frost industry quotient (iq) 3 asia-pacific collaboration service market, 2013 1. market definition...

TRANSCRIPT

Frost Industry Quotient (IQ): Asia-Pacific Collaboration Service Market, 2013

CONTENTS

1. Market Definition and Scope .......................................................................3

2. Market Assessment ......................................................................................4

2.1 Market Size and Forecast ..........................................................................4

2.2 Competitive Landscape .............................................................................6

2.3 Market Share.............................................................................................7

3. Industry Trends ............................................................................................8

3.1 Regulatory .................................................................................................8

3.2 Economic ...................................................................................................8

3.3 Technology .................................................................................................9

3.4 Competition ..............................................................................................9

4. Frost IQ Matrix: Asia-Pacific Collaboration Service Providers, 2013...........10

5. Profiles of Collaboration Service Providers ................................................11

5.1 InterCall ....................................................................................................11

5.2 Arkadin ......................................................................................................11

5.3 PGi ............................................................................................................12

5.4 Cisco..........................................................................................................12

5.5 Telstra ........................................................................................................12

5.6 BT..............................................................................................................13

5.7 Verizon .......................................................................................................13

5.8 NTT Com...................................................................................................13

5.9 AT&T..........................................................................................................14

5.10 Quanshi (Aka GNET) ...............................................................................14

5.11 Citrix Online............................................................................................14

5.12 IOCOM....................................................................................................14

6. The Analyst Word.........................................................................................15

7. Frost IQ Methodology..................................................................................16

7.1 Market Share.............................................................................................16

7.2 Growth Strategy ........................................................................................16

frost.com 3

ASIA-PACIFIC COLLABORATION SERVICE MARKET, 2013

1. Market Definition and Scope

The term ‘collaboration services market’ refers to cloud and hosted offerings ofaudio, video and web conferencing services delivered as stand-alone or integratedmodels.

Among these three segments, audio conferencing services market is at the mostmature stage, while video bridging services market is gaining popularity andcustomer attention.

At a time when most enterprises are struggling to grow their business in the highlyinterdependent and uncertain global economic situation, the impact of pricecompetition is being felt by the existing service providers of collaboration services.Meanwhile, the market faces emerging competition from countries such as China,India and Japan.

The scope of this research study only covers cloud-based services using virtualizedsoftware in a service provider cloud in either private or shared architectures.Premises-based collaboration solutions are excluded from this study.

Total market size and forecast are calculated based on recurring revenue fromaudio, video and web conferencing services, with pay-as-you-go and monthly flatrate as the primary pricing models available in the market.

Figure 1: Asia Pacific Collaboration Services Market: Market Segmentation, 2013

Source: Frost & Sullivan analysis

Collaboration services can be categorized into the following segments:

Audio Conferencing Services: Enterprise-grade, two-way, full-duplex,•interactive audio call between two or more parties.

Video Conferencing Services: Interactive meeting services that enable two•or more participants at different locations to transmit audio and video data. Itcontains video bridging services, inter-carrier exchange services, equipmentrental services, public room services, and on-site support & managementservices and so on.

frost.com4

Web Conferencing Services: Services that deliver an Internet-based, real-•time, synchronous meeting environment that can be utilized for eitherpresentation or collaboration. The most basic feature of a Web conference isthe ability to share screens, whereby conference participants see whatever ison the presenter's screen.

Others: Includes events, webcast and webinar services, which are interactive•meetings/seminars conducted via the World Wide Web. It is usually a livepresentation, lecture or workshop that happens in real time, as usersparticipate through chatting, video-chatting, file-sharing, or asking questionswith a microphone.

2. Market Assessment

2.1 Market Size and Forecasts

The collaboration services market in Asia Pacific is expected to grow at acompound annual growth rate (CAGR) of 10.9 percent over the 2012-2018 periodto reach $1,209 million by 2018.

Figure 2: Asia Pacific Collaboration Services Market: Revenue Forecast, 2012

Source: Frost & Sullivan analysis

The audio conferencing services market is moving into the mature stage in•major countries in Asia Pacific region, hence we expect a moderate CAGR of8.1 percent from 2012 to 2018, with revenues hitting $489.0 million in 2012,though the year-on-year revenue growth rate kept declining during the last fiveyears. The growth decline was seen among the mature economies like Australia,Singapore and Japan. However, emerging countries like China, India and selectedASEAN countries registered strong growth both in their new customers’acquisition and net usage across existing customer bases.

frost.com 5

Web conferencing services are expected to lead the growth in short term. Asia•Pacific web conferencing services market continued to be the fastest growingregion globally in 2012. However the market has reached a stage whereproducts and services offered seem to have similar features and functionalities.Hence, moving forward, product and service differentiation has become a vitalfactor to win customers.

There is also growing interest from enterprises in adopting video, either in a•leased manner or to have it managed end-to-end from the service provider. Themarket awareness of video collaboration services including bridging andexchange services in developed economies is growing rapidly. Australia, NewZealand, Japan and Korea showed increasing adoption of bridging and mobilevideo services.

Figure 3: Asia Pacific Collaboration Services Market: Percent Sales Breakdown, 2012

Source: Frost & Sullivan analysis

Over-the-top (OTT) vendors like Google are expected to make an impact in the•video collaboration services market in the next 3-5 years. As OTT platformscontinue to proliferate, multi-party video collaboration is likely to be part ofthe next phase of technology development. Small-to-Medium Enterprises (SME)are anticipated to be the target customer in the short run.

The Asia-Pacific market is expected to have a fairly positive outlook for the•next five to seven years. The continuing downward pressure on price will inhibitthe market growth during forecast period. Prices have declined by 5 to15percent in Asia-Pacific, as service provides offer more flexible integration acrossaudio, video and web platforms at the same or reduced prices. Hence, therecould be brisk growth in usage; however, revenues could suffer, if there aredrastic price declines.

frost.com6

The market competition is diversified with a greater variety of market•participants—including incumbent telecom operators, conferencing serviceproviders, cloud service providers and even large system integrators.

Manufacturing, banking and financial institutions, healthcare and transportation•sectors are expected to be the key verticals in driving demand for collaborationservices. In addition, the education sector in China and India, along with the oiland gas industries in India, Australia, and China are expected to provideopportunities for collaboration services during the forecast period.

2.2 Competitive Landscape

The market participants may be classified into two broad categories.

Figure 4: Classification of Collaboration Services Market Participants, 2012

Source: Frost & Sullivan analysis

Telecom operators, including both global and regional telecom companies, havebeen offering self-branded collaboration services as part of their enterpriseofferings for the past ten years. They are the pioneers in the industry and havecontributed significantly to the industry by increasing the market awareness ofcollaboration services and - driving early adoption in the enterprises. In recentyears, the growth initiatives for telecom operators have diversified into twodirections. Some carriers retained their competitive position by allying themselveswith conferencing service providers who have the expertise and advancedinfrastructure, while others continued to invest in the infrastructure andintegration to provide collaboration services as part of the UC-as-a-Serviceportfolio.

frost.com 7

Conferencing Service Providers are the pure-play vendors that provide audio, videoand web collaboration services with integrations that fits the enterprisesrequirements. Companies like InterCall, Arkadin and PGi are driving the extensiveadoption of collaboration services by delivering an enhanced user experienceachieved through a high level of service quality and by offering new and innovativetechnologies.

2.3 Market Share

InterCall, PGi and Cisco contributed 36.8 per cent of the collaboration servicesmarket share in 2012. Other notable market participants include Arkadin, NTTBizlink, Telstra, Quanshi(China), Vcube (Japan), NTT Communications (Japan), CitrixOnline, China Telecom, Verizon and so on.

Figure 5: Asia Pacific Collaboration Services Market: Market Shares by Revenue, 2012

Source: Frost & Sullivan Analysis

frost.com8

3. Industry Trends

In this section, Frost & Sullivan will examine the key trends that shape the AsiaPacific Collaboration Services Market.

3.1 Regulatory

Bring-your-own-device (BYOD) and mobility becomes essential to drive thevolume of collaboration services

Creating a BYOD policy that is consistent and clear around critical business needsis the key to an organization’s security and regulatory accountability. An effectivepolicy requires input from all stakeholders, as well as ongoing assessment of thepolicy’s relevance and effectiveness.

First of all, there should be a solid BYOD policy development process that ensuresthe policy fits the organizations’ and enterprises’ objectives, meets the end-users’expectations and is easy to administer. Having a well-structured and feasible BYODpolicy is the key barrier for enterprises in Asia Pacific region looking to plan theirinvestment on mobility solutions, particularly for large enterprises.

Secondly, deployment planning, especially planning a smooth transaction from legacyplatform and having a solid infrastructure in place as rolling out a BYOD policy iscritical. There are over 10 vendors offering mobility services with advancedcapabilities like conferencing and collaborations in the market. However, findingways to leverage on the existing infrastructure and deploy an easy-to-usecollaboration services, especially video collaboration, will be a key concern for thedecision-makers.

The third element of success is to design an end-user support model. The numberof end-users should be as sufficient, and to create an environment where IT is nolonger involved in managing devices but instead safeguarding corporate data.

Telecom regulations and governance on voice-over-IP (VoIP) is the majorbarrier for the market growth in emerging and growth countries.

Asia Pacific is the most regulated region for Internet Protocol (IP) as compared tothe other regions around the world. This results in high market entry barriers forcountries such as China, India, Vietnam, and Thailand. Hence, lack of fair competitionenvironment is hindering the growth of collaboration services especially for thesmall and medium businesses (SMB) segment of the geographies with regulatoryconstraints.

3.2 Economic

The 2013 global economy showed a year of moderate to low growth with changesin the economy growth drivers. These dynamics raised new policy challenges.Advanced economies showed signs of resurgent growth coupled with the task ofcontinuing to bolster the financial sector, pursuing fiscal consolidation, andincreasing jobs. Emerging market economies were faced with the dual challenge ofslowing growth and tighter global financial conditions. As a result, the GDP growthfor the Asia Pacific region remained relatively lower and is estimated to have grownby only 6.0 percent in 2013. Despite the growth potential of the Asia Pacific region,especially among the emerging countries, the sluggishness experienced in some ofthe larger economies meant that the overall growth momentum was affected.

frost.com 9

In the face of rising business difficulties and challenges, a growing number ofenterprises are turning to ICT technology to keep themselves competitiveexternally and collaborative internally. This increased adoption and dependence onIT have led to a corresponding increase in interest and spending on UC andcollaboration services especially those bought as-a-service. As enterprises facegreater cost pressures, they are required to justify their investments on UCsolutions and are looking to adopt those that can help in creating greater value forthe organization, beyond those just the usual communication perspectives. This hasled to increased adoption of collaboration services that help enterprises improveemployee productivity and collaboration experience.

3.3 Technology

IP audio conferencing is expected to become the mainstream solution beingadopted by enterprises in Asia Pacific as network infrastructure improves in theregion. IP audio conferencing allows customers to utilize their private IP networkinvestment for transport to the audio bridges, thus it helps customers to takeadvantage of existing infrastructure and reduces costs. The integration of IP andPublic Switched Telephone Network (PSTN) also provides users flexibility to switchto “hybrid” calls.

Unified Communication-as-a-Service (UCaaS), mainly composed of hostedtelephony services, cloud UC application services and collaboration services, isexpected to grow exponentially in the next 3 to 5 years. New hosted telephony/UCplatforms such as Cisco Hosted Collaboration Solution (HCS) and Microsoft Lyncare emerging quickly and presenting new opportunities and challenges to bothservice providers and customers.

Enterprise broadband access speed and legacy IT infrastructure continue to be theinhibitors to business growth in developing countries such as China, India,Indonesia, the Philippines, Thailand and Vietnam. However developed markets suchas Australia, Japan and South Korea are witnessing a complete rollout of multiplecollaboration services.

These matured markets usually experience a rapid adoption trend for new-releasedproducts and services. With the growing IT infrastructure migration in thedeveloping countries, the integration of conferencing services into a broadervariety of enterprise communication tools, user-friendly interface and competitiverates are the major criteria being considered by customers to adopt collaborationservices in Asia Pacific.

3.4 Competition

The Asia Pacific region is a relatively competitive market when it comes to theservice-oriented industry. The market is saturated with conferencing serviceproviders and telecom operators, both globally and regionally. Leading globalcollaboration service providers increased their market presence across the keycountries like Australia, Singapore and Hong Kong in recent years, as a result of astrong regional presence and expanded partnerships with local telecom operators.On the other hand, in non-English speaking countries like China and Japan, localcollaboration service providers contributed significantly with the plan to increasethe technology awareness with their customers. They are competing against thelocal telecom operators and global collaboration service providers withcompetitive pricing points and customized service offerings.

frost.com10

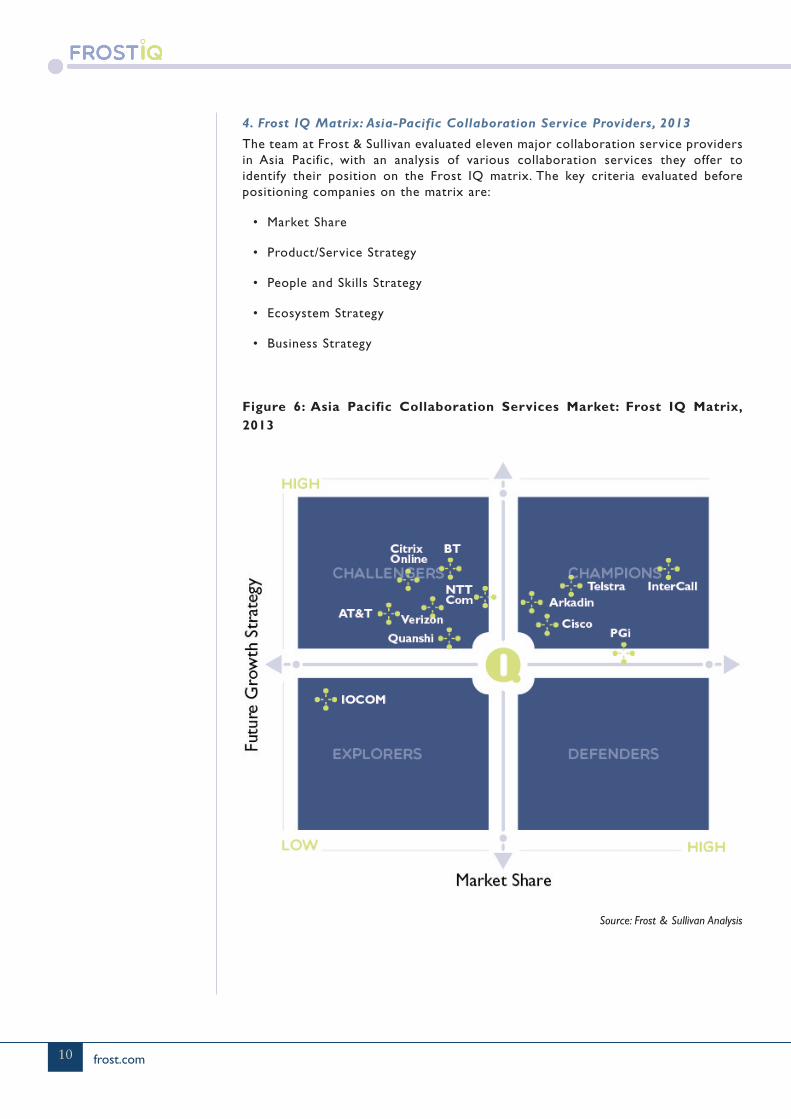

4. Frost IQ Matrix: Asia-Pacific Collaboration Service Providers, 2013

The team at Frost & Sullivan evaluated eleven major collaboration service providersin Asia Pacific, with an analysis of various collaboration services they offer toidentify their position on the Frost IQ matrix. The key criteria evaluated beforepositioning companies on the matrix are:

Market Share•

Product/Service Strategy•

People and Skills Strategy•

Ecosystem Strategy•

Business Strategy•

Figure 6: Asia Pacific Collaboration Services Market: Frost IQ Matrix,2013

Source: Frost & Sullivan Analysis

frost.com 11

As per Figure 6, five collaboration service providers emerged in the Championsquadrant, with InterCall leading the way given its dominant position in the AsiaPacific collaboration services market in 2013 and a robust future growth strategy.Telstra and Arkadin are also strong contenders. However, they face nicheopportunities in the web conferencing services segment.

Another five service providers emerged in the Challengers quadrant. These marketparticipants have a relatively smaller market share as compared to the ones mappedin the Champions quadrant. However, they do have a strong value proposition inplace to meet the future demand trends to help drive growth. Frost & Sullivanexpects these vendors in Challengers quadrant to witness strong growth in thenear future, given their solid growth strategy and expansion plans.

Because of the integration and consolidation of the collaboration services market,stand-alone video conferencing service provider IOCOM is the only one in theExplorers quadrant. IOCOM is in the early stage of market development and isexpected to have good growth potential in future.

5. Profiles of Collaboration Service Providers

5.1 InterCall

InterCall, a globally recognized brand, is the market share leader in the audioconferencing services market. In Asia Pacific, InterCall was able to attain lowdouble-digit growth rate for both mature and emerging economies in 2012. Successwas observed particularly in its unified meetings and communications offerings. Toadapt to the growing mobile workforce and changing device landscape, InterCallreleased an upgraded mobility solution –MobileMeet at the end of 2012 for Androidand iOS smart phones.

InterCall further enhanced the partnership with the two major unifiedcommunications players - Microsoft and Cisco in 2013. It became the first CiscoHosted Collaboration Solution (HCS) partner in the conferencing andcollaborations space. In addition, the service provider is also able to provide ahybrid PSTN-VoIP audio conferencing with Microsoft's Lync platform. Significantly,this integration is available for both Lync Online and Lync Server. With theseenhancements and future growth strategies in place, InterCall is progressivelybecoming a ‘Unified Communications-as-a-Service’ (UCaaS) service provider,capable of directly competing in this space with the likes of other telecomoperators.

5.2 Arkadin

Arkadin is one of the fastest-growing service providers in the Asia Pacificcollaboration services market, with its Compound Annual Growth Rate (CAGR) ofnearly 30 percent from 2010-2012. Improved customer awareness on branding,innovative business models and substantial growth in large enterprises segment arethe three key areas for its success. After its successful alliance with SingTel, Arkadinwent on to expand its partnership with the local telecom operators in Japan, China,India, and Taiwan.

In 2012, Arkadin led the market with over 25 percent year-over-year revenuegrowth in the Asia Pacific region, with phenomenal successes in the Singapore,Japan, India, and South Korea markets.

frost.com12

In 2013, Arkadin was acquired by NTT Communications - one of the leadingtelecom operators in Japan. The acquisition is expected to further drive Arkadin’sgrowth and competitiveness by leveraging NTT Com’s global infrastructure andtechnical expertise. In addition, Arkadin becomes one of the pilot partners for TataCommunications to resell Tata’s video collaboration services – Jamvee, which is agood complement of the existing service portfolio. The partnership is expected toboost the market awareness of Jamvee and also helps Arkadin capture direct growthopportunities in the video collaboration services space.

5.3 PGi

PGi, one of the leading conferencing service providers in Asia Pacific region,witnessed stable growth in the traditional audio conferencing services segment inrecent years. More importantly, the company is strategically moving to theSoftware-as-a-Service (SaaS) space to provide software-enabled collaborationservices across audio, video, and Web, which could become an importantdifferentiator against its rivals. The revenue of its self-branded web conferencingservices – GlobalMeet – doubled in 2012 as compared to the previous year.

The video collaboration application, “iMeet”, was launched in Asia Pacific in the 2ndhalf of 2012, was well accepted by existing customers and helped the companyacquire new customers. As such, PGi became the only conferencing servicesprovider that was able to offer self-branded audio, video and web collaborationservices.

5.4 Cisco

As the leading web conferencing service provider in Asia Pacific, Cisco WebExcontinued to demonstrate thought leadership by further developing WebEx into aworkspace platform. WebEx Connect integrates enterprise-grade IM/presence,audio, video and web conferencing services, as well as IP telephony into a singleplatform. WebEx Social is an enterprise social networking tool that Cisco renamedand further developed from Quad.

In Asia Pacific, Cisco has made the strategic partnership with Samsung Electronicsas part of the Samsung Enterprise Alliance Program (SEAP) 2011 where Cisco andSamsung announced a set of solutions and services for enterprise mobility. Samsungcould adopt Cisco’s Web conferencing tool ‘WebEx Meeting Center’ into theirsmartphones and tablets. This partnership had great implications on the industrywhere so far the absence of enterprise applications with no security issues hadprevented the use of web conferencing from the smartphone and tables forbusiness purposes. Therefore by solving problems and maximizing customersatisfaction, the demand for this enterprise software is expected to rise in the nextfive years. Besides Samsung Electronics, Cisco also partnered with InterCall toestablish the hosted collaboration platform.

5.5 Telstra

Telstra is one of the leading collaboration services providers in Australia market.With audio conferencing service as the core business for this segment, Telstracontinues to invest on IP audio bridge in recent years. As a result, the companymanaged to retain the customer base among key accounts, also increased customerreach among SMBs.

frost.com 13

The company is mainly focused on the research and development on videocollaboration services. The two service options – 1 Touch and Visonnet V2, based onthe latest Cisco and Polycom hosted video conferencing platforms, providebusiness-grade video service without the complexities of infrastructure equipment.Hosted collaboration services segment considered as the most promising segmentin the entire collaboration services portfolio for Telstra. In addition, Telstra startsto resell BlueJean’s video conferencing services which could be a good complementoption for customers with no or little legacy video systems in-house.

5.6 BT

Over the last three years, BT emerged as the most prominent service provider inUC-as-a-Service market in Asia Pacific region. Despite the tough economicconditions in 2012, BT executed a holistic approach in Asia Pacific UCaaS marketand recorded exponential growth. Collaboration services continue to make outsizecontributions to the entire UCaaS portfolio for BT in Asia-Pacific region.

Building on the strength of BT’s growing global presence and portfolio, which offersan extensive range of telecommunication solutions, BT has added a number of newcollaboration services in 2013. These include video bridging (both managed andcloud-based), and infrastructure hosting via a new Hong Kong based data center. Inaddition, it will be expanding its regional operational capabilities with video supportbased out of the existing customer service centre in Sydney.

With the strong regional commitment, BT is gaining traction from verticals such asretail, travel and hospitality along with professional services, especially in countrieswhere BT has a strong presence such as Australia, Hong Kong, Singapore and China.

5.7 Verizon

Verizon deployed Cisco HCS in North America and launched the service with itspilot customers in 2012. Despites that the service provider is exercising caution inresource investment, it went ahead with its entry in Asia Pacific, with some pilotdeployment started from 2nd half of 2013. Instant video services and IP audioconferencing services solution saw robust growth in the Asia Pacific region in 2013.The growth is primarily due to its existing customers in the MPLS and securityareas. The service provider lacks the resources to reach out to the local Asianenterprises and government entities.

5.8 NTT Com

NTT Communications is one of the leading local telcos that aggressively expandedits footprint beyond its home country to meet global customer demands. It is oneof the global service providers to offer Cisco Hosted Collaboration Services (HCS)via Arcstar Unified Communication Services in Japan, achieving robust growth in2012. The company also partnered with Vidyo to offer desktop video conferencingservices as part of Arcstar Unified Communication Services Portfolio.

In 2013, the company acquired France-based conferencing service provider –Arkadin. The acquisition has not made much impact on the industry yet, since thetwo companies remain operating independently so far. The first move is expectedto take place in Japan, which NTT Com will leverage on Arkadin’s advanced audioconferencing infrastructure to enhance customer experiences.

frost.com14

5.9 AT&T

AT&T is another promising global telecom operator that is increasing the marketpenetration in the conferencing and collaboration services space in Asia, especiallyin Singapore, Japan and Hong Kong. The company focuses on large multinationalcompanies and offers a bundled service portfolio among the wide range of advancedIP and networking solutions, in which conferencing services are one of thecomponents. In addition, the self-developed web conferencing service – AT&TConnect- also saw robust growth both on customer awareness and adoptions.

5.10 GNET (Aks Quanshi)

China-based conferencing service provider Quanshi is one of the leading audioconferencing service providers in the China market. The service provider recordedimpressive growth with a CAGR of over 30 percent from 2010 to 2012. Itsinnovative sales and marketing approach, excellent customer support and servicecustomization are the key success factors for Quanshi’s rapid growth. In recentyears, it also launched its own brand of web conferencing and webcasting services.The service provider’s launch of a monthly unlimited pricing plan helped to increaseits sales in the SMB segment.

5.11 Citrix Online

As the second largest web conferencing service provider in Asia Pacific region,Citrix Online focused on the market opportunities in growth geographies such asChina, Malaysia, Indonesia and Philippines.

Citrix Online established a strategic partnership with Shanghai Telecom to offerGoToMeeting as part of the brand Huiyitong to China-based enterprise customerssince October 2012. The partnership with Shanghai Telecom was successful andhelped Citrix to acquire large enterprises in Yangtze River Delta Region. It isexpected that Citrix will expand the partnership with other subsidiaries of ChinaTelecom such as Zhejiang China Telecom and Guangdong Telecom in the short term.

Apart from the progress in China market, Citrix Online also executed aggressivesales approach in ASEAN countries by establishing a direct sales team to reach outto key customer segments and held targeted marketing events to improve brandawareness.

5.12 IOCOM

IOCOM Communications, a US-based emerging desktop video conferencing andcollaboration solutions provider, offers software-based video collaborationsolutions and hosted/cloud services via its own-brand solutions – Vismeet, OEM andWhite label The key competitive differentiators for IOCOM are its flexibility,compatibility, and scalability at affordable pricing. For example, it offers a full-featured subscription model starting from $29 per month per account up to 99lines.

The company does not have a direct presence in Asia Pacific region and is lookingto develop a distribution network among the independent software vendors (ISV).At end of 2012, the company offered a promotion of unlimited number of fullyfunctioning endpoint subscriptions for less than $1 million per year for use at alllevels within the organization.

frost.com 15

6. The Analyst Word

The collaboration services market is one of the fastest growing segments in UCaaSmarket in terms of subscription base, with immense growth potential in the future.BYOD and mobility are expected to be the major growth factor to further drive theadoption in the future. According to a latest research by Frost & Sullivan, mobilecollaboration services subscribers across Asia-Pacific region are expected toexceed 1.5 Million by 2018.

Both vendors and service providers have started to offer video as a service inseveral forms to businesses. As awareness of the benefits of a service-led modelincreases, the impact of challenges to the market as a whole and to individualmarket participants will decrease. Successful market participants will need to takevideo into their service portfolio and offer a flexible, scalable and integratedplatform.

In summary, Frost & Sullivan expects that downward price pressure will continue asa result of increasing adoption of free consumer-centric services which haveimproved and reaching business-grade capabilities. Reliability, quality, range offunctionality and flexibility will continue to be the key factors when enterprises arepurchasing these services.

frost.com16

7. Frost IQ Methodology

The focus of FrostIQ is to provide a balanced assessment of selected markets. Themarkets are those that have been tracked rigorously by Frost & Sullivan analystsover a period of time. Data that has been collected, such as vendor revenue, isscrutinized and forms part of the input for the Frost IQ matrix.

The study approach provides a mix of quantitative and qualitative assessment. TheFrost IQ matrix has two major attributes. They are market share and future growthstrategy.

1 Market Share

Market share information is derived from Frost & Sullivan research programs. Theseresearch programs include market trackers and syndicated research reports. Fromthe regular research which is conducted at quarterly, semi-annual or annualintervals, analysts build a strong revenue database relating to vendors in the market.

According to the Frost IQ Matrix, the X-axis measures the share on a percentagescale. The divide line on the matrix is set at 50 percent of the market share of theleading player in that market.

2 Growth Strategy

Frost & Sullivan considers 4 main components in the growth strategy assessmentpart of Frost IQ. The guiding principle is that these components and theirsubcomponents should follow the MECE (Mutually Exclusive and ComprehensivelyExhaustive) test. The proposed components are as follows:

Product/ service strategy•

People and skills strategy•

Ecosystem strategy•

Business strategy•

There is an equal weightage to all the components with measurement on a 10 pointscale. The dividing line on the Y-axis is at the mid-point i.e. a weighted score of 5 ona 10 point scale. Analysts will provide feedback on the industry participants on theabove parameters based on continual market research and analysis.

Details of the sub-components are available, if required.

17

ABOUT FROST & SULLIVAN

Frost & Sullivan, the Growth Partnership Company, works in collaboration with clients to leverage visionary innovation thataddresses the global challenges and related growth opportunities that will make or break today’s market participants. For morethan 50 years, we have been developing growth strategies for the Global 1000, emerging businesses, the public sector and theinvestment community. Is your organization prepared for the next profound wave of industry convergence, disruptivetechnologies, increasing competitive intensity, Mega Trends, breakthrough best practices, changing customer dynamics andemerging economies?

DISCLAIMER

These pages contain general information only and do not address any particular circumstances or requirements. Frost & Sullivandoes not give any warranties, representations or undertakings (expressed or implied) about the content of this document;including, without limitation any as to quality or fitness for a particular purpose or any that the information provided is accurate,complete or correct. In these respects, you must not place any reliance on any information provided by this document forresearch, analysis, marketing or any other purposes.

This document may contain certain links that lead to websites operated by third parties over which Frost & Sullivan has nocontrol. Such links are provided for your convenience only and do not imply any endorsement of the material on such websitesor any association with their operators. Frost & Sullivan is not responsible or liable for their contents.

COPYRIGHT NOTICE

The contents of these pages are copyright © Frost & Sullivan Limited. All rights reserved.

Except with the prior written permission of Frost & Sullivan, you may not (whether directly or indirectly) create a database inan electronic or other form by downloading and storing all or any part of the content of this document.

No part of this document may be copied or otherwise incorporated into, transmitted to, or stored in any other website,electronic retrieval system, publication or other work in any form (whether hard copy, electronic or otherwise) without the priorwritten permission of Frost & Sullivan.

AucklandBahrainBangkokBeijingBengaluruBogotáBuenos AiresCape TownChennaiColomboDelhi / NCRDetroit

DubaiFrankfurtIskanderMalaysia/JohorBahruIstanbulJakartaKolkataKuala LumpurLondonManhattanMexico City

MiamiMilanMumbaiMoscowOxfordParisPuneRockville CentreSan AntonioSão PauloSeoulShanghai

ShenzhenSilicon ValleySingaporeSophia AntipolisSydneyTaipeiTel AvivTokyoTorontoWarsawWashington, DC

Contact

Tel: +65.6890.0999

Email: [email protected]

Website: www.frost.com