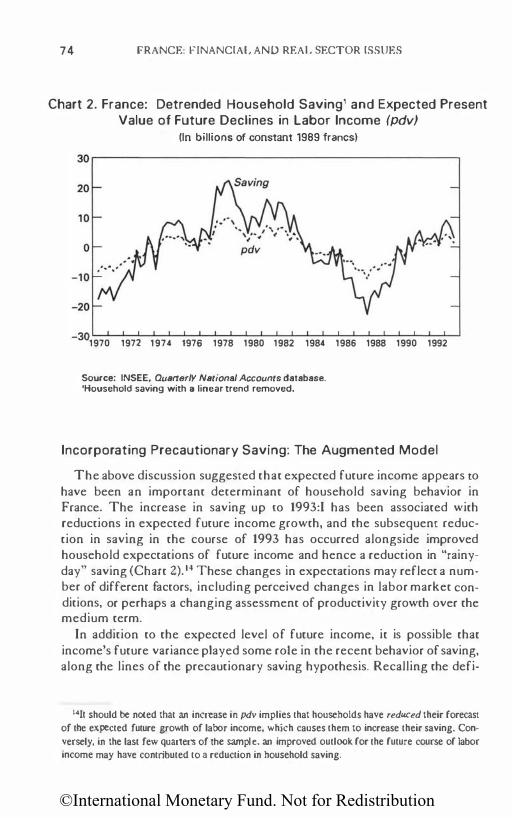

france - elibrary.imf.org...clude that the positive response of saving to interest rate increases...

TRANSCRIPT

©International Monetary Fund. Not for Redistribution

France

Financial and Real Sector Issues

©International Monetary Fund. Not for Redistribution

lhispage intentionally left hlank

©International Monetary Fund. Not for Redistribution

France

Financial and Real Sector Issues

Edited by Paul R. Masson

International Monetary Fund Washington • 1995

©International Monetary Fund. Not for Redistribution

© 1995 International Monetary Fund

Book design and production by IMF Graphics Section

Library of Congress Cataloging-in-Publication Data

France, financial and real sector issues I edited by Paul R. Masson. p. em.

Includes bilbiographical references. ISBN 1-55775-491-8 I. France-Economic policy-1981- 2. Finance, Public-France.

I. Masson, Paul R. HC276.3.F735 1995 330.994'0839-dc20

Price: US$24.00

Please send orders to: International Monetary Fund, Publication Services

700 19th Street, N.W., Washington, D.C. 20431 U.S.A. Tel.: (202) 623-7430 Telefax: (202) 623-7201

Internet: [email protected]

95-40587 CIP

©International Monetary Fund. Not for Redistribution

Contents

Acknowledgments . . . . ." . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . vii

Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

1. Why Is Unemployment in France So High? 6 Rezo Moghodom

2. Household Saving in France: Stochastic Income and Financial Deregulation . . . . . . . . . . . . . . . . . . . . . . . . . . 65 Jonotho11 D. Ostry and Jooquim Levy

3. The Link Between Real Interest Rates and French Aggregate Private Investment. . . . . . . . . . . . . . . . . . . . . 88 Mark Toy/or

4. ERM Money Supplies and the Transition to EMU . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 112 Moree/ Cossord, Timothy Ltmc, and Paul R. Masson

5. The Taxation of Returns from Personal Savings in France . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 146 Gory O'Collaghan

6. Some Considerations Relevant to Prefunded Pensions in France . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 173 Joaquim Levy

Glossary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 207

v

©International Monetary Fund. Not for Redistribution

lhispage intentionally left hlank

©International Monetary Fund. Not for Redistribution

Acknowledgments

D he work undertaken here was the result of a joint effort of the mission teams working on France, and the authors of these studies are

graceful for the advice and encouragement of their colleagues. First and foremost, thanks are due to Massimo Russo, Director of the European I Department, who influenced the topics undertaken, headed the missions to France in 1993-94, and supported the initiative of publishing these studies in a book. Michael Deppler also had many useful comments in the light of his past responsibility for work on France. Claude Bismut contributed to these studies with numerous comments and suggestions, as did various officials in Paris. However, the analysis reported here is the responsibility of the authors themselves, and does not necessarily represent the views of the Fund or other official institUtions. Simon Willson of the External Relations Department of the IMF edited the manuscript for publication and coordinated production.

We are also grateful to Aline Clark, Nahid Mejib, and Rosalind Oliver for their conscientious and good-nacured preparation of the texts, and to Susan Becker and Kote Nikoi for statistical assistance.

Paul R. Masson

vii

©International Monetary Fund. Not for Redistribution

lhispage intentionally left hlank

©International Monetary Fund. Not for Redistribution

Introduction

1':1 ranee has undergone major transformations over the past decade . .. The French economy, formerly plagued by persistent inflation and frequent devaluations, has achieved a degree of price and exchange rate stability similar to Germany's. The past decade has, in general, also been characterized by a return to fiscal rectitude in France, after the expansionary policies of the early 1980s. However, the recent recession has highlighted some severe structural problems. Most seriously, the unemployment rate has risen co levels that were previously unknown in postwar France. Moreover, the decline in real growth from the abnormally high levels of the lace 1980s revealed serious fiscal imbalances chat go beyond merely cyclical deficits.

Clearly, France faces major challenges as it enters the second half of chis decade. One is the integration of the French economy with chose of its European Union (EU) neighbors. To some extent, it is appropriate co sec this as a continuation of a long-term trend that began soon after the Second World War with the formation of the European Payments Union and the European Coal and Steel Community, and the subsequent signing of the Treaty of Rome. However, it must also be recognized that the next major step envisaged, full economic and monetary union (EMU), would represent a dramatic break with the existing regime, in which EU members retain primary control over the levers of macroeconomic policy. A successful transition to a European monetary policy will require that the economies of the member countries develop increased flexibility co substitUte for the ability to run a national monetary policy-notwithstanding the fact that this degree of freedom has not always been used co good effect.

The need for structural changes to enhance the economy's flexibility is made more pressing by not only the starting point of high unemployment, but also by constraints on the possibility of providing further subsidies or tax incentives for employment. The situation of the public finances-a general government deficit equal ro 6 percent of GOP in 1994, and a debt-to-GOP ratio that, though lower than in many of France's partners,

©International Monetary Fund. Not for Redistribution

2 FRANCE: FINANCIAL AND REAL SECTOR ISSUES

has risen alarmingly in recent years-precludes measures that would further widen the deficit. This is especially so given the context of the Maastricht Treacy: to qualify for EMU, a country must reduce its deficit below 3 percent of GOP (barring exceptional circumstances) and keep it under that ceiling thereafter. From a medium- to long-term perspective, moreover, there are worrisome tendencies related co demographic trends chat will tend to widen deficits, especially those of the social security accounts.

Unemployment is the most serious symptom of France's structural problems. l t is clear chat the high level of social chatges provides a disincentive to hiring workers, especially at low skill levels. It is also widely accepted among economists chat the relatively high minimum wage discourages hiring of some workers. To some extent, the French Government has begun co replace social charges on labor income with a broader tax on all incomes. However, the scope for reducing the tax wedge on labor income is constrained by the fact chat labor income is such a large fraction of national income, and because capital, being mobile, is difficult to tax. Given budgetary constraints, France will therefore have to build a consensus in favor of addressing structural problems by reducing social benefits and cutting back on government expenditures generally, while at the same time creating room for maneuver to reduce tax disincentives. As for the minimum wage, an attempt co reduce it for younger workers ran into widespread opposition, and this issue has become highly politicized.

The chapters that follow attempt to shed some light on these policy challenges. They were prepared as background for the 1993 and 1994 Article IV consultations with France, and have not been updated with the most recent data. However, the issues considered are still important to French policy, and the analysis contained in the studies remains valid .

•••

The first chapter, by Reza Moghadam, is an in-depth study of the causes of French unemployment and its possible remedies. The fact chat unemployment has ratcheted up over the past decade, not falling much below 9 percent even in the boom years of 1988-89, argues that high unemployment in France is a structural, not a cyclical, phenomenon. Moghadam presents evidence on the contributions of French employers to social charges-which constitute part of the tax wedge making the cost to the employer greater than the employee's remuneration; these are very high, even compared with other European countries. Empirical relationships linking long-run or structural unemployment to the employers' tax wedge and the real value of the minimum wage are presented.

©International Monetary Fund. Not for Redistribution

171trotlucrion 3

Moghadam concludes that these factors must be addressed in order to achieve a durable solution to France's unemployment problem.

The second chapter, by Jonathan Osrry and joaquim Levy, anempts to explain trends in household saving; as a ratio co disposable income, it exhibited a steady decline over the 1980s, and then rose by 4 percentage points, reaching 14 percent in 1993. Since weak consumer demand was one of the causes of the 1993 recession, discovering its causes was important ro assess the prospects for recovery. From a longer-term perspective, household saving provides a large source of funds for domestic investment, and hence will influence the economy's ability to invest profitably withour resort to foreign saving.

The authors first examine whether the fall in consumption in the early 1990s reflected precautionary saving resulting from the greater perceived riskines,; of future income. While they find some evidence that the variance of innovations to income affects saving, the impact is much smaller than rhc traditional effect of expected future income. The authors proceed ro rest a broader set of explanations of saving behavior. The most striking finding is the important role of financial deregulation during the 1980s, which encouraged household borrowing. The aurhors also conclude that the positive response of saving to interest rate increases has been permanently enhanced as a result.

The interest elasticity of investment is the subject of the next chapter, by Mark Taylor. In France, researchers have long found it difficult ro identify any separate effect of interest rates on the level of investment, which seemed to follow changes in income as predicted by the accelerator model of investment. Such a result was justified by appeal to a zero elasticity of substitution between the factors of production, which would leave no room for relative factor prices (the ratio of wages to the cost of capital) to affect employment or investment. Not only is a zero elasticity in sharp contrast with estimates for other countries, it also throws inro question the linkages through which monetary policy affects the real economy and the virtues of wage restraint in stimulating employment.

It is therefore reassuring that, using modern econometric techniques, Taylor finds a statistically significant and economically important effect of expected future real shore-term interest rates on business investmenc (through their effect on relative factor prices). Moreover, these results suggest that an important part of the slowdown of activity in 1992-93 can be attributed to high real interest rates in Europe. Indeed, gross fixed capital formation in France declined in each of the three years 1991-93, by a cumulative 1 5 percent.

The existing regime, with the objective of maimaining the French franc within rhe exchange rare mechanism (ERM) margins of fluctuation (now

©International Monetary Fund. Not for Redistribution

4 FRANCE: FINANCIAL AND REAL SECTOR ISSUES

widened to I 5 percent) has at rimes strongly constrained the room for maneuver of French monetary policy. Not only was France obliged ro match German interest rates, but, at times of srrong speculative pressure-September-November 1992 and January-March 1993-French short-term rates were raised far above German rates in order to defend the franc. These episodes illustrate the pitfalls of an incompletely credible pegged exchange rate arrangement and the advantage of full monetary union where fears of exchange rate realignment would be absent. The next swdy, by Marcel Cassard, Timothy Lane, and Paul Masson, explores ways of facilitating a smooth transition co monetary union, and, in particular, the use that could be made of a cross-country monetary aggregate. The authors point out that, given the extent of integration of financial markets that already exists among a core group of ERM countries, it is possible that shifts between currencies would lead to national demands for money being unstable. In contrast, an aggregate of those countries' money supplies might have a more stable demand funcrion. This result seems ro emerge from the data on the basis of their econometric estimates; it might therefore be desirable to give increasing weight co a coreERM monetary aggregate, relative to purely national money targets. Two other arguments reinforce this recommendation: if implemented in the anchor country (Germany) it would represent a more European approach tO monetary policy, consistent with the eventual goal of monetary union, under which policy would be guided by monetary conditions in all member countries. Empirical evidence in the form of causality tests also suggests that core-ERM money is a becrer predictor of German prices in the post-1983 period than German M3 alone, suggesting that greater attention ro a core-ERM monetary aggregate would also be in Germany's narrow interest.

The next study, by Gary O'Callaghan, considers how tax policy affects the allocation of saving and investment. In particular, he examines how differences in the taxation of various instruments in France can lead to distortions favoring one type of investment over another-often for no good economic reason. Indeed, changes co taxation in this area have often involved correcting inequities by creating a new tax-favored instrument, which then creates distortions of its own. The author argues convincingly that a level playing field in which similar instruments are taxed in the same way would increase economic efficiency.

A significant feature of the French financial system is the tax advantage granted to insurance policies, which are an important vehicle for saving. In contrast, there is little saving in the form of private (prefunded) pensions, which are very prominent in several other countries, such as the United States and the United Kingdom. Interest in private pensions has increased

©International Monetary Fund. Not for Redistribution

l11troduction 5

with the widespread recognition that the public pension system, which is financed on a pay-as-you-go basis, will not be able co maintain generous benefit levels without very large increases in contribution rates, given that in France, as in many other industrial countries, the average age of the population is projected to rise dramatically in coming decades.

The final paper, by ]oaquim Levy, considers how private pensions could be encouraged, what form they might take, and what their effect might be in stimulating the development of the French financial system. Though private pensions cannot make up for the fact that the public system is unfunded, the author argues that a transition to a system with both public pensions (somewhat reduced in generosity) and funded private pensions might minimize the welfare losses associated with the higher contributions that will be needed. Moreover, these pension plans could be managed by existing financial institutions, on the model of those in the United Kingdom or the United States, rather than involving book entries by the companies themselves, as in the German model. The resulting pool of capital might favor private ownership of France's enterprises and permit a more competitive business environment .

•• •

In conclusion, the studies in this book treat issues of central concern to the French economy's prospects until the end of the century and beyond. They are presented in the hope that they will add co the fund of economic knowledge and contribute co an informed debate of the policy issues.

©International Monetary Fund. Not for Redistribution

IGIJliii¥1ii•1@1W

Why Is Unemployment tn France So High?

REZA MOGHADAM

Gl igh unemployment in France has persisted despite the fact that in

recent years France's macroeconomic performance has compared favorably with the other major industrial or EU countries in other respects. Since 1987, growth has been in line with EU and major industrial-country averages while inflation has been below both. Low inflation has contributed to improved competitiveness and, recently, tO trade surpluses. However, employment creation was disappointing even in times of strong growth and the recent recession has led to a sharp fall in employment.

Unemployment not only puts pressure on government finances and inflicts a heavy social cost; it also has more wide-ranging economic consequences. The higher the structural unemployment in an economy, the lower its potential output, and hence the average standard of living, will bt.:. Furthermore, high unemployment can endanger the credibility of monetary policy. For example, a rise in interest rates-for instance, to protect the level of the exchange rate-may be viewed as unsustainable by the financial markets and have a perverse impact. The crises in the European ERM during 1992 and 1993 are testimony tO this. 1 There are, therefore, many rcasons to seek a better understanding of the problem of high unemploymen t.

This chapter investigates the causes of unemployment in 17ram:t.: and assesses the effectiveness of potential policy responses aimed at reducing it. The chapter is organized as follows: Section I examines the nawrc of unemployment in France; Section II identifies some of the potential facrors contributing to unemployment by comparing France with other industrial nations and by using cross-section regressions; Section Ill

1 Drazen and Masson ( 1994) find suppon for the hypothesis that persistence in unemployment can undermine the credibility of monetary policy.

6

©International Monetary Fund. Not for Redistribution

Why Is U11cmploymenl i11 Frn11ce So High? 7

provides some £ime-series evidence on the long-run and short-run causes of unemployment; Sections IV and V examine recent labor marker measures; and Section VI assesses these measures and considers other potential policy responses to structural unemployment.

I. History and Composition of French Unemployment

The Rise and Rise of U nemployment

Following the first oil shock and the onset of recession in 1974-75, unemployment in France rose continuously from just under 3 percent in 1973 co a peak of 10.7 percent in 1987. It then declined gradually to 8.8 percent in 1 990 before resuming its ascent (Chart I ).

Both labor supply and demand facrors appear to have contributed to the rise in unemployment. Between 19'70 and 1 992, the labor force grew by about 16 percent, equivalent tC' 3 .. \ million people (Chart 2). This growth came about in spite of a fall in rhc aggregate participation raceZ during the 1 980s-the increase in female participation was more than offset by a decline in male participation (Chart 2):1 The growth in the labor force was thus concurrent with an even larger increase in the population of working age, conventionally defined as those aged between 15 and 64.

During the same period, employment growth has been disappointing: there was no net increase in employment between the mid-J970s and the late 1 980s. Male employment dropped almost continuously between 1973 and 1987 as employment in the uaditionally male-dominated industrial sectors such as mining, chemicals, and metals declined. Growth in the ser .. vice sector and opportunities for part-time work boosted female employment, which has grown continuously since the early 1 970s, albeit nm as fast as the increase in the female labor force (Chart 3).

Why has the high growth of the labor force not been accompanied by an equivalent increase in employment? An increase in the labor supply should, in theory, lead to higher output through lower real wages, increased competitiveness, and increases in production capacity unless the labor market is inflexible. Besides, there have been similar demographic developments in other industrial countries: in both Canada and the United States the average rate of growth of rhe labor force since 1 970

1Defined as LF!f'W = (£ + U)IPW. where LF is the labor force, E employment. U unemployment. and PW is the population of working age.

JThe fall in the male participation rate is not independent of the rise in unemployment and is panly due to the early retirement of the old unemployed: see discussion of participation ratr by age below.

©International Monetary Fund. Not for Redistribution

8 fRANCE: FINANCIAL AND REAL SECJ'OR ISSUES

Chart 1 . France: Unemployment, Growth, and Inflation

12 .------------------------------------------------.

10

8

6

4

Total Unemployment (In percent)

.. .. .. .. ..

.. .. .. .. .. .. .. ..

· - - ..

2 �����������--�����- �������� 1971 1973 1975 1977 1979 1981 1983 1985 1987 1989 1991 1993 7 .-----------------------------------------------------. 6 5

Annual percentage change

4 3 2

0

_, 1971

CPI growth (right scale)

.......... .·

Real GOP growth (left scale)

1973 1975 1977 1979 1981

·.

1983 1985 1987 1989 1991 1993

18 16 14 12 10 8 6 4 2 0

Sources: lnstitut National de Ia Statistique et des Etudes Economiques (INSEE), National Accounts; and IMF World Economic Outlook.

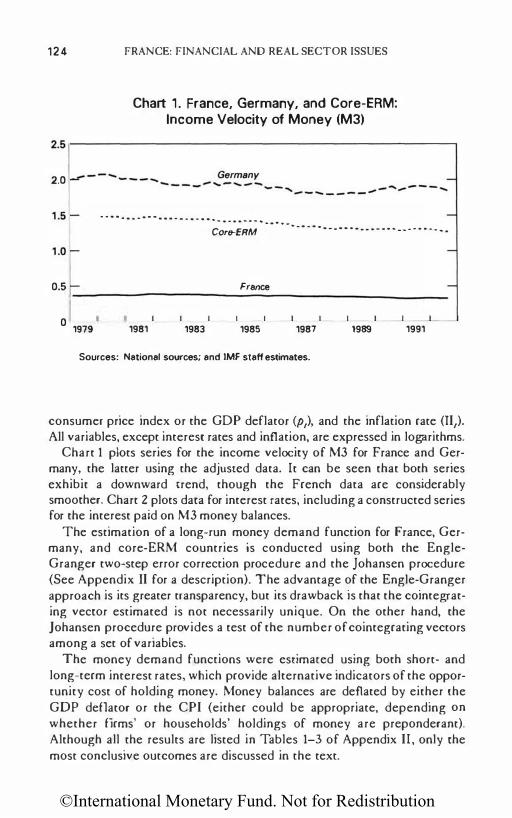

'To April 1993.

has been more than twice that in France, yet the average rate of growth of employment in the United States and Canada has been over four times that in France.

Over the last two decades the average rates of growth of the population of working age and of the labor force in France have been below the OECD average, though more or less in line with the EU average (Table 1). It is the rate of growth of employment in France that has been disappointing, particularly when compared with the OECD average in the 1980s.

©International Monetary Fund. Not for Redistribution

Why Is Unemployment i11 Fro11ce So High? 9

Chart 2. France: Labor Force, Population, and Participation

(1970 = 100) 114

112

110 .·

108

106 •• /Population

104

102

100UWWWWWWWWWWWWWWWWWWWWWW 70 72 74 76 78 80 82 84 86 88 90 92

65·0

70 72 74 76 78 80 82 84 86 88 90 92

.-------------------�120 (1970 = 100)

Population • • • • aged 1�4:'

115

110

105

UL�����������1oo 70 72 74 76 78 80 82 84 86 88 90 92

Participati on (In percent)

·-. ......... •• Male ·.

. . .

95

85

.. .. ... .. 75

65

- � �

55

70 72 74 76 78 80 82 84 86 88 90 92 45

Source: Organization for Economic Cooperation and Development (OECO), Historical Statistics.

Composition of Unemployment

Although the uend rise in unemployment can be observed in many other industrial countries, two factors characterize the French experience: unemployment peaked somewhat later than in the other major industrial countries, and the subsequent decline was not as sharp (Chart 1). This persistence suggests structural imbalances in the labor market that are also reflected in the composition of unemployment.

©International Monetary Fund. Not for Redistribution

10 FRANCE: FINANCIAL AND REAL SECTOR ISSUES

Chart 3. France: Labor Force, Employment, and Unemployment (In millions of persons)

25.-------------------------------------------------�

24

23

22

21 - ·· . ·· . . .

......... .. .. · · ..

Unemployment

.. ... .. . .. -·· .. .. ... . .. .. ... . ··. ... Total employment

..· .......... ..

11.-------------------------------------------------�

10

9

8

.. .. · 7 19;0

·. 1972

.. . .... - ··

- ·· .. · .. . .. .. .. -- ··

Unemployment

. .. . . .

Female employment

1974 1976 1978 1980 1982 1984 1986 1988 1990 1992

14.5.-------------------------------------------------,

14.0 .. ..... .. .... .... .. .. .. .. .. . .. .. ..

Unemployment 13.5 .... .. .... . .. .

13.0 Male employment

.· ... 12'5

1970 1972 1974 1976 1978 1980 1982 1984 1986 1988 1990 1992

Source: OECD. Histories/ Statistics.

©International Monetary Fund. Not for Redistribution

Why Is U11employmen1 in France So High? 11

Table 1 . Key Labor Market Indicators (Average annual percentage growth rates)

1974-79 1980-90 1990 1991 1992

Population of France 0.7 0.8 0.3 0 3 0.3 working age EU 0.7 0.7 0.3 0.2 0.2

OECD 1.2 1.0 0.7 0.6 0.5

Labor force France 0.9 0.5 0.4 0.7 0.4

EU 0.7 0.8 0.9 0.7 - 0 .2

OECD 1 . 3 1.3 1.1 0.8 0.7

Employment France 0.3 0.2 1.0 0.1 - 0.5

EU 0.2 0.6 1 . 6 0.3 - 1 .2

OECD 1.1 1.2 1.3 - 0.1

GOP growth France 2.8 2.1 2.2 0.7 1.3

EU 2.5 2.2 2.9 1.4 1 .1

OECD 2.7 2.7 2.5 0.7 1.5

Source: OECD, H•stoncal Statistics.

Youth Unemployment

The youch uncmploymcnc race has been consiscendy higher chan che roral unemployment rate and more scnsicivc co economic downcurn (Chart 4). In general, one would expect che youth unemployment rate to be above che toea! unemployment rate as the young have lower human capital. Labor market practices such as "last in, firsc our" also reinforce youth unemployment and explain irs sensitivity co economic conditions. Furthermore, there is some evidence that wage bargainers are primarily concerned wirh rhe interests of those who are employed, thar is, the "insiders," racher chan chose who seek cmploymenc, the "outsiders." For example, the insiders may rake advanragc of high wrnover costs or the uncertainties associated with employing an oursider to demand higher wages than are justified by productivi ry or inflation. This theory also helps co elucidate the persistence in youth unemployment. However, labor market features such as "last in, first our" or "insider-outsider" are not unique ro France, yet youth unemployment in France is high compared with other industrial nations (Chart 5). This suggesrs char ocher more specific factors are also at work. The minimum wage and high employer payroll taxes could have a more pronounced impact on rhe employment of the young (sec Section II below). Furthermore, many young people are poorly qualified or lack the skills sought by employers. In 1991, rhe we of

©International Monetary Fund. Not for Redistribution

12 FRANCE: FINANCIAL AND REAL SECTOR ISSUES

Chart 4. France: Unemployment-Youth, Female, and Male

25

20

15 , .

.. ... . . . 10 .. ·

01974 1976 1978 1980

14

(In percent)

, ...........

. . .. . .

.

Total unemployment1

Youth unemployment1

1982 1984 1986 1988

.... ......... .. ..... ..... 12 Female unemployment1 ,

. ·

. · . ·

__ / ----

-----

........ ...

/ ,,.,.,.---- .......

/ ...........

_,., .-"'

/" Male unemployment1

. --2 1974 1976 1978 1980 1982 1984 1986 1988

Source: INSEE. 'To April 1993.

.. ..........

1990

, . ..........

1990

'

.

1992

.·

1992

unemployment among 15-24-year-olds with only the certificot detudes pri

moires (CEP) was twice as high as for those with the boccolourlot-level diploma.

Female Unemployment

Unemployment among women has been consistently above the average unemployment rate (Chart 4). There are a number of potential causes. Part-time working, especially among women, remains less developed 1n France than in the other major industrial countries (Table 2).

©International Monetary Fund. Not for Redistribution

Why Is Unemploymmt iti France So High?

Chart 5. France: Relative Unemployment Rates, 1992 (In percent)

� Japan iiiiiiiia.. Germany I

0 5 10

Source: OECD.

France Australia

EU

Canada

New Zealand

Belgium

United Kingdom

United States

Norway

I Italy

Ireland

Finland

Sweden

Netherlands

Portugal

0 Youth unemployment

• Total unemployment

I I I I 15 20 25 30

13

Although jobs in the service sector-which provides substantial female employment-have grown faster than the average rate of increase in employment, this rate of growth has been lower than that achieved in the United States, the United Kingdom, Italy, and japan.4 There is also some evidence that, for women in particular, the probability of finding a job rises as the maximum duration of benefits draws near (see Section II below). In France, benefits are available for a longer duration than in most other industrial nations and the ratio of long-term to short-term replacement rates for women was high until January 1993, when the Government introduced a new system whereby unemployment benefits decrease more rapidly over time (see Sections II and III below).

•Commissariat general du Plan ( 1993). pp. 128-30.

©International Monetary Fund. Not for Redistribution

1 4 FRANCE: FINANCIAL AND REAL SECTOR ISSUES

Table 2. Size and Composition of Part-Time Employment (In percent)

United United Canada France Germany Italy Japan Kingdom States

(Part-time employment as a proportion of employment)

1 973

Men 4.7 1.7 1 8 3 7 6 8 2 3 8.6

Women 19.4 12.9 24.4 14 0 25.1 39 1 26.8

1992

Men 9.3 3.6 2.7 2.7 10.6 6.1 1 0.8

Women 25.9 24.5 3 4 3 10.5 34.8 44.6 25.4

(Women's share in part-time employment)

1973 68.4 82.3 89.0 58.3 70.0 90.9 66.0

1992 70.0 83.7 89.6 67.9 69.3 85.4 66.4

Souroe: OECD, Employment Outlook. 1993.

Long-Term Unemployment

About 40 percent of those who are unemployed have been out of a job for at least one year. Although this is nor exceptionally high when compared with other industrial economies (Chart 6), it is high in absolute terms. There is considerable evidence that the long-term unemployed exert no pressure on wage inflation (Layard, Nickell, and jackman (1991)). Therefore, long-term unemployment could reduce the potential output of the economy through a higher natural rate of unemployment. Pissarides ( 1982) illustrates that human capital depreciates as the duration of unemployment increases, leading to a lower probability of finding a job.

With regard to the demand-side causes of long-term unemployment, employers faced with continued uncertainty about future orders may refrain from recruitment for long periods of rime, causing the persistence of both unemployment and long-term unemployment, particularly if wages are not flexible. Labor market rigidities, such as the relative generosity of long-term benefits, employment protection legislation, the minimum wage, and high employer costs are other potential contributory factors. These factors are investigated further below. The adoption of a number of job creation and training programs makes the study of longterm unemployment even more complex. Cases and Lollivier ( 1993) characterize the French labor market as being divided into three segments: unemployment, regular employment, and marginal employment. Many job schemes fall into the last category, and there are flows between all

©International Monetary Fund. Not for Redistribution

0

0

0

Why Is Utmnploymmt in F ranee So High? 15

Chart 6. France: Relative Unemployment Rates, 1991

Total Long-Term Unemployment (As e percentage of totel unemployment)

10 20 30 40 50 60 70 80

S.lglum

S�ln lt•ly

lrel.nd GrHCe

Porru�l

United Kingdom Norw•y

Lux•mboufl/ Aultr•ll•

NewZHI•nd

Female Long-Term Unemployment (As a percentage of female unemployment)

10 20 30 40

10 20 30 40

Source: OECD, Employment Outlook. 1992.

50 60 70

Male Long-Term Unemployment (As a percentage of male unemployment)

50 60 70

80

80

©International Monetary Fund. Not for Redistribution

16 FRANCE: FINANCIAL AND REAL SECTOR ISSUES

three segments. Transition from long-term unemployment to labor market schemes and vice versa could lead to recurrent spells of unemployment rather than to long-term unemployment.

Nonemployment Rate

Another useful concept in comparing the labor market experience of different countries is the nonemployment rate,5 which combines the effects of high unemployment and low participation in the labor force. In addition to the high rate of unemployment, France has a low participation rare, particularly among men (Chart 7). The participation rate in France drops dramatically for those aged 56 and above when compared with the average of EU countries (Table 3), as a consequence of generous early retirement schemes.6

The high nonemployment rare in France is more comparable with the southern European and the Benelux countries than with the other industrial countries (Chart 8). This underutilization of labor imposes a heavy burden on government finances, through both lost tax revenue and increased social security expenditure. This burden will become increasingly serious as the proportion of the elderly in the population rises, given the need to finance pension expenditures, which operate on a pay-as-yougo basis in France. Not surprisingly, cross-country evidence suggests that the higher the nonemployment rate, the higher the budgetary expenditure on the labor market (Chart 9).

II. Causes of Unemployment

Employers' Taxes

Social security contributions in France, particularly for employers, are very high. Total employee and employer contributions as a ratio to income are higher than in all other industrial countries except Italy (Chart 9, lower

sThe nonemployment rate is defined as

where£ is employment and PW is population of working age.

"Those aged over 56 can obtain unemployment benefits without looking for work. If someone over 56 becomes unemployed as a result of company restructuring. he will be entitled to 65 percent of previous income or a maximum ofF 12,000 per month. with the employer paying I 0 percent of the cost.

©International Monetary Fund. Not for Redistribution

0

0

0

Why Is Unemployment i11 F ranee So High P 17

Chart 7. France: Relative Participation Rates, 1991

15 30 45 60

15 30 45 60

15

Source: OECO, Employment Outlook, 1992.

75

Total Participation

(In percent)

105

i..taium I Male l lnnce

���:� Participation Greece (In percent)

l��:,�� l New Ze•t•nd ���:��y

�lJ,7,�·�, "''" ; Kir,11uu•" J�fS!�msrk

75 90 105

Female Participation

(In percent)

105

©International Monetary Fund. Not for Redistribution

18 FRANCE: FINANCIAL AND REAL SECTOR ISSUES

Table 3. Participation Rates by Age Group, 1991 (In percentages)

France EU Average

Age (in years) Males Females Total Males Females Total

14-19 13.2 10.1 1 1 .7 28.5 24.3 26.4

20-24 69.8 62.9 66.2 76.3 66.5 71.4

25-29 94.9 78.0 86.3 92.0 70.3 81.2

30-34 97.1 75.1 86.0 96.2 66.8 81.5

35-39 97.3 74.5 85.9 96.8 66.6 81.6

40-44 96.8 76.0 86.4 96.2 65.7 81.0

45-49 95.3 70.4 82.9 94.3 59.5 77.0

50-54 88.4 62.1 75.2 88.9 50.6 69.6

55-59 61.9 42.4 51.8 72.7 35.9 53.8

60-64 14.6 12.4 13.4 37.1 14.6 25.3

65-69 5.3 2.4 3.7 11.3 4.4 7.5

70 and above 1.8 0.6 1.0 3.8 1.2 2.2

Total 63.7 46.2 54.5 67.5 42.6 54.6 Source: Eurostat, Labour Force Survey Results. 1991.

panel). Personal income taxes, on che ocher hand, are lower than in most ocher countries. Table 4 provides a more detailed comparison of labor costs in France and ocher major European countries for an unmarried worker. Gross labor costs in France, although below those in Italy, are substantially higher as a proportion of net earnings than in Germany and the United Kingdom. In fact, the gap with the latter two countries widened in the 1980s. The main contributor to this differential is employers' social security contributions, which are not only substantially higher than in Germany and the United Kingdom, but also increased significantly during the 1980s.

Table 4 also shows that the contribution rates of employees are noticeably higher in France than in Italy and che United Kingdom, but marginally below those in Germany. Furthermore, contributions as a ratio w nee earnings increased by some 50 percent during the 1980s. Income taxes in France, on the ocher hand, are about one third of those in the other three countries as a proportion of net earnings, and they declined marginally during che 1980s.

From a theoretical perspective, the invariance of incidence proposition (liP) implies chat the replacement of an employer tax by an equal

©International Monetary Fund. Not for Redistribution

0

0

0

Why Is U11employment i11 Fro nee So High?

Chart 8. France: Relative Nonemployment Rates, 1991

Sweden

Spain Ire land

ltsly Greece

BIJigium France

Netherlands Germany

Austria Australia Porrugal

Canada United Kingdom

United States Luxembourg

Norway Japan

Finland Denmarlr. Switzerland

Total Nonemployment (In percent)

19

10 20 30 40 50 60 70

10

Spain GretiCtt

Italy Ireland

Belgium Netherlonds

Luxembourg F111nce

Germany AustriB

Portugal Australia

Sw itzerland Japan

Canada United Kingdom

United States Norway

Finland Denmarlr.

Sweden

Female Nonemployment (In percent)

20

Switzerland Luxembourg

10

30 40 50

Italy Germany

Greece Netherlands

Finland Norway

Canada Austria

United States United Kingdom

Australia Portugal Denmarlr.

Sweden Japan

20 30

60 70

Ireland Spain

Frt1nc. 88/gium

80

Male Nonemployment (In percent)

40

Source: OECD, Employment Outlook, 1992.

90

50

©International Monetary Fund. Not for Redistribution

20 FRANCE: FINANCIAL AND REAL SECTOR ISSUES

Chart 9. Labor Market Expenditure and Social Security Contributions

Nonemployment and Labor Market Expenditure, 1990 � 6.------------------------------------------------------, C) '0 ;:5r-� 8. 4 r-

• Denmark

Ireland •

= I) 331-:6

Netherlands •

• Belgium

• Spain

c NewZe�tlltnd

• Sweden Norway • • Finland

� 21- G=many ., • United Kingdom

� 1 r-"' United States • •Portugltl

• Fr�tnce

-

-

-

-

-E Japan • � o �--��- ---�-��--��----�'----- �'--�' -----�' --� j 15 20 25 30 35 40 45 50 55

Nonemployment, percent

Social Security Contributions, 1990 (As a proportion of pretax income)

20 30 40

Source: OECO, Employment Outlook, 1992

• Employer contributions

0 Employee contributions

50 60 70

employee tax has no effect on the real economy; that is, the product wage, the consumption wage, and the level of employment will be unaffected (Layard, Nickell, and jackman (1991); Newell and Symons (1986); and OECD (1990)). However, this result may not apply-at least in the short run-if there are market imperfections; for instance, if wages are above market-clearing values and adjust slowly, or wage negotiators care only about the "insiders." Even if the liP holds, differences in tax liability

©International Monetary Fund. Not for Redistribution

Why Is Unemploymml in F ranee So High? 2 1

Table 4. Comparison of Earnings, Direct Taxes, and Social Security Contributions

(As a percentage of net earn ings for a single worker))

United Year Italy France Germany Kingdom

1 . Gross earnings 1979 1 25 125 146 142

1989 138 132 155 139

2. Employees' contribution 1979 1 1 1 5 23 9

1 989 1 2 23 27 1 3

3 . Personal income taxes 1979 14 1 0 23 33

1989 26 9 28 26

4. Net earnings (1-2-3) 1979 100 100 100 100

1989 100 100 100 100

5. Employers' contribution 1979 58 47 23 14

1989 67 59 27 14

6. Total labor cost 1979 183 172 1 69 156

1989 205 191 182 153

Source: Commissariat general du Plan (1993).

could alter the allocation of resources. For example, employer taxes apply only to the wage whereas personal or corporate income taxes also apply to income from capital. A switch from income taxes co employer taxes implies an increase in the overall rate of taxation on employment and a decrease in capital taxation, which may lead ro a substiwrion of capital for labor. Similarly, personal income taxes are usually progressive whereas social security taxes are nor. A switch from one ro the ocher could lead ro changes in the coral tax bill for many individuals and firms and affect labor supply or demand decisions.

Empirical studies (Newell and Symons (1986); and OECD (1990)) suggest that, even when using a model where the liP holds in the long run, a cut in employer taxes and an equivalent rise in employee taxes could reduce unemployment in the short run. The short-run effects may last for several years because of lags in the adjustment process (0 ECD (1988)). Cotis and Loufir (1990) find suppon for the liP in France (see below). Other authors have found that the tax wedge has a long-run effect on unemployment in France (Bean, Layard, and Nickell (1987)). We investigate this issue further in Section III using time-series data for France.

©International Monetary Fund. Not for Redistribution

22 FRANCE: FINANCIAL AND REAL SECI'OR ISSUES

Table 5. Employer Taxes, Youth and Long-Term Unemployment

where

Ordinary Least Squares Cross-Section Regressions for 15 OECD Countries'

(t-ratios in parentheses)

(UY!U! = 1 . 7 + O.Q1 CSE (2.03)

R2 = 0.27

LTU= 17.5+ 0.97 CSE (2.14)

R2= 0.26,

UY/U = ratio of youth to total unemployment rate; CSE = employers' social security contributions; and LTU = percentage of unemployed who have been unemployed for more than a year. 'Organization for Economic Cooperation and Development members Belgium. Canada, Denmark,

Finland, France. Germany, Ireland, Japan, the Netherlands. Norway. Portugal. Spa1n. Sweden, the

Un1ted Kingdom. and the United States.

Table 5 provides some cross-section evidence on the impact of employer taxes on the composition ofunemploymem in the industrial coumries.

The first equation gives the resu It of regressing the ratio of youth to total unemployment on the rate of employers' social security comriburions using cross-section data for 15 OECD countries. The results indicate a significant positive correlation between the two variables. The coefficient on employers' comriburions indicates that if they are l percentage point higher in one country than in another, then the ratio of youth to total unemployment is likely to be l percentage poim higher. In France, employer contributions are about 20 percentage points higher than the sample average, implying a similar gap for the percentage of youth unemployment. The second regression presents results for long-term unemployment that are very similar; they indicate that higher employer comributions are associated with higher long-term unemployment. When the same regressions were performed for men and women separately, the coefficients were higher in the case of women.

Admittedly, these results do not capture any theoretical relationship. However, they do suggest that high employer taxes are associated with a high incidence of youth and long-term unemployment, which are symptoms of strucrural unemployment. The resu Irs imply that increases in employers' contributions have not been passed on to employees through wage reductions.

©International Monetary Fund. Not for Redistribution

Why Is Unemploymetrt in France So High? 23

Table 6. Proportion of Employees Covered by the SMIC1 (In percent)

Males Females Total

1972 1 .8 4.6 2.7

1976 3.6 8.4 5.1

1979 3.0 6.2 4.0

1981 5.1 13.9 8.0

19832 4.6 10.4 6.6

1985 6.2 16.2 9.7

1987 5.1 12.6 7.8

1989 5.2 13.9 8.2

1992 5.1 14.1 8.6

Sources: Bazan and Martin (1991); and Ministere du Travail, de I'Emploi, et de Ia Formation Professionnelle.

'The data refer to July of each year and cover wage and salary earners in businesses employing more than ten workers in industry, commerce, and services. They cover all workers whose hourly wage is less than the new hourly SMIC rate that applies from July 1 of each year.

2New series.

The Minimum Wage

France has had an institutional minimum wage since 1950; the current SMIC (solaire minimum interprofessionne/ de croissance) was introduced in 1970. There are three mechanisms for revising the SMIC: (1) a rise of 2 percent or more in the consumer price index (CPI) automatically triggers an equivalent rise in the SMIC; (2) on july 1 every year che SMIC is revised by at least half of the increase in the real hourly wages in industry; and (3) the Government can raise the SMIC at its discretion.' These mechanisms have led to a steady rise in the real value of che SMIC.

The latest report on the SMIC by the Miniscere du Travail shows chat the number of people being paid the SMIC has risen over the last five years.s In 1992, 8.6 percent of workers or just under 2 million people received the minimum wage, with the percentage among women being much higher (Table 6). The proportion of individuals earning the SMIC is particularly high for chose who are under 26 years old: 35.5 percent of wage earners under 26 were paid the SM IC in 1992. The fact that a large

1following the election of President Mitterand, the SMIC was raised by 10 percent in May 1981.

"In fact these numbers are an underestimate since the survey carried out by the Ministc�re du Travail does n01 cover firms with less than ten employees. nor those in agriculture, coal, public transpon, and utilities.

©International Monetary Fund. Not for Redistribution

2 4 FRANCE: FINANCIAL AND REAl. SECTOR ISSUES

Chart 10. France: Youth Unemployment, Relative Minimum Wage, and Labor Market Programs

24 .----------------------------------------------. 0.52

22 20 18

16

14 12 10 .. ... ... ... .. .. .. 8

: :

/ SMIC/average wage : (right scale)

0.51 0.50 0.49 0.48 0.47 0.46 0.45 0.44

6 1974 1976 L...:.....l....---l....,...--.l._....Ll9-7..J8'---...l,-9-80..__....L19...,.8..J2_.J.1.,-98-4.L.._....I....19...,.8...l6_.J.1_988....L---','-9-90

...J..._--L19.,..9-'

2 o. 43

1000

800

600

400

200

Employment In Labor Market Programs (In thousands of persons)

o L-�,-9�7..J6-...l1-9-78...J...__.J.1_9_80�--'-,...,.98...,.2L-....L19�8..J4L-..J1-9...,.8...l6-...l1.,-98...,.8�--'-,-99...,.0L-....L19-9

�2

Sources: IN SEE; OECD; and IMF staff estimates.

number of young workers, and a growing number of people in general, are paid the SMIC suggests that it is a significant labor market factOr that may have an impact on employment.

Empirical studies on the effect of the SMIC on employment have not been conclusive. Bazen and Marrin (1991) find that "increases in the real value of the SMIC have exerted significant upward pressure on real youth earnings." However, they are unable to show conclusively that increases in real labor costs have had a negative impact on youth employment, although they believe this to be the case. Their results do suggest that

©International Monetary Fund. Not for Redistribution

Why Is Unemployment i11 France So High?

Table 7. Minimum Wage i n France and

the United States, July 1992 lin francs)

Monthly' Minimum Wage' Cost to Employer

France

United States 5,7'56 3,950

Sources: Bulletin Mensuel de Statistique; and U.S. Employment and Earnings. 'On the basis of worl<ong 169 hours a month. 2Usong an exchange rate of $1 = F 5.5.

7,943 4.254

25

moderating the relative rare of increase in the SMIC would have a favorable impact on youth employment. Chart 10 also suggests a correlation between the relative minimum wage and youth unemployment. In response to high youth unemployment, the Government has introduced a number of labor market measures (Chart 10, lower panel). Many labor market schemes are targeted at the young (see Section IV below). Given the large increase in the number of places on employment programs between 1984 and 1987, it is difficul t ro assess whether the fall in youth unemployment after 1984 was due to the fall in the relative value of the SMIC or an increase in labor market programs. It is likely that both played a role.

By adding to wage rigidity-in particular, the rigidity of relative wages by limiting wage differentials-the SMIC has several implicarions.9 To the extent that the productivity of the less skilled and less qualified is below that justified by the SMIC, they are likely to suffer unemployment. This no doubt helps explain France's high rate of youth unemployment, and also the persistence of unemploymem. The SMIC may also be an obstacle ro regional labor mobility, as it is uniform across the country and thus does not reflect regional differences in the cost of living that imply different real values for the SMIC.

The experience of other industrial counuies with a starurory minimum wage is also relevant. Empirical work in the United Stares and Canada has concluded that the minimum wage has had a negative impact on youth

9In addition 10 the SMIC, there is evidence of other types of wage rigidity that could also lead to higher unemployment. For example. there is evidence of "insider power" (Cahuc. Sevestre, and Zajdela ( 1990); Plassard and Tahar ( 1990)).

©International Monetary Fund. Not for Redistribution

26 FRANCE: FINANCIAL AND REAL SECTOR ISSUI<:S

Table 8. Minimum Wage for an 18-Year-Oid, July 1992 (In francs)

France United States2 Belgium Netherlands

Monthly Full Minimum Wage'

5,756 3,950 6.743 6,476

Monthly Minimum Wage for an 18-Year·Oid

5,756 3,365 5,226 2.947

Cost to Employer of 18-Year-Oid

7,943 3,624 7,405 3,286

Sources: Bulletin Mensuel de StatJsttque: U S. Employment and Earnmgs: and Van den Heuvel (1992).

'Using $1 = F 5.5. and July 1992 exchange rates for other currencies. 2Jn the United States there is a reduced minimum wage for 16-19-year-<>lds that is 85 percent of

the full minimum wage.

employment. 10 It is therefore instructive co compare the level of the minimum wage in France with that in other industrial countries.

The cost of employing someone at the minimum wage in France is about rwice that in the United Stares. This is due ro rwo facrors. First, the minimum wage in France is about 1 .5 rimes that in the United Stares, and, second, employers' social security contribution rates are 38 percent in France bur only 7. 7 percent in the United Stares11 (Table 7 on previous page).

A comparison with Belgium and the Netherlands is interesting because, unlike France, these countries have a lower minimum wage for the young than for ocher workers (Table 8). In France the minimum wage, ar lease in theory, applies ro anyone aged 18 or above. 12 In the Netherlands the full minimum wage applies ro those aged 23 and above. For those under 23, the minimum wage is reduced sharply.l3 In Belgium the full minimum

10See Brown (1988) for a survey of the U.S. evidence and Coe (1990) on evidence for Canada. 11 Based on internationally comparable figures compiled by the OECD ( 1992a). 12In recent years the Government has introduced a number of measures that reduced employers'

contributions and the minimum wage for young people participating in employment schemes. These measures were reinforced in June 1993, reducing the effective minimum wage substantially when participating in special schemes (see Section IV below).

13The minimum wage in the Netherlands is reduced according to the following schedule: Age Percent of minimum wage

n �o 21 72.6 20 61.5 19 52.5 18 45.5

17 39.5 16 34.5 15 30.0

©International Monetary Fund. Not for Redistribution

Why Is U11employment itJ F ranee So High?

Chart 1 1 . Ratios of Youth to Total Unemployment, 1992

·:� _,.-... •Y· Germany -�. . ..... ··"1-� -� ,., ..... _.,._'"

,,. · '" -�-., .. � .. � . . . ... . ,., I· .. -.... "'� -··

.• ;s:·� .. -...... � � "' :>. ,-, ,,.; ,.. . •Iii• q.•.•<'..tT l' ·"'" ; .. . ... ��:,;,. .... ..,,,,.. ....... !i. ,..,.,, -1 ' 4..;JI:A'! ... .... · �

V:c ,; .. ,.

' <.:,.-.!'>. ;•. . ,; ... ....

�'<'".:·� .... ., =·�· \'\.!"�). • '"'<":";•• .. 'r"' "'' :·;<;r ''if'··�

0 0.5 1.0

Source: OECD.

· � ., ,

� ,.

Netherlands

Canada

United Kingdom

:·· . . . Ireland

Spain . .,� 1 Finland

. • ' " �- ?--1'o United States � - '·''* -"(. .. Japan

France

... · -··"' '• . Belgium ·'�� ·_.' :' L_ Norway

'•"' '· Portugal ;_ Italy

1.5 2.0 2.5

27

3.0

wage applies to those aged 21 and above and there are lower rates for those under 21, although the reduction is not as sharp as in the Netherlands.'4

The existence of the youth minimum wage means that, in absolute terms, it is cheaper for an employer to employ an 18-year-old in the Netherlands or Belgium than in France, although the full minimum wage is higher in the former countries. Interestingly, the ratio of youth to coral unemployment in the Netherlands is among the lowest in the industrial countries (Charts 5 and 1 1).

There is, therefore, considerable evidence that the minimum wage in France is high by international standards, especially for rhe young. There is also some evidence thar the minimum wage affects youth, if not total, unemployment. We will pursue this issue further by doing some timeseries analysis of data for France in Section III, after we have briefly considered the other potential causes of unemployment.

14The minimum wage in Belgium is reduced according 10 the following schedule: Age Percent of minimum wage 20 92.5 19 85.0 18 17 16

77.5 70.0 62.5.

©International Monetary Fund. Not for Redistribution

28

Women

Men

where

FRANCE: FINANCIAl. AND REAL SECTOR ISSUES

Table 9. Long-Term Unemployment and Relative Generosity of Benefits

Ordinary Least Squares Cross-Section Regressions for 15 OECD Countries'

{t-ratios in parentheses)

LTU = 7.10 + 0.60 RATIO (2.47)

R2 = 0.32

LTU = 4.80 + 0.46 RATIO (2.59)

R2 = 0.34.

LTU = percentage of unemployed who have been unemployed for more than a year; and RATIO = the ratio of long-term to short-term replacement rates times 100.

•Orgamzatton for Eoonomtc Cooperation and Development members Belgium. Canada. Denmark. Finland, France. Germany, Ireland. Japan, the Netherlands. Norway. Portugal. Spain, Sweden. the Umted Kingdom, and the Untted States.

Generosity of Benefits

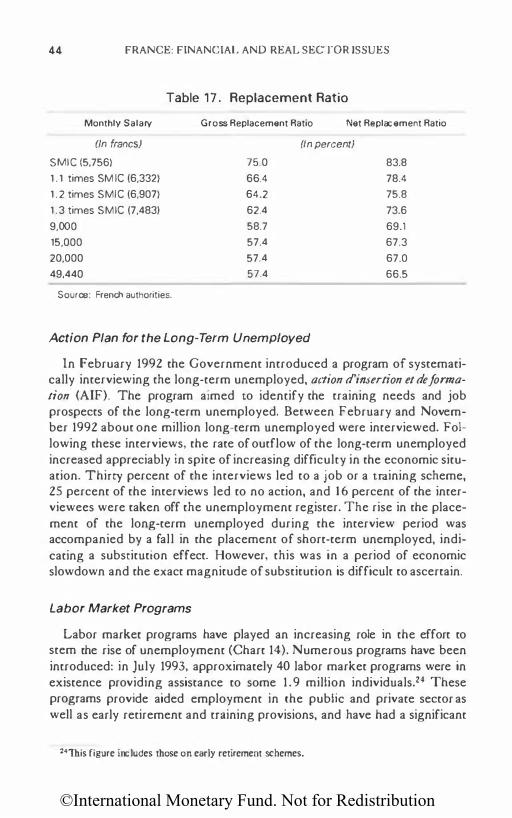

Most models of wage determination imply that benefits have a significant effect on wages (La yard and Jackman (1991 )). The impact of the replacement rate (i.e., the ratio of unemployment benefits to wages) on the decision to seek employment very much depends on the individual's circumstances and is difficult to measure at an aggregate level. Besides, some countries with a high replacement rate, such as Sweden and Norway, have low unemployment and a high participation rate. The important issue is not so much the absolute level of benefits, or even the replacement ratio, but the incentive structure of the benefit system and the characteristics of the individual (see, for example, Schmitt and Wadsworth (1993)).

One aspect of this is the duration structure of benefits. Table 9 gives the result of regressing the proportion of long-term unemployed on the ratio of the long-term to short-term replacement rate using cross-section data for 15 OECD countries. Separate regressions were performed for men and women.

Table 9 shows that there is a significant positive relationship between long-term unemployment and the generosity of long-term relative to shortterm unemployment benefits for both men and women. The equation for men suggests that if the ratio of long-term ro short-term uncmploymem benefits is 1 percentage point higher, then long-term unemployment will be 0.46 percentage points higher. Interestingly, the corresponding figure for

©International Monetary Fund. Not for Redistribution

Why Is Utumployment i11 France So High?

Table 1 0. Maximum Duration of Unemployment Benefits and Replacement Rates

{In weeks)

1981 1989

EU countries

Belgium Indefinite Indefinite

Denmark 130 130

France 156 130

Germany 52 52

Ireland 65 65

Italy 26 26

Netherlands 156

Spain 104 1 04

United Kingdom 52 52

Non-EU European countries

Austria 30 30

Finland 100 1 00

Norway 40 80

Sweden 60 60

Switzerland 36 50

Non-European OECD countries

Canada 50 50

Japan 26 30

United States 39 26

Source: OECD. Employment Outlook. 1993.

29

women is 0.60 percentage points. In the data set, which corresponds to 1991, the ratio of short-term to long-term replacement rates for France is 17 percentage points higher than the sample average for men, and 22 percentage points higher for women. The introduction of the new unemployment benefits system will reduce these ratios (see Section IV).

There are other features of the benefits system that may also have an impact on unemployment. According to the EU Commission, unemployment benefits were paid to 43 percent of those without work in France in 1989, which is substantially above the EU average of 30 percent. One cause of this phenomenon could be the duration unemployment benefits are available in France. Table 10 provides data on the maximum duration of benefits for the OECD countries. Benefit duration in France is among the longest in the OECD countries. Only in Belgium, Denmark, and the Netherlands are benefits available for a longer period.

©International Monetary Fund. Not for Redistribution

30 FRANCE: FINANCIAl, AND REAL SECTOR ISSUES

Table 1 1 . Periods for Which No Insurance Benefits Are Paid at the Start of an Unemployment Spell

Minimum Waiting Period Waiting Period if Last Job Was (for All Claims) Quit Voluntarily

Australia 7 days 2-12 weeks

Austria none 4 weeks

Belgium none 1-26 weeks

Canada 2 weeks 6 weeks Den mark none 5 weeks

Finland 5 days 6 weeks

France none complete disqualification

Germany none 12 weeks

Greece 6 days complete disqualification

Ireland 3 days 6 weeks

Japan 7 days 1-3 months

Netherlands none none

New Zealand 7-14 days 6 weeks

Norway 3 days 4 weeks

Portugal none complete disqualification

Spain none complete disqualification

Sweden none 4-10 weeks

Switzerland 5-20 days

United Kingdom 3 days 1-26 weeks

United States 1 week complete disqualification

Source: OECD. Employmenr Outlook. 1991.

Institutional Factors

Structural unemployment is also affected by the benefits administration system, hiring and firing regulations, and other institmional factors that could discourage employers from taking on new workers or the unemployed from searching for jobs. A few of these factors are examined in this section.

Unemployment Benefit Administration

France does not seem our of line with regard ro the minimum waiting period before the receipt of benefits; as in many other industrial countries, there is no minimum period. A number of countries have a minimum waiting period of a few days. However, if a person has left his job voluntarily, he would be completely disqualified from receiving benefits in France, whereas in many countries there is a waiting period of several weeks, but not a complete disqualification (Table 1 1 ).

©International Monetary Fund. Not for Redistribution

Why Is Urmnployment i11 France So HighP 31

Table 1 2 . Signing On and Other Regular Reporting by Benefit Claimants

Signing On in Person

Australia Every 2 weeks

Belgium Every day

Denmark Every 2-3 months

Japan Every 4 weeks

Portugal Monthly

Spain Every 3 months

Switzerland 3 times a week

Source: OECD. Employment Outlook. 1991.

Confirmation of Unemployed Status by Post

France

Greece

Netherlands

Monthly

Monthly

Maximum 3 months

United States Every week or 2 weeks

No Regular Procedure

Finland Germany

Sweden

Regulations concerning signing on in France are rather liberal: confirmation of unemployment status is done on a monthly basis by post (Table 12). However, France does have a system of intensified interviews by the placement and benefit administration services (Table 13).

Hiring and Firing Legislation

The 1986 work dismissal legislation in France requires that those being dismissed are given one to two months' written notice of dismissal and informed in writing of the reasons for their dismissal. At the same time this legislation removed the need co seek the permission of the Labor Ministry for collective dismissals. Other legislation in 1989 obliged companies co prove the cause of dismissal. The law in France also requires that workers be paid up to a maximum of one and a half months' salary as severance pay. Though the legal restrictions on dismissal in France are less strict than those in the southern European countries, they are more strict than those outside Europe, particularly in the United States.

Barriers to nontraditional forms of work such as pare-time or temporary work are often viewed as a form of rigidity in the labor market. We noted above that part-time working is less developed in France than in many other industrial countries (Table 2). In order to assist part-time working, the Government passed legislation in December 1992 exempting employers from SO percent of social security contributions if they took on parttime workers.

©International Monetary Fund. Not for Redistribution

32 FRANCE: FINANCIAL AND REAL SECTOR ISSUES

Table 13. Scheduling of Intensified Interviews by Unemployment Duration

Australia

Denmark

France

Germany

Netherlands

Sweden

United Kingdom

New Zealand

Source: OECD. Employment Outlook. 1991.

Scheduling of Intensified Interviews

Duration of more than 2 years

Every 3 months

4th and 13th month of unemployment (employment placement); 14th month (benefit administration)

After at least a year

Reorientation interviews after 3 years of unemployment

Unemployed over 6 months given priority

At 6 months and every 6 months thereafter

At 6 months

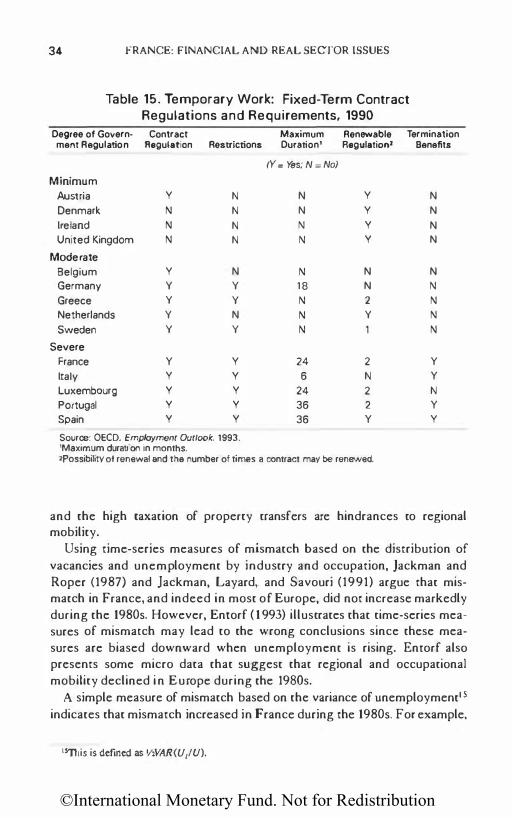

The proportion of people working on temporary contracts in France has risen continuously over the last decade from 3.3 percent of employment in 1983 to 10.2 percent in 1991 (Table 14). However, the regulations governing fixed-term contracts remain more strict in France than in most other industrial countries (Table 15). For example, in some circumstances the use of temporary contracts is restricted; there is a legal maximum duration for fixed-term contracts; and employees are entitled to termination benefits. The barriers to temporary work have to be considered in conjunction with the constraints on permanent employment such as employer taxes or hiring and firing regulations. If the regulations governing permanent employment were not rigid then employers would make use of temporary contracts only to the extent that they help in adjusting ro changes in demand. However, the existence of barriers to permanent employment would encourage greater use of temporary contracts. Therefore, given the existence of barriers to permanent employment in France and the fact that the regulations governing temporary work are more strict than in most other countries, it is difficult to argue that the rise in the proportion of temporary workers in France is a sign of enhanced labor market flexibility.

Another potential constraint on hiring nontemporary staff in France is that the employment agency, ANPE (Agence Nationale pour I'Emploi), currently has a monopoly in placing nontemporary staff. This was originally enacted ro prevent the exploitation of the unemployed, but it is no

©International Monetary Fund. Not for Redistribution

Why Is Unemp/oymmt itr Fra11ce So High? 33

Table 14. Temporary Workers (As a percentage of total employment)

1983 1988 1991

Australia 18.7 19.7

Belgium 5.4 5.0 5.1

Denmark 1 1 .5 1 1 .9

Finland 1 1 .1 13.1

France 3.3 7.8 10.2

Germany 1 1 .4 9 5

Greece 16.3 1 7 .6 14.7

Ireland 6.2 9.1 8.3

Italy 6.6 5.8 5.4

Japan 10.3 10.7 10.5

Luxembourg 3.2 3.7 3.3

Netherlands 5.8 8.7 7.7

Portugal 18.5 16.5

Spain 22.4 32.2

Turkey 7.2 6.6

United Kingdom 5.5 6.0 5.3

Source: OECD, Employment Outlook, 1993.

longer enforced. Firms regularly employ outside the ANPE. Such legal restrictions also exist in a number of other European countries (Table 16). Even though this legislation is not currently enforced, it could act as a disincentive to private firms considering entering the placement market if they fear that the legislation may be invoked in the future.

Mismatch

Evidence on the mismatch between the skills held by workers and those demanded by employers is rather difficult tO assemble. For example, indicators based on unemployment by occupation consider only the supply side of the market, and, since skills are defined on the basis of the last job held, they exclude all the unemployed without previous experience.

Data on the characteristics of the unemployed suggest some degree of mismatch. Youth unemployment is highest among those with the least qualifications (OECD (1 992b)). The long-term unemployed tend to have lower educational attainment than average and are concentrated in the least-qualified occupations (Caracosta, Fleurbaey, and Leroy (1991 )). As for regional mismatch, both the uniformity of the SMIC across the country

©International Monetary Fund. Not for Redistribution

34 FRANCE: FINANCIAL AND REAL SECTOR ISSUES

Table 15. Temporary Work: Fixed-Term Contract Regulations and Requirements, 1990

Degree of Govern· Contract Maximum Renewable Termination ment Regulation Regulation Restrictions Duration' Regulation• Benefits

IY = Yes: N = No) Minimum

Austria y N N y N Denmark N N N y N Ireland N N N y N United Kingdom N N N y N

Moderate Belgium y N N N N Germany y y 18 N N Greece y y N 2 N Netherlands y N N y N Sweden y y N N

Severe France y y 24 2 y

Italy y y 6 N y

Luxembourg y y 24 2 N Portugal y y 36 2 y

Spain y y 36 y y

Source: OECD. Employment Outlook, 1993. 'Maximum duration in months. 2Possibility of renewal and the number of times a contract may be renewed.

and the high taxation of property transfers are hindrances to regional mobility.

Using time-series measures of mismatch based on the distribution of vacancies and unemployment by industry and occupation, Jackman and Roper (1987) and Jackman, Layard. and Savouri (1991) argue that mismatch in France, and indeed in most of Europe, did not increase markedly during the 1980s. However, Encorf ( 1993) illustrates that time-series measures of mismatch may lead to the wrong conclusions since these measures are biased downward when unemployment is rising. Enrorf also presents some micro data that suggest that regional and occupational mobility declined in Europe during the 1980s.

A simple measure of mismatch based on the variance of unemployment15 indicates that mismatch increased in France during the 1980s. For example,

1SJllis is defined as Y>VAR(U11U).

©International Monetary Fund. Not for Redistribution

Why Is Unemployment in France So High? 35

Table 16. Legal Constraints on Methods of Filling Vacancies

Requirements for Notification Legality of Profit·Making of Vacancies to the Public Employment Placement

Employment Service Agencies

Australia No requirement Permitted

Austria No requirement Banned

Belgium All vacancies for Temporary work agencies external candidates only are permitted

Canada No requirement Permitted

Denmark No requirement Banned

Finland All vacancies Banned

France All vacancies for external Temporary work agencies candidates only are permitted

Germany No requirement Temporary work agencies only are permitted

Greece All vacancies Banned

Ireland No requirement Permitted

Italy Banned

Netherlands No requirement Permitted

Norway All vacancies Temporary work agencies are often permitted

Portugal No requirement Permitted

Spain All vacancies Banned

Sweden All vacancies for external Banned candidates

Switzerland No requirement Permitted

United Kingdom No requirement Permitted

United States No requirement Permitted

Source: OECD. Employment Outlook, 1991.

regional mismarch increased from 1.27 percent in 1982 ro 1.88 percent in 1990. However, regional mismatch fell ro 1.48 percent in 1992 because rhe rare of increase in unemployment was higher in regions wirh lower unemployment.t6 The same picrure emerges when considering unemployment by professional srarus; because unemployment has risen sharply among whire-collar workers (who had a relatively low unemployment rare), mismatch falls from 12.5 percent in 1990 ro 1 1 .9 percent in 1992.

16For example. the unemployment rate in Yvelines (lie de France) rose from 4.9 to 6.2 percent. a rise of 27 percent. whereas it rose from 13.5 percent to 15.5 percent in Ht!raull in Languedoc

Roussillon, a rise of 15 percent.

©International Monetary Fund. Not for Redistribution

36 FRANCE: FINANCIAL AND REAL SECTOR ISSUES

Chart 12. France: Vacancies and Labor Market Expenditure

1.0�-----------------------------------------------.

4

0 10

Vacancies and Unemployment, 1974-92 (In percent of the labor force)

5 6 7 Unemployment

8 9

Share of Active Labor Market Expenditure, 1990 (As a percentage of total labor market expenditure)

20

Spsin

Denmsrlr

Csnsdo

lrelond

Germany

Norway

Finland

United Kingdom

United States

Netherlands

Fnnce Jspsn

Belgium

30 40 50

Source: OECD, Employment Outlook, 1992.

10

60

1 1

Sweclttn Porrugsl

70

Chart 12 depicts a more formal measure of mismatch, the unem ployment-vacancy (UV) ratio (or Beveridge curve), for the period 1974-92. An

outward shift of the curve seems to have occurred: between 1978 and 1983 the same ratio of vacancies co the labor force was coupled with a higher unemployment rate than before. During the period 1984-87,

©International Monetary Fund. Not for Redistribution

Why Is Unemployment itt France So High? 37

unemployment rose while vacancies were on the rise, albeit modestly. This behavior is indicative of a small increase in mismatch.17

France spends 2.7 percent of its GOP on the labor marker; the average for the OECD is 2 percent, and for the major industrial countries excluding France, 1 . 1 percent. However, France spends much less than most other industrial countries on active labor market measures such as training, and more on passive measures such as unemployment compensation (Chart 12, lower panel). Only the former are likely to alleviate labor market mismatch.

I l l . Causes of Unemployment-Time-Series Evidence

This section presents a time-series econometric model of the determinants of the NAIRU (non-accelerating-inflation rate of unemployment) or rhe narural rate of unemploymenc The primary interest here is not to estimate a numerical value for the NAIRU but to identify a set of policy instruments that could be used co reduce it.

The Model

To understand the causes of unemployment in Britain, Layard and Nickell (1986), in an influential study, constructed an empirical model consisting of equations for prices, wages, employment, and the trade balance. Here we estimate a simplified version of their model that consists of two equations: a price equation and a wage equation. In this model, firms are assumed to operate in an imperfectly competitive environment, setting their prices on the basis of cost and demand. A key feature of the model is that wages are influenced by pressure variables such as those reviewed in the last section, for example, mismatch, the minimum wage, generosity of benefits, or import prices. If increases in the wage pressure variables lead to higher real wages, then unemployment would have to rise for price inflation to be kept in check. More formally, the model assumes that stable inflation requires consistency between two concepts:

(i) the target real wage-firms and workers bargain about nominal wages as a markup on expected value-added prices

w • = target(w- p);18 and

17Bismut (1982) illustrates that there was a significant shift of the Beveridge curve after the two oil shocks. There is n o evidence of such instability during the 1980s. However. the natness of the UV curve during the 1974-92 period and its upward slope during 1984-87 point to a small increase in mismatch.

18w and p are in logs.

©International Monetary Fund. Not for Redistribution

38 FRANCE: FINANCIAL AND REAL SECr0R ISSUES

(ii) the feasible real wage-in an imperfectly competitive market the firms are thought of as setting value-added prices as a markup on wages

p • = feasible(p - w).

The economic variable chat brings about this consistency in the long run is unemployment (Layard, Nickell, and Jackman (1991)).

The model is given below in equations (1)-(4). Since we are interested in the NAIRU, which is the long-run equilibrium concept for the unemployment rate, we have separated the long-run relationships from the dynamic ones. This is also desirable from an estimation point of view (Wren-Lewis (1990)). Equations (1) and (2) give the long-run wage and price equations; equations (3) and (4) give the dynamic framework for wages and prices.

w• = pr + a. u + azz ... + (l3 (pm -p),

p• = �.(yd - y) + �zZ-pr,

w = w• + p + 91(L) 1:! w - 92 (L) l:ip + 93(L)D.,.

p = p• + w + cp1(L)!:i p - cp2 (L) l:iw + cp3(L)DP

(1)

(2)

(3)

(4)

where w• = target real wage (i.e., target (w - p)), p• = feasible real wage (i.e., feasible (p - w)), w = nominal hourly earnings, pr = productivity or unit labor costs, p = output prices, U = unemployment rate, Pm = import prices, (yd - y ) = actual demand relative to potential outpm, z ... = ocher wage pressure variables, ZP = other variables affecting firms' margin, D..,, DP = other factOrs affecting the dynamics of wages and prices, and !!. is the difference operator. All lower-case variables are logged. 9 and cp are polynomials in the lag operatOr L and have both positive and negative powers of L, with forward terms appearing as expectations. It is also assumed that polynomials are such that the target real wage is independent of the rate of inflation, chat is, dynamic homogeneity holds.

Combining equations (3) and (4) gives

The left-hand side of equation (5) is a polynomial in changes in prices. The right-hand side of equation (5) can be regarded as a measure of inflationary pressure, which is made up of three elements: (i) w• + p•, the difference between the target real wage and the feasible real wage; (ii) a

©International Monetary Fund. Not for Redistribution

Why Is Unemployment i11 France So High? 39

polynomial in the dynamics of wage contracts; and (iii) other short-run influences on wages and prices. The first element, w• + p•, can be derived from combining equations (1) and (2):

In a steady state where inflation is constant, equation (5) implies that w• + p• = 0. Therefore equation (6) becomes a long-run relationship between the NAIRU, the level of actual demand relative to potential, (y4- y), Z,.., ZP, and import prices. For a given level of demand, equation (6) would determine the long-run influences on the NAIRU.

The Results

Because we are interested in estimating long-run relationships, an obvious way forward is to employ coincegration techniques. 19 The basic idea of cointegration is that two or more variables may be regarded as defining a long-run equilibrium relationship if they move closely together in the long run, even though they may drift apart in the short run. This long-run relationship is referred to as a coimegrating vector. Because there is a long-run relationship between the variables, a regression containing all the variables of a cointegrating vector will have a stationary error term, even if none of the variables taken alone is stationary.

We have directly estimated the long-run relationships in equations (1) and (2) above using the Johansen procedure and quarterly data for the period 1971:1-1992:IV.20 The test statistics and the estimated cointegrating vectors from the Johansen procedure are reported in Appendix I. The cointegration tests reveal the following unique wage and price equations:

w -p = pr + 0.59 smic - 0.07 U + 0.15 SK + 0.12 (pm -p), and (7)

19Culhbenson, Hall, and Taylor ( 1992) presem a survey of coimegra1ion. 20Johansen ( 1988) and Johansen and Juselius (1990) presenl a coimegralion estimation method·

ology that is based on maximum likelihood estimates of all the cointegrating vectors in a given set of variables, and provide two likelihood ratio tests for the number of cointegrating vectors.