fqhc cost reporting ceo and cfo working together june 22, 2012

TRANSCRIPT

FQHC Cost Reporting

CEO and CFO working together

June 22, 2012

CFOs and Accountants CEOs, COOs, and non-accountant

types

Who do we have in the room?

Gap is a store, not generally accepted accounting principles (GAAP).

Fast bees are something to avoid, not the Financial Accounting Standards Board (FASB)

Non-accountants

The cost report is due Our cost rate has gone down We owe Medicare or Medicaid

Other concerns??

CEOs: What happens when you hear…

The time for the annual cost reporting exercise arrives, what thoughts start to crowd your mind? New accounting staff or managers have not

coded transactions appropriately Trial balance from the auditors is still not

ready What else…..

Remember even if you have been a CFO for 20 years, that is only 20 cost reports. Unlike financial statement preparation at once per month for 20 years or 240 chances to get it right.

CFOs: Once every year cost report

To align payments with reasonably efficient FQHCs’ costs of furnishing care, thereby helping to ensure beneficiaries’ access to high-quality services.

Cost report is to accurately reflect the costs to provide FQHC-covered services to Medicare and Medicaid beneficiaries.

Goal of cost reporting:

Why it matters to have it right? (Hint: ACA 2014)

The gut check: a quick formula Learning how to count visits & FTE “Book ‘em, Danno” – your accounting

staff’s coding behavior is very important HR plays a part in cost reporting. No, they

really do. The Biggest Mistakes & Growing a

backbone How can the visionary CEO help the down-to-

earth CFO with cost report and operational analysis?

Where Are We Going Today?

Thanks to the Affordable Care Act:

Medicare is going PPS

In 2011 FQHCs have been transmitting Medicare claims with CPT/HCPCS detail

Probably 2013-14 year will be the base year for Medicare PPS calculation

Your Future, Your Cost Report

The Medicare program generally the second best payer after state Medicaid

Payer mix goal for community health centers Growing percentage of Medicare

beneficiaries served as population ages. If Medicaid is block granted, Medicare

may become the BEST payer

Baby Boomers & FQHCs

What percent of your current patients are Medicaid or dual eligible?

In 5 years you project X? 10 years?

Projections

Costs/Visits(Costs divided by

visits)

The formula

Take one month of medical expenses and divide by the medical provider visits for the month Back out your dental, pharmacy and other non-

primary medical care expenses 2012 Medicare Ceilings:

Urban: $ 126.98 Rural: $109.90

Where are you compared to these limits? If you are more efficient and doing for less, great, but most of are struggling to keep our heads above water with costs at and above $150 per visit.

My story: $54 per visit

Homework

NO!! Determining allowable DIRECT

costs takes the entire leadership and management team (as well as staff)

Counting visits is never straightforward

This is simple division. Right?

Problems: Many practice management systems

count visits from the appointment table, not the charge table

Canned reports from the vendors are RARELY accurate, usually over counting visits, inflating encounters (Misys and HC)

IT staff writing visit reports usually do NOT understand the definition of a FQHC visit.

Visits

UDS Visits are NOT Medicare/Medicaid FQHC visits

Medicare Visit: Face-to-face encounter between the patient and a physician, physician assistant, nurse practitioner, certified nurse midwife, visiting nurse, clinical psychologist or clinical social worker during which an FQHC service is rendered.

Only one visit per day (An exception: patient suffers an illness/injury subsequent to the first encounter requires additional diagnosis/treatment.)

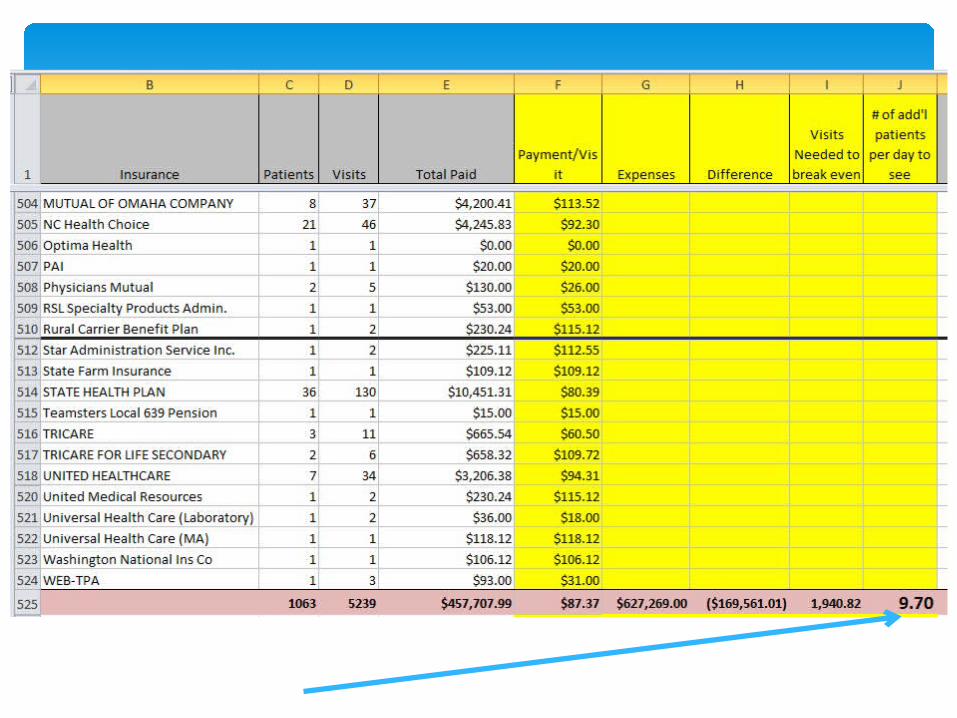

Too Many Visits – is that a problem?

NEVER accept the first report or analysis as definitive.

Run detail reports and analyze it

Visits

Generate a report from the CLAIMS system (not the appointment system) with the following fields: Patient name, Patient account, Date of service, Insurance, Claim id (unique to each claim), CPT code

Run a frequency distribution by CPT code Analyze which CPT codes are being billed.

How to Count (1 of 3)

Determine which CPT codes are FQHC visits and which are not. Most E/M codes are FQHC visits, except for

nursing visits (99211) Venipunctures and Urinalysis are not.

Flag the CPT codes that are FQHC visits

Who is best equipped to do this analysis? Not necessarily the CFO. It might be

better to have a provider work with finance staff.

How to Count (2 of 3)

Using a relational database, link the CPT code table with the claim detail table Remove duplicate entries so that for each

date of service one, and only one, claim exist for each patient.

How to Count (3 of 3)

Give your CFOs and Medical Directors what they need for financial and clinical analysis: Analytics

You need one person who is proficient with relational databases.

The power of the “what if” analysis

CEOs listen up

It is important for providers to accurately track their time because it WILL affect the cost report.

FTEs are an important part of the cost report. If you over count FTEs you may be “dinged”

for not meeting productivity floors. UDS FTEs are NOT Medicare/Medicaid

FQHC FTEs Again – providers, HR and accounting staff

must make sure that there is an accurate record of provider time.

Sidebar: Productivity Screens

The number of full time equivalent employees (FTE) of each type (i.e., physician, physician assistant, or nurse practitioner) is determined by the following formula.

Divide the total number of hours per year worked by all employees of that type by the greater of:

The number of hours per year for which one employee of that type must be compensated to meet the clinic/center’s definition of an FTE. (If the clinic/center is open on a full time basis, the usual definition of an FTE is 2,080 hours per year, 40 hours per week for 52 weeks); or

1,600 hours per year (40 hours per week for 40 weeks).

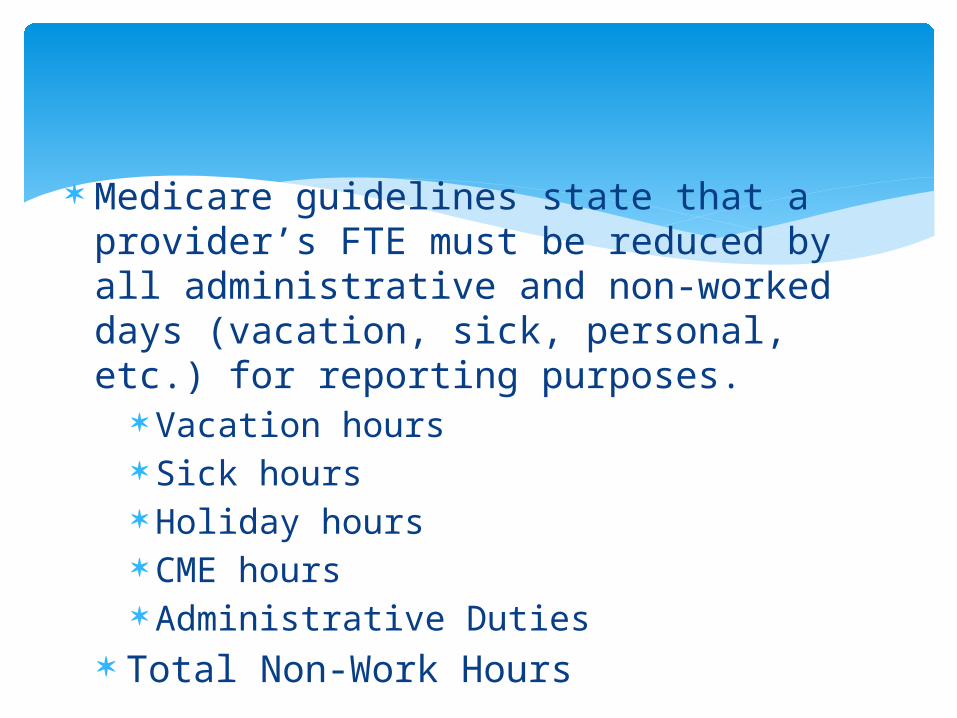

Medicare guidelines state that a provider’s FTE must be reduced by all administrative and non-worked days (vacation, sick, personal, etc.) for reporting purposes.

Vacation hours Sick hours Holiday hours CME hours Administrative Duties

Total Non-Work Hours

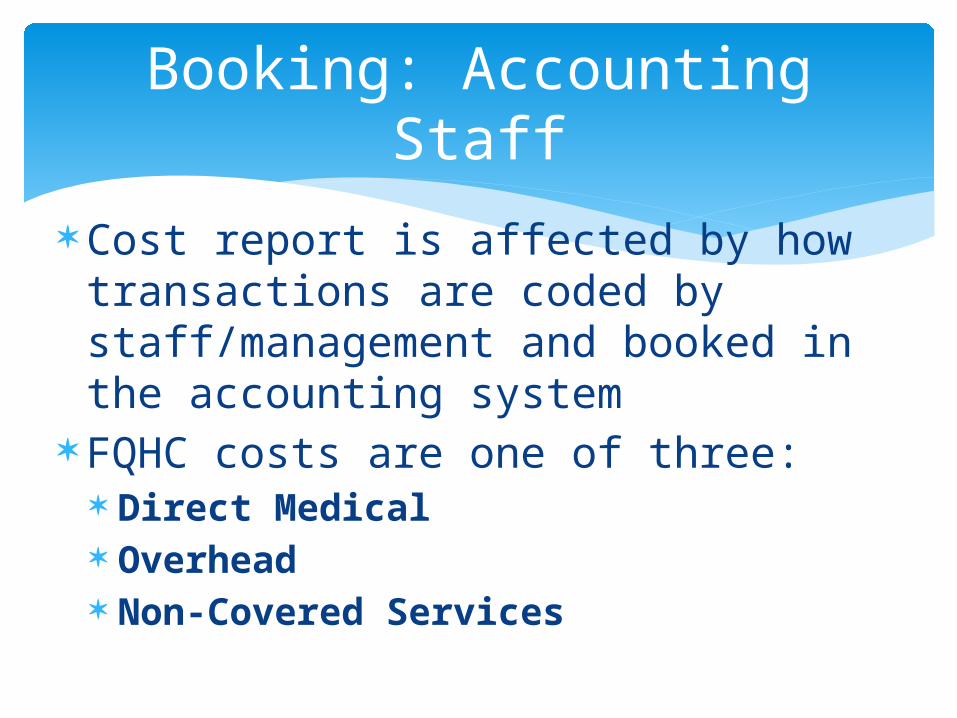

Cost report is affected by how transactions are coded by staff/management and booked in the accounting system

FQHC costs are one of three: Direct Medical Overhead Non-Covered Services

Booking: Accounting Staff

Direct costs: salary and benefits for medical and

behavioral health providers, medical supplies, etc.

Overhead: administrative salaries, utilities,

Non-covered costs: marketing, laboratory, etc.

If costs are in the Direct Medical Cost classification, every penny spent is captured

Overhead/Administrative costs are allocated over the Direct Medical Costs and the Non-Covered Costs As such, if you misclassify a Direct Medical Cost as

administrative costs, a portion of the costs will not be captured in the FQHC cost rate

Accurate coding in accounting is FUNDAMENTAL

Why does it matter which cost?

Electronic medical/health records: NGS and Palmetto try to classify as administrative

overhead Patient education materials

Electronic access to HealthWise Diabetes, Hypertension paper handouts

Staff Triage nurses working at the call center Medication assistance staff Intake staff when part of the job is preventive

health screening

But it is not so clear cut…

The CEO and Medical Director authorize the mass production of 30,000 full-color hypertension education handouts

Accounting receives the invoice from the print company and codes it as follows: G/L: Printing Supplies Dept: Medical

When the trial balance is sent to the intermediary this expense will be re-classed as administrative.

OUCH!!

Accounting and Coding

Other examples from the audience?

Job Descriptions are important For positions where job crosses two cost

centers (Direct Medical and Administrative costs) Intake staff who do PHQs

Do time studies to justify % Direct Medical and % Administrative

Human Resources

Question intermediary disallowances and adjustments Do not accept. Just because the auditor

disallows/reclasses it does not mean that should be.

Examples: Changing depreciation basis Requesting copies of BPHC CHC grant and NGAs Medical nutrition, social services

Question assumptions Medicaid story: CFO and CEO working together

Growing a backbone

Read Cost Principles & Medicare FQHC:

https://www.cms.gov/Center/Provider-Type/Federally-Qualified-Health-Centers-FQHC-Center.html?redirect=/center/fqhc.asp

Know how to argue with the rules

No reclassifications and/or adjustments reported to align costs properly

Not properly listing clinic locations which may affect per-visit payment limit(s)

No tracking & reporting of influenza & pneumococcal vaccines and/or other Part B billing issues

No reporting of Medicare bad debts - reclaim it, but prove you tried to collect

Top Ten Mistakes (Source: BKD, LLP - CPA)

Lack of review of intermediary proposed adjustments during settlement process

FQHC provider number issues No reconciliation of expenses reported on cost report with total expenses per the audited financial statements

Not reporting expenses correctly in the proper “buckets”

Incorrect computation of FTEs & related productivity standard

Inaccurate reporting of visits

UDS full-time equivalency (FTE) on Table 5 are almost always higher than Medicare and Medicaid FTE

UDS Provider Visits on Table 5 are usually higher than FQHC visits

Always question visits – never accept the first pass. Costs – ask questions about coding of expenses Give your finance and clinical staff a database expert Grow a backbone – question the intermediary’s

determination.

General rules of thumb