fred.olsen production asa - finansanalytiker · 24 months share price development of the fpso...

TRANSCRIPT

Fred.Olsen Production ASA

NFF conference 30th September 2010

THE COMPANY

“Who we are”

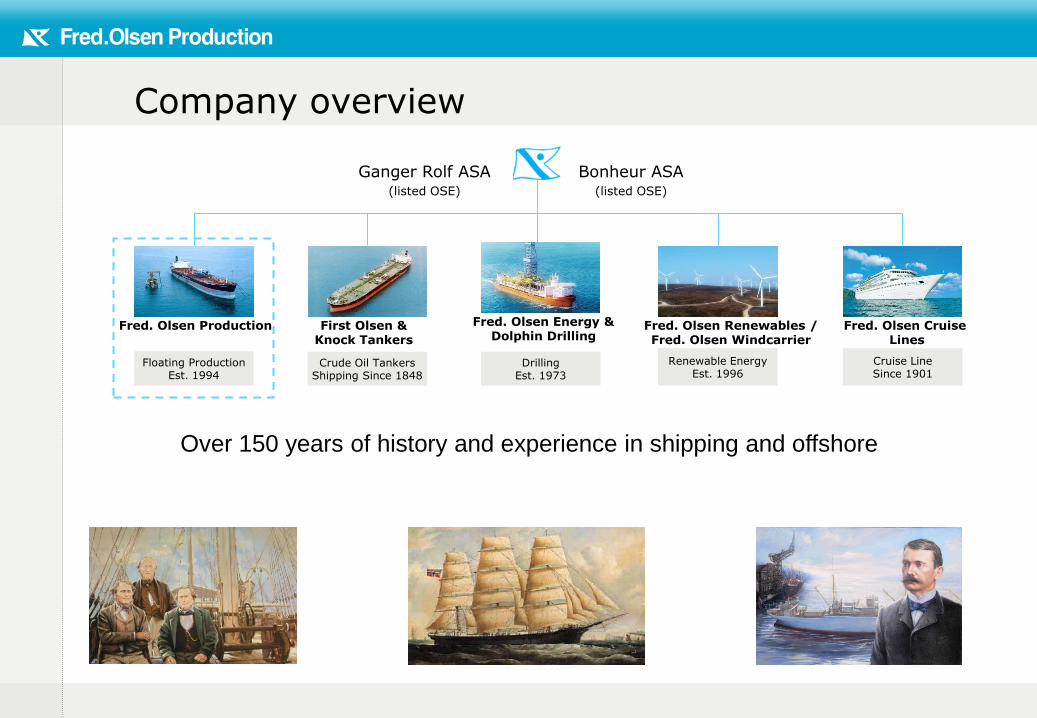

Company overview

Floating ProductionEst. 1994

Ganger Rolf ASA(listed OSE)

Bonheur ASA(listed OSE)

Cruise LineSince 1901

Renewable EnergyEst. 1996

Crude Oil TankersShipping Since 1848

DrillingEst. 1973

Fred. Olsen Production First Olsen &Knock Tankers

Fred. Olsen Energy &Dolphin Drilling

Fred. Olsen Renewables / Fred. Olsen Windcarrier

Fred. Olsen CruiseLines

Over 150 years of history and experience in shipping and offshore

Fred. Olsen Production – in brief

• Established FPS contractor since 1994

• Strong track record – 10 projects delivered

• Fleet of 4 production units:

– 3 FPSO’s

– 1 MOPU operation

• Top tier uptime performance

• Strong HSE performance

• FOP/FOM: ISO 9001, 14001 and 18001

• Approx. 450 personnel

• Core business in West Africa; worldwide presence

Track record

FSO ConversionKnock Taggart

Abacam - Nigeria

FSO ConversionKnock Nevis

Maersk - Qatar

FSO ConversionKnock Dee Soekor - SA

FPSO ConversionKnock TaggartAddax - Nigeria

FPSO UpgradePetróleo NautipaVaalco - Gabon

2009200820072006200520042003200220012000199919981997199619951994 2010

Jack-Up UpgradeBorgen Dolphin/Marc LorenceauAddax - Nigeria

Jack-Up ConversionBorgen Dolphin MOPU

Mobil Oil - Nigeria

FPSO ConversionPetróleo Nautipa

Ranger Oil - Angola

FPSO ConversionKnock Allan

CNR – Gabon

FPSO ConversionKnock Adoon

Addax - Nigeria

OPERATION

“What we do”

Current fleet & offices

Houston

Nigeria

Gabon

Oslo

Singapore

OfficeUnit

Port Harcourt

Port Gentil

Knock AllanFPSO Oil: 25,000 BOPDGas: 80 MMCFDPower 2 x 27MW

Knock AdoonFPSOOil: 60’000 BOPDGas: 10 MMCFDWI: 100’000 BWPD

Knock MuirAframax 93 builtTrading tanker in The Far East/India range

Petróleo NautipaFPSO (50% owned)Oil: 30,000 BOPDGas: 10 MMCFD

Marc LorenceauMOPU (management)Oil: 40,000 BOPDGas: 70 MMCFD

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Petroléo Nautipa

Knock Adoon

Knock Allan

Knock Muir

Marc Lorenceau

Long term contracted cashflow

Addax Petroleum - Nigeria 8y option

Addax (operations)

Vaalco - Gabon 2y option

Upgrade / Conversion

Option

Call-off option

Canadian Natural Resources – Gabon – 10 yrs (10y option)

Operations

Short term tanker T/C / Spot market

Upside potential for existing contracts

Etame Marine block; Gabon – FPSO Petróleo Nautipa

Field production horizon now extends past 2017; 2021 is likely

OML 123 block; Nigeria – FPSO Knock Adoon

Sinopec acquired Addax Petroleum August 2009

Additional reserves sanctioned to be developed through Knock Adoon

Further potential reserves being evaluated for tie-back

Field production horizon is beyond 2018

Olowi block; Gabon – FPSO Knock Allan

Platform B and C on stream; B is in line with expectations and promising

Drilling program for platform A and D expected to finish by 1Q 2011

Recoverable reserves stands at 50 million, to be reassessed when drilling program completed and results evaluated

Operational performance summary

Robust HSE performance

Excellent uptime record

Advantages from combination of maritime and offshore cultures

Vessel management and operation by Fred. Olsen Marine Services (FOM)

Full & effective integration of local staff in onshore and offshore organisation (up to 90% local staff on some units)

FINANCIALS

Financial snapshot

1H 2010 2009 2008

Turnover/revenue 57,9 115,0 80,9

EBITDA 26,4 50,7 30,7

Total assets 491,9 554,7 523,5

Book equity 249,3 264,6 263,3

Market capitalization 157,2 130,2 65,1

Enterprise value 296,3 257,1 191,1

USD million

EBITDA-margin 45,6 % 44,1 % 37,9 %

EV/EBITDA *) 5,6 5,1 6,2

*) EBITDA annualized 2010

24 months share price development of the FPSO companies listed in Oslo and the Oslo stock exchange benchmark. Indexed to 100 %

Financial multiples – listed FPSO operators

FPSO companies Market cap EV EBITDA

Ticker (USDm) (USDm) 2012E 2010E 2011E 2012E

SBM Offshore 2 829 4 525 771 2,7 2,7 2,6

BWO/PROD merged 1 166 2 630 537 3,6 2,8 2,2

Modec 703 1 091

BWO (consensus pre APL sale and merger) 757 1 223 315 2,8 2,2 1,5

Sevan 571 1 840 300 11,9 7,2 4,7

Prod (pre merger) 616 1 498 228 3,7 2,9 2,3

FOP 161 268 46 2,2 1,5 0,7

AKFP 16 756 102 7,8 6,8 6,1

Source: First Securities, Factset

NIBD/EBITDA (x)

THE FPSO MARKET

“..and where do we fit?”

Market Demand

Looking back (last 12 months):

Second half 2009: contract awards pick-up but mainly delayed projects – not a trend

First half 2010 contract activity (9 awards total):

Turn-key deliveries (EPC) – 2

Leases – 2

Redeployment – 5

Opportunities in mid-range (FOP) segment are presently limited –expected to pick up later in 2010; FOP is not in EPC market

General outlook:

External forecasts are back to 2007 levels (16-20+ per year)

Mix of projects is split 50%/20%/30% lease/redeploy/turnkey

Recovery from 2008 financial crisis is evident, including access to financing

Africa, now finally picking up (FOP “backyard”)

Market Supply

Vessel supply:

Speculative FPSO owners now out of the market. If not already on contract, likely to remain unused

Increased scrapping trend of older units (FOP, SBM, Modec, Oceaneering)

Redeployment has picked up but almost entirely on shorter contracts (5y or less)

9 vessels with contract ending in 2010, unless extended; of these 4 are 1970’s and all are 25 years old or older; further scrapping is likely

Competitive Picture:

Competitive field is reduced due to bankruptcies and retrenchment due to refinancing

Increased openings for raising capital, refinancing ongoing

No firm evidence of increased pricing discipline

Market is also segregating…… (see following slides)

Market segregation

The FPSO market is segregating into three main categories:

Top-end mega-projects (e.g. sub-salt in Brazil):

Capital intensive (CAPEX > $750 mill)

Highly complex vessels, high project execution risk

Resource intensive – large in-house teams

Mid range:

(Less) capital intensive ($250-700 mill)

Clients with balance sheet to match commitments

Complex but more flexible project execution model

Low end :

Short contract commitment

Increased residual value risk

Client credit risk

Segregation impacts – top-end

Strong growth in mega-projects (CAPEX > $750mill)

Only top-tier contractors can compete : SBM, Modec; BWO-PROD;

Driving consolidation at top end

Need for strong financial partners

Unique commercial challenges for these projects:

Longer contracts

Vessels likely to operate on single contract only

Reduced extension upside

New accounting model for leases (Exposure Draft 17. august 2010 by

IASB/FASB) – imply financial lease on the balance sheet for clients

Local content requirements increasingly onerous

EPC deliveries more and more common

Limited number of contractors, but major oil company clients maintain tight control of margins and commercial terms

Hypothesis 1– top-end: high value, high volume, lower margin, medium risk (if good project control in place – otherwise high), capital intensive projects. The major players need them and have to grow & adapt accordingly.

Segregation impacts – low-end

At the other end of the scale:

Low-end projects have been absent from the market:

Small fields with limited reserves, significant oil-price sensitivity

Clients without sufficient financing/balance sheet –counterparty risk

Shorter commitment (client financiers restriction) conflicts with financing needs/residual value risk of contractor

Result is either limited development in this segment or higher risk contracts (financier, contractor and client risk).

This niche used to be the “breeding ground” of FPSO start-ups, but is now the preserve of private equity or single vessel companies.

Hypothesis 2 – low-end: High risk contracts with comparatively higher margins but tempered by high residual value risk wiping out all value

Segregation impacts – mid range

Mid-range:

Capital requirement and complexity are a hurdle to entry for new contractors

Track record and financial standing are important

Balanced risk profile – opportunity to utilize effective risk sharing between contractor and client.

Lease model adds value - contractor is a key element to facilitating project sanction

Medium duration fixed term contracts, more emphasize on option years with contractor upside in reserve development, new tie-ins and/or oil price and production bonuses

Limited competitive field unless the top-tier companies “drop down” due to lack of top-end work

Hypothesis 3 – mid range: Balanced risk provided project control is in place. Robust margins if bidding is selective. Greater potential for growth/contract extension. The place to be?

Source: Fearnley Offshore

FPSO Operators

Outlook

Good prospects for new projects in 2011 as Africa also recovers

FOP has actively pursued Asian projects and remains well positioned

FOP positioned in mid range segment

Existing contracts have strong potential to add value

Fred. Olsen Production ASA:

Long term cash flow

Excellent operational track record

Cost efficient operation, tight cost control

Asset portfolio tidied-up in 2009/10

Trading Aframax tanker as FPSO/FSO conversion candidate

Attractive long term financing in place

Low balance sheet gearing

Strategic and financial partner in place

Well positioned to expand portfolio in mid range segment

Market value 60% of book value

Favorable financial multiples compared to other FPSO operators

A partner in a consolidation case?