frauds_northern exposure

TRANSCRIPT

8/11/2019 Frauds_Northern Exposure

http://slidepdf.com/reader/full/fraudsnorthern-exposure 1/32

Fraud Theories-Analysis

Awadhoot ApteChandni Thapar

8/11/2019 Frauds_Northern Exposure

http://slidepdf.com/reader/full/fraudsnorthern-exposure 2/32

• The intentional misrepresentation or alteration of accountingrecords regarding sales, revenues, expenses and other factors for

a profit motive such as inflating company stock values, obtainingmore favourable financing or avoiding debt obligations.

• Employees who commit accounting fraud at the request oftheir employers are subject to personal criminal prosecution.

8/11/2019 Frauds_Northern Exposure

http://slidepdf.com/reader/full/fraudsnorthern-exposure 3/32

CASH

• Most often stolen by dishonest employees.

• Target cash as it enters or leaves the business

•

Inadequate cash flow controls• Understanding these controls

8/11/2019 Frauds_Northern Exposure

http://slidepdf.com/reader/full/fraudsnorthern-exposure 4/32

FRAUDS

ON-BOOKFRAUDS

OFF-BOOKFRAUDS

8/11/2019 Frauds_Northern Exposure

http://slidepdf.com/reader/full/fraudsnorthern-exposure 5/32

• Theft of cash after it has appeared on a company’sbooks

• Examination of the victim company’s records can easily

reveal the cash shortageCASH LARCENY SCHEMES• Intentional taking away of an employer’s cash without

the consent and against the will of the employer.•

Can occur under any circumstance where an employeehas access to cash :At the point of saleFrom incoming receivables

From the victim organization’s bank deposits

8/11/2019 Frauds_Northern Exposure

http://slidepdf.com/reader/full/fraudsnorthern-exposure 6/32

ON-BOOK FRAUDS

BILLINGSCHEMES PAYROLLSCHEMESEXPENSEREIMBURSEMENTSCHEMES

CHEQUETAMPERING

SCHEMESREGISTERDISBURSEMENTSCHEMES

8/11/2019 Frauds_Northern Exposure

http://slidepdf.com/reader/full/fraudsnorthern-exposure 7/32

• Fraud aimed at the payments system of a business.• Manipulate that system and cause the business to make

a fraudulent payment to the employee.

TYPES OF BILLING SCHEMES :• Shell company schemes• Pass-through schemes•

Pay-and-return schemes• Personal-purchase schemes

8/11/2019 Frauds_Northern Exposure

http://slidepdf.com/reader/full/fraudsnorthern-exposure 8/32

• Segregation of duties

Before approving a new vendor, its legitimacy should be evaluatedby:

Obtaining its corporate records and other relevant documentsChecking its credit ratingConfirming that it is listed in telephone directoriesContacting its references from clients and othersBeing particularly cautious about a vendor with a post-office boxaddress or a name composed entirely of initials.

•

Determining whether its business address matches anyemployee’s home address Once the company approves a new vendor, the account should beclosely monitored by:

Watching for increases in the amount or frequency of billingsObserving variances from budgets or projectionsComparing its prices with those charged by other sources

8/11/2019 Frauds_Northern Exposure

http://slidepdf.com/reader/full/fraudsnorthern-exposure 9/32

• Can take place in any kind of business that issuespayroll checks to employees.

•

Employee causes his or her employer to issue apayment by making false claims for compensation.

FALSIFIED WAGES INVOLVES :• Employees claiming compensation for hours not

worked or falsifying their timesheets or timecards insome fashion.

• Manipulating the rates of pay or the hours worked.• Pay themselves bonuses when none are warranted.

8/11/2019 Frauds_Northern Exposure

http://slidepdf.com/reader/full/fraudsnorthern-exposure 10/32

• Sophisticated time clocks or systems that require aunique employee pass code to be entered whenclocking in.

•

Executive approval of all bonus-type compensation.• Mandatory vacations for those with payroll

responsibilities with another employee performingthis function in their absence.

• Executive approval of all pay checks.• The ability to modify wage rates, add employees, etc.

within the system should be restricted to only thosenecessary. These individuals should have their recordsperiodically reviewed.

8/11/2019 Frauds_Northern Exposure

http://slidepdf.com/reader/full/fraudsnorthern-exposure 11/32

• Employees are reimbursed for expenses paid on behalf ofthe employer

• Airfare, hotel bills, business meals, mileage, ground

transportation and so on• Business purpose explained and receipts attached per the

organization’s guidelines

FOUR MAJOR VARIANCES TO THESE SCHEMES:• Mischaracterized Expense Claims• Inflated Expense Claims• False Expense Claims• Multiple reimbursements

8/11/2019 Frauds_Northern Exposure

http://slidepdf.com/reader/full/fraudsnorthern-exposure 12/32

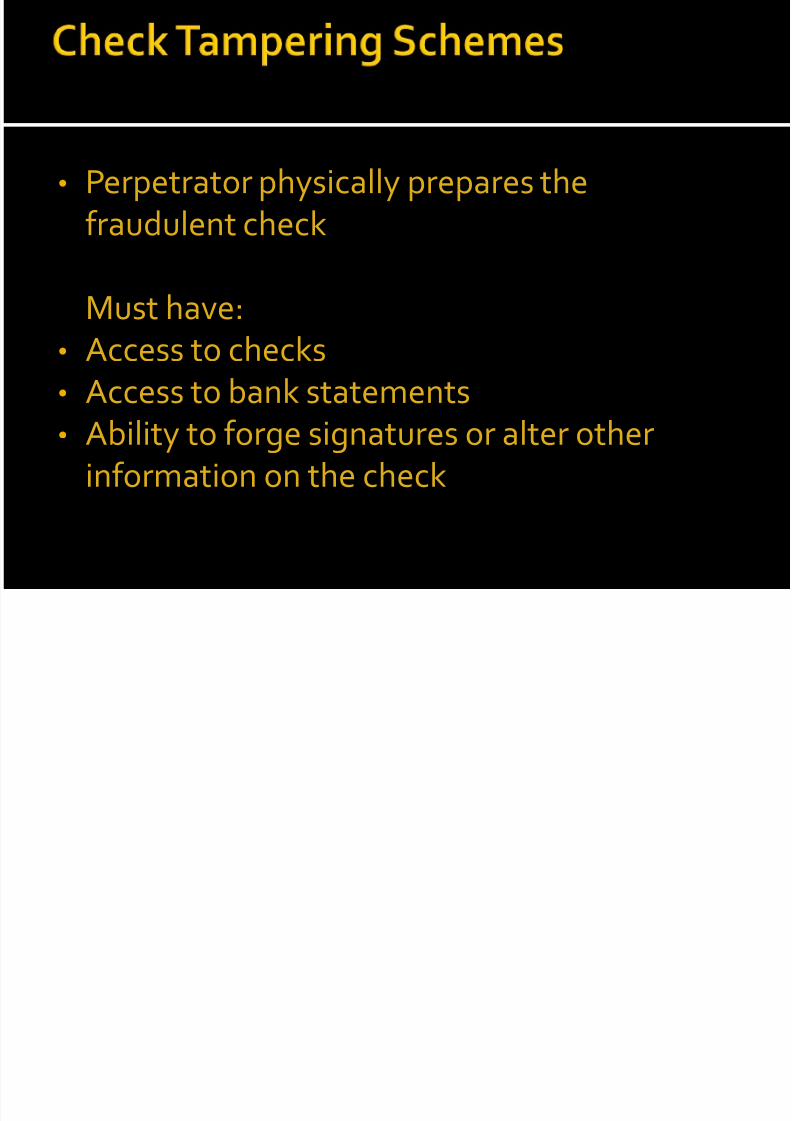

• Perpetrator physically prepares thefraudulent check

Must have:• Access to checks• Access to bank statements• Ability to forge signatures or alter other

information on the check

8/11/2019 Frauds_Northern Exposure

http://slidepdf.com/reader/full/fraudsnorthern-exposure 13/32

CHECK TAMPERING SCHEMES INCLUDE:

• Forged maker schemes, which involve forging anauthorized signature on a company check

• Forged endorsement schemes, which consist of forgingthe signature endorsement of an intended recipient of acompany check

• Altered payee schemes, which involve changing the payee

designation on the check to the perpetrator or anaccomplice• Authorized maker schemes, which occur when employees

with signature authority write fraudulent checks for theirown benefit

8/11/2019 Frauds_Northern Exposure

http://slidepdf.com/reader/full/fraudsnorthern-exposure 14/32

• Nonexistent employees are added to the payrolland another employee benefits by receiving theirwages.

• Ghost employees may never have existed, or theymay no longer be current employees of theorganization, but are intentionally left on the

payroll.• Typically more prevalent in larger organizationswith large numbers of employees and weak internalcontrols.

8/11/2019 Frauds_Northern Exposure

http://slidepdf.com/reader/full/fraudsnorthern-exposure 15/32

• Periodic payroll audits in which all employees have tophysically sign and show proper identification to receivetheir pay check.

•

Cross-reference the payroll roster for duplicate addresses orSocial Security numbers.• Verify Social Security numbers with the Social Security

Administration.• Randomly inspect your payroll database for employees with

P.O. boxes or those with no deductions (i.e., healthcare,state/fed withholdings).

• Require direct mailing of checks or have managementdistribute them physically to employees.

8/11/2019 Frauds_Northern Exposure

http://slidepdf.com/reader/full/fraudsnorthern-exposure 16/32

• Refunds and voided sales are transactions processed atthe register when a customer returns an item ofmerchandise purchased from that store. The transactionentered on the register indicates the merchandise is beingreplaced in the store‘s inventory and the purchase price isbeing returned to the customer. In other words, a refundor void shows a disbursement of money from the registeras the customer gets his money back.

• Since these schemes appear on the books as legitimate

disbursements of funds from the cash register, they areclassified as fraudulent disbursements.• In practice, an employee physically removes cash from his

cash register and absconds with it. In that respect, suchschemes are very similar to cash larceny schemes.

8/11/2019 Frauds_Northern Exposure

http://slidepdf.com/reader/full/fraudsnorthern-exposure 17/32

OFF-BOOKFRAUD

SCHEMES

SKIMMING UNRECORDEDSALES

UNDERSTATEDSALES AND

RECEIVABLES

THEFT OFCHEQUES

THROUGH THEMAIL

8/11/2019 Frauds_Northern Exposure

http://slidepdf.com/reader/full/fraudsnorthern-exposure 18/32

• Cash is removed from the entity before it enters theaccounting system.

• Receipt of the cash is never reported to the entity.

The most common skimming schemes are:• Unrecorded sales• Understated sales• Theft of incoming check• Swapping checks for cash• Theft of cash from a victim entity prior to its entry in an

accounting system• No direct audit trail• Its principal advantage is its difficulty to detect

8/11/2019 Frauds_Northern Exposure

http://slidepdf.com/reader/full/fraudsnorthern-exposure 19/32

SALES SKIMMING• Employee makes a sale of goods or services, collects the

payment, and makes no record of the transaction• Pockets the proceeds of the sale• Without a record of the sale, there is no audit trailCash

register manipulation• “No Sale” or other non -cash transaction is recorded• Cash registers are rigged so that sales are not recorded on

the register tapes• No receipt is issued

AFTER HOURS SALES• Sales are conducted during non-business hours without the

knowledge of the owners

SKIMMING

8/11/2019 Frauds_Northern Exposure

http://slidepdf.com/reader/full/fraudsnorthern-exposure 20/32

SKIMMING BY OFF-SITE EMPLOYEES• Independent salespeople• Employees at remote locations – branches or satellite offices away

from the primary business site• Poor collection procedures

UNDERSTATED SALES• Sales is recorded for a lower amount than was collected• Sales item is reduced in price or the number of units sold

THEFT IN THE MAIL ROOM– INCOMING CHECKS• Incoming checks are stolen and cashed• Customer’s account is not posted

SKIMMING

8/11/2019 Frauds_Northern Exposure

http://slidepdf.com/reader/full/fraudsnorthern-exposure 21/32

• Illegal copying of information from the mag netic strip of a credit or ATMcard. It is a more direct version of a phishing scam.

• The scammers try to steal your details so they can access your accounts.Once scammers have skimmed your card, they can create a fake or‘cloned’ card with your details on it. The scammer is then able to run up

charges on your account.• A way for scammers to steal your identity (your personal details) and useit to commit identity fraud. By stealing your personal details and accountnumbers the scammer may be able to borrow money or take out loans inyour name.SAFETY

• Keep your credit card and ATM cards safe. Do not share your personalidentity number (PIN) with anyone. Do not keep any written copy of yourPIN with the card.

• Check your bank account and credit card statements when you get them.If you see a transaction you cannot explain, report it to your credit unionor bank.

• Choose passwords that would be difficult for anyone else to guess.

SKIMMING

8/11/2019 Frauds_Northern Exposure

http://slidepdf.com/reader/full/fraudsnorthern-exposure 22/32

8/11/2019 Frauds_Northern Exposure

http://slidepdf.com/reader/full/fraudsnorthern-exposure 23/32

Gentlemen's Club featuringexotic dancers

Primary source of revenueCover ChargesSale from food and

beveragesOnly legally operating bar

offering such service- Nocompetition

8/11/2019 Frauds_Northern Exposure

http://slidepdf.com/reader/full/fraudsnorthern-exposure 24/32

Responsibility:Servers:

To serve food andbeverages

Bartenders:To provide Servers

per orderRegister sales in cash

register

Responsibility:Count the cash,

close cash register

Deposit the cash

Responsibility:Ownership

Overview of business

LarrySwenson Manager-Besty Smith

Server

Bartender

8/11/2019 Frauds_Northern Exposure

http://slidepdf.com/reader/full/fraudsnorthern-exposure 25/32

Cover Charges of $6 were charge per customer forentrance

Customer placed order with servers for food, Beer and

beveragesServer has $40 cash at the beginning of shift$3 for beer to bartender and charge customer $4 eachFood item charge to customer $12.5

Server shall return $40 at end of shiftAll transactions were carried in cash

8/11/2019 Frauds_Northern Exposure

http://slidepdf.com/reader/full/fraudsnorthern-exposure 26/32

Per Cost-Volume-Profit analysis:Profit Margin: 35% at least

At actual Profit Margin was mere 10%Total estimated loss: $379974/year

Items Sales($)

Cost ofSales($)

SalesMarkup (%)

EstimatedFraud

Actual Beer 853448 228972 373

Food 40753 51726 79

Budget Beer 1144860

228972 500 291412

Food 129315 51726 250 88562

0

100000

200000

300000

400000

500000

600000

700000

800000

900000

1000000

1100000

1200000

1300000

Beer Food

Fraud Size

Actual Fraud

8/11/2019 Frauds_Northern Exposure

http://slidepdf.com/reader/full/fraudsnorthern-exposure 27/32

On-Book Fraud(Cash Larceny)

Off-Book Fraud(Skimming)

Manager can steal part ofdeposits

Employees collecting $6 ascover charges either pocketsome money or allowed freeadmission to acquaintances

Anyone having access to cashregister can steal money from

it

Servers and bartenders couldget drinks for customers and

do not ring them in cashregister as sale and pocket itall instead

8/11/2019 Frauds_Northern Exposure

http://slidepdf.com/reader/full/fraudsnorthern-exposure 28/32

Financial statement analysis:Total estimated loss: $379974/year

Undercover Surveillance:40-Hrs in a weekRevealed that 90% of employees were stealing cash

including managerInvigilation:

Revenue generated in week during invigilation period:$30,960

Previous Week revenue: $25,775Annual week average: $22,006

Total loss due to skimming: $259,250 to $447,700 per year

8/11/2019 Frauds_Northern Exposure

http://slidepdf.com/reader/full/fraudsnorthern-exposure 29/32

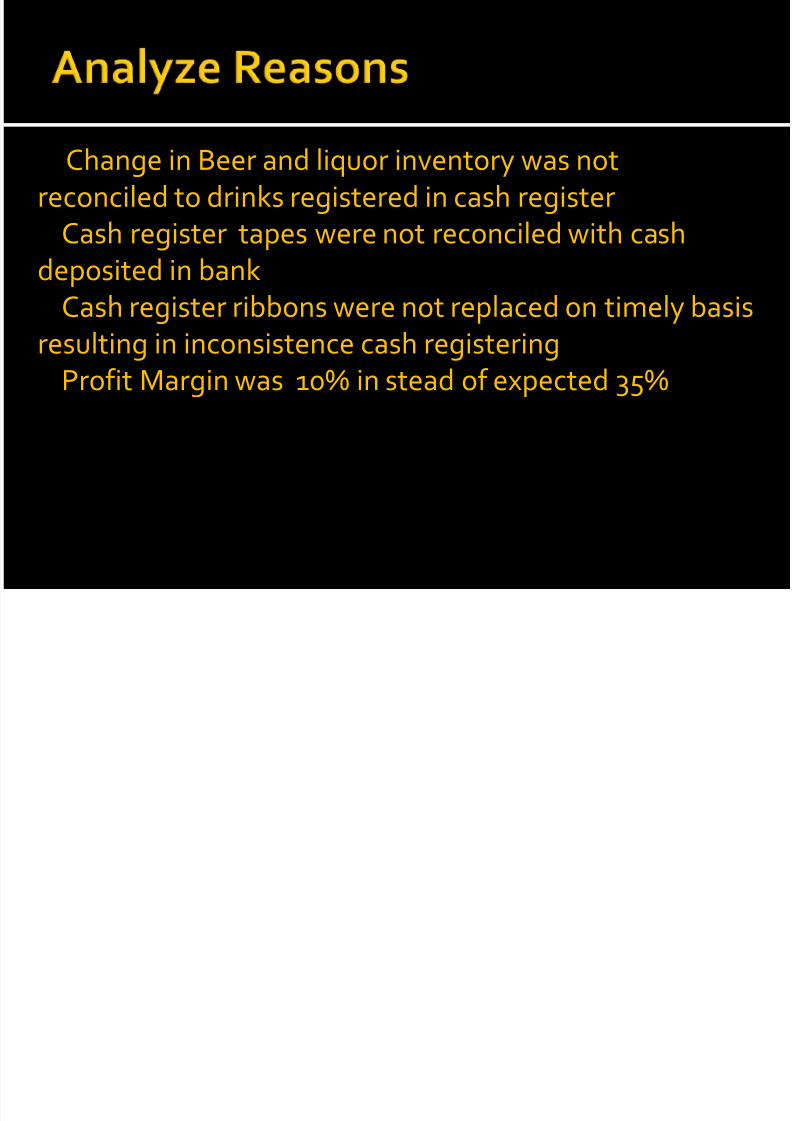

Change in Beer and liquor inventory was notreconciled to drinks registered in cash register

Cash register tapes were not reconciled with cash

deposited in bankCash register ribbons were not replaced on timely basisresulting in inconsistence cash registering

Profit Margin was 10% in stead of expected 35%

8/11/2019 Frauds_Northern Exposure

http://slidepdf.com/reader/full/fraudsnorthern-exposure 30/32

Access to alcohol and beer limited to head bartenderresponsible for shortage

Change in inventory to be reconciled with cash registerCash register and bank deposits to be checked by general

managerEmployee hotline to report any fraudSurveillance cameras at cash registersSurprise audits, Undercover surveillance, Interviews with

employeesAdditional Recommendation:Entry pass system for admission (Can be online/ offline)

8/11/2019 Frauds_Northern Exposure

http://slidepdf.com/reader/full/fraudsnorthern-exposure 31/32

All though businesses are vulnerable to Frauds, it can bedetected and prevented with investigative techniques andcareful control over the cash and other assets.

8/11/2019 Frauds_Northern Exposure

http://slidepdf.com/reader/full/fraudsnorthern-exposure 32/32

THANK YOU