROZENFOODINEUROPE

GROWTHDRIVERSANDOPPORTUNITIES

KEYTAKEAWAYS

©Euromonitor International

23

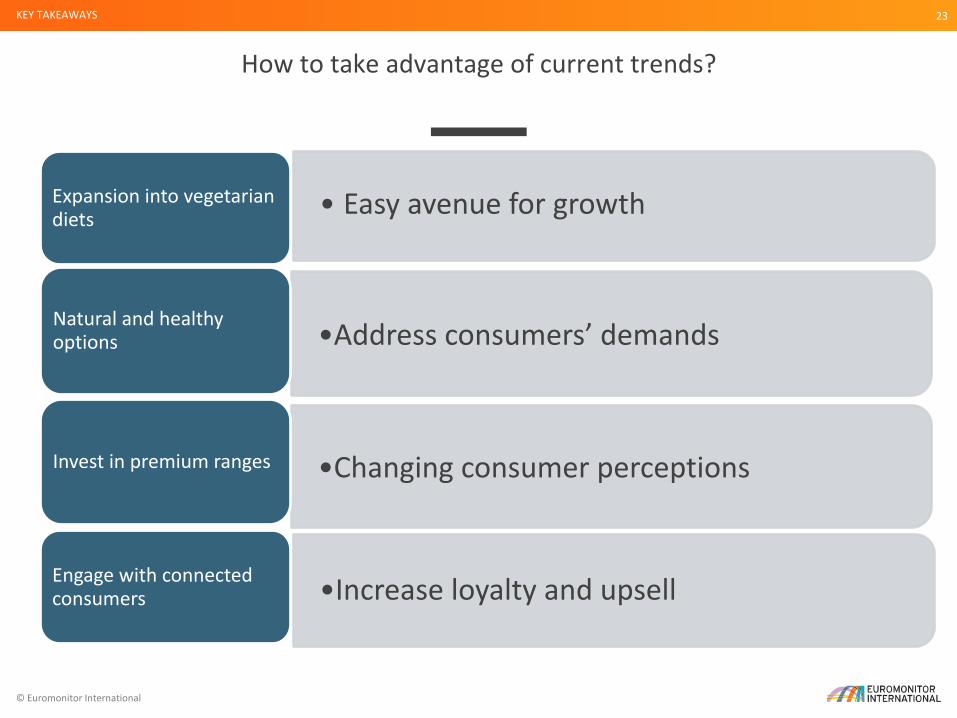

Howtotakeadvantageofcurrenttrends?

KEYTAKEAWAYS

• EasyavenueforgrowthExpansionintovegetariandiets

•Addressconsumers’demandsNaturalandhealthyoptions

•ChangingconsumerperceptionsInvestinpremiumranges

•IncreaseloyaltyandupsellEngagewithconnectedconsumers

MoreInformationDanielLojo,ResearchAnalyst(FoodandNutrition-WesternEurope)

Searchfor“EuromonitorInternationalPackagedFood”

@euromonitor

www.facebook.com/euromonitorinternational