from fat profits to hardscrabble? the outlook for china car market 2005-2010 automotive news china...

TRANSCRIPT

From Fat Profits to Hardscrabble? The Outlook for China Car Market 2005-2010

Automotive News China Conference20 April 2005

By

Michael J. DunneAutomotive Resources Asia Ltd.

Automotive News China Conference 2005

Page 2

At the cornerstone of China’s auto industry are the joint ventures that link global auto makers with Chinese partners. As competition intensifies, these relationships will come under pressure like never before.

The Outlook for China Car Market 2005-2010

Increasingly, the Chinese companies are showing signs of a desire for greater independence. That means competing with their partners inside China and for export markets.

Jilin

Liaoning

Shandong

Tianjin

Jiangsu

Beijing

Henan

Hubei

Hunan

Jiangxi

Sichuan

Chongqing

Guangdong

Guangxi

Hainan

Shanghai

Automotive News China Conference 2005

Page 3

USA

DCX Beijing Jeep Corporation, Ltd.

Ford Changan Ford Automobile Corp., Ltd.

GM Jinbei GM Automotive Co.

SAIC-GM-Wuling Automotive Stock Ltd.

Shanghai GM Automotive Co.

SGM Dongyue Automotive Co.

JapanJapan

Honda Guangzhou Honda Automobile Co., Ltd.Dongfeng Honda Motor Co., Ltd.Honda Automobile (China) Co., Ltd.

Mazda FAW Car Co., Ltd.FAW Hainan Automobile Co., Ltd.

Mitsubishi Hunan Changfeng Automobile Manufacture Co., Ltd.Nissan Dongfeng Motor Co., Ltd.

Zhengzhou Nissan Automobile Co., Ltd.Suzuki Chongqing Changan Suzuki Automobile Co., Ltd.

Changhe Suzuki Automobile Co., Ltd.Toyota Tianjin FAW Toyota Automobile Co., Ltd.

Sichuan Toyota Motor Corp.FAW Huali Motor Co., Ltd.FAW Fengyue Automobile Co., Ltd.Guangzhou Toyota Motor Co., Ltd.

South Korea

South Korea

Hyundai Beijing Hyundai Motor Company

Dongfeng Yueda Kia Automobile Co., Ltd.

GermanyGermanyBMW BMW Brilliance Automotive Co., Ltd.VW FAW-Volkswagen Automotive Company Ltd.

Shanghai Volkswagen Automotive Company Ltd.

ItalyItaly

Fiat Nanjing Fiat Co., Ltd.

FranceFrance

PSA Dongfeng Peugeot Citroen Automobile Co., Ltd.

Joint venture automotive companies in ChinaThe Outlook for China Car Market 2005-2010

Automotive News China Conference 2005

Page 4

China’s vehicle demand will climb to 5.8 million units in 2005 and approach 10 million units by 2010.

This projection assumes no interruptions in economic growth and no regulations to limit car population growth, like the quota system here in Shanghai.

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

9,000,000

10,000,000

2000 2001 2002 2003 2004 2005e 2006e 2007e 2008e 2009e 2010e

UnitsHistorical and Projected Vehicle Sales

(2000-2010e)

Passenger cars

Commercial vehicles

Source: Chinese Government and Auto Company Data

The Outlook for China Car Market 2005-2010

Automotive News China Conference 2005

Page 5

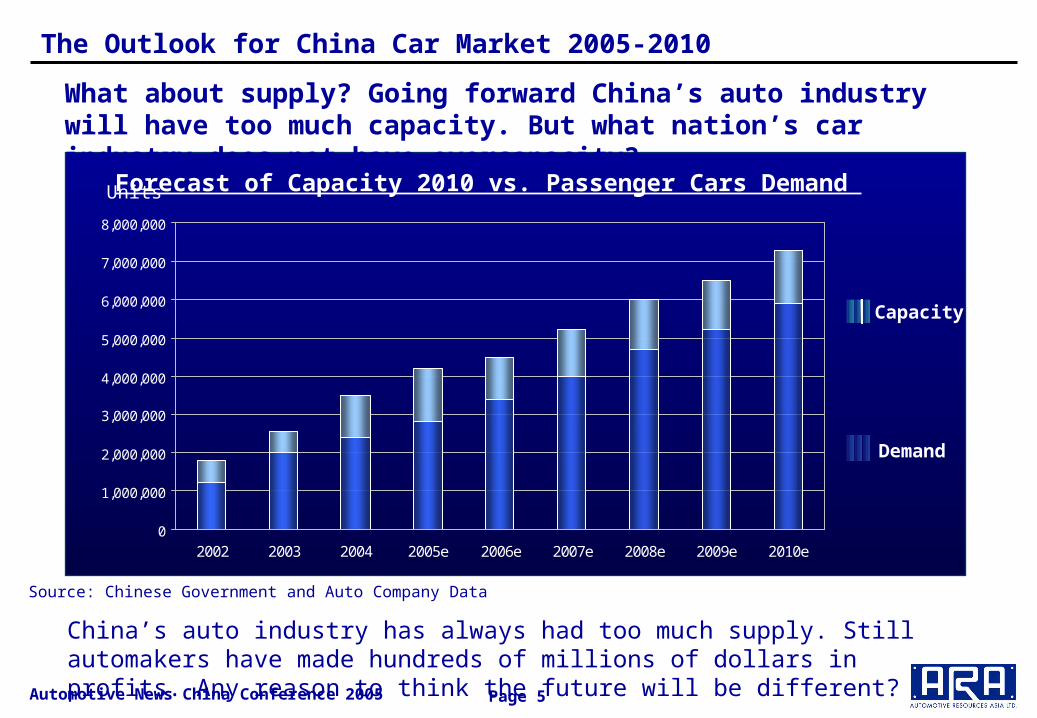

What about supply? Going forward China’s auto industry will have too much capacity. But what nation’s car industry does not have overcapacity?

China’s auto industry has always had too much supply. Still automakers have made hundreds of millions of dollars in profits. Any reason to think the future will be different?

0

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

8,000,000

2002 2003 2004 2005e 2006e 2007e 2008e 2009e 2010e

UnitsForecast of Capacity 2010 vs. Passenger Cars Demand

Demand

Capacity

Source: Chinese Government and Auto Company Data

The Outlook for China Car Market 2005-2010

Automotive News China Conference 2005

Page 6

Think of China’s automotive market in three distinct time intervals. Through 2004 competition has been relatively limited, thanks to regulation.

2005 marks the start of intense competition as Chinese and foreign brands vie for market share.

1985 - 2001 2002 - 2004 2005 - 2010

Halcyon Years The Perfect StormPerfect Competition?

Regulated Oligopoly Explosive Demand Market Share!

The Outlook for China Car Market 2005-2010

Automotive News China Conference 2005

Page 7

There are now more brands producing in China than even in the United States. China’s industry expects 40 new models and variations in 2005 alone.

Average production per model has shifted from 75,000 units per year per model in 2000 to less than 40,000 units per model in 2005. Who produces efficiently at lower volumes?

VW 53%

Honda 5%

Suzuki 8%

Others 7%

Citroen 8%

VW 27%

GM 10%

Honda 8%Hyundai 6%

Daihatsu 5%

Geely 4%

Citroen 4%

Others 16.7%

2000 2002 2004

20

40

60

80

100

27

58

95

No. of new models

1998

14

Year

Market Share 2000 A Rush of New Models Market Share 2004

1

2

3

45

1

2

3

4

5

Chery 4%

Toyota 3%

Kia 3%

FAW 2%

Dong Feng 3%

125

2005

120

140

GM 5%

Daihatsu 14%

The Outlook for China Car Market 2005-2010

Automotive News China Conference 2005

Page 8

What is the impact on prices and profits? Now, China’s price-volume distribution begins to resemble what is normal for developing markets.

Car demand in developing markets reflects incomes distribution: Many have-somes, a small percentage of unusually wealthy and not much in between.

<=US$ 12,000

US$ 12,000-18,000

US$ 18,000-24,000

>US$ 24,000

Share of Cars Priced Under $12,000: China vs. India

0%

20%

40%

60%

80%

100%

03 China 04 China 05e China 05e India

24%

75%

25%

38%

45%

The Outlook for China Car Market 2005-2010

Automotive News China Conference 2005

Page 9

China’s individual buyers - not businesses - will drive growth going forward. Affordability is key. Consider the shifts in the fastest growth segments between 2003 and 2005.

The margin on the Regal was estimated at $3,500 per unit. On the QQ, it’s closer to wood shavings.

Chery QQ (Jan-Feb 2005)

Buick Regal (2003)

Hyundai Elantra (2004)

US$4,000 - US$6,800

US$ 25,000 – US$ 40,700

US$15,000 - US$18,000

Fastest growing segments 2003-2005

The Outlook for China Car Market 2005-2010

Automotive News China Conference 2005

Page 10

Consider the case of Beijing Jeep. In 2003 it launched the Cherokee 2500, set the sticker at an aggressively-low $13,500 and doubled sales. But its success also attracted Chinese competition.

In the first two months of 2005, Beijing Jeep saw the 2500 sales was 158 units. Chinese makers as a group sold 5,304 units.

US$ 10,000

Zhongxing

Shuanghuan:

US$ 13,200

Jeep 2500

US$ 10,000

GreatWall Safe

The Outlook for China Car Market 2005-2010

Automotive News China Conference 2005

Page 11

Upstart Chinese car and parts makers have a cost structure out of line with global producers. Land. Loans. Labor. Health Care.

The real threat to profits in China comes in the form of these risk-taking insurgents.

“In The Club”

“You

ng

Tig

ers”“Y

ou

ng

Tig

ers

”

The Outlook for China Car Market 2005-2010

Automotive News China Conference 2005

Page 12

By 2007, Chery will ship 250,000 cars to North America. And by 2010, the nation will exports $100 billion worth of car parts worldwide.

To put the export target in perspective, parts exports from Japan and Mexico combined are around 80 billion dollars.

250,000 to USA in ‘07

The Next New Chery or a Maxima Clone?

The Outlook for China Car Market 2005-2010

Automotive News China Conference 2005

Page 13

China car exports in 2004 were 9,335 units. Car exports to 2010 will grow at different rates, depending on the producer and the market.

Honda plans to export 50,000 units to Europe from its majority-owned plant. Chery and Geely are signing export contracts will most developing market economies.

Chinese Automakers

Joint Ventures

Majority Owned Companies

Exporters

South AmericaMiddle East

Europe

Southeast Asia

Africa

Japan North America

The Outlook for China Car Market 2005-2010

Automotive News China Conference 2005

Page 14

Automotive parts exports from China reached $7.3 billion in 2004. (In 2005 China by comparison will already export textiles worth $100 billion.)

In 2004, Delphi exported 200 million dollars of parts. Today, most Chinese parts exports are produced in Zhejiang for the after market, not OEMs.

0

20

40

60

80

100

120

2002 2003 2004 2005 2006 2007 2008 2009 2010

Bil

lion

Doll

ars

China Parts Exports 2002 - 2010DriversDrivers

ConstraintsConstraints

1. Survival in China Market2. Global Sourcing

1. Parts & Product Match2. Logistics/Timing

Source: Chinese Government and Auto Company Data

The Outlook for China Car Market 2005-2010

Automotive News China Conference 2005

Page 15

China has the potential to become the most competitive automotive industry in the world. For suppliers and services-based companies looking to fasten a hold here, it is essential to manufacture at low cost going forward.

China’s motorcycle industry experience the same type competitive cycle during the 1990s. Low cost manufacturing is key.

1999 2003

Global40%

Chinese60%

Global98%

To Survive is to Prosper

2005

Global60%

Chinese40%

Chinese2%

China Cell Phones Market

The Outlook for China Car Market 2005-2010

Automotive News China Conference 2005

Page 16

www.auto-resources-asia.com

Bangkok

Suite 1106 Fl. Q. House Bldg.

66 Soi Asoke Sukhumvit 21 Road

Bangkok 10110

Thailand

Tel: 662 264 2050

Fax: 662 264 2051

Beijing

Suite 1026 Changan Bldg.

7 Jianguomennei Ave.

Beijing 100005

China

Tel: 8610 6510 1686

Fax: 8610 6510 1685

Shanghai

Suite 3557 CITIC Square Bldg.

1168 Nanjing Road West

Shanghai 200041

China

Tel: 8621 5292 5211

Fax: 8621 5252 4616

Thank You